Abstract

The literature gap in microfinance paradox of double bottom line (financial performance vs. outreach) has always been an interesting area of research. This paper proposes a theoretical model most suitable for Islamic Microfinance Institutions (MFIs) which enables Islamic MFIs’ to operate together with the existing financial models compliant with Islamic Shariah Law. This model is based on a distributed verification/decision-making process that might be realized (but not necessary) through blockchain. Among the available distributed verification techniques, blockchain technology is an attractive emerging computing paradigm due to its decentralized, immutable, shared, and secure data structure characteristics. This model proposes three significant propositions. First, sharing information through blockchain will allow a transparent network in MFI operations, which will raise confidence for donors resulting in a causal effect of a relatively lower profit rate to be charged by the MFIs. Second, the consensus mechanism will enable risk-sharing, a character of Islamic finance; thus, the MFIs will operate without any collateral for low-risk firms. Third, the double bottom line of MFIs' long-lasting paradox would be solved. As for practical implication of this proposed model, the causal impact of lower cost investment by the lenders would increase social welfare because of no collateral and no initial wealth requirement. The proposed model proposes a credit rationing approach where profit can be negative. No collateral will be used when calculating the creditworthiness of a borrower.

Similar content being viewed by others

Introduction

The global financial crisis in 2008 instigated developing a stable, transparent, independent, and sustainable financial system worldwide (Kayed and Hassan 2011; Petrick 2009). These financial anomalies have strained regulators consistently restrict managerial activities with rigid rules. However, facts have shown otherwise. Strict regulation in financial sectors probes a lack of investor confidence, which is against the logic of sustainable development (Nguyen 2016). Besides the regular performance agenda among the financial institutions, transparency in corporate data have been critical factors of investor confidence (Berger et al. 2011; Hoff and Stiglitz 1990; Nguyen 2016). Recent financial scandals and the adverse impact of the financial crisis on the performance of microfinance institutions (MFIs) urges for a sustainable financial model.

The precondition of a sustainable model is that an institution must have been operating without any significant influence from any internal and external institutions, which may include intermediaries, government, and relevant regulators (Adegbite et al. 2013). In practice, the traditional MFIs operation permits external institutions to privatize profits and socialize the potential losses (Adegbite et al. 2013; McGuire and Conroy 2000). However, the two are not necessarily in tension. Literature indicates that recent digital innovations, such as blockchain, have great potential to change today's business mechanism and an entire economy (Nguyen 2016). As a way out, tech-savvy enthusiasts use the internet and innovate blockchain embedded cryptocurrency. Sulkowski (2018) examined entrepreneurs' opinions who actively bring blockchain-embedded technologies into the potential market. The results reveal that blockchain-enabled technologies improve transparency and reliability which will only be realized when there is a supportive law framework.

Besides the 'tamper-proof' technology of blockchain from alteration of data, some high-profile hacks treat blockchain as un-hackable as the Titanic was unsinkableFootnote 1! Even if the technology works flawlessly, the underlying human fascination for corruption while creating the underlying records cannot be tackled using blockchain technology.Footnote 2 Blockchain is just a technology. It could be an immutable database system with excellent tracing records capabilities promoting transparency. Yet, it is just a system in which the accuracy of its output depends on the accuracy of the input. Besides a flawless blockchain-enabled technology for MFIs operation, a supportive legal framework and government policy are prerequisites before offering a sustainable model.

The application of blockchain-enabled technologies in recent times reportedly functions well in diverse areas: inventory authentication (Düdder and Ross 2017); proof-of-provinces (Verberne 2018); good labor environment and practiceFootnote 3 along with finance sectors (Chen and Bellavitis 2020; Treleaven et al. 2017; Xu et al. 2019). The first cryptocurrency was launched in 2009 with the name bitcoin that works as both a payment system and a fully digital currency (García-Corral et al. 2022). Today there are more than 6,537 cryptocurrencies on the market and 200 tokens.Footnote 4 Recently the term blockchain has shifted slightly to mean distributed ledger technology, which sheds light on a worldview that blockchain technology has potential application possibilities in many sectors beyond today's imagination (Dujak and Sajter 2019; Iansiti and Lakhani 2017; Wang et al. 2018; Fang, F., Ventre, C., Basios, M. et al.,2021). This paper proposes a blockchain-embedded model for its sustainable development and operations for microfinance institutions.

