Abstract

Background

Malaria is the single largest cause of illness in Uganda. Since the year 2008, the Global Fund has rolled out several funding streams for malaria control in Uganda. Among these are mechanisms aimed at increasing the availability and affordability of artemisinin-based combination therapy (ACT). This paper examines the availability and affordability of first-line malaria treatment and diagnostics in the private sector, which is the preferred first point of contact for 61% of households in Uganda between 2007 and 2018.

Methods

Cross-sectional surveys were conducted between 2007 and 2018, based on a standardized World Health Organization/Health Action International (WHO/HAI) methodology adapted to assess availability, patient prices, and affordability of ACT medicines in private retail outlets. A minimum of 30 outlets were surveyed per year as prescribed by the standardized methodology co-developed by the WHO and Health Action International. Availability, patient prices, and affordability of malaria rapid diagnostic tests (RDTs) was also tracked from 2012 following the rollout of the test and treat policy in 2010. The median patient prices for the artemisinin-based combinations and RDTs was calculated in US dollars (USD). Affordability was assessed by computing the number of days’ wages the lowest-paid government worker (LPGW) had to pay to purchase a treatment course for acute malaria.

Results

Availability of artemether/lumefantrine (A/L), the first-line ACT medicine, increased from 85 to100% in the private sector facilities during the study period. However, there was low availability of diagnostic tests in private sector facilities ranging between 13% (2012) and 37% (2018). There was a large reduction in patient prices for an adult treatment course of A/L from USD 8.8 in 2007 to USD 1.1 in 2018, while the price of diagnostics remained mostly stagnant at USD 0.5. The affordability of ACT medicines and RDTs was below one day’s wages for LPGW.

Conclusions

Availability of ACT medicines in the private sector medicines retail outlets increased to 100% while the availability of diagnostics remained low. Although malaria treatment was affordable, the price of diagnostics remained stagnant and increased the cumulative cost of malaria management. Malaria stakeholders should consolidate the gains made and consider the inclusion of diagnostic kits in the subsidy programme.

Similar content being viewed by others

Background

In 2017, the World Health Organization (WHO) African Region contributed 92% of the estimated 219 million cases of malaria that occurred worldwide [1]. Uganda has the third-highest global burden of malaria cases and contributes to 18% of the malaria cases in East and Southern Africa [2]. Malaria is highly endemic in 95% of Uganda and is the third leading cause of mortality in the country, after neonatal disorders and HIV/AIDS [3]. Pregnant women and children under 5 years of age are the most vulnerable population to malaria [4].

Early diagnosis and treatment of malaria contributes to a reduction in malaria transmission, disease burden and prevents deaths. Universal access to anti-malarial treatment is one of the key strategies of the WHO’s Global Technical Strategy for Malaria 2016–30 aiming to reduce malaria mortality rates by at least 90% by 2030 [5].

In 2006, the WHO recommended the use of artemisinin-based combination therapy (ACT) as the first-line treatment for uncomplicated malaria in the effort to address resistance of Plasmodium falciparum to monotherapies and improve treatment outcomes [6]. By 2009, there were concerns about access to quality-assured ACT medicines in many low-income countries (LMICs) that were grappling with a high burden of malaria, especially among the poorest people [7]. Low-cost medicines, for example, chloroquine and sulfadoxine, were widely available and heavily relied on for treatment of uncomplicated malaria, particularly in the private sector outlets [8, 9]. Unfortunately, however, these medicines had gradually become ineffective against malaria parasites. In addition, non-artemisinin-based therapies, artemisinin monotherapies, and low-quality artemisinin-based combinations were widely available [10].

The private sector plays a key role in the fight against malaria [11,12,13]. In Uganda, the private sector is the preferred first point of contact for about 61% of households [14]. One of the key barriers of access to quality assured anti-malarial treatment is the high price for ACT medicines and malaria Rapid Diagnostic Tests (RDTs) [15]. Price is a major contributor to limited access to medicines because of its impact on affordability, especially for poor people [16]. By 2009, there were few available brands of ACT medicines in the private sector, most of them unaffordable. For example, it was not uncommon to find a dose of a quality-assured, first-line ACT medicines in private sector outlets retailing at six to 21 times higher than the most commonly sold anti-malarial monotherapy regimens (often non-artemisinin-based in composition) [17].

