Abstract

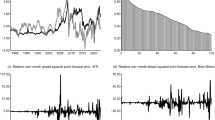

This paper investigates the (break) stationarity null hypothesis using data for 25 interest rates with different maturities and risk characteristics in Canada and the US. In contrast to a large part of the literature, this paper reports strong empirical evidence in favour of the null hypothesis of stationarity for the interest rate series.

Similar content being viewed by others

Notes

Newbold et al. (2001) being one of the few exceptions.

Refer to Cerrato et al. (2010) for a complete description of these transition functions and tests.

That is policy rue has not changed much since the post WWII experience [see Bernanke (1998) amongst the others]. Furthermore, the Canadian policy of shift towards zero inflation in February 1988 may have also caused structural breaks.

Although the evidence of stationarity is stronger using the sample period 1985–2012, we have also applied the same tests using the sample period 1985–2004 and obtained qualitatively the similar results.

We have selected the Sollis test since it is the test which shows more evidence of stationarity.

Note that, in this case, the transition function is exponential and not logistic.

References

Bernanke BS, Mihov I (1998) Measuring monetary policy. Q J Econ 113:869–902

Campbell JY, Clarida RH (1987) The term structure of euromarket interest rates. J Monet Econ 19:25–44

Cerrato M, Kim H, MacDonald R (2010) Equilibrium exchange rate determination and multiple structural changes, Discussion Papers, Dept. of Economics, University of Glasgow, 2010–2014

Galvani V, Landon S (2012) Riding the yield curve: a spanning analysis. Rev Quant Finan Acc. doi:10.1007/s11156-011-0267-7

Leybourne SJ, Newbold P, Vougas D (1998) Unit roots and smooth transitions. J Time Ser Anal 19:83–97

Moon HR, Perron B (2007) An empirical analysis of nonstationarity in a panel of interest rates with factors. J Appl Econom 22:383–400

Newbold P, Leybourne S, Sollis R, Wohar ME (2001) US and UK interest rates 1890–1934 new evidence on structural breaks. J Money Credit Bank 33:235–250

Sollis R (2005) Evidence on purchasing power parity from univariate models: the case of smooth transition trend-stationarity. J Appl Econom 20:79–98

Wu Y, Zhang H (1997) Do interest rates follow unit root process? Evidence from cross-maturity treasury bill yields. Rev Quant Finance Account 8:69–81

Acknowledgments

We would like to thank Karim Abadir for his helpful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cerrato, M., Kim, H. & MacDonald, R. Nominal interest rates and stationarity. Rev Quant Finan Acc 40, 741–745 (2013). https://doi.org/10.1007/s11156-012-0296-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-012-0296-x