Abstract

In this paper, we analyse the relationship between public primary deficit and debt for Italian sustainability over the 1862–2013 years. Our empirical strategy uses the wavelet analysis. The empirical evidence suggests the presence of a substantial fiscal sustainability in the long run for Italy. This reversed much of the results of previous empirical literature, due to traditional time series approach and a shorter time horizon.

Similar content being viewed by others

1 Introduction

The aim of this paper is to reassess the relationship between public primary deficit and debt (as GDP ratios), in order to test for Italian fiscal sustainability over the period 1862–2013. Italy has the second largest public debt/GDP ratio, and it represents the third economy in the European Union (EU), so that its public accounts stability is crucial for the whole area (Brady and Magazzino 2017a).

The main problem for Italy, however, besides its high existing debt on which it is paying high interest in absolute terms, is that its growth is too slow. Since the euro area was founded, Italy’s average annual real growth was 0.4%, just marginally above the lowest rate of 0.3% per annum for Greece and one percentage point below the mean value for the overall euro area. Italy’s low growth rate, in turn, can be attributed to several structural causes. The country has recorded near zero productivity growth for years, and businesses are often very small, focus on the domestic market, and invest too little in R&D. Major inefficiencies exist in administration, e.g. in the justice system, and capital intensity is too low, also because investment declined by as much as 30% after the financial crisis. This was recently exacerbated by problems in the banking sector, including as a result of poor investment decisions in the past and short survival rates of governments over a long period, which have led to frequent election campaigns and delays in economic policy.

Time domain analysis is the most widespread approach in the economic literature to study time series. Through such approach, the evolution of individual variables is modelled and multivariate relationships are assessed over time. Another strand of literature focuses on the frequency domain. Wavelets analysis reconciles both approaches, in the sense that both time and frequency domains are taken into account. With this approach, we are able to differentiate between short- and long-run dynamics across the whole sample period.

The wavelet transform is a powerful tool for the analysis and processing of signals and is extremely efficient in various fields of application, such as compression and denoising, and in general when dealing with non-stationary signals, as pictures. These are in fact characterized by long-term dynamics at low frequencies (backgrounds) also called trends, and short-term dynamics at high frequencies (discontinuity, edges) also called anomalies. The latter, although they occupy a relatively small percentage in the image, have a high information content and must therefore be adequately represented.

The wavelet transform has several interesting properties:

-

it is able to analyse signals with characteristics that vary over time, thanks to its good capacity for time–frequency localization;

-

it provides a representation on different scales (multi-resolution representation);

-

it is easily achievable through a filter bank.

To the best of our knowledge, this is the first paper that applies wavelet analysis to Italian data. The evidence sheds new light on Italian fiscal sustainability issue in the long run.

Besides the Introduction, the remainder of this paper is organized as follows. Section 2 gives the theoretical context and the survey of the literature. Section 3 presents the empirical results, while Sect. 5 provides robustness’ checks. Finally, Sect. 6 concludes and gives some policy recommendations.

