Abstract

With the rapid development of its national economy, China has become a major producer and consumer of energy. To guarantee the sustainable development of power industry and national economy, China should exploit fossil and renewable energy efficiently according to the development situation of generation resources. Firstly, this paper analyzes the utilization status of main generation resources in China, such as coal, hydropower and wind energy. Secondly, this paper illustrates the STEP model, which analyzes some issues for China’s generation resource utilization from political, economic, social and technological aspects. For example, the resource distribution is inconsistent with electricity demand, the renewable energy power output is intermittent, and there is some disruption in coal mining. Finally, combined with the utilization status and issues, this paper presents some improvement approaches from the perspectives of cost, efficiency and external influence.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Generation resources refer to the resources used for power generation, which include fossil energy and non-fossil energy resources in China. Among them, fossil energy resources mainly include coal and natural gas, while non-fossil energy sources consist mainly of nuclear power, hydropower, wind power, and solar power.

1.1 Background

In recent years, the energy demand has been increasing significantly. Power energy will play an important role in energy structure adjustment and sustainable development.

With the rapid development of economy, the healthy development of electric power will provide a powerful mechanism for sustainable development [1]. China’s energy consumption has been dominated by coal for a long time. Although the distribution of productivity and the distribution of energy resources are not matching, China is vigorously promoting the development of ultra-high voltage (UHV) transmission technology to achieve sustainable development of electric power [2].

The main strategy for developing generation resources in China is to optimize the coal industry structure and to develop nuclear power, hydropower, wind power and other renewable energy sources vigorously. Emission reductions from the energy sector will be promoted by increasing fossil energy quality and clean energy generation proportion [3]. At the same time, the Chinese government will strengthen the development of generation resources to coordinate the integration of renewable energy, promote the construction of the smart grid, and develop energy storage technology [4–6].

To reduce carbon emissions, developed countries attach great importance to the utilization of renewable energy. Chinese policy is that by 2020, the coal utilization proportion will be substantially reduced, coal consumption will peak by 2030, and clean coal technology will be well developed. External cost of coal utilization will be consequently reduced, ensuring sustainable growth of the economy [7, 8].

In this paper, based on the view of sustainable development, the issues and solutions of generation resource utilization in China are analyzed. Firstly, a literature review is conducted in the latter part of Section 1. Section 2 introduces the current situation of China’s generation resource utilization, which focuses on coal, wind and hydropower. Further, the existing issues in generation resource utilization are enumerated by introducing the STEP model in Section 3, with a detailed analysis of each problem. For the issues in Section 3, the solutions are put forward in Section 4 considering the aspects of cost, efficiency and externality. Section 5 concludes this paper.

1.2 Literature review

1.2.1 Research status outside China

The reformation of power systems in the world has focused on problems of low carbon technologies, environmental protection, clean energy, and green development. To address climate change and emission reduction, new electricity market and power industry reforms are studied, and renewable energy market mechanisms are explored around the world [9].

At present, the exploitation of hydro-power generation resources in developed countries has already achieved a high level, hence the exploitation of renewable energy is focused on solar energy, wind energy, geothermal and biomass power. However, renewable energy power generation (except for hydropower) is held back by lack of large investment, high cost and power intermittency, so renewable energy utilization will not be greatly increased before 2020 [10].

In Britain, the government has already established a series of laws and regulations to promote the development of renewable resources, such as the Non Fossil Fuel Convention and Electricity Law. Subsequently, the concept of renewable energy obligation exists in Britain, which provides credits for power companies engaged in renewable energy to realize sustainable development [11].

India is one of the earliest countries to carry out an electricity market reform. To influence generation resource utilization, electricity transactions are subject to price control of renewable energy generation, and the Renewable Electricity Certificate mechanism is used to improve the business case for renewable energy [12].

The United States was the major energy consumer in the world, mainly using coal, oil and natural gas. However, the renewable energy proportion of U.S.A. in 2013 was two times more than the proportion in 1993, showing the great importance that has been attached to the development of renewable energy [13].

1.2.2 Research status in China

In China, coal utilization is dominant in generation resources, which has brought serious environmental pollution. To guarantee and promote the low-carbon economy, environmental protection and sustainable development, new energy resources should be actively developed and priority given to developing hydropower, wind power and solar energy. Additionally, the efficient development of nuclear power is also necessary [14].

For the comprehensive utilization of generation resources, some scholars have conducted in-depth research in China. Litong DONG (2013) studied the comprehensive planning of generation resources, energy management, and power generation transaction [15]. Shuxiang WANG (2013) discussed the optimization model and method of comprehensive utilization for generation resources with emission reduction constraints, analyzed from generation side and the demand side, considering the linkage of these two sides [16].

In addition, Dudu LIU (2014) believed the development of smart power technology will be the key trend of the electricity industry, having an important role to promote the rational allocation and improve the utilization rate of generation resources [17]. Qingyou YAN (2013) analyzed a balanced development problem comprising environment, economy, and power by the way of system dynamics, so as to find a method to solve generation resources shortage [18].

2 Utilization status

During the 21st century, electricity demand has been growing in China with an unprecedented speed and the scale is continually expanding, so power grid construction has been continuous and will provide a solid foundation for the developing electricity market. Only a sound power market mechanism can promote the efficient use of electricity [19].

