Abstract

Job insecurity is one of the risks that workers face on the labour market. As with any risk, individuals can choose to insure against it, and we here consider marriage as one potential source of this insurance. The 1999 rise in the French Delalande tax, paid by larger private firms when they laid off workers aged 50 or over, led to an exogenous rise in job insecurity for the uncovered (younger workers) in these larger firms. A difference-in-differences analysis using French panel data reveals that this greater job insecurity for the under-50s led to a significant rise in their probability of marriage, and especially when the partner had greater job security, consistent with marriage providing insurance against labour-market risk.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Why do people get married? Weiss (1997) suggests that marriage comes with a number of economic advantages. The first reflects the benefits of specialisation between spouses (Becker, 1973, 1981). Second, in a context of imperfect credit markets, marriage may also relax credit constraints via implicit credit arrangements within households (Borenstein & Courant, 1989) and enhance investment (for example, one partner may work while the other is in education investing in their human capital). Collective and non-rival goods are also jointly produced and consumed within partnerships, with common examples being children or housework (Chiappori 1992, Van Klaveren et al., 2008). Stevenson and Wolfers (2007), in their empirical review of the changing trends in marriage and divorce in the US, highlight the roles of pre-marital cohabitation (which has risen), specialisation in marriage (now argued to be less important), the tax implications of partnership, birth control, changes in relative wages, Divorce Laws, and the marriage “matching function” (via education, the workplace and the internet).

The benefit from marriage that we will address here, which appears in both Weiss (1997) and Stevenson and Wolfers (2007), is that of risk-sharing. As noted by Hess (2004) and Shore (2010), partnerships provide insurance by allowing couples to diversify risk, as long as the exogenous income shocks of the two partners are not perfectly (positively) correlated. Couples can in addition adjust their relative labour supply to reduce the impact of shocks.

We here consider labour-market risk, and focus on the role of job loss in shaping marriage formation. We appeal to an exogenous variation in job insecurity at the individual level resulting from a French quasi-natural experiment: the 1999 increase in the Delalande tax. Introduced in 1987, this tax had to be paid by firms that laid off older workers. From January 1999 up to its abolition in 2008 the Delalande tax rose, but only for firms with 50 or more employees. Using difference-in-differences regressions exploiting this firm-size discontinuity and the perverse effects of the reform on the separation rate of younger workers, we estimate the causal impact of job insecurity on the probability of marriage.

As in Clark and Lepinteur (2022), our empirical analysis is based on the French component of the European Household Community Panel (ECHP). We first show that the 1999 increase in the Delalande tax in large firms produced greater feelings of job insecurity for the under-50s. We then consider the changes in marital status of these newly-insecure workers, as compared to a control group of under-50s in smaller firms (for whom the reform did not apply). We are interested in the way in which this exogenous greater risk affects behaviour. Clark and Lepinteur (2022) suggest that one reaction to an exogenous change in job insecurity is to reduce risk exposure, via lower fertility; we instead here ask whether individuals will take out more insurance against risk, via their marital status.Footnote 1 We will restrict our analysis here to younger workers, as most respondents aged 50 or more in our sample were already married before the reform, with only little post-reform movement out of marriage.

We conclude that greater job insecurity amongst French workers increased women’s probability of marriage by four percentage points; there is no effect for men. This is consistent with evidence on gender differences in preferences (Croson & Gneezy, 2009): women are generally less willing to take risks in the context of lotteries (Hartog et al., 2002, Holt & Laury, 2002, and Fehr-Duda et al., 2006) and portfolio selection (Sunden and Surette 1998, Finucane et al., 2000, and Charness & Gneezy, 2012). Falk et al. (2018) measure risk aversion via both a self-report (“In general, how willing are you to take risks?”) and revealed preference from a series of binary choices between a lottery and a sure return. Women were found to be more risk-averse than men in almost all of the 76 countries for which they collected data (see their Figure III). As such, women may react more to the threat of future job loss than do men. The finding of no change in the marriage probability of men with greater job insecurity does necessarily imply that they would not like to obtain insurance through marriage. However, being more at risk of layoff might have made them “riskier” partners.

We check that our estimates are robust to a number of possible confounding events, including European macroeconomic trends and the reduction in the French working week to 35 h that was announced in 1998 and implemented two years later in 2000; they are also qualitatively similar using a number of different estimation methods. While we do identify an insecurity effect on marriage, there is no change in the probability of entering a partnership in general, or indeed of leaving one: the greater probability of marriage for women then mostly reflects a shift into marriage from pre-reform cohabitation. The effect of job insecurity on women’s marriage probability is similar by age, education, and wages, but larger for women who were already mothers before the reform. Last, as predicted by risk-sharing, the probability of marriage only rises when the partner is employed and did not experience greater job insecurity due to the layoff-tax rise.

The remainder of the paper is structured as follows. Some existing work on marriage and insurance is discussed in Section 2, and the institutional background and our empirical approach to the analysis of individual-level insecurity appear in Section 3. Section 4 then presents the ECHP data and the estimation sample. Section 5 displays the main results, while the robustness tests and heterogeneity analyses appear in Section 6. The importance of partner characteristics in the light of risk-sharing theory is then discussed in Section 7. Last, Section 8 concludes.

2 Marriage as insurance: background and contribution to the literature

A number of contributions have provided indirect evidence of an insurance role of marriage. In Rosenzweig and Stark (1989), arranged marriages between families from different villages in South India significantly reduced the variability in food consumption. In addition, farm households subject to greater income risks were more likely to engage in arranged marriages at longer distances. In US data, Halla and Scharler (2012) find that the influence of idiosyncratic output-growth shocks on consumption is smaller in states where the percentage of married is higher. Bertocchi et al. (2011) consider household investment decisions, and conclude from their analysis of 14 years of Italian SHIW data that the married invest more in risky assets (as marriage is considered to be a safe asset). Anderson and Ray (2019) show that marriage protects against the risk of death, especially for women. In a similar vein, Van den Berg and Gupta (2015) use individual data from Dutch registers (from 1815 to 2000) and find a protective effect of marriage against mortality for men.

With respect to the labour market, there is a considerable literature on marriage and the business cycle. Schaller (2013) analyses 32 years of US State-level panel data: marriage is shown to be pro-cyclical, with unemployment being associated with less marriage. Lichter et al. (2006) appeal to individual-level NLSY-79 data, and conclude that the probability of transition from cohabitation to marriage rises with partner’s education and the partner working; it is lower for the unemployed. Education and employment are found to have a similar influence on marriage probability in Chinese data (Yu & Xie, 2015). Early labour-market experiences also seem to matter. Ekert-Jaffé and Solaz (2001, 2002) and Landaud (2021) analyse different French datasets to show that early-career unemployment and temporary jobs reduce the probability of forming a couple; De La Rica and Iza (2005) come to similar conclusions using Spanish data. One interpretation is that unemployment provides a negative signal about the potential partner’s unobserved characteristics. Consistent with this interpretation, in Charles and Stephens (2004), job loss increases the risk of divorce when resulting from layoff but not as a result of plant closings: they note that the former may convey information about the partner’s non-economic suitability as a mate (via, for example, their temperament). Similar results are also found in other disciplines such as Sociology and Demography (Oppenheimer, 1988, Kalmijn, 2011, de Lange et al., 2014, and van Wijk et al., 2021).