2 Empirical literature

In this section, we focus only on applied analysis on Italian fiscal sustainability. Corsetti and Roubini (1991) reported that the government finances of Italy did not satisfy the intertemporal budget constraint (IBC). Baglioni and Cherubini (1993) found that Italian fiscal policy did not follow a sustainable path in the eighties. Caporale (1995) found that Italian government cannot be considered intertemporally solvent. Vanhorebeek and Van Rompuy (1995) concluded that Italy’s fiscal policy undoubtedly leads to insolvency. For other countries, mixed results were obtained. Payne (1997) showed that Italy does not provide a clear evidence of sustainability of budget deficit. The principal implication of Artis and Marcellino (1998) is that the ratio will converge to a constant value, but not to zero. Papadopoulos and Sidiropoulos (1999) tested whether fiscal policy for the period 1961–1994 was consistent with a government intertemporally balanced budget, concluding that there is no evidence that the government of Italy can attain sustainable debts. The findings by Uctum and Wickens (2000) suggest that Italian fiscal policy was not sustainable in the years 1970–2000. Bravo and Silvestre (2002) tested for sustainability by performing an empirical analysis of cointegration between public expenditures and revenues (as ratios of GDP), pointing to the lack of possibility of sustainable budgetary paths in Italy. Afonso (2005) highlights that Italy faced the problem of having a higher growth rate for expenditures than the growth rate of revenues. Greiner and Kauermann (2008) concluded also against Italian public debt sustainability. Balassone et al. (2011) found evidence in favour of the hypotheses of a negative relation between public debt and growth. Dalena and Magazzino (2012) showed that public expenditure and revenues are cointegrated in each selected sub-period (Magazzino 2012). Casadio et al. (2012) showed that a policy intervention aimed to stimulate the GDP growth over 1.8% allows to reach the target 100% debt-to-GDP ratio. The empirical evidence by Piergallini and Postigliola (2012) shows the occurrence of a significantly positive reaction of primary surpluses to debt when the debt/GDP ratio exceeded the trigger value of 110%. Accounting for structural breaks, Trachanas and Katrakilidis (2013) suggested that the sustainability of the fiscal deficits in Italy holds only in a weak sense. Bartoletto et al. (2013) found that the dynamic of Italian public debt in the period 1861–2010 can be considered as sustainable, with the exception of the two World War years (1914–1945). Afonso and Jalles (2014) pointed out that since for Italy non-stationarity can be rejected, longer-run fiscal sustainability is not rejected. Causality tests by Magazzino and Intraligi (2015) revealed a significant causal relationship from the primary balance to the real growth rate, as well as a clear influence of the inflation on the interest rate. In contrast, the influence of public debt on growth rate emerges only marginally. Brady and Magazzino (2017b) pointed out the existence of two distinct states, both for public debt and deficit, with means and standard deviations rather different. Both states are extremely persistent. More recently, Brady and Magazzino (2019b) found a long-run relationship between public expenditure and revenues only for the sub-period 1862–1913. In essence, their results reveal that Italy had fiscal sustainability problems in the Republican age.

3 Methodology and data

We enter the debate on Italian debt sustainability by approaching it in a novel manner. Our analysis is not rooted in the time domain. We are interested in detecting and quantifying the time–frequency dependence between primary balance and lagged debt-to-GDP ratios. For that purpose, we make use of some wavelet analysis tools by analysing, firstly, the univariate features of the series through the continuous wavelet transform (CWT) (Grossmann and Morlet 1984; Mallat 2008) and the wavelet power spectrum (WPS), which give information simultaneously on time and frequency features of the data. Wavelet analysis reveals the spectral characteristics of a time series (discovering patterns and otherwise hidden information), in particular, the way in which different periodic components of the data on Italian national debt and primary balance evolve over time (Lo Cascio 2015).

The wavelet analysis allows to identify, within a time series, the short- and long-term periodic components, representing a valid alternative to the ARIMA X-11 and ARIMA X-12 for the identification of the long-term component, and to the frequency analysis for the identification of the cyclical components.

Many economic and financial time series are not stationary, which makes traditional methods ineffective in analysing them. Instead, the wavelet analysis overcomes this challenge as it does not require the assumption of stationary data.

A battery of three wavelet tools is used in analysis: the wavelet power spectrum (Torrence and Compo 1998; Grinsted et al. 2004; Ng and Chan 2012), the wavelet coherency including phase difference (Torrence and Compo 1998; Grinsted et al. 2004; Ng and Chan 2012), and partial wavelet coherency (Mihanović et al. 2009).

The wavelet transform is a tool that allows us to divide functions, operators, or data into components of different frequencies, allowing us to study them separately. The wavelet function is the ground of wavelet transformation, having as core different types of such functions, from Haar and Morlet, to Mexican hat, Paul or Daubechies wavelet. The Morlet wavelet (\(\psi_{0} \left( \eta \right)\)) is widely used in the related literature, being core of our study. It offers good results in term of balance between time (η) and frequency (ω0), having this form:

where i denotes \(\sqrt { - 1}\), while the non-dimensional frequency is 6 (Farge 1992).

The continuous wavelet transformation represents the best choice for feature extraction purposes (Tiwari et al. 2013); Aguiar-Conraria and Soares (2014, p. 647) claimed that ‘the continuous wavelet transform showed how the cross-wavelet analysis could be fruitfully used to uncover time–frequency interactions between two economic time series’.

