Abstract

Bioenergy is projected to have a prominent, valuable, and maybe essential, role in climate management. However, there is significant variation in projected bioenergy deployment results, as well as concerns about the potential environmental and social implications of supplying biomass. Bioenergy deployment projections are market equilibrium solutions from integrated modeling, yet little is known about the underlying modeling of the supply of biomass as a feedstock for energy use in these modeling frameworks. We undertake a novel diagnostic analysis with ten global models to elucidate, compare, and assess how biomass is supplied within the models used to inform long-run climate management. With experiments that isolate and reveal biomass supply modeling behavior and characteristics (costs, emissions, land use, market effects), we learn about biomass supply tendencies and differences. The insights provide a new level of modeling transparency and understanding of estimated global biomass supplies that informs evaluation of the potential for bioenergy in managing the climate and interpretation of integrated modeling. For each model, we characterize the potential distributions of global biomass supply across regions and feedstock types for increasing levels of quantity supplied, as well as some of the potential societal externalities of supplying biomass. We also evaluate the biomass supply implications of managing these externalities. Finally, we interpret biomass market results from integrated modeling in terms of our new understanding of biomass supply. Overall, we find little consensus between models on where biomass could be cost-effectively produced and the implications. We also reveal model specific biomass supply narratives, with results providing new insights into integrated modeling bioenergy outcomes and differences. The analysis finds that many integrated models are considering and managing emissions and land use externalities of supplying biomass and estimating that environmental and societal trade-offs in the form of land emissions, land conversion, and higher agricultural prices are cost-effective, and to some degree a reality of using biomass, to address climate change.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Bioenergy has been shown to be a potentially valuable, and maybe essential, strategy for long-run climate management (e.g., Bauer et al., this issue; Rose et al 2014; Clarke et al 2014; Creutzig et al 2015; Rogelj et al 2018). Biomass, as an energy feedstock, is unique in its near-term ability to sequester carbon dioxide from the atmosphere and for its versatility as a liquid, solid, or gas to support a variety of societal energy needs as a fuel for electricity, heat, transportation, or hydrogen production. Bioenergy could be particularly valuable to sectors that are more difficult to decarbonize, such as industry and transportation (Bauer et al., this issue). Moreover, when bioenergy is coupled to carbon capture and storage (BECCS), it provides an option for removing carbon dioxide from the atmosphere that could be critical for limiting global average temperature to goals like 2 °C and 1.5 °C (Clarke et al 2014; Gasser et al 2015).

However, to date, there has been notable variation in projections of bioenergy use and its implications (Bauer et al., this issue; Rose et al, 2014; Popp et al, 2014). Furthermore, global bioenergy projections imply potentially substantial annual biomass feedstock production and delivery, with concerns raised about societal and environmental risks (e.g., Hasegawa et al. 2018; Smith et al. 2014; Creutzig et al.2013; Fargione et al. 2010). Yet, the characteristics of potential biomass supplies—feedstocks, locations, and consequences—defining the opportunities, uncertainties, and risks for large-scale global bioenergy deployment are not well understood. For instance, with finite productive land resources that are already providing commercial and non-commercial value to society, land competition and management are issues central to evaluating the role of bioenergy (e.g., Keith 2001; Clarke et al 2014; Smith et al 2014 Bioenergy Appendix; Shukla et al 2019).

Conceptually, the models that evaluate potential global economic, energy, and land transformations consistent with different climate objectives produce integrated bioenergy market equilibrium solutions. In other words, they project potential biomass “quantities supplied” given biomass production characteristics and bioenergy demand, which, among other things, depend on constraints and decarbonization alternatives. Among the constraints in integrated modeling are potential controls for biomass supply externalities, such as pricing land greenhouse gas (GHG) emissions/sequestration, land protection, land preferences, or sustainability considerations (e.g., feedstock constraints). These controls may have consequences for biomass feedstock choice, location of supply, net emissions, and social outcomes.

The global integrated models provide a unique perspective on the potential for bioenergy, evaluating bioenergy through the “eyes” of the climate system. By modeling global dynamics and the very long run, the models can evaluate how the land system and emissions/sequestration might transition, and how, on net, providing biomass for energy performs as a potential climate management strategy over a century.

Underneath integrated solutions are biomass “supply” characterizations that define biomass as a potential energy feedstock and potential climate management solution. Conceptually, these “supply functions” are independent from the demand for bioenergy, representing the biomass quantities and types that could be available at different levels of demand. Coherently thinking about biomass supply requires considering a set of perspectives: the cost of producing biomass for energy, the environmental implications, and the social implications. Different categories of variables are associated with each perspective. The cost, and least-cost allocation, of biomass supply is determined by the relative opportunity costs of producing biomass for energy (across regions and feedstock types), which represents differences in land productivity and input and commodity markets. The environmental implications, such as GHG emissions, from producing biomass are driven by the cost factors, as well as land management and land use changes associated with supplying biomass. And, the social implications (e.g., food prices) are driven by the full set of cost and environmental factors.

This paper undertakes a first of a kind inter-model comparison of global biomass supply modeling within the integrated assessment modeling frameworks that project significant potential bioenergy deployment in global emissions and societal pathways for managing climate change. Using standardized increasing biomass supply and sensitivity scenarios, we characterize the implicit biomass supply within the frameworks, highlighting important elements, and informing understanding of uncertainty and risks. The experimental design reveals comparable biomass supply details relevant to biomass’ appeal for climate management and for society, providing details about the potential cost-effective supply of biomass and the implications of increasing supply.

The inter-model comparison is designed to elucidate and evaluate underlying biomass supply modeling and further understanding of uncertainty and societal risks and trade-offs of supplying biomass for addressing climate change. By elucidating modeling details and differences, we also advance transparency and inform future research.

