Abstract

China’s economic rise over the past 40 years is one of the major transformational events in modern world history. China has lifted more than 850 million people out of poverty since 1978.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

9.1 Introduction

China’s economic rise over the past 40 years is one of the major transformational events in modern world history. China has lifted more than 850 million people out of poverty since 1978 [1]. The country’s gross domestic product (GDP) has grown from about roughly $200 billion in 1980 to more than $14 trillion in 2019, a 69-fold increase, while the population only grew by 40% (to 1.4 billion) during that time. Merchandise imports in that same period grew from about $20 billion to over $2 trillion, a 100-fold increase, while exports increased 135-fold, from $18 billion to around $2.5 trillion [2].

China’s transformation has occurred in tandem with the unprecedented globalization of value chains. While global GDP grew nearly eight-fold from 1980 ($11 trillion) to 2018 ($85 trillion), the global export of goods by value during that period grew nearly tenfold, from $2 trillion to $19 trillion.

As its economy has globalized and matured, China has developed an increasingly holistic vision for the future. China’s 13th Five Year Plan (FYP) (2016–2020) has created a blueprint for the nation’s future development around five themes: innovation, coordinated development, green growth, openness, and inclusive growth. In 2018, China integrated the concepts of “Ecological Civilization” and “a community of shared future for mankind” into its Constitution. These steps by China accord with the global trend towards green growth and sustainable development, as reflected by the adoption in 2015 of the UN Sustainable Development Goals (SDGs).

Beginning in 1980, global value chains—in which production processes are broken up across countries and among specialized tasks performed by different firms—have become an increasingly important feature of the global economy; they currently account for around half of all global production [3]. While global value chains have many benefits, they also have considerable environmental impacts. The global value chains of four soft commodities—soy, beef, palm oil and wood products—are responsible for at least 40% of global deforestation and could lead to biodiversity loss, climate change, and other environmental challenges [4, 5]. The need for greening production, trade, and consumption is increasingly recognized by participants at all stages of these value chains.

As the world’s largest exporter and second-largest importer, China is at the centre of global value chains, including for the four soft commodities noted above. China accounted for almost 60% of global soy imports and was the world’s second-largest palm oil importer (following India) in 2019 [6]. China’s beef imports have grown rapidly and surpassed the United States in 2018, making China the world’s largest importer in quantity and second-largest in value (following the United States) [6]. China has also become the world’s largest importer of timber, accounting for one third of the value of global timber imports (logs and sawnwood) in 2018 [6].

It is increasingly in China’s self-interest to green its value chains, especially those for key soft commodities. As these value chains have become more complex, they are increasingly subject to a variety of risks:

-

The COVID-19 pandemic fundamentally disrupted the global economy in just a few months and exposed the vulnerabilities of global value chains to rapid and unexpected change from factors in the natural environment.

-

International trade policy shifts and disputes (such as the U.S.–China “trade war”) can cause short-term disruptions and increase longer-term uncertainty and instability in global value chains—although the imperatives of mutual economic benefit and stable political relationships are likely to reduce tensions in the longer term.

-

Political and economic events in producer countries can also affect the supply and price of export commodities.

-

Over-exploitation of a commodity can lead to decreasing availability and/or increasing prices (e.g., some fisheries and timber species).

-

Diseases, pests, and invasive species (notably COVID-19 but also African swine fever, avian flu, fire ants, African snails, and locusts) can fundamentally disrupt global value chains.

-

Regulatory requirements are becoming more stringent in both producer and end-market countries (e.g., food safety and labour standards, phytosanitary and environmental protections), and this trend is likely to accelerate in light of COVID-19.

The globalization of value chains also presents China with some positive opportunities:

-

With such a huge share of the global market, policy reforms by China are likely to trigger comparable changes in other countries. If China becomes an “early mover” in greening its soft commodity value chains, it can turn policy innovations into economic advantages.

-

Greening soft commodity value chains is also an opportunity for China to meet its climate change, biodiversity, and sustainable development commitments under environmental treaties and the SDGs.

While economic growth remains a key priority for China, the past decade has seen a gradual shift in policy towards the quality, stability, and sustainability of growth. This is exemplified in China’s aspiration to achieve an Ecological Civilization.

The vision of Ecological Civilization extends beyond China’s borders. China’s economic rise has been accompanied by a significant expansion in international engagement, exemplified by the Belt and Road Initiative (BRI) and China’s leading role, with the United States, in catalyzing a successful outcome at the 2015 Paris Climate Summit.

This report seeks to provide a convincing rationale and concrete policy options for Chinese leadership to green its global value chains for soft commodities—particularly those linked to tropical deforestation. This study focuses on soy, beef, palm oil, and forest products (timber, pulp, and paper) and builds on the findings and recommendations of a previous CCICED Special Policy Study, China’s Role in Greening Global Value Chains, published in 2016 (see Box 9.1).

