Abstract

This paper examines what happens to mortgages in the subprime mortgage market once foreclosure proceeding are initiated. A multinomial logit model that allows for the interdependence of the possible outcomes or risks (cure, partial cure, paid off, and real estate owned) through the correlation of associated unobserved heterogeneities is estimated. The results show that the duration of foreclosures is impacted by many factors including contemporaneous housing market conditions, the prior performance of the loan (prior delinquency), and the state-level legal environment.

Similar content being viewed by others

Notes

The reason lenders wait until after 90-days delinquency to start foreclosure proceedings is a hold-over from English common law called “equity of redemption.” The intent is to delay the taking of the property or the initiation of that process because the taking of someone’s home is an action with substantial and serious consequences.

Note that typically the lender “buys” the property and it becomes owned by the lender or “real estate owned”. Then the lender sells the property in an attempt to recoup as much of the losses as possible.

Another tool that could be used to reduce debt servicing requirements is to refinance into a loan with a longer repayment period or an adjustable rate loan.

The Freddie Mac Primary Mortgage Market Survey (PMMS) is used to proxy for prevailing interest rates on mortgages. Since these are subprime loans with risk premiums, the risk premium of the loan at origination is used to adjust up the PMMS rate to create a comparable market rate.

A risk in this context reflects the types of outcome (termination or cure) in each month that compete to be observed.

A well-known example illustrates a problem with this assumption. A traveler has a choice of going to work by car or by a blue bus. Let the choice probabilities be equal, implying the ratio of probabilities equals 1. Now introduce a choice of a red bus that the traveler considers equivalent to a blue bus. We would expect the probability of going to work by car to remain the same at 0.5, while the probabilities of going to work by bus would be split evenly between blue and red buses at 0.25. If this were true, then the ratio of probabilities between car and blue bus, formerly at 1, would now be equal to 2 (0.5 divided by 0.25). The multinomial logit model does not allow this possibility. Recall that there are equal probabilities of taking a blue bus and a red bus. The only profile of probabilities that fit these two constraints puts equal probability of 0.33 on each choice. The multinomial logit would therefore overestimate the probability of taking a blue or a red bus and would underestimate the probability of taking a car.

The likelihood function is maximized in SAS using Proc NLP, and the code is available on request from the author.

During estimation at most two mass points could be identified. Attempts to estimate with three mass-points could not converge or drove the size of one group to almost zero.

Phillips and VanderHoff (2004) do include a variable called default-time, but they only analyze the last observed outcome in their sample. Therefore, it is difficult to create or interpret a baseline estimate.

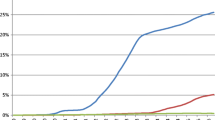

The conditional monthly probability of curing or partially curing is over 89% in the 37th month.

Replacing jud and srr with “months to complete initial action” the coefficient estimates for each outcome are cure (−0.144439), partial cure (−0.535416), REO (−0.251730), paid off (−0.421515). The mean “months to complete initial action” is 4.84 months ranging from 1 to 9 months.

References

Ambrose, B., & Capone, C. (1996). Do lenders discriminate in processing defaults. Cityscape, 2(1), 89–98.

Ambrose, B., & Capone, C. (1998). Modeling the conditional probability of foreclosure in the context of single-family mortgage default resolutions. Real Estate Economics, 26(3), 391–429.

Ambrose, B., & Capone, C. (2000). The hazard rates of first and second defaults. Journal of Real Estate Finance and Economics, 20(3), 275–293.

Ambrose, B., & Sanders, A. (2005). Legal Restrictions in Personal Loan Markets. Journal of Real Estate Finance and Economics, 30(2), 133–151.

Ambrose, B., Buttimer, R., & Capone, C. (1997). Pricing mortgage default and foreclosure delay. Journal of Money, Credit, and Banking, 29(3), 314–325.

Capozza, D., & Thomson, T. (2005) Optimal stopping and losses on subprime mortgages. Journal of Real Estate Finance and Economics, 30(2), 115–131.

Capozza, D., & Thomson, T. (2006). Subprime transitions: Lingering or malingering in default? Journal of Real Estate Finance and Economics, 33(3), 241–258.

Clapp, J., Deng, Y., & An, X. (2006). Unobserved heterogeneity in models of competing mortgage termination risks. Real Estate Economics, 34(2), 243–273.

Clauretie, T. M., & Sirmans, G. S. (2006). Real estate finance: Theory and practice, (5th ed., p. 287). Mason: Thomson South-Western Publishing.

Danis, M., & Pennington-Cross, A. (2005). A dynamic look at subprime loan performance. The Journal of Fixed Income, 15(1), 28–39.

Deng, Y., Quigley, J., & Van Order, R. (2000). Mortgage termination, heterogeneity, and the exercise of mortgage options. Econometrica, 68(2), 275–307.

Dong, X., & Koppelman, F. S. (2003). Comparison of methods representing heterogeneity in logit models. Presented at the 10th International Conference on Travel Behaviour Research, Lucerne, 10–15 August 2003.

Harding, J., Miceli, T., & Sirmans, C. F. (2000). Deficiency Judgments and Borrower Maintenance: Theory and Evidence. Journal of Housing Economics, 9(4), 267–85.

Heckman, J., & Singer, B. (1984). A method for minimizing the impact of distributional assumptions in econometric models of duration data. Econometrica, 52(2), 271–320.

Lambrecht, B., Perraudin, W., & Satchell, S. (2003). Mortgage default and possession under recourse: A competing hazards approach. Journal of Money, Credit, and Banking, 35(3), 425–442.

McFadden, D. (1978). Modeling the choice of residential location. In A. Karlquist et al (Ed.), Spatial interaction theory and residential location (pp. 75–96). Amsterdam: North-Holland.

Pence, K. M. (2003). Foreclosing on opportunity: State laws and mortgage credit. Board of Governors of the Federal Reserve System (U.S.), Finance and Economics Discussion Series: 2003-16.

Pennington-Cross, A. (2006). The value of foreclosed property. Journal of Real Estate Research, 28(2), 193–214.

Phillips, R., & Rosenblatt, E. (1997). The legal environment and the choice of default resolution alternatives: An empirical analysis. Journal of Real Estate Research, 13(2), 145–154.

Phillips, R. A., & Vanderhoff, J. H. (2004). The conditional probability of foreclosure: An empirical analysis of conventional mortgage loan defaults. Real Estate Economics, 32(4), 571–588.

Train, K. (2003). Discrete choice methods with simulation. Cambridge: Cambridge University Press.

Wen, C.-H., & Koppelman, F. S. (2001). The generalized nested logit model. Transportation Research: Part B: Methodological, 35(7), 627–641.

Yu, X. (2006). Competing risk analysis of Japan’s small financial institutions. Stanford University, Department of Economics Working Paper.

Acknowledgements

This research was started while the author was affiliated with the Federal Reserve Bank of St. Louis and the views expressed in this research are those of the individual author and do not necessarily reflect the official positions of the Federal Reserve Bank of St. Louis, the Federal Reserve System, or the Board of Governors.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Pennington-Cross, A. The Duration of Foreclosures in the Subprime Mortgage Market: A Competing Risks Model with Mixing. J Real Estate Finan Econ 40, 109–129 (2010). https://doi.org/10.1007/s11146-008-9124-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-008-9124-4