Abstract

In the context of designing modern, competitive production processes, companies face the challenge of integrating the growing ecological demands of customers and other stakeholders as well as resource scarcity on one hand and the dominant need for economic success on the other hand. An approach to meet ecological and economical goals is the improvement of the material and energy productivity. This is strongly supported by the method of material flow cost accounting (MFCA). It aims at the identification of processes’ material and energy related inefficiencies and the (monetary) quantification of their effects on the overall process chain. This chapter firstly introduces the basic methodology of MFCA. Afterwards, refinements and enhancements concerning the modeling of loops and stocks, the integration of energy and the design of a prospective MFCA are proposed. Concluding, aspects of MFCA’s practical implementation are discussed.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

The German industry spent 45 % on average for input materials in 2009 (Statistisches Bundesamt 2011).

- 2.

The definition of the specific processes may vary with the relevance of the respective ‘area’. So, a single production process can be limited to one very resource intensive production step or include a whole assembly line affecting the total resource demand only marginally.

- 3.

- 4.

ISO’s (2011) definition of a quantity center additionally includes the demand for a monetary quantification of the in- and outputs. However, as the following explanations will demonstrate, the monetary valuation of in- and output flows is based on their physical quantification which, therewith, is the sole requirement for defining a quantity center.

- 5.

Here, only the directions and the characteristics (desired or undesired) of the flows are determined. The quantification of flows follows in the second step.

- 6.

For the intended analysis, the mass of materials can be presumed as constant. So, the inputs, outputs, and changes in stocks of the quantity centers can be listed in form of a material balance.

- 7.

For reasons of simplification the quantity center structure can also be derived from that of the cost centers. But, it has to be ensured that every quantity center is attributed to only one superior cost center, if the quantity center structure is more differentiated than that of the cost centers. In case of the cost center structure is more detailed in some areas, subordinate cost centers must be attributed to the superior quantity centers correspondingly.

- 8.

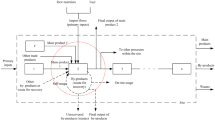

In this regard, it has to be noted again that the model records the material quantities flown within a defined time period. Since in Fig. 4 the product flow is the only flow leaving the loop, all occurred system costs are finally assigned to it.

- 9.

In case the material loss is not fully recycled and there is an undesired material output flow leaving the loop, the criticism still concerns the share of loop costs assigned to the raw material substitute flow.

- 10.

The value includes 50 € of the production process’ system costs (assigned to the material loss flow) and the system costs of the recycling process, 50 € as well. The flow of the raw material substitute is valued by its material costs only.

- 11.

For example, Volkswagen recently communicated its strategy for decreasing production’s CO2 emissions including the concrete goal of reducing the energy demand by 25 % until 2018 (Viehmann 2012).

- 12.

In the strict sense, the approach is enhanced to a material and energy flow cost accounting. For reasons of simplification, the name material flow cost accounting (MFCA) is still used in the following.

- 13.

For quantifying the energy content of ‘material based’ energy carriers, such as gas or coal, the specific heating value can be used.

- 14.

Alternatively, ITO-models of the underlying technical processes and, if needed, of sub processes can be used for the analysis. For reasons of simplification, in the following, quantity centers and processes are considered as equal.

- 15.

For details about the methods of investment appraisal mentioned in this chapter see e.g., Götze et al. (2008).

- 16.

For a detailed description of LCC’s methodology see e.g., Horngren et al. (2012).

- 17.

For instance, future techniques of recycling (end-of-life phase) may be unknown today.

- 18.

An overview of the methodology is given by ISO (2006).

- 19.

Recent approaches like the carbon footprint and the carbon accounting (see e.g., Bowen and Wittneben 2011) refer to this indicator only and can be considered as simplified or carbon specific LCA approaches.

- 20.

It has to be noted, that at least some Japanese companies successfully utilize MFCA as a technique of daily operational management and benefit from this practice (Nakajima 2010).

- 21.

