Abstract

I incorporate household debt and delinquency decisions into a standard model of lifecycle consumption-saving-investment. I also impose a punishment to the delinquent behavior by assuming that the percentage of endowment available is a linear function of the default decision. Theoretically such additional investor decisions are playing a relevant role in terms of completing markets. In practice, it enables me to derive an extended system of Euler equations which does not alter consumption-based fundamental asset pricing equation. It imposes the pricing kernel to account jointly for two additional first-order conditions. I perform empirical exercises aiming to price equity premium in United States from 1987:1 to 2018:1. I find significant elasticity of intertemporal substitution in consumption of the representative agent ranging from 0.24 to 0.55 and risk aversion from 1.82 to 3.51. This approach is also useful to account for the cross-section behavior of domestic assets. I can also use this framework to draw bounds for the household decisions on loan and delinquency and to propose a new rule of thumb relating preferences parameters and credit variables.

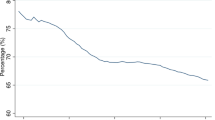

Data source: FRED

Similar content being viewed by others

Notes

Concerning the personal bankruptcy, I recognize the existence and the relevance of this formal procedure that removes unsecured debt obligations subject to some specific cases. However, I rely on one of the main findings reported in Athreya et al. (2009) to rule out this possibility. They find that unsecured credit markets pass-through increased income risk to consumption in U.S., irrespective of bankruptcy policy.

This variable is not used in the empirical exercise performed here and is not reported in Fig. 1.

References

Abel, A.: Asset prices under habit formation and catching up with the Joneses. Am Econ Rev Pap Proc 80, 38–42 (1990)

Athreya, K.: A model of credit card delinquency. In: 2012 Meeting Papers 981. Society for Economic Dynamics (2012)

Athreya, K., Sánchez, J., Tam, X., Young, E.: Labor market upheaval, default regulations, and consumer debt. Rev Econ Dyn 108, 32–52 (2015)

Athreya, K., Sánchez, J., Tam, X., Young, E.: Bankruptcy and delinquency in a model of unsecured debt. Int Econ Rev 59, 593–623 (2018)

Athreya, K., Tam, X., Young, E.: Unsecured credit markets are not insurance markets. J Monet Econ 56, 83–103 (2009)

Aiyagari, S.: Uninsured idiosyncratic risk and aggregate saving. Q J Econ 109, 659–684 (1994)

Bansal, R., Yaron, A.: Risks for the long run: a potential resolution of asset pricing puzzles. J Finance 59, 1481–1509 (2004)

Basu, S., Kimball, M.: Long-run labor supply and the elasticity of the intertemporal substitution for consumption. Working Paper, University of Michigan (2000)

Berndt, A.: A credit spread puzzle for reduced-form models. Rev Asset Pricing Stud 5, 48–91 (2015)

Bordo, M., Jeanne, O.: Boom-busts in asset prices, economic instability, and monetary policy. NBER Working Papers 8966 (2002)

Brandt, M., Cochrane, J., Santa-Clara, P.: International risk sharing is better than you think, or exchange rates are too smooth. J Monet Econ 53, 671–698 (2006)

Breeden, D.: An intertemporal asset pricing model with stochastic consumption and investment opportunities. J Financ Econ 7, 265–296 (1979)

Campbell, J., Cochrane, J.: By force of habit: a consumption-based explanation of aggregate stock market behavior. J Polit Econ 107, 205–251 (1999)

Chatterjee, S., Corbae, D., Nakajima, M., Ríos-Rull, J.: A quantitative theory of unsecured consumer credit with risk of default. Econometrica 75, 1525–1589 (2007)

Chen, X., Kontonikas, A., Montagnoli, A.: Asset prices, credit and the business cycle. Econ Lett 117, 857–861 (2012)

Cochrane, J.: A cross-sectional test of an investment-based asset pricing model. J Polit Econ 104, 572–621 (1996)

Cochrane, J.: Asset Pricing: Princeton, NJ: Princeton University Press (2001)

Cochrane, J.: Macro-finance. Rev Finance 21, 945–985 (2017)

Constantinides, G.: Intertemporal asset pricing with heterogeneous consumers and without demand aggregation. J Bus 55, 253–267 (1982)

Constantinides, G., Duffie, D.: Asset pricing with heterogeneous consumers. J Polit Econ 104, 219–240 (1996)

da Costa, C., de Jesus Filho, J., Matos, P.: Forward premium puzzle: Is it time to abandon the usual regression? Appl Econ 48, 2852–2867 (2016)

da Costa, C., Issler, J., Matos, P.: A note on the forward and the equity premium puzzles: two symptoms of the same illness? Macroecon Dyn 19, 446–464 (2015)

