Abstract

This paper examines whether the economic crisis induced by the COVID-19 pandemic exhibits a Schumpeterian “cleansing” of less productive firms. Using firm-level data collected for 34 economies up to 18 months into the crisis, the study finds that less productive firms have a higher probability of permanently closing during the crisis, suggesting that the process of cleansing out unproductive activities is occurring. The paper also uncovers strong and negative relationships of firm exit with digital presence and with innovation. These relationships are driven by small firms. The study further finds that a burdensome business environment increases the probability of firm exit, also driven by small firms, and that a negative relationship exists between firm exit and age. Finally, evidence shows that the cleansing process is disrupted in countries which have introduced policies imposing a moratorium on insolvency procedures.

Plain English Summary

The purpose of this analysis is to investigate whether firms that are more productive are less likely to cease operation during the economic crisis induced by the COVID-19 pandemic. To verify this hypothesis, the paper uses data on firm characteristics, productivity, and status of operation from 34 countries. The data on firm characteristics and productivity were collected before the crisis, while data on the operating status were collected within 18 months since the appearance of the coronavirus. The results of the paper show that indeed, more productive firms are more likely to survive the crisis. In addition, businesses that have been in operation for longer, or ones which have a website or have introduced a new product in the years before the crisis are more likely to continue existing. The positive role of digitalization and innovation is true especially for small firms. Conversely, those businesses which have to spend more time in compliance with government regulations are less likely to survive. The policy implications show the importance of digitalization and innovation, the vulnerabilities of small firms, and the significance of good governance.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The COVID-19 crisis started as an exogenous health shock that was followed by an unprecedented shutdown of businesses in specific industries, lockdown measures and social distancing guidelines introduced by governments to contain the spread of the virus, and an overall sense of insecurity. The combination of these events has exposed firms to supply and demand shocks which have reinforced each other and have affected countries around the world in a highly synchronized manner (Baqaee & Farhi, 2022; Guerrieri et al., 2022; Milani, 2021). The impact of these shocks resulted in firms’ closure in some cases. Within the context of this unprecedent challenge a question arises: is the major economic shock induced by the COVID-19 pandemic “cleansing” out unproductive firms, in line with the creative destruction process postulated by Schumpeter (1939), or is the crisis displacing productive firms?

Evidence on the effects of COVID-19 on firm exit is growing as data keep being collected while we keep living in the pandemic. This question, however, is still open. Earlier analyses on firm exit were predominantly concentrated on developed economies and focused mainly on the magnitude of exit. In the USA, using a range of existing data sources, Crane et al. (2020) found elevated exit rates, mostly among small firms and particularly in industries most sensitive to social distancing, with a 50% increase in permanent exit rate of restaurants, relative to historical rates. Another study based on surveys conducted immediately at the beginning of the crisis, in March and April 2020, showed a permanent exit rate of about 2% (Bartik et al., 2020). Still in the USA, using household-surveys, Fairlie (2020) estimates a drop of 22% of active businesses in the first 3 months of the lockdown.

Another strand of research, also at the beginning of the pandemic, has estimated the exit and survival duration through modeling the financial liquidity of firms. In Japan, estimates show a 10% increase in exit rates relative to the year prior to the COVID-19 crisis (Miyakawa et al., 2020). A large increase in the failure rate of SMEs under COVID-19, absent government support, was found also for 17 European countries (Gourinchas et al., 2020). Attempts have been made to model the liquidity cushion of firms in order to estimate the survival time of businesses. Bosio et al. (2020) show that the median firm has the means to survive between 8 and 14 weeks of total closures; however, the findings fail to support the Schumpeterian process of creative destruction. Banerjee and Kharroubi (2020) find that high short-term debt and low earnings relative to interest expenses are the two most significant financial predictors of firm exits during COVID-19.

Several months into the pandemic, studies have examined the impact of COVID-19 on the performance of surviving entrepreneurship and small businesses. Using data from California, Fairlie and Fossen (2021) show that, in the immediate aftermath of the outbreak of the COVID-19 pandemic, taxable sales declined by 17% and that businesses affected by lockdowns lost 91% of sales, putting them at significant risk of exit. However, online sales grew by 180%, highlighting the importance of digitalization to survive the pandemic. The social distancing adds another layer of challenge to business with less flexibility. Firms that adopted higher rates of working-from-home practices for their employees performed better, as shown in the USA by Zhang et al. (2021). Other studies looked at factors that helped firms’ survival. Evidence from Germany, for example, shows that the COVID-19 pandemic has placed a significant financial strain on small businesses, which would have gone bankrupt without some form of government assistance (Dörr et al., 2021). Other tools that are found to be effective for entrepreneurial ventures survival in times of economic distress are bootstrap financing measures (Block et al., 2022) and online communities where entrepreneurs came together and support each other (Meurer et al., 2022).

In parallel, as comparable firm-level data in developing economies became available, studies have extended the analysis of the impact of the COVID-19 pandemic on firms moving beyond the individual country investigations or focusing on advanced economies. Early evidence shows that the impact of the pandemic is more pronounced for firms in Sub-Saharan Africa despite the greater likelihood of adjusting operations to cope with the shock (Aga & Maemir, 2021). Using a dataset including 34 countries worldwide, Amin and Viganola (2021) show that firms with better access to finance were significantly less likely to experience a decline in sales 6 to 9 months after the pandemic was declared by the World Health Organization in March 2020. Moreover, the availability of these rich cross-country datasets has allowed extending the analysis to firm exit. Grover and Karplus (2021) find that better management practices like target-setting, monitoring, incentives, and operational practices are associated with a higher likelihood of survival for manufacturing firms, but not for firms in services sectors. Liu et al. (2021a) find that firm survival is closely associated with multi-establishment firms and state ownership, while foreign-owned firms and financially constrained businesses are more likely to interrupt or cease their operations. Other evidence points to a higher likelihood of closures (and for longer periods) by female managed firms (Liu et al., 2021b) and to a positive effect of having a website (Wagner, 2021). All these studies define firm exit either as temporary or permanent closure.

None of these studies look at the relationship between firm permanent exit and firm productivity. In the context of the COVID-19 crisis, some studies have looked at the effect of the crisis on productivity. Bloom et al. (2020), for example, analyze the effect of COVID-19 on productivity in the UK showing a reduction in private sector TFP by up to 5% in 2020. Hu and Zhang (2021), using financial data on firms worldwide, assess the impact of COVID-19 on corporate performance showing deterioration in firm performance during the pandemic. The relationship between productivity and exit is not analyzed in these studies either. Several studies have shown that firm productivity is a significant determinant of firm exit in a non-crisis situation (Aga & Francis, 2017; Baily et al., 1992; Fariñas & Ruano, 2005; Hopenhayn, 1992; Olley & Pakes, 1996), together with other factors like productive efficiency (Dimara et al., 2008) and innovation (Cefis & Marsili, 2005, 2012). Empirical analyses on firms’ responses during previous crises have shown mixed evidence. A strand of empirical evidence supports the idea that recessions intensify resource reallocation (Davis & Haltiwanger, 1992; Davis et al., 1996) and generate productive cleansing (Carreira & Teixeira, 2008; Foster et al., 2001). Other studies, however, suggest that during crises the cleansing effect may not be present, or even reversed (Baden-Fuller, 1989; Carreira & Teixeira, 2016; Foster et al., 2016; Hallward-Driemeier & Rijkers, 2013).