Some work has explicitly looked not at events that have already occurred, but rather measures of the future risk that individuals face on the labour market. Schneider et al. (2018) discuss the role of economic resources in marriage, which they extend to include wealth and expected future earnings. Schneider and Reich (2018) continue in the same line, and find that union membership (as an indicator of economic security) is a predictor of marriage in NLSY-79 data. Xie et al. (2003) also adopt an individual-level and forward-looking approach to economic insecurity, and calculate five different measures of current and future “earnings potential”: they show that all five are positively correlated with the transition from cohabitation to marriage using US Census and cohort data.

Although the role of forward-looking job insecurity in partnership formation has already been mentioned in the literature (Schneider et al., 2018, Bolano & Vignoli, 2021), we are not aware of any work that has been able to appeal to exogenous variation in job insecurity at the individual level in this context. Using difference-in-differences regressions based on a quasi-natural experiment, we here propose to estimate the causal impact of job insecurity on the probability of marriage. As opposed to past individual unemployment or current macroeconomic shocks, we are able to identify a plausible exogenous change in job insecurity following a French labour-market reform that put some workers more at risk than others of future job loss. Our findings confirm the predictions of risk-sharing theory: greater job insecurity leads to an increase in the probability of marriage for those who are arguably more risk-averse (women with children). In other words, marriage can be used as insurance in moments of economic insecurity.

3 Institutional background and empirical approach

3.1 The advantages of marriage in France

Marriage in France brings a number of financial advantages, some of which are particularly attractive for workers facing economic insecurity. First, French legislation considers cohabiting couples as two separate tax units whereas married couples count as a single tax unit. As shown in Leturcq (2012), the formula used by the French government to calculate annual income tax in the early 2000s produced a considerably-lower income tax rate for the married as compared to the cohabiting. These gains from marriage are particularly high when the income gap between the spouses is large. According to Échevin (2003), around 50% of married couples in 1999 benefited from a lower yearly income tax bill of at least 1000 Euros. Buffeteau and Echevin (2004) provide additional simulations of the financial gains from marriage in France in the early 2000s.

There are in addition a number of marital-property regimes in France. Since 1965, the standard regime is the “regime de communauté de biens réduite aux acquêts” (Frémeaux & Leturcq, 2013), in which any property owned by one of the spouses before marriage continued to be treated as belonging only to that spouse in the case of divorce. On the contrary, all property, assets and income acquired during the marriage were treated as common property and were thus subject to division in the case of divorce. Although the share of married couples opting for alternative regimes with greater individual control over the resources accumulated during marriage increased from 1975 to 2010, over 82% of newly-wedded couples were still under the “regime de communauté de biens réduite aux acquêts” that provides the greatest level of insurance between partners during our period of interest, that is the end of the 1990s (Frémeaux & Leturcq, 2013). Consequently, we can arguably consider marriage to be an insurance mechanism in most cases in France during this period.

Article 212 of the French Civil Code states that “les époux se doivent mutuellement […] secours”. The “devoir de secours” (obligation of assistance) rarely takes the form of a legal and formal transfer of resources during marriage; it is rather supposed to come about naturally via resource-pooling and solidarity between the two spouses. However, in the case of divorce or even during the divorce proceedings, the spouse with the most-favourable financial situation can be asked to transfer resources to the other spouse.

The social-security and health-insurance eligibility conditions for the unemployed with an employed partner are less restrictive when the relationship is formalised by marriage. In the case of the death of a partner, marriage also simplifies the inheritance procedures for the surviving spouse and gives the survivor the right to receive a part of the pension of the dead spouse (“pension de reversion”).

Finally, married couples must legally support each other even after a divorce. A judge may decide that a compensatory allowance should be paid to compensate for differences in living standards between the newly-separated spouses. About 100,000 people received such a benefit at the end of the 1990s, with a monthly transfer of around 2000 Francs (306 Euros).Footnote 2 The obligation to provide child support also implies the payment of an alimony to the spouse with custody of the children – with the amount of the alimony being determined either by the parents or a judge. Given that women have lower incomes than men on average, and that children were in the sole custody of the mother in 80% of divorce cases in the late 1990s in France,Footnote 3 the various pensions paid in the event of divorce can also be seen as a source of marriage-related insurance for women.

3.2 The unemployment benefit system in France at the end of the 1990s

The French unemployment insurance scheme provided two benefits at the end of the 1990s: the “allocation unique dégressive” (AUD) et “l’allocation de chômeurs âgés” (ACA). The former varies by age and the time spent in employment. The eligible unemployed need to have spent at least four months in employment out of the last eight. The duration of AUD benefits ranges from four months to five years. The AUD replacement rate changes over time: it is at its maximum level during the first months of unemployment and then falls. Only workers who had worked for over 160 trimesters were eligible for the ACA for a limited amount of time, at the full ACA replacement rate. At the end of 2000, average monthly unemployment benefits were 5202 Francs, for an average replacement rate of 68%. Note that unemployment benefits do not depend on marital status. See https://travail-emploi.gouv.fr/IMG/pdf/publication_pips_200111_n-46-1_indemnisation-chomage-99-2000.pdf for a complete description of the French unemployment benefit system.

3.3 The Delalande tax

The French government introduced the Delalande tax in 1987, with the goal of tackling rising layoffs among older workers. While there were a number of modifications between its implementation and its final abolition in 2008, the principle of the experience-rating of the tax did not change: firms that laid off older workers (where the definition of “old” has changed over time) were required to pay the Delalande tax to help balance the unemployment-insurance system. This tax was proportional to the gross wage of the laid-off worker, and was applied to private-sector permanent-contract workers. From 1987 to 1992, the amount of tax due following the layoff of a worker aged 55 or over was equal to three months of gross wages. The tax rules were revised in July 1992, January 1993, and January 1999; in particular, starting in 1992 this layoff tax was extended to all workers aged 50 or above.

Table 1 reports the different schemes of the Delalande tax over time according to firm size and the age of the laid-off worker. From 1993 to December 1998, the tax to be paid only depended on worker age, and was independent of firm size. From January 1999 up to its abolition in 2008 the Delalande tax rose, but only for firms with 50 or more employees. This tax represents a non-trivial part of the total separation costs: in Behaghel et al. (2004) the average separation costs for older workers in France ranged from 3 to 11 months of gross wages, with over half of this cost reflecting the payment of the Delalande tax.

The net effect of the Delalande contribution on employment is theoretically ambiguous. First, a company looking for a new employee might prefer to avoid the anticipated extra-cost of a dismissal due to the Delalande tax by hiring a young worker. This perverse effect was identified and then corrected with the 1992 reform which introduced an exemption from payment of the tax for all unemployed people over age 50 who find a job (after at least three months of unemployment). Behaghel et al. (2004) use this exogenous change to show that the hiring of older workers was indeed reduced before 1992 due to this tax.

