Abstract

Since the onset of the COVID-19 pandemic, financial and commodity markets have exhibited significant volatility and displayed fat tail properties, deviating from the normal probability curve. The recent Russia-Ukraine war has further disrupted these markets, attracting considerable attention from both researchers and practitioners due to the occurrence of consecutive black swan events within a short timeframe. In this study, we utilized the Quantile-VAR technique to examine the interconnectedness and spillover effects between African equity markets and international financial/commodity assets. Daily data spanning from January 3, 2020, to September 6, 2022, was analyzed to capture tail risks. Our main findings can be summarized as follows. Firstly, the level of connectedness in returns is more pronounced in the lower and upper tails compared to the median. Secondly, during times of crisis, African equity markets primarily serve as recipients of systemic shocks. Lastly, assets such as Silver, Gold, and Natural Gas exhibit greater resilience to systemic shocks, validating their suitability as hedging instruments for African equities, in contrast to cryptocurrencies and international exchange rates. These findings carry significant implications for policymakers and investors in Africa equities.

Similar content being viewed by others

Introduction

In recent years, the global economy has experienced significant uncertainty in response to the twin shocks emerging from COVID-19 pandemic and the more recent Russia-Ukraine conflict [6, 24]. The pandemic's evolving nature, characterized by virus infections, deaths, and containment measures like lockdowns and travel restrictions, has intensified economic uncertainty [6]. Additionally, the ongoing Russia-Ukraine conflict, marked by geopolitical tensions and an absence of clear resolution, has further contributed to global instability [39]. Notably, major disruptive events such as the pandemic and the Russia-Ukraine war render financial markets vulnerable and introduce systemic risks [7]. The resulting contagion effects, driven by extreme volatility, foster investor insecurity and prompt them to diversify their portfolios across various markets [79]. As risk hedging alternatives to equities, assets such as gold, crude oil, foreign currencies, and cryptocurrencies have gained prominence [25, 31, 41, 47, 48].

Amidst the turmoil witnessed in global financial and commodity markets, African equity markets have not been spared from effects of COVID-19 and the Russia-Ukraine war, and have also experienced heightened volatility since the onset of the pandemic. The initial declaration of COVID-19 as a global pandemic in March 2020 led to crashes in global equities, cryptocurrencies, exchange rate, and oil markets, with similar downturns observed in African frontier stock markets [11, 17]. However, a turn of events occurred when most financial markets, including African frontier markets, witnessed record-high prices between November 2021 and March 2022 [56]. These observations suggest that African equities are more integrated into the global economy, making them susceptible to spillover effects during times of financial uncertainty [4]. This contrasts with the traditional view of African equities as disconnected or decoupled from global markets, potentially serving as hedges for equities in industrialized economies [37].

Considering the recently observed susceptibility of African equities to international equity spillovers in the post-pandemic era, coupled with the increasing accessibility and participation of international investors in African stock markets, understanding the interconnectedness and spillover effects between African equities, financial markets, and commodity markets becomes crucial to identifying diversification benefits and detecting sources of market vulnerability [2, 4]. Paying particular attention to tail-spillover effects, which are prominent during rare and extreme events like the COVID-19 pandemic and the Russia-Ukraine war, is of paramount importance. However, most existing studies investigating spillover effects between equity markets and financial/commodity markets during these Black Swan events have primarily focused on mean-based analytical frameworks, hence neglecting tail-risk connectedness [6, 19, 20, 35, 61, 66,67,68, 69,70,71]. To address this limitation, our study employs the recently-introduced quantile vector autoregressive (QVAR) framework of Ando et al. [10], enabling the analysis of spillovers across different conditional distributions, including tail-risk connectedness.

Our study uses the quantile connectedness framework to examine the hedging properties of commodities, cryptocurrencies, and international exchange rates in relation to African equities during various market states in the post-COVID-19 era. Whilst we acknowledge the growing number of recent studies that have examined spillover effects between African equities and global financial/commodity markets [2, 12, 52, 54, 71], our study complements this prior research in two significant ways. Firstly, compared to previous studies, our research covers more recent data, incorporating crucial events like the Russia-Ukraine conflict and the subsequent transition of industrialized Central Banks from unconventional monetary policy (UMP) to traditional policy conduct, which recent studies have shown to impact spillover effects in various financial and agriculture markets [20, 35, 39, 61, 69,70,71]. Secondly, most previous studies have focused on the hedging options of one or two asset classes, such as oil [12], commodities [2], commodities and gold [71], or cryptocurrencies and precious metals [52, 54]. In contrast, we explore a more comprehensive range of alternative hedging options, including international currencies, thus providing an analysis using a more complete basket of hedging options.

The rest of this paper is organised as follows: Sect. "Literature review" discusses related literature on the topic. Sect. "Methodology" presents the methodologies while Sect. "Data" description of data. Sect. "Empirical results and discussion" presents and discusses the results while the conclusion and recommendations are provided in Sect. "Conclusion".

Literature review

The analysis of spillover effects across equity markets has a rich history, but recent global events such as the COVID-19 pandemic and the Russia-Ukraine war have revitalized interest in this specific area of study. These notable occurrences, often labeled as "Black Swan events," possess distinct characteristics. They catch us by surprise, exert an extraordinary influence, and despite their exceptional nature, efforts are made to comprehend their origins [65]. Black Swan events tend to trigger anxiety within financial markets. Investors and fund managers commonly opt for diversifying their portfolios to minimize the risks associated with heightened uncertainty. Conversely, risk-takers like speculators often seize opportunities for short-term gains amidst the turbulence in the financial realm [3, 80]. The amalgamation of fear and greed during these black swan events leads to irrational conduct among market participants, causing asset prices to deviate from their intrinsic values. As a consequence, shocks emanating from a singular equity market or a cluster of markets can cascade into other stock exchanges through inter-market connections. This occurrence arises as a product of cross-market interdependencies.

Extreme events such as the COVID-19 pandemic and Russian-Ukraine conflicts are usually associated with strong co-movement and spillover effects across financial markets and assets [22, 81]. As such, there are growing attempts to quantify the systemic risk emanating from these events. In relation to these events, emerging literature can be grouped into two. The first group of studies are those that focused on the risk-return spillover for a single type of financial asset such as equity [1, 6, 13, 21, 33, 46, 51, 64, 74, 81], commodity [16, 24, 39, 45, 58, 66, 69, 70, 76, 81], and cryptocurrency [8, 53, 57, 59, 77], and foreign exchange [73].