This paper builds on the aforementioned literature. Using World Bank Enterprise Surveys (ES) data collected for 34 countries immediately before and during the COVID-19 crisis, the paper analyzes the association between the probability of permanently exiting the market and firm productivity during the pandemic across countries. The role of mitigating and exacerbating factors is also explored. One caveat of the analysis is that the data do not allow us to distinguish between exits that would have occurred even in absence of the pandemic because of the firm dynamic process (natural exit) and those that happened because of the pandemic (excess exit). As such we cannot tell what would have been the association productivity-exit in absence of the COVID-19 crisis. What the paper does, for a subset of countries for which data are available, is to investigate whether the COVID-19 pandemic changed the association between firm exits and productivity as well as between firm exits and other relevant factors compared to previous years. Moreover, the paper investigates whether policies enacted by governments to support businesses during the COVID-19 pandemic have changed the association between productivity and firm exit.

Our results show a strong and negative relationship between labor productivity and firm exit during the COVID-19 crisis, suggesting that, unlike in other recent crises, the process of cleansing out unproductive arrangements is at play. These results extend beyond labor productivity to value added per worker. The negative relationship between productivity and firm exit may be explained by the unique characteristics of the COVID-19 crisis. Many firms entered the COVID-19 pandemic with high levels of debt, because of the 2008–2009 global financial crisis; this may have affected their capacity to access additional bank financing. At the same time, firms experienced a limited capacity to substitute across external financing sources given that all markets across all countries have been simultaneously hit (Didier et al., 2021). As such, conditions internal to the firms, including productivity and firm’s ability to quickly adapt to the changed situation, may have played a critical role in determining firm survival. Furthermore, the productivity-enhancing reallocation detected during the COVID-19 crisis is attenuated by the extensive government interventions introduced in many countries early in the pandemic to keep firms afloat.

The paper also identifies some mitigating factors. In line with a recent study (Wagner, 2021), we find a negative relationship between having a digital presence and the likelihood of permanently exiting the market during the pandemic, driven by small firms. The importance of focusing on the role of digitization as a support mechanism during crises has been highlighted also by Belitski et al. (2021) in their paper on the effects of the pandemic on small businesses and entrepreneurship. Similarly, we also find that firms that introduced a product innovation in the years before the crisis are less likely to exit the market. This relationship is also driven by small firms. This confirms the results of previous studies that found how innovation and the ability to adapt to market conditions determine the survival of firms in a non-crisis situation (Cefis & Marsili, 2005, 2012; Kato et al., 2021; Ugur & Vivarelli, 2020) as well as during crisis (Sidorkin & Srholec, 2014). Moreover, firms that invested in the purchase of fixed assets prior to the crisis are also less likely to have ceased operation. As expected, firm age is negatively correlated to firm exit, in line with the broader empirical evidence on firm survival in non-crisis situations (Jovanovic, 1982). Cumbersome regulations, as measured by having senior management spend time dealing with them, have a strong positive association with firm exit. These findings are in line with previous studies that show how policy-induced distortions can create disadvantages for firms with negative effects on firm performance (Dollar et al., 2005; Fisman and Svensson, 2007; Bigsten & Söderbom, 2006; Aterido et al., 2011) and on firm survival (Aga & Francis, 2017).

Extending the analysis to account for government interventions, the paper finds that the adoption of undifferentiated early policies imposing some form of moratorium on insolvencies have severed the productivity-exit relationship, favoring the survival of otherwise unviable firms. From a welfare perspective, besides the burden of high fiscal costs, this may impose indirect costs in the longer term; keeping distressed firms alive may severely obstruct business dynamism and structural change (Dörr et al., 2021). While it was important to intervene in support of the economy at the beginning of the pandemic, the process of ‘‘cleansing’’ out unproductive arrangements to free up resources for more productive uses is critical in facilitating recovery and growth. Therefore, further studies to empirically investigate the impact of the policy measures adopted in the different stages of the crisis on resource allocation would be important. Finally, concerning the comparison crisis with non-crisis, the results show that the negative association labor productivity-exit is a relevant determinant of firm survival during the COVID-19 crisis together with having a digital presence.

To summarize, the study contributes to the literature in the following ways. First, it uses nationally representative firm-level data for 34 economies to assess whether firm productivity contributes to firm exit during the COVID-19 crisis, also controlling for other determinants that may affect firm exit. Second, it uses a measure of firm exit that fully exploits the richness of the available data. Firm exit is measured as the permanent exit from the market based on available ES data collected immediately before the declaration of the COVID-19 pandemic, used as baseline, and three rounds of COVID-19 ES data, used as follow-up. Having up to four data points allowed to keep track of firms over time, taking into consideration not only the effects in the immediate aftermath of the crisis but also the effects after 18 months since the declaration of the pandemic. One limitation of our analysis is that the data do not allow us to assess the extent to which the displacement of less productive firms is actually leading to a more productive allocation of resources. A broader assessment of the reallocation process will be possible in the medium to long run. Third, the paper sheds light on the role of innovation and digitalization for firm performance, especially for small firms, uncovering suggestive evidence that the adoption of product innovation and the presence in the digital world are important elements for firms to survive through economic downturns.

The rest of the study is structured as follows. Section 2 provides the conceptual framework and literature review; Section 3 provides data details and summary statistics; Section 4 details the empirical strategy; Section 5 provides the results; conclusions are provided in Section 6.

2 Conceptual framework and related literature

The relationship between survival and productivity of firms has been formalized in several theoretical and empirical papers. In the standard frameworks, firms behave with the objective of profit maximization, constrained by a budget function, and are continuously faced with the choice to continue operating or to exit the market. As illustrated in the model developed by Ericson and Pakes (1995) and Olley and Pakes (1996), every firm compares the expected discounted future profit with the opportunity cost of continuing a business, linking the decision to continue operations to its productivity. Exits from the market occur when the profits fall below the threshold of variable costs in the simplest form. Extensions have added complexity to this framework to include additional dimensions that may simultaneously affect firm’s decision such as heterogenous firm-level characteristics, product lifetime, openness to trade, and market concentration (Agarwal & Gort, 2002; Ghemawat & Nalebuff, 1985; Jovanovic, 1982; Klepper, 1996).

Productivity is not only a critical determinant of firm survival, as it measures a firm’s efficiency and profitability, it also reveals important information about the efficiency of the market in which firms operate. In a well-functioning market with fair competition, more productive firms survive while less productive firms exit the market. Such dynamic allows for continuous reallocation of resources to their highest value of use. Moreover, with the threat of entry, existing businesses are under pressure to find ways to increase their efficiency, often through innovative activity. The fluidity of markets, through changing conditions and new entrants, continually raises the required productivity to remain in operations.

Explaining the interlinkages between productivity and firm survival has been under much scrutiny in the field of industry dynamics. In line with the Schumpeterian growth theory (Aghion et al., 2015), several studies have shown that firm survival occurs primarily on the basis of productivity differentials, i.e., small, less efficient, and younger firms, have a higher likelihood of exit than their more efficient counterparts (Hopenhayn, 1992; Jovanovic, 1982; Melitz, 2003; Melitz & Ottaviano, 2008). A vast literature of empirical evidence (Baily et al., 1992; Fariñas & Ruano, 2005; Olley & Pakes, 1996) corroborates this hypothesis. However, some studies have shown mixed evidence. Even in good economic times, the cleansing of less productive firms is bounded by institutional arrangements. Aga and Francis (2017) provide a comprehensive analysis of emerging and developing countries showing that, in normal times, firm productivity and the age of the firm are significant determinants of firm exit. However, the findings highlight the importance of free markets and good institutions as the effects of productivity are weakened in low-income economies, economies with limited openness to international trade, and economies with cumbersome bankruptcy procedures.