At present, the energy sources for power generation in China include coal, natural gas, wind, solar, nuclear energy, and biomass energy. By the end of 2015, the total installed capacity of China reached 1.5 TW, which increased 9.8% compared with 2014. The power generation capacities for various types of energy are shown in Table 1.

From Table 1, we can see the total installed capacity of thermal power was 990 GW in 2015, with a proportion of 65.9% in total installed capacity and an increase of 7.9% compared to the year before. The total installed capacity of hydropower is 320 GW, with a proportion of 21.3% and an increase of 5.5%. And the capacity of grid-connected wind power is 129 GW, with an increase of 34.4% compared with the last year. Additionally, the installed capacity of renewable energy accounted for 32.3% of the total.

The total installed capacity for thermal, hydro and wind power is more than 95% in 2015 in China, so the generation resources we analyze in our paper mainly refer to the utilization of coal, hydro and wind.

2.1 Utilization status of fossil energy

2.1.1 Coal resource

China’s coal resources are widely distributed. The overall pattern of geographical distribution is that coal resources are abundant in the east and the north of China.

Coal resources are mainly concentrated in the north of China. In 2014, coal reserves of north China accounted for 46.09% of the national reserves, followed by the Northwest, accounting for 39.98%, the remaining are distributed in the east, the central south region and the northeast of China. According to our calculation, coal is mainly distributed in Inner Mongolia autonomous region, Xinjiang autonomous region, Shaanxi province, Shanxi province, Ningxia province and Guizhou province, collectively accounting for about 81.6% of the national reserves. On the basis of the fourth coal forecast [20], Inner Mongolia autonomous region and Xinjiang autonomous region have the largest proven coal reserves, and followed by Shanxi province.

With the decrease of utilization proportion in coal resource, thermal power investment was 95.2 × 109 ¥ in 2014, continuing a declining trend since 1996. For the decline of coal price and technical progress, the new installed capacity was 72.62 GW in 2015, with an increase of 53.56% compared to the last year. The national thermal power installed capacity was 990 GW.

In 2015, China’s coal market demand continued to slump. The annual coal consumption dropped by 3.7% compared to 2014, while coal production continued to decrease, and the annual coal import was 204 million tons which was down by 30%. The coal inventory of key power plants in China was about 73.58 million tons by the end of 2015, which would be sufficient for 22 days.

According to “Twelve Five-Year Plan about Coal Industry Development” in China, in 2015, coal production capacity should be reached 4.1 billion tons per year [21]. Among them, large coal mine would be reached 2.6 billion tons per year, accounting for 63% of the total capacity, and medium-sized coal mine would be reached 0.9 billion tons per year, accounting for 22%, and production capacity of small coal mine would be controlled in 0.6 billion tons, accounting for 15%. Actually, it has been realized.

2.1.2 Natural gas

In China, demand for natural gas is very strong, especially with increasing control of air pollution, with many regions showing extraordinary growth. Annual gas consumption is growing faster than production, so gas supply is very tight, and ensuring supply for the peak gas consumption in the winter heating period seems to be difficult [22].

To ensure the safe use of gas, gas turbine supply is restricted. For the sake of protecting the gas supply, China raised the price of natural gas for non-residents, but the country has not formed a unified mechanism of gas turbine power generation price, and some enterprises continue to experience losses due to generation cost increase and inadequate local subsidies.

2.1.3 Other resources

In addition to coal and natural gas, there are some power plants using petroleum products. Oil generation has high pollution and is not a sustainable business, so the proportion of installed capacity has decreased greatly during nearly ten years, and was less than 0.2% in 2015.

2.2 Utilization status of renewable energy

2.2.1 Hydropower

China has abundant water resources, with the highest total amount in the world. According to our survey, by the end of July 2015, the generation output of hydropower was 534.8 TWh, an increase of 9.6% compared to the last year.

Because of the large difference between topography and rainfall in China, the geographical distribution of hydropower is unbalanced, with most distributed in the west of China. In addition, China is located in southeastern Asia and is on verge of the world’s largest ocean, which causes a characteristic monsoon climate. Thus, the runoff distributions of most rivers are uneven throughout a year and seasonal flow becomes disparate, so high-performance regulating reservoirs need to be constructed.

Water resources are concentrated in main streams, which is convenient for centralized development. By the end of 2015, the total installed capacity was about 320 GW. In downstream Jinsha River and upstream Yangtze River, the total installed capacities are 58.58 GW and 33.20 GW, respectively. Additionally, the installed capacities around Dadu River and upstream Yellow River are larger than 20 GW each, and the installed capacities around Wujiang, Nanpanjiang and Hongshui Rivers are more than 10 GW each [23].

As one of the renewable energy sources, hydro energy will become a focus in future power construction. In 2015, China’s new installed capacity of hydropower reached 16.71 GW.

According to “Twelve Five-Year Plan about Hydropower Development” in China, hydropower should increase from 120 GW to 194 GW during 2011–2015 to achieve the proportion (non-fossil energy share of total primary energy consumption) of 11.4% in 2015 and 15% in 2020 [24].

2.2.2 Wind power

The wind power market in China is growing fast and has become the largest one in the world. According to statistics from the World Wind Energy Council, the compound annual growth rate (CAGR) for global cumulative installed capacity of wind power was 23.45% during 2001–2014, and at the same time, the CAGR in China was 42%, ranking first in the world [25].