Dávila, J., Hong, J., Krusell, P., Ríos-Rull, J.: Constrained efficiency in the neoclassical growth model with uninsurable idiosyncratic shocks. Econometrica 80, 2431–2467 (2012)

Epstein, L., Zin, S.: Substitution, risk aversion, and the temporal behavior of consumption and asset returns: an empirical analysis. J Polit Econ 99, 263–286 (1991)

Fama, E., French, K.: Common risk factors in the returns on stocks and bonds. J Financ Econ 33, 3–56 (1993)

Ferreira, A., Moore, M.: Carry trade and currency risk: a two factor story. Braz Rev Econ 69, 429–449 (2015)

Gerlach-Kristen, P., Merola, R.: Consumption and credit constraints: a model and evidence from Ireland. Empir Econ 10, 10 (2018). https://doi.org/10.1007/s00181-018-1461-4

Grossman, S., Shiller, R.: The determinants of the variability of stock market prices. Am Econ Rev 71, 222–227 (1981)

Guvenen, F.: Reconciling conflicting evidence on the elasticity of intertemporal substitution: a macroeconomic perspective. J Monet Econ 53, 1451–1472 (2006)

Hall, R.: Stochastic implications of the life cycle-permanent income hypothesis: theory and evidence. J Polit Econ 86, 971–987 (1978)

Hall, R.: Intertemporal substitution in consumption. J Polit Econ 96, 339–357 (1988)

Hansen, L.: Large sample properties of generalized method of moments estimators. Econometrica 50, 1029–1054 (1982)

Hansen, L., Singleton, K.: Generalized instrumental variables estimation of nonlinear expectations models. Econometrica 50, 1269–1286 (1982)

Hansen, L., Singleton, K.: Stochastic consumption, risk aversion, and the temporal behavior of asset returns. J Polit Econ 91, 249–265 (1983)

Imrohoroğlu, A.: Cost of business cycles with indivisibilities and liquidity constraints. J Polit Econ 97, 1364–1383 (1989)

Kocherlakota, N.: On the discount factor in growth economies. J Monet Econ 25, 43–47 (1990)

Kocherlakota, N.: The equity premium: it’s still a puzzle. J Econ Lit 34, 42–71 (1996)

Kroencke, T.: Asset pricing without garbage. J Finance 72, 47–98 (2017)

Krueger, D., Lustig, H.: When is market incompleteness irrelevant for the price of aggregate risk (and when is it not)? J Econ Theory 145, 1–41 (2010)

Lucas, R.: Asset pricing in an exchange economy. Econometrica 46, 1429–1445 (1978)

Lucas, R.: Supply side economics: an analytical review. Oxf Econ Pap 42, 293–316 (1990)

Matos, P., da Costa, C.: On the relative performance of consumption models in foreign and domestic markets. Int J Financ Mark Deriv 5, 154–188 (2016)

Mehra, R., Prescott, E.: The equity risk premium: a puzzle. J Monet Econ 15, 145–161 (1985)

Mitman, K.: Macroeconomic effects of bankruptcy and foreclosure policies. Am Econ Rev 106, 2219–2255 (2016)

Ogaki, M., Reinhart, C.: Measuring intertemporal substitution: the role of durable goods. J Polit Econ 106, 1078–1098 (1998)

Rubinstein, M.: An aggregation theorem for security markets. J Financ Econ 1, 225–244 (1974)

Samuelson, P.: Lifetime portfolio selection by dynamic stochastic programming. Rev Econ Stat 51, 239–256 (1969)

Thimme, J.: Intertemporal substitution in consumption: a literature review. J Econ Surv 31, 226–257 (2017)

Yogo, M.: A consumption-based explanation of expected stock returns. J Finance 61, 539–580 (2006)

Yogo, M.: Asset prices under habit formation and reference-dependent preferences. J Bus Econ Stat 26, 131–143 (2008)

Acknowledgements

For helpful comments on earlier drafts, I thank Alex Ferreira, Carlos da Costa, Costas Meghir, Fábio Gomes, Giovanni Beviláqua, Jaime de Jesus Filho, Jefferson Bertolai, Marcelo Fernandes, Márcio Veras and Thiago Souza. Also, I thank seminar participants at various institutions and conferences and the anonymous referees for relevant remarks. All errors are mine.

Funding

I gratefully acknowledge financial support from CNPq-Brazil.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author declares that he has no conflict of interest.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Matos, P.R.F. The role of household debt and delinquency decisions in consumption-based asset pricing. Ann Finance 15, 179–203 (2019). https://doi.org/10.1007/s10436-019-00344-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10436-019-00344-1

Keywords

- Household underlying principles

- Representative agent

- Garnishment of a delinquent household endowment

- Asset pricing puzzles

- Credit market issues