Furthermore, there were equity concerns; children treated for malaria in the public sector were significantly more likely to receive ACT medicines than those treated in the private sector facilities [7].

As a result, initiatives such as the Global Fund’s (GF) Affordable Medicines Facility-malaria (AMFm) pilot in 2011 and later the private sector co-payment mechanism (CPM) in 2013 were implemented to improve access to ACT in the private sector through subsidies. Subsidies supported by interventions to improve demand are important for improving the availability and affordability of ACT medicines in the private-for-profit sector [18]. The AMFm pilot comprised of three components to promote the appropriate use of ACT in the public, private-for-profit and private-not-for-profit sectors. These components were: price reductions through negotiations with prequalified ACT medicines manufacturers to offer 90% price subsidy to selected importers, support of interventions, such as behaviour change communication and establishment of price monitoring [19]. In December 2013, the AMFm programme was rebranded to the CPM to focus only on the private sector [20] and offered a 70% price subsidy for ACT medicines, but not for RDTs [21]. These efforts were expected to culminate into a trickledown effect of reduced ACT medicines prices in the anti-malarial supply chain to the end user. Details of the CPM are outlined elsewhere [21, 22]. Table 1 lists the interventions conducted.

Whereas the report on the effect of the multi-country (including Uganda) AMFm pilot was published in 2012 under the ACTwatch group [18,19,20,21,22, 25, 26], there is a paucity of evidence relating to access to anti-malarials prior to and beyond the end of the AMFm pilot. Between 2008 and 2018, the Global Fund disbursed a cumulative total of USD 414,963,377 for strategies to improve access to anti-malarial commodities in Uganda [27]. Despite these continued efforts to support access to anti-malarial commodities in Uganda, there are limited data to show whether the initially observed positive effects were sustained in later years. This paper examines trends in availability and affordability of first-line malaria treatment and diagnostics in Uganda between 2007 and 2018.

Methods

A cross-sectional design with quantitative methods was used to assess the availability, price and affordability of ACT medicines and diagnostics using a standardized methodology co-developed by the WHO and Health Action International (HAI), adapted for anti-malarials and diagnostics [28]. This methodology prescribes a minimum of 30 facilities per sector and has been validated and used widely [29,30,31,32].

Annual studies were conducted prior to 2016 and in 2018 while quarterly studies were conducted for the period of October 2016 to Dec 2017. However, the 2007–2010, and 2014–2015 surveys did not measure the availability and prices of RDTs.

Selection of survey areas and medicine outlets

Data was collected from six regions in the country: Central, Eastern, Western, Northern, Southern and West Nile. The regions were selected as a realistic representation of the geographical characteristics of the country. One major town within one day’s car travel from the capital city was selected from each of the regions. The facilities surveyed were randomly sampled.

In each region, the main public hospital was used as an anchor from which private medicine outlets were selected within 3 h travel of the hospital. The final list of outlets surveyed was approved by the National Malaria Control Programme (NMCP). Only registered drug outlets were considered in the survey. The official list of registered pharmacies from the national medicines’ regulatory agency (National Drug Authority) was used to locate, select and verify registration status. Table 2 shows the sample frame for the surveys.

Surveyed ACT medicines and RDTs

A list of ACT medicines and RDTs was developed including the formulation and strength of each medicines. This paper however focuses on artemether/lumefantrine (A/L), adult 24 tablet pack, which is the first line recommended treatment for uncomplicated malaria [1] and also has the largest market share of ACT medicines in Uganda and was the main first line anti-malarial consistently surveyed in all the years [9, 33].