The exploration of policy options is timely in light of several key upcoming events in 2021 that China will host, including the 15th Conference of the Parties (COP-15) to the Convention on Biological Diversity (CBD), the annual China International Import Expo in Shanghai. The 26th Conference of the Parties to the United Nations Framework Convention on Climate Change (UNFCCC) in the United Kingdom presents an additional opportunity. The study is also timely in light of the process underway during 2020 to finalize China’s next FYP (2021–2025).

The focus on these soft commodity value chains is also relevant to China’s growing role as a global infrastructure investor under the BRI. The BRI is a major catalyst for infrastructure expansion in many countries, and where and how roads, ports, power grids, and mills are built is a major enabling condition for the expansion of commercial logging and agricultural production into new frontiers. The study has therefore been carried out in close coordination with the work of the BRI International Green Development Coalition, as well as CCICED’s previous and ongoing work on greening the BRI.

This study answers the following questions to identify the opportunities and barriers that greening the commodity value chain could bring to China:

-

What is the significance of soft commodity value chains for China?

-

Why should China pursue green soft commodity value chains?

-

How can China “green” its soft commodity value chains?

Three assumptions have guided the formulation of the study’s recommendations:

-

Recommendations should not interfere with the internal affairs of sovereign nations

-

Proposed solutions should be practical and low cost.

-

Recommendations should embody a Chinese approach to solving global problems, aligned with the vision of an Ecological Civilization and a community of shared future for humankind.

Box 9.1. Summary Findings and Recommendations of the 2016 CCICED Study

Conclusions

-

Global value chains need a green reboot, and China can lead the way.

-

Greening global value chains for commodities, in particular, is central to sustainable development.

-

It is in China’s interest to lead the greening of global value chains for commodities.

Recommendations

-

Play a leadership role in promoting the sustainability of global value chains in international governance and policy-making.

-

Send a clear policy signal to encourage Chinese companies and multinational companies trading in China to green their global value chains.

-

Create an action plan for greening global value chains as a core priority for the BRI.

-

Invest development aid and other financial resources in greening global value chains.

First Steps

-

State-Owned Enterprises (SOEs): The State-owned Assets Supervision and Administration Commission (SASAC) should mandate SOEs to assure the sustainability of the commodities they buy that impose major global environmental impacts.

-

Pilots: The Government of China should launch a pilot program to establish best practices for greening the global value chains for soy, palm oil, and forest products.

-

Development Assistance: The Ministry of Environmental Protection, the National Development and Reform Commission (NDRC), and the Ministry of Commerce should jointly launch a Green Global Value Chain South-South Cooperation Platform under the newly established South-South Cooperation Fund on Climate Change to support China’s major commodity supplier countries in improving the sustainability of commodity production and trade.

Box 9.2. Definition of Key Terms

Soft commodities: Raw materials and their derivatives that are grown or produced by agriculture (crops, livestock) and forestry industries.

Global value chains: Processes by which value is added across different stages from production to consumption and carried out by actors located in different parts of the world [7].

Supply chains: A component of value chains that are composed principally of the logistical linkages at a firm level [7].

Producer countries: Countries that produce a large amount of relevant commodities and often export those commodities.

Consumer countries: Countries that consume a significant amount of commodities and often import those commodities.

Due diligence: A risk management process implemented by a company to identify, prevent, mitigate, and account for how it addresses environmental and social risks and impacts in its operations, supply chains, and investments.

Traceability: The ability to follow a product or its components through stages of the supply chain (e.g., production, processing, manufacturing, and distribution).

Greening: A shorthand term for policies and practices that reduce the negative environmental and social impacts of economic investments, activities, and production processes.

9.2 What Is the Significance of Soft Commodity Value Chains for China?

Global value chains—in which production processes are broken up across countries and among specialized tasks performed by different firms—have become an increasingly important feature of the global economy since 1980. Global value chains now account for about half of all global production [3]. These chains bind the world together, linking the economies and peoples of both developing and developed countries in the trade of soft and hard commodities. The COVID-19 health pandemic and economic crisis, however, have disrupted most global value chains. How quickly these global value chains can be restored after the worldwide lockdowns are lifted remains unclear.

9.2.1 What Are Soft Commodities?

“Soft commodities” are raw materials and their derivatives that are grown or produced by the agriculture and forestry industries. These materials include plant- and animal-derived materials for use as food, fibre, feed, medicines, cosmetics, detergents, and fuels. Soft commodities contrast with “hard commodities,” which are raw materials and their derivatives that are extracted or mined, such as metals, oil, and natural gas.

Soft commodities are critical for human development and trade. They provide the world’s nutrition, feed for livestock, and raw material for paper, clothing, furniture, and buildings. While some can be domestically produced, many soft commodities are grown in areas that have a comparative advantage for production—such as the right soils, rainfall, and climate. Thus, nations typically rely on global value chains to access the soft commodities they need.