The ability to access credit in MFIs have restricted the potential growth and development of MFIs in many countries (Azad et al. 2016). Having considered the principles of blockchain technology, this paper proposes a theoretical model that will make MFIs operations sustainable. This proposed model is named a sustainable model considering its capacity to reduce profit rate for credit distribution (Hassan 2014; Chong 2021) and reduce information asymmetry due to theoretically meager chances to manipulate information (Hoff and Stiglitz 1990). Islamic MFIs, like other MFIs, aim to provide financial services on a micro-scale to assist poor people who are forsaken by commercial banks (Handayani et al. 2018). Islamic MFIs can only offer contracts to their clients based on pre-agreed profit- and loss-sharing partnerships. Thus, a blockchain embedded interest free model is most suitable for Islamic MFIs by ensuring their stability.

The contributions of this proposed model are threefold. First, by challenging the conventional credit system, our proposed blockchain-embedded model solves some critical issues in Islamic MFIs, such as information asymmetry and credit rationing, which ensures the financial sustainability of MFIs and enhances social outreach. A lower profit rate will be charged by the MFIs because the information in blockchain consensus cannot be altered or amended. Thus, the consensus mechanism will enable the risk-sharing character of Islamic MFIs (Mohamed and Ali 2018). Second, we remove the traditional non-negativity restriction in the credit rationing approach, which allows profits to be negative, and developed a model theory that does not need collateral during the loan/credit evaluation process. Third, our proposed model helps ensure sustainable social wealth by enhancing social welfare and provides a reliable and transparent credit system compared to conventional credit systems. Additionally, reliability and transparency will improve quality disclosure to lenders and borrowers and regulatory agencies and governments by facilitating the standardized monitoring of MFIs. In recent literature, monitoring has been identified to reduce loan repayment problems (Berns et al. 2021) and corrupt behavior (Azim et al. 2017). At this point, the decentralized sharing of information through our proposed model will solve the current monitoring challenges of MFIs, helping to build reputation and image by reducing the possibility of corruption scandals.

This paper has six sections. The second section reviews the literature on Islamic MFIs. "Blockchain technology: scope and areas of application in Islamic MFIs" section explains the scope and principles of blockchain technology for sustainable operations of Islamic MFIs. The proposed model for sustainable MFI operations is given in "Proposed model for MFIs" section, followed by propositions in "Propositions" section. Finally, "Conclusion" section is the conclusion.

Literature review

The target borrowers of MFIs are not financially eligible to access bank services due to financial status. Examining present conditions of more than two billion people among the developing economies with limited to no access to banking resources, Larios-Hernández (2017) studied five characteristics for the demographic: cash preference, accustomed lending practices, traditional money transfer system and remittance receipt preference, identification of personnel, and availability of infrastructure. While the scenario of financial inclusion varies across developed, developing, and underdeveloped economics, access to financial services remains a challenge in rich countries (including the UK) (Datta 2018). Relating to microfinance operations, Mader and Morvant-Roux (2019) discussed different financial inclusion approaches. Moreover, Muslims who are religious, believe in interest-free investments also possess extra sensitivity to accessing financial services from traditional MFIs since their operations are interest-rate-based.

Islamic microfinance is a special type of microfinance consistent with the principles of Islamic laws (Shariah). It is a practical application through the development of Islamic economics (Haque and Yamao 2011). Shariah prohibits the payment of fees for the loaning of money for specific terms, which is commonly known as interest (in Islamic terminology, 'riba'). All Muslim scholars are adamant that this prohibition extends to all forms of riba and that there is no difference between interest-bearing funds for consumption or investment purposes (El-Zoghbi and Tarazi 2013). Instead, money can be exchanged for any product or service in the form of collateral (Ahmad and Rafique Ahmad 2009). In the same logic, Shariah prohibits interest in personal investments. Hassan (2014) found that collective actions through Islamic microfinance groups help increase environmental awareness, economic betterment of the members, and fruitful management of the liquidity coverage ratio. Abubakar et al. (2019) examine various aspects of cryptocurrency and its Shariah compliance.

