Abstract

Housing is a basic necessity, and it is essential to properly balance its dual properties as both a consumer product and an asset for investment. However, historically, China’s real estate market has taken the path of excessive financialization in the process of accelerating economic development and urban modernization. The deviation from its attribute as an essential consumer product has negatively affected people’s livelihood, economic growth, and financial stability, and has even limited the effectiveness of counter-cyclical macroeconomic policies, which has hindered, to some extent, the progress towards common prosperity. The financialization of land and the commoditization of housing have caused the excessive financialization of China’s real estate market. They are the core issues on the supply and demand sides of this market, respectively. On the supply side, local governments have been raising financial resources through land asset liquidation and mortgage financing, which has deepened the financial cycle spanning from land prices to housing prices, and to credit supply. The balance sheet of local governments is “tied” to the land market, pushing up land prices and leading to the continuous expansion of hidden debts and real estate bubbles. On the demand side, since the institutional reform of the housing market in 1998, China has created an imbalanced supply structure characterized by a boom in developer-built housing and a shortage of low-income housing as well as long-term rental housing, with the majority of households relying on mortgages and other financial instruments to meet their housing needs. Moreover, the financialization of land and the commoditization of housing are mutually reinforcing, strengthening the dependence of local governments on land, incentivizing developers to raise debt and leverage, and guiding the allocation of bank loans to the housing market. The problem has been exacerbated by the connections between banks and some real estate companies. We believe the real estate sector should reduce excessive financialization, and that housing revert to its primary attribute as an essential consumer product. Therefore, the supply-side reform should be vigorously pursued, whereas speculative demand must be resolutely suppressed. The legislation on real estate tax should be accelerated to revamp local government funding sources. We believe China should expand the supply of high-quality low-income housing, build a multi-tiered and laddered supply system, and vigorously develop the rental housing market with legal protection.

Authors: Eric Yu Zhang, Wenlang Zhang, Qiaofeng Deng, Yuchi Zheng, Hao Li, Chao Xie.

You have full access to this open access chapter, Download chapter PDF

Since the launch of the institutional reform of the housing market in 1998, China’s urban households have achieved a significant and rapid improvement in their quality of living. However, the phenomenon of “commoditization of housing” and “financialization of land” has intensified, especially in the last decade, giving rise to the excessive financialization of the entire real estate sector. High housing prices have begun to squeeze consumption, inhibit innovation, and weaken economic growth potential. The gap between urban and rural land prices and living standards has been widening, becoming one of the major obstacles to promoting common prosperity.

As a special factor of production, land has prominent features of being both monopoly goods and financial assets. China has a special dual land system that separates urban and rural land. Urban land for development is monopolized by local governments. Under the land leasehold system, the government charges a one-time rent for the right to use residential land for a 70-year period, and this rent becomes the most important component of the housing price. High land prices and high housing prices are mutually reinforcing and make banking credit a necessity, triggering the financial attribute of real estate. The pro-cyclicality of finance tends to mask problems or leads to real estate price bubbles and irrational market booms. The rising value of existing housing is mainly captured by a few groups such as home and land buyers, developers, and financial institutions, increasing the incentive for different actors in society as a whole to invest in the real estate market and further pushing up land and housing prices.

The financialization of land has been transmitted to the housing market, causing housing price to rise excessively without the support of the real economy. In this process, the ability of ordinary households to pay for housing has been weakening, while the incentive for high-net-worth groups to invest in speculation has been strengthening, further exacerbating the uneven distribution of housing resources. Moreover, the housing market has a biased supply structure that is dominated by developer-built housing but lacks enough low-income housing, and the rental market as well as its supporting mechanisms have yet to be developed. Especially in big cities, new residents and young people generally have difficulties in both purchasing and renting housing. In addition, the policy-driven housing finance system is still weak, and the supply of low-income and rental housing and the support for low- and middle-income households are both inadequate.

The excessive financialization of the real estate market has also caused the Chinese financial system to accumulate greater risk. The financing of real estate developers has relied more on debt than equity, and their business model—featuring high debt, high leverage, and high turnover—has led to serious debt risks. Many developers have also become major shareholders of local commercial banks, which enables them to leverage up much more aggressively than other industries and expand their capital in a disorderly manner until they are “too big to fail”.

