Abstract

Recent empirical evidence raises doubt about the ability of financial market participants to generate information efficient valuations for capital market instruments whose cash flows are related to residual claims and dependent on real estate income. We contribute to this literature with the examination of value implications of non-performing loan (NPL) divestitures in the banking industry during the period 2012–2018. In a first step, we provide descriptive statistics of the European NPL market, which lacks transparency and publicly available basic information on portfolio size and components. We then analyze wealth effects of distressed loan sale announcements for a uniquely large transaction database with 317 NPL deals, which is largely driven by real estate collateral. Our results show positive stock market reactions for vendor banks following NPL divestitures that tend to be driven by real estate collateral and a size effect.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Non-performing loans (NPL), commonly referred to as loans in arrears for at least 90 days, have continuously been characterized as the top priority of the European Central Bank (ECB) and continue to attract central attention (see inter alia ECB 2018a, b). With the outbreak of the European debt crisis, the quality of banks’ assets had deteriorated in a manner that, despite robust economic recovery and a variety of regulatory efforts, NPL still today pose a threat to bank and thrift institutions. Against this backdrop, the European regulator requires banks to develop effective strategies for reducing NPL, to set up clear governance and to operate powerful workout structures (ECB 2017). The ECB assists with a variety of guidance measures, and especially since 2014, one of the core advices is active portfolio reduction, effectively requiring banks to sell or securitize their (mostly real estate based) residual claims on NPL holdings to loan investors in the secondary market.

With the divestiture of NPL, risky and complex bank assets are transferred from a bank-based to a market-based financial system, which raises a number of critical pricing issues. In order to establish a stable secondary market environment for distressed assets in the long term, efficient loan portfolio pricings and fair compensations of the given risk-return profiles are necessary. The subprime crisis of the last decade, however, revealed severe problems of global capital markets in the evaluation of related structured real estate finance products like collateralized loan obligations and similar asset-backed securities. Woltering et al. (2018) detect equity mispricing of property-holding companies in 11 countries during 2005–2014, which can be exploited using simple trading strategies based on net asset value spreads. Gallo et al. (2000), Mori and Ziobrowski (2011) and Cici et al. (2011) provide additional evidence in favor of equity mispricing in the case of U.S. REITs.

In equity capital markets, shareholders act as claimants of a company’s residual income which is very close to the bank lender’s position in distressed loan assets. Debt capital markets, on the contrary, are less liquid in comparison and potential buyers of loan portfolios are required to spend significant effort on a precise NPL evaluation. In this context, Demirgüç-Kunt and Levine (2004) analyze pricing issues with respect to accounting-based valuations of interest-bearing assets by comparing bank-based and market-based financial systems in the aftermath of financial crises. They report evidence that institutions in bank-based systems tend to postpone necessary balance sheet restructurings in order to delay the effects of losses, whereas this option is not available for investors in market-based financial systems.

If the market-based system provides superior valuation skills, the pricing of loan portfolios should mostly profit when the heterogeneity and individuality of the underlying assets is as large as in the case of real estate collateral. The NPL sale should reduce outsider uncertainty on banks’ asset values and raise confidence in their balance sheet statements. Additionally, with the sale of a loan portfolio, the bank’s management signals that it does not perceive a significantly higher evaluation as compared to investors in the secondary market. Otherwise, the transaction parties would not concede on a purchase price, which effectively clears the market. In analogy, the NPL divestiture announcement can be interpreted as a signaling from the bank’s management that it is not overconfident with respect to the proceeds from their NPL portfolios. Given that residual value exists, NPL sales recover (regulatory) liquidity immediately and transfer the risks and work-out expenses to the transferee (Irani and Meisenzahl 2017).

While NPL sales increased significantly over the last years, there is only scarce evidence on market values of debt and NPL portfolios (see Sect. 2). These are depleted into secondary markets that are less liquid and market participants take time and effort to evaluate the respective assets. As most of the banks associated with NPL divestiture activity in Europe are exchange-listed, the stock market reaction to the announcement of the sales also indicates to some degree whether the realized sales prices are generally perceived as adequate. Additionally, the sales execution by itself reduces the uncertainty on the value of current risky bank assets which brings us to expect a positive share price reaction on the announcement of NPL deals. Given the ECB pressure on banks to dispose of NPL, we assume that the regulator expects the same effect.

In addition, the window of opportunity to transfer assets under distress is narrowing, as the determination of NPL is strongly linked to macroeconomic and bank-specific factors. A number of studies expect NPL to increase during potential economic downturns (Dimitrios et al. 2016; Keeton and Morris 1987; Klein 2013; Louzis et al. 2012), inducing a supply shock for these kind of portfolios. The level of price response should depend on the level of uncertainty resolved, the specific situation of the selling bank and the quality of the buyers or the appreciation of the buyer's competence. Therefore, we expect (a) particularly positive effects in real estate deals, (b) significant explanations by bank-specific factors and (c) sales of real estate assets to be particularly connected to specialized financial investors.

The aim of this paper is to anticipate how complex asset sales whose cash flows are heavily dependent on real estate income are evaluated by capital market participants. This work provides both banks’ decision makers and regulators with an indication how the cleaning of balance sheets from distressed assets will result in revaluations of bank equity. We synthesize a unique transaction database with 476 NPL sales for the period 2012–2018. As a starting point, we clarify descriptive statistics of the European NPL market which so far lacks transparency and publicly available basic information on portfolio size and components. In particular, we are curious to understand the role of real estate in these transactions and the relevant market participants regarding real estate NPL deals. We find that about two thirds of transactions are directly related to real estate collateral. Considering mixed loan pool portfolio sales, where real estate collateral is involved in unknown proportions, this majority further increases (app. 90%). Thus, the pricing of NPL sales is largely determined by the underlying rental income and potential property proceedings in the real estate market to cover loan claims of the debtor. Second, using traditional event study methodology, we empirically analyze valuation effects of 317 distressed loan sale announcements at European banking institutions during the period 2012–2018, both generally and with a special focus on real estate collateral. Third, given significant valuation effects, we want to understand whether the effects can be explained by bank-specific characteristics of the vendor or specific characteristics of the sold NPL portfolios, such as the nature of collateral and (relative) portfolio size.

The analysis is structured as follows. Section 2 provides a literature overview and formally derives our hypotheses. Section 3 describes data synthesis and the methodology for the empirical part of the analysis. This includes a structural assessment of NPL market descriptive statistics. Section 4 presents empirical evidence on NPL sale announcement effects and critically discusses the results. Finally, Sect. 5 concludes with a summary and implications of this work.

2 Related literature and hypothesis development

The capital market based evaluation of various corporate actions like acquisitions and divestitures has traditionally been examined with event study methodology (Binder 1998; MacKinlay 1997). We connect our research to a number of studies that analyze market feedback following divestiture announcements of firms that sell non-performing (Brown et al. 1994; Lasfer et al. 1996) or non-core (Comment and Jarrell 1995; John and Ofek 1995) assets. This strand of literature generally reports positive feedback from the stock market and interprets this result as adjustment for the distress cost reduction (Lasfer et al. 1996) and reversal of value-destroying diversification (Clubb and Stouraitis 2002).

In the literature stream that examines loan announcements, James (1987) reports positive stock returns of borrowers to the announcement of large new bank loan agreements. Also, Maskara and Mullineaux (2011) as well as Huang et al. (2012) more recently focus on borrower stock returns related to large loan announcements, where sizeable information asymmetries are presented. Gande and Saunders (2012) suggest that loan sales generate moral hazard problems for banks that could potentially retain higher quality assets or convey sensitive (negative) information about borrowers (Gande and Saunders 2012; Pennacchi 1988). Dahiya et al. (2003) conduct the first series of tests with loans under distress (pp. 153). Based on a small sample of U.S. borrowers between 1995 and 1998 (n = 29), including a sub-panel (n = 15) of subpar loans, they obtain negative but insignificant results for the vendor.

We find several indications, albeit outside of the journal literature, that these findings could be transferable to banks that announce (divestiture) information about (real estate based) loan and mortgage portfolios. Dick (2010) analyzes NPL transactions from three European countries (n = 38) for the timespan 2003–2007 and documents neutral evidence. Geiger et al. (2007) analyze European NPL portfolio sales (n = 56) with real estate collateral during 1990–2005 and find significant positive stock market reactions for the loan announcements with worst credit quality and small negative significant effects for loan portfolios with better credit quality. Gentgen (2007) investigates NPL transactions from Aareal Bank (n = 4) during the period 2005 to 2007 in Germany with inconsistent results. More recently, Faa (2019) reports significant and positive announcement effects for NPL sales at Italian banks during the period 2013–2019 (n = 63).

