Abstract

Background

This paper examines the pattern of the volatility of the daily return of select commodity futures in India and explores the extent to which the select commodity futures satisfy the Samuelson hypothesis.

Methods

One commodity future from each group of futures is chosen for the analysis. The select commodities are potato, gold, crude oil, and mentha oil. The data are collected from MCX India over the period 2004–2012. This study uses several econometric techniques for the analysis. The GARCH model is introduced for examining the volatility of commodity futures. One of the key contributions of the paper is the use of the β term of the GARCH model to address the Samuelson hypothesis.

Result

The Samuelson hypothesis, when tested by daily returns and using standard deviation as a crude measure of volatility, is supported for gold futures only, as per the value of β (the GARCH effect). The values of the rolling standard deviation, used as a measure of the trend in the volatility of daily returns, exhibits a decreasing volatility trend for potato futures and an increasing volatility trend for gold futures in all contract cycles. The result of the GARCH (1,1) model suggests the presence of persistent volatility and the prevalence of long memory for the select commodity futures, except potato futures.

Conclusions

The study sheds light on significant characteristics of the daily return volatility of the commodity futures under analysis. The results suggest the existence of a developed market for the gold and crude oil futures (with volatility clustering) and show that the maturity effect is only valid for the gold futures.

Similar content being viewed by others

Background

Volatility plays a vital role in derivative pricing, hedging, risk management, and optimal portfolio selection. The concept of volatility relates to the uncertainty or risk about an asset’s value. A higher volatility means that an asset can assume a large range of values, while a lower volatility implies that an asset’s value does not fluctuate dramatically, even though it changes over time. Accurate modeling and forecasting of volatility in asset returns are major issues in financial economics. Derivative markets, particularly commodity futures markets, have become more sophisticated now a day. The futures price depends on the availability of information. A small change in price may have large effects on the trading results across futures markets. Researchers around the world showed increasing interest in the volatility of commodity futures. In the present analysis, an attempt is made to examine the trend and pattern of the volatility of daily returns of few select commodity futures in the Indian context.

As a first step, we examine the characteristics of the commodity futures. In particular, we analyze whether the price variability of a future increases or decreases when the contract approaches maturity. The Samuelson hypothesis for the selected commodity futures is tested. Samuelson (1965) argued that the volatility of the change in futures price increases as the contract approaches maturity. This phenomenon is also called the “Maturity Effect.” The purpose of testing the Samuelson hypothesis is to assess the degree of maturity of Indian commodity futures. From the view point of the Samuelson hypothesis, the prediction of price volatility is very useful for all participants in the futures market, such as hedgers, speculators, and traders. We also address the trend in daily return’s volatility across the contract cycles to decipher the volatility characteristics of the select commodity futures. To this end, we introduce the concept of rolling standard deviation.

We, then, proceed to examine the volatility aspects of the commodity futures. The steps involved in this exercise are the graphical plotting of the daily returns series, followed by its descriptive statistics. The daily returns are tested for stationarity. Then, we explored the GARCH (1, 1) model for the return volatility of the select futures.Footnote 1

The present paper derives its motivation from the following considerations. First, commodity futures as a financial asset is gaining prominence in the Indian capital market. The uninterrupted transactions in futures contracts from 2004, with a volume of trade surging from Rs 1.29 lakh crore in 2003–2004 to a peak of Rs 181 lakh crore in 2011–2012,Footnote 2 confirms the phenomenal importance of commodity futures. Second, empirically testing the Samuelson hypothesis as an indicator of developed and mature futures market seems necessary for the Indian commodity futures market. One of the key contributions of this paper is to use the GARCH (1,1) process for testing the Samuelson hypothesis on select commodity futures. Testing the Samuelson hypothesis through the β term of the GARCH (1,1) yields meaningful results, as the GARCH (1,1) assumes that the returns are uncorrelated, with zero mean. Moreover, in the GARCH (1,1) process, the present volatility does not depend on past returns, and thereby makes it a suitable methodology to test the Samuelson hypothesis. In this respect, the present analysis aims at filling a gap in the existing literature. Finally, in India, while the volatility issues related to dominant financial assets, such as company shares, have been well researched and documented, only a few studies on commodity futures have been carried out. More specifically, the trend and pattern of the volatility in the daily returns from commodities have been largely ignored in the existing literature. The remainder of this paper is organized as follows. The second section presents the literature. The third section deals with the methodology used in this paper and describes the relevant data sources. The result and discussion of the analysis are carried out in the fourth section. Finally, the fifth section provides our concluding remarks.