This paper is a product of Stanford University’s thirty-third Energy Modeling Forum study (EMF-33) “Assessing large-scale global bioenergy deployment for managing climate change” (Rose et al., this issue). The EMF-33 study overall has a goal of understanding, assessing, and improving biomass supply and demand modeling within integrated assessment frameworks. While this paper focuses on the supply of biomass for bioenergy production, a similar EMF-33 inter-model comparison evaluated bioenergy demand (Bauer et al., this issue). In addition, other EMF-33 thematic and individual model papers explore other bioenergy perspectives, including complementary biomass supply perspectives regarding residue feedstocks (Hanssen et al., this issue), food security (Hasegawa et al., this issue), Brazilian biomass and bioenergy (Koberle et al., this issue), and individual model biomass and bioenergy deep dives (Sands, this issue; Bauer et al., this issue). For an overview of the EMF-33 experiments and the full set of papers, see Rose et al. (this issue).

For the multi-model biomass supply analysis in this paper, our experimental design fixes and standardizes the global supply quantity for biomass over time and evaluates how the models meet the requirements. Specifically, we learn about how the models characterize key features that define biomass as a potential climate management strategy. For instance, we reveal what the models perceive as the least expensive biomass—in terms of biomass types and global supply locations. We also learn about how the models “see” the potential societal implications of supplying biomass in terms of economic costs (e.g., changes in food prices, consumption, and household budgets), land use change, and GHG emissions. Furthermore, we explore the effects on biomass supply within each model of trying to manage these implications. Together, these insights help us understand integrated climate management modeling solutions and the uncertainties driving differences.

We begin by describing the experimental design, scenario implementation, and modeling frameworks. We then present results, starting with global biomass feedstock supplies and projected emissions and cost implications, followed by an assessment of the biomass supply implications of managing externalities and an evaluation of implied biomass supply curves. We close out our result discussion with an evaluation of biomass quantities supplied from integrated modeling informed by our biomass supply findings. We conclude with a discussion of additional points and key insights.

1 Experimental design and models

Our scenario protocol is designed to isolate and elucidate biomass supply within the models and facilitate quantitative biomass supply comparisons and discussion about biomass supply feedstocks, land use, GHG implications, and costs. Ten modeling teams participated. All teams ran scenarios driven by exogenously specified global modern biomass primary energy supply requirements (Table 1). Models ran each scenario as a global demand for additional modern biomass that increases from zero today, rising linearly to the 2100 levels shown in Table 1. Imposing a global biomass supply requirement allows us to learn how each model endogenously allocates biomass production across regions without consideration of where the biomass might be consumed. With increasing biomass quantity requirements across scenarios, we identify the least-cost feedstocks and explore changes in the distribution of supply and its implications.

To isolate modern biomass supply and ensure comparable scenario results, there are additional scenario specification requirements. The global quantity supply requirement in each scenario is an increase above each model’s baseline modern biomass levels. “Modern” biomass is defined as cellulosic biomass feedstocks for energy use (“second generation” biomass) native to each model, where “native” refers to biomass feedstocks represented in each model, which varies by model (Table 2). This could include energy crops (woody and herbaceous), logs, and/or residue feedstocks (agriculture, forest, MSW). Food crops that can be used for bioenergy, such as corn, sugarcane, and soybeans (“first generation” biomass) and traditional biomass use are not counted against the annual modern biomass supply requirement. Furthermore, elements of bioenergy demand that might influence land use and land emission results are turned-off in each model, e.g., bioenergy technology specifications and penetration constraints, energy price feedbacks to land use, and trade constraints requiring biomass supply to be produced in the consuming region.

In addition, since we are interested in estimating and evaluating potential economic land conversion and emission implications associated with increasing biomass supply, models are run without exogenous land protection or set-aside constraints that preclude land access to economically accessible lands, such as forests and pasture. Only lands already protected from commercial activity or for environmental purposes are inaccessible in these scenarios.Footnote 1 Given our interest in “pure” biomass supply, we want land to be accessible on an economic bases, which would include lands with rising access costs associated with converting increasing acreage to commercial activity.

Note that, we do not standardize baseline socioeconomic drivers across models. Thus, despite similar global population projections, the models project differences in, among other things, economic growth and agricultural and forestry commodity demands and production that impact the competition for land-use between food, biomass, and natural areas. These differences are part of the uncertainty in results.Footnote 2

We also run sensitivity scenarios to evaluate the biomass supply implications of land protection assumptions and GHG mitigation incentives for land-based activities. For the former, models “turn-on” their default land protection assumptions. For the latter, the models apply a GHG price to the set of land-based mitigation technologies and greenhouse gasses (CO2 and non-CO2) within each model. The price is $20 per metric ton of carbon dioxide equivalent (tCO2eq) starting in 2020 and rising at 3%/year. Land mitigation options differ across the models employed in this study and include activities such as protecting existing terrestrial carbon stocks, afforestation, increasing agricultural soil carbon, and reducing non-CO2 emissions from fertilizers and livestock. See Table 2 for details regarding each model’s land protections and land-based GHG mitigation options.

In general, Table 2 provides an overview of biomass supply-related modeling structure details for the participating models. The models notably vary in important modeling characteristics—biomass feedstocks, land cover types, unmanaged land conversion opportunities, land allocation mechanism, land mitigation activities, and land protection assumptions. For example, the models are very different in how they allocate land, with a few models prioritizing food production (BET, DNE21 + , GRAPE, IMAGE) or using exogenous forest land assumptions (BET, IMAGE, NLU). Supplemental Material (SM) Figure SM1 illustrates the basic differences (and similarities) in just the land cover types modeled and their baseline evolution. Additional modeling details, of course, also factor into results (e.g., food and energy crop yields, land carbon densities, land value, specification of land-based GHG mitigation).Footnote 3

Note that, the scenarios used in this paper are very different from the carbon budget scenarios used in EMF-33 to evaluate bioenergy demand and deployment potential (Rose et al., this issue; Bauer et al., this issue). The analysis here aims to understand how biomass is supplied when integrated models run carbon budget, temperature, or other climate constraint analyses, where bioenergy decarbonization cost-effectiveness and land-related emissions would need to be considered.