Other studies have focused on the role of economic downturns. These studies postulate that beyond the competitive forces in the market, economic downturns increase the competitive pressures, making productivity differentials more impactful in determining firm survival (Caballero & Hammour, 1996; Gomes et al., 2001; Hall, 1995). Economic downturns accentuate the firm’s choice of continuing or exiting as generally firms are faced with a dual impact of declining demand and more constrained access to financing. Such circumstances, in well-functioning markets, give a comparative advantage to firms that make more efficient use of resources—hence are more productive—thereby reducing the cost of the choice to continue operating. Conversely, the relatively less productive firms have a higher opportunity cost to remain in the market.

The strand of empirical literature on cleansing during economic downturns has a greater variety of evidence. In prior economic crises, the notion of creative destruction is shown to be weaker than expected. Baden-Fuller (1989) studied the British recession during the 1980s and found that during the decline of the British steel castings industry, when a quarter of productive capacity declined in just 4 years, many of the businesses that closed were more profitable than the surviving ones. Foster et al. (2016) found that during the 2007–2009 Great Recession the extent of the cleansing effect in the USA manufacturing sector was less pronounced than expected. Ouyang (2009) provides evidence that times of economic distress destroy high-productivity firms during their infancy. Additional evidence of a failure of a cleansing phenomenon during an economic crisis comes from the East Asian financial crisis in the 1990s. The impact on the Indonesian manufacturing sector had driven firms out of business indiscriminately of their productivity in the immediate period of the crisis (Hallward-Driemeier & Rijkers, 2013). The Schumpeterian cleansing was restored shortly thereafter.

The study of resource reallocation is beyond the scope of this analysis; however, it is important to note that while some empirical evidence may point to a cleansing of unproductive firms during an economic downturn, the resource reallocation may not necessarily be welfare enhancing. Barlevy (2002) examines the reallocation of labor during business cycles and shows that recessions can exacerbate search friction of jobs resulting in less productive matches for longer periods of time. Findings from the Great Recession in the USA have shown that the reallocation has been less productivity-enhancing than in previous recessions (Foster et al., 2016). Evidence from Portugal shows that while the productivity-survivability relationship exists, the re-allocative efficiency is not confirmed as the entry rate decreased while firm exit spiked (Carreira & Teixeira, 2016).

While it is too early to assess whether resource reallocation holds during the current economic downturn, it is possible to assess whether the cleansing effect is in place during the COVID-19 crisis and whether the COVID-19 crisis differs from previous crises. The COVID-19 pandemic brought up unprecedented challenges, being marked, as never before, with mass restrictions of movement and human interactions in a globally interconnected economy. Past economic crises (such as the debt crisis of the 1980s, the 1997–1998 Asian financial crisis, and the 2008–2009 global financial crisis) originated from financial vulnerabilities. In contrast, the source of the COVID-19 crisis is an exogenous health shock that exposed firms to a combination of a supply shock and a demand shock which have reinforced each other (Baqaee & Farhi, 2020; Guerrieri et al., 2022; Eichenbaum et al., 2022). The scope and scale of the crisis are also more extensive than in past macro-financial crises, making it a unique and rare event. The COVID-19 shock has transmitted quickly within and across borders, affecting firms and industries across the globe. In these unprecedented circumstances, identifying mitigation measures, including raising additional funds, became particularly challenging. During the COVID-19 crisis, unlike during other crises, firms experienced a limited capacity to substitute across external financing sources given that all markets across all countries have been simultaneously hit (Didier et al., 2021). In response to this situation, many governments around the world swiftly enacted policies aimed to serve as shock-absorbers. They were directed both towards increasing liquidity as well as supporting adjustments in expenses, including payroll, supplier payments, and other overhead costs. Such policies, which include, among others, cash transfers, increased access to credit, labor subsidies, and suspension of insolvency procedures, played a key role in stabilizing the economy and keeping firms afloat. These interventions, which served as a lifeline to businesses to mitigate the impact of the pandemic, may have affected the cleansing process.

Examining to which extent the cleansing process holds in the COVID-19 pandemic is the aim of this analysis. There are various channels through which the COVID-19 crisis could affect the productivity-survivability relationship. The extent of the shock could be so strong and widespread to sever the relationship between productivity and firm exit or government actions could disrupt the cleansing process by providing indiscriminate support to prevent closures (Dörr et al., 2021). Conversely, the relatively more productive firms may be able to respond to the changing circumstance in a more efficient manner compared to those which are less productive, favoring the cleaning process. The COVID-19 pandemic could exacerbate the differential in productivity among firms as resources become scarcer and borrowing becomes harder. Furthermore, the productivity differential is a result of production practices, management abilities, and technological adaptation (Syverson, 2011). Since the COVID-19 pandemic was marked with mass restrictions on movement and conducting business remotely, the importance of such characteristics is amplified and thereby may affect the productivity-survivability relationship. Either less productive firms succumb to the perils of the crisis and have potential long-term economic gains through reallocation of resources; or the global pandemic has had a detrimental effect across businesses regardless of their efficiency and innovativeness, causing permanent scarring to the economy. The next section discusses the data used to test these claims.

3 Data and summary statistics

The main data used in this paper consist of establishment-level datasets for 34 economies. The sample includes 28 countries in Europe and Central Asia (ECA) and 6 countries in the Middle East and North Africa Region, East Asia and Pacific, and Sub-Saharan Africa. The dataset combines the World Bank Enterprise Surveys (ES) and the COVID-19-ES Follow up Survey (COV-ES). The COV-ES builds a dataset with ES firms as baseline and with up to three rounds of follow-up data collection. The follow-up data collection started in May 2020 for the first round, in November 2020 for the second round, and in March 2021 for the third round; fieldwork lasted about 1 month for each country in each round. Three rounds of COV-ES were collected in 19 economies, two rounds in 5 economies, and one round in 10 economies (see Table 13 in the Appendix for a detailed description of the sample composition).Footnote 1 While ES and COV-ES data are available for a total of 45 countries, the paper restricts the sample to the countries where the ES were completed either in 2019 or in 2020. This was done to minimize the time between the different moments in which firms were contacted, thereby mitigating any possible biases of identifying the firm’s operating status and the time of exit, and for having up-to-date explanatory and control variables of the firm’s characteristics right before the start of the pandemic. For a subsample of 28 countries for which data are available conducted in 2013 were combined with the data from the 2019 to replicate the analysis for a pre-crisis situation, however this analysis is subject to some of the biases discussed earlier.

The ES are nationally representative surveys of formal (registered) firms with at least five employees operating in the manufacturing or services sectors of the economies.Footnote 2 The data are fully comparable across countries and are collected via face-to-face interviews with business owners or top managers. A common sampling methodology, stratified random sampling, is used in all surveys, together with a standardized survey instrument and a uniform methodology of implementation. For each economy, the sample is stratified by industry, firm size, and location within the country. Sampling weights are provided in the surveys and are used to correct for unequal probability of selection as well as for ineligibility. The 2019–2020 ES data serve as a baseline for comparisons, thus measuring the scenario immediately before the pandemic.