Literature review

Many researchers, such as W. R. Anderson (1985), examined the Samuelson hypothesis using selected agricultural futures contracts and found support for wheat, oat, soybeans, and soybeans meal futures. Bessembinder et al. (1996) provided a new framework for the maturity effect, the ‘BCSS hypothesis’ (based on Bessembinder, Coughenour, Seguin and Smoller). This hypothesis is an extension of the Samuelson hypothesis. The authors found that the Samuelson hypothesis is more likely to hold for those commodities whose price changes can be reversed in future. Black and Tonks (2000) investigated the pattern of the volatility of commodity futures prices over time and revealed the conditions which support the Samuelson hypothesis. Allen and Cruickshank (2000) analyzed the Samuelson hypothesis for selected commodity futures of three different futures markets in three different countries. They performed a regression analysis complemented by ARCH models, and the result suggests that the Samuelson hypothesis holds in the case of maximum selected contracts. Floros and Vougas (2006) investigated the Samuelson hypothesis in the context of the Greek stock index futures market and examined the maturity effect through linear regressions and GARCH models. The result of the study suggests that volatility depends on time to maturity and gives a stronger support to the Samuelson hypothesis compared to linear regressions. Duong and Kalev (2008) examined the Samuelson hypothesis for 336 selected commodities from five futures exchanges observed between 1996 and 2003. Using the Jonckheere-Terpstra Test, OLS regressions with realized volatility, and various GARCH models, the authors find mixed evidence concerning the support for the Samuelson hypothesis. Even though many studies investigated the Samuelson hypothesis, very few contributions analyzed it in the context of the Indian commodity futures market.

Notable exceptions are Verma and Kumar (2010), who examined the application of the Samuelson hypothesis and BCSS hypothesis in the Indian commodity futures market. Gupta and Rajib (2012) also examined this issue for eight commodities, and they concluded that the Samuelson hypothesis does not hold for the majority of the considered commodity contracts.

Numerous studies investigate the volatility of futures prices worldwide.

Locke and Sarkar (1996) examined the changes in market liquidity following changes in price volatility. The results of the study suggest that market makers are most hurt by volatility in the case of inactive contracts. Richter and Sorensen (2002) analyzed a volatility model for soybean futures and options using panel data. The study suggests the existence of a seasonal pattern in convenience yields and volatility, in line with the storage theory. Chang et al. (2012) examined a long memory volatility model for 16 agricultural commodity futures. The empirical results are obtained using unit root tests, GARCH, EGARCH, APARCH, FIGARCH, FIEGARCH, and FIAPARCH model. Manera et al. (2013) examined the effect of different types of speculation on the volatility of commodity futures prices. The authors selected four energy and seven non-energy commodity futures observed over the period 1986–2010. Using GARCH models, the study suggests that speculation affects the volatility of returns, and long-term speculation has a negative impact, whereas short term speculation has a positive effect. Christoffersen et al. (2014) analyzed the stylized facts of volatility in the post-financialization period using data of 750 million futures observed between 2004 and 2013.

Two strands in the existing literature focused on volatility in the Indian commodity futures market. First, the literature is largely dominated by spot price volatility and its spillover effect on future price volatility, that is, the price discovery mechanism of the futures market. Brajesh and Kumar (2009 ) examined the relationship between future trading activity and spot price volatility for different commodity groups, such as agricultural, metal, precious metal, and energy commodities in the perspective of the Indian commodity derivatives market. P. Srinivasan (2012) examined the price discovery process and volatility spillovers in Indian spot-futures commodity markets and the result points to dominant volatility spillovers from spot to futures market. Sehgal et al. (2012) examined the futures trading activity on spot price volatility of seven agricultural commodities and found that unexpected futures trading has strong correlation on spot volatility. Chauhan et al. (2013) analyzed the market efficiency of the Indian commodity market. They found that for guar seed, the volatility in futures prices influences the volatility in spot prices and the opposite result holds for chana. The work by Chakrabarti and Rajvanshi (2013) also explored the determinants of return volatility of select commodity futures in the Indian context. Sendhil et al. (2013) examined the efficiency of commodity futures through price discovery, transmission, and the extent of volatility in four agricultural commodities and found persistence volatility in spot market. Kumar et al. (2014) examined the price discovery and volatility spillovers in the Indian spot-futures commodity market. Gupta and Varma (2015) reviewed the impact of futures trading on spot markets of rubber in India and observed bidirectional flow of volatility between spot and futures market. Vivek Rajvanshi (2015) presented a comparative study on the performance of range and return-based volatility estimators for crude oil commodity futures. Malhotra and Sharma (2016) investigated the information transmission process between the spot and futures market and found that bidirectional volatility spillovers exists between the spot and futures market.