2 Results

2.1 Global biomass feedstock supply

We begin with inter-model perspectives on the global supply of biomass, specifically evaluating the distribution of supply. Figure 1 shows the least-cost regional and feedstock supply distributions from each of the models for each of the four global biomass supply scenarios. The color indicates the region of supply, while the color shading and hatching indicate the biomass feedstock type. We immediately observe significant variation between models in the distribution of biomass feedstock production, with the distributions changing over time in all models, but the patterns very different. At lower levels of global feedstock demand (“B100,” 100 EJ/year by 2100), we find residues representing a larger fraction of the supply, while at higher levels of demand (e.g., “B400,” 400 EJ/year by 2100), energy crops and managed forest are more prominent. Thus, when modeled, residues are considered a lower cost feedstock that would dispatch first, but are of more limited supply than energy crop and managed forest feedstocks. All models exhibit greater regional diversification of feedstock production as global supply increases (over time and across scenarios); but, in some models, we observe strong regional preference for supplying biomass. For instance, in DNE21 +, Asia is a more prominent source of biomass than in the other models, while the key supplying regions are the Middle East and Africa for the AIM model, Reforming Economies for FARM, the OECD for GCAM, and Latin America for IMAGE. As for feedstock type, energy crops are a significant share of supply in all the models, while residue supplies are most prominent in BET, GRAPE, and IMAGE, and managed forest biomass supplies are cost competitive in the three models modeling forest feedstocks as an option—BET, GLOBIOM, and NLU.

Cost-effective modern biomass feedstock supply distributions over time by region and feedstock for global supplies increasing to 100, 200, 300, and 400 EJ/year in 2100

All the models, except one (NLU), exhibit increasing net land CO2 emissions globally as the demand for modern biomass increases (Fig. 2). However, for a given supply scenario, there are significant differences in the cumulative CO2 emitted, with BET, IMAGE, and MAgPIE estimating the greatest net land-related CO2 emissions, while DNE21 + , FARM, and NLU estimate the least. The results are indicative of the types of biomass feedstocks modeled, the relative cost-effectiveness of different feedstocks, and the characteristics of the locations supplying the biomass in terms of land productivity, land conversions, and carbon density assumptions. For instance, IMAGE and MAgPIE are primarily supplying energy crops, but converting larger amounts of forest and other natural lands than the other models (see discussion later on the differences in the average characteristics of supply between models). The models also vary in the sensitivity of the CO2 emissions to the level of biomass supply, with some models relatively insensitive (e.g., NLU, FARM), while all the other models project more than a doubling of CO2 emissions from a doubling of biomass supply. These results are representative of the shifts in feedstock type and source location as supply increases, as well as simply the increase in the global amount of biomass being supplied. Consistent with the differences in the distributions of feedstock supply (Fig. 1), we see large variation in regional CO2 emissions for a given biomass supply level, as well as the sensitivity across levels.

Cumulative regional net land CO2 and N2O emission changes from 2010-2100 relative to baseline and global non-energy crop price percentage changes relative to baseline in 2050 and 2100 from increasing modern global biomass supply scenarios. Figure notes: N2O data not reported (“NR”) for BET, DNE21 + , and FARM. Price data not reported for BET and DNE21 + . Prices unchanged in IMAGE due to an assumption that allocates land to food first. GLOBIOM B400 2100 price results not shown—results considered distorted and unreliable at end of horizon for that level of biomass. Price results y-axis truncates NLU B400 2100 value of 114%

For some models, regions, and supply levels, reductions in land CO2 are projected (e.g., GCAM Latin America B100 and B200, GRAPE Reforming Economies B100 to B300, IMAGE Asia B100 and B200, NLU multiple regions for B400). A combination of factors are contributing to this outcome, starting with the biomass feedstocks modeled and relative land use and land intensification opportunities that can result in changes in the competitiveness of a region in global agricultural commodity markets. For instance, a model converting less land in supplying biomass, and therefore resulting in smaller increase in land CO2, may be intensifying agricultural land management. We see evidence of this in the land nitrous oxide (N2O) results for GRAPE and NLU (see below).

Of the models that reported land N2O emission results (n = 7), most exhibit increasing land N2O emissions globally with increasing supply of modern biomass. However, like with land CO2, there are significant differences in the amounts emitted for a given level of biomass supplied, with the land N2O emissions from GRAPE significantly higher than that from the other models, and the GRAPE N2O emissions primarily from Asia and the Middle East and Africa regions. We also find variations in the sensitivity of land N2O emissions and their regional composition to the level of biomass supply. As with CO2, the N2O results are indicative of the feedstock types modeled, cost-effectiveness of feedstocks, and characteristics of the locations supplying the biomass. Note that, two models project decreases in land-based N2O emissions with increasing biomass supply (GCAM and GLOBIOM). These results are indicative of decreases in agricultural land cover acreage and livestock production, which offset agricultural production intensification on remaining croplands.

Underlying the differences in emission results between models are differences in land cover change (Fig. 3). All models exhibit increases in annual land cover conversions over time, and across scenarios, when there are increasing biomass supply requirements, but with notable differences in the specific lands converted. All of the models increase energy crop land cover, with three also increasing managed forest land (BET, GLOBIOM, NLU) and some showing more modest increases in other natural and non-energy cropland. The models vary significantly in terms of what types of land are being converted to support the increasing land cover types, with most models converting some amount of other (unmanaged) forest land, and some also converting pasture, non-energy cropland, and other natural lands (see Table 2 for model specific assumptions on allowed land conversions).

Global land cover changes relative to baseline for the 100 and 300 EJ/year in 2100 biomass supply scenarios (billion hectares per year)

Among other things, the land cover changes inform our understanding of the models with modest land CO2 results in Fig. 2. For FARM, demand for forest products (wood and paper) with a larger and wealthier population is keeping managed forest land cover relatively stable over time despite growing demand for energy and food crops. For NLU, energy crops are only permitted on cropland and pasture, and energy croplands are assumed to have below ground carbon similar to pasture. For DNE21 + , while the model projects land-use change from forest and grassland to energy crops, the carbon stock (and CO2 emission changes) associated with the land conversions is projected to be modest in part because soil carbon changes are not modeled.