The second group of studies explored the risk-return spillover across multiple financial assets such as equity, commodity, foreign exchange, and cryptocurrency. This group of studies is more closely related to the current paper, and they are further segmented into four sub-groups of literature.

The first sub-group comprises studies that have used wavelet techniques to explore spillovers between crude oil futures and stock markets in different countries. Ali et al. [7] found that there are strong co-movements and bidirectional causalities between crude oil futures and stock markets in the USA, Canada, China, Russia, and Venezuela. Similarly, Cui et al. [25] found a strong dependence structure among oil and stock markets over long-term scales, with risk spillovers transmitted mostly in the long run. Ajmi et al. [5] applied the BEKK-GARCH approach to study the volatility spillover between the USA stock, gold, and crude oil markets and found that stocks and gold drive the transmission of volatility to the crude oil market. Mezghani et al. [49] also used a similar approach to investigate six major stock markets and commodity futures and found that the COVID-19 pandemic intensified the volatility spillover among the markets, with commodity markets being the net recipients of volatility spillovers.

Another study by Mensi et al. [48] used the Markov-switching approach to study spillovers between the USA and Chinese stock, crude oil, and gold futures. The study found that gold and stock markets are the net transmitters of spillover during the low volatility regime but net receivers during the high volatility regime. By contrast, crude oil was the net receiver (transmitter) during the low (high) volatility regime. Using the spillover index, Jebabli et al. [38] analyzed volatility spillovers between the energy market and global equity markets and found spillovers from the global equity markets to the energy market. Elgammal et al. [28] also found evidence of bidirectional volatility spillovers across global equity, gold, and energy markets. In Africa, Morema and Bonga-Bonga [50] found significant volatility spillover between gold and equity markets, as well as crude oil and the equity market in South Africa. Urom et al. [71] found that African markets are weakly connected to other markets and that energy markets are the major transmitters of shocks. The study also revealed that French and South African equity markets transmitted the largest volatility spillover over the period.

The second sub-group of literature examines the risk-return spillover between equity and currency markets, including foreign exchange and cryptocurrencies. Aydogan et al. [14] investigated spillover between equity and cryptocurrencies in G7 and seven emerging markets using the VAR-GARCH approach. The study found strong return and volatility spillover between G7 stock markets and cryptocurrencies, with unidirectional spillover in most emerging markets but bidirectional in most G7 markets. Ha [34] applied TVP-VAR to study spillover between cryptocurrency and six stock markets and reported the influence of the pandemic on market linkages. The study found Bitcoin and Binance Coin to be the net receivers of spillover, while the USA stock market is the net transmitter. Zivkov et al. [82] found bidirectional volatility transmission between stock markets and exchange rates in selected East European and Eurasian countries. Kamran et al. [41] found weak correlation between Bitcoin and the Australian stock markets and hedging benefit during the crisis period. Amewu et al. [9] applied the wavelet technique for Ghana and found evidence of time-varying co-movement between foreign exchange rates and stock, with a weak association among the markets.

The third sub-group of studies analyzed the risk-return spillover between currency markets and commodities. Zhang et al. [78] investigated the information spillover from the COVID-19 pandemic to crude oil, gold, and Bitcoin markets using the time–frequency analysis method. The study revealed evidence of return and volatility spillover from the COVID-19 pandemic news to crude oil, gold, and Bitcoin, with media hype being the main transmitter of shocks to all markets. Nugroho [53] analyzed spillover for gold-backed cryptocurrencies and gold using the DCC-GARCH and spillover index techniques and found increased connectedness during COVID-19, with gold as the net receiver of spillover. Derbali et al. [26] studied the co-movement between Bitcoin and gold and found a strong correlation that reacts to COVID-19 news from the USA and China. Yildirim et al. [75] examined volatility transmission between real exchange rates and precious metals and crude oil among Mexico, Indonesia, and Turkey and found bidirectional causality between precious metals and the exchange rate, with the volatility spillover disappearing during the COVID-19 pandemic. Sayed and Charteris [61] found that the South African currency is a net recipient of volatility spillovers from commodity markets.

The fourth subgroup of studies investigates the spillover effects among various financial assets. For example, Ghorbel and Jeribi [32] employed the multivariate generalized autoregressive conditional heteroskedasticity (MGARCH) model to analyze the time-varying co-movements between G7 stock markets, crude oil, gold, Bitcoin, and the COVID-19 pandemic. Their findings suggest that crude oil transmits volatility to both stock indices and gold and Bitcoin. Ghorbel et al. [31] utilized the spillover index to demonstrate the high dependence among stock markets and identified Bitcoin as the primary transmitter of volatility during crises, while Maker and gold were the main receivers. Likewise, Elsayed et al. [29] confirmed Bitcoin's role as the primary transmitter of volatility spillovers to other assets. On the other hand, the study by Hung [36] presented mixed results, with the equity market transmitting volatility to crude oil and gold but receiving it from Bitcoin. Additionally, crude oil and gold were identified as the primary transmitters of return spillovers to Bitcoin. Similarly, Le et al. [44] revealed that Bitcoin and the Fintech index received the most significant spillovers during the COVID-19 pandemic. Another study by Shaikh [62] concluded that Brent crude oil and equity markets were the primary transmitters, while gold, West Texas Intermediate (WTI), and the US dollar index were the primary receivers. Furthermore, Wang et al. [72] found that the US and UK stock markets were net transmitters, while other markets were net receivers. Other studies with similar research interests include Chen et al. [20], Corbet et al. [23], Kakinuma [40], and Kumar and Singh [43].

Despite the growing body of literature on the spillover effects of returns and volatility among various financial markets and assets during the COVID-19 pandemic and Russian-Ukraine war, the literature on the spillover and connectedness of African equity with other financial markets and assets remains limited. Therefore, this paper aims to bridge this gap by investigating the risk-return spillover effects between African equity and other financial markets and assets during the current pandemic and Russian-Ukraine war.