The wind resource is mainly concentrated in the northern region, the southeast coastal area, and the nearby islands. The wind power density in northern area is about 200~300 W/m2 per year, some area is even up to 500 W/m2. The wind power density in southeast coastal region is more than 200 W/m2 per year, and the wind power density line is parallel to the coast.

The wind power generation has become a fast growing industry in the background of global energy shortage, serious environmental pollution and the increased demand for renewable energy. In 2015, the total installed capacity of grid connected wind power was 129 GW, an increase of 12.25 GW over the previous year. By the end of 2015, the wind power installed capacity was 129.34 GW, with a growth of 35.0% compared to the last year. However, the annual wind power equipment utilization hours were 1728 h, which dropped by 172 h over the previous year, because the development of the national transmission grid has not kept up with the development of wind power.

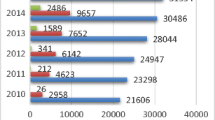

The National Energy Administration has declared that the minimum target of wind power development in the Thirteenth Five-Year Plan (2016–2020) will be 200 GW. This means the annual new installed capacity of wind power in China will be up to 20 GW. According to the planning in the Thirteenth Five-Year Plan, new installed capacity of wind power in China will be up to 100 GW during 2016–2020. Among them, new installed capacity in the northwest and the northeast will be 60 GW. New installed capacity will be 30 GW in the central east and 10 GW in offshore [26]. The future development of China’s wind power is described in Fig. 1.

Future development potential of wind power in China

2.2.3 Other resources

In addition to water and wind resources, there are other renewable energy sources for power generation in China, such as solar energy and biomass energy, but those generation resources have low proportion in China. For example, total installed capacity of solar power accounted for only 2.37% in 2015 from the Table 1, though the photovoltaic capacity of China has also ranked No. 1 in the world. The utilization proportion of other renewable energy is not high, but renewable energy will be developed continuously in the coming decades.

3 Existing issues

We illustrate the STEP model in our paper to analyze such problems as China’s generation resource utilization. Based on macroscopic angles, the STEP model presents an analysis framework with respect to political, economic, social, and technological factors. The analysis of the political aspect includes the political system, policy, laws and regulations in relevant countries or regions. The analysis of the economic aspect includes market competition and industry environment according to the domestic economic situation and developmental trend. The analysis of the social aspect includes societal factors, including cultural traditions, values and social structure. Finally, the technology aspect we will study later includes the social technology level and trend, the influence of technological breakthroughs and technical change.

This paper analyzes the issues of generation resource utilization from these four dimensions as shown in Fig. 2.

STEP model analysis

3.1 Issues of fossil energy

3.1.1 Uneven distribution of coal resources

The uneven distribution of fossil energy results in high transport cost. The inconsistency of coal production and consumption has been studied by replacing coal demand with power demand, ignoring consumption of coal outside the power sector. A Lorenz curve is fitted according to the cumulative percentage of power consumption and coal production in respective provinces. Consequently, the uneven distribution degrees can be analyzed, as illustrated in Fig. 3 [27].

Provincial coal production and consumption cumulative proportion

If \(\lambda_{i}\) is the cumulative power consumption of the i th province, and θ i is the cumulative coal production, then the Gini coefficient measures the equity of coal production and power consumption across provinces:

The graph of Gini coefficient is the crooked line in Fig. 3. A coefficient of 0 expresses perfect equality among provinces, while 1 would mean that production and consumption are completely disparate.

From the Fig. 3, when the coal production and consumption is in a balanced distribution, the Lorenz curve should be a straight line as it shows in the figure. However, the practical Lorenz curve is the crooked line in Fig. 3, which significantly deviates from the straight line. Therefore, provincial coal production and consumption has an unbalanced distribution in China, hence there is a severe inconsistency in the distribution of coal and the distribution of electricity demand.

3.1.2 Incomplete policy and regulation of coal utilization

Coal utilization policies and regulations are still imperfect, as illustrated in Table 2.

3.1.3 Technical barriers of power generation

Due to the serious environmental situation in China, the development of a low-carbon economy with improved of energy efficiency and reduced emissions have become a major requirement for sustainable development. According to our statistics, Fig. 4 presents the total and per capita carbon emissions in China from 2005–2014.

Carbon emissions and per capita carbon emissions during 2005–2014 in China

Because the thermal power is still the main power resource in China, how to apply the clean and environmental technology for thermal power generation has become an important topic.

At present, China’s main direction of technical development in thermal power industry is to maximize production efficiency and to use generation technology of high efficiency such as pulverized coal-fired boiler of super critical or ultra-super critical types, with circulating fluidized bed boiler and integrated gasification combined cycle (IGCC). A positive development and demonstration of carbon capture and storage (CCS) will be prepared and utilized for China’s zero carbon emissions. We have made a rapid development in those low-carbon and environmental-protection technologies, however the technical bottleneck of independent innovation still needs to be solved.

For example, ultra-super critical thermal power technology has a high degree of dependence on foreign countries. Technology resources of power generation equipment manufacturing enterprises are not the same, resulting in technical information asymmetry, so that the key generic technology is not perfect enough [28].

3.1.4 Unsound coordination mechanism for coal and electricity

Production capacity is the main index to assess a coal enterprise. Enterprises often want to have rapid success through high-intensity mining process. This leads to terrible phenomena such as exploiting beyond environmental capacity and mining without legal permission. Extensive exploitation, transportation, processing and consumption of coal resources will not only emit large quantities of wastes to pollute soil and water resources, but can also cause surface collapse and soil erosion. Serious earth surface subsidence, caused by mining conditions and other reasons, is costly to rehabilitate. Irresponsible mining methods have inevitably impacted on mine safety and seriously accelerated the depletion of coal resources, which will do enormous harm to the development of our national economy.

