Abstract

The basic aim of this paper is to systematically review the corporate governance research trends in Pakistan and to give directions for future researchers in this field. The methodology adopted in this paper is “Systematic Literature Review,” 108 papers have been used from the period 2002–2020 along with 17 research theses in this study. The findings of this study show two trends in corporate governance research first one form 2008 to 2016 and the second one is from 2017 to 2020. The first trend shows that corporate governance (variables) is linked with traditional topics such as firm performance, dividend policy, capital structure, cost of capital and earnings management. The theory which is mostly used in the first corporate governance trend is the agency theory. In the second trend, corporate governance (variables) are linked with multiple issues while taking various theoretical perspectives such as risk taking, tunneling, CSR, investment portfolios, board-related issues, financial distress and much more. This paper has identified and filled the research gap by writing a comprehensive review paper of the prevailing corporate governance literature and has given directions for future researchers to consider it. To the best of researchers’ knowledge, this is the first study that has systematically reviewed and synthesized the corporate governance literature by adopting the systematic literature review methodology in Pakistan an emerging economy. It is an extensive effort for the purpose to encourage the interested researchers/scholars to add and expand their contributions to the corporate governance literature in Pakistan on the potentially identified areas of corporate governance.

Similar content being viewed by others

Introduction

The basic aim of this study is to review, synthesize, assess and integrate the existing knowledge of Corporate Governance (hereafter, CG) and related topics in the Pakistani context, to examine the research trends in CG-related studies and issues in Pakistan, since the implementation of first Corporate Governance Code (hereafter, CCG) in 2002 and to give future research directions for potential researchers. The East Asian Financial Crisis 1997 and the famous Enron Scandal 2001 focused the academia, regulators and policymakers to improve governance structure in the companies and brought to light the importance of an effective institutional framework. According to Zitouni [158] since 1992 of the “Cadbury’s Report,” more than 400 CG codes have been published in different countries worldwide with different standards, principles and suggestions to effectively regulate the CG practices. Therefore, in order to improve the firm governance, board oversight and cope with international trends the Securities and Exchange Commission of Pakistan (hereafter, SECP) implemented the CCG 2002 to strengthen the board and audit committee functions, improve disclosure in the shape of the internal and external audit function and other good governance measures in line with international standards necessary for corporations.

Since the incorporation and promulgation of the CCG in 2002 in Pakistan, a new trend of research started in Pakistan and many researchers in Pakistan researched the topic of CG-related variables with firm financial performance [14, 20, 38, 47, 71, 78, 82, 94, 121, 124, 147, 148, 153], firm value [49, 90, 92, 104, 112, 135, 138, 150, 155], cost of capital [54, 61, 62, 64, 102, 122, 137], investment efficiency [129], cash holding [25, 77, 116, 146], related party transactions [34],56, 57, 141–145, accounting conservatism [111], disclosure and audit quality [102, 105, 111, 140], earnings quality [90, 92, 119], dividend policy [20, 23, 30, 32, 44, 88, 109, 123], risk taking [15, 35, 55, 97, 98, 143,144,145], corporate social responsibility [29, 51, 112] and earnings management [19, 42, 47, 61, 63, 65, 66, 73, 89, 100, 101, 107, 113, 122, 149].

The review of the above study shows that most of the studies are empirical in nature targeting specific variables, theories and utilizing various sources of data, in addition to this, there is a lack of review-based paper on CG in the Pakistani context, consequently, there was a need to make a comprehensive analysis of CG-related studies with different theories and variables. Therefore, the objectives of this study are to assess and consolidate the extant research about CG and related topics in Pakistan, to examine the research trends in the CG-related studies and issues from 2002 to 2020 in Pakistan, and provide guidance for future researchers to pursue new areas in CG related to Pakistan. In order to achieve the objectives of the study, we have gone through the review of Pakistani academic Journals recognized by the Higher Education Commission (hereafter, HEC) for the period of 2002 to 2020Footnote 1 as well as internationally published research work via a systematic literature review approach. The scope of this review paper is the studies related to CG and related topics published within Pakistani journals or international journals outside Pakistan which can be found in google scholar a bibliographic database and the largest academic articles database [8]. Moreover, CG is a very broad and a comprehensive discipline; therefore, this review study specifically focuses on those topics related to CG such as ownership structure, board structure, audit structure, CEO and board of directors’ roles & functions, CEO & board of directors’ features and family ownership, in addition to this, family business groups, business groups affiliation and earnings management-related studies are also included which may be linked with various types of dependent(predicated) variables. Moreover, the time period for this study is ranging from 2002 to 2020.Footnote 2 The reason for choosing this time period is the promulgation of the first code of corporate governance in Pakistan, furthermore, CG research gained its momentum in Pakistan after the implementation of CCG 2002 in Pakistan.

The findings of this study show two trends of CG research, one starts from the period of 2008 to 2016, and the second is from 2017 to 2020. The first trend of CG research shows that a large portion of the studies has linked CG with firm performance, dividend policy, cost of capital, capital structure and earnings manipulation. In addition to this, most of the studies in the first CG research trend have employed a small sample size, utilized the secondary sources of the data and researched under one specific theory which is in most cases agency theory. However, in the second CG research trend which is ranging for the period of 2017 to 2020 shows that CG is linked with multiple issues such as risk taking, tunneling, CSR, investment portfolios, board-related issues, financial distress, investment efficiency and much more. Moreover, the findings show that most of the studies are empirical in nature and utilize a secondary source of data and represent the study under different CG and finance-related theories. Furthermore, in this period the studies have used larger sample as compared to the first trend, additionally, the studies of this research trend show a specific element of CG such as the board of directors, CEO characteristics, specific ownership type, pyramidal ownership, and some other variables such as affiliation with group or bank, product market competition, disclosure and political connection are linked with CG and other related variables.

This review paper contributes to the CG literature particularly in Pakistan, in the following ways. Firstly, our review paper contributed systematically a comprehensive review on CG, by organizing, integrating and analyzing a body of dispersed CG work on Pakistani context. More specifically, in this review paper 125 studies have been analyzed, and then categorized them into four board research themes of CG. Secondly, this study has pointed out the focus on previous research of CG in terms of ownership structure, board structure and other related CG elements. Thirdly, to the best of our knowledge, this review is the first systematic literature review paper on CG in the Pakistani context, it is an extensive effort for the purpose to encourage the interested researchers/scholars to add and expand their contributions to the CG literature in Pakistan on the potentially identified areas of CG as identified and pointed out in “Future prospects” section in this research study. Lastly, this study not only integrated and extended the extant research on CG but offers future directions in the key identified areas of CG research to the potential CG scholars.

The scheme of the study is as follows, section 2 presents “The historical view of different corporate governance codes in Pakistan” of different corporate governance codes in Pakistan, research methods and systematic literature review steps are mentioned in section 3 “Research methods”, and results are presented in “Results and findings of the selected studies” section 4. In section 5 “Discussion”, of the study is made while this study is concluded on the future prospectus and conclusion.

The historical view of different corporate governance codes in Pakistan

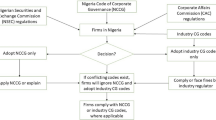

The corporate sector of Pakistan consists of financial and non-financial institutions. These institutions are regulated by the State Bank of Pakistan (SBP), and Securities Exchange Commission of Pakistan (SECP). Financial institutions such as commercial banks, microfinance banks and development finance institutions are regulated by SBP while all non-financial institutions are regulated by SECP with a listing requirements in PSX. The first code of corporate governance (henceforth, CCG) was implemented in 2002 in Pakistan. The 2002 CCG was based and formulated on the examples of different codes throughout the world [56]. In this code, it was encouraged to have an independent director in the listed companies, it made compulsory to have training programs for directors, have guidelines for the establishment of an audit committee and the Chief Executive Officer & chairman could be the same persons. The 2002 CCG has no clause of female and expert directors in the board of directors or board’s committees. After a decade of implementation, the 2002 CCG was revised in 2012 by implementing more demanding clauses regarding the board of directors, board committees and compliance clauses.