The main distinction between conventional institutions and MFIs is that the former is interest-based. At the same time, the latter is interest-free since the sharia prohibits the receiving and giving of any fixed, predetermined rate of return on financial transactions, or in other words, interest (El-Zoghbi and Tarazi 2013; Ghouse et al. 2021; Mirzaei et al. 2022). All the monotheistic religions prohibit interest due to its exploitative nature that creates inequality within society as it allows the lender to extract more wealth from vulnerable borrowers who may need to borrow money to meet their basic consumption requirements (El-Zoghbi and Tarazi 2013). It is also unfair because such a practice makes the lender richer and the borrower poorer, and the latter also must bear all the risks in the financial transaction (Austin 2004). Moreover, interest is also deemed an inequitable form of the transaction as it charges interest on loans for a productive purpose. At the same time, the moral economy of Islam encourages profit and loss sharing that reflects the level of participation between both parties.

Despite the rapid growth of MFIs in terms of their financial performances, their social outreach remains very poor compared to the total number of poor people worldwide (Churchill 2020; González Vega 1998; Meyer 2019; Sakti 2021). González Vega (1998) categorized microfinance outreach in six groups: (i) Quality- each client's value of any MFIs; (ii) Cost- both interest/profit cost and transactions cost; (iii) Depth- social value to extend the services of MFIs to any client groups; (iv) Breadth- total number of clients; (v) Length- the number credits have been offered to a client; and (v) Variety- types of financial services offered to the clients. Theoretically as well as empirically, if a microfinance institute is somehow becoming profitable, there is a high probability that it did not outreach successfully (Churchill 2020; McGuire and Conroy 2000; Meyer 2019). Thus, the objective of achieving the double bottom line (financial performance and outreach) of MFIs has been continuing to be a paradox.

Blockchain technology: scope and areas of application in Islamic MFIs

The first proposal of the blockchain concept was proposed by Nakamoto (2008). In plain words, blockchain is a type of digital record-keeping (Iansiti and Lakhani 2017). The technical elements required to enable and store are blocks, chain structure, hash algorithm, timestamp, and Merkle tree (Cong and He 2018; Iansiti and Lakhani 2017; Wang et al. 2018). Besides explaining the technical terminologies, the basic operations of a blockchain platform can be summarized to include a 'chain' of 'blocks'; a block stands for the digital data of any kind, and chain stands for the decentralized public database in which anyone of the chain owns the data without any intermediation and central control of the distribution of data. Furthermore, the timestamp, hash algorithm, and Merkle tree are technical applications to keep the record completely traceable and un-interrupt (Iansiti and Lakhani 2017; Wang et al. 2018).

The underlying technology of blockchain can be summarized in five principles (Iansiti and Lakhani 2017). First, with a distributed database, no one has control over the database. Each party within a network has equal access to the database to verify any transaction without an intermediary. Second, with the peer-to-peer transmission, no member/node works as a central node for sharing information, but rather, each node transmits and records information of a single transaction to all other nodes. Third, transparency means anyone in the system can see the information and amount of each transaction. Fourth, irreversibility of records indicates the record cannot be altered because data are linked to every node of the system. And fifth is computational logic. Using the computational logic or programmed rules, blockchain technology can automate a trigger for completing a transaction between nodes.

The digital nature of a blockchain transaction allows computer programmers to set up algorithms that automatically complete a transaction between two nodes (García-Corral et al. 2022). Therefore, the blockchain technology in the financial system will enable users to have a semi-formal since blockchain system offers a distributed ledger and privacy embedded with utmost security platform to access fund and completely ignore the need to use an interest-based financial system for operation. Thus, the adoption of blockchain technology in Islamic microfinance operations would offer a sustainable solution to poor communities and resolve the moral issue of riba among poor Muslim communities globally.