Second, a few studies specifically focus on the volatility of commodity futures. Kumar and Singh (2008) examined the volatility clustering and asymmetric nature of Indian commodity and stock market using S&P CNX Nifty for the stock market, and gold and soybean for the commodity futures market. Kumar and Pandey (2010) examined the relationship between volatility and trading activity for different categories of Indian commodity derivatives. They find a positive and significant correlation between volatility and trading volume for all commodities, no significant relationship between volatility and open interest, and an asymmetric relationship between trading volume and open interest. Kumar and Pandey (2011) examined the cross market linkages of Indian commodity futures with futures markets outside India. However, all these studies focus on the price volatility of commodity futures. In contrast with the above-mentioned studies on the Indian commodity futures market, the present study attempts to examine the return volatility of select commodity futures as financial assets.Footnote 3

Methods

The data on commodity futures are obtained from the official website of Multi Commodity Exchange (MCX), Mumbai, and cover the period from 2004 to 2012. We selected four commodities (potato, crude oil, gold, and mentha oil) from four different categories of commodity futures: Agricultural Commodity Futures, Energy, Bullions and Oil, and Oil Related Products, respectively. This choice satisfies two basic criteria: (i) the high frequency of future contracts; (ii) the large volume/value of such futures within the study period. Table 1 justifies the choice of the commodity futures.

In the commodity futures exchanges, trading takes place for 1-month, 2-month, and 3-month contract expiry cycles. However, in India, the 4-month, 5-month, and up to 1-year contract expiry cycles exist, in some cases, and we treat them as unusual exceptions. We only focus on the 1-month (near), 2-month (next-near), and 3-month (far) expiry cycles for futures. All futures contracts expire on the last Thursday of the month.

Hereafter, we provide a hypothetical example to demonstrate the steps involved in calculating the return in the logarithm form. We introduce a case based on crude oil.

-

The contract starts on July 30, 2010, and expires on October 20, 2010.

-

Nominal return for 1-month contract = ln(closing price on October 20)-ln(opening price on October 1); (October 1 is the Friday following the last Thursday of September, with 1 month to expiry, approximately.).

-

Nominal return for 2-month contract = ln(closing price on October 20)-ln(opening price on August 27); (August 27 is the Friday following the last Thursday of August, with 2 months to expiry, approximately).

-

Nominal return for 3-month contract = ln(closing price on October 20) -ln(opening price on July 30).

Here, the daily return on futures is calculated as the value of the continuously compounded rate of the return multiplied by 100. As such, the Log return of the price series = ln(Ft /Ft-1) *100, where Ft and Ft-1 are the closing prices on day t and (t-1) of a futures contract. The standard deviation of the daily return is also calculated for all the three categories of contract cycles.

We use the conventional standard deviation approach as the measure of the volatility of daily returns. A hypothetical example is as follows (Table 2).

We also introduce the concept of 25-day moving standard deviation (also known as the rolling standard deviation) as a measure of the trend in the volatility of the daily returns.

The method for calculating the rolling standard deviation is explained with the help of a hypothetical example based on crude oil futures.

-

The contract starts on July 30, 2010, and expires on October 20, 2010.

-

We consider the first 25 days starting from July 30, 2010 to calculate the standard deviation.

-

For the next period, the initial day (July 30, 2010) is left out and 1 day is added to the end of the period (August 24, 2010) so that the 25 days begin from July 31, 2010, and end on August 24, 2010. The standard deviation is calculated for these 25 days.

-

The above process is repeated for the entire length of the contract cycles to obtain the rolling standard deviation for the concerned futures.

-

In this example, 25-days are considered as the average number of trading days per month (leaving aside Sundays and other holidays). Therefore, the total annual trading days for commodity futures is 305 days.

We then proceed to plot graphically the daily returns series over time so that volatility clustering can be verified.

Descriptive statistics

To analyze the characteristics of the daily return series of the commodity futures market during the study period, the descriptive statistics show the mean (X), standard deviation (σ), Skewness (S), Kurtosis (K), and Jarque-Bera statistics results.

