Abstract

Using the vector autoregression (VAR) connectedness approach, this paper investigates dynamic volatility spillovers across 14 sectors in Vietnam’s stock market over the period 2012–2021. The study also explores the differences in sectoral spillovers before and after the outbreak of Covid-19 pandemic. Additionally, the paper also investigates the effects of the current pandemic and macroeconomic fundamentals on intersectoral connectedness in Vietnam. Our findings show that volatility transmission across sectors fluctuates significantly over the research period and spikes during the Covid-19 pandemic. The total spillover index is approximately 64.23 per cent, indicating that volatility spillovers across the Vietnamese sectors are substantial. The risks from the stock market appear to spread quickly and easily across sectors in Vietnam. Among these 14 sectors, food, fisheries, and oil and gas act as net senders of risks while real estate and pharmacy are the greatest receivers of risk. The findings also confirm that the commerce, transportation, manufacturing, and service sectors are more sensitive to the Covid-19 pandemic crisis than other sectors in Vietnam. Furthermore, the empirical results show that an increase in daily Covid-19 infections increases volatility spillover across sectors. Policy implications have emerged based on these findings from this paper for the Vietnamese government and other emerging countries.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In recent years, financial markets have had exceptionally high volatility, especially since the 2008 global financial crisis and the 2020 global stock market crash following the outbreak of Covid-19 (Zhang et al. 2020). This phenomenon has attracted considerable attention from scholars attempting to estimate systemic risk and analyze risk spillover across markets or sectors within financial markets (Zhang et al. 2020). The systemic financial risk has a negative impact on the functioning of the financial system, which erodes public confidence and jeopardizes the stability of the financial system (Billio et al. 2012).

A rapidly increasing number of studies have found that the coronavirus pandemic has had a negative impact on economies and financial markets worldwide. In Vietnam, various economic activities have been halted due to travel restrictions and lockdowns during the four waves of Covid-19 to date. As a result, the Vietnamese economy has been severely affected by the pandemic (Ho et al. 2021). Although Vietnam still achieved positive economic growth of 2.91% in 2020, this rate was at the lowest during the period 2011–2020 (General Statistics Office 2021). In addition, Vietnam’s stock market (VN-Index) experienced substantial price fluctuations over the four waves of Covid-19 (see Fig. 1). Sharp decreases from its peak were seen on the VN-Index, with declines of approximately 33.5% during the first wave (from January to April 2020), 9.7% in the second wave (from July to December 2020) and more than 12% over the third and fourth waves (since January 2021). As illustrated in Fig. 1, significant price volatility has occurred in the sectoral indices throughout the Covid-19 pandemic in Vietnam, specifically during the fourth wave. Most sectors in the Vietnamese financial market have been negatively affected by the pandemic.

Source: Ho Chi Minh Stock Exchange and Cophieu68.vn

Vietnam’s stock market index (VN-Index) and selected sectoral indices, January 2020-September 2021 (January 2, 2020 = 100%).

With respect to interconnectedness within a financial market, Zhang et al. (2020) show that, after a risk shock arises in one sector, the risk appears to affect other sectors due to strong connectedness and spillover mechanisms, and even leading to spillover to the entire national financial market. Therefore, examining the mechanisms in which systemic risk spills across sectors in a financial market is of great significance for both investors and regulators. Indeed, understanding the sectoral volatility spillover mechanism can help market participants to consider their investment strategies in time to mitigate their exposure to systemic risk. Moreover, analyzing the sectoral spillover effects could help policy makers identify the sources of risk transmission and implement appropriate measures to avoid market failure or its negative impacts on the economy (Wu et al. 2019).

Despite the vital necessity of investigating propagation of sectoral volatility, no previous study examines the contagion mechanism across sectors in the financial market in the context of Vietnam. Thus, this study contributes to the literature in the following ways. First, to the best of our knowledge, this is the first paper to investigate the volatility transmission among sectors in Vietnam’s stock market, using the popular approach proposed by Diebold and Yilmaz (2012). This research topic is currently understudied and has not been intensively explored in Vietnam. Second, the study focuses on the period of the Covid-19 pandemic and investigates changes in intersectoral connections and the risk spillover mechanism before and during the pandemic. This analysis helps to identify the leading sectors (or the risk transmitters among sectors) in Vietnam’s stock market before and after the pandemic outbreak. From the perspective of policy makers, discovering the sources of risk is likely to help mitigate systemic risk. At the same time, identifying which sectors are risk transmitters would help investors to determine the proper trading strategy. Third, the effects of the Covid-19 pandemic and macroeconomics fundamentals on the total connectedness among sectors are also investigated. Policy implications are drawn based on these findings for the Vietnamese government to consider and implement appropriate measures to manage volatility transmissions across sectors in the stock market in Vietnam.