In order to promote common prosperity, China should solve the various problems of the old development models in the real estate sector. Promoting high-quality, inclusive development of this sector is essentially a process of reducing excessive financialization, ensuring that the real demand is met and restoring the status of housing as an essential consumer product.

3.1 Excessive Financialization of China’s Land Market and Uneven Distribution of Land Rent

3.1.1 As a Factor of Production, Land Has Features of Being Both Monopoly Goods and Financial Assets

3.1.1.1 The Feature of Land as Monopoly Goods

The features of land as monopoly goods are primarily reflected in the determination of ownership. Unlike general capital goods, land ownership is more subject to political and legal influence. In times of peace and in a market economy, changes in land ownership and land use rights are mainly accomplished through market transactions. But unlike other capital goods, since the purchase and sale of land involve large sums of money, only a few people or enterprises with sufficient funding can purchase land.

The features of land as monopoly goods can amplify the negative externality to the economy as land prices rise. Among the three factors of production, i.e., labor, capital, and land, land is the most durable. Instead of promoting the formation of industrial capital, rising land rent or land price, which is part of the fixed cost of enterprise production and business operations, squeezes investment and reduces the supply capacity of the economy, thus increasing the divergence of wealth and capital.

3.1.1.2 The Features of Land as Financial Assets

The special status of land as a factor of production makes its valuation less objective and highly sensitive to interest rates. The lack of specific use and the uncertainty of future cash flows makes land price estimates less objective, and determined more by people’s psychological expectations (e.g., herding effect). Moreover, land is more durable than other productive capital, making its transaction price highly sensitive to interest rates. In addition, the high financial threshold for purchasing land often requires external financing, and buyers receiving the financing will have an advantage in land transactions and allocations. Factors affecting financing terms include credit ratings and the value of collateral. As land itself is high-quality collateral, large firms and individuals who own land tend to have an advantage in financing land purchases, resulting in an increasingly concentrated ownership of land.

Financing facilitates land transactions, and land used as collateral also promotes the expansion of financing. While collateral helps address information asymmetry in the financing process, it also reduces the willingness and incentive of lenders to do due diligence. Financing is based more on the availability and value of collateral rather than project viability and output efficiency. This gives rise to further disconnection between financial credit and the real economy. The over-expansion of debt may incur default and a deepening financial cycle spanning from real estate to credit supply.

3.1.2 Financialization and Uneven Distribution of Land Rent Increases Wealth Inequality

3.1.2.1 China’s Land Transfer Process

China practices socialist public ownership of land, i.e., national ownership and collective ownership by the working people. Land for urban development belongs to the state, while land in rural and suburban areas belongs to the rural collectives, except for land stipulated by law to be owned by the state; homesteads,Footnote 1 self-reserved land, and hills also belong to the rural collectives. Land can be granted to organizations or individuals for use, and land use rights can be transferred in accordance with the law. The state can expropriate land for public interest and compensate the owners of the expropriated land. In addition, there is a difference between the urban and rural land use systems in China. According to the 2004 version of the amended Land Management Law, in cities, “any unit or individual who needs to use land for construction must apply for the use of state-owned land in accordance with the law”. Rural land must be collected by the government before becoming tradable in the urban land market, and this rule did not change until 2020. This has led directly to the urban–rural dual structure of China’s land market in the past two decades.

The land transfer process in China involves land expropriation, government storage, transfer of land use rights, and market transactions of land use rights (Fig. 3.1):

Source CICC Research

Steps for transfer of land use rights in China.

-

At the stage of land expropriation, the compensation for urban land, rural homesteads, and collective land for development is based on the replacement cost, whereas owners of agricultural land should be compensated according to a multiple of land production value. The total compensation for owners of agricultural land comprises land compensation fee, compensation for local attachments and seedlings, resettlement subsidies, and social insurance fee. The land compensation fee belongs to the rural collective economic organization, whereas the other parts belong to the leasehold farmers. As urbanization advances and the amount of undeveloped urban land gradually diminishes, the amount of expropriated rural land has been increasing.

