Abstract

This study analyzes the effect of financial constraints (FCs) on firm dynamics. We measure FCs with an official credit rating, which captures availability and cost of external resources. We find that FCs undermine average firm growth, induce anti-correlation in growth patterns and reduce the dependence of growth volatility on size. FCs are also associated with higher volatility and asymmetries in growth shock distributions, preventing young fast-growing firms especially from seizing attractive growth opportunities and further deteriorating the growth prospects of already slow-growing firms, particularly if old. The sub-diffusive nature of the growth process of constrained firms is compatible with the distinctive properties of their size distribution.

Similar content being viewed by others

Notes

The generally accepted finding is that FCs hamper the growth prospects of firms and that this effect is stronger for younger and smaller firms (see Angelini and Generale 2008). These findings are in line with the recent theoretical literature on financing and growth models (see Cooley and Quadrini 2001; Albuquerque and Hopenhayn 2004; Clementi and Hopenhayn 2006), largely based on the models of industrial dynamics in Jovanovic (1982) and Hopenhayn (1992).

Cabral and Mata (2003) find that the evolution of the FSD is determined by firms ceasing to be financially constrained, while Fagiolo and Luzzi (2006) and Angelini and Generale (2008) conclude that FCs are not the main determinant of FSD evolution. At least part of the explanation for such seemingly contrasting evidence may come from the different proxies of FCs employed in these studies. Cabral and Mata (2003) measure FCs with age, assuming that younger firms are more constrained, while Fagiolo and Luzzi (2006) and Angelini and Generale (2008) adopt reported cash flow and survey-based measure of FCs, respectively.

These shares are computed with respect to National Accounts data by sector of activity, as reported by Eurostat. Pistaferri et al. (2010) report similar figures; they also report that the CeBi database contains approximately 7 % of all Italian manufacturing firms.

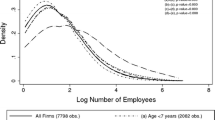

For 2003, the annual report of the Italian Statistical Office (ISTAT 2005) provides the following distribution: 82 % of firms have <10 employees; 15 % have 10–49 employees; 2 % have 50–249 employees, and 1 % have >250 employees. In our data there is a very mild overrepresentation of medium-sized to larger firms: 78 % of firms have <10 employees; 13 % fall in the 10–249 employee size class; 8 % have 50–249 employees and 1 % have >250 employees.

Explored alternatives encompass relative ranking in the cross-sectional distribution of variables supposed to strongly correlate with the availability of external finance, such as age (Cabral and Mata 2003), cash flow (Fazzari et al. 1988; Kaplan and Zingales 1997, 2000) cash flow sensitivity of cash (Almeida et al. 2004) or multivariate index based on sets of financial ratios (Cleary 1999; Lamont et al. 2001; Whited and Wu 2006; Musso and Schiavo 2008), or measures based on surveys, where managers or entrepreneurs are asked to make a self-assessment of the difficulties they face in accessing financing from banks or other institutions (Winker 1999; Angelini and Generale 2008; Campello et al. 2010).

In order to check the sensitivity of our results to the adopted classification, we also considered three alternative assignments. First, we divided firms according to their ratings in t − 2. In the second procedure, firms were assigned to FC classes on the basis of the worst rating displayed over the sample period. Finally, we restricted the analysis to firms that did never change their financial status over the whole time window (i.e., based on their ratings in the different years, they always fell in the same FC class). However, our main conclusions were not affected by the choice of the assignment procedure. All of the results are available upon request.

Nominal sales are deflated via 3-digit sectoral production price indexes made available by the Italian Statistical office, base year 2000. A basic cleaning procedure to remove a few outlying observations is applied (see Appendix 1.1 for details). Reported results refer to pooled data over 2001–2003, as 1 year is lost due to the use of 1-year lagged FC status.

The very high mean value of 35,067 firms found within HFC old firms is explained by the presence of a quite large firm (actually the largest in the dataset) which is old and HFC over the sample period. The mean size falls to 20,665 employees if we exclude this single firm from the sample.