Second, a higher Delalande tax should reduce the separation rate of older workers. Behaghel et al. (2004) also address this issue, and show that while in general the increase in the Delalande tax over time had only modest effects on this separation rate, the 1999 reform (which we analyse here) did have a greater effect in protecting older workers against separations.

Last, the theoretical model in Behaghel (2007) predicts that a higher Delalande tax has another perverse effect: it should also increase the separation rate of younger workers. The results in Georgieff and Lepinteur (2018) are consistent with these predictions. In data from the French component of the ECHP, the perceived job insecurity of younger workers in larger firms rose due to the perverse effects of the higher Delalande tax; and data from the French Labour Force Survey reveal an increase in the actual risk of layoff for the same group.

We here aim to establish the causal impact of this exogenous variation in job insecurity resulting from the 1999 reform on the marriage probability of younger workers. We do so by exploiting the firm-size discontinuity and the resulting increase in job insecurity for younger workers in treated firms. The 1999 rise in the Delalande tax provides a natural quasi-experiment allowing for a difference-in-differences (D-i-D) analysis, where the treatment group is younger workers (under age 50) in large private firms (whose job insecurity changed) and the control group younger workers in smaller private firms (who were not affected by the reform).

As the 1999 reform of the Delalande tax was announced by the French government one year beforehand (in early 1998), and the reintroduction of the firm-size discontinuity was also public knowledge by the end of 1998, employers may have strategically adjusted their labour demand before the official change in the Law. There is evidence of such anticipation effects in Georgieff and Lepinteur (2018), as employers in large firms dismissed relatively-more employees between the announcement and the implementation of the reform. Higher layoffs are found for both those aged over 50 and younger workers, so that the tax rise brought about some restructuring in the treated firms.Footnote 4 Given this anticipation, job insecurity for the younger workers in large firms may have risen before the reform’s implementation. We take this possibility into account by estimating the following D-i-D equation, including both a post-1999 treatment effect and a 1998 announcement effect of the reform:

This equation is estimated only for workers under the age of 50. Here Yit is either the perceived job security of worker i, or a dummy variable for worker i being married in year t.Footnote 5Treatit indicates whether a worker belongs to the treatment group: it is equal to one for younger private-sector workers in large firms (50+ employees) and to zero for younger private-sector workers in firms with fewer employees. The Post1998t dummy captures observations on individuals after the implementation of the higher Delalande tax (in January 1999), λt are year fixed effects (so that λ1998 covers observations in the policy-announcement year of 1998) and Xit is a set of individual characteristics. This latter contains the following variables: age dummies (in five-year bands), health status, the lagged number of children in the household,Footnote 6 the monthly wage (logged), weekly working hours, and occupation and region fixed effects. We also account for time-invariant heterogeneity by controlling for individual fixed effects µi. The main effects of λ1998 and Post1998t are entirely subsumed by the year dummies. The coefficients of interest in the equation above are α2 and α3: these respectively capture the impacts of the reform’s announcement in 1998 and its implementation from 1999 onwards on first job security and then marital status.

The risk-sharing hypothesis predicts positive and significant α2 and α3 coefficients for workers in the marriage-probability regression, reflecting their greater risk from higher job insecurity and the subsequent rise in the demand for insurance. However, it is also possible that the treatment reduces the probability of marriage, as workers who have become more at risk of layoff are now seen to be “riskier” partners.

The effects of the announcement and the implementation of the reform are expected to be of the same sign. As such, we also estimate the simpler D-i-D regression below:

where Post1997t is a dummy variable reflecting observations after the announcement year of the higher layoff tax (from 1998 onwards). The coefficient β2 in Eq. (2) now captures what we will consider as the “total effect” of the reform, starting from its announcement. As such, β2 corresponds to Eq. (1) when α2 = α3. Both Eqs. (1) and (2) will be estimated using linear techniques (although we will also estimate non-linear regressions in the robustness checks).

4 The ECHP data and the estimation sample

Our empirical analysis is based on the European Community Household Panel (ECHP). This is a nationally-representative longitudinal survey of households that covered 15 European countries (including France) between 1994 and 2001. The sample size in France was on average 12,000 adults per wave. The interviews mainly took place at the end of the year (between November and December). The ECHP data includes a large set of variables on a variety of aspects of respondents’ lives, including demographic characteristics, financial situation, employment, and health.Footnote 7 Respondents report their marital status in each ECHP wave.

The 1999 increase in the Delalande tax only applied to private-sector firms with 50 or more employees. The ECHP records the number of workers in the firm in which the respondent is employed using the following categories: “None”, “1 to 4”, “5 to 19”, “20 to 49”, “50 to 99”, “100 to 499” and “500 or more”. This is the variable that we will use to assign younger workers to the treatment or control groups.

In the first part of our analysis, we show that the higher layoff tax for those aged 50 or over in larger firms produced greater feelings of job insecurity for individuals aged under 50 working in the same firms; the main analysis will then address the question of whether this same tax rise affected marriage.

Our measure of job insecurity comes from the following ECHP question:

“How satisfied are you with your present job in terms of job security?”

The answers to this satisfaction question were given on a scale from 1 to 6, with 1 corresponding to “Not Satisfied” and 6 to “Fully Satisfied”.Footnote 8 Böckerman et al. (2011) show that this measure of perceived job security reflects objective variations in layoff and hiring rates. It is also known to be a strong predictor of individual choices on the labour market such as job quits (Clark, 2001). Footnote 9In Clark and Postel-Vinay (2009), it is also correlated with unemployment-insurance benefits, permanent contracts, and employment-protection legislation.

Our analysis sample is made up of private-sector workers between the ages of 20 and 49 with permanent contracts, and with valid information on perceived job security, job characteristics, and the sociodemographic variables. As the details of the reform were public knowledge before its implementation, employers may have deliberately changed their labour demand. We will thus only analyse workers who report the same firm size from 1997 onwards in order to address any issues of self-selection into the treatment. By doing so, we lose a little under 6% of the baseline sample (the coefficients for the effect of job insecurity on the probability of being married are actually not materially affected by this restriction). Note that we do not consider here the workers who were protected by the reform, i.e. workers aged 50+. Almost 80% of respondents in this group were already married, and there was little subsequent movement out of marriage (97.5% of those aged 50+ reported the same marital status during the years before and after the announcement of the reform). The limited within-variation considerably attenuates the statistical power for this older group.

Our analysis sample consists of 10,371 observations on 2797 different individuals over the 1995 to 2001 period (we cannot include the first 1994 ECHP wave, as it does not include information on whether the firm is public or private) between the ages of 20 and 49. Appendix Fig. 3 describes the number of observations at each stage of our sample selection. Table 2 listsFootnote 10 the descriptive statistics first for the whole analysis sample and then separately by gender. Just under half (47%) of the sample are in the treated group. With respect to our two dependent variables, 57% of observations come from individuals who report being married, and average job security is equal to 4.13. The women in our sample are on average more educated than their male counterparts but report fewer weekly working hours and lower monthly wages.