Non-energy crop price changes are an indicator of the opportunity cost of supplying biomass, i.e., the marginal cost. We are not able to directly compare biomass prices between models due to differences in model structure that impact how biomass prices are formed. In general, however, we find rising non-energy crop prices across models with increasing biomass supply—an indication of the rising cost of supplying biomass. The price impacts are modest for some models, but significant for others. Also, looking across biomass supply scenarios, we find some models exhibiting much larger increases in the non-energy crop price changes as biomass supply increases (MAgPIE and NLU). In these models, non-energy crop prices are more sensitive to the quantity supplied, indicative of inelastic supply, while those models that are less sensitive can increase the biomass supply with only modest biomass cost implications. We do, however, find one model with negative price changes (GCAM, except in the B400 case in 2100). This is indicative of the model’s modest land use change, and land productivity improvements outpacing biomass supply growth. Later in the paper, we are able to use biomass price experiments to explicitly map out biomass supply curves for some models.

2.2 Model specific biomass supply narratives

Looking across the different characteristics of supplying biomass, we tease out biomass supply narratives for each model. Table 3 presents summary metrics for each model’s B300 biomass supply results. Shown are global weighted average annual per unit energy feedstock, land cover, and emission results, as well as the non-energy crop price change results for 2050 and 2100, all relative to each model’s baseline scenario.

From these results, we can tell high-level biomass supply “stories” about each model’s tendencies and highlight differences between models. For instance, on average, biomass supply from AIM is primarily energy crops, with an increase in cropland acreage and decrease in forest and other natural lands resulting in an increase in land-based GHG emissions, as well as non-energy crop prices. Alternatively, the feedstock supply from GLOBIOM is more diversified, with residues and managed forest feedstocks representing about 50% of supply, with cropland gains similar to AIM, little loss of forest land, and a larger loss of other natural lands. The resulting global CO2 emissions are larger on average for GLOBIOM, while N2O emissions decrease and non-energy crop price changes are similar to AIM’s.

Across models, we see the largest annual average CO2 emissions from MAgPIE, IMAGE, and BET, driven by different average feedstock mixes and land cover changes, while the smallest are from DNE21 + , FARM, and NLU. For N2O, GRAPE produces the largest annual average emissions, while GLOBIOM exhibits an annual average reduction. Finally, for non-energy crop prices, NLU and MAgPIE exhibit the largest annual average increases, while the other models produce modest price increases.Footnote 4

While Table 3 is instructive for model-specific narratives and model comparison, it is difficult to derive generalizations, such as whether models relying solely on energy crops result in more land conversion and emissions. Underlying the different narratives, regarding for instance land CO2 emissions, are differences in assumptions such as soil and vegetation carbon and land productivity data, where there are large known uncertainties (Gasser et al 2020), which combine with each model’s intrinsic uncertainties in the representation of processes and the results produced.

2.3 Managing biomass supply land use and emissions externalities

The results thus far illustrate the potential for negative externalities from supplying biomass, with the potential for land conversion and emissions. Our land protection and mitigation sensitivity scenarios allow us to evaluate the implications of trying to manage these effects. Land constraints or pricing of emissions represent potential additional costs for producing biomass for energy. They also change the relative cost of feedstock types and locations. Costs will increase the most for feedstocks that are associated with greater land use change, especially on unmanaged lands, and/or more land emissions.

First, we find that the land GHG mitigation incentives result in a re-distribution of biomass supply, with changes in supply location and feedstock type. Figure 4 provides results for the 300 EJ/year in 2100 scenarios with land GHG mitigation versus without (i.e., B300C minus B300). A number of models shift supply out of Asia (e.g., DNE21 + , GRAPE, MAgPIE, AIM), and a number of models shift supply to the OECD (e.g., BET, FARM, GCAM, GRAPE, IMAGE). As for feedstock types, we see a few models with notable shifts away from energy crops towards residues (GRAPE, GCAM), but primarily we see shifts in the supplying location of energy crops and managed forest feedstocks. Finally, some models are much more sensitive to the land mitigation incentive (e.g., IMAGE redistributes over 50% of the supply).

Changes in feedstock supply due to a greenhouse mitigation incentive for land activities for the 300 EJ/year supply scenario (EJ per year). Notes: changes relative to B300 scenario

Feedstock supply distributional change results for land protection and combined land protection and GHG mitigation are found in the SM (Figure SM2). We observe that some models have more feedstock substitution with land protection than they do with the GHG mitigation incentive (AIM, DNE21 + , FARM, and NLU), while others show greater feedstock substitution with the GHG mitigation incentive (GCAM, GLOBIOM, GRAPE, and MAgPIE). Recall, of course, that the default land protection assumptions vary by model (Table 2). We find that land protection shifts biomass supply away from Latin America in three of the models (AIM, IMAGE, NLU), but they differ on where the offsetting increases in biomass supply occur. Meanwhile, DNE21 + reallocates biomass away from Middle East and Africa and Asia, while FARM reallocates away from Reforming Economies. Interestingly, with land protections included, there is little movement away from energy crops and forest feedstocks towards residues. Primarily, the location of energy crop supplies is affected. Overall, land protection is resulting in a different feedstock distribution, as some lands are no longer available for use of any kind—biomass for energy, non-energy agriculture, and GHG mitigation. Note that, IMAGE and NLU were not able to meet the B300 annual supply requirements with their default land protection assumptions. Thus, these assumptions put an upper limit of their supply of biomass and deployment of bioenergy.