The high consistency arises in particular from the uses of in- and output balances for every quantity center (see Sect. 2.2).

References

Bierer A, Götze U (2012) Energy cost accounting: conventional and flow-oriented approach accounting. J Compet 4(2):128–144. doi:10.7441/joc.2012.02.09

Bowen F, Wittneben B (2011) Carbon accounting: negotiating accuracy, consistency and certainty across organisational fields. Acc Audit Acc J 24(8):1022–1036. doi:10.1108/09513571111184742

Bundesumweltministerium (BUM), Umweltbundesamt (UBA) (eds) (2003) Leitfaden Betriebliches Umweltkostenmanagement, Berlin

Götze U, Helmberg C, Rünger G, Schubert A, Goller S, Krellner B, Lau A, Sygulla R (2010) Integrating energy flows in modeling manufacturing processes and process chains of powertrain components. In: Neugebauer R (ed) Proceedings of the 1st international colloquium of the cluster of excellence eniPROD. Wissenschaftliche Scripten, Auerbach, pp 409–437

Götze U, Northcott D, Schuster P (2008) Investment appraisal, methods and models. Springer, Berlin. doi: 10.1007/978-3-540-39969-8

Götze U, Schubert A, Bierer A, Goller S, Sygulla R (2012) Material und Energieflussanalyse—Methodik zur Optimierung von Prozessen und Prozessketten. In: Neugebauer R (ed) Proceedings of the ICMC 2012/2nd international colloquium of the cluster of excellence eniPROD. Wissenschaftliche Scripten, Auerbach, pp 99–128

Horngren CT, Datar SM, Rajan MV (2012) Cost accounting: a managerial emphasis, 14th edn. Prentice Hall, Boston

Hyršlová J, Bednaříkova M, Hájek M (2008) Material flow cost accounting, only a tool of environmental management or a tool for the optimization of corporate production processes? Sci Pap Univ Pardubice Ser A 14:131–145

ISO (2006) ISO 14040 Environmental management—life cycle assessment—principles and framework

ISO (2010) Draft International Standard ISO/DIS 14051 Environmental management—material flow cost accounting—general framework

ISO (2011) ISO 14051 Environmental management—material flow cost accounting—general framework

Jasch C (2009) Environmental and material flow cost accounting, principles and procedures. Springer, Dordrecht. doi: 10.1007/978-1-4020-9028-8

Kokubu K, Campos MKS, Furukawa Y, Tachikawa H (2009) Material flow cost accounting with ISO 14051. ISO Manag Sys 5(2):15–18

Kokubu K, Kitada H (2010) Conflicts and solutions between material flow cost accounting and conventional management thinking. In: Proceedings of the 6th APIRA. http://apira2010.econ.usyd.edu.au/conference_proceedings. Accessed Nov 12 2012

Loew T (2003) Environmental cost accounting, classifying and comparing selected approaches. In: Bennett M, Rikhardsson P, Schaltegger S (eds) Environmental management accounting—purpose and progress, Kluwer, Dordrecht pp 41–56

Möller A (2010) Material and energy flow-based cost accounting. Chem Eng Technol 33(4):567–572. doi:10.1002/ceat.200900491

Nakajima M (2006) The New Management Accounting Field Established by Material Flow Cost Accounting (MFCA). Kansai Univ Rev Bus Commer 8:1–22

Nakajima M (2008) The new development of material flow cost accounting (MFCA): MFCA analysis in power company and comparison between MFCA and TPM (Total Productive Maintenance). Kansai Univ Rev Bus Commer 10:57–86

Nakajima M (2009) Evolution of material flow cost accounting (MFCA): characteristics on development of MFCA companies and significance of relevance of MFCA. Kansai Univ Rev Bus Commer 11:27–46

Nakajima M (2010) Environmental management accounting for sustainable manufacturing, establishing management system of material flow cost accounting (MFCA). Kansai Univ Rev Bus Commer 12:41–58

Nakajima M (2011) Environmental management accounting for cleaner production: systemization of material flow cost accounting (MFCA) into corporate management system. Kansai Univ Rev Bus Commer 13:17–39

