Abstract

Financial education sans opportunities for hands-on experience and knowledge operationalization may be insufficient for promoting healthy financial behaviors. Financial capability combines financial education with financial inclusion via a savings account, thereby giving an opportunity translate knowledge into practice. This study used data from the 2012 National Financial Capability Study to examine relationships between the financial capability and financial behaviors of United States Millennials (N = 6865). Compared to their financially excluded peers, Millennials who were financially capable were 176 % more likely to afford unexpected expenses, 224 % more likely to save for emergencies, 21 % less likely to use alternative financial services, and 30 % less likely to carry burdensome debt. Interventions that focus solely on financial education or inclusion may be insufficient for facilitating Millennials’ healthy financial behaviors; interventions should instead develop financial capability.

Similar content being viewed by others

Notes

All monetary values throughout this paper are reported in US dollars.

Sometimes economic inclusion is used interchangeably with financial inclusion; however, this paper intentionally uses financial inclusion. Financial inclusion is a narrower term that can pertain to the use or ownership of financial products like savings accounts, checking accounts, and credit cards. Economic inclusion is a broader term that can pertain to the economy or distributions of income and wealth.

The original question in the 2012 NFCS asked the extent to which respondents agreed that they carried too much debt on a scale of 1 (strongly disagree) to 7 (strongly agree). Young adults were deemed to carry too much debt when they reported a 5 or higher on the scale.

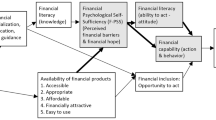

The correlation between financial education and a savings account, while significant at p < .05, was .13. This suggested that there was a weak relationship between financial education and a savings account.

References

Afandi, E., & Habibov, N. (2013). Pre-crisis and post-crisis trust in banks: Lessons from transitional countries. Munich, Germany: Munich Personal RePEc Archive. Retrieved from http://mpra.ub.uni-muenchen.de/46999/1/MPRA_paper_46999.pdf.

Angulo-Ruiz, F., & Pergelova, A. (2015). An empowerment model of youth financial behavior. Journal of Consumer Affairs, Online First. doi:10.1111/joca.12086.

Assets and Education Initiative. (2013). Building expectations, delivering results: Asset-based financial aid and the future of higher education. In W. Elliott (Ed.), Biannual report on the assets and education field. Lawrence, KS: Assets and Education Initiative (AEDI). Retrieved from http://save4ed.com/wp-content/uploads/2013/07/Biannual-Report_Building-Expectations-071013.pdf.

Bell, D., & Blanchflower, D. (2011). Young people and the Great Recession. Oxford Review of Economic Policy, 27(2), 241–267. doi:10.1093/oxrep/grr011.

Bell, L., Burtless, G., Gornick, J., & Smeeding, T. (2007). Failure to launch: Cross-national trends in the transition to economic independence. In S. Danziger & C. Rouse (Eds.), The price of independence: The economics of early adulthood (pp. 27–55). New York: Russell Sage Foundation.

Bernheim, B., D. (2014). Does financial education promote financial competence? Stanford, CA: Stanford University, Stanford Institute for Economic Policy Research. Retrieved from https://www.youtube.com/channel/UCPYXWr4J8t44gCmNYm6ORhw.

Bernheim, B. D., & Garrett, D. M. (2003). The effects of financial education in the workplace: Evidence from a survey of households. Journal of Public Economics, 87(7–8), 1487–1519. doi:10.1016/S0047-2727(01)00184-0.

Bernheim, B. D., Garrett, D. M., & Maki, D. M. (2001). Education and saving: The long-term effects of high school financial curriculum mandates. Journal of Public Economics, 80(3), 435–465. doi:10.1016/S0047-2727(00)00120-1.

Birkenmaier, J., & Fu, Q. (2015). Service usage and financial access: Evidence from the National Financial Capability Study. Journal of Family and Economic Issues, Online First. doi:10.1007/s10834-015-9463-2.