The effects on emissions and prices are, of course, of particular interest. Globally, we find that all models, except FARM and NLU, exhibit a land CO2 emission reduction, or even net uptake of carbon, relative to their baseline over the century when supplying biomass with the land GHG mitigation incentive (Fig. 5). Figure 5 provides results for the 300 EJ/year in 2100 scenarios with land GHG mitigation (B300C), land protection (B300LP), and both (B300CLP), as well as the pure supply result (B300). With the mitigation incentive, there are some increases in regional cumulative land CO2 emissions, but they are modest compared to the land carbon stock gains elsewhere. All the models exhibit land carbon gains in Asia, Latin America, and the Middle East and Africa, while there is some variation in sign across models for Reforming Economies and the OECD. These results are consistent with the shifts in the feedstock distribution we observe when there is a land GHG mitigation incentive (Fig. 4). For GCAM, GRAPE, and GLOBIOM, the large cumulative land carbon gains are associated with large and rapid afforestation.

Cumulative regional net land CO2 and N2O emission changes from 2010-2100 relative to baseline (top and middle charts) and global non-energy crop price percentage changes relative to baseline in 2050 and 2100 (bottom chart) with the modern biomass supply 300 EJ/yr in 2100 scenario and varying land GHG mitigation and protection assumptions. Notes: N2O data not reported for BET, DNE21 + , and FARM. Price data not reported for BET and DNE21 +

For all but one of the models (AIM), the model-specific land protection assumptions result in lower net land CO2 emissions than without the assumptions (B300LP vs B300), with NLU’s land protections leading to a net increase in land carbon stocks. For AIM, land protection is resulting in greater land conversion of unprotected (and lower productivity) lands and therefore greater net land CO2 emissions. The combination of land GHG mitigation and protection results (B300CLP) are in between the individual sensitivity results for most models. However, which effect dominates varies across models. For two models (GRAPE and IMAGE), mitigation and land protection combine for greater carbon uptake in the terrestrial system.

As for land N2O emissions, increasing biomass supply with land mitigation incentives results in reductions in global land-based N2O emissions in all but NLU. Emission reductions are due to N2O being priced, reduced agricultural land conversions, and the resulting shifts in the distribution of biomass supplies. All the models exhibit land N2O emission reductions in Asia, Latin America, and the Middle East and Africa. These results are consistent with the shifts in the feedstock distribution we observe due to the land GHG mitigation incentive. In general, unlike CO2 emissions, we find that land protection assumptions have little or no effect on global N2O emissions.

Finally, regarding non-energy crop prices, we find land mitigation incentives and land protection assumptions resulting in significantly larger price increases than found with the pure biomass supply scenario (B300). Nearly all the models estimate larger price increases with land mitigation or land protection. Note that price increases are larger in 2100 than 2050 due to the increasing biomass supply over time, as well as the rising GHG price and growing demand for agriculture commodities due to economic and population growth. In general, we find that modeled land protections have a more modest affect on prices than the GHG mitigation incentive; however, together they result in higher prices than either does individually.

2.4 Global and regional estimated biomass supply curves

Five modeling teams have also run biomass supply curve scenarios driven by exogenously specified prices for modern biomass (AIM, FARM, GLOBIOM, IMAGE, MAgPIE). These scenarios reveal the economic supply curves for biomass implicit within each model. With a set of increasing biomass farmgate price experiments of $3, $5, $9, and $15 per gigajoule (US$2005/GJ), we tease out each model’s implied supply curves. We implement each biomass price globally and in all time periods (i.e., identical in all regions and across time). For models not able to impose a farmgate price, a delivered marginal wholesale biomass price is used, where the point of delivery is the theoretical edge of each regional energy system.

From the five models, we find upward sloping global biomass supply curves, with the quantities supplied increasing with the price (Fig. 6). However, we also find differences across models in the location and slope of the curves, with FARM suggesting the greatest supply at any price, and AIM or GLOBIOM the smallest supply. AIM’s supply is the most inelastic (i.e., least responsive to price) and FARM’s the most elastic, with differences in land allocation formulations between models likely contributing to these differences. For instance, FARM allocates land according to relative returns, while other models use other mechanisms such as logit, constant-elasticity-of-transformation formulations, and exogenous prioritization (see Table 2 for details).

Estimated modern biomass feedstock supply curves at farmgate prices globally for 2030, 2050, and 2100 (left), and regionally for 2050 (right). Notes: FARM 2050 ME/Africa, OECD, and Reforming curves rise to 212, 284, and 309 EJ/year respectively at $15/GJ

At a given level of demand (i.e., price), we find biomass supply curves shifting out over time, indicating declining opportunity costs due, in large part, to assumed technological improvements in land sector productivity despite rising food, feed, and wood product demands. The supply curves for FARM and IMAGE shift out the most over time, while AIM and GLOBIOM shift out the least.

Within each model, we find substantial differences in biomass feedstock supplies across regions. While across models, we find large differences in implied supply for a given region, as well as differences in the ordinal ranking of regional supply, with four models estimating the largest potential supplies from Latin America and the smallest from Reforming Economies (AIM, GLOBIOM, IMAGE, MAgPIE), and another model estimating the OECD and Reforming Economies to have the largest supplies (FARM). The differences in estimated global and regional feedstock supplies between models are due to numerous differences in models, including land availability, productivity, feedstock types, and land and commodity markets. Exploring the Fig. 6 regional results further (Table SM2), we find that the models notable differ in energy crop yields (in gigajoules per hectare) and energy crop share of supply, with higher regional yields and shares associated with higher energy crop use (e.g., FARM with higher yields in Latin America versus GLOBIOM, or FARM's yields in the OECD versus AIM as well as the other models). However, yields alone are unable to fully explain regional supply differences between models. Supply differences are also influenced by, among other things, differences in production costs, commodity prices and opportunity costs, and modeling structure (e.g., feedstock options and specifications, land eligibility, and land conversion possibilities).

It is important to keep in mind that these feedstock supply estimates are supply curves, capturing the production and opportunity costs and energy value of feedstocks. The GHG emission implications of producing and using the feedstocks are not priced (or constrained) in these estimates of supply potential, but would be captured in integrated modeling solutions when land emissions can be explicitly or implicitly priced, land mitigation incentivized, and/or feedstock and land constraints activated. To help us think about the implications of these integrated elements on biomass supply, we also run the set of price experiments with the land GHG mitigation incentive. In Figure SM3, we clearly see that incentives for land-based mitigation increase the cost of providing biomass, shifting the biomass supply curves inward. Also, consistent with our earlier observations regarding the supply impact of land mitigation, the sensitivity of biomass supply to the land GHG mitigation incentive varies across models and over time with small (AIM) and large (IMAGE) shifts in supply curves implied.