We calculated the coefficients of Skewness and Kurtosis to verify whether the return series is skewed or leptokurtic. To test the null hypothesis of normality, the Jarque-Bera statistic (JB) has been applied, as follows:

where N is the number of observations, S is the coefficient of Skewness, K is the coefficient of Kurtosis, k is the number of estimated coefficients used to create the series, and JB follows a Chi-square distribution with 2 degrees of freedom (d. f.). We perform a joint test of normality where the joint hypothesis of s = 0 and k = 3 is tested. If the JB statistic is greater than the table value of chi-square with 2 d. f., the null hypothesis of a normal distribution of residuals is rejected.

Test for stationarity

For testing whether the data are stationary or not, we performed the Augmented Dickey-Fuller (Dickey and Fuller 1979) and Philips-Perron Test (PP) (Phillips and Perron 1988). The stationarity of the return series has been checked by ADF test by fitting a regression equation based on a random walk with an intercept, or drift term (φ), as follows:

where μ t is a disturbance term with white noise. Here the null hypothesis is H 0 : ∂ = 0 (with alternative hypothesis H 1 : ∂ < 0). If this hypothesis is accepted, there is a unit root in the yt sequence, and the time series is non-stationary. If the magnitude of the ADF test statistic exceeds the magnitude of Mackinnon critical value, the null hypothesis is rejected, and there is no unit root in the daily return series.

Phillips and Perron (1988) suggested an alternative (non-parametric) method to control for serial correlation when testing for the presence of a unit root. The PP method estimates the non- augmented DF test equation, and it can be seen as a generalization of the ADF test procedure, which allows for fairly mild assumptions concerning the distribution of errors. The PP regression equation is as follows:

where the ADF test corrects for higher order serial correlation by adding lagged differenced terms on the right-hand side, while the PP test corrects the t statistic of the coefficient ∂ obtained from the AR(1) regression to account for the serial correlation μt. The null hypothesis is H 0 : ∂ = 0 (with alternative hypothesis H 1 : ∂ < 0).

Test for heteroskedasticity

The presence of heteroskedasticity in asset returns has been well documented in the existing literature. If the error variance is not constant (heteroskedastic), then, the OLS estimation is inefficient. The tendency of volatility clustering in financial data can be well captured by a Generalized Autoregressive Conditional Heteroskedastic (GARCH) model. Therefore, we modeled the time-varying conditional variance in our study as a GARCH process.

To identify the type of GARCH model that is more appropriate for our data, we performed the ARCH LM test (Engle 1982). This is a Lagrange Multiplier test for the presence of an ARCH effect in the residuals. We first regressed the return series on their one-period lagged return series and obtained the residuals \( \left({\widehat{\varepsilon}}^2\right) \). Then, the residuals have been squared and regressed on their own lags of order one to four to test for the ARCH effect. The estimated equation is:

where K t is the error term. We, then, obtained the coefficient of determination (R2). The null hypothesis is the absence of ARCH error, H 0 : ϑ i = 0, against the alternative hypothesis H 1 : ϑ i ≠ 0. Under the null hypothesis, the ARCH LM statistic is defined as TR2, where T represents the number of observations. The LM statistic converges to a χ 2 distribution. Hence, we use the Lagrange Multiplier (LM) test for Autoregressive Conditional Heteroskedasticity (ARCH) to verify the presence of heteroskedasticity in the residuals of the daily return series for all commodity futures. If the ARCH LM statistic is significant, we confirm the presence of an ARCH effect.

The ARCH model as developed by Engle (1982) is an extensively used time-series models in the finance-related research. The ARCH model suggests that the variance of residuals depends on the squared error terms from the past periods. The residual terms are conditionally normally distributed and serially uncorrelated. A generalization of this model is the GARCH specification. Bollerslev (1986) extended the ARCH model based on the assumption that forecasts of the time-varying variance depend on the lagged variance of the variable under consideration. The GARCH specification is consistent with the return distribution of most financial assets, which is leptokurtic and it allows long memory in the variance of the conditional return distribution.