Exploring these aspects is even more significant for an emerging country such as Vietnam, especially in light of the country’s recent developments. Since its Doi Moi (economic renovation) in 1986, Vietnam has achieved sustainable and rapid economic growth (Vo and Ho 2021). Because of the economy’s solid foundations, it has remained resilient throughout various crises, including the pandemic. Vietnam is one of the few economies to have achieved a positive growth (2.91%) in its gross domestic product (GDP) in the first year after the outbreak of Covid-19 (2020), and GDP growth in 2022 is expected to rebound to 5.5% (World Bank 2022). In 2021, despite significant declines in most other Asian stock markets, the Vietnamese stock market increased approximately 36% (Reuters 2021). Given that impressive growth, the country was listed among the top seven stock markets, with the strongest increase in the world in 2021 (VnExpress 2022). In Asia, Vietnam’s stock market ranked first in terms of growth, outperforming Taiwan (29%) and India (23%) (Vietnam News 2022). In view of these facts, Vietnam and its stock market plays an increasingly significant role in Asia, so it is worthwhile to examine them.

Following this section, the remainder of this paper is structured as follows. Section 2 discusses and synthesizes the existing relevant literature. Section 3 presents the data sample and methodology. The empirical results are presented and discussed in Sect. 4. Finally, key conclusions and policy implications are discussed in Sect. 5.

2 Literature review

2.1 Theoretical background

Engle et al. (1990) proposed two hypotheses regarding volatility spillovers. The “heat wave” hypothesis suggests that volatility in one market will continue only in that market on the following day and will not propagate to other markets. In contrast, the “meteor shower” hypothesis postulates that volatility in one market tends to transmit to another, so a volatile day in one market will be followed by a volatile day in another market. The “meteor shower” hypothesis might be associated with the failures of market efficiency.

Aside from these hypotheses, two other primary theoretical arguments are related to volatility transmission, including the “decoupling” and “contagion” hypotheses. The “contagion” hypothesis suggests that the benefits of portfolio diversification are limited because of the increasing intensity of volatility transmission across markets during a crisis (Hkiri et al. 2017). Alternatively, the “decoupling” hypothesis posits that performance in emerging economies is independent of changes in the developed economies (Wyrobek et al. 2016). The implication of this hypothesis is that the benefits of portfolio diversification are still attainable (Bekiros 2014; Yarovaya and Lau 2016).

2.2 Empirical review

Investigating and modeling systemic risk and risk spillover have attracted massive attention from scholars worldwide (Wu et al. 2019). The methods used to research volatility spillover include Granger causality (Hong 2001; Hong et al. 2009), the generalized autoregressive conditional heteroskedasticity (GARCH) family models (Bouri et al. 2021; Cheung and Ng 1996; Gabauer 2020; Hamao et al. 1990; Hassan and Malik 2007; Malik 2022), and network topology or generalized variance decomposition under a vector autoregression (VAR) framework (Chen et al. 2022; Choi 2022; Diebold and Yilmaz 2009, 2012, 2014; Gabauer and Gupta 2018; Iwanicz-Drozdowska et al. 2021; Laborda and Olmo 2021; Shen et al. 2022; Su and Liu 2021).

In the extant literature, scholars have extensively focused on the spillover effects between financial markets and international assets (Antonakakis et al. 2017; Fassas and Siriopoulos 2019; Jung and Maderitsch 2014; Shahzad et al. 2018). These studies concentrate on the overall trends in spillover between asset classes or financial markets but do not offer insights into dynamic transmission across different sectors within an economy.

Examining the spillover effects among sectors is important because each sector is uniquely connected within the economy (Chatziantoniou et al. 2021). Recently, scholars have extended their studies to the sectoral spillover effects, using the network analysis approach. Yin et al. (2020) employ the spillover index approach to explore interindustry volatility transmission on the Shanghai Stock Exchange from 2009 to 2018. They note that evolution in the process of transmission among industries corresponds to remarkable political and financial events. Meanwhile, Chatziantoniou et al. (2021) investigate sectoral connectedness in the Indian stock market during the period 2006–2019, using the connectedness approach. They find that sectoral connectedness changes over time and became strongest during the 2008 financial crisis, the 2011 stock market crash, the 2014 national elections, and the 2016 demonetization. Shen et al. (2022) analyze volatility spillover effects among 28 different sector indices in China’s stock markets from 2000 to 2019. They find that the spillover effects became significantly stronger under extreme conditions, including the global financial crisis, the stock market crash in China and the China-US trade war.

Regarding intersectoral volatility spillover during the pandemic, Su and Liu (2021) investigate the transmission structure of financial shock across ten sectors in China from 2004 to 2020 and find that intersectoral connectedness in China’s stock market is strong. Additionally, since the outbreak of Covid-19, risk has tended to spread among sectors rapidly, leading to an increase in intersectoral connectivity. Similarly, Shahzad et al. (2021) analyze asymmetric volatility transmission across ten sectors in the Chinese stock market, employing one-minute data from January 2, 2019, to September 30, 2020. Their findings indicate the asymmetric effect of positive and negative volatility, which is intense and time varying during the pandemic. Chen et al. (2022) investigate sectoral returns and volatility spillovers in Shanghai-Shenzhen-Hong Kong Stock Markets from June 2011 to December 2020. The authors note that the spillover effects primarily occur in the short term and that the Shanghai material, energy and industrial sectors act as the risk transmitters while the Hang Seng public utilities, telecommunications and real estate construction sectors play as risk absorbers.