Since we cannot follow cohorts of firms in our data, a comparison across firms of different age is the only way to approach studying the relationship between size, age and FCs.

Here as well as throughout the work, estimates of densities are obtained using the Epanenchnikov kernel with the bandwidth set using the optimal rule described in Silverman (1986, p. 48).

Notice that the extended generalized gamma distribution applied in Cabral and Mata (2003), which possesses only one shape parameter, would not have allowed to independently account for the different behaviors observed in the two tails.

Due to the short time window of our database we cannot directly test the persistence in firm financial conditions over a long span of time. The analysis of transition matrix between FC classes reveals a significant persistence. The average 1-year probability to remain in the same class is 81.03 % for NFC firms, 75.51 % for MFC firms and 57.88 % for HFC firms.

The AR(1) specification can be replaced with a more general linear model. For the present discussion the 1-lag structure is sufficient. We checked that the inclusion of further lags does not generate significant modifications in the estimates of λ.

At the same time, separate estimation by FC class allows us to drop the condition of orthogonality with the residuals that is needed if we pool the data on the entire sample and include the FC proxy among the regressors. Since our analysis below reveals significant differences in the distribution of residuals across the FC classes, pooled estimates of Eq. (3) with FC dummies would likely produce biased results.

See Appendix 1.2 for a formal derivation of these results.

An explanation of the emergence of this stylized fact, based on the idea of dynamic increasing returns, is presented in Bottazzi and Secchi (2006).

Plots obtained with 35 bins. The procedure is robust to variation in the number of bins.

Results available upon request.

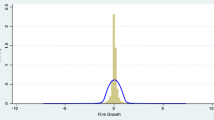

This corresponds to assume that the error term follows an AEP distribution with b l = b r = 1, and with a l and a r estimated from data.

Assuming some degree of persistence in financial conditions, this result is sufficient to explain the lack of Gaussianization in the right tail of the FSD observed in the group of old HFC firms (cf. Fig. 2 above).

The estimates for MFC firms are not presented here to keep the figures more readable. The results (available upon request) substantially replicate the findings obtained for NFC firms and thus do not affect the main conclusions.

We nonetheless explored maximum likelihood estimates of Eq. (5) with firm fixed effects and Gaussian residuals, pooling across FC classes and adding two dummy indicators for firms belonging to MFC and HFC class. The HFC dummy coefficient turned out negative and significant, suggesting that the explanatory power of ratings is not washed away by the inclusion of time invariant heterogeneity.

The use of GOM implies, by definition, that we do not consider the cash flow generated by no- operating earnings and losses. These should not be very relevant, however, since we are working with manufacturing firms. Moreover, due to the limited data availability, we cannot consider the cash flows absorbed by taxes. Assuming, as a first approximation, a constant tax rate, this would amount to a constant and consequently irrelevant shift in the value of our regressor.

As done for sales, both GOM and ASSETS are deflated with appropriate sectoral price indexes, at the 3-digit level of industry disaggregation.

We also estimated two alternative specifications, both aiming at the inclusion of negative GOM in the regression. First, using the ratio GOM/ASSETS yields a non-significant coefficient for this further variable and only results in a moderate and homogenous reduction of the heteroskedastic parameter across classes. Second, we introduced a dummy with a value of 1 when GOM is positive, and 0 otherwise: this turned significant in all classes, but without affecting the other coefficients. Further, we also experimented with a GMM-SYS estimator, but standard Sargan/Hansen tests confirm that the time span of the database is too short to identify a valid set of instruments among past levels and past differences of the covariates. All results are available upon request.

