Abstract

In this paper various types of EWMA control charts are introduced for the simultaneous monitoring of the mean and the autocovariances. The target process is assumed to be a stationary process up to fourth-order or an ARMA process with heavy tailed innovations. The case of a Gaussian process is included in our results as well.

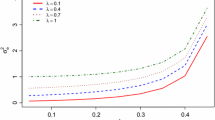

The charts are compared within a simulation study. As a measure of the performance the average run length is taken. The target process is an ARMA (1,1) process with Student-t distributed innovations. The behavior of the charts is analyzed with respect to several out-of-control models. The best design parameters are determined for each chart. Our comparisons show that the multivariate EWMA chart applied to the residuals has the best overall performance.

Similar content being viewed by others

References

Alwan, L. C. (1989). Time Series Modeling for Statistical Process Control. PhD Thesis, Graduate School of Business, Chicago.

Alwan, L. C. and Roberts, H. V. (1988). Time-series modeling for statistical process control. Journal of Business and Economic Statistics 6, 87–95.

Anderson, T. W. (1984). An Introduction to Multivariate Statistical Analysis. Wiley, New York.

Berk, K. N. (1974). Consistent autoregressive spectral estimates. Annals of Statistics 2, 489–502.

Brillinger, D. R. (1981). Time Series: Data Analysis and Theory. Springer, New York.

Brockwell, P. J. and Davis, R. A. (1991). Time Series: Theory and Methods. Springer, New York.

Gan, F. F. (1995). Joint monitoring of process mean and variance using exponentially weighted moving average control charts. Technometrics 37(4), 446–453.

Harris, T. J. and Ross, W. H. (1991). Statistical process control for correlated observations. Canadian Journal of Chemical Engineering 69, 48–57.

Kendall, M. G. and Stuart, A. (1976). The Advanced Theory of Statistics, Vol. 3. Griffin, London.

Kramer, H. G. and Schmid, W. (1997). EWMA charts for multivariate time series. Sequential Analysis 16, 131–154.

Kramer, H. G. and Schmid, W. (1998). On the average delay of control schemes. In: Advances in Stochastic Models for Reliability, Quality and Safety, v. Collani, E., Franz, J., Jensen, U., and Kahle, W. (Eds.), Birkhäuser, Boston, 341–360.

Kramer, H. G. and Schmid, W. (2000). The influence of parameter estimation on the ARL of Shewhart-type charts for time series. Statistical Papers 41, 173–196.

Lowry, C. A., Woodall, W. H., Champ, C. W., and Rigdon, S. E. (1992). A multivariate exponentially weighted moving average control chart. Technometrics 34, 46–53.

Lu, C. W. and Reynolds, M. R., Jr. (1999a). EWMA control charts for monitoring the mean of autocorrelated processes. Journal of Quality Technology 31, 166–188.

Lu, C. W. and Reynolds, M. R., Jr. (1999b). Control charts for monitoring the mean and variance of autocorrelated processes. Journal of Quality Technology 31, 259–274.

Lu, C. W. and Reynolds, M. R., Jr. (2001). CUSUM charts for monitoring an autocorrelated process. Journal of Quality Technology 33, 316–334.

MacGregor, J. F. and Harris, T. J. (1993). The exponentially weighted moving variance. Journal of Quality Technology 25, 106–118.

Montgomery, D. C. and Mastrangelo, C. M. (1991). Some statistical process control methods for autocorrelated data. Journal of Quality Technology 23, 179–204.

Montgomery, D. C. (2001). Introduction to Statistical Quality Control, Wiley, New York.

Pourahmadi, M. (2001). Foundations of Time Series Analysis and Prediction Theory, Wiley, New York.

Roberts, S. W. (1959). Control chart tests based on geometric moving averages, Technometrics 1, 239–250.

Rosenblatt, M. (2000). Gaussian and non-Gaussian Linear Time Series and Random Fields. Springer, New York.

Rosoŀowski, M. and Schmid, W. (2003). EWMA charts for monitoring the autocovariances of stationary Gaussian processes. Sequential Analysis 23, 257–285.

Rosoŀowski (2003). Control Charts for the Mean and the Autocovariances of Financial Time Series, PhD Thesis, Europe-University Viadrina, Frankfurt (Oder), Germany.

Runger, G. C. (2002). Assignable causes and autocorrelation: control charts for observations or residuals? Journal of Quality Technology 34, 165–170.

Schipper, S. and Schmid, W. (2001a). Sequential methods for detecting changes in the variance of economic time series. Sequential Analysis 20, 235–262.

Schipper, S. and Schmid, W. (2001b). Control charts for GARCH processes. Nonlinear Analysis: Theory, Methods and Applications 47, 2049–2060.

Schmid, W. (1995). On the run length of a Shewhart chart for correlated data. Statistical Papers 36, 111–130.

Schmid, W. (1997a). On EWMA charts for time series. In: Frontiers of Statistical Quality Control, Vol. 5. Lenz, H.-J. and Wilrich, P.-Th. (Eds.), Physica-Verlag, Heidelberg, 115–137.

Schmid, W. (1997b). CUSUM control schemes for Gaussian processes. Statistical Papers 38, 191–217.

Severin, T. and Schmid, W. (1999). Monitoring changes in GARCH models. Allgemeines Statistisches Archiv 83, 281–307.

Vasilopoulos, A. V. and Stamboulis, A. P. (1978). Modification of control chart limits in the presence of data correlation. Journal of Quality Technology 10, 20–30.

Yashchin, E. (1993). Performance of CUSUM control schemes for serially correlated observations. Technometrics 35, 37–52.

Wardell, D. G., Moskowitz, H., and Plante, R. D. (1994). Runlength distributions of special-cause control charts for correlated processes. Journal of Quality Technology 26, 308–317.

Willis, J. L. (2003). Implications of structural changes in the U.S. economy for pricing behavior and inflation dynamics. Economic Review First Quarter 2003. Research Publication of the Federal Reserve Bank of Kansas City available at http://www.kc.frb.org [30 July 2003].

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Rosołowski, M., Schmid, W. EWNA charts for monitoring the mean and the autocovariances of stationary processes. Statistical Papers 47, 595–630 (2006). https://doi.org/10.1007/s00362-006-0308-9

Received:

Revised:

Issue Date:

DOI: https://doi.org/10.1007/s00362-006-0308-9