In the context of the US, Laborda and Olmo (2021) used the method by Diebold and Yilmaz (2012) to analyze volatility spillovers among seven economic sectors from July 2003 to December 2020. They find that energy, banking and insurance, and biotechnology transmit risk to the rest of the US economy; banking and insurance was the largest transmitter of risk during the global financial crisis (2007–2009); but during the pandemic, the largest transmitters of risk have been energy and technology. Meanwhile, Malik (2022) uses the bivariate GARCH model to examine the volatility spillover mechanism between six major equity sectors in the US over the period April 2006–March 2021. The author finds different volatility breaks in all sectors which correspond to the Covid-19 pandemic period. The findings show that there are still volatility spillovers from one sector to the other after adjusting for volatility breaks. More recently, Choi (2022) investigates the volatility spillovers across different industries in the US stock market from January 2018 to May 2021. Findings from the paper indicate that the pandemic did increase the volatility spillovers. The author also notes that there were sudden and substantial changes in the dynamic spillovers due to the shock from energy sector on March 9, 2020, which is known as Black Monday.

To the best of our knowledge, no previous papers have studied intersectoral volatility spillovers in Vietnam, especially during the Covid-19 period. This paper fills this gap by examining volatility transmission among sectors on Vietnam’s stock market over the period January 2012 to September 2021, which also covers the four waves of Covid-19 in Vietnam.

3 Data and methodology

3.1 Data

This paper uses the daily closing price on sectoral indices in Vietnam’s stock market to analyze the sectoral volatility spillover effects.

The study also investigates the effect of the Covid-19 pandemic on intersectoral connectedness in the Vietnamese stock market. Hence, the variables of interest include the daily new Covid-19 infections; the containment and health index, representing the measures enacted by the Vietnamese government to control the pandemic; and the equity market-related economic uncertainty index, which represents the economic policy uncertainty (EPU). In addition to those variables, macroeconomic fundamentals are included in the model, including the exchange rate and the three-month interbank rate.

The data cover the period January 3, 2012, to September 15, 2021, based on data available when this study was conducted. Table 1 presents all variables employed in this study and their data sources.

3.2 Methodology

3.2.1 Sectoral volatility spillover in Vietnam’s stock market

In this study, the time series of sectoral indices are transformed into logarithmic returns as shown in Eq. (1):

where \(P_{t}^{i}\) is the closing price of the sectoral index \(i\) at time \(t\), and \(R_{t}^{i}\) is the return on the sectoral index \(i\) at time \(t\).

Stationarity tests, including the augmented Dickey-Fuller and Phillips-Perron unit-root test, are performed on the return series. The results of these tests show that all 14 returns series in the sample are stationary at level.

Next, the volatility of each sectoral index’s return is estimated using the autoregressive moving average-generalized autoregressive conditional heteroskedasticity (ARMA-GARCH) model. The ARMA process is used to model the conditional mean of the time series, while the GARCH process is employed to model the conditional variance of the time series. The ARMA \(\left( {r,s} \right)\)-GARCH \(\left( {p,q} \right)\) is described in Eqs. (2.1), (2.2) and (3):

The study’s primary objective is to investigate volatility transmission across different sectors in Vietnam's stock market. So, the next step is to adopt the network analysis approach proposed by Diebold and Yilmaz (2012, 2015) to explore the spillover effects. This approach enables a deeper examination of the association structure. Additionally, the transmission structure's direction and node weight can also be identified simultaneously (Diebold and Yilmaz 2014). The rich information and simplicity of the interpretation provided by this method make it a perfect fit for the study’s objectives.

Diebold and Yilmaz (2012, 2015) construct a spillover index based on a forecast error variance decomposition in a VAR model. The method proceeds as follows. First, the VAR model of order p is fitted to the time series of volatility obtained through the ARMA-GARCH process. Second, using the data until time t, the forecast of the volatility series for h periods ahead is estimated, and the error variance decomposition of each forecast is obtained, corresponding to the shocks from the same or other network components at time t. Last, based on the obtained forecast error variance decomposition, the volatility spillover index of each time series and the total spillover index are calculated (see Table 2).

This paper estimates the dynamic volatility spillover effects using a VAR model of order three and the generalized variance decompositions of 12-day-ahead forecast errors with 200-day rolling windows. These parameters are used by Diebold and Yilmaz (2015). The optimal order of three in the VAR model is selected based on the final prediction error (FPE) and Akaike’s information criterion (AIC). Furthermore, robustness checks are performed using various VAR lags (from lag 1 to lag 5), forecast horizons (5, 10, 15 days), and rolling windows of various lengths (250, 500, 750 days).