9.2.2 What Are the Challenges of “Business-As-Usual”?

A handful of soft commodities—soybeans, palm oil, beef, forest products (timber, pulp, and paper), coffee, and cocoa—pose significant challenges to sustainable development. A core challenge concerns deforestation, climate change, and biodiversity loss. Many countries that produce these soft commodities have high levels of biodiversity and high rates of deforestation (Fig. 9.1). In fact, soybeans, palm oil, beef, and forest products combined account for anywhere from 40% [4, 5, 73] to more than 50% of the world’s tropical deforestation [8, 9]. In major producing countries such as Brazil and Indonesia, the loss of tree cover in the last two decades is closely linked to the production of these soft commodities (oil palm and pulp and paper in Indonesia; beef and soybeans in Brazil) (Fig. 9.2). As such, these soft commodities are the world’s leading cause of biodiversity loss and greenhouse gas emissions related to land-use change [10].

Global exports of soft commodities by top-producing countries (2017)

Source Global Forest Watch (2019)

Dominant primary drivers of tree cover loss in Brazil and Indonesia.

A second challenge concerns legality. Revenue from illegally sourced timber, for example, is estimated to be $50 billion–152 billion globally per year [11]. More than 90% of the deforestation in the Brazilian Amazon is illegal and often associated with other crimes, such as drug trafficking and tax evasion [12]. An Indonesian government audit in 2019 found that around 81% of Indonesian oil palm plantations did not meet applicable regulations [13]. A significant proportion of the global supply of soft commodities is linked to illegal logging or land clearing, violation of labour laws, tax avoidance, or corrupt allocation of permits and licenses.

A third challenge concerns the social issues of equality and inclusion. For instance, women tend to experience lower participation rates in these value chains, unequal access to capital and property, and undervaluation of compensation for their work [14,15,16]. Farmers’ livelihoods may be harmed where unsustainable commodity production degrades forests and land or limits their access to high-yielding crop varieties, water, or energy. A lack of recognition of local rights over land and resources—which may be customary or informal—is another key social challenge. Labour-related issues may also arise, such as child labour, slavery, lack of collective bargaining rights, poor wages and benefits, and poor workplace safety and health conditions.

Consequently, “business-as-usual” trade in these soft commodities poses a threat to major international agreements. For example, it contravenes national laws and applicable international law. It threatens to undermine the achievement of numerous SDGs, including Goal 5 (gender equality), Goal 8 (decent work and economic growth), Goal 10 (reduced inequalities), Goal 12 (responsible consumption and production), Goal 13 (climate action), Goal 15 (life on land), and Goal 16 (peace, justice and strong institutions). Moreover, continued tropical deforestation by these commodities will make it impossible to achieve the Paris Agreement on Climate Change and the globally agreed goals and targets of the CBD.

Likewise, “business-as-usual” trade in these soft commodities poses economic threats. Recent history showcases a number of high-profile instances where business and economic performance suffered significantly due to engaging in “business-as-usual” practices. Examples include:

-

Global wood flooring manufacturer and retailer Lumber Liquidators saw its market capitalization drop by $1.1 billion in the first half of 2015 after being held criminally liable in the United States for importing illegal timber from Russia (through China). It was subsequently exposed in the media for using potentially cancer-causing levels of formaldehyde in its China-sourced laminated flooring [17].

-

Cocoa and palm oil firm United Cacao was exposed in 2016 for developing plantations in legally protected forests in the Peruvian Amazon [18]. In early 2017, the London Stock Exchange suspended trading of the firm’s stock, its CEO resigned, and its share value fell by 55% [19].

-

Five grain trading firms—Cargill, Bunge, ABC Indústria e Comércio SA, JJ Samar Agronegócios Eireli, and Uniggel Proteção de Plantas Ltda—and a number of farmers were fined a total of $29 million by the Brazilian government in 2018 for activities connected to illegal deforestation in Brazil’s Cerrado savannah [20].

-

One of the world’s iconic guitar companies, Gibson Guitar, paid a $300,000 penalty and forfeited the seized wood valued at more than $250,000 in 2012 under a criminal enforcement agreement with the United States government after having been found importing illegally harvested ebony and rosewood from Madagascar and India [21].

Moreover, as the CCICED noted in 2016, goods and ecosystem services that are critical to the global economy may degrade and even disappear if natural resources are unsustainably managed, even in the near term [7]. In addition, business-as-usual presents market, reputational, and compliance risks for the private sector as consumers and governments in both emerging and developed economies increasingly demand products that are more sustainable [4, 5, 73].

