Abstract

This paper examines the long-term linkages between seven Central and Eastern European (CEE) emerging stock markets and two developed stock markets, namely the German and the US markets. The stability of the long-run relationships is studied using recursive cointegration analysis. The results reveal that the financial linkages between the CEE markets and the world markets increased with the beginning of the EU accession process. Furthermore, the application of the Gonzalo and Granger (J Bus Econ Stat 13:27–35, 1995) methodology indicates that the examined stock markets are partially integrated, while there is also evidence that the emerging stock markets of Central and Eastern Europe except for Estonia together with the German and the US stock markets, have a significant common permanent component, which drives this system of stock exchanges in the long run. Finally, it is worthwhile to note that the global financial crisis of 2007–2009 caused a slowdown in the convergence process. In addition we find evidence that the Slovenian stock market exhibits a moderate increase in the transitory component and this may be attributed to the Slovenian full membership in the euro area.

Similar content being viewed by others

Notes

Lucas (1982) states that the important implication of integrated capital markets is the equalization among countries of marginal rates of substitution in consumption, both intertemporally and across states of nature. This paper does not attempt to address the question of international capital market integration and for the most part focuses on the purely statistical exercise of detecting and estimating cointegration relations or common stochastic trends.

During the period January 2004 to December 2004 the CEE stock exchanges under investigation recorded significantly high returns. The Romanian stock exchange recorded a return of 103.5%, the Slovakian 83.9%, the Hungarian 57.2%, the Estonian 57.1%, the Czech 50.9%, the Polish 27.9% and the Slovenian 24.7%.

Kasa (1992) is among the first studies that examine long-run convergence of major stock markets using cointegration techniques. Since then a voluminous literature has developed in the area and overall there is supportive evidence in favour of convergence of both major and emerging stock markets at least over the long-term.

The increased interest in the CEE stock exchanges is revealed by the increased market capitalization as well as the increased foreign participation in CEE stock exchanges (see Table 1).

iShares MSCI Eastern Europe 10/40 Exchange Traded Fund (ETF) launched on November 4, 2005 to offer exposure to companies in CEE emerging markets to international investors.

We select Germany and the US as the key developed markets because these markets are the biggest, in terms of market capitalization, in North America and the Eurozone, respectively, and they can serve as proxies for the rest of the mature markets in both regions, in depicting possible linkages with the emerging European stock markets examined. Furthermore, the German and the US markets have an influential role in emerging European stock market movements due to their significant investment flows in these markets (see Table 1).

Bulgaria, Latvia and Lithuania are not included in this study due to data inadequacy. Nevertheless, our sample is representative of the three different market regions, namely the Central and Eastern Europe (Czech Republic, Hungary, Poland, Slovakia, Slovenia), the Baltic (Estonia) and the Balkans (Romania).

As of this writing (January 2009), the crisis is ongoing.

The regression of ΔX t and X t - 1 on ΔX t - 1,...,ΔX t - k + 1 and μ gives the residuals R 0t and R 1t , respectively, and residual product matrices \( S_{ij} = T^{ - 1} \sum\nolimits_{t = 1}^T {R_{it} } R\prime _{jt} {\text{ }},{\text{ }}i,j = 0,1 \).

The time period was set to start in September 1997, when the calculation of the BET index started, while after 1997 the majority of the stock exchanges examined had lifted most of the restrictions on foreign investment.

Expressing the stock price indices in their national currencies restricts their changes to the movements in the stock prices only avoiding distortions of the cointegration analysis results induced by numerous devaluations of the exchange rates that have taken place in the CEE region during the period covered in our sample [see Voronkova (2003)].

However, we should note that due to the financial turmoil of 2007–2009 these stock markets lost at least 50% of their value from June to November 2008.

Romania has also followed a mass privatization program, but all of the newly privatized companies listed on an over-the-counter market, the RASDAQ. In December 1998, 5,946 companies were listed on the RASDAQ market.

ADRs are receipts for shares of stock in foreign companies that are held in a custodial account by or for a US bank. These receipts are traded on US exchanges in US dollars. ADRs entitle the owners to all dividends, capital gains or losses, and voting rights, just as if the underlying shares were owned directly.

There are ten categories which refer to controls on: Capital market securities, Money market instruments, Collective investment securities, Derivative and other instruments, Commercial credits, Financial credits, Guarantees, securities and financial backup facilities, Direct investment, Liquidation of direct investment and Real estate transactions.

The Capital Account Openness index is for 2002.

