Abstract

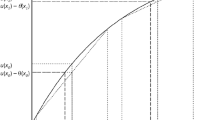

For a utility function \(u\left( x\right) \), the functions \(a\left( x\right) =-u^{\prime\prime}\left( x\right) /u^{\prime}\left( x\right) \) and \(p\left( x\right) =-u^{\prime\prime\prime}\left( x\right) /u^{\prime\prime}\left( x\right) \) are the Arrow-Pratt coefficient of absolute risk aversion (ara) and the coefficient of absolute prudence (ap). They measure respectively an agent’s sensitivity to risk and the strength of the precautionary saving motive under income uncertainty.

Similar content being viewed by others

References

1. Eeckhoudt, L., Kimball, M. (1992): Background risk, prudence and the demand for insurance. In: Dionne, G. (ed.): Contributions to insurance economics. Kluwer, Boston, pp. 239–254

2. Eeckhoudt, L., Schlesinger, H. (1994): A precautonary tale of risk aversion and prudence. In: Munier, B., Machina, M.J. (eds.): Models and experiments in risk and rationality. Kluwer, Dordrecht, pp. 75–90

3. Kimball, M.S. (1990): Precautionary saving in the small and in the large. Econometrica 58, 53–73

4. Kimball, M.S. (1993): Standard risk aversion. Econometrica 61, 589–611

5. Leland, H. (1968): Saving and uncertainty: the precautionary demand for saving. The Quarterly Journal of Economics 82, 465–473

6. McAfee, R.P. (1991): Efficient allocation with continuous quantity. Journal of Economic Theory 53, 51–74

7. Menegatti, M. (2001): On the conditions for precautionary saving. Journal of Economic Theory 98, 189–193

8. Pratt, J.W. (1964): Risk aversion in the small and in the large. Econometrica 32, 122–136

9. Pratt, J.W., Zeckhauser, R.J. (1987): Proper risk aversion. Econometrica 55, 143–154

10. Sandmo, A. (1970): The effect of uncertainty on saving decisions. The Review of Economic Studies 37, 353–360

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Maggi, M.A., Magnani, U. & Menegatti, M. On the relationship between absolute prudence and absolute risk aversion. Decisions Econ Finan 29, 155–160 (2006). https://doi.org/10.1007/s10203-006-0064-2

Received:

Accepted:

Issue Date:

DOI: https://doi.org/10.1007/s10203-006-0064-2