Abstract

This paper presents how the use of a cleaned and robust covariance matrix estimate can improve significantly the overall performance of maximum variety and minimum variance portfolios. We assume that the asset returns are modelled through a multi-factor model where the error term is a multivariate and correlated elliptical symmetric noise extending the classical Gaussian assumptions. The factors are supposed to be unobservable and we focus on a recent method of model order selection, based on the random matrix theory to identify the most informative subspace and then to obtain a cleaned (or de-noised) covariance matrix estimate to be used in the maximum variety and minimum variance portfolio allocation processes. We apply our methodology on real market data and show the improvements it brings if compared with other techniques especially for non-homogeneous asset returns.

Similar content being viewed by others

Notes

A spiked structure denotes a covariance model where some eigenvalues are located out of the “bulk”, like outliers.

A Toeplitz matrix is a diagonal-constant matrix.

Data are available upon request.

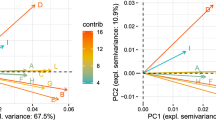

The number of group is \(p=6\) and the quantiles used are \(q_\theta \) and \(q_{1-\theta }\) with \(\theta \in [1\%, 2.5\%, 5\%, 10\%, 15\%, 25\%, 50\%]\).

References

Abramovich Y, Spencer NK (2007) Diagonally loaded normalised sample matrix inversion (LNSMI) for outlier-resistant adaptive filtering. In: IEEE international conference on acoustics, speech and signal processing (ICASSP), vol 3

Bioucas-Dias JM, Plaza A, Dobigeon N, Parente M, Du Q, Gader P, Chanussot J (2012) Hyperspectral unmixing overview: geometrical, statistical, and sparse regression-based approaches. IEEE J Sel Top Appl Earth Obs Remote Sens 5(2):354–379

Bouchaud JP, Potters M (2011) Financial applications of random matrix theory: a short review. The Oxford handbook of random matrix theory. Oxford University Press, Oxford

Bun J, Allez R, Bouchaud JP, Potters M (2016) Rotational invariant estimator for general noisy matrices. IEEE Trans Inf Theory 62(12):7475–7490

Bun J, Bouchaud JP, Potters M (2017) Cleaning large correlation matrices: tools from random matrix theory. Phys Rep 666:1–165

Cambanis S, Huang S, Simons G (1981) On the theory of elliptically contoured distributions. J Multivar Anal 11(3):368–385

Chen Y, Wiesel A, Hero AO (2011) Robust shrinkage estimation of high-dimensional covariance matrices. IEEE Trans Signal Process 59(9):4097–4107

Choueifaty Y, Coignard Y (2008) Toward maximum diversification. J Portf Manag 35(1):40–51

Choueifaty Y, Froidure T, Reynier J (2013) Properties of the most diversified portfolio. J Invest Strateg 2(2):49–70

Clarke R, Silva HD, Thorley S (2012) Minimum variance, maximum diversification, and risk parity: an analytic perspective. J Portf Manag 43(4):15

Couillet R (2015) Robust spiked random matrices and a robust G-MUSIC estimator. J Multivar Anal 140:139–161

Couillet R, Pascal F, Silverstein JW (2014) Robust estimates of covariance matrices in the large dimensional regime. IEEE Trans Inf Theory 60(11):7269–7278

Couillet R, Greco MS, Ovarlez JP, Pascal F (2015) RMT for whitening space correlation and applications to radar detection. In: IEEE CAMSAP, pp 149–152

Darolles S, Duvaut P, Jay E (2013) Multi-factor models and signal processing techniques: application to quantitative finance. Wiley, Hoboken

Darolles S, Gouriéroux C, Jay E (2013) Robust portfolio allocation with risk contribution restrictions. In: Forum GI, Paris

Fama EF, French KR (1993) Common risk factors in the returns on stocks and bonds. J Financ Econ 33(1):3–56

Fama EF, French KR (2015) A five-factor asset pricing model. J Financ Econ 116(1):1–22

Gray RM (2006) Toeplitz and circulant matrices: a review. Found Trends Commun Inf Theory 2(3):155–239

Grinold R, Rudd A, Stefek D (1989) Global factors: fact or fiction? J Portf Manag 16(1):79–88

Hachem W, Loubaton P, Mestre X, Najim J, Vallet P (2013) A subspace estimator for fixed rank perturbations of large random matrices. J Multivar Anal 114:427–447

Jay E, Duvaut P, Darolles S, Chrétien A (2011) Multi-factor models: examining the potential of signal processing techniques. IEEE Signal Process Mag 28(5):37–48