In the CCG 2012, it is made mandatory that there must be at least one independent director in the board, while in the CCG 2002 it is suggested to be one in the board. In addition to this, it is preferred in the CCG 2012 to have 1/3 of independent directors in the board. Moreover, the independence of the directors in the board is further elaborated in the 2012 CCG as compared to the 2002 CCG. The number of multiple directorships at a time was restricted to 7 companies in the CCG 2012; furthermore, the duality of CEO & chairman is withdrawn. The independence of the Audit Committee was introduced in the CCG 2012 which was not given in the 2002 CCG; furthermore, it was also included that the board chairman and audit committee chairman should not be the same person. The 2012 code does not include any clause on gender diversity and board expertise while on the other hand in addition to the audit committee, the Remuneration and Human Resource Committee were introduced in the CCG 2012 and made this code is a listing requirement in the PSX in the same manner as the previous CCG 2002.

Due to some limitations such as lack of board diversity and expertise, and in order to cope with international trends and practices, SECP revised the 2012 CCG at the end of 2017. It includes the mandatory inclusion of female directors in the board and expertise members in the audit committee as well as reduced the multiple directorships from 7 to 5 companies. The gender diversity, expertise and increase independence in the board were included due to the international trends and practices. Moreover, before the implementation of CCG 2017, there were many legal law precedents of other countries regarding gender diversity to be included in the board such as in Norway gender diversity is 40% along with Sweden 23% in the board. Moreover, there were examples of India, Kenya and Malaysia who directly intervene to address gender diversity and other board issues in the CG codes. In addition to this, at that time when the CCG 2017 was implemented in Pakistan, there was only 6 percent female directors in the listed firms which were far below in the National Assembly of Pakistan (Parliament) proportion which stood at 17 percent, women participation in the labor force in Pakistan which was 15.8% and was below than the proportion of S&P 500 and FTSE 100 companies which are 20 to 25 percent.Footnote 3

Therefore, keeping the above trends and precedents the SECP included the mandatory inclusion of female directors in the board in order to achieve at least 15% female representation in the board unto 2020. Furthermore, financially expertise members in the audit committee as well as one mandatory independent director in the AC who should be chairman of the AC are also included in the CCG 2017 following the Sarbanes Oxley Act (2002). In addition to this, it reduced the executive directors to 1/3 of the board of directors; furthermore, it improves the board independence by including the clause “not less than two members or one-third of the total members” should be independent in the board.Footnote 4

Research methods

Data period and data sources

The methodology adopted in this paper is “Systematic Literature Review.” This methodology has been conducted on the selected papers for the period of 2002–2020 in order to achieve the objectives of the study. The rationale for selecting 2002 is the starting year of CG in Pakistan, and a new trend of research had started among the Pakistani researchers to research CG-related variables with different variables. The data source for this study is “HEC Recognized National Research Journals of Management Sciences & Economics,”Footnote 5 HEC Research Repository and Google Scholar for the period of 2002 to 2020. In the HEC recognized journals list 12 are X-category Journals, 16 are Y-category Journals and 7 are Z-category Journal.

Research strategy

The methodology used in this study is “Systematic Literature Review.” In order to search the concerned topics in the HEC recognized Journals, HEC Research Repository and Google Scholar keywords strategy is implemented, a different combination of keywords has been used, those keywords were in the combination of dependent and independent variables, the details of those keywords are given in Table 1. After the review and investigation of 150 volumes of X-Category journals, 159 volumes of Y-Category journals and 19 volumes of Z-Category journals 93 papers were selected for the purpose of this study. Moreover, in the HEC Research Repository, 17 theses were also selected to evaluate it, and lastly, keywords combination research was carried out in Google Scholar up-to 10 pages for every keyword combination and resulted15 papers.

Systematic literature review steps

Step No. 1

In the first step of systematic literature review, we search the related literature with the combination of our selected keywords in our data sources such as “HEC Recognized National Research Journals of Management Sciences & Economics,” HEC Research Repository and the Google Scholar. In the first stage, the HEC X-Category journals were targeted, with the detail review of 150 volumes 39 papers were extracted from the 12 recognized journals. In the second stage, the HEC Y-Category journals were focused, after the review of 159 volumes in the 16 recognized journals 47 papers were chosen to include in this study. In the third stage, the HEC Z-Category journals were selected, 6 related papers were taken from the 7 recognized journals and 19 volumes were analyzed for this purpose. The details of the Journals and papers selected from it is presented in Table 2. In the last stage, in order to review the published theses (Ph.D.) HEC Research Repository has opted. After searching under different keywords in the repository, 17 relevant theses were taken into consideration.

Step No. 2

In the second step of the systematic literature review, Google Scholar has been utilized for searching the keywords combination. The Google Scholar is one of the key bibliographic databases [103] which the researchers used to check their thematic novelty on it, others databases are Web of Science and Scopus. We have chosen Google Scholar due to our access to it, the Web of Science and Scopus are inaccessible to us. We search out our keywords combination on Google Scholar and after each keyword research, we have search 10 pages on it. In this way, 76 research articles were found.

Step No. 3

In the third step of the systematic literature review, the research article selected in step 1 and step 2 were taken to eliminate the same and duplicate articles. The Google Scholar articles which were 76 initially was brought down to 15 articles and the eliminated articles were already scrutinized during the “HEC Recognized Journals lists” review. The selected articles from Google Scholar and the journals details are given in Table 3.

Step No.4.

In the fourth step of the systematic literature review, 108 research articles and 17 theses were thoroughly analyzed in order to extract information concerning of the author and study year, dependent variable, independent variable, sample size and population, data period, major findings of the study and theory (s) used in the concerned study or theses (Ph.D.).

The steps no 5 and 6 are carried out in the next two sections.

Results and findings of the selected studies

The results of the selected papers extracted from 38 journals have been shown in the following pages, among them 24 were Pakistani Journals and 14 were international journals. The analysis of the selected papers shows that CG-related variables are linked mostly with firm financial performance, firm value, cost of capital, dividend policy, risk taking and earnings management. In Table 4, which shows the X-Category Journals shows the results of 39 papers from 2009 to 2020. Table 4 shows that 13 out of 39 papers were linked with firm performance or firm value, 6 papers are between earnings management and CG, 3 papers show the relationship of CG with capital Structure, 2 papers are on the of dividend policy and similarly of cash holdings. The analysis of these studies shows that the majority studies used the Agency Theory in their theoretical framework and the data period is ranging for the period of 2002 to 2017.

In Table 5, the results of 47 papers of Y-Category Journals are given from 2008 to 2020. In these studies, 4 studies are linked with earnings management, 12 are linked with firm performance, and 6 studies are linked with dividend policy. The cost of capital is linked in 4 paper with CG. In addition to this, 5 papers are linking risk taking with CG, and some papers are linking CG with working capital management, corporate tax avoidance, corporate social responsibility and unexpected stock returns. Moreover, agency theory is used in most of the studies in order to check its relationship with other variables.

In Table 6, the results of Z-Category Journals are given which shows the findings of 6 studies from 2013 to 2019. In these studies, two studies show the findings of firm performance with CG-related variables, two studies are linking dividend policy with CG. In addition to this, two studies are linking CG with the market rate of returns and financial distress. Moreover, agency theory is used in most of the studies in order to check its relationship with other variables.

The results of the HEC Research Repository are depicted in Table 7, in this Table 17 theses are evaluated in order to achieve the objective of this study. The findings show that most of the theses used the CG theories in the Pakistani context such as agency theory, stakeholder theory, stewardship theory and some dividend policy-related theories. The time period of these theses is from 2009 to 2019. Most of the studies linked CG-related variables with firm performance, cash holdings, earnings management, cost of capital, capital structure, CSR, financial decision and investment efficiency. In addition to CG variables, group affiliation variable is linked in a few studies such as tunneling and related party transitions. Similar to the above discussion in these theses, most of the theses have linked CG with firm financial performance and firm value.