Data collection

Data collection teams of six persons per region worked in pairs composed of a pharmacist and social scientist. The teams were coordinated by a regional supervisor who was a pharmacist by profession. Prior to data collection, survey personnel participated in the training. One key respondent was targeted for the survey at health facility level; either the in-charge, attendant, owner or any suitable person delegated by the in-charge/owner. The respondents included medical doctors, clinical officers, nurses, nursing assistants, midwives, pharmacists and dispensers.

For each medicine available at the outlet on the day of the visit, data collectors recorded: the brand names of two products; the highest and lowest priced medicine in Uganda Shillings (UGX); the strength and price found. Any discounts or other considerations affecting the price to patients were documented. Originator medicines were included if found available.

Each regional supervisor checked all the filled data collection forms for completeness, legibility and consistency, at the end of each day and validated the data collected in 10% of the sample outlets in the region. In addition, the survey manager checked all the data collection forms for completeness and consistency. Data entry was done into an expanded standardized WHO/HAI International Price workbook with multiple quality assurance processes; for example, double entry of the unit prices and use of the workbook’s inbuilt data checking process.

Data analysis

Computation of medicine availability, prices and affordability was done according to the WHO/HAI methodology [28]. The availability of A/L was calculated as the percentage of sampled medicine outlets where the medicine was found on the day of the visit. For 2017 where quarterly studies were conducted, the annual average was taken.

The median, minimum and maximum patient prices were estimated for A/L and RDT patient prices. Medicine prices obtained during the survey were expressed as ratios relative to a standard set of international reference prices by dividing the median local unit price by the international reference unit price [34]. Medicine price ratios (MPRs) were calculated only if price data from at least four medicine outlets were available. The medicines prices (in UGX) were converted into US dollars (USD) using the prevailing mid-month exchange rates taken from the Bank Uganda website on the first day of data collection [35]. Affordability was assessed by estimating the number of daily wages required for one course of treatment using the daily salary of the lowest-paid government worker (LPGW) in Uganda, for the respective survey year [36].

Results

Availability of A/L and RDTs

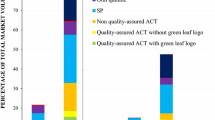

Between 2007 and 2018, the availability of A/L in the private sector facilities gradually increased from 85 to 100%. There was an increase in availability of A/L from 85 to 93% between 2007 and 2009, from which it thereafter dropped from 93 to 75% between 2010 and 2013. However, A/L availability increased from 75 to 94% between 2013 and 2014, then later peaking at 100% in 2017 and 2018. Overall, low availability of RDTs was noted despite the rise from 13% to 2012 to 37% in 2018. Trends in availability of A/L and RDTs are shown in Fig. 1.

Trends in availability of A/L and mRDTs in the private sector in Uganda

Patient prices and affordability of A/L and RDTs

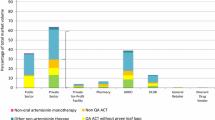

There was a gradual reduction in prices of A/L from a high of USD 8.8 in 2007 to a stable USD 1.1 between 2016 and 2018, while the price of RDTs was mostly consistent at USD 0.5. There was an increment in the prices for A/L from USD 1.7 and USD 2.3 between the end of the AMFm in 2012 and just before the introduction of the CPM in 2013. Affordability of A/L gradually dropped from 4 days’ wages in 2008 to half-a-day’s wages in 2018. Affordability of RDTs improved from about 0.6 in 2012 to about 0.3 days’ wages for LPGW by 2018. Trends in prices and affordability of A/L and RDTs are shown in Fig. 2.

Trends in prices (in USD) and affordability of A/L and mRDTs in private facilities in Uganda

Discussion

This paper presents trends in the availability, prices and affordability of first line anti-malarial treatment and diagnosis in the private sector in Uganda between 2007 and 2018. There was high availability of first line treatment A/L: at least nine of every ten private medicine outlets surveyed were found with A/L in stock reaching 100% availability in 2018. However, availability of RDTs remained below 40%. There was also a marked reduction in prices of A/L during the period from USD 8.8 to USD 1.1, but price of RDTs remained mostly stagnant at USD 0.5. Affordability of an adult dose of ACT medicine improved from 4 days’ wages to 0.5 days’ wages of the LPGW, and affordability of RDTs remained at about 0.3 day’s wages for LPGW.