The COV-ES builds on the ES methodology and it is also fully comparable across countries. Questions on the impact of the COVID-19 crisis were administered through phone interviews to all firms in the 2019–2020 ES sample. Besides collecting data on the effect of COVID-19 on firm operations,Footnote 3 the COV-ES recontacted all firms interviewed during the ES to determine their operating status. The same process was repeated during the second and the third rounds of COV-ES in select economies. Using this information, the firms interviewed in an initial round of the survey at time t (baseline ES) were coded according to their operating status as of the subsequent survey rounds, at time t + n (COV-ES round 1, COV-ES round 2, and COV-ES round 3). In each country, the latest information available is used; i.e., in countries with three rounds of COV-ES data collection, the exit is measured by referring to the situation in the third round, while the first round is used for countries with one round of COV-ES data only, and the second round only for countries which have only two rounds of the COV-ES.

3.1 Firm exit

Combining the information from the baseline and the follow-up surveys, two different measures of permanent exit are computed:

Confirmed exit—which includes establishments in the baseline that declared to be permanently closed during the COV-ES.

Assumed exit—which in addition to confirmed exits, includes firms that could not be contacted during fieldwork and were, therefore, assumed to have permanently closed.

The specific criteria used to define permanent firm exit upon recontacting a firm are presented in Table 14 in the Appendix.

There are arguments for and against concerning the use of either of the two measures. On one hand, the use of the confirmed exit is more conservative as this measure prudently includes only firms that could be contacted and that explicitly declared to have permanently ceased operations. This argument could be considered particularly suitable for the current study due to the conditions imposed by the pandemic where managers or business owners may not have been able to answer the phone due to temporary closures or changes in contact details, and yet the firm be still in the market. Therefore, restricting the exit to the confirmed cases may avoid the risk of potentially overestimating the actual firm exit. On the other hand, however, establishing a line of communication with firms that ceased operations has proven an extremely challenging task, even more with surveys conducted over the phone. Moreover, it is difficult to imagine a manager of a firm that exited the market answering the phone and participating in a firm-level survey. Under these circumstances, relying on the confirmed exit measure may underestimate the real magnitude of firm exit, making the use of the assumed exit a preferable option.

The paper follows this second approach and uses the assumed exit as the main measure of firm permanent exit from the market. The appropriateness behind the use of assumed exit is two-fold. First, as the baseline data collection was recently completed the contact information is predominantly up-to-date and therefore the risk of failing to track down the respondents is minimal. Second, in most of the countries in the sample, the follow-up data collection was conducted in three rounds. As such, attempts to contact firms were made at three different points in time, therefore further reducing the risk that the lack of an answer was due to a temporary closure. Nonetheless, to account for the potential concerns from using the assumed exit measure, robustness checks are conducted by using the confirmed exit variable.Footnote 4 It is worth mentioning that unlike previous papers on firms’ survival during COVID-19 (Grover & Karplus, 2021; Liu, et al., 2021a, Liu et al., 2021b, and Wagner, 2021), this paper does not include among “exiters” the firms that temporarily interrupted operations due to the COVID-19 outbreak. Focusing on temporary closures might generate confounding effects as, in most cases, temporary closures were mandated by local or national governments to curb the transmission of the disease and are not necessarily linked to productivity. Finally, one caveat that should be taken into consideration in both cases is that firm exit can be computed only for firms in the sample at time t and does not consider firms that may have entered the market after time t and then exited.

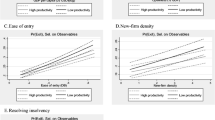

A detailed description of the explanatory and control variables used in the analysis is provided in Table 1, while Table 2 provides the summary statistics for the establishments in the sample separately for survivors and exiting firms.Footnote 5 Finally, Fig. 1 displays the kernel density functions for labor productivity, showcasing the differences in the distributions between the two sub-groups of the population. The density function that characterizes the labor productivity distribution for firms that did not exit the market (non-exiters) is further toward the right of the labor productivity density function for firms that did exit the market (exiters), showing that on average less productive firms were more likely to go out of business at different levels of productivity. While the evidence seems to support the idea of a “cleansing out” effect of the crisis, this does not mean that there is no destruction of highly productive firms. In the upper tail of the distribution, the labor productivity density functions of exiters and non-exiters converge, indicating a similar level of productivity for exiters and non-exiters.

Kernel density functions for labor productivity. Note: the sample is restricted to the observations included in the baseline regression (Table 3, column 5)

4 Empirical strategy

The baseline regression in this paper estimates the following equation:

where the subscript i denotes each firm; j the sector of activity (2-digit ISIC rev.3.1), and k the within-country location where the firm is located. The dependent variable \(Exit\) is the proxy for firm’s permanent exit from the market and it is built, as discussed above, for each firm from the ES baseline (at time t) based on their operating status at the time of the latest round of follow-up surveys (time t + n). \(Productivity\), our main explanatory variable, is the variable that captures firm performance; Firm Controls is a vector of establishment-level controls for firm characteristics and business environment. Measures for the main variable and for the controls are discussed below. The other terms are as follows: SFE, a set of dummies representing the sector of activity (sector fixed effect); LFE, a set of dummy variables indicating the within country location to which the firm belongs (location fixed effects); and TFE a set of dummies to capture the time between surveys (time fixed effect).Footnote 6 Finally, \(\epsilon\)is the usual error term. The regressions are estimated using a logistic regression model, as it is more appropriate when studying extreme event cases such as firm exit which occurs for a rare segment of the population (Hahn & Soyer, 2005). All regressions use Huber-White robust standard error clustered at within-country location and sector level. To account for the pooling data across countries, survey weights are re-scaled to sum to 1, so that each economy is equally considered in the estimations.

In our analysis, the typical concerns of potential endogeneity exist, and we cannot make any claims that the relationships investigated are causal. A possible source of endogeneity that may be impacting our results is reverse causality, i.e., the outcomes we observe may be predictors of firms’ productivity. The threat to causal identification is alleviated by using lagged explanatory variables: our estimates of firm exit rely on a cross-section of data with the dependent variable taken at the time t + n and the explanatory variables and all firm-level covariates taken from time t. Another important concern that may bias our coefficients is the omitted variable bias; there may be variables that we do not capture that are related to firms’ performance, and which affect firms’ exit. Our best response to this has been to include a rich set of firm-level controls, as we have done in all regressions. These are described in detail in the sections below.

Another concern in the analysis is the possibility that firm exit may have happened before the pandemic. To address this issue, the sample of analysis is restricted to the countries whose baseline ES surveys were completed in the year prior to the outbreak of the pandemic. While this does not fully address any events of firm exit in the period after the baseline interview and prior to the outbreak of COVID-19, the selection of the sample does minimize this time gap, therefore increasing the confidence that we are capturing exit during the COVID-19 crisis. Moreover, for many cases in the sample, the time between the outbreak of COVID-19 and the latest round of the COV-ES exceeds the time gap between the completion of the ES and the outbreak of the coronavirus, further mitigating this bias. Finally, for firms that ceased operations during COVID-19, we are unable to distinguish between exits that would have occurred even in absence of the pandemic because of the firm dynamic process (natural exit) and those that happened because of the pandemic (excess exit). As such the paper does not attempt to explain the differences in the determinant of exit pre and during the crisis, but for completeness it provides a comparison of the two situations.

4.1 Main explanatory variable

Our main explanatory variable is a measure of firm performance at the time t. We measure firm performance by firm labor productivity, defined as (log of) sales over the baseline year t (in 2009 USD) divided by the total number of permanent full-time employees.Footnote 7 This is in line with a well-established literature that uses the ES data (Aga & Francis, 2017; Amin & Okou, 2020; Clarke et al., 2015; Gui-Diby et al., 2017; Islam et al., 2020; Soppelsa et al., 2021; Varum & Rocha, 2012).