Prior to the estimation of the VECM model we conduct unit root and stationarity tests to determine the stochastic properties of the data. We employ the Elliot et al. (1996) and Elliot (1999) GLS augmented Dickey-Fuller and Ng and Perron (2001) GLS versions of the modified Phillips-Perron (1988) unit root tests. For robustness we also apply the Kwiatkowski et al. (1992) KPSS stationarity test. The results show that we are unable to reject the null hypothesis of a unit root in the data for the levels of all stock price series, whereas the returns are I(0) processes. To save space the results are available upon request.

The autocorrelation hypothesis is tested with the use of the Lagrange-Multiplier test, up to six lags. The LM-statistic is 79.15 with 0.53 p-value distributed as a chi-square with 81 dof.

Johansen (1995, Chapter 11, Corollary 11.2 and Theorem 11.3, pp. 161–162) defines a number of sub-models of the general model (2), under the assumption of cointegration and with successive restrictions on the deterministic part of the model (μ). We tested the five sub-models against each other using the likelihood ratio tests and concluded that the second model, in which there are no trends but a constant term is allowed in the cointegration relations, describes best the examined groups of markets.

To account for small sample bias we apply the small sample correction coefficient on the Likelihood Ratio Trace test as suggested by Reimers (1992).

Septhon and Larsen (1991) have shown that Johansen’s tests may be characterized by sample dependency

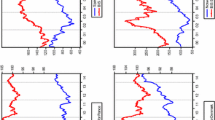

In the “X-representation” all the parameters of VECM are re-estimated during the recursions, while under the “R-representation” the short-run parameters are fixed to their full sample values and only the long-run parameters are re-estimated.

The results of the rolling window estimation are available upon request.

According to Dvorak and Podpiera (2006), the integration of the CEE stock markets increased in the months following the 2001 announcement of the EU enlargement.

The evidence on high correlation coefficients maybe due to the increased volatility of all the CEE stock markets during the last 15 months and it may be considered as an indication of financial contagion.

References

Bekaert G (1995) Market integration and investment barriers in emerging equity markets. World Bank Econ Rev 9:75–107 doi:10.1093/wber/9.1.75

Bekaert G, Harvey CR (1995) Time-varying world market integration. J Finance 50:403–444 doi:10.2307/2329414

Bekaert G, Harvey CR (1997) Emerging equity market volatility. J Financ Econ 43:29–77 doi:10.1016/S0304–405X(96)00889–6

Bekaert G, Harvey CR (2004) Chronology of economic, political and financial events in emerging markets, http://www.duke.edu/~charvey/Country_risk/chronology/chronology_index.htm

Dvorak T, Podpiera R (2006) European Union enlargement and equity markets in accession countries. Emerg Mark Rev 7:129–146 doi:10.1016/j.ememar.2005.09.009

Egert B, Kocenda E (2005) Contagion across and integration of Central and Eastern European stock markets: Evidence from intraday data. William Davidson Institute, Ann Arbor, Working paper, 798

Elliott G (1999) Efficient tests for a unit root when the initial observation is drawn from its unconditional distribution. Int Econ Rev 44:767–784 doi:10.1111/1468-2354.00039

Elliott G, Rothenberg JT, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64:813–836 doi:10.2307/2171846

Fraser P, Oyefeso O (2005) US, UK and European stock market integration. J Bus Finance Account 32:161–181 doi:10.1111/j.0306-686X.2005.00591.x

Garcia Pascual A (2003) Assessing European stock markets (co)integration. Econ Lett 78:197–203 doi:10.1016/S0165-1765(02)00245-8

Gelos G, Sahay R (2000) Financial market spillovers in transition economies. Econ Transit 9:53–86 doi:10.1111/1468-0351.00067

Gilmore CG, McManus GM (2002) International portfolio diversification: US and Central European equity markets. Emerg Mark Rev 3:69–83 doi:10.1016/S1566-0141(01)00031-0

Gilmore CG, Lucey B, McManus GM (2005) The dynamics of Central European equity market integration. IIIS, Dublin IIIS Discussion paper 69

Gonzalo J, Granger CWJ (1995) Estimation of common long-memory components in cointegrated systems. J Bus Econ Stat 13:27–35 doi:10.2307/1392518

Hansen H, Johansen S (1993) Recursive estimation in cointegrated VAR models. Institute of Mathematical Statistics, University of Copenhagen, Copenhagen Discussion Paper

Hansen H, Johansen S (1999) Some tests for parameter constancy in cointegrated VAR models. Econometrics J 2:306–333 doi:10.1111/1368-423X.00035

Johansen S (1988) Statistical analysis of cointegrating vectors. J Econ Dyn Control 12:231–254 doi:10.1016/0165-1889(88)90041-3

Johansen S (1991) Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica 59:1551–1580 doi:10.2307/2938278

Johansen S (1992a) A representation of vector autoregressive processes integrated of order 2. Econometric Theory 8:188–202