Methodology

To investigate the co-movement and volatility spillover between African equity, commodities, foreign exchanges, and cryptocurrency markets, we applied the quantile vector autoregression (QVAR) connectedness approach proposed by Ando et al. [10]. The approach is an extension of the spillover index developed by Diebold and Yilmaz [27] to account for tail behaviour of financial at different quantiles [10]. The application of this models is motivated by evidence in the literature [8, 15, 18, 30, 60, 63, 77]. The details of the estimation technique are presented below.

We follow Ando et al. [10] and begin by defining the n-variable quantile VAR process of order p as:

where \({Z}_{t}\) and \({Z}_{t-j}\) are an \(n\times 1\) dimensional vector of return and conditional volatility generated from Eqs. (1) and (2); \(\tau \) ranges from 0 to 1 which corresponds to different quantiles. We define three quantiles for this paper as 0.1, 0.5 and 0.9. The \(V\left(\tau \right)\) is an \(n\times 1\) dimensional vector of the conditional mean and \({\phi }_{j}(\tau )\) is \(n\times n\) dimensional coefficient metrices while \({\epsilon }_{t}(\tau )\) is an \(n\times 1\) dimensional vector of serially uncorrelated errors. Equation (4) can be transformed into an infinite order moving average specification of QVAR as:

We also follow the generalised forecast error variance decomposition (GFEVD) frameworks developed by Koop et al. [42] and Pesaran and Shin [55]. The H-step ahead forecast error variance decomposition matrix \({\Theta }^{H}=[{\Theta }_{ij}^{H}]\) is expressed as:

where \(\Sigma \) is the variance matrix of the error vector \(\epsilon \); \({e}_{i}\) is an \(n\times 1\) selection vector with one as the \(i\mathrm{th}\) element and zero if otherwise. Thereafter, individual element of the variance decomposition matrix is normalised by the row sum as:

where \(\sum_{j=1}^{n}{\widetilde{\Theta }}_{ij}^{H}=1\), and \(\sum_{i,j=1}^{n}{\widetilde{\Theta }}_{ij}^{H}=n.\) Based on these elements, the four measures of connectedness at each quantile are derived by applying the GFEVD. First, the total return or volatility connectedness (spillover) index (TCI) at each quantile is defined as:

The TCI index provides information on average contribution of shock to the forecast error variance among the financial markets/assets. Also, it allows for the determination of directional volatility spillover transmitted to (TO) market \(i\) from all other markets \(j\) as well as volatility received by markets \(j\) from (From) market \(i\) as shown by Eqs. (6) and (7) below:

Based on the above equations, the net spillover for each financial market/asset is computed as the difference between the gross volatility transmitted from market \(i\) to other markets/assets and gross volatility received by market \(i\) from other financial markets/assets:

In this regard, a positive net value indicates that the financial/asset is a net risk transmitter while a negative value indicates a net risk receiver.

Data

We employ daily time series data covering the period from January 3, 2020, to September 6, 2022. Our analysis covers 10 top African stock markets by market capitalization and stock performance (Botswana, the Bourse Regionale des Valeur Mobilieres, Egypt, Kenya, Mauritius, Morocco, Namibia, Nigeria, South Affrica and Tunisia), 6 top energy and precious metals commodities (copper, brent crude, natural gas, gold, platinum and silver); 2 foreign exchanges (Euro/dollar and Pound/dollar exchange rate); and 2 major cryptocurrencies (Bitcoin and Ethereum). All data used in this paper are sourced from the Investing.com and we transform the raw data into returns series using the method as:

where the daily return is given by \({R}_{it}\) and \({P}_{it}\) is the closing price of a given asset \(i\) at time \(t\) and \(t-1\).

Table 1 summarizes the acronyms used for each of the time series whereas Table 2 reports the descriptive properties and unit root tests for the returns series of each variable over the sample period. As reported in the table, majority of African equity markets recorded negative average returns over the period. Among the equity markets with positive returns, Nigeria has the highest returns (0.126%) followed by BRVM (0.038%) and Tunisia (0.025%). The worst performing equity markets are Egypt (-0.048%), Namibia (0.039%) and Kenya (0.036%). Regarding the international financial assets, apart from Euro-dollar, British pound-dollar, natural gas and platinum, other financial assets recorded positive return. It is also shown that Ethereum (0.257%), Brent crude (0.128%) and Bitcoin (0.103%) reported the highest returns. The unconditional variance as measured by the standard deviation shows that among African equity markets, Namibia (7.058), South Africa (1.551) and Egypt (1.268) exhibit the highest volatility. While Ethereum (5.389), natural gas (4.137), Bitcoin (4.070) and Brent crude (3.304) reported the largest volatility among the international financial assets. With exception of Namibia, Nigeria, and natural gas, all the returns series are negatively skewed. This indicates a high change of realising negative returns over the period. In addition, the kurtosis shows that all the return series are leptokurtic with respect to a normal distribution. Furthermore, all the returns series are stationary as indicated by the unit root tests (Augmented Dickey–Fuller-ADF and Phillips–Perron-PP) and exhibit volatility clustering behaviour as suggested by autoregressive conditional heteroscedasticity (ARCH) and Ljung–Box tests (LQ).

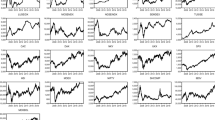

Figure 1 plots the evolution of return across African equity markets and international financial assets. The evidence from the figure shows wide fluctuation at the beginning of the sample period (January 2020–May 2020) and towards the beginning of 2022 (March 2022–May 2022) for all the returns. The periods of high fluctuation identified in the figures are associated with the World Health Organisation (WHO) declaration of COVID-19 as a global pandemic, the collapse of crude oil prices due to price war between Saudi Arabia and Russia, and surge in the global commodity prices due to Russia-Ukraine conflict [24, 25, 32]. This preliminary finding supports the need for this study.