-

At the government storage stage, the land is mainly stored on behalf of the government through the land consolidation and reserve center,Footnote 2 a special agency, or directly bought by city investment companies. Because the land consolidation and reserve centers have no financing function, local governments grant the land storage function to city investment companies for rapid urbanization. The companies use the future returns from land use rights as collateral for financing and carry out land preparation and infrastructure investment. Since 2016, the land storage function of the companies has been gradually divested, but they are still responsible for the development and improvement of land already on their books.

-

In the primary and secondary transactions of land use rights, the government first offers well-developed land in the primary market. Commercial land is more often offered through auction and bidding at relatively high prices, while industrial land was more often offered in a non-market way before 2006 with large supply and low prices. In the secondary market, properties and land are usually traded and priced together, and after the payment of transaction and VAT fees, the net proceeds from the sale mostly go to the original holder of the land use rights. The features of land as being both monopoly goods and financial assets push up land prices, and rising land prices further increases the government’s net proceeds from land sales. The cost of land expropriation and demolition, however, has also gradually increased, and therefore, in recent years, it has become increasingly difficult for local governments to demolish and relocate old homes in urban centers.

3.1.2.2 Collection and Distribution of Land Rent

There are two imbalances in China’s land market:

First, the phenomena of over-compensation and under-compensation to the farmers from whom land is expropriated exist simultaneously. The difference between the two depends on the nature and location of the expropriated land. The compensation standard of land expropriation is mainly linked to the original land use and the surrounding land price. For example, in the case of homesteads in collective land, if it is located in an urban village, the compensation rate will be higher with reference to the surrounding urban land price; but if it is located in a suburban area, farmers will receive a lower compensation fee. The latter situation became more prevalent in recent years as more than 40% of land expropriated in China’s cities has been arable land,Footnote 3 mostly on the outskirts of cities. The Land Management Law in 2004 also stipulates that compensation for expropriated farmers cannot exceed 30 times the average annual land production value (though this ceiling was removed in 2019). This has led to disparate compensation for expropriated farmers, which in turn has led to uneven distribution of wealth. Moreover, since land has a certain social security function for farmers, the issue of their social security after losing land has not been properly addressed.

Second, the price difference between industrial land and commercial land is substantial. From an international comparison perspective, industrial land prices are lower than commercial and residential land prices in all countries, but the price difference between different sites in China is even greater (Fig. 3.2). Due to the high mobility of capital, enterprises can vote with their feet to choose where to locate their operations, and local governments tend to attract enterprises by supplying a large amount of land at low price. The practice may seem to damage local interests in the short term, but the employment opportunities provided by enterprises can effectively promote local economic growth, attract population inflow, and improve tax revenue in the medium term. Therefore, local governments have a natural urge to expand the supply of industrial land and reduce that of residential land. In the long run, the government makes a rational choice by offering industrial land at low price to attract investment, which creates employment and tax revenue. However, the low price of industrial land has certain negative effects, such as excessive competition and duplicate construction among local governments, low efficiency of land use, waste of resources, and crowding of urban living and ecological space.

Source CEIC, UK HM, CICC Research

Price of residential land is much higher than that of industrial land in China.

The reasons behind both of these aforementioned phenomena, which have given rise to increased wealth disparity among the population, are:

-

First, the excessive financialization of land. After 2002, auctions have become the main method of land transfer. The government charges a one-time rent for the right to use residential land for the next 70 years, which few people could pay in a lump sum. Most of them have to take out loans, thus exacerbating the features of land as a financial asset. The pro-cyclicality of finance conceals the problem, and leads to the price bubble and irrational prosperity in the market. Moreover, the government liquidates land assets or uses land as collateral for leveraged financial activities. Under the land financialization model, the level of land price directly determines the size of local financial resources. The proceeds from land use rights sales and taxes in China rose from Rmb3.3trn to Rmb10trn between 2010 and 2020, accounting for about 50% of total income of local governments. Since being included in the budget of local government-managed funds in 2007, the proceeds have been accounting for about 90% of total budget revenue. Because how much land prices can rise depends on property prices, the financialization of land means that property price is in fact linked to local balance sheets by determining land price. As a result, the financialization of land has thus evolved into an implicit guarantee provided by local authorities to the real estate sector, giving it an unfair competitive advantage over other industries.

