Abstract

This chapter focus on the experience of the Bank Indonesia (BI) in implementing policy mix after the GFC between 2008 and 2015. It elaborates the policy challenges and policy responses that BI undertook given complex challenges in the aftermath of the GFC. Under BI's policy mix response, the integration of monetary and macroprudential policy provides better results in terms of mitigating excessive macroeconomic and financial sector fluctuations compared to any single policy instrument.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

Introduction

This chapter is designed to give a prelude to tomorrow's policy simulation exercise. This relates to our experience after the global financial crisis between 2008 and 2015. The data that we will be using in this presentation is up to 2015. The presentation will be divided into four main areas. We will begin by providing the policy context before discussing the policy challenges and policy discussions in the aftermath of the global financial crisis that we at bank Indonesia undertook, given the policy challenges at that time. We will then discuss the policy responses and close by offering some conclusions.

As will be discussed, against the backdrop of a dynamic global environment, the multitude of challenges confronting the Indonesian economy demanded a policy mix response utilizing multiple instruments. Consequently, we allowed our inflation targeting framework to become more flexible than standard ITF in terms of managing monetary and financial stability in Indonesia. Under Bank Indonesia's policy mix response, the integration of monetary and macroprudential policy provides better results in terms of mitigating excessive macroeconomic and financial sector fluctuations compared to any single policy instrument. A lot of the material in this presentation has been borrowed heavily from the main references listed here.Footnote 1

Policy Context

Global

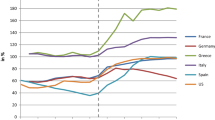

In 2008, the sub-prime mortgage default sent shockwaves of heightened counterparty risk in the global financial markets. Starting in the US financial markets, the counterparty risk increased, which drained liquidity, especially in the money markets. The resulting impact was that firms had limited access to credit and as a result, economic growth and economic transactions slowed down significantly, not only in the US but also in the European Union and other advanced economies, with spillover to emerging market economies, including Indonesia. There was a synchronized slowdown/recession in the global economy. In the aftermath of the global financial crisis, we observed boom-bust cycles in the global economy. Many explanations have been put forward why such boom-bust cycles could take place. One plausible explanation is that the structural policy measures, which are very important to address the underlying fundamental problems related to crises, were lagging behind the cyclical measures and, hence, the boom- bust cycles of economic activity appeared along the long-run trajectory. Relating to the boom-bust economic cycles were the global commodity price cycles (Figs. 8.1 and 8.2). I have put global commodity price cycles here because this relates very strongly with the Indonesian case because we are a commodity producing exporter. Some of you may remember, this was called the commodity super cycle. The cycle started early in the year 2000, in the aftermath of China’s admission to the World Trade Organization. The Chinese economy subsequently expanded and with the expansion, demand for commodities increased, triggering a commodity super cycle. Fuelling this commodity super cycle as well was the Great Moderation in advanced economies as well as the US, where inflation was quite low, which prompted the Federal Reserve to loosen its monetary policy for a prolonged period of time. That also fueled the commodity price boom. This ended during the global financial crisis.

Source IMF-WEO database and World Bank

World economic growth.

Global commodity prices index

Conditions recovered but given the sluggishness in the global economic recovery, and a permanent slowdown in the Chinese economy, we saw that commodity prices slowly went down afterwards. This is important because our current account, which also records our trade balance, depends heavily on the commodity cycle. In response to this fear of a growth slowdown and the threat of deflation as well as to avoid a repeat of the Great Depression, the Federal Reserve, the US monetary authority, embarked on an unprecedented policy, namely quantitative easing (QE). More recently, this has become quantitative tightening but in the aftermath of the global financial crisis in 2009–2010, the Federal Reserve implemented quantitative easing. This amounted to the printing of US dollars. The Fed was printing money by purchasing assets, not only from financial corporations but also non-financial corporations. That created excess liquidity, as intended, which lowered yields and the Fed Funds Rate but increased the asset side of the Federal Reserve's balance sheet (Figs. 8.3 and 8.4). When the asset side of the Federal Reserve's balance sheet increases, it means the bank is printing money. The Fed added extra US dollar liquidity into the US economy. The idea was that the excess liquidity would, in turn, reflate the US economy and avoid a prolonged recession along with the threat of deflation. Nevertheless, the quantitative easing had a spillover effect on the global economy in the form of large and volatile capital flows. The money permeated into many corners of the global financial markets, including emerging market economies and Indonesia. That is the global context of where we found ourselves in the aftermath of the global financial crisis from 2008–2010.