Birkenmaier, J., Sherraden, M. S., & Curley, J. (2013). Financial capability and asset develoment: Research, education, policy, and practice. New York: Oxford University Press.

Carlin, J., Galati, J., & Royston, P. (2008). A new framework for managing and analyzing multiply imputed data in Stata. The Stata Journal, 8(1), 49–67.

Chan, P. (2011). Beyond barriers: Designing attractive savings accounts for lower-income consumers. Washington, DC: New America Foundation. Retrieved from http://assets.newamerica.net/sites/newamerica.net/files/policydocs/chan_beyondbarriers_workingpaper_1.pdf.

Chiteji, N. (2007). To have and to hold: An analysis of young adult debt. In S. Danziger & C. Rouse (Eds.), The price of independence: The economics of early adulthood (pp. 231–258). New York: Russell Sage Foundation.

Cole, S., Paulson, A., Shastry, G.K. (2014). High school curriculum and financial outcomes: The impact of mandated personal finance and mathematics courses. Cambridge, MA: Harvard Business School. Retrieved from http://www.hbs.edu/faculty/Publication%20Files/13-064_c7b52fa0-1242-4420-b9b6-73d32c639826.pdf

Council for Economic Education. (2014). Survey of the states: 2014. Washington, DC: Council for Economic Education. Retrieved from http://www.councilforeconed.org/wp/wp-content/uploads/2014/02/2014-Survey-of-the-States.pdf

Cramer, R. (2010). The big lift: Federal policy efforts to Create Child Development Accounts. Children and Youth Services Review, 32(11), 1538–1543. doi:10.1016/j.childyouth.2010.03.012.

Currie, J., & Moretti, E. (2003). Mother’s education and the intergenerational transmission of human capital: Evidence from college openings. The Quarterly Journal of Economics, 118(4), 1495–1532. doi:10.1162/003355303322552856.

de Basa Scheresberg, C. (2013). Financial literacy and financial behavior among young adults: Evidence and implications. Numeracy: Advanced Education in Quantitative Literacy. doi:10.5038/1936-4660.6.2.5.

Emmons, W., & Noeth, B. (2014). Five simple questions that reveal your financial health and wealth. St. Louis, MO: Federal Reserve Bank of St. Louis. Retrieved from https://www.stlouisfed.org/~/media/Files/PDFs/publications/pub_assets/pdf/itb/2014/In_the_Balance_issue_10.pdf.

Federal Deposit Insurance Corporation. (2012). 2011 FDIC survey of banks’ efforts to serve the unbanked and the underbanked. Washington, DC: FDIC. Retrieved from https://www.fdic.gov/unbankedsurveys/2011survey/2011execsummary.pdf.

Federal Deposit Insurance Corporation. (2014). 2013 FDIC national survey of unbanked and underbanked households. Washington, DC: FDIC. Retrieved from https://www.fdic.gov/householdsurvey/2013report.pdf.

Fernandes, D., Lynch, J, Jr, & Netemeyer, R. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883.

Fox, J., Bartholomae, S., & Lee, J. (2005). Building the case for financial education. Journal of Consumer Affairs, 39, 195–214. doi:10.1111/j.1745-6606.2005.00009.

Friedline, T. (2013). Children as potential future investors: Do mainstream banks augment children’s capacity to save? (Report III of III). Lawrence, KS: Assets & Education Initiative, University of Kansas School of Social Welfare. Retrieved from https://assetsandedu.drupal.ku.edu/sites/assetsandedu.drupal.ku.edu/files/docs/Mainstream_Banks.pdf

Friedline, T., & Elliott, W. (2013). Connections with banking institutions and diverse asset portfolios in young adulthood: Children as potential future investors. Children and Youth Services Review, 35(6), 994–1006. doi:10.1016/j.childyouth.2013.03.008.

Friedline, T., Elliott, W., & Nam, I. (2011). Predicting savings from adolescence to young adulthood: A propensity score approach. Journal of the Society for Social Work and Research, 2(1), 1–22. doi:10.5243/JSSWR.2010.13.