In using the coal resources, the contradictions between coal and electricity markets remain unsolved in China. Furthermore, the quantities of coal within energy market and the demand for electricity are often incompatible.

When there is a shortage of coal supply, the coal price climbs high, leading to losses for electric power enterprises which do not have an opportunity to pass on costs to an electricity market, and a “shortage of electricity” would emerge. Coal companies will probably restrain their production in order to reduce loss when the coal price drops. If the supply of coal is relatively adequate, this coal contradiction will be eased to some extent. On the other hand, if extreme weather occurs or a serious imbalance between supply and demand emerges, there will be various obstacles throughout the transmission of the coal leading to chaos in the energy market. The contraction is reflected by a disharmony between coal price and electricity price, and consequently a poor benefit distribution in supply chain. Both the incomplete linkage of prices and inconsistent reform of power and coal markets are major factors of contradiction between coal and electricity. Unfortunately, the situation is becoming much worse than our expectation.

3.2 Issues of renewable energy

3.2.1 Uneven distribution of renewable resource

Renewable resources are mainly distributed in the north, the northeast, and the west of China, but the majority of power demand is concentrated in the central, the south and the east. Therefore, power transmission issue becomes an inevitable requirement. Interconnection problem would undoubtedly be the bottleneck against the rapid development of renewable resources unless we can find a way to harmonize interconnection, transmission, and power consumption.

Wind power is taken as an example. Figure 5 is the Lorenz curve of the cumulative proportion of wind power capacity and power demand proportion in each province of China. Figure 6 shows the Lorenz curve of under developed wind power and power demand.

Lorenz curve of wind power capacity and power demand

Lorenz curve of technological exploitable wind power and power demand

From the figures above, we can see that when the cumulative proportion of wind power capacity and power demand are in a balanced distribution, the Lorenz curve should be a straight line, however, the Lorenz curve in Fig. 6 deviates from the straight line very much. Considering the exploitable wind power capacity, the Lorenz curve in Fig. 6 shows an even more severe inconsistency in the distribution of wind power and the distribution of electricity demand. Therefore, as more wind power is developed, the requirement for power transmission will increase even faster than before.

What worsens the problem is the intermittency of wind power, its utilization has become a serious problem. A large scale of power system needs to be built to consume the wind power. Apart from the local consumption of wind power, through inter-district is also in need by transmitting the power to load center to achieve cross-regional consumption [29].

3.2.2 Technological backward of power generation

In 2014, there were more than 200 corporations in the Chinese wind power manufacturing industry. In the meantime, the giant wind turbine manufacturing enterprises were rising, and their domestic market share was also increasing. Additionally, production of solar silicon technology has reached a milestone level, and solar cell manufacturing market is constantly expanding. China has established a manufacturing industry in renewable energy equipment, and possesses the ability for large-scale manufacturing.

However, apart from the wind power, hydropower, solar power, most generation technology in renewable energy is still the slow development. The bottleneck mainly exists in the following aspects: low technological level, insufficient technology investment, restricted innovation ability, weak equipment manufacturing ability and high dependence on foreign imports.

Due to the inadequate product testing system, evaluation system and technology standards, training for technical staff is not able to meet the need of the rapidly developing market, while the technical support service system is not entirely established. Therefore, the technology standard of renewable energy generation needs to be further enhanced.

3.2.3 Insufficient policies and regulations

The primary impediment to the development of renewable energy is the absence of sufficient policies and regulations. Though the Renewable Energy Law has been implemented, from a general view, the procedural law is not detailed and lacks some incentives such as fiscal interest discount policy, preferential tax policy and R&D policy. This is for two main reasons. One is the absence of some corresponding mechanism for the policies, such as incomplete policy to support the development of solar energy, wind energy and biomass energy. The other is the poor coordination of management at all levels, which causes decentralization of funds and redundant construction, so the macro-control ability has been always weak.

3.2.4 Ecological damage

At present, the utilization of hydropower is undergoing a rapid development in China. However, some ecological damage can be no longer ignored.

Hydropower construction could deteriorate the ecological diversity of river evolution, and the local shape of the river would be homogenized and discontinuous, because a majority of construction projects are built over natural river channels. Hydropower projects are always harmful for forest, grassland, and cropland. Damage to the vegetation largely affects the habitat of terrestrial animals. Industrial effluents and domestic waste water that discharge directly without treatment in hydropower plant construction process largely affect physical and chemical properties of the river channel, and further deteriorate the environment of river life [30].

Introducing biomass energy is also an urgent task today, since fossil energy is experiencing a significant decrease. China has vast geographical areas which provide a great environment for developing biomass energy. However, in the process of developing biomass energy, there is potential hazard for food crops and farmland we should be concerned about.

On one hand, the basic materials for biomass energy are crops, especially food crops, which are in great need, resulting in the rising food price. On the other hand, farmers are not willing to plant bioenergy crops since bioenergy crops would take too much money and energy compared with traditional crops.

3.2.5 Other issues

1) High generation cost

To solve the high cost issue of renewable energy generation, China has undertaken some serious actions, such as fixed feed-in tariffs and cost-sharing policy. Under such promotion, renewable energy has developed rapidly, especially for wind and solar power.