Source US Federal Reserve; FRED database

US monetary policy and global risk.

Unconventional monetary policy (balance sheet of fed)

Domestic

With the dynamics of the global financial markets and global economy together with the heightened uncertainty that went with it, as a small and very open economy with strong integration in the global financial market, how did Indonesia fair? What were the key risk factors the policy authorities had to cope with in the aftermath of the global financial crisis? Those were the questions in the back of our minds as policymakers in Indonesia at that time. Actually, we found that inflation in Indonesia, at that time, was quite manageable. The disinflation path continued. An excepting a few episodes where administered prices went up, inflation in Indonesia remained around the target corridor. The higher administered prices typically related to government fiscal reform in the area of subsidies. For example, the government lifted the product-based subsidies on energy and used the money for people-based subsidies, such as education. This was part of the fiscal consolidation policy of the government and fiscal reform. The shaded area on the graph (Fig. 8.5) represents the target range of headline inflation set jointly by the government and central bank. Looking at the components of CPI inflation, core inflation (blue line) remained within the target range, even during periods of rising administered prices (Fig. 8.6). The fact that core inflation was maintained within the target corridor set by the government and Bank Indonesia suggests that monetary policy was able to limit the second-round effect of price shocks to inflation. This demonstrates the credibility gains of monetary policy in terms of information management. Bank Indonesia was happy with this outcome. It suggested that monetary policy had gained credibility. The question then becomes how to secure the credibility gains given the risk factors affecting the Indonesian economy in the aftermath of the global financial crisis? Most of the risks related to increasing macro vulnerability in the aftermath of the global financial crisis. In 2009–2010, Indonesia's balance of payments enjoyed a current account surplus most of the time before starting to decline into a deficit in 2011–2012. This relates to the commodity price bust because a significant portion of our exports are commodity based, such as crude palm oil (CPO), coal, nickel and so on. That was the first macro vulnerability we observed. In 2012–2013, the current account deficit widened and started to constrain economic growth in Indonesia, thereby increasing economic vulnerability in the country. GDP growth remained solid at around 5%, however, which sustained the confidence of investors in the global financial markets (Fig. 8.7). Therefore, investors kept buying Indonesian securities, which financed our current account deficit through the capital and financial account. At that time, the capital and financial account recorded large surpluses. The balance thus reflected an external posture. We saw increasing vulnerability in terms of our current account, but we were able to finance the current account through the capital and financial account, especially portfolio flows, thanks to quantitative easing. A lot of the money flowed from the US through the global financial markets, such as wholesale funding and local currency bonds in emerging markets, due to the spillover impact of quantitative easing. Consequently, we were able to finance our current account deficit (Fig. 8.8).

Indonesia inflation: headline CPI

Indonesia inflation by component CPI

Indonesia GDP growth

Indonesia inflation by component CPI

Notwithstanding, such conditions brought other risks because capital flows are prone to volatility and shifts in investor sentiment or expectations about the stance of global monetary policy and the relative parity of interest rates between the home country and the host country, for instance. Figure 8.9 shows the composition of instruments in the capital and financial account flows. The flows were dominated by the bond market and equity market, mostly investors buying Indonesian local currency government bonds. The chart shows that shifts in investor confidence, for example during the euro crisis in 2011, precipitated a drop in the capital and financial account, meaning that capital flowed out of Indonesia. The flows would subsequently resume before another shock, this time the Taper Tantrum, would trigger more capital outflows. The Taper Tantrum was prompted by a statement issued by Ben Bernanke concerning the Fed’s upcoming plan to normalize monetary policy. This spurred a portfolio adjustment by global investors, which affected our financial markets as capital flowed out of the country. This happened again in 2015 when the Fed actually began normalizing its monetary policy and reducing its balance sheet.