The Generalized Arch Model (GARCH)

The GARCH model (Bollerslev 1986) assumes that the volatility at time t is not only affected by q past squared returns but also by p lags of past estimated volatility. The specification of a GARCH (1, 1) is given as:

mean equation:

variance equation:

where ω > 0, α ≥ 0, β ≥ 0, and r t. is the return of the asset at time t, μ is the average return, and ε t is the residual return. The parameters α and β capture the ARCH effect and GARCH effect, respectively, and they determine the short-run dynamics of the resulting time series. If the value of the GARCH term β is sufficiently large, the volatility is persistent. On the other hand, a large value of α indicates an insensitive reaction of the volatility to market movements. If the sum of the coefficients is close to one, then, any shock will lead to a permanent change in all future values. Hence, the shock is persistent in the conditional variance, implying a long memory.

Wald test

The Wald test estimates the test statistic by computing the unrestricted regression equation, without imposing any coefficient restrictions, as specified by the null hypothesis. The Wald statistic (under the null hypothesis) measures how the unrestricted estimates satisfy the restrictions. If the restrictions are valid, then, the unrestricted estimates should fulfill the restrictions.

We consider a general nonlinear regression model:

where β is a k vector of parameters to estimate. Any restrictions on the parameters can be written as:

where g is a smooth q dimensional vector imposing q restrictions on β.

Under the null hypothesis H˳, the Wald statistic has an asymptotic χ2 (q) distribution, where q is the number of restrictions.

The result of the above tests is derived using Eviews 7.

Result and discussion

The Samuelson hypothesis is tested by the daily returns for the select commodity futures, and the results are reported in Table 3. There is no clear trend and pattern in the percentage of the standard deviation among the selected commodities, except the gold futures, for which the Samuelson hypothesis holds. For other commodity futures (potato, crude oil, and mentha oil) this assumption is not confirmed.Footnote 4 For crude oil and mentha oil, the volatility of daily returns is greater for the 3-month (far) contract, followed by the 1-month (near) contract and the 2-months (next near) contract. The only exception is observed for potato futures, for which the volatility of daily returns for the 2-month (next near) contract is greater than that for the 1-month (near) contract. This phenomenon may be attributed to two possible reasons: (1) the underdeveloped and/or developing futures market in India, which acts as a barrier to the fulfillment of the Samuelson hypothesis; (2) since the volatility of daily returns for the 3-month (far) contract is greater for the selected three commodity futures (potato, crude oil, and mentha oil), the trend may be attributed to the initial euphoric behavior in the futures market, resulting from the initiation of a future contract.

Table 3 also presents the rolling standard deviation of the four commodity futures for all the three types of contract cycles.

To explore the trend in the volatility of daily returns for the selected commodity futures, we used the methodology known as 25-days rolling standard deviation. Figures 1, 2 and 3 depict the trends of the volatility for each commodity futures, where the x-axis measures the number of contracts traded and the y-axis measures the standard deviation in percentage (%) terms.

Trends based on rolling standard deviation for 1 (Near) month contract

Trends based on rolling standard deviation for 2 (next near) month contract

Trends based on rolling standard deviation for 3 (far) month contract

For potato futures, there is a decreasing trend in volatility for near, next near, and far month contracts, with near contract exhibiting the least declining trend in volatility, and far month contract showing the maximum declining trend in volatility.

For crude oil and mentha oil futures, the near month volatility trend of daily returns is almost constant, and the magnitude of rolling standard deviation (volatility trend) is the highest for the far month contract.

For gold futures, the trend in volatility is increasing for all types of contract (1-month, 2-month, and 3-month). Moreover, this rise in the trend in volatility is greater for the 1-month contract, suggesting that the gold futures trend is more volatile as the contract approaches the maturity date.

The descriptive statistics for daily return series of the select commodity futures are summarized in Table 4.

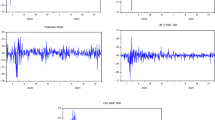

The average daily returns for all commodity futures are either close to zero or negative throughout the study period. The descriptive statistics show that the returns are negatively skewed. Since the estimated coefficients for the Skewness of the return series are different from zero, the underlying return distributions are not symmetric. The estimated coefficients for the Kurtosis of the daily return series are relatively high, suggesting that the underlying distributions are leptokurtic or heavily tailed and sharply peaked toward the mean compared to a normal distribution. The observed Skewness and Kurtosis indicate that the distribution of daily return series is non-normal. The Jarque-Bera normality test also shows the non-normality of the return distributions, as the estimated values of the Jarque-Bera statistic of all the return series are statistically significant at the 1% level (Figs. 4, 5, 6 and 7).