3.2.2 The impact of the Covid-19 pandemic on the volatility transmission across sectors

Together with the analysis of the sectoral spillover effects for the entire research period from January 2012 to September 2021, the effects of the Covid-19 pandemic and macroeconomic fundamentals on intersectoral spillovers in Vietnam’s stock market are also estimated. The subsample (ranging from January 2019 to September 2021) is used for this empirical analysis. The regression model is presented in Eq. (4):

where \({\text{TSI}}_{t}\) represents the total volatility spillover index at time \(t\). \({\text{Newcase}}_{t}\) is the number of daily Covid-19 infection cases at time \(t\). \({\text{Containment}}_{t}\) is the containment and health index at time \(t\) (representing the government’s policies in response to the Covid-19 pandemic). \({\text{EPU}}_{t}\) is the economic policy uncertainty index at time \(t\).\({\text{ Exchange}}_{t}\) is the change in the exchange rate at time \(t\). \({\text{Interbank}}_{t}\) is the change in the three-month interbank interest rate at time \(t\), and \(\varepsilon_{t}\) is the residual.Footnote 1

4 Empirical results

4.1 The sectoral volatility spillover in Vietnam’s stock market

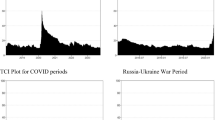

Based on the analyses of Diebold and Yilmaz (20122015), the total volatility spillover index is estimated (see Fig. 2). The total volatility spillover had soared since the first two Covid-19 cases were recorded in Vietnam on January 23, 2020, and it had remained exceptionally high until September 2021, when this analysis was conducted. In general, the volatility spillover among sectors appears to fluctuate over the study period and particularly spike during the Covid-19 pandemic. This finding is similar to Laborda and Olmo (2021) and Su and Liu (2021).

Total volatility spillover in Vietnam’s stock market, January 2012-September 2021 (200-day rolling windows). Notes: The red line marks January 23, 2020, when the first two Covid-19 cases in Vietnam were recorded

The details of volatility spillovers across sectors in the sample are presented in Table 3 and illustrated in Fig. 3. As shown in Table 3, the total spillover index is about 64.23%, indicating that the sectoral volatility spillover within Vietnam’s stock market is relatively strong. As a result, the stock market risks appear to spread across sectors quickly. Theoretically, this result confirms the “meteor shower” hypothesis or the “contagion” hypothesis (mentioned in Sect. 2.1), which suggest that volatility is likely to spread across sectors.

Sectoral volatility net spillover in Vietnam’s stock market, January 2012-September 2021 (200-day rolling windows). Note: The red line marks January 23, 2020, when the first two Covid-19 cases in Vietnam were recorded

Table 3 also shows that, over the research period, three sectors, including food, fisheries, and oil and gas, play a role as transmitters of risk because they had the highest "net" values. These sectors are regarded as sources of risk transmission, implying that when significant volatility emerges in these sectors, volatility spreads to other sectors very quickly. As such, policy makers need to identify and consider the characteristics of these sectors when designing appropriate measures to avoid market failure or mitigate negative impacts on the financial market.

The recipients of the highest risk are real estate and pharmacy, with net values of − 37.46% and − 27.36%, respectively. Because those two sectors receive the most risks from other sectors, they appear to be the market's most vulnerable and fragile sectors. Similarly, Yin et al. (2020) find that these two sectors play a role as risk absorbers in China’s stock market. In addition, the remaining sectors also act as net recipients of risk, in particular including technology, which is also found to be a net receiver by Yin et al. (2020), Chatziantoniou et al. (2021), Laborda and Olmo (2021) and Su and Liu (2021).

Figure 3 illustrates each sector's "net" values from January 2012 to September 2021 with 200-day rolling windows. Food and fisheries almost acted as risk transmitters, especially during the Covid-19 pandemic. Among the risk absorbers, aviation, commerce, energy, pharmacy, real estate, steel, and transportation received the most risks from other sectors during the Covid-19 period, meaning that investing in those sectors might have high risk for investors during the pandemic. Additionally, manufacturing, oil and gas, and technology appeared to be risk absorbers in 2020 whereas they became risk transmitters in 2021. Meanwhile, banking and services turned from risk-transmitting sectors into risk-absorbing sectors in 2021, when the Covid-19 outbreaks became more devastating, with a complete lockdown of Ho Chi Minh City, the largest local economy in Vietnam, for more than five months.

Next, to explore the change in sectoral volatility transmission before and during the current pandemic, spillover effects are estimated for two subsamples: the periods before the pandemic (January 3, 2012, to January 22, 2020) and during the pandemic (January 23, 2020, to September 15, 2021).

The results in Table 4 indicate that volatility transmission is significantly more robust during the Covid-19 period than before the pandemic outbreak. The total spillover index is significantly higher during the pandemic than before it (83.25% compared with 60.28%). Figure 4 illustrates the pairwise spillover of pairs of sectors in the network, indicating clearly that volatility spread across sectors in both periods, before and during the Covid-19 pandemic.

Sectoral volatility spillover comparison between the periods before and during the Covid-19 pandemic. Notes: Blue (yellow) nodes illustrate the net transmitter (receiver) of shocks. Vertices are weighted by the averaged net pairwise directional connectedness measures. The size of nodes represents the weighted average net total directional connectedness

Furthermore, as presented in Table 4 and Fig. 4, after the Covid-19 outbreak, commerce and transportation changed from risk transmitters to risk absorbers. Meanwhile, after the pandemic, manufacturing and services changed from risk recipients to risk senders. These findings imply that those four sectors were more sensitive to the Covid-19 pandemic crisis than other sectors in the stock market. As in the results for the full sample, food and fisheries consistently play a role as the leading risk senders, whereas real estate is consistently the largest risk absorber before and during the pandemic.

