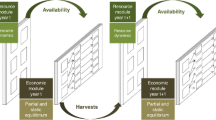

Abstract

The famous “Faustmann” equation, which allows for identifying the most profitable tree species on a given unstocked piece of land, assumes constant timber prices. In reality, timber prices may fluctuate dramatically. Several authors have proven for monocultures that waiting for an acceptable timber price (reservation price) before harvesting (flexible harvest policy) increases the net present value of forest management. The first part of this paper investigates how efficient a flexible harvest strategy may be applied in mixed forests and whether the optimal species mixture is changed under such harvest policy. Mixtures of the conifer Norway spruce [Picea abies (L.) Karst] and the broadleaf European beech (Fagus sylvatica L.) were investigated. In order to evaluate mixed forests, the risks and the correlation of risks between tree species as well as the attitude towards risk of the decision-maker (risk-aversion is assumed) were considered according to the classical theory of optimal portfolio selection. In the second part we took up a recent critique on modern financial theory by Mandelbrot. Whether or not the assumption of normally distributed financial flows, which are supposed to occur under risk, would be appropriate to evaluate the risk of forest management was investigated. Market and hazard risks as well as their correlation were integrated in the evaluation of mixed forests by means of Monte-Carlo simulations (MCS). The risk of the timber price fluctuation was combined with the natural hazard risk, caused mainly by insects, snow and wind. Applying the μ-σ-rule, the mean net present value (NPV) from 1,000 simulations and their standard deviation were used for the optimisation. Given a low-return, risk-free interest rate to assess potential species mixtures of the Norway spruce and European beech, optimal proportions of European beech increased according to the theory of optimum portfolio selection with growing risk aversion from 0 (ignorance of risk) to 60% (great risk-aversion). In relation to a fixed harvest policy, the net present value of both, Norway spruce and European beech, could be increased significantly. Since the hazard risks of European beech were substantially lower compared with the Norway spruce (relation of susceptibility 1:4) beech benefited more from the flexible harvest policy. A comparison of simulated frequency distributions of the NPV with the expected density functions under the assumption of a normal distribution revealed significant differences. Only in the case of European beech was the general shape of the simulated frequency distribution similar to a normal distribution (bell-shaped curve). However, the density of NPV close to the mean was much greater than expected under the assumption of a normal distribution. Consequently, the frequency of a negative NPV for a European beech forest was greatly overestimated when applying the normal distribution. Though the shape of the simulated frequency distribution was rather different from a normal distribution for Norway spruce the simulated part of negative NPV was quite well approximated by the normal distribution. Therefore the simulated and expected frequencies of negative NPV were similar in case of Norway spruce; only a slight underestimation was seen in the assumption of a normal distribution. It can be concluded that actually simulated frequencies of negative NPV seem to be better measures for risk than computed probabilities of negative NPV, which assume normal distribution. As the risk for European beech was greatly overestimated by the conventional assumption of a normal distribution, the optimal proportions of European beech were surely rather underestimated according to the theory of portfolio. MCS on optimum mixtures derived by the classical portfolio theory seems necessary to test the robustness of such mixtures.

Similar content being viewed by others

Notes

The NPV is formed by the sum of all appropriately discounted net revenue flows.

An earlier exemplary paper has already been written on this topic (see Knoke et al. 2001).

For European beech also rotation periods between 101 and 110 years were tested in order to provide identical investment periods.

Locally related survival probabilities for forest offices in Baden-Württemberg were published, for example, by Hanewinkel and Holcey (2005).

If two rotation periods of different lengths were compared (e.g. 100 and 120 years) considering only one rotation period would be a biased evaluation (see Knoke et al. 2005).

Here the NPV was reduced on average by €2,182 per ha, which was the sum of the discounted overhead costs.

References

Bamberg G, Coenenberg AG (1992) Betriebswirtschaftliche Entscheidungslehre. Vahlen, München

Baumgarten M, Teuffel K von (2005) Nachhaltige Waldwirtschaft in Deutschland. In: Teuffel K von, et al (eds) Waldumbau. Springer-Verlag, Berlin Heidelberg New York, pp 1–10

Bavarian State Forest Service (2001) Jahresbericht 2001. Bavarian State Ministry of Agriculture and Forests, Munich

Brazee R, Mendelsohn R (1988) Timber Harvesting with Fluctuating Prices. For Sci 34:359–372

Deegen P, Hung BC, Mixdorf U (1997) Ökonomische Modellierung der Baumartenwahl bei Unsicherheit der zukünftigen Temperaturentwicklung. Forstarchiv 68:194–205

Dieter M (1997) Berücksichtigung von Risiko bei forstbetrieblichen Entscheidungen. Schriften zur Forstökonomie Bd. 16. Frankfurt/Main: J.D. Sauerländer’s

Dieter M (2001) Land expectation values for spruce and beech calculated with Monte Carlo modelling techniques. For Policy Econ 2:157–166

Elton EJ, Gruber MJ (1995) Modern portfolio theory and investment analysis, 5th edn. Chichester, Wiley, New York

Gerber HU, Pafumi G (1998) Utility functions: from risk theory to finance. North Am Actuarial J 2:74–100

Gong P (1998) Risk preferences and adaptive harvest policies for even-aged stand management. For Sci 44:496–506

Haight RG (1990) Feedback thinning policies for uneven-aged stand management with stochastic prices. For Sci 36:1015–1031