Evolution of return across African equity markets and international financial assets

Empirical results and discussion

This section provides the analysis of return and volatility connectedness and spillover between African equities and international financial assets based on QVAR approach. Specifically, the analysis is based on lag 2 selected by Akaike information criteria (AIC) and 10-steps ahead forecast error variance decomposition together with 150-days rolling window. One interesting feature of QVAR is the ability capture the connectedness and spillover at lower and upper tails of the conditional distributions [10]. Such a feature provides information on the pattern of connectedness and spillover under extreme market conditions. As a result, three different quantiles (such as 0.05, 0.50, and 0.95) are compared, corresponding to bearishish (lower), normal (median), and bullish (upper) market conditions. In this section, we first present and discuss the result of the quantile static connectedness and spillover followed by the network connectivity diagrams, the dynamic spillover analysis and lastly the net directional spillovers.

Quantile static connectedness analysis

We start by reporting the results of static connectedness analysis between African equity markets and international financial assets. Tables 3, 4 and 5 report the results of the static return connectedness for the three quantiles. As reported in the tables, the total connectedness index (TCI) varies across the three quantiles, indicating the return spillover between African equity markets and international financial assets is dependent on market conditions. Importantly, the results show strong connectedness at the lower (91.89%) and upper (91.69%) quantiles compared to the median (57.67%) quantile. This finding implies that extreme negative and positive shocks emanating from events such as COVID-19 pandemic, oil price war between Saudi Arabia and Russia and Russia-Ukraine war, have significant impact on the pattern of returns spillover at lower and upper tails. Moreover, the contributions to and from others for both the lower and upper quantiles are much larger than those in the median quantile. These results are consistent with the recent works of Al-Shboul et al. [8], Billah et al. [15], Farid et al. [30] which observed similar patterns across different market states.

Next, we consider the static directional spillover which shows the amounts of spillovers received and transmitted as well as the net spillover at different quantiles. Focusing on the net spillovers, we observe that under bearishish market condition (Panel A of Table 3), African equity markets (except for Kenya and South Africa) are mostly the net receivers while majority of financial/commodities assets (except for brent oil, natural gas and silver) are net transmitters. Also, the results show that the largest recipient of spillover is Botswana (− 8.57%), followed by Mauritius (− 5.63%) and Tunisia (− 4.16%) while the largest contributor to spillovers is the British pound/dollar (8.7.3%) followed by crude oil (5.02%) and platinum (4.08%). Interestingly, we observe a role reversal under normal market condition (Panel B of Table 4) with all the international financial assets being the net receivers while half of African equity markets are net transmitters. Among the international financial assets, the largest recipient of spillovers is natural gas (− 20.01%), crude oil (− 13. 64%) and Bitcoin (− 6.13%) whereas the biggest contributors of spillover are Botswana (84.57%), South Africa (8.35%) and Mauritius (7.48%). Similarly, the result in Panel C of Table 5 shows that under the bullish market condition, majority of international financial assets are the recipients of spillover while most Africa equity market are transmitters. The results specifically show that South Africa (8.27%), Nigeria (7.40%) and Tunisia (4.37%) are largest contributors whereas natural gas (− 2.47%), gold (− 2.24%), and silver (− 2.14%) are the largest recipients of return spillover. Therefore, the above findings indicate that African equity markets are recipient of return spillovers from the international financial assets and commodities during bearishish market condition but constitute a major source of spillovers during normal and bullish market conditions.

Overall, the findings from the static connectedness analysis can be summarized in three points. Firstly, we find stronger overall market connectedness at the tail-end distributions. This implies that investors should be more concerned about spillover effects during the bullish and bearish markets compared to tranquil periods. Similar conclusions were drawn by Bouri et al. [18], Shahzad et al. [63], Farid et al. [30], Rao et al. [60] and Yousaf and Yarovaya [77] yet for different financial markets. Secondly, Kenya is the only equity market which is resilient to systemic shocks in all market states. This would imply that this equity market is more disconnected from systemic shocks and thus offers support to the traditional intuition that African equities are better diversifies of market risk due to their lack of connectedness to global markets [37]. To a lesser extent, similar conclusions can be drawn for South Africa (bullish and tranquil markets and Mauritius (tranquil and bull markets which show resilient over two states and yet are exposed to shocks at the tail end distributions. The remaining majority of African equities are either vulnerable to spillover shocks in two market state (BRVM, Botswana, Morocco, Namibia or at all market states (Egypt, Nigeria and Tunisia hence highlighting their need for diversification with other asset classes. Lastly, energy commodities and precious metals appear to more resilient to systematic shocks compared to financial assets such cryptocurrencies and exchange rates and during bearishs and bullish. In particular, we find that brent oil, gas and silver (cooper, gas and platinum are suitable for diversification purposes during bearish (bullish markets. These results are interesting to observe since they contradict conventional literature which advocates for Gold and Bitcoin as suitable diversifies of risk in African equities [52, 54, 71]. Overall, we conclude that a select few commodities are resilient to systemic shocks and hence could serve as viable diversifiers for the host of African equities which were found to be susceptible to spillover shocks.

Network connectivity plot for return and volatility

In this section, the analysis of network connectivity for return and volatility is provided to better visualise the degree of connectedness and spillover between African equities and international financial assets. Figure 2 plots the network connectivity of the variables under different quantiles with the blue (yellow) colour represents net transmitter (receiver) of shocks. The size of the node depends on the amounts of shocks received or transmitted. Thus, the larger the node, the higher the amounts of shocks received or transmitted and vice versa. Also, the edges represent the origin and direction of spillovers while the thickness of the edge shows the degree of the connectedness.

Network connectivity plot for returns

Consistent with the results of static analysis, we observe in Fig. 2a that under bearishish market condition, African equity markets are shock receivers except Namibia and South Africa. The figure shows that Botswana and Mauritius are the largest recipients of spillovers from the international financial assets. By contrast, the international financial assets are net transmitters except natural gas. The largest return transmitters are British pound/dollar and platinum. Under normal markets conditions as reflected in Fig. 2b, African equity markets are mainly net shock receivers from the system, especially Botswana, Mauritius, Nigeria, Tunisia and BRVM. It also shown African equity markets like Kenya and South Africa large contributors to the systemic shocks. Again, it is observed that most international financial asset are transmitters under normal markets conditions with the British pound/dollar and crude oil as the leading transmitters of shock. In terms of bullish market condition in Fig. 2c, we observe reversal of role with African equity markets being the primary transmitters while international financial assets as the receivers. The leading contributors are among the African equity markets are Botswana, Morocco, Mauritius, South Africa and Namibia. These findings collaborate the results of the static return analysis presented in the previous section.