4.2 The impact of the Covid-19 pandemic on volatility transmission across sectors

The ordinary least squares (OLS) regression with Newey and West (1987) standard errors is employed to investigate the effects of the pandemic (proxied by new cases of infection with Covid-19, Newcase, and the containment and health index, Containment), economic policy uncertainty (EPU), and macroeconomic fundamentals (proxied by the exchange rate, Exchange, and the interbank rate, Interbank), on sectoral volatility spillover (proxied by the total spillover index, TSI) (see Table 5).

The findings indicate that the daily increase in new infections increase intersectoral connectivity, implying that sectoral volatility spillovers became stronger during the pandemic. As a result, market risk easily spreads across sectors in this period. Meanwhile, mitigating economic policy uncertainty appears to help reduce intersectoral connectedness within Vietnam’s stock market. This shows that the more the government managed to deal with market-related economic uncertainty, the more it could curb the risk transmission across the sectors. Additionally, reducing the interest rate might increase total volatility spillover. The interest rate reduction appears to signal to the market that the economy needs support from the central bank/government. This signal increases volatility spillover across sectors in Vietnam’s stock market.

4.3 Robustness test

The empirical results presented in Sect. 4.1 are based on the VAR model of order three, 12-day-ahead forecast errors, and 200-day rolling windows. In this section, the sensitivity analysis is performed using different VAR lag orders (from lag 1 to lag 5),Footnote 2 forecast horizons (5, 10, 15 days),Footnote 3 and rolling windows (250, 500, 750 days)Footnote 4 to confirm the robustness of the empirical results (see Fig. 5).

The robustness test of the total volatility spillover index of Vietnam’s stock market. Notes: In each figure, the blue band corresponds to the total spillover index using the VAR order from 1 to 5 days. The solid dark blue line represents the total spillover index using the VAR order of three, the lag length employed for analysis in Sect. 4.1

Figure 5 shows that total spillovers tend to become smoother when the window is longer, during which detailed information might be lost. Additionally, when the forecast horizon is longer, the total spillover index appears to be more significant. Similarly, higher VAR orders appear to be associated with stronger spillover effects. However, the variations in VAR lag lengths, forecast horizons, and rolling windows appear to have minor impacts on the total spillover index. The trends in the total spillover index under various conditions remain the same. Therefore, the sensitivity analysis confirms that the total spillover effects are very robust across possible combinations of alternative model specifications.

5 Conclusions and policy implications

This study examines volatility transmission across sectors in Vietnam’s stock market from January 2012 to September 2021 using the network analysis method proposed by Diebold and Yilmaz (2012). They developed a spillover index based on a forecast error variance decomposition of the VAR model. Additionally, the effects of the coronavirus pandemic and macroeconomic fundamentals on intersectoral connectedness in the stock market are also investigated. Each of the findings from this analysis and the respective policy implications are summarized and discussed in turn below.

First, sectoral volatility transmission oscillates throughout the research period and spikes during the Covid-19 pandemic in 2020–2021. The total spillover index is approximately 64.23 per cent, implying that sectoral connectedness is relatively strong. The risks appear to spill over quickly across sectors in Vietnam's stock market. Additionally, the robustness test confirms that the total spillover effects are robust to variations in the VAR order, forecast horizons, and rolling windows.

Second, food, fisheries, and oil and gas are found to play a role as risk transmitters or risk transmission sources over the research period. After a significant shock occurs, these sectors need to be stabilized first to mitigate the spread of the risk, as they are likely to transmit risks rapidly and intensely to other sectors. For food and fisheries sectors, the government should create a trade environment with open, predictable and transparent supplies, ensuring a reliable food network. For oil and gas sector, comprehensive legal reforms are required because Vietnam’s Law on Petroleum, enacted in 1993, show several limitations and the overlapping regulations appear to cause difficulties for gas projects to be implemented smoothly. Meanwhile, real estate and pharmacy are found to act as the greatest risk receivers during the research period. Based on this finding, the government should also pay more attention to these sectors as they appear to absorb the most risks and become the most vulnerable and fragile sectors in the market. The Vietnamese government's supports might include: (i) setting the legal framework to control real estate trading activities, ensuring sustainable development of the property market and avoiding real estate bubble (for real estate sector); and (ii) developing a modern, standardized and professional medicine distribution system (for pharmacy sector). From the investors’ perspective, identifying sectors acting as risk transmitters and risk absorbers could help them design appropriate investment portfolios for risk minimization. More specifically, investors should avoid investment portfolios with highly related sectors or stocks, such as a portfolio including stocks from real estate and pharmacy sectors.