However, the rapid development of renewable energy has brought a difficulty into power grid. Some activities and policies result in wasting hydro, wind, and solar energy. Under the policy of fixed feed-in tariffs, the bottleneck of renewable energy development lies in the perfect substitutability to traditional energy, leading to a growing resistance for traditional energy power. Renewable resources are no longer an effective compliment for traditional power, but turn into a significant competitor in the market. Because the renewable generation resource occupies the market share of the traditional energy and erodes the interests of traditional energy enterprises, resistance is inevitable.

Although Renewable Energy Law specifies the full protective compulsory acquisition regulation in the renewable field, some regulations cannot be perfectly implemented due to the lack of a corresponding penalty mechanism. A fixed-price has not fully solved the problem of power transmission and consumption of renewable energy, although it has offered a solution to the generating department. Generation costs of renewable energy in 2010–2020 are listed in the Table 3 [31].

2) Unstable market demand

The renewable energy market has an unstable demand in China, with low maturity and inadequate capacity. Both characteristics prevent the sustainable and healthy development of the market. More than that, seasonality and instability of such renewable energy as wind power, hydropower and solar power also impede the rapid development of the market. Therefore, to develop a stable market demand, government should develop mandatory market security for renewable energy generation.

4 Solutions

According to the issues in Section 3, this paper proposes some solutions from the aspects of cost, efficiency and external effects. The framework in this section is shown in Fig. 7.

Framework of solutions

4.1 Lowering the cost

4.1.1 Encouraging the efficient replacement

Due to issues in power system management, local protectionism policies and value added tax (increasing the generation cost), the phenomenon of wind curtailment and water curtailment has repeatedly appeared, and a lot of wind power and hydropower is wasted. Therefore, efficient replacement between hydropower and thermal power needs to be motivated constantly, and the total cost of power generation would be reduced.

In addition, the second round of power market reformation of China is still in the initial stage, and power enterprises should improve the implementation of contract for difference (CFD) methods. The CFD method means that a part of electricity is subject to bidding and the remainder is contracted. In this method, because the efficiency of old units and the efficiency of new ones are different, an Efficient Displacement Optimization Model can be constructed to reduce the cost of generation resource utilization.

4.1.2 Introducing appropriate competition

At present, to achieve price bidding, China has realized an initial separation of power plants and grid enterprises, which creates conditions to optimize the allocation of resources. However, the separation of power plants and grid enterprises is the re-division of internal assets within a monopoly electricity system and competitive bidding only changes the distribution pattern of monopoly profits [32].

So far, electricity tariffs in China are still based on government pricing instead of bidding. Thus, competitions among enterprises are not based on low costs. Enterprise decision makers spend more time lobbying public officials than lowering their costs, and their profits comes from their negotiation outcomes with the government department instead of their competitive efficiency. The two-part electricity pricing includes capacity price and electricity price. The capacity price is determined by a cost-plus approach, it is unable for the government to get clear information about the operating costs and the return rate of power enterprises, leading to a huge difference of tariff for generator sets of the same type. The lack of fair competition among power plants is not conducive to reducing utilization costs of generation resources.

Therefore, China could learn from foreign mature power market patterns, then design reasonable tariff model to reduce the cost of generation resource utilization and improve the efficiency. Table 4 shows the competition mode of some major foreign wholesale electricity markets [33].

China could learn the market reform from foreign successes, and strengthen research on effective competition in electricity markets, to improve the utilization efficiency of generation resources.

4.1.3 Using multiple power delivery pathways

In traditional power market with a single buyer, only the distribution company buys power and sells it to the all of the users. With the continuous development of China’s electricity market, multiple pathways for delivering electricity will emerge. The development of multiple power delivery pathways can reduce the utilization cost and increase utilization efficiency of generation resources.

1) Big user direct purchase of electricity

Big user direct purchase of electricity is not only conducive to the promotion of energy saving and emission reduction, but also helpful to reduce the utilization cost of the generation resource. In the case of direct power supply, generating units with large capacity, low energy consumption and low-cost are more competitive and able to obtain more opportunities, which will motivate improvement of the overall efficiency of generation enterprises [34].

At the same time, hydropower units with a certain scale can participate in the direct power supply like thermal units and compete with each other. The low cost of existing hydropower is the obvious competitive advantage, so development of hydropower and low-cost power resource would be promoted.

2) Electricity delivery

The distributions of generation resource and electricity demand in China are not well-matched. The main resources are concentrated in the western and northern regions, while the demand is mainly concentrated in the eastern and coastal developed areas. These objective conditions result in long-distance transport of power through a large interconnected power grid, for the power demand of different regions in China could be satisfied.

Therefore, increasing the development and construction of power delivery market in northwest China can transform resource advantages into economic advantages. Electricity delivery is not only advantageous to coordinated development of China’s regional economy, but also conducive to promote production of high value-added products and reduce transportation cost of generation resource [35].

3) Energy storage system

The application of energy storage systems is an effective way to reduce the utilization cost of generation resource. Energy storage technology can effectively adjust the energy consumption and realize load shifting, demand management and power load balancing. The first application of energy storage system in China is pumped hydro storage. Pumped hydro storage, which greatly improves the stability and security of the power system, serves as load shifting, frequency and phase modulation, and contingency reserve [36, 37].