Given the relevance of physical capital among the determinants of firm efficiency, focusing on the measure of labor productivity alone would severely limit the analysis. For this reason, capital is controlled by capturing the firm’s investment in fixed assets such as machinery, vehicles, equipment, land, or buildings (new or used) in the year preceding the survey. This variable is used in the baseline regression as it has the advantage of being available for the full sample. We are aware of the limitations of using a variable that captures the purchase of capital and not the stock of capital in the firm. We try to mitigate these limitations by running robustness checks with other proxies for capital, despite the smaller sample for which these variables are available. These include a measure of the cost of capital, calculated as the (log of the) sum of the cost of fuel and electricity incurred by the firm, which serves as a proxy of how much capital is employed in the provision of services or the manufacturing of goods, as they reflect the utilization of fixed assets employed in the production process. This measure is available for all firms in the sample, subject to the willingness to respond. All amounts are deflated and converted from local currency units into 2009 USD.

Another limitation of using labor productivity is that it does not take into consideration operating costs or allow identifying firm’s profit. Ideally, TPF would have been considered. The use of TFP for this analysis, however, is problematic. First, TFP cannot be computed for the services sector, which is part of our sample; second, the data requirements to produce accurate TFP estimates are extensive. Financial data needed to compute TFP are only available for a subset of manufacturing firms, and thus using TFP comes at the cost of a significant decline in sample size.Footnote 8 An alternative way of taking operating costs into consideration is by computing value added, for which the reduction in sample size is more contained. In our sample, value added for manufacturing firms is computed as the difference between the value of sales and the total cost of raw materials and intermediate goods, divided by the number of permanent full-time employees. For retailers and selected other services firms, this is defined as the difference between the value of sales and the total cost of finished goods/materials to resell. Value added cannot be computed for some service providers such as hotels or restaurants. Given these limitations, which reduced the sample by 44%, this measure has been used as a robustness check.

4.2 Control variables

This section presents the controls used throughout this analysis, along with justifications from the literature as to the relevance and importance of their inclusion. Besides productivity, the age of the firms is also an important variable to consider when analyzing firm survival. Older firms may lay out more substantial investments than younger firms (Cull & Xu, 2005; Ericson & Pakes, 1995); they may also benefit from the process of learning by doing, productivity enhancements, and knowledge of customers and markets (Aga & Francis, 2017). By contrast, younger firms tend to have higher risks of exit compared to older ones as they may also have less established relations with customers and suppliers and less access to resources and networks than older firms. We measure the age of the firm as the (log of) years of operations.

Like age, the size of the firm exhibits similar patterns and arguments. The measure of firm size used is the log-transformed number of permanent and temporary full-time employees working in the establishment. Several reasons explain why smaller firms may show higher exit rates during crises. Smaller firms may be more severely affected by crises due to limited financial, technological, and human resources and greater dependence on customers, suppliers, and markets (Beck et al., 2005; Butler & Sullivan, 2005; Gertler & Gilchrist, 1994). Conversely, they may be more flexible in adjusting to downturns, being more able to exploit market niches and activities characterized by agglomeration economies, rather than scale economies, and being less reliant on formal credits compared with larger firms and thus less inert and less subjected to sunk costs (Liu et al., 1999; Tan & See, 2004). Varum and Rocha (2012) show that, during downturns, size reduces firms’ exit risk by less; the hazard rate increases more rapidly in size. Kim et al. (2015) studied the effect of the Korean crisis in 1997–1998 on small firms holding foreign currency-denominated debt and found that small firms with more short-term foreign debt were more likely to declare bankruptcy. Being part of a multi-establishment firm is also relevant for firm survival. The risk of exit is lower for establishments that belong to multi-unit firms as compared to single-unit establishments suggesting the presence of information and risk sharing mechanisms within a group (Shiferaw, 2009).

Our matrix of establishment-level controls also includes variables measuring outward orientation such as exporter status and foreign ownership. Exporting can be considered as a form of risk diversification through the spread of sales over different markets with potentially different business cycle conditions or in a different phase of the product cycle (Hirsch & Lev, 1971). Therefore, exports might provide a chance to substitute sales at home with sales abroad when a negative demand shock hits the home market and would force a firm to close otherwise (Wagner, 2013). This argument is still valid even in the case of shock that hit globally, such as the one induced by the COVID-19 pandemic, as countries were hit in different ways, with different magnitude, and at different points in time. Furthermore, Baldwin and Yan (2011) argue that non-exporters are in general less efficient than exporters (younger, smaller, and less productive); as a result, one expects that non-exporters are more likely to fail than exporters.

Foreign ownership has also appeared to have provided a higher degree of resilience to crisis, possibly due to intra-group lending mechanisms supporting affiliates facing external credit constraints (Kolasa et al., 2010). However, findings on the role of foreign ownership on firm survival are ambiguous. For example, Li and Guisinger (1991) and Gibson and Harris (1996) have found that foreign firms are less likely to exit, whereas Bernard and Sjöholm (2003), Görg and Strobl (2003), Pérez et al. (2004), and Baggs (2005) found opposite results.

Following a well-established strand of literature, we also control for management’s characteristics. Manager capabilities are found to be positively related to investment (McMillan & Woodruff, 2002) and innovation (Crowley & Bourke, 2018), and to be determinants of the selection of firms into international markets (Sala & Yalcin, 2015). More experienced managers may be more likely to better navigate the crisis, and thus manager’s experience is captured in the empirical specification. Besides the manager’s experience, the gender of the manager is also included among the controls in our regression analysis. Female-owned businesses are found to be more short-lived than male-owned businesses in a non-crisis situation (Kalnins & Williams, 2014). Similarly, a recent study found that women-led businesses are more likely to close, temporarily or permanently, due to the COVID-19 crisis (Liu et al., 2021b). During previous crises, women entrepreneurs were found to downsize their activities (Cesaroni et al., 2015). Finally, a study by Islam et al. (2020) found a productivity gap between firms that do and do not have a female top manager, which may possibly impact firm exit.

The business environment is known to impact firm productivity (Aterido et al., 2011; Commander & Svejnar, 2011), as well as firm entry (Klapper et al., 2004), and firm exit (Aga & Francis, 2017). We capture the business environment by including measures of infrastructure and regulations. Infrastructure is measured by whether the firm experienced electrical outages, and regulations are captured by a measure of whether senior management has spent any time dealing with regulations. Access to finance has also been found to be related to firm productivity (Gatti & Love, 2008; Rajan & Zingales, 1998). Through financing, firms are also likely to have the ability to mitigate the impacts of temporary shocks that would otherwise force them to exit; as such, access to finance may play a role in determining which firms survive and which firm exit the market (King & Levine, 1993; Levine, 2005). Firm’s access to external finance is captured by a measure of whether a firm has a loan or line of credit and by a measure of reliance on loans to finance working capital.

Moreover, we control for digital presence of the firm, as measured by the firm having its own website. Evidence shows that digital adoption is associated with productivity gains at the firm level (Cusolito et al., 2020; Kharlamov & Parry, 2021) and with firm resilience in a time of crisis (Wagner, 2021). The productivity gains linked to innovation and digitalization may be weaker in the presence of skill shortages, which may relate to the complementarities between digital technologies and other forms of capital, including human capital (Gal et al., 2019). Thus, we also control whether the establishment provides training to the workforce. We also control for firm’s innovation, as measured by having the firm introduced a product innovation in the three years before the baseline survey.Footnote 9The evidence from the existent literature indicates that the effect of innovation on firm survival and productivity is positive (Ugur & Vivarelli, 2020), with positive survival effects being reported for product innovation (Audretsch, 1991; Audretsch & Mahmood, 1995; Banbury & Mitchell, 1995; Fontana & Nesta, 2009), organizational innovation (Polder et al., 2009; Raffo et al., 2008; and Siedschlag et al., 2010), and patenting (Kato et al., 2021), and with persistence of process innovation for firms that survived crises is limited to process innovations (Antonioli & Montresor, 2021).