All in all, the empirical evidence from prior literature is broad but inconclusive. None of the earlier studies were able to synthesize large sample sizes across different asset classes, countries and longer timespans simultaneously. Research in the banking literature yields a number of arguments in favor of a positive market reaction following NPL divestiture. There is evidence that banks are generally incentivized to sell loans to meet (short-term) liquidity needs under the new Basel III regime, either by raising capital or reducing the amount of risk-weighted assets (Boudriga et al. 2009; Irani and Meisenzahl 2017). As a consequence, bank capitalization is altered in favor of the capital adequacy ratio, adjusting banks’ balance sheets in favor of the security holders (Kwan and Eisenbeis 1997). Considering that failing banks generally report significant proportions of NPL prior to failure or distress (Berger and DeYoung 1997; Jin et al. 2011), selling risky assets may also be interpreted as a signaling to the equity market about the vendor’s willingness to ensure smooth functioning after negative shocks (Granja et al. 2017), while banks continue to operate under increased regulatory pressure (ECB 2018a, b). In addition, NPL sales should reduce the bank’s complexity, transfer the future management costs to the transferee and help to increase financial stability (Krause et al. 2017; Irani and Meisenzahl 2017). Thus, we first hypothesize:

Hypothesis 1

Announcements of NPL divestiture activity coincide with significant positive valuation effects, as measured by the cumulative abnormal returns of the vendor share price.

Given the current market characteristics in the European NPL market (see Sect. 3.1), the pricing of NPL portfolios is largely defined by expected rental income and potential property sale proceeds in the real estate market to cover the debtors’ loan claims. Real estate generally demands a highly distinct skillset to adequately manage important features of collateral, as it is characterized by its immobility, heterogeneity, complexity and indivisibility (see Breuer and Nadler 2012). Yet, its tangibility gives both the vendor and the acquirer the opportunity to estimate its intrinsic value and facilitates the evaluation compared to the appraisal of corporate or unsecured consumer debt. Based on this tangibility, the bidding price on real estate loans should likely be higher compared to other types of collateral. This should, in turn, affect the revaluation of bank capitalization in excess, ultimately inducing banks to carry less risk (Berger and DeYoung 1997; Salas and Saurina 2002). In the literature that analyzes NPL determinants at the loan level, a number of studies have started to account for real estate separately, the results yielding a further indication about the distinct features (see Adelino et al. 2016; Beck et al. 2015; Ghosh 2015). For these reasons, we hypothesize an appraisal difference depending on collateral quality, expressed in the net effect of distinct real estate attributes:

Hypothesis 2

Due to its distinct features, the sale of real estate NPL is reflected in excess significant positive cumulative abnormal returns of the vendor, as compared to the overall cumulative abnormal returns of vendor banks.

Given that valuation effects also depend on the specific situation of the vendors the question arising is to what extent the abnormal returns can be explained upon the basis of vendor characteristics. This question is particularly appealing for both investors and regulators alike. Investors might target those banks having the highest likelihood in generating positive abnormal returns. Regulators might adjust their guidance accordingly. Prior research has widely acknowledged the interlinkage between a bank’s amount of NPL and its insolvency risk (see Arena 2008; Berger and DeYoung 1997; Jin et al. 2011; Whalen 1991), leading us to expect NPL divestiture to result in a significant reduction of bank-specific risk. More specifically, prior studies have emphasized the impact of a bank’s bad loans to total loans ratio upon bank-specific risk (Kwan and Eisenbeis 1997), as weakest institutions generally exhibit higher proportions of NPL prior to failure (Berger and DeYoung 1997; Jin et al. 2011). Based on this evidence, we would expect valuation effects to be positively related to those vendor characteristics that proxy for idiosyncratic risk. For instance, given that big transactions tremendously enhance the future prospects of these firms, we hypothesize that they should result in above-average positive shareholder wealth effects. We therefore formulate our third hypothesis as follows:

Hypothesis 3

The valuation effects observable around the announcement of NPL sales are more positive for vendors characterized by high proxies for idiosyncratic risk as for instance a bank’s ratio of NPL to total loans or the magnitude of sold NPL in percent of a bank’s total assets.

If NPL sales help to reduce the idiosyncratic risk of vendor banks especially regulators have to understand which institutions take the risk involved in those sold portfolios. The buyers should be willing but also capable to manage the NPL credit risk to guarantee a stabilization of the banking sector by these transactions. While potential vendors usually have superior knowledge about the quality of their assets, the bargaining power in divestiture situations under distress is limited, while at the same time, the regulator continues to undermine the necessity of capable secondary markets (e.g. ECOFIN 2018). With regard to real estate collateralized NPL, active resolution strategies in terms of e.g. redevelopments of underlying properties are necessary to turn from non-performing to performing assets. Typically, investors willing to engage within these high-risk transactions are considered to be opportunistic (Rottke and Gentgen 2008). Shilling and Wurtzebach (2012) find that funds allocated to the real estate sector in 2009 primarily come from value-add and opportunistic investors (U.S. market). These specialized institutional bidders on the buy-side are highly experienced in the valuation of NPL portfolios. Linked to the net effect of distinct attributes of real estate, they exhibit a demanding skillset that is needed to manage the workout of real estate collateral. Driven by different opportunity cost of capital, we would thus expect the opportunistic investors’ buying position to be most accentuated in NPL divestiture situations that involve real estate collateral. We therefore hypothesize as follows:

Hypothesis 4

The largest buyer group of real estate collateralized NPL are opportunistic investors, rather than other types of investors as for instance (investment) banks.

The remainder of this paper is devoted to data synthesis, formal methodology and the presentation of results.

3 Data and methodology

3.1 Data

Our analysis concentrates on announcement effects of NPL divestitures in the securities market based on the event study methodology. This methodology is accredited to the seminal work of Fama et al. (1969)Footnote 1 and allows to estimate the impact of new and unexpected information on a company’s market-based perception of corporate value (MacKinlay 1997). In efficient capital markets, it is expected that security prices always correctly reflect all publicly available information (Fama 1970). Having received broad attention in corporate finance research, event study methodology today serves as the central instrument in event-induced research (Corrado 2011; Kothari and Warner 2007). Corrado (2011) structurally documents the advancement of short-term event study methodology and its many applications, and Binder (1998) gives a critical review of the theoretical advancement since 1969, including hypothesis testing and the use of different benchmarks for the estimation of expected returns. The basis of every event study is a thorough event selection and cleaning process.

Initial event selection. We accumulate publicly available NPL transaction data for the period January 1st 2012 to December 31st 2018. We start to identify NPL deal announcements using Debtwire’s NPL Coverage database that actively reports information about NPL trades. Next, we apply deep learning based text recognition techniques using Tesseract to gather deal data from publicly available NPL research reports. The two main sources in the segment are industry advisors Deloitte and Cushman & Wakefield. This first quest leads to a possible identification of 709 European NPL deals. As this raw data stems from multiple resources and dates may not necessarily reflect the announcement date when the new information reaches the market, we develop a comprehensive three-step cleaning process. We visualize sample size development and the sample composition with respect to each database source in Appendix C.

NPL data cleaning. First, we sort for vendor, date and project name to identify potential duplicates. Line-by-line examining conflicted data, we ensure that the highest level of deal information remains in the sample and merge duplicates if it leads to more detailed information. In this step, 605 deals remain in the sample. Second, we run several availability checks. The name of the vendor has to be disclosed unequivocally, the date of the announcement has to be clear, the collateral type has to be known and also the country of collateral. More importantly, we match for unique identifiersFootnote 2 in each category by hand. Where possible, we control for acquirers, detailed loan status and book value of the loans and match the information in a unified format. Having confirmed normal distribution of daily data, we first employ the 15th day of a month if only the event month of a deal is available. To ensure valid results, we later review announcement dates for all NPL deals that appear in the event study by hand. We particularly cross-check news announcements to ensure for the earliest arrival of new events in the market. Transactions in GBP-currency are converted to Euro at the historic exchange rate. NPL divestitures that were cancelled or only rumored about are exempted from the study. We group collateral types into four larger categories, namely real estate, consumer, corporate and mixed loans. In this initial “descriptive sample”, 476 NPL sales remain and are functional to characterize the European NPL market.

