Abstract

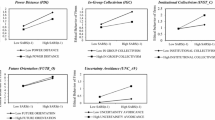

This study aims to examine the relationship between national cultural dimensions and the probability of a firm being externally audited. It uses a large set of representative micro-data from nearly 3000 firms across 34 industries in 13 countries in Eastern Europe and the Middle East over the period 2008–2010, and Schwartz’s cultural dimensions, namely autonomy, embeddedness, egalitarianism and hierarchy. The findings show that the relationship between firm audits and cultural autonomy and egalitarianism is strongly positive and statistically significant. Specifically, they show that an increase of one standard deviation (SD) in affective autonomy increases the probability that a firm will engage in an external audit by 3.37%. Along the same lines, a 1 SD increase in egalitarianism leads to a 8.36% increase in the likelihood of a firm engaging in an external audit. However, there is no clear evidence that embeddedness and hierarchy play a role in firms’ external auditing trends. These findings remain robust to the use of several confounding factors at the firm and country levels. This research highlights its uniqueness in the choice of national culture as a determinant for the likelihood of external audits.

Similar content being viewed by others

References

Abdel-Khalik, A. R. (1993). Why do private companies demand an audit? A case for organizational loss of control. Journal of Accounting, Auditing and Finance, 8, 31–52.

Abdolmohammadi, M., & Sarens, G. (2011). An investigation of the association between cultural dimensions and variations in perceived use of and compliance with internal auditing standards in 19 countries. The International Journal of Accounting, 46, 365–389.

Afifunddin, H. B., & Siti-Nabiha, A. K. (2010). Towards good accountability: The role of accounting in Islamic religious organisations. World Academy of Science, Engineering and Technology, 66, 1133–1139.

Alchian, A. A., & Demsetz, H. (1972). Production, information costs, and economic organization. American Economic Review, 62, 777–795.

Alzeban, A. (2015). The impact of culture on the quality of internal audit: an empirical study. Journal of Accounting, Auditing and Finance, 30(1), 57–77.

Bik, O. and Hooghiemstra, R., 2018. Cultural differences in auditors’ compliance with audit firm policy on fraud risk assessment procedures. Auditing: A Journal of Practice and Theory 37 (4), 25–48.

Brett, J.M. and Okumura, T., 1998. Inter-and intracultural negotiation: U.S. and Japanese negotiators. The Academy of Management 41 (5), 495–510.

Brown, P., Preiato, J., & Tarca, J. (2014). Measuring country differences in enforcement of accounting standards: an audit and enforcement proxy. Journal of Business Finance and Accounting, 41(1–2), 1–52.

Carey, P., Simnett, R. and Tanewski, G., 2000. Voluntary demand for internal and external auditing by family businesses. Auditing: A Journal of Practice and Theory 19 (S1), 37–51.

Cieslewicz, J. K. (2014). Relationships between national economic culture, institutions, and accounting: Implications for IFRS. Critical Perspectives on Accounting, 25(6), 511–528.

Chow, C. W. (1982). The demand for external auditing: size, debt and ownership influences. The Accounting Review, 57(2), 272–291.

Eulerich, M. and Ratzinger-Sakel, N.V.S., 2017. The Effects of Cultural Dimension on the Internal Audit Function-A Worldwide Comparison of Internal Audit Characteristics. Working paper, University of Hamburg.

Gray, S. J. (1988). Towards a theory of cultural influence on the development of accounting systems internationally. Abacus, 24(1), 1–15.

Gray, S. J., & Vint, H. M. (1995). The impact of culture on accounting disclosures: Some international evidence. Asia-Pacific Journal of Accounting, 21, 33–43.

Gorodnichenko, Y., & Roland, G. (2017). Culture, Institutions and the Wealth of Nations. Review of Economics and Statistics, 99(3), 402–416.

Guiso, L. (2009). Cultural bias in economic exchange? Quarterly Journal of Economics,124(3), 1095–1131.

Hamid, S., Craig, R., & Clarke, F. (1993). Religion: a confounding cultural element in the international harmonization of accounting? Abacus, 29(2), 131–148.

Hofstede, G. (1980). Culture’s Consequences: International Differences in Work Related Values. Beverly Hills, CA: Sage Publications.