Hanewinkel M, Holcey J (2005) Quantifizierung von Risiko durch altersstufenweise Ermittlung von Übergangswahrscheinlichkeiten mit Hilfe von digitalisierten Forstkarten. In: Teuffel K von, et al (eds) Waldumbau. Springer-Verlag, Berlin Heidelberg New York, pp 269–277

Knoke T (2002) Value of perfect information on red heartwood formation in beech (Fagus sylvatica L.). Silva Fennica 36:841–851

Knoke T, Moog M, Plusczyk N (2001) On the effect of volatile stumpage prices on the economic attractiveness of a silvicultural transformation strategy. ForPolicy Econ 2:229–240

Knoke T, Stimm B, Ammer C, Moog M (2005) Mixed forests reconsidered: a forest economics contribution to the discussion on natural diversity. For Ecol Manag 213:102–116

Kouba J (2002) Das Leben des Waldes und seine Lebensunsicherheit. Forstwissenschaftliches Centralblatt 121:211–228

Lohmander P (1993) Economic two stage multi species management in a stochastic environment: the value of selective thinning options and stochastic growth parameters. Syst Anal-Model-Simul 11:287–302

Lüpke B, Spellmann H (1999) Aspects of stability, growth and natural regeneration in mixed Norway spruce-European beech stands as a basis of silviculture decisions. In: Olsthoorn AFM et al. (eds). Management of mixed-species forests: silviculture and economics. Wageningen: IBN-DLO Scientific contributions, pp 245–267

Mandelbrot BB, Hudson RL (2005) Fraktale und Finanzen: Märkte zwischen Risiko, Rendite und Ruin. Piper, München

Markowitz H (1952) Portfolio selection. J Finance 7:77–91

Möhring B (1986) Dynamische Betriebsklassensimulation – Ein Hilfsmittel für die Waldschadensbewertung und Entscheidungsfindung im Forstbetrieb. Berichte des Forschungszentrums Waldökosysteme-Waldsterben der Universität Göttingen Band 20

Möhring B (2004) Betriebswirtschaftliche Analyse des Waldumbaus. Forst Holz 59:523–530

Penttinen M, Lausti A (2004) The competitiveness and return components of NIPF ownership in Finland. Finnish J Business Econ, Spl Edn 2/2004

Pflaumer P (1992) Investitionsrechnung. Oldenburg Verlag, München, Wien

Pretzsch H (2005) Diversity and productivity in forests: evidence from long-term experimental plots. In: Scherer-Lorenzen et al. (eds) Forest diversity and function: temperate and boreal systems. Ecological studies, vol 176. Springer-Verlag, Berlin Heidelberg New York, pp41–64

Reed WJ (1996) Predicting the present value distribution of a forest plantation investment. For Sci 42:378–387

Runzheimer B (1999) Operations research. Gabler, Wiesbaden

Sharpe WF (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. J Finance 14:425–442

Spellmann H (2005) Produziert der Waldbau am Markt vorbei? Allg. Forstzeitschrift/Der Wald 60:454–459

Spremann K (1996) Wirtschaft, Investition und Finanzierung. 5., vollständig überarbeitete, ergänzte und aktualisierte Auflage. Oldenbourg: München und Wien

Teeter LD, Caulfield JP (1991) Stand density management under risk: effects of stochastic prices. Can J For Res 21:1373–1379

Thomson TA (1991) Efficient combinations of timber and financial market investments in single-period and multiperiod portfolios. For Sci 37:461–480

Valkonen S, Valsta L (2001) Productivity and economics of mixed two-storied spruce and birch stands in Southern Finland simulated with empirical models. For Ecol Manag 140:133–149

Wagner JE, Rideout DB (1991) Evaluating forest management investments: the capital asset pricing model and the income growth model. For Sci 37:1591–1604

Wagner JE, Rideout DB (1992) The stability of the capital asset pricing model’s parameters in analysing forest investments. Can J For Res 22:1639–1645

Waller LA, Smith D, Childs JE, Leslie AR (2003) Monte Carlo assessment of goodness-of-fit for ecological simulation models. Ecol Model 164:49–63

Weber M-W (2002) Portefeuille- und Optionspreis-Theorie und forstliche Entscheidungen. Schriften zur Forstökonomie Band 23. Sauerländer’s, Frankfurt a.M

Wippermann Ch, Möhring B (2001) Exemplarische Anwendung der Portefeuilletheorie zur Analyse eines forstlichen Investments. Forst Holz 56:267–272

Yool A (1999) Comments on the paper: on repeated parameter sampling in Monte Carlo simulations. Ecol Model 115:95–98

Zinkhan FC, Cubbage FW (2003) Financial analysis of timber investments. In: Sills EO, Abt KL (eds) Forests in a market economy. Forestry sciences, vol 72. Kluwer, Dordrecht, Boston, London, pp 77–95

Acknowledgements

The authors wish to thank Mrs. Edith Lubitz for the language editing of the manuscript and two anonymous reviewers for valuable suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Communicated by Hans Pretzsch

Rights and permissions

About this article

Cite this article

Knoke, T., Wurm, J. Mixed forests and a flexible harvest policy: a problem for conventional risk analysis?. Eur J Forest Res 125, 303–315 (2006). https://doi.org/10.1007/s10342-006-0119-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10342-006-0119-5