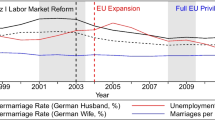

Although we focus on a particular part of the French population, i.e. young private-sector workers with a permanent contract, the share of married workers in our estimation sample is similar to that in national statistics (see Fig. 1). The share of cohabiting workers in our sample is slightly higher than the national figure, which likely reflects that we exclude individuals above age 49. The marriage share in the French adult population fell steadily from 1990 to 2009 in Fig. 1, from 56 to 52%. Over the same period, the share of cohabiting individuals rose markedly by 9.5 percentage points (from 6.7 to 16.2%).

Marriage and cohabitation rates in France from 1990 to 2009. The marriage and cohabitation rates correspond respectively to the number of married and cohabiting individuals divided by the size of the adult population. These rates were calculated using data from the INED time series on the number of married and cohabiting couples (https://www.ined.fr/fr/tout-savoirpopulation/chiffres/france/couples-menages-familles/couples_menages_familles/) and the UN website (http://data.un.org/Data.aspx?d=POP&f=tableCode%3A22) for the adult population

5 Main results

The effect of the higher Delalande firing tax on the perceived job security of younger workers appear in Table 3. These results come from the analysis sample described in Table 2. Columns (1), (3), and (5) of Table 3 display the D-i-D estimates of Eq. (1), where we separately identify the effects of the announcement and implementation of the tax change. The estimates in columns (2), (4), and (6) then refer to the coefficients in Eq. (2), where we combine the effects of the announcement and implementation of the reform into one “total” effect. The first two columns of Table 3 show the estimates for the whole sample, while columns (3), (4) and (5), (6) respectively refer to those for women and men.

Column (1) reveals that the perceived job security of younger workers in large firms fell significantly after the 1999 rise in the layoff tax (as compared to that of younger workers in smaller firms, where the layoff tax remained unchanged). This fall is seen after both the announcement and the implementation of the higher layoff tax. The magnitude of the estimates is in line with the findings in Georgieff and Lepinteur (2018) and Clark and Lepinteur (2022).Footnote 11 We carry out pairwise Wald-tests to confirm that there is no statistical difference between the estimated announcement and implementation impact of the tax change in the first and second rows. Column (2) then combines these two into one variable reflecting the total effect of the reform. Unsurprisingly, the estimated coefficient on this variable turns out to be significantly different from zero, negative, and of similar size to the two coefficients in column (1). Our estimates suggest that the perceived job security of younger workers in treated firms fell by 0.2 points due to the 1999 increase in the Delalande tax: from Table 2, this corresponds to a change of one-sixth of a standard deviation. We find similar estimates for women and men in the remaining columns of Panel A. Although the reform effects look larger for men, given the associated standard errors these gender differences are not significant. We can replicate these results using a simple binary variable for job security (comparing values 1–4 against 5-6): all of the treatment estimates continue to be significant, with an effect that is again larger, but not significantly so, for men.

Panel B of Table 3 assesses the impact of greater job insecurity on the probability of being married in the same analysis sample.Footnote 12 The estimated coefficients for the whole sample in columns (1) and (2) are positive but not significant at conventional levels. As it has been suggested that women are on average more risk averse than men (Sunden &d Surette, 1998; Finucane et al., 2000; Hartog et al., 2002; Holt & Laury, 2002; Fehr-Duda et al., 2006; Croson & Gneezy, 2009; Charness & Gneezy, 2012), we might expect these estimates to differ by gender. The results in columns (3) and (4) show that women are significantly more likely to be married following the implementation of the reform. In line with Panel A, the pairwise Wald-tests again confirm that there is no statistical difference between the anticipation and implementation effects of the reform. We combine these two effects in column (4), and find that the rise in the Delalande tax increased the probability of being married for women by just over four percentage points.Footnote 13 This corresponds to 7.5% of the pre-reform share of married women in the treated group (57%). It is also half of the observed difference in female marriage rates between the early- and late −20 age groups (see Table 7).

There is no significant marriage effect for the corresponding sample of men in columns (5) and (6). A first possibility is that prime-age women who worked in permanent private-sector jobs in the 1990s in France were differentially selected than their male counterparts. The comparison of the pre-reform characteristics of men and women who do and do not appear in our estimation sample actually reveals only small differences: there is more positive selection of women into the estimation sample by education than there is for men, and less selection by hours of work. However, we control for both of these variables in our estimations (and will, in addition, show below that there is no differential effect of the reform treatment on marriage by either education or hours of work).

Second, this may reflect that men are on average less risk-averse: the rise in job insecurity from the 1999 increase in the Delalande tax may not have had much effect on their demand for insurance. Last, men who looked for insurance through marriage may not have been able to find it: their greater job insecurity may make them less attractive. This is consistent with Ekert-Jaffé and Solaz (2001, 2002) and Landaud (2021), where men without a job or in temporary employment were less likely to be partnered.

Third, according to Oppenheimer (1988) and subsequent work (see Kalmijn, 2011, for a detailed review), the job security of men has a greater influence on the marriage decision than does that of women in societies where men are traditionally considered as the breadwinner. In our case, the loss in job security caused by the 1999 rise in the Delalande tax may be more detrimental for men in the sense that their “value” as a spouse is reduced.

One of the requirements for D-i-D estimation to produce causal effects is that of a common trend in the dependent variable in the control and treatment groups in the absence of the policy reform. Figure 5 in the Online Appendix provides additional evidence in favour of the parallel-trend assumption by plotting the time profile of average perceived job security and the marriage probability for the control and treatment groups. In the spirit of an event-study, Fig. 2 thus plots the estimated yearly effects of being in the treatment (as opposed to the control) group on perceived job security (in Panel A) and the probability of being married (Panel B). The left-hand side shows the results for the whole sample and the right-hand figure those for men and women separately.Footnote 14 None of the pre-reform announcement estimates (that can be considered as placebos) in Fig. 2 are significantly different from zero, providing evidence in favour of the common-trend assumption.Footnote 15 On the contrary, all the post-reform announcement estimates in Panel A are significantly different from zero with no significant differences by sex. The fall in perceived job security is also constant over time, so that there does not seem to be any adaptation to the 1998 rise in the Delalande tax. The figures in Panel B confirm what we saw in Table 3: only women reported a greater probability of marriage rose after the announcement of the reform. As with perceived job security, the treatment effects on marriage remain stable over time.Footnote 16

Parallel-trend assumption—panel results. The data come from the French component of the ECHP panel. The analysis sample is made up of individuals who work in the private sector, with a permanent contract, and who are aged between 20 and 49. There are 10371 observations in the whole sample (2797 individuals), 4248 observations in the sample of women (1175 individuals), and 6123 observations in the sample of men (1622 individuals). Each point shows the gap in the outcome between the treatment group (i.e. being a younger worker in a firm with 50 or more employees) and the control group (being a younger worker in a firm with fewer than 50 employees) in that year, as compared to the same gap in the omitted year (1995). These numbers come from regression analyses that control for year and individual fixed effects, as well as age dummies (in five-year bands), health status, the (lagged) number of children in the household, the log of the monthly wage, weekly working hours, and occupation and region fixed effects. The error bars represent the 90% confidence intervals. The dotted vertical line shows the date at which the increase in the Delalande tax was announced, and the dashed vertical line the date of its implementation. Men and women were interviewed at the same date; we have slightly left-shifted the points for men so that the confidence intervals can be seen