-

Second, the distribution of land rents is not as reasonable as it should be. The value-added portion of land in the secondary market is mainly captured by a few groups such as land buyers and real estate developers. Financial institutions that provide land financing also benefit from the related business. The situation stimulates people’s incentive to invest in the housing market and pushes up land and housing prices further. The rise in urban housing price is mainly due to the rise in land price, which is backed by the increase in differential land rent mainly because of the improvement in surrounding public services such as education, transportation, and medical facilities. Such improvement results from government investment and has little relationship with the private sector. According to the theory of land rent, the increase in land rent due to such improvement should go to the government as a result. However, the lack of real estate tax makes the net benefit mostly go to homeowners. This exacerbates the wealth inequality within the household sector, because whether or not residents buy homes and how soon they do so affect the distribution of wealth.

-

Third, the infrastructure investment boom in the urbanization process may suppress the supply of residential land. In the case of limited government debt, it is probable that local governments may weigh in favor of industrial land supply but against that of commercial land, which then leads to higher monopoly land rents. In addition, China’s regional land supply has favored the central and western parts of the country since 2003, and land constraints in the eastern region have intensified, pushing up the price of residential land there. In recent years, China has started to implement relevant reforms in coordinating land supply between regions, emphasizing market-based supply of industrial land, and raising the proportion of residential land supply.

-

Fourth, the strengthening connections between real estate enterprises and banks have created a financial “binge” for some real estate enterprises, giving rise to significant financial risk. China’s new homes are normally sold for future delivery. Developers therefore operate with high leverage, high turnover, and high profitability, which has not only boosted land prices but also increased risks. Developers also participate in bank operations, which is a problem particularly prominent at municipal commercial banks. In addition to being a major shareholder of banks, some real estate enterprises also issue wealth management products. As the government offers explicit guarantees for banks, the close connections between banks and real estate companies means that the latter also have de facto access to the government’s financial safety net. This may further enhance their unfair competitive advantage over other industries by allowing them to leverage up much more aggressively than other industries until they are “too big to fail”.

If the problem of unreasonable distribution of land rent is solved, the features of land as a financial asset should be reduced and a real estate tax should be imposed. If the proceeds from the sale of land use rights is viewed as a tax, the regressive nature of the entire tax system may deepen further and worsen social wealth inequality when urban residential land prices continue to rise. The government efforts to tax the real estate are not sufficient now (Fig. 3.3). The tax should reduce local governments’ reliance on land proceeds and enable the government to gain a major portion of land appreciation brought through public service provision. The government can redistribute the tax to alleviate the uneven wealth distribution. In addition, it is necessary to build a unified land market in urban and rural areas; to focus on the reasonable distribution of land appreciation income among the government, collectives, and farmers; and to explore more ways for farmers to continuously benefit from economic and social development with their land equity.

Source Wind, CICC Research

Most of Chinese government’s land rents are derived from land transactions. Note Chinese government collects land rent from: (1) Sale of land-use rights; (2) tax on land transaction including value-added tax, contract tax, farmland use tax; (3) tax on land possession including property tax (mainly on business properties), urban land utilization tax.

3.2 Housing Market: Imbalanced Resource Distribution and an Imperative Need to Restore the Status of Housing as a Consumer Product

3.2.1 Major Problems in China’s Housing Market

3.2.1.1 Imbalance in Housing Distribution

Housing is an essential consumer product. Excessive increase in housing price has led to a continued erosion of affordability of housing. New residents, young people, and other groups in large cities face difficulties in solving the problem in a market-based way, whereas the older generation occupies more properties. Rising housing prices have led to a growing imbalance and widened the gap between urban and rural residents’ housing assets, with urban residents enjoying much more housing value per capita than their rural peers in 2019,Footnote 4 according to our calculation. The distribution of housing resources is the most important indicator of housing inequality, as measured by the 2017 China Household Financial Survey (CHFS),Footnote 5 which shows that:

-

The imbalance seems to be low in terms of the number of housing units. In terms of the number of units owned by urban households within the country’s towns (Fig. 3.4), 13% of urban households do not own a housing unit, 69% own one, and 18% own two or more. The average ratio of the number of housing units to the number of households is 1.10 (similar to that of mature markets overseas) and the Gini coefficient of the number of units is 0.27, indicating fairly balanced distribution. If we only count the housing in towns and cities where people currently live (not considering their housing in other towns and cities), the concentration of distribution would rise, with about 16% owning no housing unit, 66% owning one, and 18% owning two or more. The average ratio of the number of housing units to the number of households would be 1.03, indicating a slight supply shortage based on the experience of mature markets that tend to see relatively stable housing prices with a reasonable vacancy rate of 10–15%.