Banking and market data. For event study inclusion, vendors have to be a publicly listed financial institution, with liquid daily trading data during the 140 trading daysFootnote 3 preceding and 20 trading days following the event date, applying an event cutoff-date of 31st October 2018 due to the benchmark measure of normal returns discussed below. Attributing (European) subsidiary institutes to parent banks, if reasonable, we identify daily return data for 58 banks in the sample using Thomson Reuters Datastream. We retrieve daily percentage changes of the Datastream Return Index as daily stock returns in Euro, adjusted by dividends. We mark the occurrence of confounding events, i.e. NPL sales by banks within the event window of another deal by the same vendor, to control for a possible bias of our results. We check for robustness by including and excluding these follow-up events in the sample, but find that they should remain in the study as test results are not affected qualitatively. In addition to the return data, we collect a set of bank-specific variables from Thomson Financial Datastream to use both in the cross-sectional regression analysis of abnormal returns as well as in the descriptive characterization of vendors. As benchmark measure for normal returns, we obtain data for the Sharpe (1964) and Lintner (1969) model by applying the MSCI Europe as a proxy for the European market index. As additional audit of robustness, we obtain corresponding data for the STXE 600 banks that sector-specifically cover the 47 largest European banks, based on their market capitalization. As a proxy for the risk-free rate, we apply the EU AAA-rated government bond yield rate with a 10-year maturity. Last, we drop all vendors without liquid daily trading data (measured in zero-percent return days) during the 140 trading days preceding and 20 days following the announcement date to ensure sufficient liquidity across the sample as NPL sales may coincide with financial turbulence of the seller themselves. This final step resulted in an event study sample of 317 NPL trades with a GBV in excess of €300bn from 58 financial institutions.

In Table 1 and Appendix A, we provide summary stats for both this reduced event study sample as well as the larger descriptive sample to account for a potential bias due to excluding financial institutions that are unlisted or have insufficient daily and liquid return data. Both panels are consistent. With regards to transaction volumes, while the smaller single-name transactions or portfolio baskets start with GBVs of €5 m, the largest transactions amount up to €26bn face value. These large block transactions oftentimes account for NPL disposal into bad-banks or similar government endowed entities. Note, GBVs do not represent actual transaction prices.

Table 1 additionally reports the different collateral classes in the sample. The mapping procedure for collateral types is documented in Appendix F. Based on a mere GBV-valuation, app. Two thirds of the collateral (66.1%) are real estate loans. The other third accounts for consumer loans (5.7%), corporate loans (4.0%), and mixed loan pools (24.2%). Regarding the latter category, these loans represent a mixture of the other three loan types in an unknown proportion. For this reason, we estimate the actual real estate proportion to be higher. Real estate and mixed loan pools together pinpoint the dominant and distinct role of real estate collateral in the European distressed loan sale market, yielding a first indication regarding our second hypothesis.

Appendix A reports an overview of the top transaction parties (both vendors and acquirers) as well as key transaction markets for both the larger descriptive market sample as well as the event study example. In regards to the country assignment of a transaction, we hypothesize some ambiguity in the data at this point, as many portfolio deals involve collateral from multiple countries, yet independent of the location of the vendor. Nevertheless, in line with industry expert and regulatory commentators, the majority of transactions in the sample stems from Italy, Spain and the UK (70.0%). For this approximation, we later include a binary dummy for Italy in the multivariate regressions since Italian deals represent the largest subgroup. Considering the dominant buyer groups, the opportunistic private equity funds Cerberus, Lone Star and Blackstone account for a third of the deal volume. The largest single buyer party are securitizations or sales to consortia of multiple buyers, which we cannot assign precisely (15.9%). Thus, we explore these structures in more detail using logistic regressions in Sect. 4. Considering the sell-side, the present sample appears rather homogeneous as the five largest vendors account for much less of the market volume (30.1%) compared to the acquirer group (51.3%). In line with anticipated media coverage, the largest single vendors are Banca Monte dei Paschi di Siena (6.8%), UKAR (i.e. UK Asset Resolution; 6.3%), Banco Santander (6.1%) and NAMA (Ireland Asset resolution vehicle; 5.7%). The yearly distribution of transactions for both samples, the descriptive (n = 476) and the event study sample (n = 317), is illustrated in Appendix B.

Table 2 reports the key financial characteristics for the vendors of the smaller event study sample (n = 317), where we are able to retrieve the corresponding financial data from the Datastream database.Footnote 4 Again, the event study sample serves as a fair proxy of the larger descriptive sample of the current NPL market. The data shows the expected concentration of key ratios within our sample of firms divesting loans under distress.

3.2 Methodology

We measure short-term valuation effects of banks’ NPL divestiture announcements by applying common event study methodology. Thus, we first require a benchmark measure of normal returns (Brown and Warner 1980; MacKinlay 1997), as abnormal returns are defined as actual ex-post returns over the event window, exceeding returns that would have been expected without the event taking place (MacKinlay 1997). As this paper entirely deals with equities from the financial industry, note that the performance of more sophisticated multi-factor models, such as the Fama and French (1993) three-factor model is disputed for explaining the cross-section of banking stocks (see Viale et al. 2009). Thus, we first employ the one factor Sharpe (1964)–Lintner (1969) capital asset pricing model (CAPM), based on the MSCI Europe, followed by an analysis of robustness using deviations from market adjusted returns that account for sector-specific bank returns in the European financial industry, namely the STXE 600 banks. We measure expected normal returns using CAPM, calculating a stock’s daily return as follows:

where \(E\left( {R_{it} {|}X_{t} } \right)\) indicates the expected daily normal return \(R\) for each bank \(i\) at time \(t\), dependent upon the conditioning information \(X_{t}\) of our chosen asset pricing model (MacKinlay 1997). Variable \(rf_{t}\) denotes the risk-free rate which is proxied by the EU AAA-rated government bond yield rate (10-year maturity). \(MKTRF_{t}\) is the excess return on the European equity market, i.e. the return on the MSCI Europe minus the risk-free rate and \({\upalpha }_{{{\text{it}}}}\) indicates security-specific error terms. We apply both a 140 and an extended 273 trading days estimation window to ensure robustness of the results. The event period itself is not included in the estimation period “to prevent the event from influencing the normal performance model parameter estimates” (MacKinlay 1997, p. 15). Respective betas are then used to predict normal stock returns over the event window. Considering the short-term horizon of the estimation (cf. Barber and Lyon 1996), we decide to estimate abnormal returns for each financial institution \(i\), by calculating respective daily abnormal returns (AR) in comparison to the one factor-model:

ARs are calculated over a whole 41-day event window, from \(T_{1}\) to \(T_{2}\), comprised of 20 pre-event days (t = − 20), one event day and 20 post-event days (t = + 20). We define the event t0 to be the earliest announcement of NPL divestiture during the timespan January 1st 2012 to October 31st 2018. Next, we aggregate abnormal returns of stock returns for all events respectively (CAR):

where \(CAR_{i}\) is the cumulative abnormal return for a financial institution \(i\) and \(T_{1}\), \(T_{2}\) indicates the event window. Last, we report the cumulative average abnormal returns \(CAAR_{{T_{1} T_{2} }}\) over the chosen event window throughout all NPL divestiture announcements for all stocks:

We employ the parametric test statistics of Boehmer et al. (1991) and the non-parametric test statistics of Corrado and Zivney (1992) to test for the statistical significance of ARs and CARs aggregated over all financial institutions in the sample. Further, we control for changes between median and mean CAARs. We apply the same methodology on a number of subsamples across different collateral classes and for the robustness checks.

Subsequently, we perform multivariate regression analyses to identify key value drivers of abnormal returns following NPL divestiture announcements, using a series of bank-specific deal characteristics. In this paper, we employ cross-sectional analyses in the form:

where we apply observed CARs for the [\(-\)5;\(+\)5] event window as dependent variable. \(npl\_tl_{i}\) is defined as a bank’s NPL to total loans ratio, \(roa\_5y_{i}\) is the bank’s 5-year average return on assets (ROA), \(ceq\_ta_{i}\) the firm-specific common equity to total assets ratio, \(loanloss\_rll_{i}\) indicates a bank’s actual loan losses in percent of reserves for loan losses, \(capad_{i}\) reports the respective Tier 1 capital adequacy ratio and \(gbvnpl\_ta_{i}\) the ratio of sold NPL’s gross book value (GBV) to the respective bank’s total assets. Next, due to the high number of NPL deals announced in Italy, we include a binary Italy dummy (\(italy\_dummy_{i}\)). Finally, we include a dummy variable indicating whether (1) or not (0) respective NPL deals are collateralized by real estate (\(re\_dummy_{i}\)). Standard errors are clustered on vendor-level. All data for bank-specific characteristics is obtained via Thomson Reuters Datastream/Worldscope. Detailed variable explanations and calculations are presented in Appendix D.