The causal interpretation of our estimates also relies on there being no endogenous changes in the sample composition. By initially excluding the workers who reported a change in firm size after the announcement of the reform, we addressed the issue of self-selection into treated or control firms. This restriction addresses both the influence of workers changing jobs and firms adjusting the number of employees. However, we also need to ensure that the reform, via differences in layoff decisions between small and large firms, did not change the sample composition. We rule out this possibility in Appendix Tables 8 and 9, where we find no significant differences in the gaps between the control and treatment groups with respect to most observable characteristics before and after the reform’s announcement. However, weekly working hours in the treatment group dropped significantly more (both in the whole sample and for women) than in the control group. This is unsurprising: in 2000, the standard workweek in France fell from 39 to 35 h for workers in firms with 20 employees and more. While we do not worry about the whole sample (as there is no significant effect of the 1999 rise of the Delalande tax on the probability to be married for the whole sample), our treatment estimates for women might then capture the influence of the 2000 shorter workweek. We will rule out this possibility in the robustness section by dropping workers in firms with fewer than 20 employees from the estimation sample. Last, it could be argued that Appendix Tables 8 and 9 do not tackle endogenous changes in unobservable characteristics: we will also address this issue in the robustness check section.

Last, we ask in Table 10 whether the total impact of the increase in the Delalande Tax led to other changes in terms of marital status and couple formation. The first column of this table reproduces the estimated marriage coefficients from columns (2), (4) and (6) of Table 3 for comparison. We then consider in column (2) the probability of being in a partnership, irrespective of legal marital status: the estimates here show that the greater job insecurity from the reform had no effect on being in a couple in general. Combined with the results for marriage, we thus expect (for women) a negative reform effect on cohabitation, which is indeed what we find in column (3) of Panel B: women whose job insecurity rose following the change in the Delalande tax are less likely to be in a non-married relationship. As the ECHP is a household panel, where all adults are interviewed, and as we here focus on the transition from cohabitation to marriage, it might be thought that the estimation results for men and women should be identical (as we are looking at the two sides of a couple). This is not the case in Table 10. The explanation is that the men and women in this table do not come from the same sample of cohabitees: fully one-half of treated women who we observe switching from cohabitation to marriage marry men who are not in the sample in Panel C (as the men’s jobs are temporary or in the public sector, they are not active in the labour force, or they are aged 50 or over).

Last, Columns (4) and (5) of Table 10 look in turn at being divorced/separated or never having been in a relationship, finding no significant effects for men, women, or the whole sample.Footnote 17 That our results only concern cohabitation-marriage transitions may reflect the rather short run of post-reform observations. Had the ECHP survey continued beyond 2001, we may well have found other types of transitions too, as moving from being single or divorced to married likely takes more time than switching from cohabitation to marriage.

6 Robustness checks and heterogeneity

The estimates in Table 3 refer to the effect of the 1999 rise in the Delalande tax on first perceived job security and then marital status for the whole sample. We now turn to a number of robustness checks, and then ask whether the effects of job insecurity on the probability of being married are larger for certain types of workers. The analyses here refer to the total impact of the 1999 rise in the Delalande tax, as in Eq. (2).Footnote 18 We have also estimated the analogous effect of all of our robustness and heterogeneity tests for the estimated effect of the reform on perceived job security; these results appear in Appendix Table 11.

6.1 Robustness tests

6.1.1 Ruling out confounding events

As noted above, the 2000 working-time reduction was another notable labour-market reform around the time of the modification in the Delalande tax. In 1998, the French Ministry of Labour decided to reduce the standard workweek from 39 to 35 h, but only in larger firms (those with 20 employees or more). A shorter workweek may induce worries about job security due to potential effects on firm profitability, affecting our estimated coefficients. We evaluate this possibility by excluding all workers who were unaffected by the 35-hour week (those in firms with under 20 employees). As such, all of the workers in the restricted analysis sample will have been affected by the 35-hour week in the same way. This exclusion drops around 15% of the original estimation sample. The resulting estimated coefficients in column (1) of Table 4 are close to those in the baseline (in columns (2), (4) and (6) of Panel B in Table 3). Note that when we exclude workers in firms with under 20 employees from our estimation sample, the differences in weekly working hours in Tables 8 and 9 become statistically insignificant.

As part of our identification relies on changes over time, we should check that any effect comes from the change in the Delalande tax, and not some wider macro-economic changes. We rule this out by re-estimating our baseline D-i-D equations using samples of employees with similar characteristics from neighbouring and arguably-similar countries (where of course the French layoff tax did not apply). Although the ECHP is relatively well-harmonised across countries, we have to restrict this comparison to Spain, Italy, and Denmark due to data limitations.Footnote 19 The resulting D-i-D estimates for these three countries in columns (2), (3), and (4) of Table 4 are not significantly different from zero. The impact of job insecurity on the share of married women does not then seem to reflect macroeconomic trends.

6.1.2 The estimation method

Our main results above come from fixed-effect analyses, comparing the same individual before and after the labour-market reform. We expect fixed-effects and OLS analyses to produce different estimates for two reasons. First, the former introduce attenuation bias when there is measurement error: in absolute terms, the resulting FE estimates would be lower than their OLS counterparts. Second, unobserved individual time-invariant characteristics that are correlated with the treatment and are not controlled for in pooled analyses will bias the OLS estimates. Column (5) of Table 4 lists the treatment effects without individual fixed effects. These are somewhat larger than the baseline estimates (that include individual fixed effects) but are not statistically different.

We also ask whether our results are influenced by the way in which we define the dependent variable. As we use linear-probability models with individual fixed-effects, our baseline regressions treat the probability of being married as a cardinal variable. However, it can be argued that non-linear estimation is more suitable for this dummy dependent variable. Column (6) of Table 4 thus applies a conditional fixed-effect logit model to re-estimate our main regression. The results remain the same: job insecurity significantly increases the probability of being married for women only.

6.1.3 Sample composition

Firm size is reported by the respondent and may not be accurate. In this case, individuals can be mis-allocated to firm-size groups, and hence to the control or treatment groups. This mis-reporting may be random, in which case we estimate a lower bound of the treatment (as some of the control group are treated, and some of the treated group are not). A potentially more-serious problem arises if the mis-allocation is not random, conditional on the control variables in our regressions. We address mis-reporting using a regression in line with the donut regression-discontinuity design. We here drop employees who are close to the firm-size treatment threshold of 50 employees: from the firm-size categories listed in Section 3, this implies re-estimating the treatment without respondents who report working in firms with “20 to 49 employees” or “50 to 99 employees”. Intuitively, mis-judgement may cause workers to erroneously report a firm-size category above or below the correct value, but not to jump three categories (so that they report a firm size of under 20 employees when the real value is over 100 employees, for example).