In addition to HEC recognized journals and HEC Research Repository, the third source which is utilized in this study is Google Scholar. In Table 8, fifteen selected papers is given which is included after the elimination and deletion of similar studies. The studies period is from 2009 to 2020. In these studies, the dependent and independent variables are quite different as compared to the previous tables. Here in these tables CG, group affiliation, EM and political connections variables are used as independent variables which are not evident in the other tables as shown in the study.

The results and presentation of the selected studies is given in the above mentioned tables, these tables include author and study period, dependent and independent variables, sample and data period, key findings of the studies(theses) and in the last column, the theory which is used in the study is given.

Discussion

The objectives of this paper are to assess and consolidate the extant research about CG and related topics in Pakistan, and to examine the research trends in the CG-related studies and issues from 2002 to 2020 in Pakistan. So in order to achieve the objectives of the study, this review paper starts with the HEC recognized Pakistani Journals at the first stage and we have reviewed 35 Journals, from these journals the related paper has been extracted these are mentioned in Table 2, in the second stage Google Scholar a bibliographic database and largest academic articles database [8] searches out to find and analyze the related studies, this result 15 related studies starting from 2009 to 2020 in the 14 international journals. Moreover, the first decade of twenty first century in Pakistan is the decade of establishing and launching different management sciences and social sciences journals, the first study was traced back to 2008 in which [16] linked CG characteristics with capital structure decisions. This indicates that Pakistani research journals were starting operating and promoting research in business, finance and other social sciences fields. In addition to this, the second decade of the twenty first century is the decade of budding the CG and related topics research in the Pakistani journals.

Features of the reviewed papers

In this study, a set of 108 research papers and 17 theses has been reviewed. The descriptive details of articles reviewed are given in Table 9, the most articles have been picked up from Y-category journals while less are taken from Z-category journals. The analysis of this review shows that the majority of the study has empirical in nature except for five studies which are literature reviews or qualitative studies [26, 42, 74, 98, 132]. Most of the studies targeting non-financial firms of PSX, utilized a secondary source of data and using agency theory. In addition to this, the sample size of the most of the studies are too small ranging from 10 to 170 listed financial and non-financial firms of PSX. Moreover, 42 articles have used only one theory, 12 articles/theses have been used two theories while 14 articles/theses have been used more than two theories. Additionally, 58 articles/theses did not apply or mention any theory while 52 articles/theses used the agency theory, 3 articles/theses have been used resource dependence theory, 3 articles/theses have been used Stakeholder and 3 articles/theses have been used Stewardship theory. Furthermore, we have made the analysis of the findings, from this analysis different CG themes and subthemes have been emerged. The details of CG themes and subthemes are given in the following paragraphs.

Corporate governance and related studies

The CG (aggregate) is the first major and most used theme in this study. The CG is linked with 65 studies with diverse types of dependent variables in this review study. The researcher has used CG as an aggregate of ownership structure and board structure proxies. Moreover, the researcher in the Pakistani context linked CG with firm performance in 22 studies but the findings are inconclusive [20, 70, 82, 124], with EM in 13 studies [19, 65, 66, 73, 107, 122], with firm risk in 5 studies [35, 98, 136, 143,144,145], with Cash Holding in 4 studies, [24, 25, 116], with CSR in 3 studies [46, 51, 110] and with other topics in 18 studies [16, 26, 31, 36, 71, 79, 99, 108, 115].

Ownership structure and related studies

The ownership structure is one of the important elements of CG. Pakistan is famous for its concentrated ownership structure. The majority of the firms in Pakistan are family owned and have concentrated ownership [17, 58]. The second theme which is generated from this review paper is ownership structure. The findings of this review show that ownership structure-related studies mainly revolves around the firm performance mainly financial performance [45, 68, 70, 78, 147, 148, 150]. In addition to this, some studies link ownership structure with EM [37, 73, 110], dividend policy [18, 33, 80, 88, 109, 127], cash holdings [77] and other related topics [41, 52, 55, 87, 125, 128, 135]. Ownership themes that emerged from this review paper are family ownership, excess ownership, institutional ownership and managerial/director ownership.

Board structure and board characteristics

The highest decision making and supervisory body in the companies’ management hierarchy is the board of directors, and it is one of the most important element of CG for monitoring and supervision the management. In this review paper, 18 studies have been related to board structure and board of directors’ characteristics. The findings show that four studies linked board-related variables with dividend policy [18, 23, 33, 127] & five studies with firm performance [21, 27, 93, 106, 126] while three studies linked it with EM [119, 149, 160]. Moreover, other studies linked it with cash holding, financial distress, working capital, CSR and Banks efficiency etc. [29, 97, 114, 133, 146, 154]. Moreover, from this review paper following subthemes of board of directors such as CEO Duality, Gender diversity, Executive Compensation, Board Composition, Audit Committee and, Board of directors &CEO characteristics have been emerged.

The controlling shareholders and pyramidal ownership

In addition to the abovementioned themes of CG, the findings of this study show that, the following additional themes are also emerged such as controlling shareholders and pyramidal ownership (business groups’ affiliations). In the 13 studies, the controlling shareholders’ ownership and pyramidal ownership have been linked with firm performance [17, 48, 147, 148, 152], tunneling [56, 57, 141], earnings manipulations [37], dividend policy[44], related party transactions [141, 143,144,145], capital structure[95] and cash holding [85, 86]. Moreover, the findings of the studies show that controlling shareholders’ relationship with firm performance is inclusive and mixed [17, 151]. Moreover, Hussain [56] added that in concentrated firms there are a huge amount of related party transactions. In addition to this, Bhutta et al. [37] reported that pyramidal ownership is positively related to EM while [95] added that 85 percent of pyramidal ownership firms used debt to run business in Pakistan.

Theoretical underpinning and linked theories

The findings of this study show that there are several theories have been used in the field of CG with related dependent variables. The most used theory during the period of 2002–2020 is the agency theory, which is used in 65% of this review study. Agency theory has been adopted in 52 studies which are quantitative in nature, linking it with firm performance [28, 47, 67, 94, 118, 130, 138] typically the researcher tried to link it with confit of interest hypothesis which arises due to separation of ownership and control [43, 72]. Additionally, the agency theory has been applied to the topics of earnings management [19, 42, 63, 73, 75, 89, 107] and financial reporting quality [119, 129] to check the board of directors monitoring and controlling role over the companies’ management. Moreover, the researchers have also linked the agency theory with dividend policy and related party transactions [32, 37, 56, 109, 127] to check it with Type II Agency Problem in the concentrated ownership firms. In addition to this, some research studies have linked agency theory with cost of equity and cash holdings [24, 25, 50, 137]. Moreover, in 2008 to 2016 period most of the studies have used either agency theory or did not explicitly apply any theory or their theoretical framework in their studies. Additionally, about 10% (8) studies have used packing order theory [98, 122], trade off theory [109, 122], stakeholder theory [25, 135, 138], and stewardship theory [101] along with agency theory.

Furthermore, in the period of 2008 to 2016, the literature relied mostly on agency theory, then on other theories such as trade off theory, stakeholder theory and stewardship theory. However, in the last four years of this review study data period, a significant number of theories have been applied by the researchers in the literature. Moreover, the most used theory from the period of 2017 to 2020 is agency theory about 39% (31) researchers have used the agency theory perspective in their studies [20, 36, 44, 54, 126, 147, 148] linking with firm financial performance, earnings manipulation, cost of equity and cash holding, etc., In addition to this, a combination of agency and other theory such as stewardship theory, upper echelon theory, stakeholder theory, resource dependence theory, signaling theory and other theories have been applied in 12 quantitative studies, which count about 15 percent of total studies. Furthermore, a resource dependence theory is applied with agency theory in the study of [146], to examine that board is an effective resource in handling corporate cash holdings, the stewardship theory is linked along with agency theory on EM [63, 90, 92]. In addition to this, the upper echelon theory is used along with agency theory and contingency theory to check the features of top female directors/management on firm performance & risk taking [97]; moreover, information asymmetry theory is used along with agency theory to link it with dividend smoothing [23]. Additionally, the studies of [29, 62, 90, 92] have used stakeholder theory along with agency theory in different research perspectives such as CSR, earnings quality and earnings manipulation. Also, there are a limited number of studies that have used other theories such as positive accounting theory [91], gender socialization theory [149], socioeconomic wealth [129] and signaling theory [61]. However, during the period of 2017 to 2020, there are 27 studies which are about 34 percent of the total studies, did not have any explicit and clear theoretical framework or theory used in their studies.