We also explored a further specification considering two-period lags of size, ASSETS and GOM. This allows for a check of varying effects over time and provides a further control for possible endogeneity of covariates at t − 1. The estimates of λ retain their signs and magnitudes, again displaying negligible values for NFC firms, and then become increasingly negative as FCs become stronger. Second lag coefficients of GOM and ASSETS absorb part of the first lag effects of these variables. The most noticeable difference compared to the estimates presented in Table 2 is a significant reduction in the age coefficient, whose magnitude becomes comparable with that of the other regressors and across FC classes. Also notice that estimates of the extended model in Eq. (6) by employment classes confirm the minor role of censoring in driving the findings: patterns in λ reproduce the estimates reported in Table 3 above. All the results are available upon request.

References

Albuquerque, R., & Hopenhayn, H. A. (2004). Optimal lending contracts and firm dynamics. Review of Economic Studies, 71, 285–315.

Almeida, H., Campello, M., & Weisbach, M. S. (2004). The cash flow sensitivity of cash. Journal of Finance, 59, 1777–1804.

Amaral, L., Buldyrev, S., Havlin, S., Maass, P., Salinger, M., Stanley, H., & Stanley, M. (1997). Scaling behavior in economics: The problem of quantifying company growth. Physica A, 244, 1–24.

Angelini, P., & Generale, A. (2008). On the evolution of firm size distributions. American Economic Review, 98, 426–438.

Bond, S., Elston, J., Mairesse, J., & Mulkay, B. (2003). Financial factors and the investment in Belgium, France, Germany, and the United Kingdom: A comparison using company panel data. The Review of Economics and Statistics, 85, 153–165.

Bottazzi, G., & Secchi, A. (2005). Growth and diversification patterns of the worldwide pharmaceutical industry. Review of Industrial Organization, 26, 195–216.

Bottazzi, G., & Secchi, A. (2006). Explaining the distribution of firms growth rates. The RAND Journal of Economics, 37, 235–256.

Bottazzi, G., & Secchi, A. (2011). A new class of asymmetric exponential power densities with applications to economics and finance. Industrial and Corporate Change, 20, 991–1030.

Bottazzi, G., Secchi, A., & Tamagni, F. (2008). Productivity, profitability and financial performance. Industrial and Corporate Change, 17, 711–751.

Brown, J. R., Fazzari, S. M., & Petersen, B. C. (2009). Financing innovation and growth: Cash flow, external equity, and the 1990s R&D boom. Journal of Finance, 64, 151–185.

Cabral, L. M. B., & Mata, J. (2003). On the evolution of the firm size distribution: Facts and theory. American Economic Review, 93, 1075–1090.

Campello, M., Graham, J., & Harvey, C. R. (2010). The real effects of financial constraints: Evidence from a financial crisis. Journal of Financial Economics, 97, 470–487.

Cleary, S. (1999). The relationship between firm investment and financial status. Journal of Finance 54, 673–692.

Clementi, G. L., & Hopenhayn, H. A. (2006). A theory of financing constraints and firm dynamics. The Quarterly Journal of Economics, 121, 229–265.

Cooley, T. F., & Quadrini, V. (2001). Financial markets and firm dynamics. American Economic Review, 91, 1286–1310.

Crouhy, M., Galai, D., & Mark, R. (2001). Prototype risk rating system. Journal of Banking & Finance, 25, 47–95.

Devereux, M., & Schiantarelli, F. (1990). Investment, financial factors, and cash flow: Evidence from U.K. panel data, in Asymmetric information, corporate finance, and investment. Cambridge, MA: National Bureau of Economic Research, pp. 279–306.

Fagiolo, G., & Luzzi, A. (2006). Do liquidity constraints matter in explaining firm size and growth? Some evidence from the Italian manufacturing industry. Industrial and Corporate Change, 15, 173–202.

Fazzari, S. M., & Petersen, B. C. (1993). Working capital and fixed investment: new evidence on financing constraints. RAND Journal of Economics, 24, 328–342.

Fazzari, S. M., Hubbard, R. G., & Petersen, B. C. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 1988, 141–206.

Fligner, M. A., & Policello, G. E. (1981). Robust rank procedures for the Behrens-Fisher problem. Journal of the American Statistical Association, 76, 141–206.