Source BI; ADB

Indonesia: capital and financial flow.

As of 2015, around 40% of Indonesia's local currency government bonds were held by global investors and, hence, prone to shifts in market expectations (Fig. 8.10). It helped us finance our current account deficit but there were risks associated with it. There is always a trade-off in terms of policy; a policy dilemma that is encountered. Another policy issue/dilemma was to avoid boom-bust cycles, where the real sector and financial sector tend to move in a pro-cyclical way. When an economy is booming, credit is also booming (Fig. 8.11).

Foreign holding of local currency government bond

Source BI

Indonesia: domestic credit.

When the business cycle begins to decline, the financial cycle is still increasing and that is something to be avoided because rapid credit growth (boom) will eventually bust because, as with the experience of advanced economies before the global financial crisis, a rapid credit boom masks the concentration of risk, making it unobservable. This can catch policymakers off-guard. There is uncertainty with regards to where the concentration of risk is.

Policy Challenges and Discussion

Policy Challenges

That was the global and domestic policy context but what are the policy challenges? I have distilled all the dynamics of the domestic and global economies into this one matrix (Fig. 8.12). There are four episodes, namely 2008–2009, 2010–2011, 2012–2013 and 2014–2015. Monetary stability is on the y-axis and financial stability on the x-axis. With monetary stability, you have high inflation, implying a period of growing risk to price stability, and low inflation where the risks to price stability are actually subdued. In terms of financial stability, there is high credit growth that usually increases the concentration of risk due to lower lending standards, and also low credit growth. This matrix is important as later on we will see what kind of policies should be used in each of these episodes.

Policy challenges in four different time

This chart presents another way of looking at the policy challenges, which was our way of thinking at that time. We are an inflation targeting country, and our target is inflation, but we have dual objectives. However, there would be no price stability without financial system stability. To maintain macroeconomic stability, financial system stability is also required. Macroeconomic stability is our mandate, but we also have to consider financial stability as well because the real sector and the financial sector tend to behave in tandem in a pro-cyclical way. Pro-cyclicality usually embodies risk-taking behavior. This is usually a source of risk concentration and functions as a financial accelerator. Risk-taking behavior is also influenced by the dynamics of the global environment, particularly the world interest rate or global capital flows. When interest rates in advanced economies are low, namely an accommodative monetary policy stance, it means they are printing money. Risk-taking behavior will consequently affect us in the domestic economy because Indonesia is a small open economy and well-integrated into the global capital markets because we issue bonds that can be purchased by foreigners, which we need in order to finance our current account deficit. Basically, we need to finance our development.

In 2011, when we published the Indonesia Economic Report for 2010, the terms ‘policy trilemma’ and ‘policy mix’ were used in our press release because they featured very much in our thinking in 2010. We have the classic Mundell Trilemma, which says that as a country, you want access to the global capital and credit markets but if you want access, you have to allow the exchange rate to float, namely you cannot control your exchange rate, and you have to somehow let your monetary policy adjust to shifts in global sentiment. This means that the reaction function of monetary policy must be allowed to be a function of other central banks’ reaction function. This means that if the Federal Reserve is thinking of raising its interest rate, other central banks may have to follow suit in response. Parity must be maintained along with the competitiveness of your financial instruments. Nevertheless, that would make us prone to exchange rate and financial market volatility. There is another trilemma, known as the Financial Trilemma, and the concept was first introduced in 2011 by Schoenmaker (2011) (Fig. 8.13). It has also appeared in the International Journal of Central Banking. According to the Financial Trilemma, if a central bank desires financial integration (access to global capital and credit markets), it must follow the rules or regulatory regimes that have international standards. The authorities must be disciplined not to follow discretionary local rules. For example, Basel III implementation safeguards the financial system from potential risks to financial stability, but some policy autonomy is lost in terms of setting your own national policy. There is another trilemma, known as the Governance Trilemma. If you want your rule to be universal and democratic, you cannot have effective rules. A good example of this is the United Nations, a democratic institution with universal coverage but somewhat ineffective.