The Corporate Governance Research Trends in Pakistan

The findings of this study show two research trends of CG in Pakistan, one is from 2008 to 2016 and the second is from 2017 to 2020. The first CG research trend which is from the period of 2008 to 2016 focuses on the studies which have linked CG with firm performance, dividend policy, cost of capital, capital structure and earnings manipulation. In addition to this, in terms of the research design, most of the studies have employed the quantitative research design and tested the relationship among different variables empirically. Moreover, most of the studies utilized the secondary sources of the data and most often have very small sample size of both financial and non-financial companies of PSX. In terms of theory used in a particular paper or thesis majority of the studies carried out their research under one specific theory which is in most of the cases the agency theory. Surprisingly, the findings of this review study also reported that 31 studies in the first trend of CG in Pakistan which is ranging from 2008 to 2016 did not explicitly adopt any theoretical framework to carry out their research objectives. Additionally, two studies [26, 98] are qualitative in nature the former is a literature review paper focusing on CG issues in Pakistan and the latter is a systematic review linking CG with firm risk in financial institutions.

The second research trend of CG which is ranging from the period of 2017 to 2020.This research trend is more advance in terms of theories used, research methodology employed, sample size handled and CG issues tackled. The findings of this review show that in the second CG research trends the topic of CG is linked with multiple burning and contemporary issues such as risk taking, tunneling, CSR, investment portfolios, board-related issues, financial distress, investment efficiency and much more as compared to the first CG research trend in which the traditionally typical topics have been empirically investigated. Moreover, the findings show that most of the studies are empirical in nature, utilizing a secondary source of data and representing the study under different CG and finance-related theories. However, there are two studies that are qualitative in nature, in one study CG is linked with firm performance and the authors[74] provided a descriptive evidence on that in a detail literature review manner; moreover, [132] made an attempt via a qualitative data analysis method that how political connections may help the financing strategies of companies’ to build enterprise. In addition to this, the sample period of the second research trend is richer and representative in both financial and non-financial firms as compared to the first CG research trend. Furthermore, the studies in of the recent past show specific elements of CG such as the board of directors, CEO characteristics, gender diversity, specific ownership type, pyramidal ownership, and some other variables such as affiliation with group or bank, product market competition, disclosure and political connection, etc.

Future prospects

The findings of this study show that aggregate CG is linked and tested with diverse topics, but there is a lack of research related to CG and its impact on Research & Development, Innovation, Marketing strategies, Operational efficiency, Institutional shareholders investment and CG characteristics in family owned and non-family owned businesses. Furthermore, as we know that ownership structure is one of the most important element of CG, ownership structure determines the agency problem, the review of this paper shows that agency problem has not been clearly investigated in the Pakistani context which is famous for family owned businesses and ownership concentrations. Therefore, agency problems especially the Type II Agency Problem must be tackled by the future researchers. Moreover, as we have documented that a bundle of studies in this paper linked CG with firm performance (financial performance) and non-financial performance and corporate social performance is missing in the literature so future studies should focus on this issue too. Additionally, there are State Owned Enterprises (hereafter, SOEs) in Pakistan, and research on it is quite limited; therefore, future researchers may focus on SOEs performance, its governance issues, the role of political connections & CG in SOEs and the impact of SOEs on economy and society. In addition to this, the board of directors is also one of the important element of CG, as we have shown that board characteristics is mostly linked with firm performance and EM examining the monitoring role of the board of directors; however, studies on the advisory role of the board is missing; therefore, future researchers may consider it to address this empirical gap. Moreover, future studies may investigate the questions such as that how the board of directors affects corporate decisions, what are their roles in different types of organizations especially in family and public sectors organizations and what is the impact of independent, and more diverse boards on firm social and non-financial performance. Moreover, future researchers may focus on the issues of executive compensations especially CEO’s, CSR and qualitative research focusing on CG and related variables. Furthermore, as discussed in the previous section that most of the articles have not applied any theoretical framework, thus future scholars are advised through this research study to link-related theories in their research questions to increase the quality of their research. Additionally, the agency issues in concentrated and pyramidal ownership firms is unexplored future researchers may implement research agenda on this side as well. Moreover, the future discussion may be for the future scholars to study the published papers other than two streams, financial and non-financial as well as the multidimensional study and the study of the CG variables meta-analysis with a large sample can be a strong contribution and impact. Finally, future researchers if wanted to write a review paper may consider other Citation databases such as Web of Science, JSTOR, SCOPUS and Science Direct.Footnote 6

Conclusion

The objectives of the study were to research the trends of CG in Pakistan after the promulgation of CCG in Pakistan, to accumulate, consolidate and analyze a stock of CG-related research and give potential CG researchers pathways for future research on CG and associated topics. A systematic literature review approach is adopted in order to achieve the objectives of the study. After a thorough review of 328 volumes of HEC recognized social sciences journals, 93 papers were extracted covering the topics of firm performance, dividend policy, cost of capital and capital structure and earnings manipulation in most of the papers. Moreover, 15 research articles were extracted from the international journals via researching through google scholar, in addition to these research articles, 17 research theses have been analyzed in this review paper downloaded from the HEC Research Repository. In this review paper, 108 research articles have been analyzed consisting of 104 empirical studies, on diverse CG topics from 24 local HEC recognized journals and 14 international journals. The findings of this study show that one article is a systematic review, three articles were non-empirical (descriptive) and 104 were empirical papers along with 17 Ph.D. research theses. In addition to this, this review study has explored various theories that have been applied with agency theory is the most used theoretical framework. Furthermore, through the analysis of this paper four board themes of related to CG has been identified, such as aggregate CG, ownership structure variables, board structure variables and the controlling and pyramidal ownerships. Moreover, through this review paper, two CG research trends have been identified and discussed. The first research trend of CG shows that from 2008–2016 mostly papers link CG with firm performance, dividend policy, cost of capital, capital structure and earnings manipulation; however, in the second research trend which is ranging from 2017 to 2020 shows some emerging issues such as the characteristics of board of directors, ownership structure types more specifically family ownership and issues related with the separation of ownership and control, board diversity, CEO characteristics, client importance in family businesses, CSR, financial distress and much more. Moreover, the findings of this review paper reported that the most used theory in CG research trends is agency theory which is about 65 percent of total reviewed studies; additionally, the other most used theory is resource dependence theory, stakeholder theory and stewardship. By achieving the objectives of this systematic review study, it has contributed a comprehensive CG knowledge to existing CG literature focusing on Pakistan by filling the identified gap of this study.

Limitation of the study

This review paper synthesized systematically a stock of CG-related studies to provide opportunities for research scholars, policymakers and practitioners to get benefit from it. Similarly, like other studies, this review paper has some limitations. Firstly, the keywords used in this review paper are limited due to the scope of the study. Secondly, the time period of this research study is from 2002 to 2020, which may be a potential limitation that needs to be addressed by the future researchers. Thirdly, we have used only google scholar a bibliographic database and the largest academic articles database [8] to search the CG-related papers focusing on the Pakistani context, while the world renowned academic articles databases such as Web of Science, SCOPUS and Science Direct are skipped in this research study due to the accessibility issues.

Availability of data and materials

We have used secondary sources to complete our study. No new data are used or produced in this study.

Notes

This study will review the Journals up-to July 2020, because all new issue will appear online by the end of June or in the mid of July whether the Journal is bi-annually or quarterly.

In addition to footnote 1, the HEC abolished all the X, Y and Z category Journals related to business and economics into one Y-Category under HJRS, there is why the scope of this study is unto July 2020.

