Abstract

The notion of Internal Financial Law for an investment is introduced. Through this generalization of the IRR a general notion of outstanding capital is obtained. After the introduction of a generalized version of NPV a decomposition of this parameter is offered which is strictly connected to the notion of ROE.

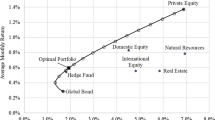

Some applications to yield averaging for portfolios is provided.

Similar content being viewed by others

References

M. Bromwich (1970),Capital budgeting — a survey, Journal of Business Finance, 2, n. 3, pp. 3–26.

A. Cerquetti (1988),Tassi medi di rendimento di obbligazioni singole e in portafoglio, Pubblicazioni dell'Istituto di Matematica, Un. “G. D'Annunzio”, Pescara.

G. Diale (1989),On multiple IFL, to appear.

E. Levi (1964),Corso di Matematica Finanziaria e Attuariale, Giuffrè, Milano.

H. Levy, M. Sarnat (1978),Capital Investment and Financial Decisions, Prentice Hall International, Englewood Cliffs.

M. Lonzi (1986)Aspetti Matematici nella Ricerca di Condizioni di Unicità per il Tasso interno di Rendimento, Rivista di Matematica per le Scienze Economiche e Sociali.

M. Lonzi (1988),Valore Attuale e Montante nei progetti puri, Presented to Rivista di Matematica per le Scienze Economiche e Sociali.

E. Luciano (1989),A new Perspective on Dynamic Portfolio Policies in this issue.

E. Luciano, L. Peccati (1990),The decomposition of random discounted cash-flows, to be presented at the Fifth International Conference on the Foundations of Utility, Risk and Decision Theory (FUR V), Duke University, Durham, USA.

P. Manca (1990),The splitting up of a Financial Project into uniperiodic Consecutive projects, in this issue.

J.C.T. Mao (1970)Survey of Capital Budgeting: Theory and Practice, Journal of Finance, May, pp. 349–360.

C.J. Norstrom (1972)A Sufficient Condition for a Unique Nonnegative Internal Rate of Return, Journal of Financial and Quantitative Analysis, vol. 7, June, pp. 1835–1838.

L. Peccati (1987),DCF e risultati di periodo, Atti dell'XI Convegno AMASES, Torino-Aosta (to appear).

L. Peccati (1989a),Di tassi e di tasse, presented at the “Convegno sulla Matematica Applicata all'Economia e all'Ingegneria”, Un. “G. D'Annunzio”, Pescara, 26–28 Jan.

L. Peccati (1989b),Un metodo di valutazione di un investimento in un portafoglio assicurativo, presented at the “Giornata di Studio sul tema: Analisi e Gestione del Rischio Finanziario”, Istituto Italiano degli Attuari, Roma.

C.S. Soper (1959),The Marginal Efficiency of Capital: A Further Note. In The Economic Journal, vol. 69, March, pp. 174–177.

F. Weston, E. Brigham (1978),Managerial Finance, 6 ed., Hinsdale, Holt-Saunders International Editions, Dryden Press.

F.M. Wilkes (1983),Capital Budgeting Techniques, 2nd ed., New York, J. Wiley & Sons.

M. Uberti (1990),The decomposition of the present value of foreign currency bonds, to appear.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Peccati, L. Multiperiod analysis of a levered portfolio. Rivista di Matematica per le Scienze Economiche e Sociali 12, 157–166 (1989). https://doi.org/10.1007/BF02085598

Issue Date:

DOI: https://doi.org/10.1007/BF02085598