Abstract

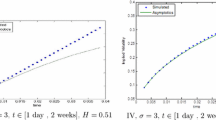

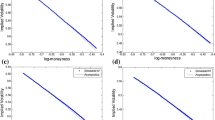

We consider the stochastic volatility model d S t = σ t S t d W t ,d σ t = ω σ t d Z t , with (W t ,Z t ) uncorrelated standard Brownian motions. This is a special case of the Hull-White and the β=1 (log-normal) SABR model, which are widely used in financial practice. We study the properties of this model, discretized in time under several applications of the Euler-Maruyama scheme, and point out that the resulting model has certain properties which are different from those of the continuous time model. We study the asymptotics of the time-discretized model in the n→∞ limit of a very large number of time steps of size τ, at fixed \(\beta =\frac 12\omega ^{2}\tau n^{2}\) and \(\rho ={\sigma _{0}^{2}}\tau \), and derive three results: i) almost sure limits, ii) fluctuation results, and iii) explicit expressions for growth rates (Lyapunov exponents) of the positive integer moments of S t . Under the Euler-Maruyama discretization for (S t ,logσ t ), the Lyapunov exponents have a phase transition, which appears in numerical simulations of the model as a numerical explosion of the asset price moments. We derive criteria for the appearance of these explosions.

Similar content being viewed by others

References

Andersen L, Piterbarg V (2009) Moment explosions in stochastic volatility models. Finance Stochast 11:29–50

Aristoff D, Zhu L (2014) On the phase transition curve in a directed exponential random graph model. arXiv:1404.6514[math.PR]

Bally V, Talay D (1995) The law of the Euler scheme for stochastic differential equations: I. Convergence rate of the distribution function. Probab Theory Relat Fields 104:43–60

Bernard C, Cui Z, McLeish D (2017) On the martingale property in stochastic volatility models based on time-homogeneous diffusions. Math Finance 27:194–223

Chatterjee S, Diaconis P (2013) Estimating and understanding exponential random graph models. Ann Stat 41:2428–2461

Chesney M, Scott L (1989) Pricing European currency options: A comparison of the modified Black-Scholes model and a random variance model. J Financ Quant Anal 24:267–284

Dembo A, Zeitouni O (1998) Large deviations techniques and applications, 2nd Edition. Springer, New York

Ellis R (2005) Entropy, large deviations and statistical mechanics, (Classics in mathematics). Springer, New York

Forde M, Pogudin A (2013) The large-maturity smile for the SABR and CEV-heston models, Int. J. Th Appl. Finance 16(8)

Friz P, Keller-Ressel M (2013) Moment explosions in stochastic volatility models the Encyclopedia of Quantitative Finance, Rama Cont (Ed.) Wiley, New York

Glasserman P, Heidelberger P, Shahabuddin P (1999) Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Math Finance 9(2):117–152

Glasserman P, Kim K-K (2010) Moment explosions and stationary distributions in affine diffusion models. Math Finance 20(1):1–33

Glasserman P (2010) Monte Carlo methods in financial engineering. Springer, New York

Gulisashvili A, Stein EM (2009) Implied volatility in the Hull-White model. Math Finance 19(2):303–327

Guyon J (2006) Euler scheme and tempered distributions. Stoch Process Appl 116(6):877–904

Hagan P, Kumar D, Lesniewski A, Woodward D (2003) Managing smile risk, Wilmott Magazine, 84–108

Hull J, White A (1987) Pricing of options on assets with stochastic volatilities. J Finance 42:281–300

Jäckel P, Kahl C (2008) Hyp Hyp Hooray, Wilmott Magazine, 70–81

Jourdain B (2004) Loss of martingality in asset price models with lognormal stochastic volatility preprint

Jourdain B, Sbai M (2013) High order discretization schemes for stochastic volatility models, J. Comp Finance 17(2)

Kloeden PE, Platen E (1992) Numerical solution of stochastic differential equations. Springer, Berlin

Lewis A (2000) Option valuation under stochastic volatility: with mathematica code. Finance Press, Newport Beach

Lions P-L, Musiela M (2007) Correlations and bounds for stochastic volatility models. Annales de l’Institut Henri Poincaré 24:1–16

Pirjol D (2014) Emergence of heavy-tailed distributions in a random multiplicative model driven by a Gaussian stochastic process. J Stat Phys 154:781–806

Pirjol D, Zhu L (2015) On the growth rate of a linear stochastic recursion with Markovian dependence. J Stat Phys 160:1354–1388

Pirjol D, Zhu L (2017) Asymptotics for the discrete time average of the geometric Brownian motion and Asian options To appear in Advances in Applied Probability

Radin C, Yin M (2013) Phase transitions in exponential random graphs. Ann Appl Probab 23:2458–2471

Scott L (1987) Option pricing when the variance changes randomly: theory, estimation and an application. J Financ Quant Anal 22:419–438

Sin CA (1998) Complications with stochastic volatility models. Adv Appl Probab 30(1):256–268

Talay D, Tubaro L (1990) Expansion of the global error for numerical schemes solving stochastic differential equations. Stoch Anal Appl 8(4):483–509

Varadhan SRS (1984) Large deviations and applications. SIAM, Philadelphia

Wang TH, Laurence P, Wang SL (2010) Generalized uncorrelated SABR models with a high degree of symmetry, Quantitative Finance, 1–17

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Pirjol, D., Zhu, L. Asymptotics for the Euler-Discretized Hull-White Stochastic Volatility Model. Methodol Comput Appl Probab 20, 289–331 (2018). https://doi.org/10.1007/s11009-017-9548-5

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11009-017-9548-5

Keywords

- Linear stochastic recursion

- Lyapunov exponent

- Phase transitions

- Critical exponent

- Large deviations

- Central limit theorems