Daily return series graph of Potato futures

Daily return series graph of mentha oil futures

Daily return series graph of crude oil futures

Daily return series graph of gold futures

The correlogram test is conducted to address the presence of serial correlation in the residuals. We observe no serial correlation in the residuals up to 24 lags for the gold and crude oil futures in all types of contract cycles. This result holds for the 3-month (far) mentha oil contracts and potato near and next near contracts, as reported in Table 5.

The ADF and PP tests are performed to verify the stationarity of the daily return series, and the statistics are presented in Table 6. The p values of the ADF and PP tests are <0.05, which leads to conclude that the data used for the entire study period are stationary.

Both the test statistics reported in Table 6 reject the null hypothesis at the 1% significance level, with the critical value of −3.43 for both the ADF and PP tests. These results confirm that the series are stationary.

The graphs of daily returns confirm the absence of a clustering effect for potato futures and menthe oil futures. Only the 3 month contracts for menthe oil futures exhibits a small clustering effect for some periods. The graphs of crude oil and gold futures for all types of contracts show that the daily return series exhibits a clustering effect or volatility.

Table 7 presents the result of the ARCH-LM test (Engle 1982) of heteroskedasticity. This test detects the presence of the ARCH effect in the residuals of the daily return series. The ARCH-LM test statistic is significant for all types of contract cycles of gold commodity futures and the near and next near month contract of crude oil commodity futures, as well as for the mentha oil next nearFootnote 5 contracts. The result confirms the presence of ARCH effects in the residuals as the test statistics are significant at 1% level. Hence, the results confirm the need for the analysis of the GARCH effect. The ARCH-LM statistic is not statistically significant for all types of potato contracts and mentha oil near contracts. Moreover, in the case of far month contracts of crude oil and mentha oil futures, we find no evidence of ARCH effect in the residuals. These findings are in line with the negligible amount of volatility clustering exhibited by the daily returns’ volatility graph. Hence, the results seem to confirm the need for the analysis of the GARCH effect.Footnote 6

The GARCH model is used for modeling the volatility of daily return series for the three types of contracts (near, next near, and far contracts) for crude oil and gold commodity futures and only for next near and far month contracts for mentha oil futures. The result of the GARCH (1,1) model is shown in Table 8. All the parameters of the GARCH analysis are statistically significant.

The constant (ω), ARCH term (α), and GARCH term (β) are statistically significant at the 1% level. In the variance equation, the estimated β coefficient is considerably greater than the α coefficient, which implies that the volatility is more sensitive to its lagged values. The result suggests that the volatility is persistent. Moreover, the β term is greater for the near month contract cycles for gold futures, which confirms the validity of the Samuelson hypothesis. The sum of these coefficients (α and β) is close to unity, which indicates that a shock will persist for many future periods, suggesting the prevalence of long memory. However, the Wald test indicates the acceptance of the null hypothesis that α + β = 1 for far month contract cycles of gold futures only.

To check the robustness of the GARCH (1,1) model, we employed the ARCH-LM test (Engle 1982) to verify the presence of any further ARCH effect. As shown in the Table 7, the ARCH- LM test statistic for the GARCH (1,1) model does not show any additional ARCH effect in the residuals of the model, which implies that the variance equation is well specified for the select commodity futures.

As a result, we can conclude that, among the select commodity futures, the clustering effect is present in the volatility of daily returns for crude oil and gold commodity futures in all contract cycles. Mentha oil futures also present a clustering effect in far month contracts.

Conclusions

This paper addresses the volatility of four select commodity futures: potato, mentha oil, crude oil, and gold. All the three types of contract cycles (near month, next near month, and far month) are considered for volatility analysis. The conventional approach based on standard deviation as a measure of volatility is considered to test the Samuelson hypothesis. To further corroborate the findings, the β-term of the GARCH (1,1) is also used to verify the Samuelson hypothesis. The results suggest that the Samuelson hypothesis does not hold for the select commodity futures in the Indian context, except for the gold futures. These results are in line with the findings of Gupta and Rajib (2012) and suggest that the Indian gold futures market is as developed as in the advanced countries.

The trend in the volatility of daily returns is captured by the concept of rolling standard deviation. The volatility trends in crude oil and mentha oil futures highlight the significance of the available information as the far month volatility is higher than the near month volatility. The fluctuations in the world markets for oil commodities have a lagged impact on the domestic market. Finally, the objective of futures market in terms of price discovery and hedging against future risks seems to be satisfied for potato futures. To test the presence of a unit root in the daily return series, we performed the ADF and PP tests. The results confirmed the stationarity of the daily return series for all the commodity futures.