Fig. 3.4

Source 2017 CHFS, CICC Research

More than 10% of households own no housing; about 20% own at least two homes.

-

The distribution of housing area and value is more uneven. The Gini coefficients for the floor area, market value, and disposable income of households are 0.48, 0.72, and 0.54, respectively, with the wealthiest 10% of households owning one-third of the total housing floor area and 40% of the total household income, and the bottom 50% owning only about 20% of the floor area and market value, as well as 20% of the total income.

-

The possession of housing resources (and purchase leverage) is highly correlated with income level. Because housing price kept rising in the past decade and there is no real estate tax, housing has become an important means of investment for high-income households. “Buy-to-let” and hoarding of housing resources have led to a continuous pooling of housing resources to high-income households. We measured the housing resource possession of households in different income groups in 2017, and found out that the top 1% and 10% wealthiest households owned 3.1 and 2.2 housing units on average (Fig. 3.5). In terms of level of leverage, the bottom 20% of households have a borrowing balance equivalent to 46% of the total housing value, while the percentage for the highest 20% income group is 14%. Debt repayment pressure is also significantly negatively correlated with income level, with the ratio of borrowing balance to average disposable income standing at 4.5 times and 1.5 times for the lowest and highest income groups, respectively.

Fig. 3.5

Source 2017 CHFS, CICC Research

High-income households own more homes than low-income ones.

3.2.1.2 Difficulty in Meeting Demand for Rental Housing

Demand for rental housing in China’s major cities is strong, but the market is unable provide high-quality and stable supply of rental housing. According to our estimation, by the end of 2021, the number of urban renters exceeded 200 mn people, concentrated in the eastern coastal city clusters and regional hub cities. The concentration rates of the top 10, 30, and 50 biggest cities were 31%, 49%, and 59%, respectively. However, from the supply side, the market and supporting system are relatively underdeveloped, which makes it more difficult for new residents, young people, and other groups to find a place to live in big cities.

-

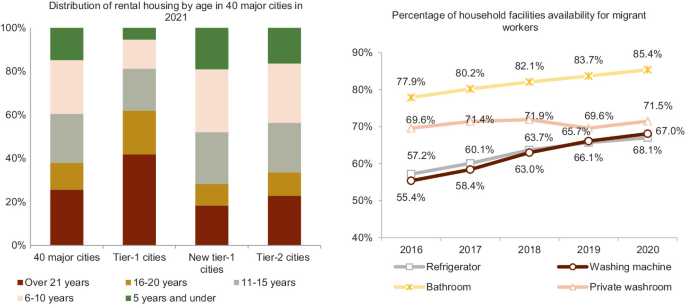

The living environment is crowded, and the quality of old housing is declining. The total housing supply is insufficient, which makes it difficult for renters to live in a decent way. According to the 2015 statistical census data and our estimation, the per capita living area of urban rental households is less than 27 m2, only 60% of that of home-owning households (Fig. 3.6). In cities where the demand for rental housing is strong, the difference in living environment between renters and owners is even greater. Moreover, the existing housing stock is old and lacks living facilities, and tend to be of poor quality. The average age of rental housing in tier-1 and new tier-1 cities is 18 and 12 years, and the proportion of houses built before 2000 is over 40%. About 30% of the housing rented by migrant workers lack basic living facilities such as refrigerators, washing machines, and independent toilets (Fig. 3.7).

Fig. 3.6

Source National Bureau of Statistics, CICC Research

Rental housing is usually crowed, especially in cities with a higher percentage of renters.

Fig. 3.7

Source BeiKe Holdings, National Bureau of Statistics, CICC Research

Rental housing is usually old and lacks household facilities.

