Abstract

This article describes aspects of the economic analyses that were performed on three matters on which economists in the Bureau of Economics at the Federal Trade Commission have worked during this past year. The first two matters were merger investigations: They (separately) involved tobacco manufacturers and food distributors. While these investigations shared some common attributes, such as the importance of the proposed divestitures, this essay demonstrates how our analysis must vary based on the types of information and the competitive concerns presented by specific transactions. The third section discusses a general economic approach to estimating consumer harm from data breaches, which is illustrated with an example of an application to a recent case.

Similar content being viewed by others

Notes

See FTC Fiscal Year 2017 Congressional Budget Justification at https://www.ftc.gov/system/files/documents/reports/fy-2017-congressional-budget-justification/2017-cbj.pdf.

One example of a large Commission study on which BE economists have been working is an ongoing study of remedies in FTC merger cases, https://www.ftc.gov/news-events/press-releases/2015/01/ftc-proposes-study-merger-remedies. BE staff also disseminate articles via the BE Working Papers series (https://www.ftc.gov/policy/reports/policy-reports/economics-research/working-papers), many of which end up being the basis for articles published in academic economics journals.

See, for instance, numerous advocacy comments at https://www.ftc.gov/policy/advocacy/advocacy-filings.

FTC & Department of Justice (2016).

Ibid. at 5.

See https://www.ftc.gov/competition-enforcement-database for a table of these merger and non-merger enforcement statistics for each year starting in 1996.

Supra note 4.

Conference materials can be found at https://www.ftc.gov/news-events/events-calendar/2015/11/eighth-annual-federal-trade-commission-microeconomics-conference.

For a discussion of the FTC’s investigation of this merger, see FTC, Analysis of Agreement Containing Consent Order to Aid Public Comment, In the Matter of Reynolds American Inc. and Lorillard Inc. at https://www.ftc.gov/system/files/documents/cases/150526reynoldsanalysis.pdf.

See the FTC’s Administrative Complaint, In re Sysco Corp., Dkt. No. 9364 (F.T.C. Feb. 19, 2015), available at https://www.ftc.gov/system/files/documents/cases/150219syscopt3cmpt.pdf.

FTC v. Wyndham Worldwide Corp., 799 F.3d 236 (3d Cir. 2015).

For more on potential industry coordination, see Ciliberto and Kuminoff (2010).

The explanation for this effect is just the reverse of the typical description of how a merger of substitutes can cause prices to increase. In this instance, lowering the price of one of the substitute products becomes more profitable when the products are not jointly owned because the owner of one product has no incentive to internalize how this lower price will cannibalize the sales of the other product.

These approaches both assumed that the manufacturer sells its product directly to the consumer. In fact, the manufacturer sells to a distributer who sells to a retailer, who sells to a consumer. Given facts that were uncovered during the investigation about the ways in which prices are set in the industry, we felt that this was an appropriate simplification.

Both of these build on Farrell and Shapiro (2010).

Formally \(D_{jm} = -\left( {\frac{{\partial Q_{j} }}{{\partial P_{j} }}} \right)^{ - 1} \left( {\frac{{\partial Q_{m} }}{{\partial P_{j} }}} \right)\).

While in some contexts it is possible to obtain a diversion ratio from a “natural experiment”, this usually gives the diversion ratio when a product is removed from the choice set. While in a bargaining context like health care, this is the relevant diversion ratio (see Raval et al. 2015) in the posted price context it is not. However, specific functional form assumptions—including logit—imply that the diversion ratio is constant or close to constant over a range of prices, in which case a diversion ratio from a natural experiment may be informative (see Conlon and Mortimer 2013).

Formally, \(D_{jm} = \mathop \sum_{g} w_{j}^{g} D_{jm}^{g}\), where \(w_{j}^{g}\) is the share of demand for product j that is purchased by group g. Note that these weights could differ at pre and post-merger prices. We used the pre-merger weights.

In this case, we put a weight of one on the diversions from the regular users of that product. For example, to compute the diversion ratio from j to m, we only used regular users of j.

When we consider price discrimination, it is important to establish that arbitrage is not possible. In this case, reselling and delivering to other customers is not practical since delivery is an essential component of the initial purchase.

Supra note 12.

See U.S. Department of Justice & the Federal Trade Commission (2010, p. 6).

This is easiest to demonstrate in the context of a bidding model with full information about rivals, which can be motivated by the large amount of information that sales reps collect about customers; but similar conclusions could be drawn from auction models without full information.