For volatility modeling, we first considered the graphical representation of volatility clustering along with the descriptive statistics for all contract cycles of each commodity future. We, then, introduced a correlogram to check for serial correlation in the residuals, and, finally, the ARCH-LM test was conducted to check for the presence of an ARCH effect. All contract cycles of potato futures did not show any volatility clustering, and the result of the ARCH-LM test ruled out any ARCH effects in the daily return series. However, for all types of contract cycles of gold futures, we found unambiguous volatility clustering, and the ARCH-LM test results also suggested the presence of an ARCH effect. These results are in line with the findings of Kumar and Singh (2008) for gold futures.

For mentha oil and crude oil futures, the result obtained from the volatility clustering and ARCH- LM test was ambiguous for different contract cycles. Although the result of the ARCH-LM test implied no ARCH effect for the far month of mentha oil and crude oil futures, a trace of volatility clustering was observed in the daily return graph. Hence, we considered the far month contracts of mentha oil and crude oil futures for the GARCH analysis.

Furthermore, the result of the GARCH (1,1) model shows that three parameters, the constant(ω), ARCH (α) term, and GARCH (β) term, are significant at the 1% level. In the variance equation, the estimated β coefficient is greater than the α coefficient, which implies that the volatility is more sensitive to its lagged values. Hence, the volatility is persistent. The sum of these coefficients (α and β) are close to the unit, which suggests that a shock will persist for many future periods. This is particularly true for gold futures of far month contract, in line with the findings of Kumar and Singh (2008).

The volatility clustering effect shows that the crude oil and gold futures markets are rather similar. The crude oil futures market is largely dependent on the global market conditions, which are highly volatile. The spillover effect of global volatility has an impact on the Indian crude oil futures market. Other significant macroeconomic variables (such as the interest rate, exchange rate, and so on, which are fluctuating in nature) have a significant impact on gold futures market in India. Thus, after examining the Samuelson hypothesis and volatility features, we concluded that, out of the selected commodity futures, gold futures are well developed and organized in the Indian market.

Notes

The aim of this paper is to portrait the simplest form of return volatility of the select commodity futures. Therefore, advanced volatility models (like EGARCH, TGARCH, PGARCH) are not considered, although the inclusion of such models would definitely enrich the present study.

Data source: www.fmc.gov.in

The factors affecting the return volatility of commodity futures (like trading volume and open interest) are not under the purview of the present study as that would unnecessarily complicate and shift the focus out of the presented issue.

Identical results hold for gold futures, for which we test the Samuelson hypothesis using the β term of GARCH (1, 1) model as a measure of volatility, as reported in Table 8.

The graph for the next near month contract of menthe oil shows volatility clustering although the Jarque-Bera value suggests that the residuals are not normally distributed. In addition, the correlogram shows that the residuals are serially correlated. Therefore we perform the ARCH-LM test and we observe the presence of ARCH effect.

Although the result of the ARCH-LM test implies no ARCH effect for the far month contract of mentha oil and crude oil futures, a trace of volatility clustering is observed in the daily return graph. Hence, we also consider the far month contracts of mentha oil and crude oil futures for the GARCH analysis.

References

Allen DE, Cruickshank SN (2000) Empirical testing of the Samuelson hypothesis: an application to futures markets in Australia, Singapore and the UK. Working paper, School of Finance and Business Economics, Edith Cowan University

Anderson RW (1985) Some determinants of the volatility of futures prices. J Futur Mark 5(3):331–348

Bessembinder H, Coughenour JF, Seguin PJ, Smoller MM (1996) Is there a term structure of futures volatilities? Reevaluating the Samuelson hypothesis. J Deriv 4:45–58

Black J, Tonks I (2000) Time series volatility of commodity futures prices. J Futur Mark 20(2):127–144

Bollerslev T (1986) Generalized autoregressive conditional Heteroskedasticity. J Econ 31(3):307–327

Chakrabarti BB, Rajvanshi V (2013) Determinants of return volatility: evidence from Indian commodity futures market. J Int Financ Econ 13(1):91–108

Chang C, McAleer M, Tansuchat R (2012) Modelling long memory volatility in agricultural commodity futures returns. Unpublished Working Paper 15093:10, Complutense University of Madrid

Chauhan KA, Singh S, Arora A (2013) Market efficiency and volatility spillovers in futures and spot commodity market. The agricultural sector perspective. SBIM VI(2):61–84

Christoffersen P, Lunde A, Olesen K (2014) Factor structure in commodity futures return and volatility. Working Paper, CREATES

David A. Dickey and Wayne A. Fuller (1979) Distribution of the Estimators for Autoregressive Time Series With a Unit Root. J Amer Stat Asso 74(366):427–431.