Several successful applications of blockchain-enabled technologies in Islamic financial institutions can be traced, aiming to strengthen Shariah-compliant business models (Abubakar et al. 2019; Alam et al. 2019; Kabra et al. 2020; Mohamed and Ali 2018; Fang et al. 2021; García-Corral et al. 2022). For example, Emirates NBR can be tracked as the first Islamic bank to integrate blockchain technology initially for cheque-based payment (Kabra et al. 2020). Similarly, Al Hilal bank was followed for the first successful application of blockchain technology for Sukuk (an income-bearing Islamic Shariah contract similar to conventional bond) transactions (Alam et al. 2019). Blossom's SmartSukuk is another successful blockchain-enables Sukuk initiative by Indonesia. In addition, South Africa-based POCertify applied blockchain for halal certifications. Finally, global Sadaqah is a Malaysian-based blockchain initiative of a charity organization.

Proposed model for MFIs

Traditional credit model

The traditional MFI credit model is described in Fig. 1. MFIs receive funds from either or all available sources: private equity, financial institutions, and personal donors (Ledgerwood 1998). According to their policy, organizational structure, and partner organizations, the MFIs then distribute and channelize the fund to the poor people (Ledgerwood 1998). Based on the character of institutional structure (i.e., formal, semi-formal, and informal), MFIs' objectives and operations may differ (Ledgerwood 1998; McGuire and Conroy 2000). Recently, MFIs have been cooperating with other development agencies (i.e., government, NGOs, donors) to enhance operating efficiency (Adegbite et al. 2013; Austin 2004; McGuire and Conroy 2000). Thus, the partner organizations' characteristics may also impact MFIs' objectives and operations.

Traditional credit model in MFIs

Among others, the traditional credit model was described by Stiglitz and Weiss (1981), Bester (1985), and Wang et al. (2018). Based on the theory of collateral and limited liability along with the presence of information asymmetry, Stiglitz and Weiss (1981) examined why banks cannot increase the collateral requirement (or decrease borrowers' debt-to-equity ratio) besides knowing that there is a relatively higher demand of loans out in the market? Here, as per the credit channel theory, asymmetric information in the credit market propagates the effect of the interest rate channel. Their findings revealed that the observationally identical borrowers may or may not receive loans from a bank. Even if the rejected borrowers are willing to pay a higher interest rate for their loans or increase their collaterals, this would only upsurge the riskiness of a bank's portfolio by either encouraging them to invest in risky projects or discouraging safe investors. Details of the model are given below.

Following the models of Adegbite et al. (2013), Austin (2004), Ledgerwood (1998), McGuire and Conroy (2000), Stiglitz and Weiss (1981), and Wang et al. (2018), this section will describe the traditional credit model of MFIs. Assume that a hypothetical credit market has asymmetric information. Let us consider that loan takers classify under either \(i = :1:low risk,2:high risk\). The total credit amount is presented as M. The expected return, probability of success of an investment/project, and probability of failure of an investment/project shall be given as \(\pi_{i} \left( r \right) for loan taker and p_{i} \left( r \right) for MFIs, P_{i } and 1 - P_{i}\) respectively.

According to Stiglitz and Weiss (1981), \(P_{1} X_{1} = P_{2} X_{2}\) because of mean preserving spread of returnsFootnote 5\(\left( {X_{i} } \right)\). The MR indicates total profit/interest earned, where R indicates gross profit rate (we are calling this profit rate since Islamic MFIs cannot charge interest) asked by MFIs. Primarily, R is determined by the market by analyzing opportunity costs. Finally, we assume that a credit institution depositor a deposit rate as denoted with \(\left( s \right)\). Based on the above assumptions, the basic models of expected returns in a traditional financing system can be expressed in Eq. 1 and 2. They explain the expected return expected of a loan taker and an MFIs, respectively.

We now assume that initial investment \(\left( W \right)\) is 0, collateral (\(C\)) is 0, and probability of success of a high-risk project \(\left( {P_{2} } \right)\) is higher than a low-risk project (\(P_{1} ):\) \(P_{2} > P_{1}\). This is to be mentioned here that, unlike the traditional MFIs operation, this model contributes theoretically by proposing that a loan taker can receive MFIs loan even without any collateral and initial investment. Theoretically, this assumption may increase the default risk of that loan taker, yet our model illustrates a better probability of success for a high-risk project. After adjusting the assumptions of Islamic MFIs into the traditional credit market model, the modified equations would be as follows:

The modifications are based on the following assumptions:

-

a)

Initial wealth W is 0

-

b)

Collateral C is 0

-

c)

If a project fails, the return is negative but not more than the loan amount M.

