Abstract

Most condominiums in China are sold forward on a pre-sale market, where purchasers and developers transact on an underlying property that is not yet completed. During the pre-sale period home buyers face a significant forward contract risk. However, home buyers can borrow mortgages from banks so that they can effectively share the forward contract risk with banks. This explains the phenomenon of irregularly high early-stage default and prepayment rates observed in residential mortgage lending in China, where there are few, if any, financial incentives for mortgage borrowers to exercise either put or call options. Mortgages collateralized by forward housing assets are riskier than are those with underlying assets traded on the spot market. However, currently Chinese mortgage banks charge the same rate to all mortgage borrowers. This inefficiency in risk sharing between mortgage borrowers’ groups in the forward and spot housing markets leads to mispricing in secondary mortgage sales and mortgage-backed security trading.

Similar content being viewed by others

Notes

As of March 2007 the exchange rate of Chinese Yuan (CNY) is one U.S. dollar = 7.74 CNY.

There is a long history of not using risk-based interest rates in China or other central-planning economies. It is also a tradition that in those countries a unified product or service is provided to all consumers.

We use the terms ‘forward market’ and ‘pre-sell market’ interchangeably.

The pre-sale period used to be around four years, but has now decreased to one to two years.

A sample pre-sale contract can be found at the Miami real estate Web site, http://www.miamirealestatetrends.com

An alternative sampling method, namely stratified sampling, can be used for a large dataset. To correct for possible sample selection bias, a weighting scheme that is assumed to be independent of error distribution can be used in the maximum likelihood estimation. Specifically, the weight addresses the stratified choice-based sampling of mortgages across loan status cells. The weight is commonly defined as the inverse of the probability that the loan is being selected from a cell in which it was sampled.

Since 2006, the China Banking Regulatory Commission has established a series of rules for building up the personal credit system and regulating pre-sale practices.

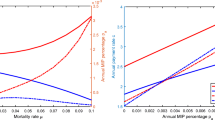

Typically one cannot estimate directly which default option is in the money without knowing the entire path of individual house values. However, we can use the initial loan-to-value ratio and the diffusion process of house prices to estimate the critical value for a borrower to exercise the put option, known as the probability of negative equity.

Log Likelihood and the Schwarz-Bayesian Criterion (SBC), reported at the bottom of the table, provide for a comparison of the goodness of fit among alternative models. Models with lower values are considered preferable.

The construction of a DCI index is similar to that of a Herfindahl index. The higher the index, the more concentrated the defaulted loans are to developers.

It is worthy of mention that a DCI—a measure of developer’s local market share—is only one way of proxying the developer’s default risk. Other omitted factors, such as developer’s default history, local market environment, etc., might also trigger developer default. We thank the editor for pointing this limitation out.

References

Black, F., & Scholes, M. S. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81, 637–654. doi:10.1086/260062.

Blinder, A. S. (1973). Wage discrimination: reduced form and structural estimates. The Journal of Human Resources, 8(4), 436–455 Fall 1973.

Buser, S. A., & Hendershott, P. H. (1984). Pricing default free mortgage. Housing Finance Review, 3, 405–429.

Case, K. E., & Shiller, R. J. (1989). The efficiency of the market for single family homes. American Economic Review, 79(1), 125–137.

Chang, L. O., & Ward, C. W. (1993). Forward pricing and the housing market: the pre-sales housing system in Taiwan. Journal of Property Research, 10(3), 217–227.

Chau, K. W., Wong, S. K., & Yiu, C. Y. (2003). Price discovery function of forward contracts in real estate markets—an empirical test. Journal of Financial Management of Property and Construction, 8(3), 129–137.

Chau, K. W., Wong, S. K., & Yiu, C. Y. (2007). Housing quality in the forward contracts market. Journal of Real Estate Finance and Economics, 34(3), 313–325. doi:10.1007/s11146-007-9018-x.

Cox, D. R. (1972). Regression models and life-tables. Journal of the Royal Statistical Society, B, 34(2), 187–220.

Cox, D. R. (1975). Partial likelihood. Biometrika, 62, 269–276. doi:10.1093/biomet/62.2.269.

Deng, Y., & Gabriel, S. A. (2006). Risk-based pricing and the enhancement of mortgage credit availability among underserved and higher credit-risk populations. Journal of Money, Credit and Banking, 38(6), 1431–1460. doi:10.1353/mcb.2006.0079.

Deng, Y., Quigley, J. M., & Order, R. V. (2000). Mortgage terminations, heterogeneity and the exercise of mortgage options. Econometrica, 68(2), 275–307. doi:10.1111/1468-0262.00110.