Dynamic connectedness analysis

Next, we applied the rolling window to investigate the time-varying connectedness between African equity markets and international financial assets. As before, we perform the analysis across the three quantiles (lower, median, and upper) and plot the total dynamic connectedness in Fig. 3. From Fig. 3, it can be observed from the figures that the total return connectedness index exceeds 98% at the lower and upper quantiles while exceeding 70% at the median quantile. This finding indicates that the degree of connectedness appears extremely high at the lower and upper quantiles compared to the median quantile. Also, this finding collaborates the results of the static return connectedness.

Dynamic connectedness for return

We further observe heightened connectedness across the three quantiles over the periods February 2020–July 2020, September 2020–January 2021, May 2021–September 2021, November 2021–January 2022, and February 2022–onwards. These periods are associated with five extreme events. The first period (February 2020–July 2020) corresponds to the early period of COVID-19 pandemic, and crude oil price war between Saudi Arabia and Russia. The second period (September 2020–January 2021) is associated with the second wave of the COVID-19 pandemic, the January 6th capital riot in the USA and the release of the clinically approved COVID-19 vaccination. The third period (May 2021–October 2021) corresponds to the third wave of the COVID-19 pandemic which is associated with the delta variant. The fourth period (November 2021–January 2022) covers the fourth wave of the pandemic due to the omicron variant. The fifth period (February 2022–present) covers the start of the Russian-Ukraine war and the reversion back to monetary policy ‘normalization period’ of Central Banks in industrialized economies.

The analysis of the total dynamic connectedness provides two key findings. Firstly, even after accounting for dynamic time-variation we still find that the extent of connectedness between African equity markets and financial/commodity assets peaked during the periods extreme market events compared to normal market condition. Secondly, investors and market regulators should pay attention events related to the COVID-19 pandemic, Ukraine-Russia war and US monetary policy since higher connectedness is observed during these periods. However, we cannot determine the extent to which individual markets are affected spillovers during different market events and we shed light on this in the next section.

Net directional spillover

Lastly, we examine the dynamic net direction spillover effects for individual markets, and plot our findings in Fig. 4a–c for the 5th, 50th, and 95th quantiles, respectively. The findings reveal switching effects from net transmission to net receivers of shocks across all markets throughout the entire time window. Therefore, our interpretation focuses on the dominance of the net transmission effect, particularly during periods of higher market connectedness indicated by our time-varying dynamic connectedness index.

a Net directional return spillover (quantile = 0.05). b Net directional return spillover (quantile = 0.50). c Net directional return spillover (quantile = 0.95)

Starting with the results at the median quantile, we find that Botswana, Kenya, Mauritius, Morocco, Namibia, and South Africa (BRVM, Egypt) equities are primarily net transmitters (receivers) of shocks. Significant peaks are observed at the onset of the pandemic, around November 2021, and at the beginning of the Russia-Ukraine war. Conversely, most commodities and financial assets are predominantly net receivers, except for Copper and Silver, which act as net transmitters of shocks, especially during periods of higher market connectedness.

At the tail-end distribution of the quantile connectedness, the switching between net transmitters and receivers of shocks is even more pronounced than at the median quantile. However, some markets are consistently net receivers/transmitters at this distribution. For example, at the 5th quantile, commodities such as Brent, Natural Gas, and Gold (Botswana) are major transmitters of shocks during bearish markets, while Nigeria is predominantly a net receiver. Conversely, at the 95th quantile, only Gold, Silver, and African equities such as Nigeria, South Africa, Mauritius, Namibia, and Nigeria act as predominant transmitters of shocks, while Botswana is primarily a net receiver.

Overall, these findings suggest that African equities exhibit greater resilience to market shocks during tranquil market states but become more susceptible during extreme events. This underscores the notion that African equities have become more interconnected with global markets, particularly in the post-COVID era [2]. As for diversification, commodities like Gold, Silver, and Copper display resilience to market shocks across different market states, making them suitable for consideration by investors seeking a more diversified portfolio. These findings contradict the conclusions of Omane-Adjepong and Alagidede [54], who suggest that cryptocurrencies offer better diversification for African equities compared to traditional commodities like precious metals or energy commodities.

Conclusion

This paper investigated the connectedness and spillover between African equity and international financial assets using the Quantile-VAR measurement to generate condition for lower (0.05), middle (0.50) and upper (0.95) quantiles. In particularly, our analysis covers ten African equity markets (namely Botswana, BRVM, Egypt, Kenya, Mauritius, Morocco, Namibia, Nigeria, South Africa and Tunisia), two foreign exchange rate (Euro/dollar, and British pound/dollar), six commodities (Brent crude oil, copper, gold, natural gas, platinum and silver), and two cryptocurrencies (Bitcoin and Ethereum). Also, we use the daily data over the period 3 January 2020 to 6 September 2022 to account for the effect of COVID-19 pandemic and Russia-Ukraine war.

Our findings reveal three distinct episodes characterized by heightened tail-connectedness among the markets. Firstly, during the stock and oil market crashes in April 2020, prompted by the global economic shutdown in response to the pandemic, followed by a significant market upswing after the approval of COVID-19 vaccinations from December 2020 to March 2021. Secondly, during the announcement of various COVID-19 variants between 2020 and 2021. Lastly, during the ongoing Ukraine-Russia conflict the reversion back to monetary policy ‘normalization period’ of Central Banks in industrialized economies. In each of these extreme co-movements, the individual financial and commodity markets exhibit increased vulnerability to systemic spillover shocks.

Moreover, the study identifies the net transmitters and net receivers of systemic tail-end shocks to assess the hedging benefits of cryptocurrency and commodity assets against African equity tail-risk during extreme events. We find that most African equity markets, cryptocurrencies, and exchange rates primarily act as recipients of systemic shocks in the post-COVID-19 era. Conversely, certain commodities such as Gold, Silver, and Natural Gas emerge as significant transmitters of these shocks, highlighting their potential as hedging assets. These results challenge the conventional belief that African equities are decoupled from international markets and suggest their unsuitability for diversification purposes against financial and commodity assets. Additionally, they question the notion that cryptocurrencies serve as superior hedging options compared to traditional commodities like Gold and Gas.