-

Second, the rights and interests of tenants are not effectively protected. Influenced by supply and demand, the rental housing market shows certain characteristics of a seller’s market. Tenants generally lack bargaining power and bear many risks of breach of contract, and violations of rights and interests occur frequently, typically including arbitrary rent increases, early termination of contracts, non-refundable or less refundable deposits after expiration of contracts, and lack of repair and maintenance services for indoor facilities. Therefore, it is difficult for renters to live comfortably and sustainably. According to statistics from the Anjuke Research Institute, about 40% of tenant groups experienced infringement incidents in 2020.

-

Third, renters do not have the same access to social public services as homeowners. The price of housing not only includes the value of residential use, but also involves the capitalization of access to education, medical care, and other public services. The household registration system is linked to social public resources, resulting in most renters not enjoying the same public services as homeowners (i.e., “different rights for the same residence”), and problems relating to their children’s education, and their basic medical care and social security are more prominent.

3.2.1.3 The Quality of Old Housing Is Deteriorating

With the decline in basic functions (including residence, employment, consumption, etc.), areas that developed decades ago may have difficulty in meeting the daily work and living requirements of local residents. According to a Ministry of Housing and Construction announcement, in 2020, the country had approximately 170,000 old districts to be renovated, with a total construction area of approximately 4bn sqm, involving 42 mn households.Footnote 6 According to the small-scale census data from the National Bureau of Statistics, in 2015, it was estimated that about 50% of the urban housing stock was built before 2000, dominated by residents’ self-built properties and public housing. Considering the scale of new housing supply and demolition of old housing in recent years, the stock of housing aged over 20 years accounted for 30% of the total area (8–10 bn sqm) by the end of 2021, of which “old villages”, “old factories”, and “old commercial districts” occupied at least 3–4bn square meters, involving 30–40 mn households.

There are hidden dangers in old houses and incomplete housing facilities. On the one hand, due to the low construction standard, unreasonable design, low quality of some construction materials, and the lack of professional property management services, some of the older housing stock has been exposed to quality and safety hazards, such as aging of pipelines and settlement of the main structure. On the other hand, since urban construction is carried out in neighborhoods, the problem of old cities is not only a decline in the quality of housing in individual neighborhoods, but also an overall decline in the basic functions of the neighborhoods in which they are located, such as deterioration of the living environment, damage to municipal facilities, abandonment of factories and shopping streets, and relocation of public facilities (such as education and medical care), which reduces the livability of the neighborhoods.

Moreover, older communities tend not to be age-friendly. At the individual home level, there are many indoor thresholds, poor air circulation, and a lack of facilities to help the elderly; at the community level, there are a shortage of elevators installed, obstacles in the front space of the building (such as floor locks and flying wires), and a lack of home care and community dining services for single elderly or physically disabled elderly.

3.2.1.4 Relative Lag in Development of Housing Finance

China’s real estate financial system emerged simultaneously with the housing market reform. Development loans and mortgage loans were created to solve the problem of insufficient housing supply and affordability. However, the level of financial services and the variety of financial products today have yet to improve. The problem of the relatively lagging development of the housing financial system is reflected on both the supply and demand sides of the market.

From the demand side, low- and middle-income households lack financial support to buy homes. To guard against financial risk, the down payment threshold for mortgage loans is high, with an average actual down payment ratio of 50–60% because of limited mortgage quotas. Middle and low-middle income households need to turn to private lending, which involve higher cost and risk, while high-income households are more advantaged. The situation exacerbates the uneven distribution of housing resources. According to our calculation, among all of the households that borrow to purchase housing, over 70% of the households holding the 0–20% and 20–40% percentile of the home market value in 2017 have sought private lending, creating leverage of 36% and 18%, respectively. In contrast, only 19% of the highest percentile group (80–100%) have used private lending, corresponding to leverage of about 2% (Fig. 3.8).

Source 2017 CHFS, CICC Research

Households with low housing asset value tend to purchase housing with more private lending, and thus bear a higher leverage ratio.