Third, commerce, transportation, manufacturing, and services appear to be more sensitive to the Covid-19 pandemic crisis than other sectors in the stock market. Their roles have changed from risk recipients (risk transmitters) to risk transmitters (recipients) after the pandemic outbreak. Therefore, the Vietnamese government should implement policies to stabilize those sectors when they start experiencing shocks due to crises. These supportive policies should include, but not be limited to, offering low-cost loans and providing tax breaks and exemptions for companies in those sectors.

Fourth, our empirical results show that the increase in new Covid-19 infections tend to raise connectivity among sectors, meaning that the pandemic probably amplifies volatility transmission and that market risks could be transmitted easily across sectors during the pandemic. As such, the Vietnamese government should consider adopting comprehensive Covid-19 control measures proposed by the World Health Organization to halt the spread of the virus. Especially, the government should accelerate vaccination against Covid-19 to reduce the number of new infections, which in turn could help mitigate sectoral volatility transmission within the stock market.

Last, mitigating economic policy uncertainty appears to help reduce sectoral spillovers in the Vietnamese stock market. Policymakers should monitor the EPU index to assess the changes in sectoral spillovers. Then, they can implement timely and focused responses, such as stabilizing the sectors playing as the greatest risk transmitters/receivers and adjusting determinants of sectoral spillovers to reduce the spillovers.

Although the original VAR connectedness approach of Diebold and Yilmaz (2012) is widely employed in existing studies, the standard VAR model can be used only to examine mean connectedness dynamics but not time-varying spillovers in different volatility regimes (i.e., normal versus extreme conditions). This creates a limitation in this study. Therefore, future studies should adopt the quantile VAR (QVAR) model, which enables investigation of time-varying connectedness among different quantiles. This approach could help reveal the differences between high- and low-volatility regimes, which could offer significant insights for both policy makers and portfolio managers.

Notes

All the variables employed in model (4) are stationary. The regression (4) is estimated using the Ordinary Least Square (OLS). Moreover, the p-values should be corrected for Newey and West (1987) standard errors, which are considered to be robust to autocorrelation and heteroskedasticity (Narayan et al. 2021).

The accuracy of the VAR forecasts changes significantly among different lag lengths. The VAR models with relatively short lags appear to produce more accurate forecasts than the models with longer lags (Hafer and Sheehan 1989). As such, a VAR order from 1 to 5 is chosen.

The forecasting horizons (5, 10, 15 days) are used in the sensitivity analysis, as done by Greenwood-Nimmo et al. (2019), who find their estimation results robust to changes in the forecast horizon of 5, 10, and 15 days.

A rolling-window analysis can extract the time-varying characteristics of the spillover effects across different sectors. It appears more accurate to use this method for identifying the crucial sectors in the network (Su and Liu 2021). However, the selection of the window length could be a trade-off between smooth data (with long windows) and noisy data (with short windows) (Ji and Fan 2016). As such, different window lengths, ranging from short to long, are employed in the robustness tests (i.e., 250, 500, 750 days).

References

Antonakakis N, Chatziantoniou I, Filis G (2017) Oil shocks and stock markets: Dynamic connectedness under the prism of recent geopolitical and economic unrest. Int Rev Financ Anal 50:1–26. https://doi.org/10.1016/j.irfa.2017.01.004

Baker SR, Bloom N, Davis SJ (2022) Equity market-related economic uncertainty index. FRED, Federal Reserve Bank of St. Louis; FRED, Federal Reserve Bank of St. Louis. https://fred.stlouisfed.org/series/wlemuindxd

Bekiros SD (2014) Contagion, decoupling and the spillover effects of the US financial crisis: Evidence from the BRIC markets. Int Rev Financ Anal 33:58–69. https://doi.org/10.1016/j.irfa.2013.07.007

Billio M, Getmansky M, Lo AW, Pelizzon L (2012) Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Mark Inst Financ Mark Risks Financ Crisis 104(3):535–559. https://doi.org/10.1016/j.jfineco.2011.12.010

Bouri E, Gabauer D, Gupta R, Tiwari AK (2021) Volatility connectedness of major cryptocurrencies: The role of investor happiness. J Behav Exp Finance 30:100463. https://doi.org/10.1016/j.jbef.2021.100463

Chatziantoniou I, Gabauer D, Marfatia HA (2021) Dynamic connectedness and spillovers across sectors: Evidence from the Indian stock market. Scot J Polit Econ. https://doi.org/10.1111/sjpe.12291

Chen W, Li R, Yao Y (2022) Return and volatility spillovers among sector indexes in Shanghai-Shenzhen-Hong Kong stock markets: Evidence from the time and frequency domains. Emerg Mark Finance Trade. https://doi.org/10.1080/1540496X.2022.2072204

Cheung Y-W, Ng LK (1996) A causality-in-variance test and its application to financial market prices. J Econom 72(1):33–48. https://doi.org/10.1016/0304-4076(94)01714-X

Choi S-Y (2022) Dynamic volatility spillovers between industries in the US stock market: evidence from the Covid-19 pandemic and Black Monday. North Am J Econ Finance 59:101614. https://doi.org/10.1016/j.najef.2021.101614

Diebold FX, Yilmaz K (2009) Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ J 119(534):158–171. https://doi.org/10.1111/j.1468-0297.2008.02208.x