Gibrat, R. (1931). Les inègalitès èconomiques. Paris: Librairie du Recuil Sirey.

Hall, B. H. (1987). The relationship between firm size and firm growth in the us manufacturing sector. Journal of Industrial Economics, 35, 583–606.

Hall, B. H. (2002). The financing of research and development. Oxford Review of Economic Policy, 18, 35–52.

Hopenhayn, H. A. (1992). Entry, exit and firm dynamics in long run equilibrium. Econometrica, 60, 1127–1150.

Hymer, S., & Pashigian, P. (1962). Firm size and rate of growth. Journal of Political Economy, 70, 556–569.

Istituto Nazionale di Statistica (ISTAT) (2005). Rapporto Annuale 2004. Rome: Istituto Nazionale di Statistica.

Jovanovic, B. (1982). Selection and the evolution of industry. Econometrica, 50, 649–670.

Kaplan, S. N., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112, 169–215.

Kaplan, S. N., & Zingales, L. (2000). Investment-cash flow sensitivities are not valid measures of financing constraints. The Quarterly Journal of Economics, 115, 707–712.

Kashyap, A., Lamont, O., & Stein, J. (1994). Credit conditions and the cyclical behavior of inventories. The Quarterly Journal of Economics, 109, 565–592.

Kumar, M. S. (1985). Growth, acquisition activity and firm size: Evidence from the United Kingdom. Journal of Industrial Economics, 33, 327–338.

Lamont, O., Polk, C., & Saá-Requejo, J. (2001). Financial constraints and stock returns. The Review of Financial Studies, 14, 529–554.

Lotti, F., Santarelli, E., & Vivarelli, M. (2003). Does Gibrat’s law hold among young, small firms? Journal of Evolutionary Economics, 13, 213–235.

Mansfield, E. (1962). Entry, Gibrat’s law, innovation, and the growth of firms. The American Economic Review, 52, 1023–1051.

Michelacci, C., & Quadrini, V. (2009). Financial markets and wages. Review of Economic Studies, 76, 795–827.

Musso, P., & Schiavo, S. (2008). The impact of financial constraints on firm survival and growth. Journal of Evolutionary Economics, 18, 135–149.

Oliveira, B., & Fortunato, A. (2006). Firm growth and liquidity constraints: A dynamic analysis. Small Business Economics, 27, 139–156.

Panetta, F., Schivardi, F., & Shum, M. (2009). Do mergers improve information? Evidence from the loan market. Journal of Money, Credit and Banking, 41, 673–709.

Pavitt, K. (1984). Sectoral pattern of technical change: Towards a taxonomy and a theory. Research Policy, 13, 343–373.

Pistaferri, L., Guiso, L., & Schivardi, F. (2010). Credit within the firm. NBER Working Papers 15924. Cambridge, MA: National Bureau of Economic Research.

Rajan, R. G., & Zingales, L. (1998). Financial dependence and growth. American Economic Review, 88, 559–586.

Silverman, B. W. (1986). Density estimation for statistics and data analysis. London: Chapman & Hall/CRC.

Stanley, M., Amaral, L., Buldyrev, S., Havlin, S., Leschhorn, H., Maass, P., Salinger, M., & Stanley, H. (1996). Scaling behaviour in the growth of companies. Nature, 379, 804–806.

Whited, T. M. (1992). Debt, liquidity constraints, and corporate investment: Evidence from panel data. Journal of Finance, 47, 1425–1460.

Whited, T. M. (2006). External finance constraints and the intertemporal pattern of intermittent investment. Journal of Financial Economics, 81, 467–502.

Whited, T. M., & Wu, G. (2006). Financial constraints risk. The Review of Financial Studies, 19, 531–559.

Winker, P. (1999) Causes and effects of financing constraints at the firm level. Small Business Economics, 12, 169–181.