Last, we perform logistic regressions to analyze the relationship between distinct types of investors and underlying NPL collaterals. For this purpose, we classify investors into five categories as follows: specialized (small) investors (\(buyer\_type{ }1\)), opportunity funds (\(buyer\_type{ }2\)), consortia of multiple buyers/securitization (\(buyer\_type{ }3\)), (investment-) banks (\(buyer\_type{ }4\)), and undisclosed investors (\(buyer\_type{ }5\)). We start by using the real estate dummy of the overall event study sample (n = 317) as dependent variable, indicating whether the respective NPL is collateralized by real estate. As predictors, we choose the above-mentioned set of firm characteristics and buyer types and thus run logistic regressions as follows:

where \(P\left( {re\_dummy = 1{|}X} \right)\) indicates the probability of being a real estate collateralized NPL transaction conditional upon our chosen set of bank-specific characteristics. \(G\) is a specific function taking values between 0 and 1, when applying logistic regression. As a robustness check, we run logistic regressions using each buyer type as dependent variable, respectively. When running corresponding logistic regressions, the maximum likelihood estimation method is used.

4 Empirical results

4.1 Abnormal returns following NPL divestiture announcements

We begin the analysis by concentrating on the short-term valuation effect following the announcement of NPL divestitures at European banks. For each announcement, we test our first hypothesis that the announcing banks experience significant positive valuation, as measured by the cumulative abnormal returns of the vendor.

In Table 3, we report our baseline event study results around the announcement dates for the 58 banks in the sample. Panel A documents our first model, the Sharpe (1964)–Lintner (1969) one factor asset pricing model, based on the MSCI Europe. Mean CAR amounts to 1.71%, significant at the 1% level (z score: 3.76) for the [− 5; + 5] event window. In Panel B, we present a market estimation robustness, based on the STXE 600 bank index, representing the movement of the 47 largest European banks. Mean CAR declines by 29 bps to 1.42% in Panel B, again significant at the 1% level (z score: 3.90).

CAARs are tested for statistical significance using both the parametric test by Boehmer et al. (1991) and the non-parametric test procedure, introduced by Corrado and Zivney (1992), that test the hypothesis that CAARs equal zero. Our findings are robust across both statistics and we also monitor for sign changes between mean and median CARs, again affirming the result during the significant event window [− 5; + 5]. We estimate CAARs over multiple event windows, with the maximum event window being [− 20; + 20] and an estimation window of [− 140; − 21]. As additional audit of coherence, we have checked the robustness with an extended estimation window of [− 273; − 21], i.e. one full trading year, but the results are not affected quantitatively. Furthermore, we mark the occurrence of confounding events, i.e. NPL sales by banks within the event window of another deal by the same vendor, to control for a possible bias of our results. We check for robustness by including and excluding these follow-up events in the sample, but find that they should remain in the study as test results are not affected qualitatively. Furthermore, we do not detect a time-fixed effect, analyzing deals for each year separately.

We interpret our results as a clear indication affirming the first hypothesis, that announcements of NPL divestiture cause positive valuation effects, as abnormal returns are defined as actual ex-post returns over the event window, exceeding returns that would have been expected without the event taking place (MacKinlay 1997). This finding underpins earlier results by Geiger et al. (2007) on a much broader basis and—in contrast to the findings of Dahiya et al. (2003)—indicates that NPL divestiture activity generates shareholder wealth in the short-term. We assert this early finding to the fact that failing banks generally report significant proportions of NPL prior to failure or distress (Berger and DeYoung 1997; Jin et al. 2011) and thus interpret the sale of non-performing assets as a signaling about the vendor’s willingness to ensure smooth functioning after negative shocks (Granja et al. 2017). Banks currently operate under increasing regulatory and supervisory pressure to dispose of NPL (ECB 2018a, b). In this regard, the signaling about smooth functioning after negative shocks is extended by showing security holders the willingness to comply to regulatory pressure.

On the contrary, considering longer event windows around the announcement date, such as [− 20; + 20], the positive valuation effect appears to vanish over time. We interpret this finding as a first indicator that information related to NPL sale announcements tend to be priced rather quickly within the equity market and in favor of the idea of a short-term signaling effect. This potentially corroborates an information-efficient pricing of assets under distress and leads to potential negative returns in the longer term. Thus far, our findings therefore do not raise doubts about the ability of market participants to generate information efficient valuations of NPL that are primarily collateralized by real estate (cash flows). Regarding a deeper interpretation of this result, in particular regarding changes of leverage and relative size of sold NPL, more analyses during Sects. 4.2 and 4.3 appear necessary.

4.2 Real estate driven abnormal returns

An important aspect to regulators and banks’ decision makers alike is whether the valuation effect is driven by specific types of collateral. Thus, we split the overall event study sample into four smaller buckets, for each type of underlying collateral accordingly. We generally employ the same methodology and test statistics as for the overall analysis in Sect. 4.1.

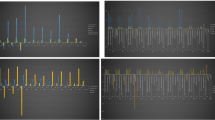

The value of real estate NPL portfolios is largely determined by (expected) rental income and (potential) property sale proceeds in the real estate market. Figure 1 compares CAARs resulting from NPL sale announcements for each day of the significant [− 5; + 5] event window of the overall sample (n = 317) as well as a subsample exhibiting NPL sales with real estate collateral (n = 188). This evaluation is based on the one-factor pricing model applying the MSCI Europe as the corresponding market return (i.e. Panel A in Table 3). Employing the market return estimation based on the bank index as robustness yields the same result, and for reasons of brevity is thus not shown in the paper (i.e. Panel B in Table 3). Figure 1 highlights that the positive valuation effect is more severe for NPL sales collateralized by real estate as compared to the overall sample. The excess return of 37 bps of the real estate sample during the event window [− 5; + 5] as compared to the overall sample is highly significant, yielding evidence in favor of our second hypothesis.

Cumulative average abnormal returns following NPL divestiture announcements. This figure shows the cumulative average abnormal return performance of the sample for real estate collateral (n = 188) and the overall NPL sale sample (n = 317) during 2012 to 2018. The Sharpe (1964)–Lintner (1969) capital asset pricing model is used by applying the MSCI Europe for the computation of CAARs

Along this line of interpretation, Table 4 displays a more detailed analysis of each collateral class separately. Regarding the real estate sample, results are significant at the 1% level (z score: 3.86). In addition to our main event window [− 5; + 5], CAARs for the [− 1; + 1] event window increases from 0.52 to 0.79% and from 0.33 to 0.62% for the [0; + 0] event window. Statistical significance of the windows [− 1; + 1] and [0; + 0] increases in the real estate sample accordingly. At the same time, the lack of significance for the non-real estate subsamples should be interpreted with caution. The power of the test statistics decreases with the smaller sample sizes of consumer loans (n = 45), corporate loans (n = 28), and mixed loans (n = 56), increasing the probability of an error of type II about the null hypothesis H0. We acknowledge from prior descriptive statistics in Table 1 that the distribution of deals in the event study sample is indeed representative for the secondary NPL market in Europe to the best of our knowledge.

Results from Fig. 1 and Table 4 together pinpoint that capital markets evaluate the sales of real estate NPL portfolios to be relatively more attractive as compared to other kinds of NPL portfolios in the short-term. We interpret this observation as the net effect of distinct real estate attributes. Its tangibility gives both vendor and the acquirer the opportunity to estimate its intrinsic value and facilitates the evaluation compared to the appraisal of corporate or unsecured consumer debt. The result affirms our second hypothesis and adds to a trending research topic, namely accounting for real estate separately in NPL research (see inter alia Adelino et al. 2016; Beck et al. 2015; Ghosh 2015). To verify a more specific possible interpretation of this finding, we perform cross-sectional analyses of abnormal returns in the next subsection.

4.3 Cross-sectional analyses of abnormal returns

We continue to analyze key value drivers of abnormal returns following NPL sale announcements by testing our third hypothesis that CARs can be explained by a set of accounting variables that proxy for idiosyncratic risk. To obtain first insights on how bank-specific vendor characteristics relate to abnormal returns, we sort corresponding CARs into deciles, applying results obtained from the [− 5; + 5] event window due to its highest statistical significance (from lowest to highest CARs; P1 to P10). For each CAR decile, we report cross-sectional averages of cumulative abnormal returns as well as cross-sectional averages of the following bank-specific variables: NPL to total loans ratio (\(npl\_tl\)) NPL to equity ratio (\(npl\_eq\)), five-year average return on assets (\(roa\_5y\)), common equity to total assets ratio (\(ceq\_ta\)), actual loan losses in percent of reserves for loan losses (\(loanloss\_rll\)), Tier 1 capital adequacy ratio (\(capad\)), ratio of sold NPL’s GBV to bank’s total assets (\(gbvnpl\_ta\)) and the Italy dummy (\(italy\_dummy\)). Table 5 summarizes corresponding results. Panel A reports findings for our overall event study sample (n = 317). Panel B presents insights obtained from the real estate subsample (n = 188).