Friedline, T., Johnson, P., & Hughes, R. (2014). Toward healthy balance sheets: Are savings accounts a gateway to young adults’ asset diversification and accumulation? Federal Reserve Bank of St. Louis Review, 96(4), 359–389.

Friedline, T., & Rauktis, M. (2014). Young people are the front lines of financial inclusion: A review of 45 years of research. Journal of Consumer Affairs, 48(3), 535–602. doi:10.1111/joca.12050.

Friedline, T., & Song, H. (2013). Accumulating assets, debts in young adulthood: Children as potential future investors. Children and Youth Services Review, 35(9), 1486–1502. doi:10.1016/j.childyouth.2013.05.013.

Fry, R. (2013). Young adults after the recession: Fewer homes, fewer cars, less debt. Washington, DC: Pew Research Center. Retrieved from http://www.pewsocialtrends.org/files/2013/02/Financial_Milestones_of_Young_Adults_FINAL_2-19.pdf

Garbinsky, E., Klesse, A., & Aaker, J. (2014). Money in the bank: Feeling powerful increases saving. Journal of Consumer Research, 41(3), 610–623. doi:10.1086/676965.

Grinstein-Weiss, M., Sherraden, M., Gale, W., Rohe, W., Schreiner, M., & Key, C. (2013). The ten-year impacts of Individual Development Accounts on homeownership: Evidence from a randomized experiment. American Economic Journal: Economic Policy, 5(1), 122–145. doi:10.1257/pol.5.1.122.

Grinstein-Weiss, M., Spader, J., Yeo, Y. H., Taylor, A., & Freeze, E. B. (2011). Parental transfer of financial knowledge and later credit outcomes among low-and-moderate-income homeowners. Children and Youth Services Review, 33(1), 78–85. doi:10.1016/j.childyouth.2010.08.015.

Gudmunson, C., & Danes, S. (2011). Family financial socialization: Theory and critical review. Journal of Family and Economic Issues, 32, 644–667. doi:10.1007/s10834-011-9275-y.

Guo, S., & Fraser, W. M. (2010). Propensity score analysis: Statistical methods and applications. Thousand Oaks, CA: Sage Publications Inc.

Hall, S., & Willoughby, B. (2015). Relative work and family role centralities: Beliefs and behaviors related to the transition to adulthood. Journal of Family and Economic Issues, Online First. doi:10.1007/s10834-014-9436-x.

Hodson, R., & Dwyer, R. (2014). Financial behavior, debt, and early life transitions: Insights from the National Longitudinal Survey of Youth, 1997 Cohort. Columbus, OH: The Ohio State University, Department of Sociology. Retrieved from http://www.nefe.org/Portals/0/WhatWeProvide/PrimaryResearch/PDF/Financial%20Behavior%20Debt%20and%20Early%20Life%20Transitions-Final%20Report.pdf

Imbens, G. W. (2000). The role of the propensity score in estimating dose–response functions. Biometrika, 87(3), 706–710. doi:10.1093/biomet/87.3.706.

Jamison, J., Karlan, D., & Zinman, J. (2014). Financial education and access to savings accounts: Complements or substitutes? Evidence from Ugandan Youth Clubs (NBER Working Paper No. 20135). Cambridge, MA: National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w20135

John, D. (1999). Consumer socialization of children: A retrospective look at twenty-five years of research. The Journal of Consumer Research, 26(3), 183–213. doi:10.1086/209559.

Kim, J., LaTaillade, J., & Kim, H. (2011). Family processes and adolescents’ financial behaviors. Journal of Family and Economic Issues, 32(4), 668–679. doi:10.1007/s10834-011-9270-3.

Kutner, M., Nachtsheim, C., Neter, J., & Li, W. (2005). Applied linear statistical models (5th ed.). Boston: McGraw-Hill.

Little, R., & Rubin, D. (2002). Statistical analysis with missing data (2nd ed.). New York: Wiley.

Long, J. S. (1997). Regression models for categorical and limited dependent variables. Thousand Oaks: SAGE Publications.