Thus, the estimated loss is ≤ M. Here, Eqs. 3 and 4 completely ignores the probability of failure of any project based on the assumptions of W = 0 and C = 0. Theoretically, with higher collateral, the rate of interest/profit (R) is supposed to get lower (Berger et al. 2011). In the case of Islamic MFIs, this paper proposes a new scheme based on blockchain to indicate the rate of R.

Blockchain embedded model

The underlying condition for getting approval of credit from a blockchain-embedded system requires receiving a decentralized consensus by providing a minimum degree of information for verification approval of credit (Cong and He 2018). Therefore, a modified model for a blockchain embedded credit system is provided in this subsection. For illustration, a low-risk investment from MFIs will be examined using a blockchain-embedded model, and a high-risk investment is presented with a traditional model. Finally, Eq. 5 describes the expected return of a low-risk loan taker through a blockchain model.

Here, \(f\) is the usage fee of blockchain technology for the loan taker, and D is the default loss of a loan receiver. As shown in Eq. 5, M is the compensation the lender would make in a traditional model. However, in the case of Islamic MFIs, W is 0; hence, the modified model would be:

Here, the equation introduces a category in a total investment of credit by all MFIs with (\(a)\) and \(\left( {1 - a} \right)\) is the portion of MFIs credit distributed by the government as we assumed that in any country, collaborative work between MFIs and the government could only work appropriately (Sulkowski 2018; Treleaven et al. 2017). Furthermore, without involving government in the blockchain embedded MFIs operation, the legal framework would not work prospectively. Thus, the expected return of MFIs from investments into a low-risk investment would be:

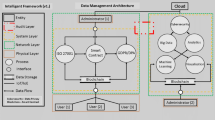

Here, g is the cost involved by MFIs for using blockchain technology (Janssen et al. 2020). Figure 2 depicts a blockchain-embedded credit system for Islamic MFIs. Figure 2 presents that during a transactions in the blockchain-embedded credit system, all the stakeholders: donors; financial institutions; Islamic MFIs; credit receiver and private equity providers, will be notified and through distributive ledger system of blockchain, the Islamic MFIs require no additional document to be produced and submitted to the creditors, loan receivers, government agencies and whatsoever. Nevertheless, distributive ledger automatically updates all stakeholders on the updates of any loan repayments and failures.

Proposed blockchain embedded credit system for MFIs

For the blockchain service provider, the return can be calculated using \(\delta_{i} \left( r \right)\):

Now, if the expected return from a high-risk firm is intended with a low-risk firm (assuming that \(R_{1}\) will equal here), its expected return would be:

Blockchain in Islamic MFI financing—does the adoption improve social welfare?

Subject to the ability of this blockchain-embedded model to distinguish between a low-risk firm and a high-risk firm, the return from a low-risk firm would be positive (Eq. 10). However, if a high-risk firm that takes a loan from the traditional system can be intended with its counterpart (low-risk firm \(R_{1}\)), the return of a high-risk firm would be lower than the benefit derived from the traditional manner (Eq. 11).

Now, subject to the satisfaction parameter of default loss D:

Thus, the expected outcome of this proposed blockchain embedded Islamic MFI model would explain a reasonable default cost, D, within which all low-risk firms would prefer to switch their business to a blockchain-embedded credit market. In contrast, high-risk firms will continue in the traditional market. Thus, the credit rationing problem (high-risk vs. low-risk firms) in any credit market (Bester 1985) has been mitigated through a blockchain model.

Finally, since the high-risk firms will continue borrowing from the local market, the total social wealth will maximize with an assumption that low-risk firms will adopt blockchain technology:

Propositions

The first proposition for using blockchain-embedded technology by Islamic MFIs is reducing information asymmetry among MFIs, donors, government, loan receivers, and all other parties. The information will be decentralized, and under consensus, the lending and borrowing function in Islamic MFIs would be more seamless and effective (González Vega 1998; Iansiti and Lakhani 2017; Treleaven et al. 2017). Secondly, the causal effect of such symmetric information with all the Islamic MFI stakeholders would ignore collateral requirements (Stiglitz and Weiss 1981). Thus, the traditional credit market could easily fit into the modified model, as shown in Eq. 6.