Findings from this study are consistent with those reported from a similar programme by ACTwatch that reported an increase in availability of RDTs between 2009 and 2015, but availability remained lower in the private sector compared to the public sector in countries where AMFm programme was administered by the Global Fund [9]. The findings not only focus on RDTs but include ACT medicines, cover a longer period and confirm a sustained effect of the programme in Uganda.

There was a decline in the availability of A/L between 2010 and 2013 dipping below the 80% WHO benchmark in 2013, which may be the result of the high volatile prices of ACT medicines on the market after the introduction of AMFm [21, 37]. After 2013, availability of A/L gradually improved to 100% which could be attributed to consistent supply together with support interventions such as behaviour change communication to improve demand and price monitoring to study changes in the private sector [38]. The changes observed could have been influenced by increased generic competition which led to a reduction in prices of the ACT medicines. It is important to also note that supporting activities to increase awareness about malaria treatment guidelines by health practitioners in the private sector, as well as continuous stakeholder engagements at all levels was helpful [33]. Health system actors particularly in the public sector should therefore learn from and scale up this experience.

Parasitological confirmation particularly with RDTs at community level is important to reduce unnecessary treatment with anti-malarial drugs and to improve the diagnosis of other febrile illnesses. However, availability of RDTs improved slightly over the study period but remained low (below 40%) due to the fact that there were no incentives geared towards making the commodity more available and affordable. Also, contextual aspects such as RDTs being regarded in the private sector as a product sale and not a paid service may have played a role [38]. The high RDT prices push the overall price of malaria diagnosis and treatment to nearly one day’s wages for LPGW. This makes starting treatment almost unaffordable—the WHO benchmark for affordability is 1-day wages [28]—which may lead to suspected malaria patients being treated without confirmatory tests. This is a bottleneck towards successful optimization for the ‘Test, Treat and Track’ Policy for malaria in the private sector [39]. Administering the anti-malarial medicines without a confirmed positive diagnosis may, in the long run, expose the patient to development of resistant strains of the Plasmodium as well as the wastage of resources, especially in case the patient does not have malaria [40, 41].

Cumulatively, enormous investments have been made towards malaria control in Uganda, contributing towards improved availability of commodities and the gradual decline of burden of mortality in the country [42,43,44]. An estimated 90% of the Global Fund grants are annually spent on the procurement of medicines and health commodities [45]. However, disbursement for malaria control interventions was relatively stagnant between 2007 and 2018, with the exception of 2015 when the private sector CPM’s supportive interventions were also implemented to meet the growing demand for the medicines [39, 45]. Consistent and sufficient financing of all recommended strategies is important to ensure elimination of malaria.

The marked reduction in prices of A/L over the review period may warrant further investigation but was largely attributed to global and national efforts aimed at making the products more affordable. In addition, improved access to cheap generics led to increased price competition in the market which improved affordability of treatment of acute malaria. Furthermore, the Ministry of Health of Uganda in 2016 instituted an initiative to regulate the prices of ACT medicines on the private sector market by setting a Recommended Retail Price (RRP) for the ACT medicines (by pack size) which could also have influenced the stability of A/L prices. It should be noted that the prices of ACT medicines remained stable at USD 1.1 between 2016 and 2018, which may further demonstrate that a combination of subsidies, support interventions and price capping policy initiatives could be effective towards ensuring affordability and sustainable access to medicines [46]. However, this RRP was higher than that set earlier on during the AMFm pilot of USD 0.47 for an adult dose of ACT medicine [25].

The anti-malarial market still faces other challenges including uncertainty about the quality of the anti-malarial medicines and RDTs, market speculations at the end of the CPM funding rounds which force hoarding of products by wholesalers and absence of health insurance for majority of the vulnerable populations. In addition, there are concerns about the sustainability of the gains made by the CPM given that the programme is largely donor-funded and there are minimal strategies in place for business continuity in case donor funding ceases, as well as plans to absorb any possible after-shocks [47]. On the other hand, the results observed in this study present opportunities for learning from the private sector that can be utilised for the public sector.