Overall, our findings are valuable for market participants seeking to explore tail-risk hedge strategies and leverage opportunities presented by sharp downward market swings and increased investment payoffs during extreme market movements. Additionally, these findings have implications for market regulators, who can monitor market contagion effects and implement appropriate regulatory measures to mitigate systemic risks. These implications are particularly relevant given the ongoing global uncertainty surrounding the pandemic, the Russia-Ukraine conflict, and other geopolitical tensions.

Availability of data and materials

The data are attached as Additional file 1.

Abbreviations

- ADF:

-

Augmented Dickey Fuller

- AIC:

-

Akaike information criteria

- ARCH:

-

Autoregressive conditional heteroscedasticity

- BEKK-GARCH:

-

Baba, Engle, Kraft and Kroner Generalized autoregressive conditional heteroscedasticity

- BRVM:

-

Bourse Regionale des Valeur Mobilieres

- COVID-19:

-

Coronavirus 19

- GFEVD:

-

Generalised forecast error variance decomposition

- VAR-GARCH:

-

Vector autoregressive generalized autoregressive conditional heteroscedasticity

- DCC GARCH:

-

Dynamic conditional correlation generalized autoregressive conditional heteroscedasticity

- MGARCH:

-

Multivariate generalized autoregressive conditional heteroscedasticity

- NFT:

-

Non-fungible tokens

- QVAR:

-

Quantile vector autoregressive

- TCI:

-

Total connectedness index

- TVP-VAR:

-

Time varying parameter vector autoregressive

- UK:

-

United Kingdom

- US:

-

United States

- VAR:

-

Vector autoregressive

- WAEMU:

-

West African Economic and Monetary Union

- WHO:

-

World Health Organization

- WTI:

-

West Texas Intermediate

References

Abdullahi SI (2022) Islamic equities and COVID-19 pandemic: measuring Islamic stock indices correlation and volatility in period of crisis. Islam Econ Stud 29(1):50–66

Agyei SK, Bossman A (2023) Exploring the connectedness between commodities and African equities. Cogent Econ Finance 11(1):e2186035

Ahmed W, Kutan A, Gupta S (2021) Black swan events and COVID-19 outbreak: sector level evidence from the US, UK, and European stock exchanges. Int Rev Econ Financ 75:546–557. https://doi.org/10.1016/j.iref.2021.04.007

Akhtaruzzaman M, Benkraiem R, Boubaker S, Zopounidis C (2022) COVID-19 crisis and risk spillovers to developing economies: evidence from Africa. J Int Dev 34(4):898–918

Ajmi H, Arfaoui N, Saci K (2021) Volatility transmission across international markets amid COVID 19 pandemic. Stud Econ Finance 38(5):926–945

Akinlaso MI, Robbana A, Mohamed N (2022) Volatility transmission within financial markets during the COVID-19 pandemic: are faith-based investors well off in Tunisia? J Islam Account Bus Res 13(1):98–113

Ali SRM, Mensi W, Anik KI, Rahman M, Kang SH (2022) The impacts of COVID-19 crisis on spillovers between the oil and stock markets: evidence from the largest oil importers and exporters. Econ Anal Policy 73:345–372

Al-Shboul M, Assaf A, Mokni K (2022) When bitcoin lost its position: cryptocurrency uncertainty and the dynamic spillover among cryptocurrencies before and during the COVID-19 pandemic. Int Rev Financ Anal 83:102309

Amewu G, Junior PO, Amenyitor EA (2022) Co-movement between equity index and exchange rate: fresh evidence from COVID-19 era. Sci Afr 16:e01146

Ando T, Greenwood-Nimmo M, Shin Y (2022) Quantile connectedness: modeling tail behaviour in the topology of financial networks. Manag Sci 68(4):2377–3174

Arif M, Naeem M, Farid S, Nepal R, Jamasb T (2022) Diversifier or more? Hedge and safe haven properties of green bonds during COVID-19. Energy Policy 168:e113102

Asafo-Adjei E, Adam AA, Darkwa P (2021) Can crude oil price returns drive stock returns of oil producing countries in Africa? Evidence from bivariate and multivariate wavelet. Macroeconomics and Finance in Emerging Market Economies (forthcoming)

Asl MG, Rashidi MM (2021) Dynamic diversification benefits of Sukuk and conventional bonds for the financial performance of MENA region companies: empirical evidence from COVID-19 pandemic period. J Islam Account Bus Res 12(7):979–999

Aydogan B, Vardar G, Taçoglu C (2021) Volatility spillovers among G7, E7 stock markets and cryptocurrencies. J Econ Adm Sci. https://doi.org/10.1108/JEAS-09-2021-0190

Billah M, Karim S, Naeem MA, Vigne SA (2022) Return and volatility spillovers between energy and BRIC markets: evidence from quantile connectedness. Res Int Bus Finance 62:101680

Bildirici M, Bayazit NG, Ucan Y (2020) Analyzing crude oil prices under the impact of COVID-19 by using LSTARGARCHLSTM. Energies 13:2980

Boateng E, Adam AM, Owusu PJ (2021) Modelling heterogenous relationship between crude oil and implied volatility index and the African stocks in the coronavirus pandemic. Resour Policy 74:e102389

Bouri E, Lucey B, Saeed T, Vo XV (2020) Extreme spillovers across Asian-Pacific currencies: a quantile-based analysis. Int Rev Financ Anal 72:e101605

Bouri E, Cepri O, Gabauer D>, Gupta R (2021) Return connectedness across asset classes around the COVID-19 outbreak. Int Rev Financ Anal 73:e101646

Chen Y, Xu Y, Hu M (2022) Asymmetric volatility spillovers and dynamic correlations between crude oil price, exchange rate and gold price in BRICS. Resour Policy 78:102857

Cheng T, Liu J, Yao W, Zhao AB (2022) The impact of COVID-19 pandemic on the volatility connectedness network of global stock market. Pac Basin Financ J 71:101678