With δt time spacing and scale s, the continuous wavelet transformation for a discrete time series {xn}, with n = 0…N − 1, is:

A wavelet power spectrum (WPS) can be performed as \(\left| {W_{n}^{x} } \right|^{2}\), revealing the local variance. The edge effects of the observations are shown by a cone of influence, the right interpretations being registered below cone. In this case, the null hypothesis is that the data-generating process is the result of a stationary process with a certain background power spectrum Pf. Under the null, the distribution for the local wavelet power spectrum has the form below:

where f is the Fourier frequency by Pf mean spectrum for the wavelet scale s (i.e. s ≈1/f). χ2 denotes the product of two distributions, and σ is the variance. Pf is higher than p, when v has value 1 for real wavelet and 2 in the case of complex one.

Supposing now two time series, x = {xn} and y = {yn}, the co-movement between them is depicted by cross-wavelet spectrum the wavelet coherency (WTC), as follows:

where S is the smoothing operator for both time and scale.

The WTC also allows to investigate the phase difference ϕx,y of considered series x = {xn} and y = {yn}, as follows:

with \({\Re }\) and \({\Im }\) as the real and imaginary parts of a complex number, respectively. The series are in phase and x leads y, when \(\phi_{x,y} \in \left[ {0, \frac{\pi }{2}} \right]\), while for \(\phi_{x,y} \in\) \(\left[ { - \frac{\pi }{2}, 0} \right]\), y leads x, respectively. Conversely, the series are in anti-phase for phase difference π or − π. Herein, x leads y, when \(\phi_{x,y} \in \left[ { - \pi , - \frac{\pi }{2}} \right]\), and y leads x, for \(\phi_{x,y} \in \left[ { \frac{\pi }{2}, \pi } \right]\), respectively.

Mihanović et al. (2009) propose the partial wavelet coherency (PWC) in order to analyse the effects of two time series y and x, after eliminating the influence of the third one z. The squared of partial wavelet coherence is the ground of PWC, with this form after the removal of the effects of z:

Our empirical analysis uses the time series data of lagged public debt x (% of GDP, B) and primary deficit y (% of GDP, PD) for Italy in the 1862–2013 years. We used the data recently reconstructed by Forte (2011).Footnote 1 Moreover, we derived the inflation series z to isolate the effect of co-movement between x and y (calculated as the variation of the consumer price index) from the ISTAT website.

However, the empirical strategy starts with the analysis of the stationarity properties of the variables. To this extent, besides the well-known unit root tests by Dickey and Fuller (1979), Phillips and Perron (1988), Kwiatkowski et al. (1992), Leybourne (1995), and Elliott et al. (1996), we employed also the more recent Kapetanios et al. (2003) and Kapetanios and Shin (2008) tests.

4 Empirical results

Although the stationary is not required feature in wavelet approach (Aguiar-Conraria et al. 2008), ‘the assumption of stationary statistics provides a standard by which any non-stationarity can be detected’ (Torrence and Compo 1998, p. 71).

Therefore, we applied time series tests on stationarity and unit root to determine the order of integration of our variables. Table 1 shows the results.

All tests suggest that public debt is non-stationary, while primary deficit is stationary (at levels). However, the first difference of B can be considered as a stationary process. Thus, we can conclude that public debt is integrated of order one, or I(1), while primary deficit is integrated of order zero, or I(0). Obviously, these findings imply that these series cannot share a stationary long-run relationship (no cointegration).

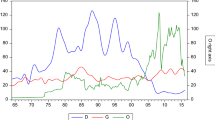

In Fig. 1, we show, on the left side, the plots of public debt/GDP and primary deficit/GDP ratios, observed over the 1862–2013 period. On the right side of the figure, we illustrate the wavelet power spectra (WPS) of the series. The analysis has been carried out by using the codes freely offered by Grinsted et al. (2004), and Ng and Chan (2012). The colour code for power range goes from blue (low power) to yellow (high power).

Sources: our elaborations on Forte (2011) and ISTAT data

Public debt and primary deficit over GDP and their power spectrum (Italy, 1862–2013).

Looking at the series of deficit as a share of GDP, we observe two negative peaks during the interwar period. However, it is interesting to note how, in general, the primary balance improved soon after the debt crisis events. Regarding the debt as share of GDP, we can identify five major events, which in chronological order are due to the Great Depression (1897, with the fall of aggregate income), World War I (1920), World War II (1943), the EMS and political crises (1994), and the recent Great Recession (2013).