In addition, a new energy storage system called superconducting magnetic energy storage (SMES) has been proposed. SMES has many advantages, such as long life, high capacity and low pollution. However, due to the demanding requirements for operating environment and complex system structure, SMES remains at the stage of research, but is a development trend for energy storage [38].

4.2 Improving the efficiency

4.2.1 Using electricity futures

Electricity futures transactions can be conducted among generation enterprises. The enterprises would adjust their power output to maximize returns by opening or covering short positions. If the futures can be delivered in a physical form, the generation resource will flow among blocked output power plants or plants with different types, for example, the power generation resources will flow from blocked output power plant to the normal output power plant. So the compensation effect of plants with different types can be played, and optimal allocation of generation resources would be promoted. For the replacement of generation resources, futures transactions will also bring additional income [39].

4.2.2 Using multiple pricing mechanisms

In the process of reformation of power system, reforming price mechanism is a key task. Continuous innovation and improvement of price mechanism can improve use efficiency of generation resources.

1) Tiered electricity pricing

Residential electricity has been protected in China, so the price is low. The low price can easily cause a waste of electricity. Electricity conservation awareness needs to be raised. Tiered electricity pricing can influence residential electricity habits through economic means. It also can strengthen the awareness of saving electricity, and guide sustainable development of energy production or consumption, to improve the utilization efficiency of the generation resource [40].

2) Time-of-use (TOU) price

TOU pricing can apply to any users but is mainly implemented in industry and commerce, especially for large industrial users. To improve the use efficiency of generation resource and ease the imbalance between power supply and demand, China should apply TOU policy widely. The development of TOU pricing should carefully divide tariff periods. For regions with constrained power supply, with peak load in summer or winter, a variable peak pricing policy should be introduced in addition to fixed TOU pricing. Guiding the demand structure through pricing mechanism can stabilize the peak load and make the load rate more accurate [41].

The tiered electricity pricing and the TOU pricing will promote the optimal use of resources. TOU price, allowing for times when the wind turbines are running, can guide users to use electricity in trough times conscientiously. In this way the utilization proportion of renewable energy could be increased [42].

4.2.3 Joint schedule of virtual power plant (VPP) and energy power plant (EPP)

VPP can be considered as a power management system which participates in the electricity market and grid operation as a special plant. The VPP can achieve the coordination and optimization of distributed power, controllable load, energy storage systems and electric vehicles through advanced communication technologies and software systems [43].

EPP is used for power saving, but not for power generating. It has become a new energy-saving idea popularized in China. Using energy saving replacement or reconstruction for electrical equipment and new energy-saving technology, EPP could reduce the electricity load and promote peak load shifting [44].

Jointly scheduling VPP and EPP can improve efficient utilization of generation resource, which can effectively promote renewable energy generation. The scale of renewable energy generation in China continues to increase. The small unit capacity and the intermittent output of renewable energy generation can cause many impacts on the large grid when interconnected separately.

However, if renewable energy could combine into a VPP with other distributed power to participate in grid operation, the effect of intermittency on external systems would be eliminated through internal optimization. Therefore, the power quality will be improved and the efficient use of renewable energy power will be achieved. At the same time, the VPP will enable renewable energy generation to obtain the maximum economic benefit from the electricity market. Moreover, the EPP can not only integrate demand management projects, but also incorporate other energy-saving projects, such as residual pressure and energy generation in industrial enterprises and combustible waste gas generation.

4.3 Improving the external effects

To reduce emissions from using generation resources, a renewable portfolio standard (RPS) [45] has been proposed in China, and a carbon emissions trading market [46] is under development. However, the RPS and the carbon emissions trading market are in preliminary stage of development, the corresponding policies and market supervision are far from perfect. Thus, this part puts forward the following suggestions.

4.3.1 Providing protection policy

The development of RPS and carbon emissions trading market needs a set of policies and laws. Considering the national conditions, China should draw lessons from foreign relevant experiences to introduce or improve some policies or administrative rules. Furthermore, the Chinese government should clarify the legal status of emission rights acquirement and emissions trading, and should provide policy guarantee for the implementation of a RPS.

4.3.2 Strengthening market supervision

There are many participants in carbon emissions trading, including buyers and sellers, third-party service companies, rule makers, and regulators. To prevent market manipulation, unfair punishment or illegal transaction behavior, the behavior of relevant subjects should be regulated and market supervision should be strengthened, to ensure a sustainable development of carbon trading.

The department for regulating RPS should be given necessary power to enforce it. This department should fulfill its oversight responsibility for renewable energy quota obligations so that it can carry out punishments when an enterprises’ activities do not meet the quota obligations.

4.3.3 Developing trading pilots

RPS and carbon emissions trading system should be gradually developed. We could expand the pilots in different regions according to the foundation, differences and relations of regional economies, and aim to trial different systems. In the pilot areas, the overall level of economic development should be high, and an extended geographical scope is needed.

In particular, pilot industries of carbon emissions trading should include steel, cement, electric power, aviation and other industries with huge carbon emissions, and then gradually expand to other industries.

4.3.4 Improving financial transaction system

Financial institutions and enterprises are encouraged to participate in carbon finance trading, such as carbon swaps and carbon futures. Other carbon financial derivative products will be gradually developed. Considering credit products, the low-carbon credit product should be innovated in a commercial bank on the basis of characteristics of carbon emissions trading projects. This product depends on project financing which gives preferential loans to low-carbon industry projects. Furthermore, a carbon stock option mechanism should be implemented. Introducing the option mechanism is helpful for increasing transaction amount, energizing the market, as well as regulating the market transactions.