Johansen S (1992b) Determination of cointegration rank in the presence of a linear trend. Oxf Bull Econ Stat 54:383–397

Johansen S (1994) The role of the constant and linear terms in cointegration analysis of stationary variables. Econometric Rev 13:205–229 doi:10.1080/07474939408800284

Johansen S (1995) Likelihood-based inference in cointegrated vector autoregressive models. Oxford University Press, Oxford

Kasa K (1992) Common stochastic trends in international stock markets. J Monet Econ 29:95–124 doi:10.1016/0304-3932(92)90025-W

Kwiatkowski D, Phillips PCB, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J Econom 54:159–178 doi:10.1016/0304-4076(92)90104-Y

Linne T (1998) The Integration of the Central and Eastern European equity markets into the international capital markets. Institut für Wirtschaftsforschung Halle, Halle Working Paper

Lucas RE (1982) Interest rates and currency prices in a two-country world. J Monet Econ 10:335–359 doi:10.1016/0304-3932(82)90032-0

MacKinnon JG, Haug AA, Michelis L (1999) Numerical distribution functions of likelihood ratio test for cointegration. J Appl Econ 14:563–577 doi:10.1002/(SICI)1099-1255(199909/10)14:5<563::AID-JAE530>3.0.CO;2-R

Ng S, Perron P (2001) Unit root tests in ARMA models with data dependent methods for selection of the truncation lag. J Am Stat Assoc 90:268–281 doi:10.2307/2291151

Phylaktis K, Ravazzolo F (2005) Stock market linkages in emerging markets: implications for international portfolio diversification. J Int Financ Mark Inst Money 15:91–106 doi:10.1016/j.intfin.2004.03.001

Reimers H-E (1992) Comparison of tests for multivariate co-integration. Statist Papers 33:335–359 doi:10.1007/BF02925336

Röckinger M, Urga G (2001) A time-varying parameter model to test for predictability and integration in the stock markets of transition economies. J Bus Econ Stat 19:73–84 doi:10.1198/07350010152472634

Scheicher M (2001) The comovements of stock markets in Hungary, Poland and the Czech Republic. Int J Finance Econ 6:27–39 doi:10.1002/ijfe.141

Schotman P, Zalewska A (2005) Non-synchronous trading and testing for market integration in Central European emerging markets. CEPR, London Discussion Paper

Sephton PS, Larsen KH (1991) Tests of exchange market efficiency: fragile evidence from cointegration tests. J Int Money Finance 10:561–570 doi:10.1016/0261-5606(91)90007-7

Sims CA (1980) Macroeconomics and reality. Econometrica 48:1–48 doi:10.2307/1912017

Syriopoulos T (2004) International portfolio diversification to central European stock markets. Appl Financ Econ 14:1253–1268 doi:10.1080/0960310042000280465

Voronkova S (2003) Instability in the long-run relationships: Evidence from the Central European emerging stock markets. Institute for International Integration Studies, Dublin Discussion Paper, Symposium on International Equity Market Integration

Voronkova S (2004) Equity market integration in central European emerging markets: A cointegration analysis with shifting regimes. Int Rev Financ Anal 13:633–647 doi:10.1016/j.irfa.2004.02.017

Acknowledgments

An earlier version of this paper was presented at the 1st International Workshop in Economics and Finance, University of Peloponnese, Tripolis, 14–16 May 2007 and thanks are due to conference participants for many helpful comments and discussions. This paper has also benefited from comments by seminar participants at the University of Bern and the University of Crete. Syllignakis acknowledges generous financial support from PENED 2003 under research grant #03ED46 co-financed by E.U.-European Social Fund (75%) and the Greek Ministry of Development-GSRT (25%). Kouretas acknowledges financial support by a Marie Curie Transfer of Knowledge Fellowship of the European Community’s Sixth Framework Programme under contract number MTKD-CT-014288, as well as by the Research Committee of the University of Crete under research grant #2257. We also thank Panayiotis Diamandis, Anastassios Drakos, Dimitris Georgoutsos, George Karathanassis, Dimitris Moschos and Leonidas Zarangas for many helpful comments and discussions and Minoas Koukouritakis for providing us his Matlab code for the common trend eigenvalue problem. We also thank the Editor George Tavlas and an anonymous referee for valuable comments that improved the manuscript substantially. The usual caveat applies.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Syllignakis, M.N., Kouretas, G.P. German, US and Central and Eastern European Stock Market Integration. Open Econ Rev 21, 607–628 (2010). https://doi.org/10.1007/s11079-009-9109-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-009-9109-9

Keywords

- Central and Eastern European stock market integration

- Cointegration

- Common stochastic trends

- Permanent and transitory components