The colour contour for each of the two series shows that the wavelet power is not constant over time as well as across frequencies. The public debt and deficit over GDP series do not share so many common features in terms of wavelet power. In fact, deficit has high power at medium and low frequencies (7–32 years band of scale), around 1890–1970. On the contrary, debt exhibits very high power at medium frequencies only (6–24 years band of scale), over the period 1910–1950. Moreover, for the two series, volatility is very low at all other (not mentioned) frequencies across time. The thick black curve in the right panel of Fig. 1 represents the cone of influence, while the black contours inside the cone denote the 5% significance levels against an ARMA (1, 1) null. The significance values were obtained from Monte Carlo simulations.

In Fig. 2, on the left side, we compute the wavelet coherency between public deficit and debt, while on the right one, we plot the partial wavelet coherency, after controlling for inflation. The concept of wavelet partial coherency is an extension of the concept of wavelet coherency just like partial correlation is an extension of the simple correlation.

Sources: our elaborations on Forte (2011) and ISTAT data

Wavelet coherence of pair ‘deficit–debt’ (a) and partial wavelet coherence of pair ‘deficit–debt’ by controlling for inflation (b) (Italy, 1862–2013). Notes (1) The arrows suggest the phase difference status between variables. They are in phase when the arrows are pointed to the right (positively related) and out of phase when the arrows are pointed to the left (negatively related). (2) The deficit is leading when the arrows are oriented to the right and up, or to the left and down, respectively. Otherwise, the debt is leading when the arrows are pointed to the right and down, or to the left and up, respectively. (3) The power range goes from blue colour (low power) to yellow one (high power). (4) The variables have a cyclical effect in the phase and anti-cyclical effect in the anti-phase.

We show, in spectra (a) and (b), the wavelet coherency (and partial coherency after controlling for inflation) between lagged debt and deficit to output ratios and their related phase difference. The local correlation was high and statistically significant (yellow colour) during the periods of range 1970–1985 (around 2–4 years of scale), 1882–1888 (around 3–6 years of scale), 1950–1970 (around 7–14 years of scale), 1890–1920 (around 12–16 years of scale), and 1890–1935 (around 16–28 years of scale).

At a high frequency, over the period 1970–1985 (around 2–4 years of scale), as the arrows are pointed to the right and up, the deficit positively drives the debt, and the variables are in phase. The variables are in anti-phase during 1882–1888 (around 3–6 years of scale), the arrows being oriented to the left side but up. Herein, the debt leads deficit with a negative sign.

At a medium frequency, the debt still leads the deficit with a negative sign over 1950–1970 (around 7–14 years of scale), the arrows being pointed to the left and up. Otherwise, at a similar frequency, deficit positively drives debt for the period 1890–1920 (around 12–16 years of scale). Herein, the arrows are oriented to the right and up, the variable being in phase.

At a low frequency, it is clear that the debt negatively drives deficit over 1890–1935 (around 16–28 years of scale), the arrows being pointed to the left and up. In this case, the variables are out of phase.

However, given the fact that debt changes gradually, only a long time scale is meaningful for fiscal sustainability. In the longer period cycle (16–32 years of scale), we found an only one area of high power (in yellow) in correspondence with the years 1890–1935: here, the two variables are in anti-phase (negative correlation). Notwithstanding, as pointed out above, in this period deficit decreases follow lagged debt increases, consistently with Bohn equation, which implies a sustainable fiscal policy.

Fiscal sustainability problems arise at a medium frequency (around 12–16 years of scale) during the last Historical Left governments, the ‘Trasformismo’ era, the Giolittian age, and the World War I years (from 1890 to 1920) (Forte and Magazzino 2016). In fact, here we found a high power area with the variables in a phase relation, but public deficit leads the debt, so that further increases of deficit/GDP ratio push up the debt stock, putting pressure on the Italian public finances. Nevertheless, this represents a period of fiscal insolvency characterized by a short persistence, as the arrows change their direction between 16 and 28 years of scale.

Regarding the wavelet partial coherency, we considered the coherency of the debt and deficit conditionally to the inflation rate, observing strong partial coherency for the period 1882–1888 (around 3–6 years of scale), 1890–1920 (around 12–16 years of scale), and 1890–1935 (around 16–28 years of scale). In those periods, both spectra exhibit the same pattern of the wavelet coherency, indicating that the inflation rate does not add anything to the relationship between public debt and deficit. Differently, for two sub-periods of time: 1950–1970 (around 7–14 years of scale) and 1970–1985 (around 2–5 years of scale), the inflation seems to play a crucial role as its effect completely attenuates the co-movement of interest variables.