As presented in Table 5, average cumulative abnormal returns range from lowest − 8.42% (P1) to highest 16.58% (P10) within Panel A. Notably, deals that are conducted by banks exhibiting highest NPL to total loans ratios (\(npl\_tl\)) as well as highest NPL to equity ratios (\(npl\_eq\)) and highest ratios of sold NPL’s GBV to bank’s total assets (\(gbvnpl\_ta\).) are the ones yielding highest abnormal returns (P10). We interpret this result as a first indication of a size effect, driven by the relative size of the liquidation of risky assets. Concerning the real estate subsample, average cumulative abnormal returns range from lowest − 8.53% (P1) to highest 14.01% (P10). Again, highest returnsre obtained for banks exhibiting highest NPL to total loans ratios (\(npl\_tl\)) as well as highest NPL to equity ratios (\(npl\_eq\)) and highest ratios of sold NPL’s GBV to bank’s total assets (\(gbvnpl\_ta\)). Within both panels, lowest (P1) and highest (P10) returns seem to be driven by Italian NPL deals that represent the largest country subgroup in the sample.

To analyze the relationship between bank-specific characteristics and observed abnormal returns in more detail, we next perform cross-sectional regression analyses using observed CARs for our overall sample (n = 317) as dependent variable. As explanatory variables, we apply the above-listed set of firm-specific characteristics with the exception of NPL to equity ratios (\(npl\_eq\)) to avoid potential multicollinearity issues. Additionally, we add a real estate dummy within the regression analysis, indicating whether respective NPL are collateralized by real estate. Table 6 summarizes cross-sectional regression results using CARs for the following event windows: [− 5; + 5] in Panel A, [− 10; + 10] in Panel B as well as [− 20; + 20] in Panel C. Within each panel, the left column reports results obtained from applying the MSCI Europe. The right column illustrates findings once applying the STXE 600 bank index.

As shown in Table 6, company characteristics exhibiting statistical significance in explaining CARs within the [− 5; + 5] event window are a firm’s NPL to total loans ratio (\(npl\_tl\)) (5% significance level) as well as the ratio of sold NPL’s GBV to banks’ total assets (\(gbvnpl\_ta\)) (1% significance level). Statistical significances of these variables even increase once applying the STXE 600 bank index instead of the MSCI Europe. Whereas there exists a positive economic link between a firm’s NPL to total loans ratio and its respective abnormal returns, firms exhibiting higher common equity to total assets ratios (\(ceq\_ta\)) tend to show a more negative performance. Additionally, the five-year average return on assets (\(roa\_5y\)) as well as actual loan losses in percent of reserves for loan losses (\(loanloss\_rll\)) turn statistically significant at the 5% level once applying the STXE 600 bank index rather than the MSCI Europe. These results underline various facets of a size effect. Relatively large NPL portfolio sales unburden the restructuring teams in vendor banks significantly more than smaller sales. But a portfolio sale of a given size is more helpful for a bank with a lower level of common equity because these institutions become more stable after the transaction. More ECB pressure on the weakest financial institutions to clean balance sheets from distressed assets will result in short-term above-average revaluation of bank equity.

For the [− 10; + 10] event window, the explanatory power of a firm’s NPL to total loans ratio (\(npl\_tl\)) disappears in both columns. Conversely, statistical significance of the variable \(gbvnpl\_ta\) even increases within both columns of Panel B. Once taking into account the [− 20; + 20] event window, the explanatory power of the variables \(npl\_tl\), \(roa\_5y\), \(ceq\_ta\), \(loanloss\_rll\) and \(gbvnpl\_ta\) disappears entirely. This finding confirms baseline event study results reported in Sect. 4.1. Information related to NPL sale announcements tend to be priced quickly within the equity market. Thus, the explanatory power of bank-specific characteristics concerning abnormal returns following NPL sale announcements vanishes over time (i.e. once taking into consideration longer event windows). We interpret these findings as a confirmation of our third hypothesis, stating that valuation effects observable around the announcement of NPL sales can be explained by a set of bank-specific characteristics that proxy for idiosyncratic risk, as for instance the bank’s ratio of NPL to total loans, its common equity in percent of total assets and the GBV of sold NPL in percent of a bank’s total assets.

To test for the robustness of these results, we conduct several fixed-effects regressions, leaving either NPL collateral type, buyer type, vendor bank or NPL-size constant. Fixed-effects regressions provide unbiased estimates by controlling for unobserved heterogeneity (Wooldridge 2005), taking into account that the explanatory power of bank-specific characteristics for observed CARs might vary substantially between different types of observations. For instance, the explanatory power of the relative size of sold NPL (\(gbvnpl\_ta\)) might vary considerably between different collateral types. Real estate collateralized NPL generally constitute higher burdens on banks’ balance sheets. Contrarily, the size effect might potentially disappear once controlling for consumer loans only. It is thus important to account for fixed-effects estimates within our regressions to ensure unbiased results and in doing so robustness of our third hypothesis.

When running fixed-effects regressions, we apply the least squares dummy variable model (LSDV). In line with Eq. (5), we use observed CARs for the [− 5; + 5], [− 10; + 10] as well as the [− 20; + 20] event windows as dependent variables and our previously specified set of bank characteristics as corresponding independent variables. Results of fixed-effects model specifications are provided in the Online Appendix.Footnote 5

Our main inference of reported fixed-effects regressions is that the size-effect (\(gbvnpl\_ta\)) remains statistically significant in explaining abnormal returns within all of the above-listed regression specifications (ranging between the 1 and 5% significance level). Most importantly, the size effect is shown to be independent of collateral type, buyer type or vendor bank. Our robustness tests confirm that the explanatory power of this size effect vanishes over time once taking into account longer event windows. Also, we find the NPL to total loans ratio (\(npl\_tl\)) to maintain its statistical significance within three out of four fixed-effects model specifications (ranging between the 5 and 10% significance level). Similar to the size-effect, the explanatory power of the NPL to total loans ratio (\(npl\_tl\)) disappears over time. When holding vendor banks constant, however, a firm’s NPL to total loans ratio (\(npl\_tl\)) has no statistically significant power in explaining observed CARs at all. Overall, fixed-effects regression findings underline that information related to NPL divestitures seem to be priced quickly within European equity markets. Also, in line with previously reported findings, we document supporting evidence within all fixed-effects model specifications that over longer periods (i.e. over the [− 20; + 20] event window), Italian banks seem to perform particularly poorly in comparison to the overall European market. However, the statistical relevance of banks’ common equity in percent of total assets (\(ceq\_ta\)) cannot be confirmed in any of the model specifications.

Overall, the findings of additionally conducted robustness checks still support our third hypothesis, implying that valuation effects observable around the announcement of NPL sales can be explained by a set of bank-specific characteristics that proxy for idiosyncratic risk. Most importantly, we are able to validate that positive stock market reactions are driven by a size effect.

4.4 Cross-sectional buy-side analyses

We proceed by investigating the relationship between different types of investors and previously categorized NPL collaterals. While potential vendors usually have superior knowledge about the quality of their assets, the bargaining power in divestiture situations under distress is limited. In our fourth hypothesis, we hypothesize that real estate collateralized NPL are dominantly acquired by opportunistic investors. We expect specialized institutional bidders on the buy-side to be highly experienced in the valuation of complex real estate NPL portfolios. We therefore perform logistic regressions, using the real estate dummy of our overall sample (n = 317) as the dependent variable and our chosen set of bank characteristics as well as corresponding buyer types as explanatory variables.

Table 7 summarizes results obtained from our first-step logistic regression analysis (Panel A) and corresponding margins at means for each indicator variable (Panel B).

As shown in Table 7, the probability of being a real estate collateralized NPL transaction is highest when sellers exhibit high five-year average ROAs (\(roa\_5y\)) while simultaneously having high actual loan losses in percent of reserves for loan losses (\(loanloss\_rll\)). Conversely, the probability of being a real estate collateralized transaction decreases for Italian deals. On an aggregate basis, the predicted probability of being a real estate collateralized NPL transaction is highest (0.84) for buyer type 2 (opportunity funds) and lowest for undisclosed buyers (0.19) as well as consortia of multiple buyers/securitization (0.41). Our findings imply that opportunity funds in particular tend to acquire NPL collateralized by real estate, therefore confirming our fourth and final hypothesis. We relate this finding to the specific knowledge and experience needed to cope with real estate as an asset class as well as the high potential of value creation and the risk associated within these kind of transactions.

As a robustness check, we next run logistic regressions using each buyer type as dependent variable separately. Table 8 summarizes respective regression results.