5 Conclusions

In summary, here are the following conclusions.

1) From the status of China’s generation resource utilization, we can make several conclusions. Firstly, the demand of China’s coal market continues to slump, while coal imports decrease but remain at a large scale. Secondly, as one of the renewable energy sources, hydro energy will become the key renewable energy in future power construction. Thirdly, wind power generation is growing fast under the background of global energy shortage. Finally, natural gas and other resources are rapidly developing in China.

2) Section 3 illustrates the STEP model to summarize some issues for China’s generation resource utilization. In political aspect, currently there are no appropriate policies on generation resource utilization. In economic aspect, high generation cost and unstable market demand may hinder the further development of renewable energy. In social aspect, uneven distribution of resources results in a high utilization cost. Meanwhile, ecological damage problem caused by generation resource utilization cannot be ignored. In technological aspect, how to use fossil energy in a sustainable way has become an important topic. Generation technology for China’s renewable energy industry is still lagging behind international levels.

3) This paper presents some improvement approaches for generation resource utilization from the perspectives of cost, efficiency and external influence. The efficient replacement between different power plants can save the generation resource and improve the utilization efficiency. Introducing competitive mechanisms and perfecting bidding methods can promote generation enterprises to optimize the utilization mode of generation resource and to reduce utilization cost. Using multiple pathways for electricity delivery alleviates the imbalance of resource allocation, so that generation resource utilization can be more efficient. Generation resource can be obtained among different generators through electricity futures. Designing different levels of electricity tariff including TOU can optimize utilization structure of generation resource. Joint schedule of VPP and EPP can improve efficient utilization of generation resource, which effectively promotes renewable energy generation. Finally, developing RPS and a carbon emissions trading market can effectively reduce the impact of generation resource utilization on the environment, as well as negative external effects of fossil energy utilization.

Above all, accelerating the development and utilization of renewable energy will become the only way to alleviate the pressure of energy and environment in China. China’s generation resource utilization will move towards low carbon, environmental protection and sustainability.

References

Luo JG, He BL, Xing YT (2014) The prediction of China’s power industry development. Energy China 36(6):31–35 (in Chinese)

Liang ZP, Li YS, Hu HC et al (2012) Design of UHV AC transmission line in China. Eur Trans Electr Power 22(1):4–16

Chen L, Zhang YC (2013) The mid long term electric power development in China of the “12th Five-Year” energy plan. Energy China 35(9):26–29 (in Chinese)

Kan LM (2014) Strengthen the management of China’s electric power development planning. Chin Foreign Entrep 4X:101 (in Chinese)

Yuan JH, Shen JK, Pan L et al (2014) Smart grids in China. Renew Sustain Energy Rev 37(3):896–906

Yan XH, Xu YJ, Ji L et al (2013) Forecasting and analysis on large-scale energy storage technologies in China. Electr Power 46(8):22–29 (in Chinese)

Zhang SL (2008) Electric power industry reform and electricity market construction in Vietnam. East China Electr Power 36(1):67–70 (in Chinese)

Chen L (2012) The international comparative study of the electric power industry regulation. Ph.D. Thesis. Fujian Normal University, Fuzhou, China, pp 20–29 (in Chinese)

Vlachos AG, Biskas PN (2014) Embedding renewable energy pricing policies in day-ahead electricity market clearing. Electr Power Syst Res 116(11):311–321

Hu GY (2014) The leading country electric power industry development analysis. J North China Electr Power Univ: Soc Sci 1:7–10 (in Chinese)

Hussey J (2014) British renewable electric power development (trans: Zhang S). China Electr Equip Ind 6: 45–49 (in Chinese)

Nie XW (2014) India’s power industry development: achievement, problems and enlightenment. Econ Res Guide 7:235–240 (in Chinese)

Zhang QL (2014) The study between US-Japan’s energy tax systems and related industry development. Ph.D. Thesis. Jilin University, Changchun, China, pp 5–20 (in Chinese)

Guo B (2013) The development and prospect of China’s electric power resources. J Gansu Radio Telev Univ 23(3):18–20 (in Chinese)

Dong LT (2013) Energy-saving mechanism design models and methods research in power integrated resource planning. Ph.D. Thesis. North China Electric Power University, Beijing, China, pp 3–30 (in Chinese)

Wang SX (2013) The Optimization model and method for comprehensive utilization of power resources under the constraint of emission reduction. Ph.D. Thesis. North China Electric Power University, Beijing, China, pp 1–20 (in Chinese)

Liu DD (2013) Intelligent power technology promotes the reasonable allocation for electric power resource. Technol Enterp 16:95 (in Chinese)

Yan QY, Tang XF, Kong C et al (2013) Study on electric power resource substitution based on system dynamic analysis. Water Resour Power 31(5):183–185 (in Chinese)

Chen X, Zhang TT (2014) The prospect of power industry. Guide Science-Technology Mag 14:181 (in Chinese)

Song HZ (2013) Study on the distribution characteristics and the exploration and development prospect of coal resource of China. Ph.D. Thesis. China University of Geoscience, Beijing, China, pp 10–25 (in Chinese)

Notice on coal industry development in “Twelfth Five Year Plan”. National Development and Reform Commission (NDRC) of China, Beijing, China, 2012-03-18 (in Chinese)