The third and most important opportunity of using a blockchain-embedded model in Islamic MFIs would be a low-profit rate R since creditor information is available, thus lowering the probability of manipulation; this formulates a self-sufficient system to track risky investors. In addition, the tamper-proof and algorithmic execution characteristics of blockchain technology may also enhance the reliability of the conventional credit system. It is also easy to ensure proper monitoring by the regulators or doners. Finally, the overall social wealth will increase for applying blockchain technology among the MFIs.

Conclusion

New developments in the era of technological innovation and adoption include the acceptance and advancement of next-generation information technologies (i.e., cloud computing, data mining, artificial intelligence, and mobile internet). Blockchain, one of the most attractive technologies in recent years, has seen extensive growth and great potential for applications in financial sectors (Conoscenti et al. 2016; Iansiti and Lakhani 2017; Larios-Hernández 2017; Nguyen 2016; Wang et al. 2018). However, blockchain is just a technology. It could be an immutable database system with excellent tracing records capabilities promoting transparency. Yet. It is just a system in which the accuracy of its output depends on the accuracy of the input. The governance issues of blockchain technology can be a challenge to the proposed model. Last but not least, high operating costs and computer able experts can be considered as detrimental factors for implementation of blockchain embedded MFIs. Borrowers’ or loan takers’ computer literacy is also a concern. MFIs are mostly targeting on ‘Ultra poor’- who might not have smart phone or even internet access, then how the proposed model to solve this issue? Yes, some countries like Bangladesh initiates the Union digitalization Programs- every Union Offices should have internet access.

The proposed theoretical model has the following implications: First, this paper addresses the unsolved issue of information asymmetry and credit rationing in the traditional credit system of MFIs, specifically in Islamic MFIs. The nature of an Islamic MFI business model kept the MFIs from reaching the double bottom-line (financial sustainability and social outreach). Second, this paper develops a model theory to show that social wealth will grow sustainably if low-risk firms receive loans from Islamic MFIs through our blockchain embedded model. Finally, one of the primary upgrades on this proposed model is that a credit rationing approach is introduced where profit can be negative. No collateral will be used when calculating the creditworthiness of a borrower.

To the best of our knowledge, this is one of the first papers that examines the application possibility of using blockchain technology in MFIs, especially in Islamic MFIs. Despite the earlier relevant model provided by Wang et al. (2018), the major contribution of this model that it mainly suitable for Islamic MFIs instead of traditional MFIs. This model may however, also application to general MFIs. Since Islamic Law strictly prohibits fixed income generated money transaction agreement, only transparent and accountable model like this is most application. Overall, with the assumption of zero initial wealth and zero collateral of this model perfectly fits this model for the actual group of needy people in the society. Finally, the proposed model also justifies that overall social welfare may be achieved. Therefore, this paper provides a lot of scope for future research. A few key areas would be including smart contracts in analyzing and distributing information asymmetry and credit rationing for the MFI financing issue and examining financial inclusion for socio-economic development.

Availability of data and materials

None.

Notes

Swati Khandelwal, Hackers Stole $32 Million in Ethereum; 3rd Heist in 20 Days, THE HACKER NEWS (July 19, 2017), https://thehackernews.com/2017/07/ethereum-cryptocurrency-hacking.html (accessed August/24/2020).

See The great chain of being sure about things, THE ECONOMIST (Oct. 31, 2015), (accessed August/24/2020) https://www.economist.com/briefing/2015/10/31/the-great-chain-of-being-sure-about-things.

Data from https://coinmarketcap.com (accessed August/23/2020). Tokens are digital assets such as vouchers, debt instruments (IOUs), or real-world objects. They are mostly based on the Ethereum blockchain.

In probability and statistics, a mean-preserving spread (MPS) is a change from one probability distribution A to another probability distribution B, where B is formed by spreading out one or more portions of A's probability density function or probability mass function while leaving the mean (the expected value) unchanged. See https://www.sciencedirect.com/science/article/abs/pii/0022053170900384?via%3Dihub.