Source Schoenmaker (2011)

Financial Trilemma.

Policy Discussion: Managing Capital Flows

Another theme in our discussion was how to manage capital flows. In 2011–2012, the main message coming out of the IMF and World Bank was about capital flows. It is a question of how to handle capital surges and capital inflows. During 2011–2013, a lot of capital was flowing to emerging markets. We were the recipients of large capital inflows. This triggered macroeconomic concerns. First, the national economy may overheat due to excess liquidity. Second, we might lose competitiveness because our exchange rate is appreciating. Most central banks manage this by accumulating foreign reserves but this incurs a sterilization cost.

Those are the macroeconomic concerns but there are also financial stability risks because a credit boom usually carries with it concentration risk and the potential for asset price bubbles. Hence, to manage capital surges, the idea was first to implement consistent macroeconomic policies and prudential policies. This should be the central bank's primary response. Then, you mitigate the risk through capital flow management, which is a sort of capital control. There is a question about whether you are willing to implement capital controls and how stringent they should be. That forms part of the discussion too and, ultimately, we decided against it because we did not know what the investor reaction would be. That would represent a significant change in regime. Instead, what we decided was to implement the primary response, namely macro policies and prudential policies, because during periods of capital inflow, higher interest rates would actually increase the inflows even more. Macroprudential policies helped us because it placed less burden on our primary instrument, the policy rate.

Monetary Policy Versus Macroprudential Policy

Macroprudential policy can be used to support monetary policy in order to curb credit in certain sectors without raising the interest rate. Macroprudential policy addresses risks to the financial system caused by a weakening of financial conditions, financial and sectoral imbalances as well as imprudent behavior and so on. On the other hand, monetary policy addresses the risks associated with economic growth, inflation, current account deficits and exchange rates. Both sets of risks are interrelated (interconnected) but require different policies to address the risks. Furthermore, monetary and macroprudential policies may conflict from time to time, implying a trade-off. For example, during asset price bubbles, credit must be squeezed through higher interest rates. If such a situation is accompanied by low inflation, however, it could contract the economy even more and inflation would be too low, even below the target, but higher interest rates would attract more capital flows. These are the trade-offs that must be considered, such as tighter monetary policy through higher reserve requirements to reduce exchange rate pressures could create liquidity problems for banks or macroprudential policy which requires high capital to maintain the stability of the financial system could hamper economic growth (aggregate demand) or a loose monetary policy that encourages growth may lead to excessive credit expansion and financial instability.

Policy Discussion

In a nutshell, increasing global financial market integration and large capital flows prompted the monetary authority to shift away from corner solutions towards a middle solution with regards to the trilemma, making the impossible trinity possible. That was the joke at the time, how to make the impossible trilemma possible? Hence, the need emerged for a more flexible and refined inflation targeting framework (ITF). Pure ITF only cares about inflation but that would have been too simplistic for us as a small open economy.

Policy Response

Our policy response was to integrate monetary and macroprudential policy, with a view that there is no macroeconomic stability without financial system stability. That was our main justification. Economic dynamics during financial crises have shown that monetary policy needs to be further directed to anticipate macroeconomic instability risk stemming from the financial system. The central bank needs to strengthen the framework of monetary and financial system stability, which requires monetary and macroprudential policy integration. The goal of macroprudential policy is to guarantee financial system resilience as a whole in a bid to support financial intermediation.