Lusardi, A. (2011). Americans’ financial capability (NBER Working Paper No. 17103). Cambridge, MA: National Bureau of Economic Research. Retrieved from http://www.astrid-online.it/Dossier–d1/United-Sta/FINANCIAL-1/Forum-to-E/Lusardi_Forum_02_10.pdf

Lusardi, A., Michaud, P-C., & Mitchell, O. (2012). Optimal financial knowledge and wealth inequality (NBER Working Paper No. 18669). Cambridge, MA: National Bureau of Economic Research.

Lusardi, A., & Mitchell, O. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 6–44. doi:10.1257/jel.52.1.5.

Lusardi, A., Mitchell, O., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380. doi:10.1111/j.1745-6606.2010.01173.x.

Lusardi, A., Schneider, D., & Tufano, P. (2011). Financially fragile households: Evidence and implications (NBER Working Paper No. 17072). Cambridge, MA: National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w17072

Mandell, L. (2008). Financial literacy in high school. In A. Lusardi (Ed.), Overcoming the saving slump: How to increase the effectiveness of financial education and saving programs (pp. 257–279). Chicago: University of Chicago Press.

Mason, L., Nam, Y., Clancy, M., Kim, Y., & Loke, V. (2010). Child development accounts and saving for children’s future: Do financial incentives matter? Children and Youth Services Review, 32(11), 1570–1576. doi:10.1016/j.childyouth.2010.04.007.

Mian, A., & Sufi, A. (2014). House of debt: How they (and you) caused the Great Recession, and how we can prevent it from happening again. Chicago, IL: University of Chicago Press.

Mills, G., & Monson, W. (2013). The rising use of nonbank credit among US households: 2009–2011. Washington, DC: The Urban Institute. Retrieved from http://www.urban.org/UploadedPDF/412868-the-rising-use-of-nonbank-credit.pdf?RSSFeed=Urban.xml

Mishel, L., Bivens, J., Gould, E., & Shierholz, H. (2012). The state of working America (12th ed.). Ithaca, NY: Cornell University Press.

Nam, Y., Kim, Y., Clancy, M., Zager, R., & Sherraden, M. (2013). Do Child Development Accounts promote account holding, saving, and asset accumulation for children’s future? Evidence from a statewide randomized experiment. Journal of Policy Analysis and Management, 32(1), 6–33. doi:10.1002/pam.21652.

Owens, L., & Cook, K. (2013). The effects of local economic conditions on confidence in key institutions and interpersonal trust after the Great Recession. The Annals of the American Academy of Political and Social Science, 650(1), 274–298. doi:10.1177/0002716213500636.

Royston, P. (2009). Multiple imputation of missing values: Further update of ice, with an emphasis on categorical variables. The Stata Journal, 9(3), 466–477.

Rubin, B. (2014). Employment insecurity and the frayed American dream. Sociology Compass, 8(9), 1083–1099. doi:10.1111/soc4.12200.

Saunders, J., Marrow-Howell, N., Spitznagel, E., Dore, P., Proctor, E. K., & Pescario, R. (2006). Imputing missing data: A comparison of methods for social work researchers. Social Work Research, 30(1), 19–31. doi:10.1093/swr/30.1.19.

Scanlon, E., Buford, A., & Dawn, K. (2009). Matched savings accounts: A study of youths’ perceptions of program and account design. Children and Youth Services Review, 31(6), 680–687. doi:10.1016/j.childyouth.2009.01.003.

Schafer, J. L., & Graham, J. W. (2002). Missing data: Our view of the state of the art. Psychological Methods, 7, 147–177. doi:10.1037//1082-989X.7.2.147.

Schreiner, M., & Sherraden, M. (2007). Can the poor save? Saving and asset building in individual development accounts. New Brunswick: Transaction.

Sherraden, M. (1991). Assets and the poor. Armonk, New York: M.E. Sharpe Inc.