Overall, the supply curve representation of biomass supply provides another level of understanding, informing interpretation of the earlier feedstock supply distribution results (Fig. 1), as well as integrated modeling use of biomass (next section). Among other things, the supply curves make explicit the least-cost regional ranking within each model and shed light on which models perceive biomass as less or more expensive as a fuel.

2.5 Integrated biomass quantity demanded

The results above elucidate key aspects of supplying biomass, which are necessary for evaluating the long-run opportunities for bioenergy in climate management—potential least-cost feedstock supply, and potential GHG emissions, food price, and land conversion implications of supplying increasing amounts of biomass for energy. As such, they inform our interpretation of integrated modeling results, where the supply and demand for biomass (and associated land and conversion GHG emissions) are modeled simultaneously. In integrated modeling, the biomass demand is a function of the markets for providing economic goods and services, as well as decarbonization, and the resulting biomass quantities represent the quantity demanded in market solutions. We therefore conclude our results section with an evaluation of integrated biomass quantity demanded results in terms of our insights from the biomass supply experiments. Here we take advantage of the EMF-33 “bioenergy demand” experiments (Bauer et al., this issue), which provide projections for potential future energy and land systems for a scenario consistent with global climate goals. These results include projected deployments of bioenergy technologies and the biomass feedstock quantities supplied, as well as deployment projections for non-bioenergy technologies and fuels. In identifying potential bioenergy strategies in the context of global decarbonization for future climate management, the integrated modeling solutions account for all of the biomass supply features we have revealed above, as well as other factors.

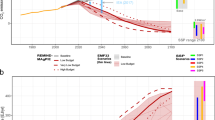

Figure 7 provides the regional and feedstock type market solutions for quantities of biomass demanded over time from the EMF-33 integrated modeling climate management scenario consistent with limiting global average warming to 2 °C. This particular scenario included model default full mitigation technology portfolios, including bioenergy with CCS (BECCS), and endogenous modeling of land-based emissions and carbon pools.Footnote 5 The first thing to note is that the models clearly project that it is cost-effective to use increasing amounts of biomass globally over time. However, annual biomass use and growth vary significantly between models for the same climate future, with 2100 total global biomass use reaching as little as 87 EJ/year (IMACLIM-NLU) and as much as 424 EJ/year (REMIND-MAgPIE). We also find that residues and energy crops dominate the market supply quantities of all the models, and managed forest feedstock use is notably absent from models that include it as an option (BET, FARM, MESSAGE-GLOBIOM, GRAPE, REMIND-MAgPIE), except for a visible amount in FARM early on.Footnote 6 In general, as discussed below, the price on land emissions is high, creating a strong incentive to store carbon in existing and new forests and increasing the cost of supplying forest and other biomass for energy.

Integrated modeling global demands for biomass feedstocks (EJ/year) from a standardized climate management scenario consistent with limiting global average warming to 2 °C. Notes: Results for MESSAGE-GLOBIOM represented differently because managed forest and energy crop use could not be differentiated. MESSAGE uses a generic biomass feedstock supply from GLOBIOM that is a combined supply of managed forest and energy crop feedstocks. Residues were still able to be differentiated and are shown separately as they are for the other models. FARM and REMIND-MAgPIE global biomass use in 2100 reach 431 and 416 EJ/year, respectively

In addition, we find that the regional (and feedstock) distributions differ sharply from the least-cost supply distributions (Fig. 1), which illustrates the role of the other biomass supply factors that are accounted for in integrated modeling, such as the estimated land GHG emissions of supplying biomass, the biomass supply implications of pricing land emissions, and the assumed land protections (Table 2) and their implications for supplying biomass, as well as the market for bioenergy, which depends on energy technology options. Every model, except MESSAGE-GLOBIOM, has a notably different biomass supply distribution across regions compared to Fig. 1 (for similar biomass quantity levels). For instance, we observe a significant shift away from supplying biomass from the ME/Africa in AIM, while FARM shifts away from biomass from Reforming Economies towards supply from the OECD, Asia, and ME/Africa, and IMAGE shifts from a supply dominated by Latin America towards one more balanced across regions.

As noted, the EMF-33 integrated scenarios price land GHG emissions, which we saw above can have a significant impact on feedstock supply as well as land emissions (Figs. 4 and 5). In this case, however, the integrated modeling GHG prices are much higher than the GHG price path we applied in our biomass supply scenarios, ranging from $104 to $1,260/tCO2 in 2050, versus $49/tCO2 in 2050 from our biomass supply land mitigation sensitivity scenario. See Table SM3 for a summary of additional integrated modeling results—global biomass primary energy in 2100, cumulative land CO2 and N2O emissions, 2050 GHG price, and 2050 change in non-energy crop prices. Regarding land emissions, we observe that in most models, the cumulative CO2 and N2O emissions are directionally similar, but the strength of the implications has changed. Some models, however, do exhibit changes in the sign of the affect. For instance, taking into account differences in biomass supply quantities, we find GRAPE and IMAGE producing increases in land CO2 emissions (Table SM3) versus decreases found in their biomass supply only modeling with a carbon price and land protection (Fig. 5), and we see changes in the sign of N2O emission effects for MESSAGE-GLOBIOM and REMIND-MAgPIE.