The SECP implemented Fourth Code of Corporate Governance in 2019 based on the “Comply and Explain” Principles which has Mandatory, Recommendatory and Comply and Explain Provision. https://www.secp.gov.pk/document/listed-companies-code-of-corporate-governance-regulations-2019/.

“HEC Recognized National Research Journals of Management Sciences & Economics” on May 04, 2020.

For more future research directions the scholars may get help from the studies as we have reported under the heading of Further Readings.

Abbreviations

- CG:

-

Corporate Governance

- CCG:

-

Corporate Governance Code

- SECP:

-

Securities and Exchange Commission of Pakistan

- HEC:

-

Higher Education Commission

- CEO:

-

Chief Executive Officer

- CSR:

-

Corporate Social Responsibility

- SBP:

-

State Bank of Pakistan

- PSX:

-

Pakistan Stock Exchange

- EM:

-

Earnings management

References

Further Readings

Akram M, Ghosh K, Sharma D (2021) A systematic review of innovation in family firms and future research agenda. Int J Emerg Mark. https://doi.org/10.1016/j.ibusrev.2021.101924

Post C, Byron K (2015) Women on boards and firm financial performance: a meta-analysis. Acad Manag J 58(5):1546–1571

Alhossini MA, Ntim CG, Zalata AM (2021) Corporate board committees and corporate outcomes: an international systematic literature review and agenda for future research. Int J Account 56(1):1–73. https://doi.org/10.1142/S1094406021500013

Azila-Gbettor EM, Honyenuga BQ, Berent-Braun MM, Kil A (2018) Structural aspects of corporate governance and family firm performance: a systematic review. J Family Bus Manage 8(3):306–330. https://doi.org/10.1108/JFBM-12-2017-0045

Cucari N (2019) Qualitative comparative analysis in corporate governance research: a systematic literature review of applications. Corp Govern 19(4):717–734. https://doi.org/10.1108/CG-04-2018-0161

Darouichi A, Kunisch S, Menz M, Cannella AA (2021) CEO tenure: an integrative review and pathways for future research. Corp Govern Int Rev 29(6):661–683. https://doi.org/10.1111/corg.12396

E-Vahdati S, Zulkifli N, Zakaria Z (2019) Corporate governance integration with sustainability: a systematic literature review. Corp Govern 19(2):255–269. https://doi.org/10.1108/CG-03-2018-0111

Farah B, Elias R, Aguilera R, Abi Saad E (2021) Corporate governance in the Middle East and North Africa: a systematic review of current trends and opportunities for future research. Corp Govern Int Rev 29(6):630–660. https://doi.org/10.1111/corg.12377

Geyer-Klingeberg J, Hang M, Rathgeber A (2020) Meta-analysis in finance research: opportunities, challenges, and contemporary applications. Int Rev Financ Anal 71:101524. https://doi.org/10.1016/j.irfa.2020.101524

Khatib SFA, Abdullah DF, Elamer AA, Abueid R (2021) Nudging toward diversity in the boardroom: a systematic literature review of board diversity of financial institutions. Bus Strateg Environ 30(2):985–1002. https://doi.org/10.1002/bse.2665

Kutan A, Laique U, Qureshi F, Rehman IU, Shahzad F (2020) A survey on national culture and coraporate financial decisions: current status and future research. Int J Emerg Mark. https://doi.org/10.1108/IJOEM-12-2019-1050

Nguyen THH, Ntim CG, Malagila JK (2020) Women on corporate boards and corporate financial and non-financial performance: a systematic literature review and future research agenda. Int Rev Financ Anal 71:101554. https://doi.org/10.1016/j.irfa.2020.101554

Abbas M, Aslam MA, Naheed K, Aamir M (2019) Interrelationship among corporate governance, working capital management, and firm performance: panel study from Pakistan. Paradigms 13(1):75–82. https://doi.org/10.24312/1800064130112

Abdullah F, Shah A, Khan SU (2012) Firm performance and the nature of agency problems in insiders-controlled firms: Evidence from Pakistan. Pak Dev Rev 4(51):161–182. https://doi.org/10.30541/v51i4iipp.161-183

Khan MI, Khan SI (2018) Impact of ownership structure and firm size on the operational risk management of Islamic banks in Pakistan. J Bus Tour 04(01):209–217

Ahmad I (2008) Corporate governance and capital structure decisions of the Pakistan listed textile firms. NUML Int J Bus Manage 2(2):14–22

Ahmad I, Oláh J, Popp J, Máté D (2018) Does business group affiliation matter for superior performance? Evidence from Pakistan. Sustainability (MDPI) 10(9):1–19. https://doi.org/10.3390/su10093060

Ahmad MN, Khan MN, Ullah F, Khan Y (2019) Board composition, ownership structure and dividend payout policy: evidence from PSX-100 index of Pakistan. J Bus Tour 05(01):55–73

Ahmad S, Khan AS, Zahid M (2020) The impact of corporate governance on earnings management: the case of Pakistan textile industry. J Bus Tour 06(01):71–87

Akbar M, Hussain S, Ahmad T, Hassan S (2019) Corporate governance and firm performance in Pakistan: dynamic panel estimation. Abasyn J Soc Sci 12(2):213–230. https://doi.org/10.34091/ajss.12.2.02

Ali A, Nasir SB (2015) Impact of board characteristics and audit committee on financial performance: a study of manufacturing sector of pakistan. IBA Bus Rev 10(1):147–166

Ali B, Shah S (2017) The impact of corporate governance on working capital management efficiency: a quantitative study based on Pakistani manufacturing firms. City Univ Res J 07(2):272–284

Ali Z, Ullah A, Ali A (2019) Board structure and dividend smoothing: a case of Pakistani listed firms. Bus Rev 14(2):65–91

Alim W, Khan SU (2016) Corporate governance and cash holdings: evidence from family controlled and non-family business in Pakistan. Pak J Appl Econ, pp 27–41

Alina Masood AS (2014) Corporate governance and cash holdings in listed non-financial firms in Pakistn. Bus Rev 9(2):74–97

Ameer B (2013) Corporate governance-issues and challenges in Pakistan. Int J Acad Res Bus Soc Sci 3(4):79–96

Amin I, Iftikhar N, Yasir M (2013) Board composition, CEO duality and corporate financial performance. Bus Econ Rev 5(1):13–28. https://doi.org/10.22547/ber/5.1.2

Ashfaq S, Kayani GM, Saeed MA (2017) The impact of corporate governance index and earnings management on firms’ performance: a comparative study on the islamic versus conventional financial institutions in Pakistan. J Islam Bus Manage 7(1):126–139. https://doi.org/10.26501/jibm/2017.0701-010

Aslam S, Abdul M, Makki M, Mahmood S, Amin S (2018) Gender diversity and managerial ownership response to corporate social responsibility initiatives: empirical evidence from Australia. J Manage Sci 12(2):131–151

Aurangzeb XX, Dilawer T (2012) Earning management and dividend policy: evidence from Pakistani textile industry. Int J Acad Res Bus Soc Sci 2(10):362–372

Ayaz M (2017) Corporate governance from shariah perspective: a comparative study of Pakistani and Malaysian corporate governance frameworks for islamic financial institutions. International Islamic University Islamabad

Azeem M (2019) Corporate governance, financial constraints and dividend policy: evidence from Pakistan. COMSATS University Islamabad (CUI) Lahore Campus

Azhar U, Saeed SK (2015) Board composition, ownership structure and dividen policy in Pakistan. Jinnah Bus Rev 3(2):32–41

Azim F, Mustapha MZ, Zainir F (2018) Impact of corporate governance on related party transactions in family-owned firms in Pakistan. Inst Econ 10(2):22–61

Bakksh A, Akram M, Aslam S, Ahmad M (2020) Corporate governance, risk-taking and financial performance of islamic and conventional banks: evidence from Pakistan and Malaysia. Paradigms 11(1):152–158. https://doi.org/10.24312/20000122

Batool I, Jaffery MY (2020) Corporate governance bundles and corporate tax avoidance: a cross country study. City Univ Res J 10(1):151–166