9.2.3 Why Is China Important?

China has emerged as the centre of trade in these soft commodity value chains. Driven by demand from the country’s rising middle class and limited potential for expanding domestic production commensurate to demand, China is now the world’s largest single country importer of soy, beef, and timber, as well as the world’s second-largest importer of palm oil (behind India) (Table 9.1). Chinese demand is larger than that from the European Union (EU) and North America for imported soy and pulp and paper. Moreover, Chinese demand is roughly on par with the entire EU for palm oil (Fig. 9.3) and is projected to grow [4, 5, 73]. Since it is the world’s largest or second-largest importer of these soft commodities, China is a key actor. If China takes proactive steps in collaboration with the other major markets—the EU, the United States, and India—the world will be able to transition from the “business-as-usual” approach toward a more sustainable path for soft commodity value chains.

Share of global imports (2015, 2025)

The BRI is another avenue where China can play a key role in greening global soft commodity supply chains. In 2019, China’s trade with BRI countries exceeded $1.3 trillion and comprised about 30% of China’s total trade [22]. By April 2019, China had signed BRI cooperative agreements with 125 countries [23], including many of the world’s major soft commodity producer nations in Asia, Africa, and Latin America. Importantly, the Chinese government has signalled an intent to ensure that the BRI advances sustainable, “green” value chains in these countries. In 2017, the Ministry of Ecology and Environment, the Ministry of Foreign Affairs, the Ministry of Commerce, and the NDRC jointly published Promoting the Green Belt and Road Initiative. This guidance highlights the need to strengthen value chain management in a manner that promotes green production, green procurement, green consumption, and international cooperation to achieve greener value chains.

9.2.4 What Is a “Green” Soft Commodity?

What are the defining environmental and social characteristics of a “green” soft commodity value chain? Environmental characteristics include the efficient use of natural resource inputs, low levels of waste, and low amounts of pollution. More fundamentally, green soft commodity value chain sourcing and production processes do not directly or indirectly cause the degradation, fragmentation, or conversion of natural forests and other important natural ecosystems (e.g., grasslands). This means, for instance, that “green” soy, palm oil, and beef production in producer countries does not involve the clearing and conversion of natural tropical forests and other ecosystems. For wood products, it means that timber is not extracted at an industrial scale from high-conservation value forests (i.e., intact or primary forests). Complementing this, a green soft commodity is one in which productivity per hectare (i.e., yields) of existing agricultural land is high or improving—since boosting yields on existing agricultural land is a key approach to avoiding the need to convert natural ecosystems.

Social characteristics include respect for the internationally recognized rights and interests of Indigenous Peoples, local communities, women, children, and workers. They include protections from discrimination, exploitation, and unsafe or unhealthy working conditions.

A green soft commodity value chain is also a legal value chain, in which both national laws and international legal obligations regarding permitting, licensing and harvesting, environmental and social impact assessment, payment of taxes and other fees, participatory decision-making processes, and labour rights and protections are observed according to the national laws and international obligations. And a green soft commodity value chain is a transparent value chain, in which all stakeholders have access to relevant information about the legality and sustainability of production and trade processes, from the field to the ultimate market.

Although fully greening soft commodity value chains involves improvements along each stage of the value chain, this study will focus on the production stage—particularly the social and environmental impacts of land acquisition, the conversion of natural ecosystems, and farming and forestry practices. This focus is justified for at least four reasons:

-

First, this is the stage of a soft commodity value chain that has the most impact on climate change, biodiversity, and land-related rights. That is because it is the growing or extraction of commodities that directly causes the loss or degradation of natural ecosystems and of the rights and livelihoods of Indigenous Peoples and local communities. The loss and degradation of forests, peatlands, and mangroves are major contributors to global greenhouse gas emissions—an important factor in regulating local climate and the leading driver of biodiversity loss [24, 25]. In fact, for many major soft commodities of importance to China, the conversion of land is the commodity’s major contribution to greenhouse gas emissions (Fig. 9.4).

Fig. 9.4

Share of greenhouse gas emissions per stage in the value chain for selected soft commodities

-

Second, climate change and biodiversity conservation are high on intergovernmental agendas for the years 2020 and 2021. The next Conference of Parties to the global agreement on climate change is slated to feature “nature-based solutions,” which include forest conservation and more sustainable agriculture. The next Conference of Parties to the UN CBD, to be hosted by China, will set the global agenda for biodiversity conservation for the next decade.

-

Third, delinking soft commodities and deforestation is high on global finance and private sector agendas. This is evidenced by the incorporation of sustainability standards in global investment firms such as BlackRock and major collaborations on this issue convened by the Consumer Goods Forum, World Economic Forum, and others.

-

Fourth, it is most practical to green soft commodity value chains in a step-by-step approach. Trying to address every sustainability aspect of a value chain all at the same time could be too overwhelming and thus lead to paralysis. Rather, focusing first on one of the most important and high-profile issues currently could enable governments and companies to take targeted, concrete action now. Investments in improving traceability, for example, can benefit both sustainability goals and value chain cost-effectiveness. And this could have an outsized impact since improving the basics of production will have knock-on benefits in other parts of the value chain. Other sustainability issues can be added to the agenda once sufficient progress is made.