Sherraden, M. S. (2013). Building blocks of financial capability. In J. Birkenmaier, M. S. Sherraden, & J. Curley (Eds.), Financial education and capability: Research, education, policy, and practice (pp. 3–43). New York: Oxford University Press.

Sherraden, M. S., & McBride, A. M. (2010). Striving to save: Creating policies for financial security of low-income families. Ann Arbor, MI: University of Michigan Press.

Shim, S., Barber, B., Card, N. A., Xiao, J., & Serido, J. (2010). Financial socialization of first-year college students: The roles of parents, work, and education. Journal of Youth and Adolescence, 39(12), 1457–1470. doi:10.1007/s10964-009-9432-x.

Taylor, M. (2011). Measuring financial capability and its determinants using survey data. Social Indicators Research, 102(2), 297–314. doi:10.1007/s11205-010-9681-9.

Taylor, P., Doherty, C., Parker, K., & Krishnamurthy, V. (2014). Millennials in adulthood: Detached from institutions, networked with friends. Washington, DC: Pew Research Center. Retrieved from http://www.pewsocialtrends.org/files/2014/03/2014-03-07_generations-report-version-for-web.pdf

Taylor, P., Fry, R., Cohn, D., Livingston, G., Kochhar, R., Motel, S., & Patten, E. (2011). The old prosper relative to the young: The rising age gap in economic well-being. Washington, DC: Pew Research Center. Retrieved from http://www.pewsocialtrends.org/files/2011/11/WealthReportFINAL.pdf

Totenhagen, C., Casper, D., Faber, K., Bosch, L., Wiggs, C., & Borden, L. (2014). Youth financial literacy: A review of key considerations and promising delivery methods. Journal of Family and Economic Issues, 36, 1–25. doi:10.1007/s10834-014-9397-0.

Urban, C., Schmeiser, M., Collins, J. M., & Brown, A. (2015). State financial education mandates: It’s all in the implementation. Washington, DC: FINRA Investor Financial Education Foundation. Retrieved from http://www.finra.org/sites/default/files/investoreducationfoundation.pdf

Wheeler-Brooks, J., & Scanlon, E. (2009). Perceived facilitators and barriers to saving among low-income youth. Journal of Socio-Economics, 38(5), 757–763. doi:10.1016/j.socec.2009.03.015.

Wiedrich, K., Collins, J. M., Rosen, L., & Rademacher, I. (2014). Financial education & account access among elementary students: Findings from the Assessing Financial Capability Outcomes (AFCO) Youth Pilot. Washington, DC: CFED. Retrieved from http://cfed.org/assets/pdfs/AFCO_Youth_Full_Report_Final.pdf

Xiao, J. J., & Anderson, J. G. (1997). Hierarchical financial needs reflected by household financial asset shares. Journal of Family and Economic Issues, 18(4), 333–355. doi:10.1023/A:1024991304216.

Xiao, J. J., Chen, C., & Chen, F. (2014). Consumer financial capability and financial satisfaction. Social Indicators Research, 118(1), 415–432. doi:10.1007/s11205-013-0414-8.

Yeung, W. J., & Conley, D. (2008). Black-white achievement gap and family wealth. Child Development, 79(2), 303–324. doi:10.1111/j.1467-8624.2007.01127.x.

Acknowledgment

This research was supported by a grant from the FINRA Investor Education Foundation. All results, interpretations and conclusions expressed are those of the research team alone, and do not necessarily represent the views of the FINRA Investor Education Foundation or any of its affiliated companies. No portion of this work may be reproduced, cited, or circulated without the express written permission of the authors. The FINRA Investor Education Foundation, established in 2003 by FINRA, supports innovative research and educational projects that give underserved Americans the knowledge, skills and tools necessary for financial success throughout life. For details about grant programs and other FINRA Foundation initiatives, visit www.finrafoundation.org.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Friedline, T., West, S. Financial Education is not Enough: Millennials May Need Financial Capability to Demonstrate Healthier Financial Behaviors. J Fam Econ Iss 37, 649–671 (2016). https://doi.org/10.1007/s10834-015-9475-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10834-015-9475-y