With many moving parts, integrated results and differences across models are difficult to unpack. However, our detailed biomass supply assessment helps us understand the integrated outcomes. For instance, we found earlier that supplying biomass is relatively more expensive for NLU than the other models in terms of non-energy crop price impacts, which contributes to IMACLIM-NLU’s relatively limited use of biomass in Fig. 7. Similarly, in the integrated scenario, AIM uses relatively little biomass due in part to is inelastic and relatively expensive biomass supply (Fig. 6), while IMAGE uses relatively little biomass due to a combination of factors, including the model allocating land for food production first, which precludes biomass feedstock production competition with food, as well as its large land CO2 emissions associated with supplying biomass and the significant decrease in its biomass supply curve when land emission are priced. Alternatively, with FARM’s biomass supply relatively inexpensive and only modest land CO2 emission implications, FARM uses a large amount of biomass in the integrated scenario. While GCAM and MESSAGE-GLOBIOM use more moderate amounts of biomass in the integrated scenario, they do so with large cumulative net land CO2 uptake due to significant afforestation, which, in GCAM, results in an over 500% increase in 2050 non-energy crop prices.Footnote 7

While the biomass supply insights inform our understanding of integrated modeling results, there are still additional factors in play that cause the integrated outcomes to differ from what the individual model biomass supply results would suggest on their own. For example, the biomass supply characteristics we have elucidated do not give us the full story for REMIND-MAgPIE. REMIND-MAgPIE uses a large amount of biomass in the integrated result, but biomass supply in MAgPIE is associated with relatively high land CO2 emissions and non-energy crop price impacts, with the price impacts even greater with land GHG mitigation incentives and land protection assumptions. In addition to considering the costs and emissions associated with supplying different regional levels and types of biomass, as well as land protection constraints, the integrated modeling endogenously models the demand for biomass, which represents bioenergy technology cost and performance assumptions and feedstock preferences (Daioglou et al., this issue), bioenergy local consumption constraints and trade opportunities, and the cost-effectiveness of bioenergy relative to other decarbonization options across the global economy and over time.

Finally, and importantly, the integrated results highlight that, even when considering land emissions, land conversion, and crop price implications, bioenergy could still be a large and cost-effective long-run climate management strategy. Thus, employing bioenergy as a part of the portfolio for managing the climate system will likely have trade-offs, and those trade-offs could be cost-effective in terms of minimizing the net decarbonization welfare implications for society.

3 Conclusion

This study reveals and evaluates the modeling of modern biomass supply within ten integrated assessment models that are frequently used to identify potential global emission pathways for managing climate. We find that biomass supply within each model is defined by its production costs, as well as various environmental and social implications of supplying biomass for energy. Biomass supply results vary widely between models, beginning with differences in the biomass feedstocks modeled and land conversions allowed, but also includes a myriad of other factors that together define the opportunity cost of producing modern biomass, as well as the emissions, land use, land management, and agricultural market implications, which are relevant to issues like food security, biodiversity, and water quality. We also find that managing the land use and emission externalities of supplying modern biomass affects the least-cost feedstock supply mix as well as the societal cost (prices) for consumers—for biomass and non-energy crops.

We find global biomass supply to be dominated by residue and energy crop feedstocks; however, managed forest feedstocks are only considered by a few models. We also find that adding constraints on land use change and/or prices on land GHG emissions increases the cost of supplying biomass and alters the region-feedstock composition, but a significant supply is still available. Overall, we find little consensus across models on where biomass could be cost-effectively produced, and what the implications might be of doing so. This could imply that there are many options for supplying biomass globally, but it also highlights the need for more detailed assessment of opportunities, as well as the need for experience with larger projects that yield primary data and improve model calibration.

Elucidating and assessing biomass supply gave us new insights into integrated modeling bioenergy results, helping us better understand individual model outcomes, difference between models, and better characterize the uncertainty. However, in the end, other factors beyond biomass supply also contribute to integrated outcomes. Our analysis also revealed that bioenergy deployment in integrated modeling is taking into account emissions and land use externalities of supplying biomass and finding that environmental and societal trade-offs in the form of land emissions, land conversion, and higher agricultural prices are to some degree a reality of using biomass to address climate change. Specifically, we find that increasing the supply of modern biomass to help manage the climate is cost-effective over the long-run and includes some level of externalities and trade-offs, even when they are being managed.

This research was undertaken to increase transparency and understanding of integrated bioenergy results. While we feel we have taken a novel and important step with this study, we have also identified several dimensions for further biomass supply analyses. The lack of consensus on the carbon intensity of primary energy from biomass is an indication of the complexity of land-use processes and markets, as well as uncertainty in land carbon and productivity data and GHG accounting. These are two issues where progress is needed to inform how and if bioenergy will be incorporated into climate policies, and the relative roles of large-scale bioenergy, reforestation, and afforestation. Furthermore, a key issue not considered in our scenarios is policy implementation. We run stylized global biomass supply scenarios for diagnostic purposes. We also consider comprehensive global land GHG pricing and abstract aggregate land protection constraints. Actual policy and markets will develop differently from what is modeled here, with regionally differentiated sector and technology specific policies. Finally, there are fruitful opportunities for more detailed biomass supply assessment—evaluating individual regional feedstocks and eligibility, land productivity and trends, food and feed demands, and potential commodity trade development, as well as a comprehensive analysis that includes additional perspectives of societal importance, such as water resources, biodiversity, food security (e.g., Hasegawa et al., this issue), and natural versus regenerated forests.

Data availability

The dataset generated during the current study is available from the corresponding author on reasonable request.

Notes

Note that we standardize the forests protected today across models to the FAO FRA (2010) “Conservation of biodiversity” forests. http://countrystat.org/home.aspx?c=FOR&ta=T03FO000&tr=2.

Standardizing socioeconomic assumptions across models is far from straightforward and not necessarily desirable. Standardizing the socioeconomic drivers affecting biomass supply requires recalibration of some models and detailed implementation coordination across all models. In addition, while we lose some diagnostic insights by not standardizing, we also gain insights in terms of capturing more of the overall uncertainty relevant to policy.

See Table SM1 for additional detail regarding each model’s alternative non-energy uses for residue feedstocks, land allocation mechanism, and land-based GHG mitigation representation.

GCAM’s weighted average price change is also modest, but slightly negative.