This assessment has been made using a standardized, tested, reliable, and validated WHO/HAI methodology that has been used widely across the world for the measurement of access to medicines [29]. The WHO/HAI methodology uses a cross-sectional design but this assessment provides a longitudinal view of historical trends over a period of 12 years which increases reliability. The assessment is based on several studies conducted annually or quarterly and, therefore, used different samples. This should not be a problem because the standard WHO/HAI methodology recommends thirty outlets in a sector for a survey to achieve enough data points for analysis [29], which was achieved in all years. The findings presented here are not intended to give a full view of the country’s pharmaceutical supply chain but to stimulate policy discussions. The study was conducted in the formal private sector and therefore informal/unlicensed facilities which mainly offer treatment to the majority of the rural population were not included. Also, the study does not explore various supply chain and socio-economic factors which affect availability and affordability.

Conclusions

Subsidies to the private sector have had a positive impact on the availability and affordability of A/L that should improve malaria management especially among the vulnerable population of pregnant women and children. However, future considerations could be made towards providing subsidies for RDTs in the private sector to improve affordability of the cumulative cost of the test and treatment of malaria.

Availability of data and materials

The datasets used and/or analysed are available on request from the corresponding author.

Abbreviations

- ACT:

-

Artemisinin-based combination therapy

- RDTs:

-

Malaria rapid diagnostic tests

- GF:

-

Global Fund

- AMFm:

-

Affordable Medicines Facility-malaria

- CPM:

-

Private sector co-payment mechanism

- A/L:

-

Artemether/lumefantrine

References

WHO. World malaria report. Geneva: World Health Organization; 2018.

WHO. World malaria report. Geneva: World Health Organization; 2016.

Institute for Health Metrics and Evaluation. Global Burden of Disease Data, in Country profile-Uganda. Institute for Health Metrics and Evaluation; 2017.

Ministry of Health (MoH). The Uganda Malaria Reduction Strategic Plan (2014–2020): accelerated nationwide scale up to achieve universal coverage of cost effective malaria prevention and treatment interventions. Kampala; 2014.

WHO. Global technical strategy for malaria 2016–2030. Geneva: World Health Organization; 2015.

WHO. Guidelines for the treatment of malaria. Geneva: World Health Organization; 2006.

Littrell M, Gatakaa H, Evance I, Poyer S, Njogu J, Solomon T, et al. Monitoring fever treatment behaviour and equitable access to effective medicines in the context of initiatives to improve ACT access: baseline results and implications for programming in six African countries. Malar J. 2011;10:327.

Newton PN, Hanson K, Goodman C. Do anti-malarials in Africa meet quality standards? The market penetration of non quality-assured artemisinin combination therapy in eight African countries. Malar J. 2017;16:204.

ACTwatch PSI. Malaria market trends in sub-Saharan Africa: 2009–2016. Population Services International and ACTwatch; 2017.

IFC International. Multi-Country Baseline Report: Independent evaluation of the Affordable Medicines Facility - malaria (AMFm) Phase 1. The Global Fund to Fight AIDS, Tuberculosis, and Malaria; 2012.

Davis B, Ladner J, Sams K, Tekinturhan E, de Korte D, Saba J. Artemisinin-based combination therapy availability and use in the private sector of five AMFm phase 1 countries. Malar J. 2013;12:135.

Sabot OJ, Mwita A, Cohen JM, Ipuge Y, Gordon M, Bishop D, et al. Piloting the global subsidy: the impact of subsidized artemisinin-based combination therapies distributed through private drug shops in rural Tanzania. PLoS ONE. 2009;4:e6857.

Kedenge SV, Kangwana BP, Waweru EW, Nyandigisi AJ, Pandit J, Brooker SJ, et al. Understanding the impact of subsidizing artemisinin-based combination therapies (ACTs) in the retail sector–results from focus group discussions in rural Kenya. PLoS ONE. 2013;8:e54371.