Prammer HK (2009) Integriertes Umweltkostenmanagement Bezugsrahmen und Konzeption für eine ökologisch nachhaltige Unternehmensführung. Habilitation University of Linz, Linz

Schmid U (2001) Schwachstelle Datenqualität: Flusskostenrechnung in der Praxis bei Sortimo International. Ökol Wirtsch 2001(6):16–17

Schmidt M (2012) Material flow cost accounting in der produzierenden Industrie. In: von Hauff M, Isenmann R, Müller-Christ G (eds) Industrial ecology management. Gabler, Wiesbaden, pp 241–255. doi:10.1007/978-3-8349-6638-4_15

Schubert A, Goller S, Sonntag D, Nestler A (2011) Implementation of energy-related aspects into model-based design of processes and process chains. In: Proceedings of the 2011 international symposium on assembly and manufacturing. doi:10.1109/ISAM.2011.5942344

Schweitzer M, Küpper H-U (2011) Systeme der Kosten- und Erlösrechnung, 10th edn. Vahlen, Munich

Statistisches Bundesamt (ed) (2011) Statistical yearbook 2011 for the Federal Republic of Germany including “International tables”, Wiesbaden

Strobel M, Redmann C (2002) Flow cost accounting, an accounting approach based on the actual flows of materials. In: Bennett M, Bouma JJ, Wolters T (eds) Environmental management accounting: informational and institutional developments. Kluwer, Dordrecht, pp 67–82

Strobel M, Wagner F (1999) Flußkostenrechnung als Instrument des Materialflußmanagements. uwf 7(4):26–28

Sygulla R, Bierer A, Götze U (2011) Material flow cost accounting, proposals for improving the evaluation of monetary effects of resource saving process designs. In: Proceedings of the 44th CIRP conference on manufacturing systems. http://www.tu-chemnitz.de/wirtschaft/bwl3/DownloadAllgemeinOffen/44thCIRP_MFCA.pdf. Accessed 12 Nov 2012

Viehmann S (2012) Winterkorn will VW grüner machen. zeit online. www.zeit.de/auto/2012-03/volkswagen-umweltschutz. Accessed 12 Nov 2012

Viere T, Prox M, Möller A, Schmidt M et al (2011) Implications of material flow cost accounting for life cycle engineering. In: Hesselbach J, Herrmann C (eds) Globalized solutions for sustainability in manufacturing. Proceedings of the 18th CIRP international conference on life cycle engineering. Springer, Berlin pp 652–656. doi:10.1007/978-3-642-19692-8_113

Wagner B, Nakajima M, Prox M (2010) Materialflusskostenrechnung—die internationale Karriere einer Methode zu Identifikation von Ineffizienzen in Produktionssystemen. uwf 18:197–202. doi:10.1007/s00550-010-0189-1

Acknowledgments

The authors like to thank the European Union (European Regional Development Fund) and Germany’s Free State of Saxony for funding the Cluster of Excellence ‘Energy-Efficient Product and Process Innovation in Production Engineering’ (eniPROD®) as well as the Deutsche Forschungsgemeinschaft (DFG) for funding this work within the Collaboration Research Centre ‘SFB 692’.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2014 Springer-Verlag London

About this chapter

Cite this chapter

Sygulla, R., Götze, U., Bierer, A. (2014). Material Flow Cost Accounting: A Tool for Designing Economically and Ecologically Sustainable Production Processes. In: Henriques, E., Pecas, P., Silva, A. (eds) Technology and Manufacturing Process Selection. Springer Series in Advanced Manufacturing. Springer, London. https://doi.org/10.1007/978-1-4471-5544-7_6

Download citation

DOI: https://doi.org/10.1007/978-1-4471-5544-7_6

Published:

Publisher Name: Springer, London

Print ISBN: 978-1-4471-5543-0

Online ISBN: 978-1-4471-5544-7

eBook Packages: EngineeringEngineering (R0)