Jay E, Terreaux E, Ovarlez JP, Pascal F (2018) Improving portfolios global performance with robust covariance matrix estimation: application to the maximum variety portfolio. In: 26th European signal processing conference (EUSIPCO)

Kelker D (1970) Distribution theory of spherical distributions and a location-scale parameter generalization. Sankhyā Indian J Stat Ser A 32(4):419–430

Kritchman S, Nadler B (2009) Non-parametric detection of the number of signals: hypothesis testing and random matrix theory. IEEE Trans Signal Process 57(10):3930–3941

Laloux L, Cizeau P, Bouchaud JP, Potters M (1999) Noise dressing of financial correlation matrices. Phys Rev Lett 83:1468

Laloux L, Cizeau P, Potters M, Bouchaud JP (2000) Random matrix theory and financial correlations. Int J Theor Appl Finance 3(03):391–397

Ledoit O, Péché S (2011) Eigenvectors of some large sample covariance matrix ensembles. Probab Theory Relat Fields 151(1):233–264

Ledoit O, Wolf M (2003) Improved estimation of covariance matrix of stock returns with an application to portfolio selection. J Empir Finance 10:603–621

Ledoit O, Wolf M (2004) A well-conditioned estimator for large-dimensional covariance matrices. J Multivar Anal 88:365–411

Maillard S, Roncalli T, Teiletche J (2010) The properties of equally weighted risk contributions portfolios. J Portf Manag 36:60–70

Marčenko VA, Pastur LA (1967) Distribution of eigenvalues for some sets of random matrices. Matematicheskii Sbornik 1(4):457–483

Markowitz HM (1952) Portfolio selection. J Finance 7(1):77–91

Maronna RA (1976) Robust \(M\)-estimators of multivariate location and scatter. Ann Stat 4(1):51–67

Melas D, Suryanarayanan R, Cavaglia S (2009) Efficient replication of factor returns. MSCI Barra research paper no. 2009-23

Ollila E, Tyler DE, Koivunen V, Poor HV (2012) Complex elliptically symmetric distributions: survey, new results and applications. IEEE Trans Signal Process 60(11):5597–5625

Pascal F, Chitour Y, Ovarlez JP, Forster P, Larzabal P (2008) Covariance structure maximum-likelihood estimates in compound Gaussian noise: existence and algorithm analysis. IEEE Trans Signal Process 56(1):34–48

Pascal F, Chitour Y, Quek Y (2014) Generalized robust shrinkage estimator and its application to STAP detection problem. IEEE Trans Signal Process 62(21):5640–5651

Plerou V, Gopikrishnan P, Rosenow B, Amaral LAN, Stanley HE (2001) Collective behavior of stock price movements: a random matrix theory approach. Phys A 299:175–180

Potters M, Bouchaud JP, Laloux L (2005) Financial applications of random matrix theory: old laces and new pieces. Acta Physica Polonica B 36(9):2767–2784

Rosenberg B (1974) Extra-market components of covariance in security markets. J Financ Quant Anal 9(2):263–274

Rousseeuw P, Driessen KV (1999) A fast algorithm for the minimum covariance determinant estimator. Technometrics 41:212–223

Sharpe WF (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. J Finance 19(3):425–442

Terreaux E, Ovarlez JP, Pascal F (2017) New model order selection in large dimension regime for complex elliptically symmetric noise. In: 25th European signal processing conference (EUSIPCO), pp 1090–1094

Terreaux E, Ovarlez JP, Pascal F (2017) Robust model order selection in large dimensional elliptically symmetric noise. arXiv:1710.06735

Terreaux E, Ovarlez JP, Pascal F (2018) A Toeplitz–Tyler estimation of the model order in large dimensional regime. In: IEEE international conference on acoustics, speech and signal processing (ICASSP)

Tyler DE (1987) A distribution-free \({M}\)-estimator of multivariate scatter. Ann Stat 15(1):234–251

Vinogradova J, Couillet R, Hachem W (2013) Statistical inference in large antenna arrays under unknown noise pattern. IEEE Trans Signal Process 61(22):5633–5645

Ward JHJ (1963) Hierarchical grouping to optimize an objective function. J Am Stat Assoc 58:236–244

Yang L, Couillet R, McKay MR (2015) A robust statistics approach to minimum variance portfolio optimization. IEEE Trans Signal Process 63(24):6684–6697

Yang L, Couillet R, McKay MR (2017) Minimum variance portfolio optimization in the spiked covariance model. In: Proceedings of IEEE 7th computational advances in multi-sensor adaptive processing workshop (CAMSAP)