Diebold FX, Yilmaz K (2012) Better to give than to receive: Predictive directional measurement of volatility spillovers. Int J Forecast 28(1):57–66. https://doi.org/10.1016/j.ijforecast.2011.02.006

Diebold FX, Yilmaz K (2014) On the network topology of variance decompositions: Measuring the connectedness of financial firms. J Econom 182(1):119–134. https://doi.org/10.1016/j.jeconom.2014.04.012

Diebold FX, Yilmaz K (2015) Financial and macroeconomic connectedness: a network approach to measurement and monitoring. Oxford University Press, USA

Dong E, Du H, Gardner L (2020) An interactive web-based dashboard to track Covid-19 in real time. Lancet Infect Dis 20(5):533–534. https://doi.org/10.1016/S1473-3099(20)30120-1

Engle RF, Ito T, Lin W-L (1990) Meteor showers or heat waves? Heteroskedastic intra-daily volatility in the foreign exchange market. Econometrica 58(3):525–542. https://doi.org/10.2307/2938189

Fassas AP, Siriopoulos C (2019) Intraday price discovery and volatility spillovers in an emerging market. Int Rev Econ Finance 59:333–346. https://doi.org/10.1016/j.iref.2018.09.008

Gabauer D (2020) Volatility impulse response analysis for DCC-GARCH models: The role of volatility transmission mechanisms. J Forecast 39(5):788–796. https://doi.org/10.1002/for.2648

Gabauer D, Gupta R (2018) On the transmission mechanism of country-specific and international economic uncertainty spillovers: Evidence from a TVP-VAR connectedness decomposition approach. Econ Lett 171:63–71. https://doi.org/10.1016/j.econlet.2018.07.007

General Statistics Office (2021) Viet Nam economy in 2020 the growth of a year with full of bravery. General Statistics Office. https://www.gso.gov.vn/en/data-and-statistics/2021/01/viet-nam-economy-in-2020-the-growth-of-a-year-with-full-of-bravery/

Greenwood-Nimmo M, Huang J, Nguyen VH (2019) Financial sector bailouts, sovereign bailouts, and the transfer of credit risk. J Financ Mark 42:121–142. https://doi.org/10.1016/j.finmar.2018.11.001

Hafer RW, Sheehan RG (1989) The sensitivity of VAR forecasts to alternative lag structures. Int J Forecast 5(3):399–408. https://doi.org/10.1016/0169-2070(89)90043-5

Hale T, Angrist N, Goldszmidt R, Kira B, Petherick A, Phillips T, Webster S, Cameron-Blake E, Hallas L, Majumdar S, Tatlow H (2021) A global panel database of pandemic policies (Oxford Covid-19 Government Response Tracker). Nat Hum Behav 5(4):529–538. https://doi.org/10.1038/s41562-021-01079-8

Hamao Y, Masulis RW, Ng V (1990) Correlations in price changes and volatility across international stock markets. Rev Financ Stud 3(2):281–307. https://doi.org/10.1093/rfs/3.2.281

Hassan SA, Malik F (2007) Multivariate GARCH modeling of sector volatility transmission. Quart Rev Econ Finance 47(3):470–480. https://doi.org/10.1016/j.qref.2006.05.006

Hkiri B, Hammoudeh S, Aloui C, Yarovaya L (2017) Are Islamic indexes a safe haven for investors? An analysis of total, directional and net volatility spillovers between conventional and Islamic indexes and importance of crisis periods. Pacific-Basin Finance J 43:124–150. https://doi.org/10.1016/j.pacfin.2017.03.001

Ho CM, Pham TT, Nguyen HL-P, Vo DH (2021) Does the Covid-19 pandemic matter for market risks across sectors in Vietnam? Heliyon. https://doi.org/10.1016/j.heliyon.2021.e08453

Hong Y (2001) A test for volatility spillover with application to exchange rates. Stud Estim Test 103(1):183–224. https://doi.org/10.1016/S0304-4076(01)00043-4

Hong Y, Liu Y, Wang S (2009) Granger causality in risk and detection of extreme risk spillover between financial markets. Recent Dev Financ Econom 150(2):271–287. https://doi.org/10.1016/j.jeconom.2008.12.013

Iwanicz-Drozdowska M, Rogowicz K, Kurowski Ł, Smaga P (2021) Two decades of contagion effect on stock markets: Which events are more contagious? J Financ Stab 55:100907. https://doi.org/10.1016/j.jfs.2021.100907

Ji Q, Fan Y (2016) Evolution of the world crude oil market integration: A graph theory analysis. Energy Econ 53:90–100. https://doi.org/10.1016/j.eneco.2014.12.003

Jung RC, Maderitsch R (2014) Structural breaks in volatility spillovers between international financial markets: Contagion or mere interdependence? J Bank Finance 47:331–342. https://doi.org/10.1016/j.jbankfin.2013.12.023

Laborda R, Olmo J (2021) Volatility spillover between economic sectors in financial crisis prediction: Evidence spanning the great financial crisis and Covid-19 pandemic. Res Int Bus Finance 57:101402. https://doi.org/10.1016/j.ribaf.2021.101402