9.3 Why Should China Pursue Green Soft Commodity Value Chains?

As the world’s largest importer and consumer of soft commodities, China has the power to catalyze positive change across the global economy. But why would China find it in its self-interest to do so? There are five principal reasons: (1) to ensure consistency with China’s vision of an Ecological Civilization, (2) to strengthen supply chain safety and security, (3) to uphold the law, (4) to respond to tomorrow’s markets, and (5) to optimize China’s international environmental reputation.

9.3.1 Ensure Consistency with China’s Vision of Ecological Civilization

The greening soft commodity value chains is entirely consistent with and supportive of China’s vision of an Ecological Civilization, at home and abroad, as laid out by the country’s highest leadership. At the 19th National Congress of the Communist Party in 2017, President Xi Jinping stated that: “Taking a driving seat in international cooperation to respond to climate change, China has become an important participant, contributor and torchbearer in the global endeavour for ecological civilization.” He continued, noting that:

The dream of the Chinese people is closely connected with the dreams of the peoples of other countries … We must keep in mind both our internal and international imperatives, stay on the path of peaceful development, and continue to pursue a mutually beneficial strategy of opening up, cultivat(ing) ecosystems based on respect for nature and green development … We should, acting on the principles of prioritizing resource conservation and environmental protection and letting nature restore itself, develop spatial layouts, industrial structures and ways of work and life that help conserve resources and protect the environment.

Embarking on the journey to make Chinese soft commodity value chains “green” would be a concrete manifestation of this vision. It also would help ensure that the 2021 CBD summit in Kunming is a resounding success.

9.3.2 Strengthen Supply Chain Safety and Security

The COVID-19 crisis is placing immense scrutiny on the safety of global trade and the long-term security and stability of global value chains. Greening soft commodity supply chains can be a component of an effective strategy for addressing both challenges.

First, greening soft commodity value chains can help make global trade safer. This is because environmental health is linked to human health. A number of recent scientific studies point to a link between the conversion of natural ecosystems, increased human contact with wildlife, the emergence of new (and the spread of old) zoonotic diseases, and epidemics (or even pandemics) harming human health [26]. Examples include Ebola, coronaviruses, Marburg, Zika, and malaria [27, 28] (Box 9.3). In light of COVID-19, the global community, businesses, and citizens will be paying greater attention to ensuring that a country’s economic activities—such as what it trades and from where—are not triggering the emergence and spread of zoonotic diseases. Avoiding economic activities that lead to deforestation can reduce this risk of contributing to human diseases.

Second, greening soft commodity value chains can help secure the long-term stability of supply (and therefore stability of price) of soft commodities. This is because the long-term availability of soft commodities depends in part on how those resources are managed today. For example, recent studies find that clearing too much of the Amazon for soybeans and cattle will lead to a decline in rainfall in Brazil’s “soy belt,” thereby reducing the country’s soy production in the long term [27, 29]. Soon-to-be-published analysis indicates that the yield shocks could be on the order of 10%, generating losses worth USD 700 million per year [30]. Where unsustainable production leads to social conflict and corruption, the stability of commodity supply and price from that region can fluctuate unpredictably. And for some commodities, such as certain species of timber, overexploitation can lead to the commercial collapse in supply. Thus, sustainable management today ensures availability for tomorrow at stable prices. Conversely, unsustainable management may trigger supply scarcity, unreliability, and volatile prices.

Box 9.3. How Do Green Value Chains Contribute to Human Health?

Green soft commodity value chains can contribute to human health by reducing the risks of zoonotic diseases that spread from animals to humans. More than 60% of emerging infectious diseases are zoonotic in origin, and the majority (70%) of these zoonotic pathogens have emerged because of increased human-wildlife contact—driven by humans and livestock encroaching on natural ecosystems [31, 32].

Deforestation and forest degradation—and exploitation of wild animals—are implicated in the emergence over the past few decades of zoonotic disease outbreaks such as Ebola, SARS, avian flu, and COVID-19 [26]. One study found that Ebola outbreaks in Central and West Africa were significantly associated with forest losses in the previous two years [70]. When forests are cleared for soft commodity production, the buffer zones separating humans from animals or the pathogens that animals harbour are reduced or lost [33].

Establishing green value chains is therefore key to ensuring that economic activities are not causing ecological degradation that increases the likelihood of human exposure to zoonotic viruses.

9.3.3 Uphold the Law

Greening its soft commodity value chains would enable China and Chinese companies to uphold the law. This is important for at least three reasons:

-

It is simply the right thing to do. It is a longstanding principle of China’s foreign policy to respect international law, as well as to respect the sovereignty and laws of other countries (Box 9.4). Laws regarding the production and trade of soft commodities are quickly strengthening around the world. This fast-changing context necessitates the greening of soft commodity value chains if China is to adhere to its longstanding principles and if Chinese enterprises are to remain in legal compliance in the foreign jurisdictions where they do business.