Finally, we include within-country location fixed effects and industry fixed effects. The use of within-country location fixed effects as control implies that all time invariant national and subnational characteristics that may impact firm exit, such as GDP growth and GDP level, trade openness, and business-related regulations are accounted for in the regressions. Similarly, differences in the intensity of the spread of COVID-19, as well as in the measures put in place by the governments to mitigate the impact of the pandemic, are also accounted for through the within-country location fixed effects.

As a measure of robustness, in place of the within-country location fixed effects, the analysis also employs a vector of country-level controls to account for the magnitude of variation in some of the country characteristics. To control for certain economic and social characteristics, the following variables are employed from the World Bank World Development Indicators: real GDP per capita, the share of the population at age of 65 or above, and the openness to trade measured as the sum of imports and exports as a percentage of GDP.Footnote 10 To control for the extent of the outbreak of COVID-19 and government policies taken to mitigate the outbreak, two measures are taken from Oxford University: the total number of COVID-19 positive cases per one billion inhabitants, and the stringency index which is a composite measure of closures and restrictions. Finally, to control for the quality of the institutions, the analysis includes a measure of government effectiveness using data extracted from the World Governance Indicators.

5 Estimation results

In this section, we present log-odds ratios obtained from logit estimations.Footnote 11 Unless stated otherwise, all relationships discussed in the next paragraphs are significant at the 5% level or less. The associated marginal effects are provided in Panel B in each regression table.

5.1 Baseline regression results

Our baseline regression results are provided in Table 3. The table presents a set of logit regressions starting with a parsimonious specification and adding the various controls sequentially.Footnote 12 For all specifications considered, the relationship between permanent exit of firms and labor productivity is negative and statistically significant, suggesting that a process of creative destruction may be at work. The estimated marginal effect of productivity ranges from − 0.014 to − 0.019. Thus, for 1% increase in labor productivity, the associated decrease in the probability of permanently exiting the market equals 1.4 to 1.9 percentage points. In our calculations, this implies that moving from the 10th percentile value of labor productivity (about $8,500 per worker in 2009 USD) to the 90th percentile (about $160,000 per worker) reduces the probability of exit between 3.3 and 4.5 percentage points.Footnote 13 This result points to a silver lining of the COVID-19 pandemic by which relatively more productive firms are less likely to permanently close and scar the markets. The consistent and negative association between productivity and likelihood of exiting the market is in line with a well-established literature that widely regards firms with higher productivity as facing a lower risk of exiting the market in a non-crisis situation (Aga & Francis, 2017; Baily et al., 1992; Fariñas & Ruano, 2005; Hopenhayn, 1992; Olley & Pakes, 1996). The results, however, are in contrast with the evidence on previous crises that found the relationship between productivity and firm exit to be attenuated or reversed (Baden-Fuller, 1989 in the UK; Foster et al., 2016 in the USA; Hallward-Driemeier & Rijkers, 2013 in Indonesia).

Several controls show a significant relationship with firm permanent exit and in the anticipated direction. First, we found a negative association between having a digital presence and the probability of exit. Results show that the estimated marginal effect of having a website is − 0.046 to − 0.051; thus, firms that had a digital presence before the crisis are 4.6 to 5.1 percentage points less likely to exit the market than firms that did not. Having a digital presence supports firm performance through several channels; it fosters efficient market intermediation through lower search, transaction, and transportation costs potentially increasing profitability and the volume of trade and making prices more competitive (Cusolito et al., 2022). We also find that innovative firms have a significantly higher likelihood to survive during the COVID-19 crisis, as expected and discussed in the prior section. The coefficients for the marginal effects indicate that firms that introduced an innovation in the 3 years prior to the crisis have 2.6 to 2.7 percentage points lower likelihood of permanently closing during the pandemic. Similar results were obtained in the context of the early 2010s financial crisis in Europe where an analysis also based on the ES data shows that pre-crisis innovation affected their survival odds and performance (Sidorkin & Srholec, 2014). Our results confirm that introducing new products and adapting the business models allows firms to adjust to market developments, allowing them to better cope in times of crisis (Archibugi et al., 2013; Dachs et al., 2017).

A cumbersome business environment is also correlated with firm permanent exit, though with a coefficient being significant at 10% level. Firms where senior management spent any time in dealing with regulations are between 2.2 and 2.4 percentage points more likely to exit the market than firms where senior management did not, confirming the critical role of regulations in explaining firm productivity and firm dynamic (Aga & Francis, 2017; Aterido et al., 2011; Commander & Svejnar, 2011; Klapper et al., 2004). In line with expectations, the estimated coefficients of the variable measuring the firm’s years of operations (or firm age) and of having purchased fixed assets the year before the crisis are also negative, and statistically significant, the latter only at 10% level. This is consistent with the literature for both developed and developing countries (Aga & Francis, 2017; Bernard & Sjöholm, 2003; Frazer, 2005). Finally, contrary to expectations, measures of access to finance do not yield results of statistical significance in relation to firm exit.Footnote 14

5.2 Robustness of estimates

A series of alternative specifications are estimated to confirm the results obtained in the baseline analysis. This first set of robustness checks aims at checking the proxy used to measure the main explanatory variable, labor productivity, by integrating, to the extent possible, measures of capital. The baseline analysis includes a measure of labor productivity and controls for any investments in fixed capital. Two alternative sets of model specifications are considered in order to corroborate the baseline estimates on the main explanatory variable—one substitutes the control for fixed capital with the cost of capital usage, while the other uses a measure of value added instead of labor productivity. Both are defined in Sect. 4.1.

The results which account for the cost of capital are presented in Table 4. Even when controlling for the expenses incurred on electrical usage and fuel, the marginal effects of labor productivity on the probability of exit remain negative, consistent, and robust with the marginal effects ranging from − 0.013 to − 0.017. Similarly, the Schumpeterian cleansing result is confirmed when using value added per worker instead of sales per worker as a measure of productivity. The results are presented in Table 5. The magnitude of the coefficient for the marginal effects in this specification is in line with the main specification, with a percent increase in value added being associated with a decrease in the probability of permanently exiting the market ranging from 1.3 to 1.7 percentage points.Footnote 15 In the next sections, we discuss several model extensions. In all the regressions presented now onwards, column 5 of Table 3 is used as the main specification for the remainder of the analysis.

5.3 Model extension: accounting for government policies on insolvency

Government interventions can affect the market process, and by extension, the Schumpeterian cleansing process as well. Early evidence from Germany has shown that the widespread measures implemented to avoid corporate bankruptcies altered the cleansing process by allowing businesses to survive that otherwise would not have (Dörr et al., 2021). Given that many governments enacted policies to support businesses during the COVID-19 pandemic which may have contributed to a less pronounced association between productivity and firm exit, the robustness of the estimates warrants an examination controlling for these types of interventions.

To assess the role of government intervention, in line with the examination by Dörr et al. (2021), the paper considers the baseline regression in a split sample which accounts for whether changes in the insolvency laws relevant to private business were implemented. During the COVID-19 crisis, several countries have amended their insolvency laws, often through the introduction of a moratorium on the filing of insolvency petitions. Such actions may have not only reduced the number of businesses exits but also potentially attenuated the association between productivity and firm survival. While it is not possible to measure the exit rate in absence of such measures, the robustness of the results can be accounted for.