Duong NH, Kalev SP (2008) The Samuelson hypothesis in futures markets: an analysis using intraday data. J Bank Financ 32(4):489–500

Engle RF (1982) Autoregressive conditional Heteroskedasticity with estimates of the variance of UK inflation. Econometrica 50(4):987–1007

Floros C, Vougas VD (2006) Samuelson’s Hypothesis in Greek stock index futures market. Invest Manag Financ Innov 3(2):154–170

Gupta A, Varma P (2015) Impact of futures trading on spot markets: an empirical analysis of rubber in India. East Econ J 42(3):1–14

Gupta KS, Rajib P (2012) Samuelson hypothesis & Indian commodity derivatives market. Asia-Pacific Finan Markets 19:331–352

Kumar B (2009) Effect of futures trading on spot market volatility: evidence from Indian commodity derivatives markets. Social Science Research Network

Kumar B, Pandey A (2010) Price volatility, trading volume and open interest: evidence from Indian commodity futures markets. Social science research network

Kumar B, Pandey A (2011) International linkages of the Indian commodity futures market. Mod Econ 2:213–227

Kumar B, Singh P (2008) Volatility modeling, seasonality and risk-return relationship in GARCH-in-mean framework: the case of Indian stock and commodity markets. W.P. No. 2008-04-04, IIMA, 1-35

Kumar MM, Acharya D, Suresh BM (2014) Price discovery and volatility spillovers in futures and spot commodity markets : some Indian evidence. J Adv Manag Res 11(2):211–226

Locke P, A Sarkar (1996) Volatility and liquidity in futures markets. Research paper #9612, Federal Reserve Bank of New York

Malhotra M, Sharma KD (2016) Volatility dynamics in oil and oilseeds spot and futures market in India. Vikalpa 41(2):132–148

Manera M, Nicolini M, Vignati I (2013) Futures price volatility in commodities markets: the role of short term vs long term speculation. Università di Pavia, Department of Economics and Management, DEM Working Paper Series 42

Phillips PCB, Perron P (1988) Testing for unit roots in time series regression. Biometrika 75:335–346

Rajvanshi V (2015) Performance of range and return based volatility estimators:evidence from Indian crude oil futures market. Glob Econ Financ J 8(1):46–66

Richter M, Sorensen C (2002) Stochastic volatility and seasonality in commodity futures and options: the case of soybeans. Working Paper, Copenhagen Business School

Samuelson PA (1965) Proof that properly anticipated prices fluctuates randomly. Ind Manag Rev 6:41–49

Sehgal S, Rajput N, Dua KR (2012) Futures trading and spot market volatility: evidence from Indian commodity markets. Asian J Finan Acc 4(2):199–217

Sendhil R, Kar A, Mathur CV, Jha KG (2013) Price discovery, transmission and volatility: agricultural commodity futures. Agric Econ Res Rev 26(1):41–54

Srinivasan P (2012) Price discovery and volatility spillovers in Indian spot – futures commodity market. IUP J Behav Finance 9:70–85

Verma A, Kumar VSRVC (2010) An examination of the maturity effect in the Indian commodities futures market. Agric Econ Res Rev 23:335–342

Acknowledgements

The authors are indebted to three anonymous referee of this journal for their constructive comments of on the earlier draft of the manuscript. However, the usual disclaimer applies.

Funding

There is no financial assistance received in carrying out this particular research activity.

Availability of data and materials

The dataset is obtained from the publicly available repository, MCX, India website.

Author information

Authors and Affiliations

Contributions

BG initiated the thematic concept of the current research while IM carried out the exercise using statistical tools and techniques with the help of EViews 7. Both authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not Applicable.

Consent for publication

Not Applicable.

Competing interests

The authors declare that they have no competing interests.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Mukherjee, I., Goswami, B. The volatility of returns from commodity futures: evidence from India. Financ Innov 3, 15 (2017). https://doi.org/10.1186/s40854-017-0066-9

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s40854-017-0066-9