Specifically, the scenario constrains energy and industry CO2 emissions from 2011 to 2100 to 1000 billion tons of CO2, which is consistent with limiting warming to 2 °C. The scenario also prices land and non-CO2 GHG emissions with a GHG price derived from the emission budget constraint. Thus, the modeling does not make an assumption about biomass carbon neutrality, but instead models land-based emissions and sequestration dynamics explicitly. Note that, sensitivity scenarios prohibiting BECCS found similar global bioenergy use levels to be cost-effective for decarbonization, especially as a liquid fuel for transportation (Bauer et al., this issue; Rose et al, 2014).

Only energy crops are available in the FARM biomass supply modeling. In the integrated modeling (shown in Fig. 7), FARM includes energy crops, managed forest, and residue biomass feedstocks. Similarly, as noted earlier (Table 2 notes), REMIND-MAgPIE results in Fig. 7 include residue use, while MAgPIE, on its own, only models dedicated energy crop feedstocks.

The GCAM non-energy crop price increase is driven primarily by the afforestation carbon sequestration incentive, which is particularly strong with high carbon prices (Calvin et al, 2014).

References

Bauer N et al. (this issue). Global energy sector emission reductions and bioenergy use: overview of the bioenergy demand phase of the EMF-33 model comparison. Climatic Change.

Calvin KV, Wise MA, Kyle P, Patel PL, Clarke LE, Edmonds JA (2014) Trade-offs of different land and bioenergy policies on the path to achieving climate targets. Clim Change 123:691–704

Clarke L et al (2014). Assessing transformation pathways. In: Climate change 2014: mitigation of climate change. Contribution of working group III to the fifth assessment report of the Intergovernmental Panel on Climate Change [Edenhofer, O et al (eds)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

Creutzig F et al (2013) Integrating place-specific livelihood and equity outcomes into global assessments of bioenergy deployment. Environ Res Lett 8:035047

Creutzig F et al (2015) Bioenergy and climate change mitigation: an assessment. GCB Bioenergy 7:916–944

Daioglou V et al (this issue). Bioenergy technologies in long-run climate change mitigation: results from the EMF-33 study. Climatic Change.

Fargione JE et al (2010) The ecological impact of biofuels. Annu Rev Ecol Evol Syst 41:351–377

Gasser T et al (2015) Negative emissions physically needed to keep global warming below 2°C. Nature Commun 6(1):1–7

Gasser T et al (2020) Historical CO2 emissions from land-use and land-cover change and their uncertainty. Biogeosciences 17:4075–4101

Hanssen SV et al (this issue) Biomass residues as twenty-first century bioenergy feedstock—a comparison of eight integrated assessment models. Climatic Change.

Hasegawa T et al (2018) Risk of increased food insecurity under stringent global climate change mitigation policy. Nature Clim Change 8:699–703

Hasegawa T et al (this issue). Food security under high bioenergy demand toward long-term climate goals. Climatic Change.

Keith, DW (2001). Sinks, energy crops and land use: coherent climate policy demands an integrated analysis of biomass. Climatic Change 49(1–2).

Köberle A et al (this issue). Can global models provide insights into regional mitigation strategies? A diagnostic model comparison study of bioenergy in Brazil, Climatic Change.

Popp A et al (2014) Land-use transition for bioenergy and climate stabilization: model comparison of drivers, impacts and interactions with other land use based mitigation options. Clim Change 123(3–4):495–509

Rogelj J et al (2018) Scenarios towards limiting global mean temperature increase below 1.5 °C. Nat Clim Chang 8:325–332

Rose SK et al (2014) Bioenergy in energy transformation and climate management. Clim Change 123(3–4):477–493

Rose et al (this issue). An overview of the Energy Modeling Forum 33rd Study: assessing large-scale global bioenergy deployment for managing climate change, Climatic Change.

Sands RD (this issue). Large-scale biomass supply: trade-offs across agricultural futures, in preparation.

Shukla PR et al (eds) (2019). Climate change and land: an IPCC special report on climate change, desertification, land degradation, sustainable land management, food security, and greenhouse gas fluxes in terrestrial ecosystems. In press.

Smith P et al (2014). Agriculture, forestry and other land use (AFOLU). In: Climate change 2014: mitigation of climate change. Contribution of working group III to the fifth assessment report of the Intergovernmental Panel on Climate Change [Edenhofer O et al (eds)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

Acknowledgements

We have benefitted from participant feedback from various conferences, including MIT’s Global Forum and the Integrated Assessment Modeling Consortium, and very constructive comments from three anonymous referees. All errors and misperceptions remain with the authors. The findings and conclusions in this publication are those of the authors and should not be construed to represent those of the author’s institutions or be regarded as an official government determination or policy. Fujimori and Hasegawa were supported by the Environment Research and Technology Development Fund (JPMEERF20211001 and JPMEERF20202002) of the Environmental Restoration and Conservation Agency of Japan, Sumitomo Foundation. Sands participation is supported by the U.S. Department of Agriculture, Economic Research Service. For Muratori, the analysis was performed while at the Pacific Northwest National Laboratory.

Author information

Authors and Affiliations

Contributions

Rose led the development of the scenario design and data reporting, analysis of results, and manuscript writing. Popp, Fujimori, Havlik, Weyant, Wise, and van Vuuren contributed to scenario design, results assessment, and modeling. Brunelle, Cui, Daioglou, Frank, Hasegawa, Humpenöder, Kato, Sands, Sano, Tsutsui, Doelman, Muratori, Prudhomme, Wada, Yamamoto performed model development and runs, data submission and updates.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

This article is part of the Topical Collection on “Assessing Large-scale Global Bioenergy Deployment for Managing Climate Change (EMF-33)” edited by Steven Rose, John Weyant, Nico Bauer, Shinichiro Fuminori, Petr Havlik, Alexander Popp, Detlef van Vuuren, and Marshall Wise

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Rose, S.K., Popp, A., Fujimori, S. et al. Global biomass supply modeling for long-run management of the climate system. Climatic Change 172, 3 (2022). https://doi.org/10.1007/s10584-022-03336-9

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10584-022-03336-9