Abstract

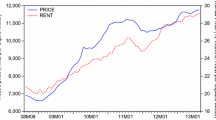

Between June 1998 and March 2006, the price index of apartment houses in Seoul, Korea, more than doubled, while fundamentals such as GDP, wage, and population increased by less than 35%. This study examines the role of a rational speculative bubble in this price surge. We find that unobservable information explains part of the price volatility; and that a rational bubble proxy is a significant driver of prices. However, neither latent information nor rational bubble is enough to explain the recent housing price appreciation, even in conjunction with observable fundamentals.

Similar content being viewed by others

References

Abraham JM, Hendershott PH (1996) Bubbles in metropolitan housing markets. J Hous Res 7: 191–207

Bjorklund K, Soderberg B (1999) Property cycles, speculative bubbles and the gross income multiplier. J Real Estate Res 18: 151–174

Blanchard OJ, Watson MW (1982) Bubbles, rational expectations and financial markets. NBER working paper no. 945

Bourassa SC, Hendershott PH, Murphy J (2001) Further evidence on the existence of housing market bubbles. J Prop Res 18: 1–19

Brooks C, Katsaris A, McGough T, Tsolacos S (2001) Testing for bubbles in indirect property price. Cycles 18: 341–356

Caginalp G, Porter D, Smith V (2000) Overreactions, momentum, liquidity, and price bubbles in laboratory and field asset markets. J Psychol Financial Mark 1: 24–48

Campbell JY (1990) Measuring the persistence of expected returns. Am Econ Rev Proc 80: 43–47

Campbell JY, Shiller RJ (1987) Cointegration and tests of present value models. J Political Econ 95(5): 1062–1088

Campbell JY, Shiller RJ (1988a) Stock prices, earnings, and expected dividend. J Finance 43(3):661–676. Papers and Proceedings of the Forty-seventy Annual Meeting of the American Finance Association, Chicago, Illinois

Campbell JY, Shiller RJ (1988b) The dividend-price ratio and expectations of future dividends and discount factors. Rev Financial Stud 1(3): 195–228

Chan HL, Lee SK, Woo KY (2001) Detecting rational bubbles in the residential housing markets in Hong Kong. Econ Model 18: 61–73

Chung HS, Kim JH (2004) Housing speculation and housing price bubble in Korea KDI School of Pub Policy & Management Paper No. 04–06. SSRN: http://ssrn.com/abstract=535882

Diba BT, Grossman HI (1988) Explosive rational bubbles in stock prices. Am Econ Rev 78(3): 520–530

Evans GW (1991) Pitfalls in testing for explosive bubbles in asset prices. Am Econ Rev 81(4): 922–930

Flavin M, Nakagawa S (2008) A model of housing in the presence of adjustment costs: a structural interpretation of habit persistence. Am Econ Rev 98(1): 474–495

Greene WH (1997) Econometric analysis, 3rd edn. Prentice-Hall, Englewood Cliffs

Guirguis H, Giannikos C, Anderson R (2005) The US housing market: asset pricing forecasts using time varying coefficients. J Real Estate Finace Econ 30(1): 33–53

Hamilton JD (1994) Time series analysis. Princeton University Press, Princeton

Harvey AC (1989) Forecasting, structural time series models and the Kalman filter. Cambridge University Press, Cambridge

Himmelberg C, Mayer C, Sinai T (2005) Assessing high house prices: bubbles, fundamentals and misperceptions. J Econ Perspectives 19(4): 67–92

Hwang M, Quigley J, Son J (2006) The dividend pricing model: new evidence from the Korean housing market. J Real Estate Finace Econ 32(3): 205–228

Ito T, Iwaisako T (1995) Explaining asset bubbles in Japan. BOJ Monet Econ Stud 14: 143–193

Kim K-H (2004a) Housing and the Korean economy. J Housing Econ 13: 321–341

Kim N-H (2004b) An introduction of the 2000 & 2005 population and housing census in Korea, in Population Census Div. Korea National Statistical Office

Kim K-H, Kim C-H (2002) What drives Korean land use regulations? Paper presented at the presidential address at the AsRES-AREUEA Joint International Conference, Seoul

Kim K-H, Lee HS (2000) Real estate price bubble and price forecasts in Korea. Paper presented at the 5th AsRES Conference, Beijing

Kim K-H, Suh S-H (1993) Speculation and price bubbles in the Korean and Japanese real estate markets. J Real Estate Finance Econ 6: 73–87

Kim K-H, Suh S-H (2002) Urban economics: theory and policy, 3rd edn. Hong-Moon Sa, Seoul

Kim J-C, Kim D-H, Kim J-J, Ye J-S, Lee H-S (2000) Segmenting the Korean housing market using multiple discriminant analysis. Constr Manag Econ 18: 45–54

Kim K-H (1993) Housing prices, affordability and government policy in Korea. J Real Estate Finance Econ 6(1): 55–72

Koenker R, Bassett G (1982) Robust tests for heteroscedasticity based on regression quantiles. Econometrica 50: 43–61

Lee JS (1997) An Ordo-liberal perspective on land problems in Korea. Urban Stud 34(7): 1071–1084

Lei V, Noussair CN, Plott CR (2001) Nonspeculative bubbles in experimental asset Markets: lack of common knowledge of rationality vs. actual irrationality. Econometrica 69(4): 831–859

Levin EJ, Wright RE (1997) Speculation in the housing market?. Urban Stud 34(9): 1419–1437

Lim HY (2003) Asset price movements and monetary policy in South Korea, in Monetary policy in a changing environment, BIS Papers No. 19. http://www.bis.org/publ/bppdf/bispap19.htm

Malppezzi S, Wachter SM (2005) The role of speculation in real estate cycles. J Real Estate Lit 13: 143–166

Mankiw NG, Romer D, Shapiro MD (1985) An unbiased reexamination of stock market volatility. J Finance 40: 677–689

Piazzesi M, Schneider M, Tuzel S (2007) Housing, consumption and asset pricing. J Financial Econ 83(3): 531–569

Renaud B (1993) Confronting a distorted housing market: can Korean polices break with the past? . In: Krause L, Park F-K (eds) Social issues in Korea: Korean and American perspectives. KDI Press, Seoul, pp 291–331

(2001) The rise in house prices in Dublin: bubble, fad or just fundamentals. Econ Model 18: 281–295

Shiller RJ (1990) Market volatility and investor behavior. Am Econ Rev Proc 80(2): 58–62

Weeken O (2004) Asset pricing and the housing market. Bank of England Quarterly Bulletin, Spring 2004

Xiao Q (2005) Property market bubbles: some evidence from Seoul and Hong Kong, Ch. IV. PhD Thesis, Division of Economics. Nanyang Technological University, Singapore

Xiao Q (2007) What drives Hong Kong’s residential property market—A Markov switching present value model. Physica A 383: 108–114

Xiao Q (2008) Determination of price and rental: theory and tests using City office data. Paper presented at the 15th Annual European Real Estate Society Conference, Krakow, Poland

Xiao Q, Liu Y (2007) The residential market of Hong Kong: rational or irrational? Appl Econ 99999:1

Yao R, Zhang H (2005) Optimal consumption and portfolio choices with risky housing and borrowing constraints. Rev Financial Stud 18(1): 197–239

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Xiao, Q., Park, D. Seoul housing prices and the role of speculation. Empir Econ 38, 619–644 (2010). https://doi.org/10.1007/s00181-009-0282-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-009-0282-x