-

Other leading importers are strengthening laws on soft commodities. Worldwide scrutiny of the legality of soft commodities is rapidly increasing. With respect to timber, for instance, many of the world’s major importing nations recently have established laws banning the import of illegally harvested or traded wood products. These nations include the EU, the United States, Australia, Japan, and South Korea, which account for 52% of the world’s forest product imports [34]. In addition, since 2017, the UN Convention on International Trade in Endangered Species (CITES) has listed hundreds of timber species, many of which feed the Chinese furniture industry, for protection from illegal trade.

This trend towards more stringent scrutiny on legality is rapidly spreading to other soft commodities. In 2019, for instance, the European Commission started exploring policies to ensure imports of commodities such as soybeans, palm oil, and beef are not linked to illegal deforestation. An analogous measure is being discussed in the U.S. Congress in 2020. Beyond governments, numerous multinational companies, industry associations, and commercial banks have stepped up efforts to eliminate illegality from their value chains [73]. Likewise, more than 200 endorsers—including governments, companies, and civil society organizations—have supported The New York Declaration on Forests to halt deforestation in agricultural commodity value chains [35].

-

Exporting countries are introducing and enforcing laws on soft commodities. Several of China’s major soft commodity production and trading partners have put in place laws to curtail the illegality (and increase the sustainability) of their soft commodity production and trade (Box 9.4). Moreover, they are taking enforcement action. In 2016, for example, Spanish banking giant Santander incurred a $15 million fine for lending money to farmers illegally destroying Brazilian forests [36, 37] China and Chinese companies could send a signal of supporting the enforcement of these laws and being good trade partners by greening their soft commodity value chains.

Box 9.4. Would Chinese Efforts to Green Its Soft Commodity Supply Chains Interfere with the National Sovereignty of Its Trading Partners?

Chinese efforts to green its soft commodity supply chains would not interfere with the national sovereignty of its trading partners. Rather, by greening its soft commodity supply chains, China actually would support the national sovereignty of its trading partners. This is because many of China’s trading partners already have in place laws that encourage legal and sustainable soft commodity production and trade. Examples include:

-

Indonesia: Recent Indonesian policies aim to get illegality and deforestation out of its timber and palm oil supply chains. For example, Indonesia’s Low Carbon Development Initiative (LCDI)—launched in 2019 as a program of the Ministry of National Development Planning (BAPPENAS)—sets the country’s economic development agenda. The LCDI calls for increased supplies of sustainable palm oil and timber via yield increases and using degraded land while avoiding the conversion of natural forests and peatlands [38]. Also, in 2019, the Indonesian president announced a permanent moratorium on new forest clearing for plantations and logging in 66 million hectares of primary forest and peatland 71. In addition, the country has established a National Timber Legality Assurance System to prevent trade in illegally harvested timber. This has enabled a Voluntary Partnership Agreement with the European Union (EU) that ensures only legal timber from Indonesia enters the EU market in return for faster, streamlined processes as timber reaches the EU border [39]. China seeking to “green” its palm oil and timber supply chains would support Indonesia’s implementation of these nationally approved economic development plans, government policies, and government trade programs.

-

Brazil: More than 90% of deforestation in the Brazilian Amazon is illegal and often associated with other crimes, such as drug trafficking and tax evasion [12]. Consequently, a number of existing public policies in Brazil focus on preventing illegal deforestation. For example, the Forest Code stipulates the maximum land area per farm that can be cleared for agriculture per biome (e.g., 20% in the Amazon, 65%–80% in the Cerrado) [40]. Any clearing beyond that is illegal, and the products generated on such farms are in violation of the law. In addition, Brazil’s Nationally Determined Contribution (NDC) to the Paris Agreement on Climate Change calls for strengthening policies and measures to achieve zero illegal deforestation in the Brazilian Amazon by 2030 [41]. Therefore, China seeking to ensure that the soybeans and beef it imports from Brazil are legal and “green” would support the Brazilian implementation of these laws and commitments.

-

Africa: Many countries in Africa, a growing source of tropical timber for China, have laws in place to eliminate illegal logging and avoid loss of their natural forests. For example, over the past decade, at least eight African countries (Cameroon, Central African Republic, Côte d’Ivoire, Democratic Republic of Congo, Gabon, Ghana, Liberia, Republic of the Congo) have signed or are in the process of negotiating Voluntary Partnership Agreements with the EU to ensure that only legally harvested timber enters European and domestic markets [42]. In 2018, the Republic of the Congo issued Joint Ministerial Decree 9450, which stipulates that new agricultural development greater than 5 ha can only be developed on savannahs and not in forests [43]. The Democratic Republic of the Congo’s National REDD + Strategy and Investment Plan steers large-scale agricultural development toward savannahs, as well. Therefore, China seeking to ensure that future timber imports from the Congo Basin are legal and that any future palm oil imports from the region are deforestation-free aligns with government policies and programs of these nations.