The estimated treatment coefficients from the baseline analysis (in panel B of Table 3) and these “donut” regressions (in the last column of Table 4) are of the same size, although the estimate of the latter for women is no longer significant (due to the smaller sample size when we drop two firm-size categories, producing larger standard errors). That the estimated coefficient does not change between the two specifications helps to dispel any concerns regarding any systematic mis-reporting of firm size.Footnote 20

The last robustness check addresses the issue of attrition. 16% of both the treatment and control group left the analysis sample between the announcement of the reform and the last wave (with no noticeable differences between men and women). Our estimates may be biased if the implementation of the reform and attrition are not independent, in particular, if the marriage probability of leavers falls once they leave the survey. We rule out this issue in two ways. First, we can make use of the two attrition weights supplied by ECHP (we do not use weights in our main regressions). When we do so, our results are little affected.

We can also calculate the “unobserved” D-i-D in the attrition group that would be required to cancel out our main treatment effect. From Table 3, the difference in the probability of being married between women in treated and non-treated firms rose by 4 percentage points post-reform. To cancel this figure out, we would require the analogous figure for the 16% of women in the attrition group to be a fall of 21 percentage points after the reform (= 0.04*84/16%). This figure is more than double the largest age effect on marriage in column (4) of Table 7, and does not seem plausible.

6.2 Heterogeneity analysis

The estimates in Panel B of Table 3 show the average effect of the 1999 increase in the Delalande tax for employees in large firms. In Table 5 we consider whether these effects might change across types of workers. We first consider age as this may ambiguously affect the treatment. First, one could argue that the older workers may have less of an incentive to get married as they will spend less time on the labour market threatened by the rise in the Delalande tax than younger workers. But we also know that workers just below the age-50 threshold perceived a greater risk of job loss (as shown in Georgieff & Lepinteur, 2018) and that risk-aversion increases with age (Falk et al., 2018). We investigate by interacting the total effect of the reform with a dummy for being born in 1963 (the median birth year in the estimation sample) or before. The resulting estimates appear in columns (1) and (6) of Table 5 for women and men respectively: neither interaction term is significant. The estimated interaction terms using different birth-year thresholds are also insignificant. We also interacted the treatment effect with multiple age categories (in five- and ten-year bands) but continue to find no significant interaction terms. All of these results are available upon request.

We second know that the relationship between fertility decisions and job insecurity likely depends on education and earnings (Chevalier & Marie, 2017; Clark & Lepinteur, 2022), and ask whether an analogous relationship is found for marriage. We thus interact the treatment effect with dummies for “High-education” (for workers with post-secondary education) and “High-wage” (for workers with above-median wage), measured in the pre-reform years only.Footnote 21 The estimated coefficients on these interactions in columns (2), (3), (7) and (8) of Table 5 suggest no significant difference in the effect of job insecurity on marriage by education or wages.Footnote 22

Our last interactions concern pre-reform family characteristics. Columns (4) and (9) show that the treatment effect is significantly larger for women who had at least one child before the reform. One natural interpretation is that women with children are exposed to greater risk than men with children, as in France the former ended up with sole custody of the children in 80% of separations in the early 2000s. We also interact the treatment effects with the number of children in the household in 1998 (i.e. just before implementation of the reform). The results are displayed in columns (5) and (10). The estimated coefficients are positive and significant (and of the same size) only for women with one or two children (although that for women with three or more children is not statistically different from that for mothers with one or two children).

Why does the effect of job insecurity differ across some groups of workers? It is possible that the impact of the change in the Delalande tax on job insecurity is stronger for some workers, and especially those who already had children. We investigate in Appendix Table 12, where we replicate our heterogeneity analysis using perceived job security as the dependent variable. None of the interaction terms attracts a significant coefficient, so that impact of the reform was the same in terms of perceived job security for all of the different types of workers we consider.

A second possibility is that the relationship between perceived job security and marital status varies across workers, for reasons of risk-aversion. In Görlitz and Tamm (2015), the higher risk-aversion due to parenthood is larger for women. As such, mothers arguably constitute the most risk-averse group of workers in our estimation sample, which might explain why they are the most likely to get married after a rise in their job insecurity.

7 Risk-sharing theory

Our results above are in line with risk sharing theory, as the rise in marriage following greater job insecurity only appears for the arguably most risk-averse workers (women with children), although we have not yet provided any explicit test of this theory. In Hess (2004) and Shore (2010), couples manage income risk by trying to ensure that the two partners’ exogenous income shocks are not perfectly positively correlated. In the context of the reform analysed here, we thus expect a stronger treatment effect for women whose partner has a more stable job.

This is what we test in Table 6, where we interact the reform effect with dummy variables for different types of partners. Columns (1) and (4) show the average effect of the reform for women and men, as in Panel B of Table 3, while columns (2) and (5) show the estimated coefficients of the interaction of the reform with a dummy for “Employed Partner”. As risk-sharing theory would predict, the shift from cohabitation to marriage (following the results in Table 10) is only higher for women whose partners are currently working.Footnote 23 We find no significant results for any of the groups of men.

We then take the treatment status of the partner into account. Under risk-sharing, household members try to avoid correlated risks. The marriage incentives from job insecurity should then be weaker for women whose partner is also affected by the reform. The estimates in column (3) are in line with this prediction: marriage only rises significantly for women whose partner is not affected by exogenously-higher job insecurity. We found no significant differences in this respect for the partner working in the public vs. private sector or having a permanent vs. temporary contract (although this latter might reflect a lack of statistical power, as only around 3% of partners in our estimation sample had temporary contracts). We continue to find no significant marriage results for any of the groups of men (in the last column of Table 6).

8 Conclusion

Job insecurity increases the probability of marriage for women. The 1999 reform in the French labour market taxed the layoffs of older workers, but at the cost of switching risk to younger workers. As the higher layoff tax was applied only in larger firms, we can estimate difference-in-difference regressions. We find that the reform-induced exogenous change in the future probability of job loss both reduced perceived job security, and led to a robust significant rise in the probability of being married for women. Our identification strategy here evaluates the effect of job insecurity on the probability of being married for individuals who were in employment both before and after the reform (and not those who changed their labour-force status): as such, our insecurity is forward-looking and does not apply to events that have already taken place.

Our results are novel as they are, to the best of our knowledge, the first that appeal to a natural labour-market experiment to show that risk-sharing is one of the causes of marriage. Job insecurity increased the probability of marriage for women, and more so for those who are probably more risk-averse (mothers). In line with risk-sharing theory, we show that this marriage effect was not found for couples in which the layoff risk rose for both partners after the 1999 tax rise (i.e. couples where both members worked in treated firms). The lack of any effect for men may reveal their lower risk-aversion with respect to job insecurity, or the greater difficulty that insecure men face on the marriage market.

Part of the attraction of marriage then seems to be the risk-sharing it provides. Why then don’t all couples get married? There are a wide variety of factors at play here, including cultural norms. Some of these can be argued to be economic. In the same way that employment protection legislation might discourage hiring due to the costs of firing, more rigid or expensive divorce procedures may discourage some couples from marrying. In this case, more flexible divorce procedures may lead to more people getting married, as would a more-advantageous tax treatment of the married relative to the cohabiting. The flexibility of marriage and the labour market can thus be considered as intertwined.

