Abstract

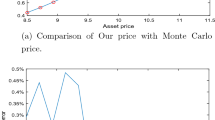

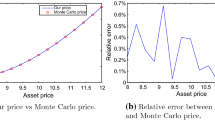

Ritchken and Trevor (1999) proposed a lattice approach for pricing American options under discrete time-varying volatility GARCH frameworks. Even though the lattice approach worked well for the pricing of the GARCH options, it was inappropriate when the option price was computed on the lattice using standard backward recursive procedures, even if the concepts of Cakici and Topyan (2000) were incorporated. This paper shows how to correct the deficiency and that with our adjustment, the lattice method performs properly for option pricing under the GARCH process.

Similar content being viewed by others

References

Brockhaus O., M. Farkas, A. Ferraris, D. Long and M. Overhaus, Equity Derivatives and Market Risk Models (Risk Publications, 2000).

Cakici, N. and K. Topyan, “The GARCH Option Pricing Model: A Lattice Approach.” Journal of Computational Finance, Summer 71–85 (2000).

Duan, J. C., “The GARCH Option Pricing Model.” Mathematical Finance 5, 13–32 (1995).

Duan, J. C., E., Dudley, G.. Gauthier and J. G., Simonato, “Pricing Discretely Monitored Barrier Option by a Markov Chain.” Journal of Derivative 10(4), 9–31 (2003).

Duan, J. C, and Simonato, “American Option Pricing under GARCH by a Markov Chain Approximation.” Journal of Economic Dynamic and Control 25, 1689–1718 (2001).

Kallsen, J. and M. Taqqu, “Option Pricing in ARCH-Type Models.” Mathematical Finance 8, 13–26 (1998).

Ritchken, P. and R. Trevor, “Pricing Options Under Generalized GARCH and Stochastic Volatility Process.” Journal of Finance 54, 337–402 (1999).

Author information

Authors and Affiliations

Corresponding author

Additional information

JEL Classification: C10, C32, C51, F37, G12

Rights and permissions

About this article

Cite this article

Wu, CC. The GARCH Option Pricing Model: A Modification of Lattice Approach. Rev Quant Finan Acc 26, 55–66 (2006). https://doi.org/10.1007/s11156-006-7033-2

Issue Date:

DOI: https://doi.org/10.1007/s11156-006-7033-2