9.3.4 Respond to Tomorrow’s Markets

China has emerged as a global powerhouse for today’s markets. But future economic success rests on China meeting the needs of tomorrow’s markets. These markets will increasingly demand greener consumption and greener production [44]. When it comes to soft commodities, these markets are trending toward “green” in three ways:

-

Evolving Chinese consumer preferences. History shows that, as per capita incomes rise in nations, consumers increasingly care about the social and environmental sustainability of the products they purchase [45]. Thus, rising concern about sustainability typically coincides with a rising middle class. China is no different. For instance, a 2017 survey found that more than 70% of Chinese consumers were willing to pay a 10% premium for sustainably produced goods [46].

-

Globalizing retailer and manufacturer norms. The business norms of multinational retailers and manufacturers of products containing soft commodities are rapidly shifting towards greater sustainability and are being applied equally across all geographies. Walmart’s sustainability policies, for instance, apply to all Walmart stores [47]. These business norms include value chain policies, as well. Walmart is working with its global suppliers to evaluate and share progress on key environmental and social issues in supply chains covering more than 100 product categories, including pulp, paper, and timber products [47]. In 2019, retail giant H&M announced that it would no longer source leather from Brazil due to the role of cattle ranching in Amazon forest fires and deforestation [48]. The company applied this policy to all of its stores worldwide; there was no separate policy for stores in Europe versus those in China. Mars—a major manufacturer of chocolate and other soft commodity-based products—has adopted a comprehensive set of policies to eliminate deforestation from its supply chains [49].

-

Tightening capital market policies. A growing critical mass of institutional investors is developing investment guidelines to limit access to capital by borrowers whose investments in soft commodity production and trade result in tropical deforestation. In September 2019, for instance, 230 institutional investors representing $16.2 trillion in assets under management called on companies to take urgent action in light of the devastating forest fires in the Amazon: “As investors, who have a fiduciary duty to act in the best long-term interests of our beneficiaries, we recognize the crucial role that tropical forests play in tackling climate change, protecting biodiversity and ensuring ecosystem services” [50].

In light of these reasons, greening soft commodity value chains now can help position China and its companies for the rapidly approaching markets of tomorrow. And acting now would send market signals that ensure an adequate supply of green commodities at competitive prices (Box 9.5).

Box 9.5. Can Green Palm Oil Meet Increased Chinese Demand at a Reasonable Price?

China—and the world—can continue to use palm oil without destroying tropical forests and without paying a large “green premium.” In terms of supply, global demand for palm oil certified by the Roundtable on Sustainable Palm Oil (RSPO) equates to ~10% of global palm oil supply, yet ~20% of global supply is already certified [51]. Thus, the palm oil market today could already absorb additional “green” demand.

In terms of price, green palm oil compared to “business-as-usual” palm oil can be quite close. For example, recent pricing from a major palm oil supplier indicates only a 3–4% premium for segregated sustainable crude palm oil and just a 1% premium for non-segregated sustainable crude palm oil. This variation is less than the variation in spot market prices on a weekly basis [52]. As more sustainable supply becomes available, the cost of sustainable production likely will decline and thereby further help ensure cost competitiveness.

As a major palm oil importer, China can play an important role in accelerating growth in the supply of green palm oil. If China were to send a clear preferential sourcing signal that a steadily increasing share of its palm oil will need to be green, the market would respond. Such a “demand signal”—with demand expected by the market to ratchet up over time—would give producers the incentive and time needed to ramp up production in advance, avoiding any potential future shortfalls in supply and keeping prices stable.

Satisfying 100% market demand for a green soft commodity, however, will not happen overnight. For example, the supply of green, deforestation-free palm oil is not sufficient to meet demand if all buyers asked for it today. This is also true for soy. It will take some time for supply to catch up to such complete demand. A signal by China would stimulate suppliers to start working now to meet that future demand. And as both supply and demand for green soft commodities increase, prices will come down.

9.3.5 Optimize China’s International Environmental Reputation

China is committed to international development and environment agreements such as the UN Framework Convention on Climate Change (UNFCCC) and its Paris Agreement on Climate Change, the UN CBD, the CITES, and the UN SDGs. By sending a strong political signal that it will start greening its soft commodity value chains, China can position itself positively as a responsible global player in these landmark agreements.

Business-as-usual soft commodity value chains are a leading cause of damage to ecosystems, biodiversity, and a stable climate. This damage undermines the objectives of each of these international agreements. As the largest importer of soft commodities affecting tropical forests, China has a very important role—complementing the influence of the EU, the United States, and India—to play in minimizing this damage and helping the world fulfill these agreements.

International expectations of China are high as the country prepares to host the COP-15 to the CBD in 2021. The upcoming COP will set the global agenda for biodiversity conservation for the next decade. What vision will China—as the COP President—bring, and what actions of its own can China put on the table to inspire others?