Acknowledgements

We would like to thank Fideas Capital for supporting this research and providing the data. We thank particularly Pierre Filippi and Alexis Merville for their constant interaction with the research team at Fideas Capital. Moreover, this research was conducted within the “Construction of factorial indexes and allocation” under the aegis of the Europlace Institute of Finance, a joint initiative with Fideas Capital.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Communicated by Philippe de Peretti.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Brief description of alternative covariance matrix estimators

Appendix: Brief description of alternative covariance matrix estimators

Here, we briefly introduce some well-known covariance matrix estimators. In the following, \(c = m/N\) and \(\widehat{\mathbf {E}} = \widetilde{\mathbf {R}}\widetilde{\mathbf {R}}^{\mathrm{T}} / N\) is the standardized SCM where \(\widetilde{\mathbf {R}} = (\widetilde{\mathbf {r}}_i)_{i \in [1,m]}\) as defined in Sect. 4.4.

1.1 A.1 Eigenvalue clipping (or RMT-SCM)

Laloux et al. (2000) proposed Eigenvalue clipping in order to separate signal and noise subspaces using Marčenko and Pastur (1967) boundary properties of the eigenvalues. The Eigenvalue clipping estimator of \(\widehat{\mathbf {E}}\) is as follows:

with \(\mathbf {u}_k\) the eigenvector associated to the eigenvalue \(\lambda _k\) of \(\widehat{\mathbf {E}}\), and \(\lambda _k^{clip}\) defined as follows:

where \({\widetilde{\lambda }}\) is chosen such that \(Tr(\widehat{\mathbf {E}}_{clip}) = Tr(\widehat{\mathbf {E}})\).

1.2 A.2 Ledoit and Wolf shrinkage (or LW)

Ledoit and Wolf (2003) introduced some shrinkage estimators particularly adapted to financial asset returns and based on the single factor model of Sharpe (1964), where the factor is a market index. LW is a linear combination of the SCM and the covariance matrix containing the market information. This model can be written as follows:

where \(r_{i,t}\) is the return of stock i at time t , \(\alpha _i\) is the active return of the asset i, \(F_t\) is the market index return at time t, \(\beta _i\) is the asset sensitivity to the market index return, and \(\epsilon _{i,t}\) is the idiosyncratic return for asset i at t. This latter term is assumed to be uncorrelated to the market index. Then the covariance matrix writes:

with \(\varvec{\beta } = [\beta _1, \ldots , \beta _m]^{\mathrm{T}}\), \(\sigma ^2_F\) is the variance of the market returns and \(\varvec{\Omega }_\epsilon \) the covariance matrix of the idiosyncratic error.

An estimator for \(\mathbf {M}_r\) can be determined:

where each \(\hat{\beta _i}\) is estimated individually using the OLS estimator based on Eq. (10) and the \(\widehat{\varvec{\Omega }}_\epsilon \) is a diagonal matrix composed of the OLS residual variances. Finally, \({\hat{\sigma }}^2_F\) is the sample variance of the market returns.

The shrinkage-to-market estimator from Ledoit and Wolf is therefore equal to:

where \(\gamma \in [0, 1]\) is the shrinkage parameter estimated as in Ledoit and Wolf (2003), and \(\mathbf {S}\) is the SCM of asset returns.

1.3 A.3 Rotational invariant estimator (or RIE)

Bun et al. (2016, 2017) proposed an optimal rotational invariant estimator for general covariance matrices by computing the overlap between the true and sample eigenvectors introduced first by Ledoit and Péché (2011). For large m, the optimal rotational invariant estimator (RIE) of \(\widehat{\mathbf {E}}\) is as follows:

with \(\mathbf {u}_k\) the eigenvector associated to the eigenvalue \(\lambda _k\) of \(\widehat{\mathbf {E}}\), and \(\lambda _k^{RIE}\) defined as follows:

where \(z_k = \lambda _k - i \, N^{-1/2}\) is a complex number and s(z) denotes the discrete form of the limiting Stieltjes transform

We also ensure that \(Tr(\widehat{\mathbf {E}}_{RIE}) = Tr(\widehat{\mathbf {E}})\). For this purpose, we multiply each \(\lambda _k\) by \(\nu \) with \(\nu = \sum \nolimits _{k=1}^m \lambda _k / \sum \nolimits _{k=1}^m \lambda _k^{RIE}\).

Rights and permissions

About this article

Cite this article

Jay, E., Soler, T., Terreaux, E. et al. Improving portfolios global performance using a cleaned and robust covariance matrix estimate. Soft Comput 24, 8643–8654 (2020). https://doi.org/10.1007/s00500-020-04840-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00500-020-04840-9