Wu CQ (2012) Next 10-year natural gas usage trend in China. Int Pet Econ Z1:110–115 (in Chinese)

Liu W (2015) China’s hydropower installed capacity accounted for 1/4 of the world. Economic Daily, 2015-05-20 (in Chinese)

2014 in the proportion of oil and gas production share accounted for more than 7. CBIW, 2015-10-24 (in Chinese)

Analysis on cumulative installed capacity and growth rate of wind power in the world in 2001-2014. China Industrial Information Network, 2015-12-11 (in Chinese)

Xiao Q (2014) Wind power development framework in “13th Five-Year Plan”. China Energy News, 2014-10-27, pp 1–2 (in Chinese)

Ji LQ, Wang JJ, Wang JP (2011) Analysis on the technological bottleneck of 1000 MW ultra-supercritical coal-fired power generation in China. East China Electr Power 39(6):976–979 (in Chinese)

Zhou DY, Gao GY (2014) Difficulties and countermeasures of developing renewable energy in China. Price: Theory Pract 6:116–117 (in Chinese)

Zhu LZ, Chen N, Han HL (2011) Key problems and solution of wind power accommodation. Autom Electr Power Syst 35(22):29–34 (in Chinese)

Zhang CQ, Feng XT, Zhou H et al (2013) Rockmass damage development following two extremely intense rockbursts in deep tunnels at Jinping II hydropower station, Southwestern China. Bull Eng Geol Environ 72(2):237–247

Song YH (2014). Research on inter-regional allocation optimization model of electric power resource in China. Ph.D. Thesis. North China Electric Power University, Beijing, China, pp 12–24 (in Chinese)

Li YQ, Tan ZF (2006) Research on promoting China’s electric power resources and economic means to optimize the allocation. China Electr Power Educ 4:71–74 (in Chinese)

Ma L, Fan MH, Guo L et al (2014) Latest development trends of international electricity markets and their enlightenment. Autom Electr Power Syst 38(13):1–9. doi:10.7500/AEPS20140520007 (in Chinese)

Sun J, Wang YL (2009) Research on the admission standard of large consumers direct-purchasing based on the externality theory. In: Proceedings of the 2009 Asia-Pacific power and energy engineering conference (APPEEC’09), Wuhan, China, 27–31 Mar 2009, pp 2664–2668

Du PW, Wang ZY, Diao R et al (2011) Application of Kalman filter to improve model integrity for securing electricity delivery. In: Proceedings of the 2011 IEEE/PES power systems conference and exposition (PSCE’11), Phoenix, AZ, USA, 20–23 Mar 2011, 7 pp

Teng XL, Gao ZH, Zhang YY et al (2014) Key technologies and the implementation of wind, PV and storage co-generation monitoring system. J Mod Power Syst Clean Energy 2(2):104–113. doi:10.1007/s40565-014-0055-1

Gao ZY, Fang JJ, Zhang YN et al (2014) Control strategy for wayside supercapacitor energy storage system in railway transit network. J Mod Power Syst Clean Energy 2(2):181–190. doi:10.1007/s40565-014-0060-4

Devillers N, Péra MC, Bienaimé D et al (2014) Influence of the energy management on the sizing of electrical energy storage systems in an aircraft. J Power Source 270:391–402

Yang HM, Liu SD, Feng WL (2009) Research on efficiency of electricity futures market. Power Syst Prot Control 37(4):9–15 (in Chinese)

Zhang HJ, Tan ZF, Xu H (2013) Research on generation coal-saving effect of the tiered pricing of residential electricity under different power generation structures. In: Automatic control and mechatronic engineering. In: Proceedings of the 2nd international conference on automatic control and mechatronic engineering (ICACME’13), Bangkok, Thailand, 21–22 Jun 2013, pp 679–701

Chen SH, Tang CJ, Huang CW et al (2013) Study on the formulation strategy of residential time-of-use rate when connected to the smart grid. Mon J Taipower Eng 773:38–58 (in Chinese)

Liu XD (2012) 2030 may become the turning point of China’s electric power demanding. China Energy News, 2012-10-22, pp 1–5 (in Chinese)

Moutis P, Hatziargyriou ND (2014) Decision trees aided scheduling for firm power capacity provision by virtual power plants. Int J Electr Power Energy Syst 63:730–739

Ramonas C, Adomavicius V (2013) Research of the converter control possibilities in the grid-tied renewable energy power plant. Electron Electr Eng 19(10):37–40

Schuman S, Lin A (2012) China’s renewable energy law and its impact on renewable power in China: progress, challenges and recommendations for improving implementation. Energ Policy 51:89–109

Huang J, Xue F, Song XF (2013) Simulation analysis on policy interaction effects between emission trading and renewable energy subsidy. J Mod Power Syst Clean Energy 1(2):195–201. doi:10.1007/s40565-013-0015-1

Acknowledgment

The authors would like to thank the anonymous referees and the editor of this journal. This work was support by the National Natural Science Foundation of China (No. 71273090) and Fundamental Research Funds for the Central Universities (No. 2015XS44).

Author information

Authors and Affiliations

Corresponding author

Additional information

CrossCheck date: 31 March 2016

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

TAN, Z., CHEN, K., JU, L. et al. Issues and solutions of China’s generation resource utilization based on sustainable development. J. Mod. Power Syst. Clean Energy 4, 147–160 (2016). https://doi.org/10.1007/s40565-016-0199-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40565-016-0199-2