Choi SY (2022) Volatility spillovers among Northeast Asia and the US: evidence from the global financial crisis and the COVID-19 Pandemic. Econ Anal Policy 73:179–193

Corbet S, Hou YG, Hu Y, Oxley L, Xu D (2021) Pandemic-related financial market volatility spillovers: evidence from the Chinese COVID-19 epicentre. Int Rev Econ Finance 71:55–81

Corbet S, Goodell JW, Gunay S (2020) Co-movements and spillovers of oil and renewable firms under extreme conditions: new evidence from negative WTI prices during COVID-19. Energy Econ 92:104978

Cui J, Goh M, Li B, Zou H (2021) Dynamic dependence and risk connectedness among oil and stock markets: new evidence from time-frequency domain perspectives. Energy 216:119302

Derbali A, Naoui K, Jamel L (2021) COVID-19 news in USA and in China: which is suitable in explaining the nexus among Bitcoin and gold? Pac Account Rev 33(5):578–595

Diebold FX, Yilmaz K (2012) Better to give than to receive: predictive directional measurement of volatility spillover. Int J Forecast 28:57–66

Elgammal MM, Ahmed WMA, Alshami A (2021) Price and volatility spillovers between global equity, gold, and energy markets prior to and during the COVID-19 pandemic. Resour Policy 74:102334

Elsayed AH, Gozgor G, Lau CKM (2022) Risk transmissions between bitcoin and traditional financial assets during the COVID-19 era: the role of global uncertainties. Int Rev Financ Anal 81:102069

Farid S, Naeem MA, Paltrinieri A, Nepal R (2022) Impact of COVID-19 on the quantile connectedness between energy, metals and agriculture commodities. Energy Econ 109:105962

Ghorbel A, Fakhfekh M, Jeribi A, Lahiani A (2022) Extreme dependence and risk spillover across G7 and China stock markets before and during the COVID-19 period. J Risk Finance 23(2):206–244

Ghorbel A, Jeribi A (2021) Contagion of COVID-19 pandemic between oil and financial assets: the evidence of multivariate Markov switching GARCH models. J Invest Compliance 22(2):151–169

Ghorbel A, Loukil S, Bahloul W (2022) Connectedness between cryptocurrencies, gold and stock markets in the presence of the COVID-19 pandemic. Eur J Manag Bus Econ. https://doi.org/10.1108/EJMBE-10-2021-0281

Ha LT (2022) Interlinkages of cryptocurrency and stock markets during COVID-19 pandemic by applying a TVP-VAR extended joint connected approach. J Econ Stud. https://doi.org/10.1108/JES-01-2022-0055

Hasan M, Naeem MA, Arif M, Shahzad SJH, Vo XV (2022) Liquidity connectedness in cryptocurrency market. Financ Innov. https://doi.org/10.1186/s40854-021-00308-3

Hung NT (2022) Asymmetric connectedness among S&P 500, crude oil, gold and Bitcoin. Manag Finance 48(4):587–610

Iyke B, Ho S (2021) Investor attention on COVID-19 and African stock returns. MethodsX 8:e101195

Jebabli I, Kouaissah N, Arouri M (2022) Volatility spillovers between stock and energy markets during crises: a comparative assessment between the 2008 global financial crisis and the Covid-19 pandemic crisis. Financ Res Lett 46:102363

Just M, Echaust K (2022) Dynamic spillover transmission in agricultural commodity markets: what has changed after the COVID-19 threat? Econ Lett 217:110671

Kakinuma Y (2022) Nexus between Southeast Asian stock markets, bitcoin and gold: spillover effect before and during the COVID-19 pandemic. J Asia Bus Stud 16(4):693–711

Kamran M, Butt P, Abdel-Razzaq A, Djajadikerta HG (2022) Is Bitcoin a safe haven? Application of FinTech to safeguard Australian stock markets. Stud Econ Finance 39(3):386–402

Koop G, Pesaran MH, Potter SM (1996) Impulse response analysis in nonlinear multivariate models. J Econom 74(1):119–147

Kumar P, Singh VK (2022) Systemic spillover dynamics of crude oil with Indian financial indicators in post WPI revision and COVID era. Resour Policy 77:102773

Le LT, Yarovaya L, Nasir MA (2021) Did COVID-19 change spillover patterns between Fintech and other asset classes? Res Int Bus Finance 58:101441

Li J, Liu R, Yao Y, Xie Q (2022) Time–frequency volatility spillovers across the international crude oil market and Chinese major energy futures markets: evidence from COVID-19. Resour Policy 77:102646

Liu X, Chen Z, Chen Z, Yao Y (2022) The time-varying spillover effect of China’s stock market during the COVID-19 pandemic. Physica A 603:127821

Majumder SB (2022) Searching for hedging and safe haven assets for Indian equity market: a comparison between gold, cryptocurrency and commodities. Indian Growth Dev Rev 15(1):60–84

Mensi W, Reboredo JC, Ugolini A (2021) Price-switching spillovers between gold, oil, and stock markets: evidence from the USA and China during the COVID-19 pandemic. Resour Policy 73:102217

Mezghani T, Hamadou FB, Abbes MB (2021) The dynamic network connectedness and hedging strategies across stock markets and commodities: COVID-19 pandemic effect. Asia-Pac J Bus Adm 13(4):520–552

Morema K, Bonga-Bonga L (2020) The impact of oil and gold price fluctuations on the South African equity market: volatility spillovers and financial policy implications. Resour Policy 68:101740

Nguyen DT, Phan DH, Ming TC, Nguyen VL (2021) An assessment of how COVID-19 changed the global equity Market. Econ Anal Policy 69:480–491

Nkrumah-Boadu B, Owusu PJ, Adam AM, Asafo-Adjei E (2022) Safe haven, hedge and diversification for African stocks: cryptocurrencies versus gold in time–frequency perspective. Cogent Econ Finance 10(1):e2114171

Nugroho BA (2021) Spillovers and bivariate portfolios of gold-backed cryptocurrencies and gold during the COVID-19 outbreak. J Islam Account Bus Res 12(7):1055–1076

Omane-Adjepong M, Alagidede IP (2021) Exploration of safe havens for Africa’s stock markets: a test case under COVID-19 crisis. Financ Res Lett 38:e101877