Bhutta AI, Knif J, Sheikh MF (2016) Ownership concentration, client importance, and earnings management: evidence from Pakistani business groups. SSRN Electron J. https://doi.org/10.2139/ssrn.2852255

Bhutta NT (2014) Corporate entrepreneurship, agency cost and firm performance: Evidence from developed and developing economies. International Islamic University, Islamabad

Daud Z, Qazi LT, Atta-Ur-Rahman X (2015) Corporate governance and external finance: an empirical study of the banking and financial sector of the. Pak Bus Rev 16(4):759–788

Ehsan S (2018) Corporate social responsibility: Measurement, and its nexus with earning’s management and corporate governance. COMSATS University Islamabad, Lahore Campus

Ehsan S (2018) Essays on impact of banks’ ownership structure: Evidence from Pakistan. National University of Sciences & Technology, Islamabad

Ehsan S, Abbas Q, Nawaz A (2018) An inquiry into the relationship between earnings’ management, corporate social responsibility and corporate governance. Abasyn J Soc Sci 11(1):104–116

Fama EF, Jensen MC (1983) Separation of ownership and control. J Law Econ 26(2):301–325

Fareed MA, Hassan A (2017) Impact of managerial entrenchment and group affiliation on dividend policy in emerging economy of Pakistan empirical evidence from Kse listed non-financial firms. Jinnah Bus Rev 5(1):11–22

Farooq K, Manzoor A (2019) Role of ownership in corporate governance and its impact on firm performance: a case of companies listed in Pakistan Stock exchange. Glob Manag J Acad Corp Stud 9(2):165–187

Farooq SU, Ullah S, Kimani D (2015) The relationship between corporate governance and corporate social responsibility (CSR) disclosure: evidence from the USA. Abasyn J Soc Sci 8(2):197–212

Fayyaz M (2016) Executive compensation, firm performance and corporate Governance: COMSATS Institute of Information Technology (CIIT) Islamabad, Campus

Ghani WI, Haroon O, Ashraf J (2011) Business groups’ financial performance: evidence from Pakistan. Glob J Bus Res 5(2):27–39

Gul S, Rashid A, Muhammad F (2018) The impact of corporate governance on cost of capital: The case of small, medium, and large cap firms. Pak Bus Rev 20(2):354–374

Gul S, Rashid A, Muhammad F (2019) The impact of corporate governance on cost of capital: the case of small, medium, and large cap firms. J Bus Stud 12(1):247–271. https://doi.org/10.1017/CBO9781107415324.004

Gull S, Zaidi KS, Butt I (2020) Corporate governance and corporate social responsibility: a study on telecommunication sector of Pakistan. Int J Manage Res Emerg Sci 10(2):65–71

Hasan A, Butt SA (2009) Impact of ownership structure and corporate governance on capital structure of Pakistani listed companies. Int J Bus Manage 4(2):50–58. https://doi.org/10.1017/CBO9781107415324.004

Hassan M, Rizwan M (2016) Corporate governance under multi- theoretical perspective. J Bus Stud 12(2):68–86

Hassan S, Kayani GM, Ayub U (2018) Corporate governance and cost of equity capital using DCAPM. Abasyn J Soc Sci 11(2):335–351

Hussain A, Rehman DA, Siddique A, Rehman H (2018) Impact of ownership structure on bank risk taking: a comparative analysis of conventional banks and Islamic banks of Pakistan. J Bus Tour 4(1):175–181

Hussain S (2019) Tunneling or propping: evidence from family business groups of Pakistan [National University of Sciencecs and Technology, Islamabad, Pakistan]. Doi:https://doi.org/10.22547/ber/10.2.5

Hussain S, Safdar N (2018) Tunneling: evidence from family business groups of Pakistan. Bus Econ Rev 10(2):97–122. https://doi.org/10.22547/ber/10.2.5

Hussain S, Safdar N (2018b) Ownership structure of family business groups of Pakistan. In: 9th economics & finance conference, London, pp 75–89. Doi:https://doi.org/10.20472/efc.2018.009.006

Hussain S, Shah SMA (2017) Corporate governance and downside systematic risk with a moderating role of socio-political in Pakistan. Bus Econ Rev 9(4):235–260. https://doi.org/10.22547/ber/9.4.11

Ihsan A, Raza W, Jan S, Ullah H (2018) Effect of board independence on earning response coefficient (ERC): Evidence from Pakistan. Abasyn J Soc Sci 4(2):153–164. https://doi.org/10.26710/reads.v4i2.386

Ilyas M (2018) Impact of corporate governance on earnings management and cost of capital: evidence from Pakistan. Abdul Wali Khan University Mardan.

Ilyas M, Jan S (2017) Corporate governance and cost of capital: evidence from Pakistan. Glob Manage J Acad Corp Stud 7(2):10–21

Ilyas M, Khan I, Khan MN, Khan T (2017) Corporate governance and earnings manipulation: empirical analysis of non-financial listed firm of Pakistan. J Manage Sci 11(4):283–304

Ilyas M, Khan I, Urooge S (2019) Earnings manipulation and the cost of capital: Empirical investigation of non-financial listed firms of Pakistan. J Manage Sci 6(1):96–104. https://doi.org/10.20547/jms.2014.1906107

Iqbal AM, Khan I, Ahmed Z (2015) Earnings management and privatisations: Evidence from Pakistan. Pak Dev Rev 54(2):79–96. https://doi.org/10.30541/v54i2pp.79-96

Iqbal A, Zhang X, Jebran K (2015) Corporate governance and earnings management: a case of Karachi stock exchange listed companies. Indian J Corp Govern 8(2):103–118. https://doi.org/10.1177/0974686215602367

Iqbal K, Kakakhel SJ (2016) Corporate governance and its impact on profitability of the pharmaceutical industry in Pakistan. J Manage Sci 10(1):73–82

Jabeen M, Ali S (2017) Exploring the relationship between institutional shareholders’ heterogeneity and firm-level governance practices: evidence from Pakistan’s non-financial industries. J Manage Sci 11(2):229–245

Jamal AH, Shah SZA (2017) The impact of corporate governance on the financial distress: evidence from Pakistani listed companies. Jinnah Bus Rev 5(2):49–53

Javid AY, Iqbal R (2008) Ownership concentration, corporate governance and firm performance: evidence from pakistan. Pak Dev Rev 47(4):643–659. https://doi.org/10.5958/0976-5506.2018.01297.4

Javid AY, Iqbal R (2010) Corporate governance in Pakistan: corporate valuation, ownership and financing. In: PIDE working papers (issue 57)

Jensen MC, Meckling WH (1976) Theory of the firm: managerial behavior, agency costs and ownership structure. J Financ Econ 3(4):305–360

Kamran K, Shah A (2014) The impact of corporate governance and ownership structure on earnings management practices: evidence form listed companies in Pakistan. Lahore J Econ 19(2):27–70. https://doi.org/10.1016/j.sbspro.2014.03.686

Khalid R, Ali T, Javed MU (2019) Corporate governance : theory and practice impact of corporate governance on firm performance. Jinnah Bus Rev 7(1):66–75

Khalid W, Kashif-Ur-Rehman. XX (2019) Impact of insider trading & earnings management on the mechanism of Pakistani stock market during stock market bubble. J Manage Sci 13(2):23–32

Khalid Z, Yasser F, Ajmal MM (2015) The pricing of discretionary accruals: evidence from Pakistan. J Manage Res 2(2):1–23

Khalil MS, Nadeem MA, Khan MT, Shahzad S (2016) The impact of managerial ownership on the cash holdings in the cement sector of Pakistan. J Bus Tour 02(1):97–105

Khan FU, Nouman M (2017) Does ownership structure affect firm’s performance? Empirical evidence from Pakistan. Pak Bus Rev 19(1):1–23. https://doi.org/10.22555/PBR.V19I1.1243

Khan MI, Riaz S (2019) Corporate governance as a predictor of liquidity management. Pak Bus Rev 21(2):244–258. https://doi.org/10.1108/JMH-01-2014-0015

Khan MK, Ali R, Tariq S (2018) Impact of ownership structure on corporate dividend policy and performance. KASBIT Bus J 11(1):110–130