References

Adegbite E, Amaeshi K, Nakajima C (2013) Multiple influences on corporate governance practice in Nigeria: Agents, strategies, and implications. Int Bus Rev 22(3):524–538

Ahmad AUF, Rafique Ahmad AB (2009) Islamic microfinance: the evidence from Australia. Humanomics 25(3):217–235. https://doi.org/10.1108/08288660910986946

Alam N, Gupta L, Zameni A (2019) Application of Blockchain in islamic finance landscape fintech and islamic finance. Springer, London, pp 81–98

Altwijry OI, Mohammed MO, Hassan MK, Selim M (2021) Developing a Shari’ah based FinTech money creation free [SFMCF] model for Islamic banking. Int J Islam Middle East Financ Manag 16(3):201–234. https://doi.org/10.1108/IMEFM-05-2021-0189

Austin R (2004) Of predatory lending and the democratization of credit: preserving the social safety net of informality in small-loan transactions. Am Univ Law Rev 53(6):20–35

Azad MAK, Masum AKM, Munisamy S, Sharmin DF (2016) Efficiency analysis of major microfinance institutions in Bangladesh: a Malmquist index approach. Qual Quant 50(4):1525–1537. https://doi.org/10.1007/s11135-015-0219-8

Azim MI, Sheng K, Barut M (2017) Combating corruption in a microfinance institution. Manag Audit J 32(4/5):445–462. https://doi.org/10.1108/MAJ-03-2016-1342

Berger AN, Scott Frame W, Ioannidou V (2011) Tests of ex-ante versus ex-post theories of collateral using private and public information. J Financ Econ 100(1):85–97. https://doi.org/10.1016/j.jfineco.2010.10.014

Berns JP, Shahriar AZM, Unda LA (2021) Delegated monitoring in crowdfunded microfinance: evidence from Kiva. J Corp Finan 66:101–164. https://doi.org/10.1016/j.jcorpfin.2020.101864

Bester H (1985) Screening vs. rationing in credit markets with imperfect information. Am Econ Rev 75(4):850–855

Chen Y, Bellavitis C (2020) Blockchain disruption and decentralized finance: the rise of decentralized business models. J Bus Ventur Insights 13:10–51

Chong FHL (2021) Enhancing trust through digital Islamic finance and blockchain technology. Qual Res Financ Mark 13(3):328–341

Churchill SA (2020) Microfinance financial sustainability and outreach: is there a trade-off? Empirical Econ 59(3):1329–1350

Dujak D, Sajter D (2019) blockchain applications in supply chain. In: Kawa A, Maryniak A (eds) SMART supply network. Springer International Publishing, Cham, pp 21–46

Fang F, Ventre C, Basios M et al (2021) Cryptocurrency trading: a comprehensive survey. Financ Innov 8(13):2–59. https://doi.org/10.1186/s40854-021-00321-6

García-Corral FJ, Cordero-García JA, de Pablo-Valenciano J, Uribe-Toril J (2022) A bibliometric review of cryptocurrencies: how have they grown? Financ Innov 8(2):2–32. https://doi.org/10.1186/s40854-021-00306-5

Ghouse G, Aslam A, Bhatti MI (2021) Role of islamic banking during COVID-19 on political and financial events: application of impulse indicator saturation. Sustainability 13(21):116–119. https://doi.org/10.3390/su132111619

Handayani W, Haniffa R, Hudaib M (2018) A Bourdieusian perspective in exploring the emergence and evolution of the field of Islamic microfinance in Indonesia. J Islamic Account Bus Res 9(4):482–497. https://doi.org/10.1108/jiabr-10-2017-0142

Haque MS, Yamao M (2011) Prospects and challenges of Islamic microfinance programmes: a case study in Bangladesh. Int J Econ Policy Emerg Econ 4(1):95–111. https://doi.org/10.1504/IJEPEE.2011.038875

Hassan AH (2014) The challenge in poverty alleviation: role of Islamic microfinance and social capital. Humanomics 30(1):76–90

Hoff K, Stiglitz JE (1990) Introduction: imperfect information and rural credit markets: puzzles and policy perspectives. World Bank Econ Rev 4(3):235–250

Iansiti M, Lakhani KR (2017) The truth about blockchain. Harv Bus Rev 95(1):118–127

Kabra N, Bhattacharya P, Tanwar S, Tyagi S (2020) MudraChain: Blockchain-based framework for automated cheque clearance in financial institutions. Futur Gener Comput Syst 102:574–587