Pesaran HH, Shin Y (1998) Generalized impulse response analysis in linear multivariate models. Econ Lett 58(1):17–29

Phiri A, Anyikwa I, Moyo C (2023) Co-movement between COVID-19 and G20 stock market returns: a time frequency analysis. Heliyon 9(4):e14195

Polat O, Günay EK (2021) Cryptocurrency connectedness nexus the COVID-19 pandemic: evidence from time–frequency domains. Stud Econ Finance 38(5):946–963

Rastogi S, Doifode A, Kanoujiya J, Singh SP (2021) Volatility integration of gold and crude oil prices with the interest rates in India. South Asian J Bus Stud. https://doi.org/10.1108/SAJBS-02-2021-0074

Raza SA, Shah N, Guesmi K, Msolli B (2022) How does COVID-19 influence dynamic spillover connectedness between cryptocurrencies? Evidence from non-parametric causality-in-quantiles techniques. Financ Res Lett 47:102569

Rao A, Gupta M, Sharma GD, Mahendru M, Agrawal A (2022) Revisiting the financial market interdependence during COVID-19 times: a study of green bonds, cryptocurrency, commodities, and other financial markets. Int J Manag Finance 18(4):725–755

Sayed A, Charteris A (2022) Is the rand a commodity currency? A volatility spillover analysis. Invest Anal J. https://doi.org/10.1080/10293523.2022.2090079

Shaikh I (2021) On the relation between the crude oil market and pandemic Covid-19. Eur J Manag Bus Econ 30(3):331–356

Shahzad SJH, Bouri E, Kristoufek L, Saeed T (2021) Impact of the COVID-19 outbreak on the US equity sectors: evidence from quantile return spillovers. Financ Innov 7:e14

Si DK, Li XL, Xu X, Fang Y (2021) The risk spillover effect of the COVID-19 pandemic on energy sector: evidence from China. Energy Econo 102:105498

Taleb N (2007) The Black Swan: the impact of the highly improbable. Random House, USA

Umar Z, Aziz S, Tawil D (2021) The impact of COVID-19 induced panic on the return and volatility of precious metals. J Behav Exp Finance 31:e100525

Umar Z, Jareño F, Gonzalez M (2021) The impact of COVID-19 related media coverage on the return and volatility connectedness of cryptocurrencies and fiat currencies. Technol Forecast Soc Change 172:e121025

Umar Z, Trabelsi N, Alqahtani F (2021) Connectedness between cryptocurrency and technological sectors: international evidence. Int Rev Econ Finance 71:910–922

Umar Z, Jareño F, Escribano A (2022) Analysis of the dynamic return and volatility connectedness for non-ferrous industrial metals during the COVID-19 pandemic crisis. Stud Econ Finance. https://doi.org/10.1108/SEF-01-2022-0045

Umar Z, Sayed A, Gubareva M, Vo XV (2022) Influence of unconventional monetary policy on agricultural commodities futures: network connectedness and dynamic spillovers of returns and volatility. Appl Econ. https://doi.org/10.1080/00036846.2022.2103084

Urom C, Ndubuisi G, Lo GD, Yuni D (2023) Global commodity and equity markets spillovers to Africa during the COVID-19 pandemic. Emerg Mark Rev. https://doi.org/10.1016/j.ememar.2022.100948

Wang D, Li P, Huang L (2022) Time-frequency volatility spillovers between major international financial markets during the COVID-19 pandemic. Finance Res Lett 46:102244

Wei Z, Luo Y, Huang Y, Guo K (2020) Spillover effects of RMB exchange rate among B&R countries: before and during COVID-19 event. Financ Res Lett 37:101782

Yasir M, Onder AO (2022) Time-varying herding spillover for emerging countries: evidence from BRIC countries and Turkey. Rev Behav Finance. https://doi.org/10.1108/RBF-10-2021-0218

Yildirim DC, Erdogan F, Tari EN (2022) Time-varying volatility spillovers between real exchange rate and real commodity prices for emerging market economies. Resour Policy 76:102586

Yosthongngam S, Tansuchat R, Yamaka W (2022) Volatility spillovers between ethanol and corn prices: a Bayesian analysis. Energy Rep 8:1030–1037

Yousaf I, Yarovaya L (2022) The relationship between trading volume, volatility and returns of Non-Fungible Tokens: evidence from a quantile approach. Financ Res Lett 50:103175

Zhang H, Hong H, Guo Y, Yang C (2022) Information spillover effects from media coverage to the crude oil, gold, and Bitcoin markets during the COVID-19 pandemic: evidence from the time and frequency domains. Int Rev Econ Finance 78:267–285

Zhang D, Hu M, Ji Q (2020) Financial markets under the global pandemic of COVID-19. Financ Res Lett 36:101528

Zhang N, Wang A, Ul-haq N, Nosheen S (2021) The impact of COVID-19 shocks on the volatility of stock markets in technologically advanced countries. Economic Research-Ekonomska Istrazivanja. https://doi.org/10.1080/1331677X.2021.1936112

Zhou W, Chen Y, Chen J (2022) Risk spread in multiple energy markets: extreme volatility spillover network analysis before and during the COVID-19 pandemic. Energy 256:124580

Zivkov D, Gajic-Glamoclija M, Duraskovic J (2022) Volatility spillover analysis between stocks and exchange rate markets in short and long terms in East European and Eurasian countries. Int J Emerg Mark. https://doi.org/10.1108/IJOEM-01-2021-0082

Acknowledgements

The authors have no acknowledgements to offer.

Funding

No funding was provided for the research.

Author information

Authors and Affiliations

Contributions

IA contributed to writing the literature review and methods section whilst also perform the DDC analysis of the empirical section. AP wrote the introduction and parts of the method and also performed the wavelet coherence analysis. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare that they have no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Additional file 1.

African equities, foreign exchange and cryptocurrencies 2020–2022 daily data.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Anyikwa, I., Phiri, A. Connectedness and spillover between African equity, commodity, foreign exchange and cryptocurrency markets during the COVID-19 and Russia-Ukraine conflict. Futur Bus J 9, 48 (2023). https://doi.org/10.1186/s43093-023-00227-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s43093-023-00227-y