From the supply side, the fiscal support for housing finance is insufficient, while corporate financing of developers relies more on debt than equity. Low-income housing is the main category in the supply system for serving low- and middle-income families. At present, the policy-based housing finance system for the investment and financing of low-income housing remains weak. In addition, real estate enterprises are increasingly reliant on debt financing because of limited access to equity financing. The business model of borrowing money with short maturity for medium- and long-term investment has led to the high debt, high leverage, and high turnover for real estate companies. This has also increased their vulnerability to the industry slowdown and increased debt pressure.

3.2.2 Restoring the Attribute of Housing as a Consumer Product

3.2.2.1 Building a Stratified Supply Ladder of Housing Products

The current situation of housing inequality reflects, to a large extent, the contradiction between diversified demand and a supply structure dominated by developer-built housing. While bridging the gap between supply and demand, efforts should be made to deepen the reform of the housing supply structure, realize sufficient stratification on the supply side to build a ladder of housing products, and guarantee the basic rights of residents to live decently.

Two aspects are worthy of attention. First, focusing on the development of a multi-level and continuous housing supply system. The multi-level property supply is reflected in two dimensions. The first is the balanced development of rental and for-sale housing sub-markets, and the second is a balance between market-oriented and low-income products. The continuous housing supply reflects that housing products, whether for rent or sale, should be abundant enough to realize the transition from pure low-income housing supply to pure market-oriented housing supply. Second, a fully stratified supply system must meet the housing needs of different individuals during their life-cycles. From a static perspective, the supply system should be able to meet the reasonable needs of households with different affordability levels and preferences for renting and purchasing homes. More importantly, from a dynamic perspective, as their consumption power increases, people can independently choose different upgrade patterns of housing products.

3.2.2.2 Establishing a Real Estate Tax System

Real estate tax is prevalent in major developed countries, and provides a source of fiscal revenue and helps curb housing speculation too. Solving the land and housing problems in China entails a tax system targeting housing possession, which is important for the long-term development of the housing market. Taxes on housing possession mainly include real estate tax, vacancy tax, and inheritance tax, among which real estate tax is the most common, the most discussed, and the least controversial in economics. It can improve the structure of housing possession and realize the secondary distribution of wealth.

Real estate tax can also help promote the reform of local governments’ fiscal system and reduce their dependence on land finance. As the focus of China’s urban development gradually shifts from green-field development to long-term renewal and maintenance, it is difficult for local governments to maintain their finance through large-scale transfer of land use rights. Taxes on real estate ownership, which are difficult to hide, are counter-cyclical, and have a large tax base, may become a reliable source of revenue for local governments and promote the reform of the fiscal system that reduces the dependence on land finance. In addition, the standardization of real estate tax collection and management may facilitate the functional transformation of local governments. They may invest more resources in improving public services and maintaining infrastructure in order to obtain a sufficient tax base, and the positive feedback from real estate tax to public expenditure and then to population migration will reward city governments with superior management capabilities. The concern is that this may aggravate the financial and economic disparities among different regions, and it remains to be explored whether or not to establish a mechanism for the redistribution of real estate tax among them to reduce disparities.

3.2.2.3 Developing the Rental Housing Market and Strengthening Legal Protection

The shortage of rental housing supply in large cities is essentially a problem of the housing supply structure amid the total shortage of housing supply. The supply channels of rental housing include individual rentals, informal housing (such as urban villages and work sheds), business-run apartments, and government-provided housing. More than 80% of the current supply relies on the transfer of unused housing resources. This structure creates a “trickle-down effect”, i.e., families may satisfy their own needs before releasing housing of poor quality and location to the rental market, which may amplify the problem of insufficient rental supply in large cities. Continuous expansion of the rental housing market is the key direction of China’s housing policy, which focuses on adjusting the housing supply structure while supplementing the supply.

From a long-term perspective, protecting the rights and interests of tenants is as important as supplementing supply, which is a key aspect affecting the development of the rental housing market. In order to offer affordable and stable housing for tenants, it is necessary to adjust the relationship between the rights and obligations of the parties concerned through special legislation and protect the rights and interests of tenants sufficiently.