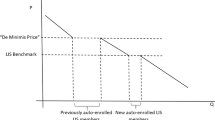

While national customers were the most likely to see the distance to the next-best alternative increased by the merger, in some local areas the next-best alternative also would have been significantly further away if the merger had taken place.

Indeed, one of the more interesting questions that arose in this case is why smaller foodservice distributors continued to exist in a market where variety and scale matter. One possible reason is that while large foodservice distributors often must carry all manufacturers in a product category to serve their large client base, smaller foodservice distributor may be able to negotiate price concessions with manufacturers in exchange for carrying and promoting only one product in various categories. Smaller distributors can then use the prices that they gain in exchange for that promotion to “get their foot in the door” with customers. Alternatively, smaller foodservice distributors may specialize in certain categories and offer different quality products in those categories.

See FTC Privacy and Security Update (2015) at https://www.ftc.gov/reports/privacy-data-security-update-2015.

For example, the Federal Reserve Bank of Boston’s Survey of Consumer Payment Choice is one potential source of information on the percentage of households with access to different payment instruments, such as debit and credit cards. See https://www.bostonfed.org/publications/survey-of-consumer-payment-choice.aspx.

The approach that is laid out in this paper adopts an ex ante perspective: It assumes that the firm's deficient data security practices injured affected customers by increasing the risk that their sensitive data would be stolen, used for identity theft, and result in corresponding costs to consumers. Under the assumptions that consumers have rational expectations with regard to the relevant probabilities and economic costs, and are risk-neutral, an equivalent estimate of consumer injury could be obtained by an ex post analysis that calculated the harm imposed on consumers whose sensitive information was actually stolen and who, thus, actually experienced the consumer costs associated with identify theft.

References

Ciliberto, F., & Kuminoff, N. V. (2010). Public policy and market competition: how the master settlement agreement changed the cigarette industry. The BE Journal of Economic Analysis and Policy, 10(1), 1–46.

Conlon, C. T., & Mortimer, J. H. (2013). An experimental approach to merger evaluation. NBER Working Paper No. 19703.

Farrell, J., Balan, D. J., Brand, K., & Wendling, B. W. (2011). Economics at the FTC: Hospital mergers, authorized generic drugs, and consumer credit markets. Review of Industrial Organization, 39(4), 271–296.

Farrell, J., & Shapiro, C. (2010). Antitrust evaluation of horizontal mergers: An economic alternative to market definition. The BE Journal of Theoretical Economics. doi:10.2202/1935-1704.1563.

Federal Trade Commission & Department of Justice. (2016). Hart-Scott-Rodino Annual Report, Fiscal Year 2015. Retrieved October 14, 2016, from FTC Web site: https://www.ftc.gov/system/files/documents/reports/federal-trade-commission-bureau-competition-department-justice-antitrust-division-hart-scott-rodino/160801hsrreport.pdf.

Jaffe, S., & Weyl, E. G. (2013). The first-order approach to merger analysis. American Economic Journal: Microeconomics, 5(4), 188–218.

Miller, N., Remer, M., Ryan, C., & Sheu, G. (2016). Upward Pricing Pressure as a Predictor of Merger Price Effects. EAG Discussion Paper 16-2. Retrieved October 14, 2016 from DOJ Web site: https://www.justice.gov/atr/file/829271/download.

Miller, N. H., Remer, M., Ryan, C., & Sheu, G. (2017). Pass-through and the prediction of merger price effects. Journal of Industrial Economics. http://www.jindec.org/?q=article/pass-through-and-prediction-merger-price-effects%03 (forthcoming).

Raval, D., Rosenbaum, T., & Tenn, S. (2015). Semiparametric discrete choice model: An application to hospital mergers, mimeo.

U.S. Department of Justice & the Federal Trade Commission. (2010). Horizontal merger guidelines. Retrieved October 14, 2016, from FTC Web site. http://www.ftc.gov/os/2010/08/100819hmg.pdf.

Acknowledgements

We thank Tim Daniel, Janis Pappalardo, Dave Schmidt, Andrew Stivers, Aileen Thompson and Michael Vita for helpful comments. The views that are expressed in this article are those of the authors and do not necessarily reflect those of the Federal Trade Commission or any of the individual Commissioners.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Hanner, D., Jin, G.Z., Luppino, M. et al. Economics at the FTC: Horizontal Mergers and Data Security. Rev Ind Organ 49, 613–631 (2016). https://doi.org/10.1007/s11151-016-9548-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11151-016-9548-6