These empirical findings are in line with previous results by Afonso and Jalles (2014), who concluded that the solvency condition would be satisfied for Italy. As noted above, a sustainability crisis emerges only in the years 1890–1920. However, this effect is not persistent and it is not registered for low frequencies. Thus, our results pointed out that, in a long-term horizon (beyond 16 years), the meaningful for sustainability, Italian public finances fulfilled fiscal solvency condition, consistently with Bohn (2011).

5 Robustness’ checks

The robustness check is performed having as ground the public debt/GDP variable, and the rest ones are the primary deficit/GDP and the inflation rate. Although our work follows the Lo Cascio (2015) approach, some bias in the wavelet estimations can arise as the variables are expressed in different terms (i.e. stock versus flow).

Hence, in order to deal with this challenge, we check for robustness by using the public debt/GDP in term of flow as absolute stock year-on-year change. In fact, the change denotes the variable’s first difference. We note that such correction should not be judged as a ‘realization of a stationarity process with mean zero’ (Percival and Walden 2000, p. 319). Moreover, this step also supposes a simple detrending process. Additionally, Mutascu (2018, p. 446) shows that ‘the adjustment will also increase the level of volatility although the series have annual frequency (i.e. the volatility is more visible for data with infra-annual frequency)’.

Two scenarios are followed: the first scenario takes into account the lagged public debt/GDP in its first difference, while the second one uses the lagged public debt/GDP without trend component in first difference. The series is detrended by subtracting its mean. The second scenario just tries to offer more accuracy to public debt/GDP variable treatment.

For both scenarios, we replicate the wavelet coherency and partial wavelet coherency tools by alternatively using the aforementioned adjusted lagged public debt/GDP variable, and primary deficit/GDP and inflation, respectively.

Figure 3, in ‘Appendix’, plots in the left side the wavelet coherency of pair ‘deficit–debt in first difference’ (a), and the partial wavelet coherence of pair ‘deficit–debt in first difference’ by controlling for inflation (b). Figure 4, also in ‘Appendix’, replicates the same previous wavelet methods but considers detrended debt in its first difference.

Wavelet coherence of pair ‘deficit–debt in first difference’ (a) and partial wavelet coherence of pair ‘deficit–debt in first difference’ by controlling for inflation (b) (Italy, 1862–2013). Notes For interpretations, see the explanations from Fig. 2

Wavelet coherence of pair ‘deficit–detrended debt in first difference’ (a) and partial wavelet coherence of pair ‘deficit–detrended debt in first difference’ by controlling for inflation (b) (Italy, 1862–2013). Notes For interpretations, see the explanations from Fig. 2

It is clear that by working with public debt/GDP in term of flow, both Figs. 3 and 4 output the same results irrespective of variable treatment. Moreover, those findings quasi-exactly fit the core estimations from Fig. 2, showing that main results are robust to public debt/GDP in term of flow. In other words, the main outcomes are not sensitive to characteristic of public debt/GDP variable as it is expressed in term of stock or flow, reinforcing the core results illustrate in Fig. 2.

6 Concluding remarks and policy implications

Public debt sustainability is a debated issue in economics. In this study, we assess the relationship between public debt and primary balance (both as GDP ratio) for Italy over the years 1862–2013 by using a wavelet coherence approach. These empirical findings are in line with previous results by Afonso and Jalles (2014), while it overturns applied findings due to studies on a shorter time period horizon. Therefore, using a long-run perspective (152 annual observations) together with a new econometric approach (wavelet analysis) we are able to shed new light on the sustainability of Italian public accounts. Analysing the wavelet coherence, a sustainability crisis emerges in the years 1890–1920 only. However, this effect is not persistent and registered for a medium period. Thus, our results pointed out that, in a long-term horizon (beyond 16 years), which is the only meaningful for sustainability, Italian public finances fulfilled fiscal solvency condition, consistently with Bohn (2011).

Nevertheless, the results of the present studies must be taken cautiously. In fact, in the last years (2014–2018), the Italian public debt-to-GDP ratio has constantly fallen above 130%, far from the threshold that Reinhart and Rogoff (2010) judged as a threat for the growth prospects of a country. In addition, as shown by Legrenzi and Milas (2012), a slow fiscal adjustment process operating through changes in taxes rather than changes in government expenditures is not surprising for Italy.