Kayed RN, Hassan MK (2011) The global financial crisis and Islamic finance. Thunderbird Int Bus Rev 53(5):551–564

Larios-Hernández GJ (2017) Blockchain entrepreneurship opportunity in the practices of the unbanked. Bus Horiz 60(6):865–874. https://doi.org/10.1016/j.bushor.2017.07.012

Ledgerwood J (1998) Microfinance handbook: an institutional and financial perspective. The World Bank, New York

McGuire PB, Conroy JD (2000) The microfinance phenomenon. Asia Pac Rev 7(1):90–108

Meyer J (2019) Outreach and performance of microfinance institutions: the importance of portfolio yield. Appl Econ 51(27):2945–2962

Mirzaei A, Saad M, Emrouznejad A (2022) Bank stock performance during the COVID-19 crisis: does efficiency explain why Islamic banks fared relatively better? Ann Oper Res 314(2):1–39

Mohamed H, Ali H (2018) Blockchain, fintech, and islamic finance: building the future in the new islamic digital economy. Walter de Gruyter GmbH & Co KG, New York

Petrick JA (2009) Toward responsible global financial risk management: the reckoning and reform recommendations. J Asia-Pac Bus 10(1):1–33

Stiglitz JE, Weiss A (1981) Credit rationing in markets with imperfect information. Am Econ Rev 115(3):393–410

Sulkowski A (2018) Blockchain, business supply chains, sustainability, and law: the future of governance, legal frameworks, and lawyers. Del J Corp Law 43:303–345

Treleaven P, Brown RG, Yang D (2017) Blockchain technology in finance. Computer 50(9):14–17

Wang R, Lin Z, Luo H (2018) Blockchain, bank credit, and SME financing. Qual Quant 15(7):12–33. https://doi.org/10.1007/s11135-018-0806-6

Xu M, Chen X, Kou GA (2019) Systematic review of blockchain. Financ Innov 5(27):2–14. https://doi.org/10.1186/s40854-019-0147-z

Abubakar M, Hassan MK, Haruna MA (2019) Cryptocurrency tide and islamic finance development: any issue? In: Disruptive innovation in business and finance in the digital world, Emerald Publishing Limited, London.

Cong LW, He Z (2018) Blockchain disruption and smart contracts. Retrieved from https://ssrn.com/abstr act=31383 82, London.

Conoscenti M, Vetrò A, Martin JCD (2016) Blockchain for the internet of things: a systematic literature review. Paper presented at the 2016 IEEE/ACS 13th international conference of computer systems and applications (AICCSA). UK

Düdder B, Ross O (2017) Timber tracking: reducing the complexity of due diligence by using blockchain technology. Available at SSRN 3015219

El-Zoghbi M, Tarazi M (2013) Trends in Sharia-compliant financial inclusion. Brief. Washington, DC: CGAP, New York.

González Vega C (1998) Microfinance: broader achievements and new challenges. Econ Sociol Occas Paper No. 2518, 12(3): 1–19

Nakamoto S (2008) Bitcoin: a peer-to-peer electronic cash system. Bitcoin.org. https://bitcoin.org/bitcoin.pdf. Accessed: 24.02. 2020.

Nguyen QK (2016) Blockchain - a financial technology for future sustainable development. Paper presented at the 2016 3rd International Conference on Green Technology and Sustainable Development (GTSD). Greece

Sakti A (2021) Proposing new Islamic microfinance model for sustainable Islamic microfinance institution. In: Islamic finance and sustainable development. Palgrave Macmillan, Cham, pp 349–378

Verberne J (2018) How can blockchain serve society? Paper presented at the World Economic Forum. Greece

Funding

None.

Author information

Authors and Affiliations

Contributions

PW participated in concept development and editing. MH has developed the idea further and editing. AKA participated in concept development and has written the first draft. AR has revised the first draft. NA has contributed to model development. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare that they have no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Wanke, P., Hassan, M.K., Azad, M.A.K. et al. Application of a distributed verification in Islamic microfinance institutions: a sustainable model. Financ Innov 8, 80 (2022). https://doi.org/10.1186/s40854-022-00384-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s40854-022-00384-z