As shown in Table 8, the real estate dummy is positive and statistically significant only for buyer type 2 (opportunity funds), however, negatively significant for buyer type 3 (consortia of multiple buyers/securitization) and 5 (undisclosed investors). This finding suggests that real estate collateralized NPL tend to be acquired by opportunistic investors while simultaneously being avoided by consortia of multiple buyers and undisclosed investors. These results overall confirm our fourth hypothesis, implying that real estate collateralized NPL mainly tend to be acquired by opportunity funds.Footnote 6

5 Conclusion

This study synthesizes a unique transaction database of 476 NPL deals during the period 2012–2018. Decomposition of this data enables deeper understanding about the secondary market for loan sales under distress, which so far lacks transparency and publicly available information on a broad basis. Following the financial crisis of the past decade, financial institutions in the European bank-based system are still in the restructuring process of bad assets and effectively hold large portfolios of NPL on their balance sheets. Our analysis has regulatory implication, as the ECB currently ascribes the NPL-issue high priority, assisting with a variety of guidance measures. In particular since 2014, the core advice is active portfolio reduction, that requires banks to sell their oftentimes real estate based NPL holdings to loan investors, thus resulting in a strengthening of the secondary loan sale market.

The descriptive analysis reveals that the sell-side of the secondary market is relatively granular, while we face narrow buy-side structures. While smaller single-name transactions or portfolio baskets start with GBVs of €5 m, the largest transactions amount up to €26bn face value. These large block transactions oftentimes account for NPL disposal into bad-banks or similar government endowed entities. Based on GBV, two thirds of the collateral (66.1%) are real estate loans. The other third accounts for consumer loans (5.7%), corporate loans (4.0%) and mixed loan pools (24.2%), which represent a mixture of the other three loan types in an unknown proportion. For this reason, we estimate the actual real estate proportion to be higher. Real estate and mixed loan pools together pinpoint the dominant role of collateral in the European distressed loan sale market. Thus, the price setting for NPL portfolios is largely driven by tangible assets whose cash flow depends on rental income and property sales proceeds.

Recent empirical evidence raises doubts about the ability of financial market participants to generate information efficient valuations for real estate capital market instruments. We contribute to this stream of literature with the empirical examination of value implications for a subset of 317 NPL divestiture announcements at 58 listed banks during 2012–2018. Our results provide robust evidence in favor of a significant positive stock market reaction at vendor banks following NPL sales, which are driven by a size effect and real estate collateral in these transactions. This finding underpins earlier (more anecdotal and non-international) results by Geiger et al. (2007) on a much broader basis and indicates that capital markets perceive the realized sales prices to be attractive for vendors. While failing banks generally report significant proportions of NPL prior to failure or distress (Berger and DeYoung 1997; Jin et al. 2011), the sale of non-performing assets may be interpreted as a signaling about the vendor’s willingness to ensure smooth functioning after negative shocks (Granja et al. 2017). In addition, this signaling provides security holders with positive information about the bank’s willingness and ability to comply with increased regulatory pressure.

In regards to a potential divergence among different types of underlying collateral, we analyze each collateral class separately, detecting an excess return driven by real estate loans. We interpret this finding as evidence that capital markets evaluate the sales of real estate NPL portfolios as comparatively more attractive, compared to other kinds of NPL portfolios, such as unsecured corporate debt. We attribute this observation to the net effect of distinct real estate attributes. Its tangibility gives both vendor and the acquirer the opportunity to estimate its intrinsic value and facilitates the evaluation compared to the appraisal of corporate or unsecured consumer debt. But real estate also demands a very distinct skillset to adequately manage important features of real estate collateral in interdisciplinary teams of practitioners, representing high opportunity costs of capital for the vendor. With the sale of NPL portfolios, these very demanding management tasks are transferred out of the vendor banks and generate new capacities for highly specialized human resources.

Last, applying cross-sectional regression analyses, we find that bank-specific characteristics such as the vendor’s bad loan to total loans ratio are consistent drivers of abnormal returns, providing evidence in favor of a size effect concerning relative asset scaling. This finding undermines recent research in the banking literature, suggesting that banks are generally incentivized to sell loans to meet their (short-term) liquidity needs under the Basel III regime, either by raising capital or reducing the amount of risk-weighted assets (Boudriga et al. 2009; Irani and Meisenzahl 2017). As a consequence, bank capitalization is altered in favor of the capital adequacy ratio, making bank’s balance sheets more appealing to the security holder (Kwan and Eisenbeis 1997). Along this line of reasoning, the alteration is most accentuated if vendors decide to liquidate relevant portions of problematic assets. Finally, performing logistic regressions, we are also able to detect that real estate NPL to a large extent are acquired by opportunity funds and tend to be avoided by consortia of multiple buyers and undisclosed investors, potentially reflecting reduced opportunity costs of capital. We attribute this finding to the specific knowledge and human resources needed by investors to cope with real estate as an asset class.

Change history

07 September 2021

A Correction to this paper has been published: https://doi.org/10.1007/s11573-021-01060-x

Notes

Examples of the difficulties would be “Residential real estate” vs. “RESI”; “Deutsche Bank AG” vs. “Deutsche Bank”; “UK” vs. “England” etc.

We include an extended estimation period of 273 trading days, i.e. one full trading year, in the robustness checks. The variation did not influence the overall result.

See Appendix E for descriptive statistics of all applied variables.

The Online Appendix can be found in the online version of the article available at SSRN.

References

Adelino M, Schoar A, Severino F (2016) Loan originations and defaults in the mortgage crisis: the role of the middle class. Rev Financial Stud 29(7):1635–1670. https://doi.org/10.1093/rfs/hhw018

Arena M (2008) Bank failures and bank fundamentals: a comparative analysis of Latin America and East Asia during the nineties using bank-level data. J Bank Finance 32(2):299–310. https://doi.org/10.1016/j.jbankfin.2007.03.011

Ball R, Brown P (1968) An empirical evaluation of accounting income numbers. J Account Res 6(2):159–178. https://doi.org/10.2307/2490232

Barber BM, Lyon JD (1996) Detecting abnormal operating performance: the empirical power and specification of test statistics. J Financ Econ 41(3):359–399. https://doi.org/10.1016/0304-405x(96)84701-5

Barker CA (1956) Effective stock splits. Harvard Bus Rev 34(1):101–106

Beck R, Jakubik P, Piloiu A (2015) Key determinants of non-performing loans: new evidence from a global sample. Open Econ Rev 26(3):525–550. https://doi.org/10.1007/s11079-015-9358-8

Berger AN, DeYoung R (1997) Problem loans and cost efficiency in commercial banks. J Bank Finance 21(6):849–870. https://doi.org/10.1016/S0378-4266(97)00003-4

Binder J (1998) The event study methodology since 1969. Rev Quant Finance Account 11(2):111–137. https://doi.org/10.1023/A:1008295500105

Boehmer E, Musumeci J, Poulsen AB (1991) Event-study methodology under conditions of event-induced variance. J Financial Econ 30(2):253–272. https://doi.org/10.1016/0304-405x(91)90032-F

Boudriga A, Boulila N, Jellouli S (2009) Banking supervision and nonperforming loans: a cross-country analysis. J Financial Econ Policy 1(4):286–318. https://doi.org/10.1108/17576380911050043

Breuer W, Nadler C (2012) Real estate and real estate finance as a research field—an international overview. Zeitschrift für Betriebswirtschaft 82(S1):5–52. https://doi.org/10.1007/s11573-011-0524-1

Brown SJ, Warner JB (1980) Measuring security price performance. J Financial Econ 8(3):205–258. https://doi.org/10.1016/0304-405x(80)90002-1

Brown DT, James CM, Mooradian RM (1994) Asset sales by financially distressed firms. J Corp Finance 1(2):233–257. https://doi.org/10.1016/0929-1199(94)90004-3

Cici G, Corgel J, Gibson S (2011) Can fund managers select outperforming REITs? Examining fund holdings and trades. Real Estate Econ 39(3):455–486. https://doi.org/10.1111/j.1540-6229.2010.00304.x

Clubb C, Stouraitis A (2002) The significance of sell-off profitability in explaining the market reaction to divestiture announcements. J Bank Finance 26(4):671–688. https://doi.org/10.1016/S0378-4266(01)00169-8

Comment R, Jarrell GA (1995) Corporate focus and stock returns. J Financial Econ 37(1):67–87. https://doi.org/10.1016/0304-405X(94)00777-X

Corrado CJ (2011) Event studies: a methodology review. Account Finance 51(1):207–234. https://doi.org/10.1111/j.1467-629X.2010.00375.x

Corrado CJ, Zivney TL (1992) The specification and power of the sign test in event study hypothesis tests using daily stock returns. J Financial Quant Anal 27(3):465–478. https://doi.org/10.2307/2331331

Dahiya S, Puri M, Saunders A (2003) Bank borrowers and loan sales: new evidence on the uniqueness of bank loans. J Bus 76(4):563–582. https://doi.org/10.1086/377031

Demirgüç-Kunt A, Levine R (2004) Financial structure and economic growth: a cross-country comparison of banks, markets, and development. MIT Press, Cambridge

Dick M (2010) Der Verkauf von Non Performing Loans: eine Analyse von NPL-Transaktionen aus Bankensicht (1. Aufl. ed.). Gabler, Wiesbaden