Khan MN, Ilyas M, Urooge S (2020) Country governance and corporate governance as determinants of firm efficiency; empirical study of Pakistan. J Bus Tour 06(01):241–254

Khan MWJ, Saeed U (2019) Impact of corporate governance on financial performance of sugar sector firms listed in Pakistan stock exchange. Abasyn J Soc Sci 12(2):329–341. https://doi.org/10.34091/ajss.12.2.10

Khan N, Shah FA (2019) The impact of earnings management on dividend policy: empirical analysis of kse-100 index firms. J Bus Tour 05(02):79–88

Khan S, Kamal Y, Khan A, Hussain A, Rafiq M, Bibi M, Shah SFA, Shah Z, Khan M (2020) The impact of ownership types on the value of discretionary accruals: What is the role of audit committee? Evidence from Pakistan. Int J Econ Financ 10(4):141–150. https://doi.org/10.32479/ijefi.10081

Khan Y, Amjad M, Batool S, Bashir OU (2016) Corporate governance factors drive firms ’ earning per share: evidence from Pakistan stock exchange listed companies. J Bus Tour 02(2):123–132

Khan Y, Saqib M, Ahmad A (2016) Cash holdings and business group membership in Pakistan. Discourse 02(02):75–83

Khattak ZZ, Sallam A, Abbas S, Khushnood M (2018). Pyramidal ownership composition and firm ’ s capital structure policy. Abasyn J Soc Sci, pp 30–41

Latif A, Khan MT, Khan MN (2016) Ownership structure and its impact on dividend policy: a case of non—financial companies in Pakistan. J Bus Tour 02(01):63–73

Latif AS, Abdullah F (2015) The effectiveness of corporate governance in constraining earnings management in Pakistan. Lahore J Econ 20(1):135–155

Latif AW, Latif AS, Abdullah F (2017) Influence of institutional ownership on earnings quality: evidence for firms listed on the Pakistan stock exchange. Pak Bus Rev 19(3):668–687

Latif K (2018) Interactions between corporate governance, earnings quality attributes and value of firm: empirical analysis from non-financial sector of Pakistan. International Islamic University, Islamabad

Latif K, Bhatti AA, Raheman A (2017) Earnings quality: a missing link between corporate governance and firm value. Bus Econ Rev 9(2):255–279. https://doi.org/10.22547/ber/9.2.11

Majeed A, Ahmed S, Ghafoor Z (2018) Does cultural diversity of board of directors and audit committee dynamic affect firm performance? Evidence from firms in Karachi Meezan index. J Islam Bus manage 8(2):465–479

Makki MAM (2010) Impact of corporate governance on intellectual capital efficiency and financial performance. National College Of Business Administration & Economics, Lahore

Malik QUZ, Afza T (2016) Do group affiliated firms specialize in debt? evidence from Pakistan. J Econ Admin Sci 32(1):1–20. https://doi.org/10.1108/jeas-07-2015-0020

Mehmood Y, Farid Hasnu SA (2020) Investment-cash flow sensitivity and financing constraints: study of Pakistani business group firms. Rev Socio-Econ Perspect 5(1):99–128. https://doi.org/10.2139/ssrn.3471042

Mukarram S (2018) Does board gender diversity matter ? Evidence from Indian listed firms. COMSATS UniversityIslamabad Islamabad Campus–Pakistan

Nasar A, Mugheri MS, Rahaman Z (2013) Managing risk factors through corporate governance for financial institutions of Pakistan. KASBIT Bus J 6:114–123

Nasr MA, Ntim CG (2018) Corporate governance mechanisms and accounting conservatism: evidence from Egypt. NICE Res J 11(3):386–407. https://doi.org/10.1108/CG-05-2017-0108

Nazir MS, Afza T (2018) Does managerial behavior of managing earnings mitigate the relationship between corporate governance and firm value? Evidence from an emerging market. Future Bus J 4(1):139–156. https://doi.org/10.1016/j.fbj.2018.03.001

Nazir S (2015) The relationship between corporate governance and firm value. Comsats Institute of Information Technology (CIIT) Lahore Campus.

Nosheen S, Faisal M (2018) Corporate governance, disclosure quality, and cost of equity: evidence from Pakistan. Lahore J Bus 6(2):63–91

Paul J, Criado AR (2020) The art of writing literature review: What do we know and what do we need to know? Int Bus Rev 29(4):1–7. https://doi.org/10.1016/j.ibusrev.2020.101717

Rafay A, Sadiq R, Ajmal M (2016) The effect of IAS-24 disclosures on governance mechanisms and ownership structures in Pakistan. Lahore J Bus 5(1):15–36

Rafy A, Ajmal M (2014) Earnings management through deferred taxes recognized under IAS 12: evidence from Pakistan. Lahore J Bus 3(1):1–19

Rahman HU, Rehman S, Zahid M (2018) The impact of boardroom national dirversity on firms’ performance and boards’ monitoring in emerging markets: a case of Malaysia. City Univ ResJ 08(01):1–15

Rasheed SM, Fareena S, Yousaf T (2019) Corporate governance and real earnings management: evidence form Pakistan stock exchange. Pak Bus Rev 21(2):292–305

Rehman R, Hasan M, Mangla IU, Sultana N (2012) Economic reforms, corporate governance and dividend policy in sectoral economic growth in Pakistan. Pak Dev Rev 4(51):133–145. https://doi.org/10.30541/v51i4iipp.133-146

Rizvi FA (2011) Impact of ownership structure on corporate dividend policy and performance. National University of Sciences and Technology Islamabad.

Saeed A, Hashmi AM, Javid AY (2019) Corporate social responsibility and earnings management: the moderating role of family ownership. Abasyn J Soc Sci 12(1):164–178

Saeed MB, Saeed SK (2018) Corporate governance and accounting conservatism: moderating role of audit quality and disclosure quality. Bus Econ Rev 10(2):123–150. https://doi.org/10.22547/ber/10.2.6

Sajid (2017) The impact of corporate governance on firm value, payout policy, cost of capital, and corporate social responsibility. Air University, Islamabad

Sajjad T, Abbas N, Hussain S, Ullah S, Waheed A (2019) The impact of corporate governance, product market competition on earning management practices. J Manag Sci 13(2):59–83

Saleem I, Aftab S, Khan MA, Ullah Z (2019) Director’s multiple identities and board tasks: a moderating role of the power. City Univ Res J 9(4):730–749

Shabbir AH, Tahir S, Aziz B (2013) Corporate governance through ownership structure: evidence from KSE-100 index. South Asian J Manage Sci 7(2):49–62

Shah IA (2018) Corporate governance, product market competition , corporate diversification and value of cash holding. International Islamic University Islamabad

Shah IA, Shah SZA (2018) Effect of corporate governance on cash holding: the role of product market competition. NICE Res J 11(1):39–57

Shah MA, Baloch QB (2018) Board characteristics and firms’ financial performance in eras of corporate governance codes 2012 in manufacturing sector of Pakistan. J Manag Sci 12(3):81–91

Shah SF, Rashid A, Shahzad F (2019) Does board structure improve financial reporting quality? Evidence of real earnings manipulation among Pakistani firms. Abasyn J Soc Sci 12(2):311–328. https://doi.org/10.34091/ajss.12.2.09

Shah SMA, Shanwari I (2015) Detecting earning management: deferred taxes vs accruals: a Pakistani perspective. J Account Finance Emerg Econ 1(2):111–134. https://doi.org/10.26710/jafee.v1i2.68

Shah SZA (2009) Corporate governance and financial performance a comparative study of developing and developed markets [Muhammad Ali Jinnah University]. http://prr.hec.gov.pk/jspui/bitstream/123456789/2819/1/306S.pdf

Shah SZA, Butt SA, Hasan A (2009) Corporate governance and earnings management an empirical evidence form Pakistani listed companies. Eur J Sci Res 26(4):624–638