UBOS. Uganda national household survey 2016/17. Kampala: Uganda Bureau of Statistics; 2017.

Palafox B, Patouillard E, Tougher S, Goodman C, Hanson K, Kleinschmidt I, et al. Prices and mark-ups on antimalarials: evidence from nationally representative studies in six malaria-endemic countries. Health Policy Plan. 2015;31:148–60.

WHO. Medicines strategy 2008–2013. Geneva: World Health Organization; 2008.

O’Connell KA, Gatakaa H, Poyer S, Njogu J, Evance I, Munroe E, et al. Got ACTs? Availability, price, market share and provider knowledge of anti-malarial medicines in public and private sector outlets in six malaria-endemic countries. Malar J. 2011;10:326.

Tougher S, Ye Y, Amuasi JH, Kourgueni IA, Thomson R, Goodman C, et al. Effect of the Affordable Medicines Facility—malaria (AMFm) on the availability, price, and market share of quality-assured artemisinin-based combination therapies in seven countries: a before-and-after analysis of outlet survey data. Lancet. 2012;380:1916–26.

Morris A, Ward A, Moonen B, Sabot O, Cohen JM. Price subsidies increase the use of private sector ACTs: evidence from a systematic review. Health Policy Plan. 2015;30:397–405.

The Global Fund. Operational Policy Manual. Operational Policy note: Private Sector Co-Payment Mechanism for ACTs. The Global Fund, Geneva; 2017.

Tougher S, Hanson K, Goodman C. What happened to anti-malarial markets after the Affordable Medicines Facility-malaria pilot? Trends in ACT availability, price and market share from five African countries under continuation of the private sector co-payment mechanism. Malar J. 2017;16:173.

Opiyo N, Yamey G, Garner P. Subsidising artemisinin-based combination therapy in the private retail sector. Cochrane Database Syst Rev. 2016;3:CD009926.

Ministry of Health. National Policy on Malaria Treatment. Kampala: Ministry of Health; 2005.

WHO. Guidelines for the treatment of malaria. Geneva: World Health Organization; 2010.

Kaula H, Buyungo P, Opigo J. Private sector role, readiness and performance for malaria case management in Uganda, 2015. Malar J. 2017;16:219.

Palafox B, Patouillard E, Tougher S, Goodman C, Hanson K, Buyungo P, et al. ACTwatch 2009 Supply Chain Survey Results, Uganda. Nairobi: ACTwatch project, Population Services International; 2012.

The Global Fund. Global Fund Disbursements updated 2020. Available from: https://data-service.theglobalfund.org/downloads.

WHO. Measuring medicine prices, availability, affordability and price components. Geneva: World Health Organization; 2008.

Madden JM, Meza E, Ewen M, Laing RO, Stephens P, Ross-Degnan D. Measuring medicine prices in Peru: validation of key aspects of WHO/HAI survey methodology. Rev Panam Salud Pública. 2010;27:291–9.

Cameron A, Mantel-Teeuwisse AK, Leufkens HG, Laing RO. Switching from originator brand medicines to generic equivalents in selected developing countries: how much could be saved? Value Health. 2012;15:664–73.

Anson A, Ramay B, de Esparza AR, Bero L. Availability, prices and affordability of the World Health Organization’s essential medicines for children in Guatemala. Glob Health. 2012;8:22.

Cameron A, Bansal A, Dua T, Hill SR, Moshe SL, Mantel-Teeuwisse AK, et al. Mapping the availability, price, and affordability of antiepileptic drugs in 46 countries. Epilepsia. 2012;53:962–9.

HEPS-Uganda. Assessing Access to Co-Paid Artemisinin-Based Combination Therapies for Malaria in Uganda. Kampala: Coalition For Health Promotion and Social Development (HEPS-Uganda); 2017.

Management Sciences for Health. International Drug Price Indicator Guide. Arlington, USA: 2014.