Bank Indonesia Policy Mix

In 2008–2009, Bank Indonesia maintained accommodative monetary and macroprudential policy. In fact, macroprudential policies were around before the term ‘macroprudential policy’ was invented. Some of the prudential regulations were macroprudential in nature. In 2008–2009, some of the elements of macroprudential policy were already there. The overall stance of monetary and macroprudential policy was loosening/accommodative. During the period of capital inflows from 2010–2011, we could not raise the interest rate even though, at that time, we saw rising credit growth, which could feed into inflation down the road. Therefore, we implemented macroprudential policy. Simultaneously, we loosened monetary policy and tightened macroprudential policy. In 2012–2013, we experienced inflation shocks. There was a shortage of basic food necessities at that time along with productivity shocks. Consequently, inflation began to rise. As the monetary authority, we could not let that hike in inflation feed through into the inflation expectations and cause second-round effects on the overall price level. In response, we tightened our monetary policy stance, while the macroprudential policy stance remained tight. In 2014–2015, when we saw that credit growth had already begun to decline and we were happy there was no boom or sudden bust in the credit growth, namely there was a smooth transition from rapid credit growth to slower credit growth, we relaxed our macroprudential policy stance.

Optimal Policy Response

In 2010–2011, rapid capital inflows led to excess liquidity and the commodity super-cycle prompted a capital account surplus. Therefore, we implemented a mixed policy response by letting exchange rates appreciate, accumulating reserve assets, increasing the reserve requirement to mitigate the impact of US dollars flowing into the domestic economy, including the foreign exchange reserve requirement, implementing a 6-month holding period for investors buying central bank bills and a net open position to limit banks from having wholesale funding from the markets to only 30% of capital. Foreign exchange exposure up to 30% of capital was permitted. Now we are experiencing capital outflows, we have relaxed the holding period but at that time we required investors to hold their position for at least six months.

In 2012–2013, we allowed our exchange rate to be more flexible as capital outflows prompted rupiah depreciation. We also conducted dual intervention. To ensure the financial system was not deprived of liquidity, however, we purchased government bonds in the secondary market. We also tightened the LTV rules because there were concerns about banks allocating too much credit to the property sector and also to households to purchase property and motorcycles. In Indonesia, motorcycles are everywhere, which is partly a legacy of this era of easy access to finance. Some of these loans to purchase motorcycles were sub-prime. We also introduced a loan-to-deposit ratio linked to the reserve requirements. We had a range for our LDR of 80- 92% at that time. Below 80%, we would punish the banks for not lending to people and so the excess would be put towards the reserve requirement. Above 92%, we would punish the banks for being a risk taker. This was an LDR-linked RR, which can be tightened or loosened as required.

In 2014, we introduced another regulation relating to rising private external debt. A lot of Indonesian non-bank corporations were financing their activities through private debt. We did not like this trend due to the risks that would emerge from global shocks, leading to volatility in the financial markets. Therefore, we required non-financial corporations to hedge their foreign exchange exposures. In general, our policy response was a mixture of allowing the exchange rate to be more flexible at times through dual intervention and accumulating reserve assets, and the Bank Indonesia policy rate. We tried to balance the three indicators of international reserves, exchange rates and BI rate.

Structural Reform: Promoting FDI

The issue is foreign capital. Portfolio flows carry a lot of volatility but there is a part of the inflows that we would love to have, namely FDI or foreign direct investment. In addition to the policy mix, the government implemented many structural reforms that allowed Indonesia to be a desirable place for investment (FDI). Consequently, a lot of FDI regulations have been relaxed, including foreign ownership regulations. Before, we requested FDI firms coming to Indonesia to have a 50% share with local partners. Therefore, if it was a USD10 billion investment for example, where would we find a local investor able to invest USD5 billion? Not too many Indonesian people have USD5 billion to throw around. Consequently, we relaxed the regulations. From the fiscal policy side, the need to finance our economy through foreign savings meant it was important to maintain long- term fiscal sustainability. From 2012 onwards, therefore, the path of our fiscal policy has been one of consolidation. We are trying to reach a surplus in our primary balance. Perhaps later, one of our colleagues from the Ministry of Finance could explain fiscal consolidation in Indonesia.