Deng, Y., Zheng, D., & Ling, C. (2005). An early assessment of residential mortgage performance in China. Journal of Real Estate Finance and Economics, 31(2), 117–136. doi:10.1007/s11146-005-1368-7.

Dunn, K. B., & McConnell, J. J. (1981). Valuation of mortgage-backed securities. Journal of Finance, 36, 599–617. doi:10.2307/2327521.

Findley, M. C., & Capozza, D. R. (1977). The variable rate mortgage: an option theory perspective. Journal of Money, Credit and Banking, 9, 356–364. doi:10.2307/1991985.

Green, J., & Shoven, J. B. (1986). The effect of interest rates on mortgage prepayment. Journal of Money, Credit and Banking, 18, 41–50. doi:10.2307/1992319.

Han, A. K., & Hausman, J. (1990). Flexible parametric estimation of duration and competing risk models. Journal of Applied Economics, 5(1), 1–28. doi:10.1002/jae.3950050102.

Kau, J. B., & Keenan, D. C. (1995). An overview of the option-theoretic pricing of mortgages. Journal of Housing Research, 6(2), 217–244.

Kau, J. B., Keenan, D. C., Muller, W. J., & Epperson, J. F. (1992). A generalized valuation model for fixed-rate residential mortgages. Journal of Money, Credit & Banking, 24, 279–299.

Liu, P. (2007). Asset pricing implications of hedging in real estate market, Ph.D. Dissertation, Haas School of Business, University of California, Berkeley.

Merton, R. C. (1973). Theory of rational option pricing. Bell Journal of Economics and Management Science, 4, 141–183. doi:10.2307/3003143.

Oaxaca, R. (1973). Sex discrimination in wages. In O. Ashenfelter, & A. Rees (Eds.), Discrimination in labor markets. Princeton, NJ: Princeton University Press.

Ong, S. E. (1997). Building defects, defect warranty and disincentive effects of precompletion marketing. Journal of Property Finance, 8(1), 35–50. doi:10.1108/09588689710160507.

Ong, S. E. (1999). Aborted property transactions: seller under-compensation in the absence of legal recourse. Journal of Property Investment & Finance, 17(2), 126–144. doi:10.1108/14635789910258516.

Quigley, J., & Van Order, R. (1995). Efficiency in the mortgage market: the borrower’s perspective. Journal of the American Real Estate and Urban Economics Association, 18(3), 237–252. doi:10.1111/1540-6229.00520.

Schwartz, E. S., & Torous, W. N. (1989). Prepayment and the valuation of mortgage-backed securities. Journal of Finance, 44, 375–392. doi:10.2307/2328595.

Schwartz, E. S. & Torous, W. N. (1993). Mortgage prepayment and default decisions: a Poisson regression approach. Journal of the American Real Estate and Urban Economics Association, 21(4), 431–449.

Stanton, R. (1995). Rational prepayment and the valuation of mortgage-backed securities. Review of Financial Studies, 8(3), 677–708. doi:10.1093/rfs/8.3.677.

Wong, S. K., Yiu, C. Y., Tse, M. K. S., & Chau, K. W. (2006). Do the forward sales of real estate stabilize spot prices? Journal of Real Estate Finance and Economics, 32(3), 289–304. doi:10.1007/s11146-006-6803-x.

Yi, X. R., & Huang, C. (2007). International comparison of housing pre-sale system, Jiangsu. Soc Sci :2007–03. in Chinese.

Yiu, C. Y., Hui, E. C. M., & Wong, S. K. (2005). Lead–lag relationship between the real estate spot and forward contracts markets. Journal of Real Estate Portfolio Management, 11(3), 253–262.

Acknowledgement

The authors thank Kwong-Wing Chau, Man Cho, Pierre Collin-Dufresne, Tom Davidoff, Robert Edelstein, Dwight Jaffee, Charles K. Y. Leung, Seow Eng Ong, John Quigley, Adam Szeidl, and Nancy Wallace for helpful discussions. We are also grateful to the conference participants at the 2007 American Real Estate Society Conference in San Francisco, the 2007 Symposium on Real Estate and Housing in Singapore, 2007 International AREUEA meeting in Macau, 2008 AREUEA annual meeting in New Orleans and seminar participants at Cornell University and Haas School of Business, at U.C. Berkeley. Liu acknowledged financial support from the Berkeley Fellowship. All errors are ours.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Deng, Y., Liu, P. Mortgage Prepayment and Default Behavior with Embedded Forward Contract Risks in China’s Housing Market. J Real Estate Finance Econ 38, 214–240 (2009). https://doi.org/10.1007/s11146-008-9151-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-008-9151-1