Budget constraints should be used flexibly, at least temporarily, to allow the country to accompany the recovery path with structural reforms that lighten the burden of fiscal adjustment, creating the conditions for a better equilibrium between budgetary rigour and development process. Household wealth can be an auxiliary parameter for assessing the sustainability of public debt, but this involves the distribution of wealth, how it is registered, as well as the political capacity of the government to tax it.

Notwithstanding, our empirical results should not deter Italian policymakers from solving some long-standing economic problems, as the high public debt/GDP ratio, the inability to restructure and cut public expenditures, the excessive tax evasion, the modest productivity growth, the unsustainable bureaucratic and judicial inefficiency, a heavy taxation on energy, and a diffuse corruption, all factors that undermine Italian economic growth as well as its fiscal sustainability (Magazzino 2012; Bini Smaghi 2017; Cottarelli 2018; Brady and Magazzino 2019a).

Availability of data and materials

The data are available upon request.

Notes

For years 2009–2013, we used the ISTAT data, https://www.istat.it/it/prodotti/banche-dati/serie-storiche.

References

Afonso A (2005) Fiscal sustainability: the unpleasant European case. FinanzArchiv 61(1):19–44

Afonso A, Jalles JT (2014) A longer-run perspective on fiscal sustainability. Empirica 41:821–847

Aguiar-Conraria L, Soares MJ (2014) The continuous wavelet transform: moving beyond uni- and bivariate analysis. J Econ Surv 28(2):344–375

Aguiar-Conraria L, Azevedo N, Soares MJ (2008) Using wavelets to decompose the time–frequency effects of monetary policy. Physica A 387:2863–2878

Artis M, Marcellino M (1998) Fiscal solvency and fiscal forecasting in Europe. CEPR discussion paper 1836

Baglioni A, Cherubini U (1993) Intertemporal budget constraint and public debt sustainability: the case of Italy. Appl Econ 25:275–283

Balassone F, Francese M, Pace A (2011) Public debt and economic growth in Italy. Quaderni di Storia Economica: Bank of Italy, 11 Oct 2011

Bartoletto S, Chiarini B, Marzano E (2013) Is the Italian public debt really unsustainable? An historical comparison (1861–2010). CESIfo working paper, 4185, April

Bini Smaghi L (2017) La tentazione di andarsene. Fuori dall’Europa c’è un futuro per l’Italia. il Mulino, Bologna

Bohn H (2011) The economic consequences of rising U.S. government debt: privileges at risk. Finanzarchiv 67(3):282–302

Brady GL, Magazzino C (2017a) Sustainability of Italian budgetary policies: a time series analysis (1862–2013). Eur J Gov Econ 6(2):126–145

Brady GL, Magazzino C (2017b) The sustainability of Italian public debt and deficit. Int Adv Econ Res 23(1):9–20

Brady GL, Magazzino C (2019a) Government expenditures and revenues in Italy in a long-run perspective. J Quant Econ 17(2):361–375

Brady GL, Magazzino C (2019b) The sustainability of Italian fiscal policy: myth or reality? Econ Res Ekonomska Istraživanja 32(1):772–796

Bravo ABS, Silvestre AL (2002) Intertemporal sustainability of fiscal policies: some tests for European countries. Eur J Polit Econ 18:517–528

Caporale GM (1995) Bubble finance and debt sustainability: a test of the government’s intertemporal budget constraint. Appl Econ 27:1135–1143

Casadio P, Paradiso A, Rao BB (2012) The dynamics of Italian public debt: alternative paths for fiscal consolidation. Appl Econ Lett 19(7):635–639

Corsetti G, Roubini N (1991) Deficits, public debt and government solvency: evidence from OECD countries. J Jpn Int Econ 5:354–380

Cottarelli C (2018) Il macigno. Perché il debito pubblico ci schiaccia e come si fa a liberarsene. Feltrinelli, Milano

Dalena M, Magazzino C (2012) Public expenditure and revenue in Italy, 1862–1993. Econ Notes 41(3):145–172

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74(366):427–431

Elliott G, Rothenberg TJ, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64(4):813–836

Farge M (1992) Wavelet transforms and their applications to turbulence. Annu Rev Fluid Mech 24:395–457

Forte F (2011) L’economia italiana dal Risorgimento ad oggi, 1861–2011. Cantagalli, Siena