Conclusion

Against the backdrop of a dynamic global environment, the multitude of challenges confronting the Indonesian economy demanded a policy mix response utilizing multiple instruments. Consequently, we allowed our inflation targeting framework to become more flexible than standard ITF in terms of managing monetary and financial stability in Indonesia. Under BI's policy mix response, the integration of monetary and macroprudential policy provides better results in terms of mitigating excessive macroeconomic and financial sector fluctuations compared to any single policy instrument.

Interaction

- Speaker::

-

Please elaborate on foreign ownership of banks.

- Participant::

-

Regarding foreign ownership of banks, we regulate everyone equally, foreign and domestic. An individual can buy a bank up to 20% of bank equity or 30–40% for a financial institution. This applies to foreign and domestic investors.

- Speaker::

-

All of the data and your experiences in the presentation are up to 2015, especially in terms of how the central bank formulated its policy response from the challenges that were encountered. From 2016–2018, however, 16 economic policy packages were introduced by the government, some of which would have influenced the central bank policy mix. How can we manage these 16 economic policy packages to ensure that our macroprudential policy, in the years ahead, remains effective?

- Participant::

-

This question concerns structural reforms conducted by the government. There have already been 16 economic packages since 2016 that were directed towards many things, including social protection, promoting foreign investment and so on. Some of those policies have been quite effective in terms of social protection. Furthermore, some of the FDI measures have also been effective but more recently, when our current account deficit tended to persist, the government started to strengthen the FDI policies with many more relaxations, including tax holidays and R&D incentives, for example, to allow FDI to enter Indonesia. These are not short-term solutions. We will only see the benefits of these reforms later in the long run. We have just planted the seeds, but it will take time for the trees to produce fruit. The reforms conducted by the government contained massive infrastructure projects, which required imports. Nevertheless, we were able to control a manageable current account deficit through import control policy. In 2018, the current account deficit was even narrower, showing how effective the policies had been.

References

Agung, J. J. S. M., Harmanta & Tarsidin, 2016. Managing Monetary and Financial Stability in a Dynamic Global Environment: Bank Indonesia's Policy Perspectives. BIS Papers, Volume 88, pp. 157–188.

Juhro, S. M., 2014. The Linkages between Monetary and Financial Stability: Policy Perspectives and Case Study. BI Occasional Paper.

Juhro, S. M., 2015. The Role of Central Bank in Promoting Sustainable Growth: Perspectives on The Implementation of Flexible ITF in Indonesia. Afro Eurasian Studies Journal, 4(1).

Schoenmaker, D., 2011. The Financial Trilemma. Economic Letters, 111(1), pp. 57–59.

Warjiyo, P. & Juhro, S. M., 2016. Kebijakan Bank Sentral: Teori dan Praktik. Jakarta: PT RajaGrafindo Persada.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License (http://creativecommons.org/licenses/by-nc-nd/4.0/), which permits any noncommercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if you modified the licensed material. You do not have permission under this license to share adapted material derived from this chapter or parts of it.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2022 BI Institute

About this chapter

Cite this chapter

Agung, J., Juhro, S.M., Kurniati, Y., Anglingkusumo, R., Sahminan (2022). Bank Indonesia Policy Mix. In: Warjiyo, P., Juhro, S.M. (eds) Central Bank Policy Mix: Issues, Challenges, and Policy Responses. Springer, Singapore. https://doi.org/10.1007/978-981-16-6827-2_8

Download citation

DOI: https://doi.org/10.1007/978-981-16-6827-2_8

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-16-6826-5

Online ISBN: 978-981-16-6827-2

eBook Packages: Economics and FinanceEconomics and Finance (R0)