Table 6 shows the logistic regression estimates of the model, broken down into two subsamples which account for the policies enacted.Column (1) reflects the model which excludes from the sample the countries that introduced bankruptcy moratorium policies or mitigating policies, while column (2) excludes the countries that did not make any legal changes pertaining to insolvencies. The breakdown of the countries in the subsets they belong are presented in Table 18 in the Appendix.

The results of the analysis confirm that the association labor productivity-exit persists in countries that did not release firms from their insolvency filing obligations. The estimates of the covariates are of similar magnitude, direction, and significance as those of the baseline model, showing robustness in the analysis. However, for the subsample of countries that have taken mitigating policies, the relationship between productivity and likelihood of exit is severed. Under those institutional environments, survival is instead primarily dependent on innovation, having a website, and reliance on exports.

5.4 Model extension: comparing firm exit pre- and during crisis

The primary focus of this analysis is to examine the relationship between productivity and firm exit during the COVID-19 pandemic, for which the empirical evidence is discussed in the earlier sections. A question that naturally arises when looking at the results of the analysis is whether the productivity-exit association uncovered during the COVID-19 crisis is similar or different compared to a regular, non-crisis, period; or, in other words, if the association uncovered would have been the same in absence of the COVID-19 pandemic crisis. While we cannot answer the latter, as we do not have a counterfactual to compare our results with, we try to address the former by tapping into ES data collected between 2013 and 2019.

This section presents the results of this analysis. The sample used is composed of a subset of 28 countries for which 2013 ES data are available, in addition to the 2019 ES and COVID-ES.Footnote 16 With the available data, a variable that measures firm exit between 2013 and 2019 is built following the same approach used for the 2019 ES-COV-ES exit, together with the variable of interest (labor productivity in 2013) and other covariates. Table 7 presents the results of the baseline model estimated for the 2013–2019 data (column 1) and for the 2019 ES-COVID-ES data (column 2). The results for 2019 COVID-ES data are in line with the results of the baseline model for the full sample (Table 3 column 5) with productivity, age, innovation, and digital presence being negatively correlated with firm exit and the coefficient for a cumbersome business environment showing a positive correlation. As far as the comparison of crisis with non-crisis, the results show that labor productivity, despite having the same direction of the coefficient, is not statistically significant in its association with firm exit in the non-crisis period. The coefficients of the proxies for digital presence, innovation, and business environment retain the sign and significance of the association. This seems to suggest that the beneficial roles of digitalization and innovation are not peculiar to the COVID-19 circumstances but more of a determinant of firm survival in place also in regular time. The same applies to the exacerbating role of a cumbersome business environment.

In order to compare the magnitude of the effect of these variables across the time periods, a set of pooled regressions was also run, in which the interaction between the regressors of interest and the dummy variable identifying the COVID-19 crisis is added to the right side of the equation. Table 8 presents the coefficients of these interactions.Footnote 17 Consistent with the results shown in Table 7, the effect of productivity on likelihood of exit estimated for the COVID-19 period is statistically different from the effect estimated using the 2013–2019 sample, suggesting that productivity is a relevant determinant of exit especially during a crisis period. Similar conclusions can be drawn for the longevity of the firm and for digitalization. The estimates suggest that the negative association between years of activity and likelihood of exiting the market is stronger during the COVID-19 period or, in other words, that younger firms, generally less resilient than older ones, are suffering even more during the crisis induced by the pandemic. Estimates also show that having a digital presence, as measured by firm having their own website, is also a more relevant determinant of firm survival during the COVID-19 crisis. On the other hand, the effects of burdensome regulations and product innovation are not statistically different between the different periods of this analysis.

While the results of this comparison are suggestive, caution is needed in their interpretation given some limitations in the data used. First, there is a remarkable difference in the period considered in the two samples, with the pre-crisis period of exit being analyzed in a time span of 6 years on average and the crisis in a shorter span of about 1 year. This has some implications: (1) more firms may exit the market in a 6-year period as compared to a year period as shown by the mean of the dependent variable in the two regressions. While the greater degree of exit may not directly affect the relationship between productivity and survivability, it is important to highlight the difference. (2) Attrition of firms is higher as some firms may have moved or changed their contact information. This is a potential source of identification bias as it is possible that some of the firms for which the contact information was out of date are assumed to have exited the market, while they may continue in existence. This identification problem is likely to introduce a downward bias on the coefficient of sales per worker. For the analysis during the crisis, this bias is less prevalent as the time gap between the surveys is much shorter. Lastly, (3) the measure of productivity is far too outdated to establish the relationship between productivity and exit. Over time, the characteristics of firms and their productivity change. Since the exact date of exit is not available, it is noisy to base the analysis only on the most recently observed level of productivity. This bias affects both firms that have survived and those that have exited. In addition, the composition of countries in the sample differs slightly, as data for higher income European countries is not available in the pre-crisis period. While Tables 7 and 8 provide the estimates for the same subset of countries for which data is available, this comparative analysis rests primarily on developing economies in Eastern Europe, Central Asia, and North Africa. It remains unknown whether the relationship between productivity and exit would remain insignificant should it include data from higher income economies that have relatively more developed and well-functioning markets.

5.5 Model extension: controls for country-level characteristics

Substituting the within-country location fixed effects with a vector of controls that capture the country’s economic and COVID-19 specific characteristics allows the analysis to shed light on how the magnitude of the individual country characteristics affect the likelihood of firm exit. The model specification to which this extension is applied controls for the same set of firm-level characteristics used in baseline regression (Table 3 column 5). Results are presented in Table 9.

In addition to ensuring robustness in the findings of the baseline model and the extensions of examining the impact of country characteristics on exit, this specification includes a measure of the duration between the baseline ES survey and the COV-ES follow-up. This measure attempts to control for any potential identification issues in which firms ceased operations prior to the outbreak of COVID-19. The time duration between the surveys is calculated by taking the difference between the time of the baseline ES survey and the COV-ES follow-up at the firm level, then averaged for all firms per country. The coefficients of this variable are presented in the even numbered columns, (2) and (4), of Table 9. While unsurprisingly its effect on exit is positive and hence indicating that the longer the period between the surveys, the higher the likelihood of exit, the coefficient on labor productivity remains stable in magnitude and direction with the baseline results, and robust regardless of the model specification. Moreover, this specification includes variables to control for the intensity of the COVID-19 health emergency in the different countries and the related policy responses, including school closures, workplace closures, and travel bans as provided by the Oxford stringency index. For this index, we used the values referring to the last day of the data collection fieldwork of the follow-up surveys in each of the countries, with the aim of gauging the severity of the pandemic at different time points and in different locations. Some weak evidence points to an adverse effect of the stringency index on the likelihood of survival of the firm, but further investigation is warranted to make any conclusions on whether this may be due to the severity of the infections or to the policies implemented to control it.

Controlling for country-specific characteristics in place of within-country location fixed effects yields results similar to those obtained in the baseline specification. The main variable of interest, labor productivity, remains robust with marginal effects ranging from − 0.021 to − 0.023. In addition, the majority of the other variables which were found significant in Sect. 5.1—age of the firm, the purchase of fixed assets, the time spent by managers in dealing with government regulations, having of a website by the firm—remain robust in direction, magnitude, and significance.