Bank of Uganda. Exchange Rates. 2016. https://www.bou.or.ug/bou/collateral/exchange_rates.html.

Ministry of Health. Essential Medicines and Health Supplies List of Uganda. Kampala: Ministry of Health; 2016.

Kangwana BP, Kedenge SV, Noor AM, Alegana VA, Nyandigisi AJ, Pandit J, et al. The impact of retail-sector delivery of artemether–lumefantrine on malaria treatment of children under five in Kenya: a cluster randomized controlled trial. PLoS Med. 2011;8:e1000437.

Carland C, Goentzel J, Montibeller G. Modeling the values of private sector agents in multi-echelon humanitarian supply chains. Eur J Operational Res. 2018;269:532–43.

Okungu V, Mans J. efficiency, equity, and effectiveness of malaria funding in Uganda: making the case for reforming public financing for health. Int J Health Serv Res Policy. 2019;4:131–44.

Thu AM, Phyo AP, Landier J, Parker DM, Nosten FH. Combating multidrug-resistant Plasmodium falciparum malaria. FEBS J. 2017;284:2569–78.

Bruxvoort K, Goodman C, Kachur SP, Schellenberg D. How patients take malaria treatment: a systematic review of the literature on adherence to antimalarial drugs. PLoS ONE. 2014;9:e84555.

Dillon A, Friedman J, Serneels P. Health information, treatment, and worker productivity: experimental evidence from malaria testing and treatment among Nigerian sugarcane cutters. The World Bank; 2014.

Renschler JP, Walters KM, Newton PN, Laxminarayan R. Estimated under-five deaths associated with poor-quality antimalarials in sub-Saharan Africa. Am J Trop Med Hyg. 2015;92(Suppl 6):119–26.

Kenangalem E, Poespoprodjo JR, Douglas NM, Burdam FH, Gdeumana K, Chalfein F, et al. Malaria morbidity and mortality following introduction of a universal policy of artemisinin-based treatment for malaria in Papua, Indonesia: A longitudinal surveillance study. PLoS Med. 2019;16:e1002815.

The Global Fund. Audit Report: Global Fund Grants to the Republic of Uganda. Geneva, Office of the Inspector General, The Global Fund; 2016.

Tougher S, Mann AG, Group A, Ye Y, Kourgueni IA, Thomson R, et al. Improving access to malaria medicine through private-sector subsidies in seven African countries. Health Aff. 2014;33:1576–85.

Orsi F, Singh S, Sagaon-Teyssier L. The creation and evolution of the donor funded market for antimalarials and the growing role of southern firms. Sci Technol Soc. 2018;23:349–70.

Acknowledgements

The authors acknowledge the data collection teams led by Denis Kibira and Anthony Ssebagereka. We appreciate Daphne Ssebugwawo who edited the manuscript.

Funding

This research did not receive any funding.

Author information

Authors and Affiliations

Contributions

DK conceptualized the research, wrote the first draft, AS undertook data analysis and contributed to manuscript drafting; HAH, JO, HK, MS, TR, HL and AM revised the manuscript and critically reviewed its contents. AM critically reviewed the manuscript, provided comments and guidance on all drafts of manuscript. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethical approval and consent to participate

The annual surveys were conducted to inform Ministry of Health (MoH) programming. MoH provided approval for the surveys and introduction letters to health facilities for the data collectors. Ethical approval was not necessary given that human subjects were not involved.

Consent for publication

Not applicable.

Competing interests

All authors declare no competing interests.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/. The Creative Commons Public Domain Dedication waiver (http://creativecommons.org/publicdomain/zero/1.0/) applies to the data made available in this article, unless otherwise stated in a credit line to the data.

About this article

Cite this article

Kibira, D., Ssebagereka, A., van den Ham, H.A. et al. Trends in access to anti‐malarial treatment in the formal private sector in Uganda: an assessment of availability and affordability of first‐line anti‐malarials and diagnostics between 2007 and 2018. Malar J 20, 142 (2021). https://doi.org/10.1186/s12936-021-03680-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s12936-021-03680-8