Data availability

This study uses retrospective de-identified data collected by Eurostat.

Notes

The analysis in Clark and Lepinteur (2022) does not use the same sample as we do here. Their fertility analysis is carried out on the sample of workers who were already married before the reform and continued to be married after it. On the contrary, we explicitly model moves between marital statuses.

See more details in http://www.justice.gouv.fr/art_pix/rapport-prest-compens.pdf.

One aim of this restructuring may have been to avoid the tax by having fewer than 50 employees, as in Garicano et al. (2016). We will address this selection into firm size issue below by dropping workers who reported that their firms’ size changed in any year after the date at which the reform was announced.

We also consider in Appendix Table 8 the following complete set of marital outcomes: partnered, partnered but not married, divorced or separated, and never in a relationship.

It is not clear whether children should be included in the list of control variables. Marriage may encourage parenthood, or alternatively, those who already have children may be more likely to marry. Including the lagged number of children in the household as a control somewhat attenuates concerns about reverse causality. The effect of job insecurity on marriage turns out to change only little when we do not control for the lagged children variable.

For more details about the dataset, see http://ec.europa.eu/eurostat/web/microdata/european-community-household-panel.

Figure 4 in the Appendix plots the distribution of self-reported job security. Around 70% of the respondents use the values of 4 or 5 on the 1–6 scale. Negative skewness of this type is commonly found for subjective measures.

This quit analysis can also be carried out using the ECHP data: the probability of both the end of the job match, and of layoffs in particular, at time t are negatively correlated with self-reported job security at time t-1.

The fall in the number of observations due to missing values (from 13,966 to 10,936 observations) is mostly due to missing firm size. As firm size is essential in defining the treatment status in our regressions, we do not impute its missing values. Balance tests confirm that the observable characteristics of the observations dropped due to missing firm size are not significantly different from those with valid information. Around 1,000 observations are also lost because of missing values for weekly working hours. Again, these dropped observations have characteristics similar to those in the estimation sample.

The figures are not exactly the same, as the analysis samples differ across the papers. In Georgieff and Lepinteur (2018), the ECHP analysis sample pools workers of all ages, and a triple difference-in-differences is used to identify the estimated effect of the firing tax on workers below 50 and 50 or above (the age threshold). Clark and Lepinteur (2022) analyse the same age group as we do here, namely the under-50’s, but focus on the fertility behaviour of those who were already married before the reform and continued to be so afterwards.

Appendix Table 7 reports the estimated coefficients for all of the control variables.

These regressions include a number of sociodemographic controls, as noted at the foot of the table. The inclusion of these controls does not change the treatment effects. This is not surprising if the assignment to the treatment is random. The results without these control variables are available upon request.

In these latter figures we have slightly horizontally-shifted the curves for men and women so that the confidence intervals around the estimates can be seen clearly.

In the bottom-right panel of Figure A3, the marriage rate of women in the treatment group is lower than that of women in the control group before the reform. Table 9 reveals that women in the treatment group are more educated and work more hours, both of which are associated with less marriage in this age group.

These results can be explained by timing effects and changes at the extensive margin. In the first case, the decision to marry has already been taken and the reform has simply brought it forward. In the second case, the reform may have encouraged women who had not initially planned to marry to do so. Our data do not allow us to distinguish between these two cases. It is however plausible to think that the timing effect would fall over time. This is not what we see in Panel B of Fig. 2: the stable treatment effect for women suggests that timing does not play a major role.

The marital-status categories in Table 10 are not mutually-exclusive: an individual can be both divorced and in a new relationship. We find similar results to those in Table 10 when we estimate a multinomial-logit model using the following mutually-exclusive categories: “Married in a partnership”, “Non-married in a partnership”, “Divorced or separated with no partner” and “Never in a relationship” (we exclude widows here, as there are too few observations). These results are available upon request.

We obtain similar results for both the robustness checks and heterogeneity analyses when we separately estimate the effects of the announcement and implementation of the reform.

The variables in the final waves of the ECHP in Belgium and Germany do not allow us to accurately distinguish the public from the private sector, or to measure perceived job security.

As in Clark and Lepinteur (2022), we can consider public-sector workers as an alternative control group but none of our treatment estimates here were significantly different from zero at conventional levels. However, the marriage probability pre-trends differ significantly between the treatment group and public-sector workers, casting doubt on the validity of this control group. All of these results are available upon request.

We also interacted the treatment effects with a continuous measure of monthly wage (in logs), which produces similar results. Using household income rather than the monthly wage also makes no difference.

With respect to hours of work, interactions with pre-reform hours either as a continuous variable or as a dummy for part-time work (between 1 and 29 h per week) yielded no significant estimates.

The interactions in Table 6 refer to the partner’s current labour-market position. As such, the employed in row 2 may have started work after their partner was treated. Equally, in rows 3 and 4, partner treatment may have caused individuals to switch into more secure jobs (i.e. those that are not affected by the higher Delalande tax). If we only consider the partner’s pre-reform employment status, we do not allow for these behavioural reactions (if we do so we actually find similar estimates, although the coefficients are less precisely-estimated).

References

Anderson, S., & Ray, D. (2019). Missing unmarried women. Journal of the European Economic Association, 17, 1585–1616.

Becker, G. S. (1973). A theory of marriage: Part I. Journal of Political Economy, 81, 813–846.

Becker, G. S. (1981). Altruism in the family and selfishness in the market place. Economica, 48, 1–15.

Behaghel, L., Crépon, B., & Colin-Sédillot, B. (2004). Contribution Delalande et transitions sur le marché du travail. Economie et Statistique, 372, 61–88.

Behaghel, L. (2007). La protection de l’emploi des travailleurs âgés en France : Une évaluation ex ante de la contribution Delalande. Annales d’Economie et de Statistique, 85, 41–80.

Bertocchi, G., Brunetti, M., & Torricelli, C. (2011). Marriage and other risky assets: A portfolio approach. Journal of Banking and Finance, 35, 2902–2915.

Böckerman, P., Ilmakunnas, P., & Johansson, E. (2011). Job security and employee well-being: Evidence from matched survey and register data. Labour Economics, 18, 547–554.

Bolano, D., & Vignoli, D. (2021). Union formation under conditions of uncertainty: The objective and subjective sides of employment uncertainty. Demographic Research, 45, 141–186.

Borenstein, S., & Courant, P. N. (1989). How to carve a medical degree: Human capital assets in divorce settlements. American Economic Review, 79, 992–1009.

Buffeteau, S., & Echevin, D. (2004). Fiscalité et mariage. Economie Publique, 13, 3–28.

Charles, K. K., & Stephens, M. (2004). Job displacement, disability, and divorce. Journal of Labor Economics, 22, 489–522.

Charness, G., & Gneezy, U. (2012). Strong evidence for gender differences in risk taking. Journal of Economic Behavior and Organization, 83, 50–58.

Chevalier, A., & Marie, O. (2017). Economic uncertainty, parental selection, and children’s educational outcomes. Journal of Political Economy, 125, 393–430.

Chiappori, P. A. (1992). Collective labor supply and welfare. Journal of Political Economy, 100, 437–467.