3.2.2.4 Accelerating Sustainable Urban Renewal

A long cycle of urban renewal, high financial pressure, and the difficulty in aligning the interests of different parties are the main challenges faced by urban renewal work, but there are still successful cases of urban renewal and renovation. The UK government established a special fund to support urban renewal in 2001, and regularly injects capital into the fund through the fiscal budget. According to the profitability of the projects and the need to implement the projects, the fund provides full subsidies, low-interest loans, and equity investment to attract social capital. At the same time, a multi-party partnership model involving community residents, social capital, and the public sector has been established, and the degree of participation of residents and the degree of public–private partnership are important selection indicators to consider at the bidding stage.

In order to accelerate the promotion of urban renewal and renovation, we believe it is necessary to pay attention to asset-light operation and accelerate the cultivation of large-scale operators by reducing taxes and fees and providing renovation subsidies. It is also necessary to emphasize the role of industrial development in promoting urban renewal, to pay attention to restoring the original employment function of industrial development, and to bring into play the industrial promotion ability of urban renewal enterprises, in our view.

3.2.2.5 Improving the Policy-Based Housing Finance System

We believe that while promoting the stratification of the housing supply structure, a multi-level finance system should be established to meet the reasonable demand of households with different income levels. China’s housing finance framework should be a multi-level system that combines open commercial finance and closed policy-based finance. The former should be the main channel, with the latter serving as a supplement.

To sum up, solving problems in the real estate market to promote common prosperity is essentially a process of exploring a new development model for the real estate market. The key is to curb excessive financialization and to restore the status of housing as an essential consumer product. Potential solutions include rationalizing the land pricing mechanism, implementing real estate tax, building a ladder of housing products, and promoting the reform of the financial sector. In order to fundamentally reverse the excessive financialization of real estate, it is necessary to resolutely curb investment and speculative demand and to push ahead on supply-side reforms which include de-financializing the land market and accelerating the implementation of real estate tax. Moreover, the real estate market is facing the challenge of resolving the debt risk accumulated from excessive financialization. We need to find effective ways to accelerate the resolution of the debt problems of real estate enterprises and urban investment companies.

Notes

- 1.

Rural homestead is a special kind of land reserved for rural household or individual to use as residential base.

- 2.

Land reserve refers to the act of organizing pre-development and storage for future land supply. The land consolidation and reserve centers undertake the specific implementation of land reserve work.

- 3.

Ministry of Housing and Urban–Rural Development, P.R. China [1].

- 4.

The per capita value of properties owned by urban and rural residents in 2019 was Rmb370,000 and Rmb59,000, respectively.

- 5.

This comprises three major databases on Chinese households, small and micro enterprises, and urban and rural community governance. The fourth-round survey samples in 2017 covers 29 provinces, 355 counties, and 1428 village across China, with a sample size of 40,011 households.

- 6.

People’s Daily Overseas Edition [2].

References

Ministry of Housing and Urban-Rural Development, P.R. China. (2020). China urban construction statistical yearbook 2020 (in Chinese). https://www.mohurd.gov.cn/file/2021/20211012/f88e6161ebf4bcbd4ffde8d1e9b64f0e.xls?n=2020%E5%B9%B4%E5%9F%8E%E5%B8%82%E5%BB%BA%E8%AE%BE%E7%BB%9F%E8%AE%A1%E5%B9%B4%E9%89%B4

People’s Daily Overseas Edition. (2019, July 3). 170,000 old communities will be renovated. People’s Daily. http://www.gov.cn/xinwen/2019-07/03/content_5405506.htm

Author information

Authors and Affiliations

Consortia

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License (http://creativecommons.org/licenses/by-nc-nd/4.0/), which permits any noncommercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if you modified the licensed material. You do not have permission under this license to share adapted material derived from this chapter or parts of it.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2024 The Author(s)

About this chapter

Cite this chapter

CICC Research, CICC Global Institute. (2024). Real Estate: Returning to Real Demand and Reducing Excessive Financialization. In: Building an Olive-Shaped Society . Springer, Singapore. https://doi.org/10.1007/978-981-97-0804-8_3

Download citation

DOI: https://doi.org/10.1007/978-981-97-0804-8_3

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-97-0803-1

Online ISBN: 978-981-97-0804-8

eBook Packages: Economics and FinanceEconomics and Finance (R0)