Dimitrios A, Helen L, Mike T (2016) Determinants of non-performing loans: evidence from Euro-area countries. Finance Res Lett 18:116–119. https://doi.org/10.1016/j.frl.2016.04.008

Dolley JC (1933) Characteristics and procedure of common-stock split-ups. Harvard Bus Rev 11(3):316–326

ECB (2017) Guidance to banks on non-performing loans. https://www.bankingsupervision.europa.eu/ecb/pub/pdf/guidance_on_npl.en.pdf

ECB (2018a) Introductory statement to the press conference on the ECB Annual Report on supervisory activities 2016 (with Q&A) [Press release]. https://www.bankingsupervision.europa.eu/press/speeches/date/2017/html/se170327.en.html#qa

ECB (2018b) Second ordinary hearing in 2018 at the European Parliament’s Economic and Monetary Affairs Committee [Press release]. https://www.bankingsupervision.europa.eu/press/speeches/date/2018/html/ssm.sp181120.en.html

ECOFIN (2018) Banking Union: Council endorses package of measures to reduce risk [Press release]. https://www.consilium.europa.eu/en/press/press-releases/2018/12/04/banking-union-council-endorses-package-of-measures-to-reduce-risk/pdf

Faa LC (2019) The effects of non-performing loans disposals on banks' stock prices: evidence from Italy. POLITESI digital archive of PhD and post graduate theses. https://www.politesi.polimi.it/handle/10589/145839?mode=full&submit_simple=Show+full+thesis+record

Fama EF (1970) Efficient capital markets: a review of theory and empirical work. J Finance 25(2):383–417. https://doi.org/10.2307/2325486

Fama EF, French KR (1993) Common risk-factors in the returns on stocks and bonds. J Finance Econ 33(1):3–56. https://doi.org/10.1016/0304-405x(93)90023-5

Fama EF, Fisher L, Jensen MC, Roll R (1969) The adjustment of stock prices to new information. Int Econ Rev 10(1):1–21. https://doi.org/10.2307/2525569

Gallo JG, Lockwood LJ, Rutherford RC (2000) Asset allocation and the performance of real estate mutual funds. Real Estate Econ 28(1):165–184. https://doi.org/10.1111/1540-6229.00797

Gande A, Saunders A (2012) Are banks still special when there is a secondary market for loans? J Finance 67(5):1649–1684. https://doi.org/10.1111/j.1540-6261.2012.01769.x

Geiger F, Rottke NB, Schiereck D (2007) Marktreaktionen auf Portfolioverkäufe-Transaktionen Not leidender Immobiliendarlehen in Deutschland. Zeitschrift für immobilienwirtschaftliche Forschung und Praxis, H 3:15–16

Gentgen J (2007) Strategien deutscher Banken: der Umgang mit immobiliengesicherten Problemkrediten, vol 3. Springer, Berlin

Ghosh A (2015) Banking-industry specific and regional economic determinants of non-performing loans: evidence from US states. J Financial Stab 20:93–104. https://doi.org/10.1016/j.jfs.2015.08.004

Granja J, Matvos G, Seru A (2017) Selling failed banks. J Finance 72(4):1723–1784. https://doi.org/10.1111/jofi.12512

Huang WH, Schwienbacher A, Zhao S (2012) When bank loans are bad news: evidence from market reactions to loan announcements under the risk of expropriation. J Int Financial Mark Inst Money 22(2):233–252. https://doi.org/10.1016/j.intfin.2011.09.004

Irani RM, Meisenzahl RR (2017) Loan sales and bank liquidity management: evidence from a US credit register. Rev Financial Stud 30(10):3455–3501. https://doi.org/10.1093/rfs/hhx024

James C (1987) Some evidence on the uniqueness of bank loans. J Financial Econ 19(2):217–235. https://doi.org/10.1016/0304-405x(87)90003-1

Jin JY, Kanagaretnam K, Lobo GJ (2011) Ability of accounting and audit quality variables to predict bank failure during the financial crisis. J Bank Finance 35(11):2811–2819. https://doi.org/10.1016/j.jbankfin.2011.03.005

John K, Ofek E (1995) Asset sales and increase in focus. J Financial Econ 37(1):105–126. https://doi.org/10.1016/0304-405X(94)00794-2

Keeton WR, Morris CS (1987) Why do banks' loan losses differ? Econ Rev Federal Reserve Bank Kansas City 72(5):3–21

Klein N (2013) Non-performing loans in CESEE; determinants and impact on macroeconomic performance. In: Paper presented at the IMF Working Paper WP/13/72. International Monetary Fund, Washington D.C

Kothari S, Warner JB (2007) Econometrics of event studies. Handb Empir Corp Finance 1:3–36

Krause T, Sondershaus T, Tonzer L (2017) Complexity and bank risk during the financial crisis. Econ Lett 150:118–121. https://doi.org/10.1016/j.econlet.2016.11.026

Kwan S, Eisenbeis RA (1997) Bank risk, capitalization, and operating efficiency. J Financial Serv Res 12(2–3):117–131. https://doi.org/10.1023/A:1007970618648

Lasfer MA, Sudarsanam PS, Taffler RJ (1996) Financial distress, asset sales, and lender monitoring. Financial Manag 25(3):57–66. https://doi.org/10.2307/3665808

Lintner J (1969) The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets: a reply. Rev Econ Stat 51(2):222–224. https://doi.org/10.2307/1926735

Louzis DP, Vouldis AT, Metaxas VL (2012) Macroeconomic and bank-specific determinants of non-performing loans in Greece: a comparative study of mortgage, business and consumer loan portfolios. J Bank Finance 36(4):1012–1027. https://doi.org/10.1016/j.jbankfin.2011.10.012

MacKinlay AC (1997) Event studies in economics and finance. J Econ Lit 35(1):13–39

Maskara PK, Mullineaux DJ (2011) Information asymmetry and self-selection bias in bank loan announcement studies. J Financial Econ 101(3):684–694. https://doi.org/10.1016/j.jfineco.2011.03.019

Mori M, Ziobrowski AJ (2011) Performance of pairs trading strategy in the US REIT market. Real Estate Econ 39(3):409–428. https://doi.org/10.1111/j.1540-6229.2010.00302.x

Myers JH, Bakay AJ (1948) Influence of stock split-ups on market price. Harvard Bus Rev 26(2):251–255

Pennacchi GG (1988) Loan sales and the cost of bank capital. J Finance 43(2):375–396. https://doi.org/10.2307/2328466

Rottke N, Gentgen J (2008) Workout management of non-performing loans. J Prop Invest Finance 26(1):59–79. https://doi.org/10.1108/14635780810845163

Salas V, Saurina J (2002) Credit risk in two institutional regimes: Spanish commercial and savings banks. J Financial Serv Res 22(3):203–224. https://doi.org/10.1023/a:1019781109676

Shilling J, Wurtzebach C (2012) Is value-added and opportunistic real estate investing beneficial? If so, why? J Real Estate Res 34(4):429–461

Sharpe WF (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. J Finance 19(3):425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x

Viale AM, Kolari JW, Fraser DR (2009) Common risk factors in bank stocks. J Bank Finance 33(3):464–472. https://doi.org/10.1016/j.jbankfin.2008.08.019

Whalen G (1991) A proportional hazards model of bank failure: an examination of its usefulness as an early warning tool. Econ Rev 27(1):21–31

Woltering RO, Weis C, Schindler F, Sebastian S (2018) Capturing the value premium—global evidence from a fair value-based investment strategy. J Bank Finance 86:53–69. https://doi.org/10.1016/j.jbankfin.2017.06.009

Wooldridge JM (2005) Fixed-effects and related estimators for correlated random-coefficient and treatment-effect panel data models. Rev Econ Stat 87(2):385–390. https://doi.org/10.1162/0034653053970320

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The original version of this article was revised due to a retrospective Open Access order.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendices

Appendix A: Overview of NPL market characteristics

GBV (€bn) | Number of deals | Percentage | Cum. percentage | |

|---|---|---|---|---|

Panel A: descriptive sample (n = 476) | ||||

A: Five largest vendors | ||||

Banca Monte dei Paschi di Siena | 33.26 | 3 | 6.8 | 6.8 |

UK asset resolution (UKAR) | 30.66 | 4 | 6.3 | 13.0 |

Banco Santander | 29.70 | 4 | 6.1 | 19.1 |

NAMA | 28.14 | 19 | 5.7 | 24.8 |

UniCredit | 25.89 | 17 | 5.3 | 30.1 |

Other (174) | 342.39 | 429 | 69.9 | 100.0 |

Total | 490.05 | 476 | 100.0 | 100.0 |

B: Five largest acquirers | ||||

Consortium/securitizations | 77.82 | 32 | 15.9 | 15.9 |

Cerberus | 74.11 | 34 | 15.1 | 31.0 |

Lone Star | 41.75 | 14 | 8.5 | 39.5 |

Blackstone | 39.58 | 14 | 8.1 | 47.6 |

Fortress | 18.32 | 5 | 3.7 | 51.3 |

Other (141) | 238.47 | 377 | 48.7 | 100.0 |

Total | 490.06 | 476 | 100.0 | 100.0 |

C: Five largest markets | ||||

Italy | 167.37 | 140 | 34.2 | 34.2 |

Spain | 113.86 | 113 | 23.2 | 57.4 |

UK | 61.68 | 51 | 12.6 | 70.0 |

Ireland | 54.38 | 48 | 11.1 | 81.1 |

Multinational | 22.83 | 13 | 4.7 | 85.7 |

Other (21) | 69.93 | 111 | 14.3 | 100.0 |

Total | 490.06 | 476 | 100.0 | 100.0 |

Panel B: event study sample (n = 317) | ||||

A: Five largest vendors | ||||

Banco Santander | 32.05 | 15 | 10.4 | 10.4 |

Unicredit | 26.49 | 21 | 8.6 | 19.0 |

Banca Monte dei Paschi | 25.56 | 3 | 8.3 | 27.3 |

BBVA | 21.70 | 7 | 7.0 | 34.3 |

Banco de Sabadell | 20.38 | 19 | 6.6 | 40.9 |

Other (53) | 182.22 | 252 | 59.1 | 100.0 |

Total | 308.40 | 317 | 100.0 | 0.0 |

B: Five largest acquirers | ||||

Consortium/securitizations | 52.45 | 24 | 17.0 | 17.0 |

Cerberus | 45.77 | 24 | 14.8 | 31.8 |

Blackstone | 38.98 | 9 | 12.6 | 44.5 |

Lone Star | 23.05 | 9 | 7.5 | 52.0 |

Fortress | 17.48 | 3 | 5.7 | 57.6 |

Other (92) | 130.67 | 248 | 42.4 | 100.0 |

Total | 308.40 | 317 | 100.0 | 0.0 |

C: Five largest markets | ||||

Italy | 103.23 | 91 | 33.5 | 33.5 |

Spain | 101.40 | 69 | 32.9 | 66.4 |

Ireland | 30.48 | 26 | 9.9 | 76.2 |

UK | 26.58 | 34 | 8.6 | 84.9 |

Germany | 8.23 | 15 | 2.7 | 87.5 |

Other (21) | 38.48 | 82 | 12.5 | 100.0 |

Total | 308.40 | 317 | 100.0 | 0.0 |

Appendix B: Distribution of NPL transactions per year

Year | Panel A: Descriptive sample (n = 476) | Panel B: event study sample (n = 317) | ||||

|---|---|---|---|---|---|---|

Number of deals | Percentage | Cumulative percentage | Number of deals | Percentage | Cumulative percentage | |

2012 | 2 | 0.2 | 0.2 | 2 | 0.6 | 0.6 |

2013 | 84 | 17.9 | 18.1 | 53 | 16.7 | 17.4 |

2014 | 21 | 4.4 | 22.5 | 22 | 6.9 | 24.3 |

2015 | 100 | 21.0 | 43.5 | 66 | 20.8 | 45.1 |

2016 | 102 | 21.4 | 64.9 | 55 | 17.4 | 62.5 |

2017 | 95 | 20.0 | 84.9 | 70 | 22.1 | 84.5 |

2018 | 72 | 15.1 | 100.0 | 49 | 15.5 | 100.0 |

Total | 476 | 100.0 | 100.0 | 317 | 100.0 | 100.0 |

Appendix C: Visualization of the data cleaning process by type of source

Appendix D: Variable definitions and computational details

# | Abbrev. | Computational details (datastream definitions) |

|---|---|---|

1 | \(npl\) | Non-Performing Loans (WC02285) represent the amount of loans that the bank foresees difficulty in collecting It includes but is not restricted to: Non-accrual loans; Reduced rate loans; Renegotiated loans; Loans past due 90 days or more It excludes: Assets acquired in foreclosures; Repossessed personal property |

2 | \(npl\_tl\) | Non-Performing Loans % Total Loans (WC15061) is computed as a firm's Non-Performing Loans/Loans-Total * 100 |

3 | \(npl\_eq\) | Non-Performing Loans % Equity (WC15067) is calculated as a bank's Non-Performing Loans/Common Shareholders' Equity * 100 |

4 | \(roa\_5y\) | Return on Assets—5 Yr Avg (WC08330) is the arithmetic average of the last five years of Return on Assets (ROA) ROA (Banks): Net Income before Preferred Dividends + ((Interest Expense on Debt-Interested Capitalized) × (1 − Tax Rate))/Average of Last Year's (Total Assets − Customer Liabilities on Acceptances) and Current Year's (Total Assets − Customer Liabilities on Acceptances) × 100. Customer Liabilities on Acceptances only subtracted when included in Total Assets ROA (Insurance Companies): (Net Income before Preferred Dividends + ((Interest Expense on Debt-Interest Capitalized) ×(1-Tax Rate))) + Policyholders' Surplus)/Average of Last Year's and Current Year’s Total Assets × 100 ROA (Other Financial Companies): (Net Income before Preferred Dividends + ((Interest Expense on Debt-Interest Capitalized) × (1 − Tax Rate)))/Average of Last Year's (Total Assets − Custody Securities) and Current Year’s (Total Assets − Custody Securities) × 100 |

5 | \(ceq\_ta\) | Common Equity % Total Assets (WC08241): Banks: Common Equity/(Total Assets − Customer Liabilities on Acceptances) × 100 Customer Liabilities on Acceptances only subtracted when included in Total Assets Insurance Companies: (Common Equity + Policyholders' Equity)/Total Assets × 100 Other Financial Companies: Common Equity/(Total Assets − Custody Securities) × 100 |

6 | \(loanloss\_rll\) | Actual Loan Losses % Reserves for Loan Losses (WC15085) are computed as a bank's Net Loan Losses/Reserve for Loan Losses × 100 |

7 | \(gbvnpl\_ta\) | GBV of sold NPL % total assets |

8 | \(capad\) | Capital adequacy ratio tier 1 (WC18157) represents the ratio of Tier 1 Capital to total risk-weighted assets, calculated in accordance with banking regulations and expressed as a percentage. Tier 1 Capital includes common shareholders’ equity and qualifying preferred stock, less goodwill and other adjustments |

Appendix E: Summary statistics of included variables

Overall sample (n = 317) | Real estate subsample (n = 188) | |

|---|---|---|

Panel A: non-performing loans in €bn | ||

Mean | 21.50 | 18.50 |

Standard deviation | 20.02 | 18.50 |

Min. | 0.13 | 0.59 |

Max. | 84.40 | 79.80 |

Panel B: non-performing loans % total loans | ||

Mean | 9.79 | 9.26 |

Standard deviation | 7.90 | 6.55 |

Min. | 0.30 | 0.30 |

Max. | 63.13 | 31.77 |

Panel C: non-performing loans % equity | ||

Mean | 97.18 | 93.06 |

Standard deviation | 82.26 | 75.04 |

Min. | 3.13 | 3.13 |

Max. | 541.51 | 331.13 |

Panel D: return on assets—5 year avg | ||

Mean | 0.61 | 0.64 |

Standard deviation | 0.55 | 0.54 |

Min. | − 2.63 | − 1.06 |

Max. | 7.17 | 7.17 |

Panel E: common equity % total assets | ||

Mean | 6.65 | 6.62 |

Standard deviation | 2.80 | 3.18 |

Min. | 2.91 | 2.91 |

Max. | 40.34 | 40.34 |

Panel F: actual loan losses % reserves for loan losses | ||

Mean | 22.85 | 25.84 |

Standard deviation | 23.33 | 26.57 |

Min. | − 25.87 | − 25.87 |

Max. | 123.48 | 123.48 |

Panel G: capital adequacy ratio tier 1 | ||

Mean | 13.54 | 13.63 |

Standard deviation | 1.66 | 1.74 |

Min. | 9.04 | 9.04 |

Max. | 20.10 | 20.10 |

Panel H: GBV of Sold NPV % total assets | ||

Mean | 0.77 | 0.64 |

Standard deviation | 1.91 | 1.41 |

Min. | 0.0026 | 0.0026 |

Max. | 9.36 | 9.36 |

Appendix F: Collateral mapping procedure

Clear Identifier → 3rd Order (49 Identifiers Left) | Grouping → 2nd Order (29 Identifiers Left) | Grouping → 1st Order (4 Identifiers Left) |

|---|---|---|

Consumer Loans | Consumer Loans | Consumer Loans |