Clark, A. E. (2001). What really matters in a job? Hedonic measurement using quit data. Labour Economics, 8, 223–242.

Clark, A. E., & Postel-Vinay, F. (2009). Job security and job protection. Oxford Economic Papers, 61, 207–239.

Clark, A. E., & Lepinteur, A. (2022). A natural experiment on job insecurity and fertility in France. Review of Economics and Statistics, 104, 386–398.

Croson, R., & Gneezy, U. (2009). Gender differences in preferences. Journal of Economic Literature, 47, 448–74.

De la Rica, S., & Iza, A. (2005). Career planning in Spain: Do fixed-term contracts delay marriage and parenthood? Review of Economics of the Household, 3, 49–73.

de Lange, M., Wolbers, M. H., Gesthuizen, M., & Ultee, W. C. (2014). The impact of macro-and micro-economic uncertainty on family formation in the Netherlands. European Journal of Population, 30, 161–185.

Échevin, D. (2003). L’individualisation de l’impôt sur le revenu: Equitable ou pas? Economie et Prévision, 4, 149–165.

Ekert-Jaffé, O., & Solaz, A. (2001). Unemployment, marriage, and cohabitation in France. Journal of Socio-Economics, 30, 75–98.

Ekert-Jaffé, O., & Solaz, A. (2002). Couple formation in France: The changing importance of labor market early career path. Journal of Bioeconomics, 4, 223–239.

Falk, A., Becker, A., Dohmen, T., Enke, B., Huffman, D., & Sunde, U. (2018). Global evidence on economic preferences. Quarterly Journal of Economics, 133, 1645–1692.

Fehr-Duda, H., De Gennaro, M., & Schubert, R. (2006). Gender, financial risk, and probability weights. Theory and Decision, 60, 283–313.

Finucane, M. L., Alhakami, A., Slovic, P., & Johnson, S. M. (2000). The affect heuristic in judgments of risks and benefits. Journal of Behavioral Decision Making, 13, 1–17.

Frémeaux, N., & Leturcq, M. (2013). Plus ou moins mariés: L'évolution du mariage et des régimes matrimoniaux en France. Économie et Statistique, 462, 125–151.

Garicano, L., Lelarge, C., & Van Reenen, J. (2016). Firm size distortions and the productivity distribution: Evidence from France. American Economic Review, 106, 3439–3479.

Georgieff, A., & Lepinteur, A. (2018). Partial employment protection and perceived job security: evidence from France. Oxford Economic Papers, 70, 846–867.

Görlitz, K., & Tamm, M. (2015). Parenthood and risk preferences. Ruhr Economics Papers No. 552.

Halla, M., & Scharler, J. (2012). Marriage, divorce, and interstate risk sharing. Scandinavian Journal of Economics, 114, 55–78.

Hartog, J., Ferrer‐i‐Carbonell, A., & Jonker, N. (2002). Linking measured risk aversion to individual characteristics. Kyklos, 55, 3–26.

Hess, G. D. (2004). Marriage and consumption insurance: What’s love got to do with it? Journal of Political Economy, 112, 290–318.

Holt, C. A., & Laury, S. K. (2002). Risk aversion and incentive effects. American Economic Review, 92, 1644–1655.

Kalmijn, M. (2011). The influence of men’s income and employment on marriage and cohabitation: Testing Oppenheimer’s theory in Europe. European Journal of Population, 27, 269–293.

Landaud, F. (2021). From employment to engagement? Stable jobs, temporary jobs, and cohabiting relationships. Labour Economics, 73, 102077.

Leturcq, M. (2012). Will you civil union me? Taxation and civil unions in France. Journal of Public Economics, 96, 541–552.

Oppenheimer, V. K. (1988). A theory of marriage timing. American Journal of Sociology, 94, 563–591.

Rosenzweig, M. R., & Stark, O. (1989). Consumption smoothing, migration, and marriage: Evidence from rural India. Journal of Political Economy, 97, 905–926.

Schaller, J. (2013). For richer, if not for poorer? Marriage and divorce over the business cycle. Journal of Population Economics, 26, 1007–1033.

Schneider, D., Harknett, K., & Stimpson, M. (2018). What explains the decline in first marriage in the United States? Evidence from the Panel Study of Income Dynamics, 1969 to 2013. Journal of Marriage and Family, 80, 791–811.

Schneider, D., & Reich, A. (2018). Marrying ain’t hard when you got a union card? Labor union membership and first marriage. Social Problems, 61, 625–643.

Shore, S. H. (2010). For better, for worse: Intrahousehold risk-sharing over the business cycle. Review of Economics and Statistics, 92, 536–548.

Stevenson, B., & Wolfers, J. (2007). Marriage and divorce: Changes and their driving forces. Journal of Economic Perspectives, 21, 27–52.

Sunden, A. E., & Surette, B. J. (1998). Gender differences in the allocation of assets in retirement savings plans. American Economic Review, 88, 207–211.

Van den Berg, G. J., & Gupta, S. (2015). The role of marriage in the causal pathway from economic conditions early in life to mortality. Journal of Health Economics, 40, 141–158.

Van Klaveren, C., Van Praag, B., & Van den Brink, H. M. (2008). A public good version of the collective household model: An empirical approach with an application to British household data. Review of Economics of the Household, 6, 169–191.

Weiss, Y. (1997). The formation and dissolution of families. Why marry? Who marries whom? And what happens upon divorce. Handbook of Population and Family Economics, 1, 81–123.

Xie, Y., Raymo, J., Goyette, K., & Thornton, A. (2003). Economic potential and entry into marriage and cohabitation. Demography, 40, 351–367.

Yu, J., & Xie, Y. (2015). Changes in the determinants of marriage entry in post-reform urban China. Demography, 52, 1869–1892.

Acknowledgements

We are grateful to the Editor and two anonymous referees for making good points that helped us to develop our analysis. We would also like to thank Petri Böckerman, Arnaud Chevalier, Thomas Dohmen, Markus Gebauer, Kevin Lang, Marion Leturcq, Giorgia Menta, Anne Solaz, and seminar participants at the IZA/HSE seminar for their help and feedback. We acknowledge financial support from CEPREMAP, the Fonds National de la Recherche Luxembourg (Grant C18/SC/12677653), and EUR grant ANR-17-EURE-0001.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Sample Selection. Each box shows the number of observations in the French ECHP sample, from the raw data (95,171 observations) to the sample that is used in our empirical analyses (10,371 observations)

The Distribution of Perceived Job Security in the ECHP. The data come from the French component of the ECHP panel. The analysis sample is made up of individuals who work in the private sector, with a permanent contract and who are aged between 20 and 49

Average perceived job security and the probability of being married by treatment group. The dotted vertical line indicates the date at which the rise in the Delalande tax was announced, and the dashed vertical line the date of its implementation

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Clark, A.E., D’Ambrosio, C. & Lepinteur, A. Marriage as insurance: job protection and job insecurity in France. Rev Econ Household 21, 1157–1190 (2023). https://doi.org/10.1007/s11150-022-09635-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11150-022-09635-5