Hope, O. K. (2003). Firm-level disclosures and the relative roles of culture and legal origin. Journal of International Financial Management and Accounting, 14(3), 218–248.

Hope, O. K., Kang, T., Wayne, T., & Yoo, Y. K. (2008). Culture and auditor choice: a test of the secrecy hypothesis. Journal of Accounting and Public Policy, 27, 357–373.

Jaggi, B., & Low, P. Y. (2000). Impact of culture, market forces, and legal systems on financial disclosures. International Journal of Accounting, 35(4), 495–519.

Jensen, M. C., & Meckling, J. W. (1976). Theory of the firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360.

Kagitcibasi, C. (1997). Individualism and collectivism. In J. F. Berry, M. H. Segall, & C. Kagitcibasi (Eds.), Handbook of cross-cultural psychology (Vol. vol, p. 3(pp. 1–49).). London: Allyn & Bacon.

Kleinman, G., Lin, B. B., & Bloch, R. (2019). Accounting enforcement in a national context: an international study. International Journal of Disclosure and Governance, 16(1), 1–21.

Kostova, T., Nell, P. C., & Hoenen, A. K. (2018). Understanding agency problems in headquarters-subsidiary relationships in multinational corporations: a contextualized model. Journal of Management, 44(7), 2611–2637.

Long, J. S. (1997). Regression Models for Categorical and Limited Dependent Variables. Thousand Oaks, CA: Sage Publications.

Maali, B., & Napier, C. (2010). Accounting, religion and organisational culture: the creation of Jordan Islamic Bank. Journal of Islamic Accounting and Business Research, 1(2), 92–113.

Nedelcu, M., Siminica, M., & Turlea, C. (2015). The correlation between external audit and financial performance of banks from Romania. Amfiteatru Economic, 17(9), 1273–1288.

Nemes, S., Jonasson, J. M., Genell, A., & Steineck, G. (2009). Bias in odds ratios by logistic regression modelling and sample size. BMC Medical Research Methodology, 9, 56.

Ng, S., Lee, J. A., & Soutar, G. N. (2007). Are Hofstede’s and Schwart’s values frameworks congruent? International Marketing Review, 24(2), 164–180.

North, D.C., 1990. Institutions, institutional change and economic performance. Cambridge University Press

Salter, S. B., & Niswander, F. (1995). Cultural influence on the development of accounting systems internationally: A test of Gray’s (1988) theory. Journal of International Business Studies, 26(2), 379–397.

Sarens, G., & Abdolmohammadi, M. (2011). Monitoring effects of the internal audit function: Agency theory versus other explanatory variables. International Journal of Auditing, 15, 1–20.

Schwartz, S. H. (2006). A theory of cultural value orientations: explication and applications. Comparative Sociology, 5, 136–182.

Schwartz, S. H. (1999). A theory of cultural values and some implications for work. Applied Psychology, 48(1), 24–47.

Steemkamp, J.-B. E. M. (2001). The role of national culture in international marketing research. International Marketing Review, 18(1), 30–44.

Tabellini, G. (2010). Culture and Institutions: Economic Development in the Regions of Europe. Journal of the European Economic Association, 8(4), 677–716.

Tabellini, G. (2008). Institutions and Culture. Journal of the European Economic Association, 6(2–3), 255–294.

Tauringana, V., & Clarke, S. (2000). The demand for external auditing: managerial share ownership, size, gearing and liquidity influences. Managerial Auditing Journal, 15(4), 160–168.

Williamson, O. E. (1975). Markets and hierarchies analysis and antitrust implications: a study in the economics of internal organization. New York: Free Press.

Wiseman, R. M., Cuevas-Rodriguez, G., & Gomez-Mejia, L. R. (2012). Towards a social theory of agency. Journal of Management Studies, 49, 202–222.

Wingate, M. L. (1997). An examination of cultural influence on audit environments. Research in Accounting Regulation, 10A(S1), 129–148.

Zarzeski, M. (1996). Spontaneous harmonization effects of culture and market forces on accounting disclosure practices. Accounting Horizons, 10(1), 18–38.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Diallo, B. Do National Cultures Matter for External Audits? Evidence from Eastern Europe and the Middle East. J Bus Ethics 172, 347–359 (2021). https://doi.org/10.1007/s10551-020-04482-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10551-020-04482-9