Forte F, Magazzino C (2016) Government size and economic growth in Italy: a time-series analysis. Eur Sci J 12(7):149–169

Greiner A, Kauermann G (2008) Debt policy in euro area countries: evidence for Germany and Italy using penalized spline smoothing. Econ Model 25:1144–1154

Grinsted A, Moore SJ, Jevrejeva C (2004) Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Process Geophys 11:561–566

Grossmann A, Morlet J (1984) Decomposition of Hardy functions into square integrable wavelets of constant shape. SIAM J Math Anal 15:723–736

Kapetanios G, Shin Y (2008) GLS detrending-based unit root tests in nonlinear STAR and SETAR models. Econ Lett 100:377–380

Kapetanios G, Shin Y, Snell A (2003) Testing for a unit root in the nonlinear STAR framework. J Econ 112:359–379

Kwiatkowski D, Phillips PCB, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: how sure are we that economic time series have a unit root? J Econ 54(1–3):159–178

Legrenzi G, Milas C (2012) Nonlinearities and the sustainability of the government’s intertemporal budget constraint. Econ Inq 50:988–999

Leybourne SJ (1995) Testing for unit roots using forward and reverse Dickey–Fuller regressions. Oxf Bull Econ Stat 57:559–571

Lo Cascio I (2015) A wavelet analysis of US fiscal sustainability. Econ Model 51:33–37

Magazzino C (2012) Politiche di bilancio e crescita economica. Giappichelli, Turin

Magazzino C, Intraligi V (2015) La dinamica del debito pubblico in Italia: un’analisi empirica (1958–2013). Rivista italiana di economia demografia e statistica 59(3):167–178

Mallat SG (2008) Wavelet tour of signal processing. Academic Press, Cambridge

Mihanović H, Orlić M, Pasrić Z (2009) Diurnal thermocline oscillations driven by tidal flow around an island in the Middle Adriatic. J Mar Syst 78:S157–S168

Mutascu M (2018) A time–frequency analysis of trade openness and CO2 emissions in France. Energy Policy 115:443–455

Ng EKW, Chan JCL (2012) Geophysical applications of partial wavelet coherence and multiple wavelet coherence. J Atmos Ocean Technol 29:1845–1853

Papadopoulos AP, Sidiropoulos GP (1999) The sustainability of fiscal policies in the European union. Int Adv Econ Res 5(3):289–307

Payne JE (1997) International evidence on the sustainability of budget deficits. Appl Econ Lett 4(12):775–779

Percival DB, Walden AT (2000) Wavelet methods for time series analysis. Cambridge University Press, Cambridge

Phillips PCB, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–346

Piergallini A, Postigliola M (2012) Fiscal policy and public debt dynamics in Italy, 1861–2009. Rivista Italiana degli Economisti 17(3):417–440

Reinhart CM, Rogoff KS (2010) Growth in a time of debt. Am Econ Rev 100:573–578

Tiwari A, Mutascu M, Andries A (2013) Decomposing time–frequency relationship between producer price and consumer price indices in Romania through wavelet analysis. Econ Model 31:151–159

Torrence C, Compo GP (1998) A practical guide to wavelet analysis. Bull Am Meteor Soc 79:605–618

Trachanas E, Katrakilidis C (2013) Fiscal deficits under financial pressure and insolvency: evidence for Italy, Greece and Spain. J Policy Model 35:730–749

Uctum M, Wickens M (2000) Debt and deficit ceilings, and sustainability of fiscal policies: an intertemporal analysis. Oxf Bull Econ Stat 62(2):197–222

Vanhorebeek F, Van Rompuy P (1995) Solvency and sustainability of fiscal policies in the EU. De Economist 143(4):457–473

Acknowledgements

Comments from the participants at the Giornata di studio in onore di Gian Cesare Romagnoli (Rome, November 2018) as well as from the anonymous referees and the Editor are gratefully acknowledged. All remaining errors are our own.

Funding

Not applicable.

Author information

Authors and Affiliations

Contributions

CM wrote Sections Introduction, Empirical literature, Empirical results and Concluding remarks and policy implications; and 5 MM wrote Sections Methodology and data and Robustness’ checks. Both authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Magazzino, C., Mutascu, M. A wavelet analysis of Italian fiscal sustainability. Economic Structures 8, 19 (2019). https://doi.org/10.1186/s40008-019-0151-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s40008-019-0151-5