Malik F (2022) Volatility spillover among sector equity returns under structural breaks. Rev Quant Finance Account 58(3):1063–1080. https://doi.org/10.1007/s11156-021-01018-8

Narayan PK, Phan DHB, Liu G (2021) Covid-19 lockdowns, stimulus packages, travel bans, and stock returns. Finance Res Lett 38:101732. https://doi.org/10.1016/j.frl.2020.101732

Newey WK, West KD (1987) A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55(3):703–708. https://doi.org/10.2307/1913610

Reuters (2021) Vietnam stocks hit new milestone in record run. Reuters. https://www.reuters.com/markets/stocks/vietnam-stocks-hit-new-milestone-record-run-2021-11-25/

Ritchie H, Mathieu E, Rodés-Guirao L, Appel C, Giattino C, Ortiz-Ospina E, Hasell J, Macdonald B, Beltekian D, Roser, M (2020) Coronavirus pandemic (Covid-19). Our World In Data. https://ourworldindata.org/coronavirus

Shahzad SJH, Mensi W, Hammoudeh S, Rehman MU, Al-Yahyaee KH (2018) Extreme dependence and risk spillovers between oil and Islamic stock markets. Emerg Mark Rev 34:42–63. https://doi.org/10.1016/j.ememar.2017.10.003

Shahzad SJH, Naeem MA, Peng Z, Bouri E (2021) Asymmetric volatility spillover among Chinese sectors during Covid-19. Int Rev Financ Anal 75:101754. https://doi.org/10.1016/j.irfa.2021.101754

Shen Y-Y, Jiang Z-Q, Ma J-C, Wang G-J, Zhou W-X (2022) Sector connectedness in the Chinese stock markets. Empir Econ 62(2):825–852. https://doi.org/10.1007/s00181-021-02036-0

Su X, Liu Z (2021) Sector volatility spillover and economic policy uncertainty: evidence from China’s stock market. Mathematics. https://doi.org/10.3390/math9121411

Vietnam News (2022) Stock market to make robust gains as 2022 arrives. Vietnamnews.Vn. http://vietnamnews.vn/economy/1111584/stock-market-to-make-robust-gains-as-2022-arrives.html

VnExpress (2022) Vietnam stock market 7th biggest gainer globally. VnExpress International – Latest News, Business, Travel and Analysis from Vietnam. https://e.vnexpress.net/news/business/data-speaks/vietnam-stock-market-7th-biggest-gainer-globally-4412066.html

Vo DH, Ho CM (2021) Foreign investment, economic growth, and environmental degradation since the 1986 “Economic Renovation” in Vietnam. Environ Sci Pollut Res 28(23):29795–29805. https://doi.org/10.1007/s11356-021-12838-5

World Bank (2022) The World Bank in Vietnam [Text/HTML]. World Bank. https://www.worldbank.org/en/country/vietnam/overview

Wu F, Zhang D, Zhang Z (2019) Connectedness and risk spillovers in China’s stock market: a sectoral analysis. Econ Syst 43(3):100718. https://doi.org/10.1016/j.ecosys.2019.100718

Wyrobek J, Stańczyk Z, Zachara M (2016) Global financial crisis and the decoupling hypothesis. In: Wilimowska Z, Borzemski L, Grzech A, Świątek J (Eds), Information systems architecture and technology: proceedings of 36th international conference on information systems architecture and technology – ISAT 2015 – Part IV (pp 51–61). Springer International Publishing. https://doi.org/10.1007/978-3-319-28567-2_5

Yarovaya L, Lau MCK (2016) Stock market comovements around the Global Financial Crisis: Evidence from the UK, BRICS and MIST markets. Res Int Bus Finance 37:605–619. https://doi.org/10.1016/j.ribaf.2016.01.023

Yin K, Liu Z, Jin X (2020) Interindustry volatility spillover effects in China’s stock market. Phys A Stat Mech Appl 539:122936. https://doi.org/10.1016/j.physa.2019.122936

Zhang W, Zhuang X, Wang J, Lu Y (2020) Connectedness and systemic risk spillovers analysis of Chinese sectors based on tail risk network. North Am J Econ Finance 54:101248. https://doi.org/10.1016/j.najef.2020.101248

Acknowledgements

The study was supported by The Youth Incubator for Science and Technology Programme, managed by Youth Development Science and Technology Center—Ho Chi Minh Communist Youth Union and Department of Science and Technology of Ho Chi Minh City, the contract number is "30/2021/HĐ-KHCNT-VƯ " signed on 8th, December, 2021.

Author information

Authors and Affiliations

Contributions

All authors contributed to the study conception and design. Material preparation, data collection and analysis were performed by TH-ND, NTN and DHV. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors have no competing interests to declare that are relevant to the content of this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Dang, T.HN., Nguyen, N.T. & Vo, D.H. Sectoral volatility spillovers and their determinants in Vietnam. Econ Change Restruct 56, 681–700 (2023). https://doi.org/10.1007/s10644-022-09446-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10644-022-09446-9