Acknowledgments

The research leading to this work has received funding from the European Community’s Seventh Framework Programme (FP7/2007–2013) under Socio-economic Sciences and Humanities, grant agreement no. 217466. We also acknowledge financial support from the Institute for New Economic Thinking, INET inaugural grant no. 220 and the Italian Ministry of University and Research as a part of the PRIN 2009 program (grant protocol no. 2009H8WPX5). The authors wish to thank Alex Coad, Andrea Generale, Alessandra Guariglia, Luigi Guiso, Werner Holzl, Alan Hughes, Mariana Mazzucato, Franco Peracchi, Fabiano Schivardi, Sidney Winter and an anonymous referee for insightful comments to earlier drafts. We are also grateful to participants at the 2010 meeting of the European Association for Research in Industrial Economics (Istanbul, Turkey), those at the 2010 meeting of the European Economic Association (Glasgow, UK), those at the 2010 meeting of the International Schumpeter Society (Along, Denmark), and those at the DIME Workshop “Financial Constraints, Firm and Aggregate Dynamics” (Sophia-Antipolis, France). Useful discussions with participants to seminars at Scuola Superiore Sant’Anna, Pisa, Italy, at the University of Paris 1, Pantheon-Sorbonne, France, at the Einaudi Institute for Economics and Finance, Rome, Italy, at the European Central Bank, Frankfurt, Germany, and at the WIFO-Austrian Institute of Economic Research, Vienna, Austria, are also acknowledged. The usual disclaimers apply.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

1.1 Cleaning

We removed a few anomalous data from our sample. Cleaning was performed using Total Sales as a reference variable. For each firm, a missing value was inserted, in the place of the original value of Total Sales, when the latter lay outside the interval

where the median is computed over the years for which data are available for firm i. Table 5 shows yearly descriptive statistics computed before and after the cleaning. It is apparent that the procedure does not introduce any relevant change to the data.

1.2 Asymptotic behavior of the autoregressive process

Consider the model of firm size evolution described in Eq. (3), where the shocks \(\epsilon\) are independent and identically distributed according to a probability density f with mean c. Let us neglect, for the sake of simplicity, the firm and FC-class specific subscripts and the heteroskedasticity correction (i.e. set σ(s t−1) = 1). Let also s 0 be the initial size of the firm. By recursive application of Eq. (3), the size after T time steps, s T , can be written as the weighted sum of T independent random variables

Consider the cumulant generating function of the size at time T, \(\tilde{g}_{s_T}\), defined as the logarithm of the Fourier transform of the unconditional distribution

Due to the i.i.d. nature of the shocks it is immediate to see that

where \(\tilde{g}_{s_0}\) and \(\tilde{f}\) are the cumulant generating functions of the initial size distribution and of the shocks distribution, respectively. As a consequence, if the initial size distribution and the shocks distribution possess the cumulant of order n, then the size distribution at time T also possesses it and it reads

Let \(M_{{\rm s}_{t}}\) and \(V_{{\rm s}_{t}}\) be the mean and variance of the size distribution at time t, respectively. Under the hypothesis of a constant λ the evolution of \(M_{{\rm s}_{t}}\) and \(V_{{\rm s}_{t}}\) from t = 0 to t = T is given by

where \(M_{\epsilon}\) and \(V_{\epsilon}\) are the mean and variance of the shocks \(\epsilon\). Therefore, for λ = 0, the variance and mean increase proportionally to T and, for the Central Limit Theorem, the FSD converges in distribution to a lognormal. Conversely, when λ < 0 the FSD converges to a stationary distribution with finite variance \(V_{\epsilon}/(1-(1+\lambda)^2).\)

Rights and permissions

About this article

Cite this article

Bottazzi, G., Secchi, A. & Tamagni, F. Financial constraints and firm dynamics. Small Bus Econ 42, 99–116 (2014). https://doi.org/10.1007/s11187-012-9465-5

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-012-9465-5

Keywords

- Financial constraints

- Firm size distribution

- Firm growth

- Credit ratings

- Asymmetric exponential power distribution