Shah SZA, Yuan H, Zafar N (2010) Earnings management and dividend policy an empirical comparison between Pakistani listed companies and Chinese listed companies. Int Res J Financ Econ 35:51–60

Shahid MS, Abbas M, Rizwan M (2019) Corporate governance practices can mitigate the influence of capital structure on firm performance : a cross-country empirical study. Pak Bus Rev 21(2):318–335

Shahid MS, Felimban RH, Naheed K, Aleem U, Nawaz S (2014) Ownership structures, investors confidence and financial decisions in family firms: evidence from Gcc Markets. J Bus Stud 14(1):52–68

Shahid MS, Gul F, Hasnain A (2017) Impact of board size and composition on the efficiency of banks: evidence from Pakistan. NUML Int J Bus Manage 12(1):59–76

Shahid MS, Gul F, Rizwan M, Bucha MH (2016) Ownership structure, board size, board composition and dividend policy: new evidence from two emerging markets. J Bus Stud 12(2):25–36

Shahid MS, Nawaz S, Ali L (2018) Does ownership structure influence financial decisions: evidence from Pakistan. NUML Int J Bus Manage 13(2):51–64

Shahzad F (2018) Financial reporting quality, family business and Investment efficiency. Air University Islamabad

Sharif S (2016) Investment opportunity set, corporate governance practices and performance of modarabas. Glob Manage J Acad Corpor Stud. https://doi.org/10.2139/ssrn.2817821

Sheikh NA, Rafique A (2018) Effects of firm specific measures and board attributes on working capital : evidence from textile industry of. Pak Bus Rev 20(3):535–546

Shoukat A (2020) Political connection and enterprise development ( a case study of nishat business group ). J Contemp Res Soc Sci 2(1):8–25

Siddique I, Saleem I, Ahmed A (2019) When does the affiliate director matter more for family firms? Paradigms 13(1):12–18. https://doi.org/10.24312/1900018130103

Sohail I, Saeed MB, Murtaza Z (2013) Corporate governance and firm performance: a study on moderating effects of firm size and leverage on the relationship between corporate governance and firm performance in banking sector of Pakistan. Jinnah Bus Rev 1(2):40–46

Tahir SH (2014) Impact of family ownership on value and financial decisions of a firm: a comparative analysis of family and non-family companies listed at Karachi Stock Exchange (Pakistan). Government College University, Faisalabad

Tahir SH, Afzal A, Liaqat S, Tahir F, Ullah MR (2019) Corporate governance, working capital management and firm risk: empirical evidence from Pakistan stock exchange (PSX). J Manage Sci 13(4):65–73

Tahir SH, Ghafoor N, Ahmad G (2017) Corporate governance and cost of equity paradox : a case of family firms in emerging markets. J Manage Sci 11(4):43–50

Tariq YB (2014) Impact of corporate governance practices on firm performance [Mohammad Ali Jinnah University Islamabad]. Doi:https://doi.org/10.37200/IJPR/V24I2/PR200399

Tashfeen R, Hayat S, Mallik A (2019) Quality of corporate governance risk management in dealing with unanticipated events: evidence from Pakistan. Lahore J Bus 8(1):1–24. https://doi.org/10.35536/ljb.2019.v8.i1.a1

Ullah A, Shah S, Asif M (2018) The impact of corporate governance on voluntary disclosure : evidence from Pakistan. City Uniy Res J 08(02):155–167

Ullah H (2014) Examining tunneling behavior and its causes and consequences in business groups: empirical evidence from listed firms in the Pakistan stock exchange. Institute of Management Sciences Peshawar, Pakistan

Ullah H, Shah A (2015) Related party transactions and corporate governance mechanisms: evidence from firms listed on the Karachi. Pak Bus Rev 17(3):663–680

Ullah H, Shah A, Shah SHA (2019) Do capital markets punish tunneling behaviour of business groups? Agency perspective of related party transactions. J Appl Econ Bus Stud 3(1):15–40

Ullah M, Malik HA, Zeb A, Rehman A (2019) Mediating role of capital structure between corporate governance and risk. J Manage Sci 13(3):47–56

Ullah N, Mujtaba A, Aman N (2019) Does corporate governance and islamic label mitigates over investment of free cash flow? Evidence from Pakistan. NUML Int J Bus Manage 14(1):156–171. https://doi.org/10.1017/CBO9781107415324.004

Ullah S, Kamal Y (2017) Board characteristics, political connections, and corporate cash holdings: the role of firm size and political regime. Bus Econ Rev 9(1):157–179. https://doi.org/10.22547/ber/9.1.9

Ullah W (2017) Understanding the dynamics of business groups in Pakistan: a focus on the financial performance and dividend policy

Ullah W, Ali S, Mehmood S (2017) Impact of excess control, ownership structure and corporate governance on firm performance of diversified group firms in Pakistan. Bus Econ Rev 9(2):49–72. https://doi.org/10.22547/ber/9.2.3

Umer R, Abbas N, Hussain S (2019) The gender diversity and earnings management practices: evidence from Pakistan. City Univ Res J 10(2):342–357

Usman M, Alam HM (2020) Ownership structure and business firm value: a study of non-financial sector of Pakistan. South Asian J Manage Sci 14(1):61–81. https://doi.org/10.21621/sajms.2020141.04

Waseemullah, Hasan A (2017) Family ownership, excess control and firm performance: a focus on the family firms in Pakistan. Paradigms 11(2):141–150. Doi:https://doi.org/10.24312/paradigms110203

Waseemullah, Hasan A (2018) Business group affiliation and firm performance—evidence from pakistani listed firms. Pak Dev Rev 57(3):351–371. Doi:https://doi.org/10.30541/v57i3pp.351-371s

Yasser QR (2011) Corporate governance and firm performance: An analysis of family and non-family controlled firms. Pak Dev Rev 50(1):47–62. https://doi.org/10.30541/v50i1pp.47-62

Zahra K, Khan MJ, Warraich MA (2018) CEO characteristics and the probability of financial distress: evidence from Pakistan. NUML Int J Bus Manage 13(2):117–129. https://doi.org/10.1017/CBO9781107415324.004

Zain FAM, Muda WA, Rashid N (2018) The mediating effect of disclosure on the relationship between corporate governance mechanisms and firm performance of Islamic banks. Int J Acad Res Bus Soc Sci 8(12):1–12. https://doi.org/10.6007/ijarbss/v8-i12/5066

Zaman QU (2018) Capital structure dynamics and bank affiliation of business groups: evidence from Pakistan. Seisense J Manage 1(1):22–37

Zeb A, Hussain DA, Rahman DA (2019) Earnings management and dividend policy: testing audit quality for the moderating effect. J Bus Tour 05(01):45–54

Zitouni T (2016) Index approach of corporate governance. Glob J Manage Bus Res Finance 16(2):97–109

Zulfiqar-Ali-Shah S, Ali Butt S (2009) The impact of corporate governance on the cost of equity: empirical evidence from Pakistani listed companies. Lahore J Econ 14(1):139–171. https://doi.org/10.35536/lje.2009.v14.i1.a6

Zulfiqar S, Zafar N, Durrani TK (2009) Board composition and earnings management an empirical evidence form Pakistani listed companies. Middle Eastern Finance Econ 4(3):27–37

Acknowledgements

We acknowledged the administration of Institute of Management Sciences, Peshawar, Pakistan during this research by providing the facilities and using the Ph.D. Scholar Room.

Funding

Not applicable.

Author information

Authors and Affiliations

Contributions

This research idea was given by SK, YK and SH have given comprehensive comments and suggestions as well as reviewed and proof read. Furthermore, MA has given insight on theories, findings and developing thematic themes out of the findings. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors reported no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Khan, S., Kamal, Y., Hussain, S. et al. Corporate governance looking back to look forward in Pakistan: a review, synthesis and future research agenda. Futur Bus J 8, 24 (2022). https://doi.org/10.1186/s43093-022-00137-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s43093-022-00137-5

Keywords

- Corporate governance

- Systematic literature review

- Agency theory

- Firm performance

- Earnings management

- Family businesses

- CSR

- Financial distress and Pakistan stock exchange