5.6 Model extension: small firms versus medium-sized and large firms

In this section, we explore how the relationship between firm permanent exit and productivity and between firm permanent exit and the other explanatory variables that show a significant relationship with firm exit varies depending on firm size. These heterogeneities are estimated by repeating the baseline estimations for the subsamples of small firms (firms with 5 to 49 employees) and medium and large firms (50 employees and more), respectively.Footnote 18 Results are shown in Table 10.Footnote 19

As highlighted in the literature, small firms may be more severely affected by crises; therefore, understanding if the negative relationship between productivity and firm exit is driven by this sub-sample of firms becomes particularly important when designing policy and targeting government interventions (Pedauga et al., 2021). The same considerations hold for the analysis of the role of the mitigating factors identified in the analysis, such as innovation, digital presence, and investment, and for exacerbating factors, such as the effect of the business environment. The prediction is that the role of mitigating and exacerbating factors may be stronger for smaller firms as they may have fewer channels to smooth the negative effects of the crisis and therefore, they may be more exposed to the risk of exiting the market.

Results in Table 10 confirm the predictions. That is, the negative relationship between having its own website, having introduced an innovation, age of the firm and firms exit is confirmed only for small firms. None of these variables is significant for the subsample of medium and large firms. The same holds for the relationship between a cumbersome business environment and firm exit, which is positive and significant only for small firms (i.e., a cumbersome business environment increases the likelihood of firm exit for small firms). On the contrary, spending time dealing with government regulation reduces the likelihood of exiting the market for medium and large firms, significant at 10% level, together with the purchasing of fixed assets. No differences based on firm size are found when looking at the role of labor productivity which is negatively correlated with firm exit for small firms as well as for medium and large firms.

5.7 Model extension: low productive versus high productive firms

The results presented in earlier sections show a strong association between labor productivity and the likelihood of firms permanently closing their operations. At the same time, other firm characteristics, such as digital presence, investment, innovation, and the regulatory burden appear to influence the survival likelihood. A question that arises, however, is whether the crisis had a disproportionate effect on highly productive firms in presence of other vulnerabilities and what factors help mitigating or exacerbating firm exit among those firms. To answer this question, the baseline estimation was repeated for the subsample of firms in the top and bottom half of the labor productivity distribution; interactions with firm size have been also explored.

The coefficients of the baseline regression (odds ratios and marginal effects) are presented in Table 11, while the results for interactions on firm size are illustrated in Table 12. The first column (1) of Table 11 presents the results for the bottom half of firms in terms of labor productivity, and column (2) shows the results for the top half. The results suggest that the crisis is affecting the private sector in line with the cleansing out process rather than scarring the economy by destroying productive firms. Indeed, the positive association between sales per worker and firm exit holds only for the bottom half of firms in terms of labor productivity, consistently with the distribution of productivity presented in Fig. 1. This means that while productivity differential matters for less productive firms, the survival among businesses with sales per worker in the top half of the distribution is determined by other factors. In this group, firms in which senior management spends more time dealing with government regulations have a higher likelihood to succumb to the perils of the pandemic, while businesses that are part of a multi-establishment firm and firms that introduced a product innovation before the pandemic are more likely to survive. Interestingly, among the more productive firms, firms with foreign ownership are also more likely to exit the market, in line with the results of a strand of empirical literature (Bernard & Sjöholm, 2003; Görg & Strobl, 2003; Pérez et al., 2004; and Baggs, 2005).

Labor productivity retains its strong and significant association with the likelihood of ceasing operations for firms that fall in the lower half of labor productivity distribution, with the mitigating factors being the purchase of fixed assets and the digital presence. Digital presence is negatively associated with firms also for more productive firms, with significance at the 10% level. Finally, regardless of where a business lies in the spectrum of labor productivity, an important factor that increases the likelihood of survival is the age of the firm. Interestingly, the mitigating effect of having a website is particularly relevant for small firms in the bottom half of the labor productivity distribution, while having introduced a product innovation is more relevant for small firms in the top half of the distribution. Once again, these findings confirm that being adaptable and having a digital presence are crucial characteristics to navigate the effects of the crisis induced by the COVID-19 pandemic.

6 Conclusions

Crises are periods of intensified adjustments. From a theoretical point of view, they may accelerate the Schumpeterian process of creative destruction, by pushing unproductive arrangements out of the market, or exacerbate market imperfections, displacing productive firms. While empirical analyses on the role of productivity on firms’ responses during previous crises have shown mixed evidence, in the case of the COVID-19 pandemic evidence on the impact of productivity on firm survival remained uncovered. The present paper attempts to fill this gap in the literature using firm-level data collected before and after the outbreak of the COVID-19 crisis for 34 countries. The paper also extends the analysis to the identification of elements that may increase firm adaptability and, therefore, promote firm survival.

The results show that there is a strong positive relationship between productivity and firm survival, consistent with the theoretical predictions of the Schumpeterian creative destruction. In addition, the paper confirms the positive role of firm age for firm survival and uncovers suggestive evidence of a positive role of (product) innovation, firm investment, and digital presence, in particular for small firms. The results point to a negative effect of a cumbersome business environment. Finally, in countries with government interventions in the insolvency procedures the Schumpeterian cleansing process was disrupted.

There are several policy implications that can be drawn from our findings. First, our results confirm the importance of supporting innovation and digitalization in the private sector. The ability to quickly adapt to rapidly changing market conditions, captured by the ability of firms to innovate, has been key in the past months. To the same extent, having a digital presence has increased its relevance as a way to offset the physical remoteness imposed by the social distance requirements put in place to reduce the transmission of the virus. Supporting firms in keeping the momentum and increasing their efforts in innovation and digitalization may help in promoting sustained productivity growth. Second, the paper claims specific attention to small firms that may benefit, proportionally more compared to large and more established firms, from improvements in innovation and from digitalization. Third, the results point to the benefit of agile regulations and good governance. The findings suggest that the burdensome regulations that tax the time of managers decrease the likelihood of survival. Putting these policies into practice can be a lengthy endeavor, but in the short-term particular emphasis should be placed on avoiding lasting damage to human capital and productivity (Loayza et al., 2020).

While this analysis points to evidence of exit among less productive firms, using data collected up to eighteen months after the declaration of the pandemic, further investigation is required to draw conclusions on the long-term impact of the COVID-19 crisis on the private sector. Some of the big questions that remain to be answered are (1) whether the initial evidence of a higher likelihood of exit by less productive firms remains in the later stages of the pandemic, (2) whether there are economic gains from the reallocation of the resources, both labor and capital, of the businesses that have ceased their operations, and (3) how different are the new entrants on the market and whether the implications of COVID-19 will permanently affect the organization of firms.

Change history

02 August 2023

A Correction to this paper has been published: https://doi.org/10.1007/s11187-023-00807-w

Notes

The paper uses the data collected and published up to September 2021.

More information on the ES methodology is available at https://www.enterprisesurveys.org/en/methodology.

The questionnaires used for the ES and COV-ES surveys are available on the Enterprise Surveys website https://www.enterprisesurveys.org/en/enterprisesurveys data are also publicly available for download. The website also presents indicators built from the establishment-level data.

In addition to this analysis, for which results are presented in the on-line appendix, we also compared the differences between survivors and exiters based on the assumed exit and survivors and exiters based on the confirmed exit. The differences between the two groups are the same in the two samples.

Additional details about the sample are presented in the Appendix.

The time between surveys is measured by the time that elapsed between the baseline and the follow-up survey measured in 6-month periods.

Note that outliers are removed through the following procedure: total annual sales and number of permanent full-time employees are first log-transformed, then trimmed at plus and minus three standard deviations from the mean.