China providing a clear signal that it is embarking on a serious effort to green its soft commodity value chains, along with other major economies, would be an inspiring and well-received response. It would help set the Post-2020 Biodiversity Framework on the path towards a more successful decade and help enshrine “nature-based solutions” as a cornerstone to the Paris Agreement. It would establish China as an important participant, contributor, and torchbearer on the global stage in biodiversity, climate change, and sustainable development. Moreover, it would support soft commodity-producing countries in their own efforts to lift small farmers (including women farmers) out of poverty (Box 9.6) and to meet their own obligations under these international agreements (Box 9.7).

Box 9.6. Does Greening Soft Commodity Supply Chains Hurt Small-Scale Farmers in Producer Countries?

Greening soft commodity supply chains does not hurt small-scale farmers in producer countries, as long as proactive policy measures are established to support their economic interests. Done correctly, it can help smallholders boost yields and increase market access.

Small-scale or “smallholder” farmers are important suppliers for some soft commodities. For example, smallholders produce about 40% of the world’s palm oil [53]—yet they produce under 12% of the world’s soybeans [72]. Smallholders tend to be less productive per hectare and less able to implement new sustainability practices than large farms due to lower access to inputs, finance, and technical know-how. For example, palm oil yields of smallholders in Indonesia are approximately 20–25% lower than those of corporate-managed plantations [69]. Women farmers are particularly disadvantaged in terms of productivity and income, with less access to seeds, fertilizers, finance, and land than men [16].

Shifting to green soft commodity production can benefit smallholders by catalyzing improvements in efficiency (e.g., more judicious use of fertilizers), production per hectare (i.e., yields), access to inputs, and ultimately income. Such improvements in efficiency and yields are a core component of greening soft commodities. Agricultural companies and government programs can support these improvements. Over the past decade, for instance, multinational agribusinesses such as Olam, Sime Darby, Musim Mas, and others have increasingly offered smallholders training, financing, inputs, and administrative support to adopt sustainable cultivation methods and avoid forest clearing. For example, Musim Mas has developed palm oil training for smallholders in Indonesia to boost yields in a sustainable manner while adopting improved health and safety practices [54]. Overseas development assistance from China could complement these private sector interventions, providing technical assistance, inputs, and access to subsidized financing to support the transition to more sustainable agricultural practices.

Box 9.7. Can Greening Supply Chains Help China’s Trading Partners Meet International Agreements?

Yes, China greening its soft commodity supply chains can help trading partner countries meet their obligations under several UN agreements. For instance, it would support developing country partners that have committed to reducing emissions from deforestation and forest degradation in their NDCs under the UNFCCC and the Paris Agreement on Climate Change. It would support the implementation of Article 3 of the CBD, which articulates inter alia that States have the “responsibility to ensure that activities within their own jurisdiction or control do not cause damage to the environment of other States …”. And it would support controlling the trade in rosewood (hongmu) species listed by CITES, for which China is overwhelmingly the world’s largest importer [55].

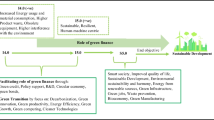

9.4 How Can China “Green” Its Soft Commodity Value Chains?

China has an unprecedented opportunity to play a catalytic role in greening the world’s soft commodity value chains. Doing so would support the country’s own development, business, and diplomatic objectives, as well as make a significant contribution to shared global biodiversity, climate, and SDGs. China can achieve this using three broad strategies. First, establish an ambitious and comprehensive strategy and supporting institutional arrangements at the highest level of government regarding green value chains. Second, adopt policies that require, encourage, or support companies supplying soft commodities to China to progressively green their value chains. Third, incorporate these policies in broader Chinese priorities and initiatives on trade, South–South cooperation, and green finance.

9.4.1 Establish a National Green Value Chain Strategy and Provide Policy and Institutional Support

Three steps to establish an ambitious and comprehensive national policy that is supported institutionally include:

-

A.

Announce a new Chinese policy initiative on greening soft commodity value chains.

-

B.

Establish an Inter-Ministerial National Committee on Value Chain Security and Sustainability.

-

C.

Establish a Global Green Value Chain Institute.

9.4.1.1 Announce a New Chinese Policy Initiative on Greening Soft Commodity Value Chains

At both CBD COP-15 and the Shanghai Expo—two high-profile international events that China will host in 2021 focusing on environment and trade, respectively—China can launch a new initiative signalling a move towards green value chains for key soft commodities for which China is a major importer and which have a significant impact on natural ecosystems. At COP-15, this initiative could be included in the package of Chinese deliverables on biodiversity conservation—at home and abroad—that China announces. The Shanghai Expo could help raise greater awareness of green value chains among importers and exporters worldwide and hence facilitate the implementation of the new policies and initiatives.

China could leverage this national commitment to encourage others to join a multilateral commitment on greening soft commodity value chains. This commitment could be part of a “Kunming Declaration” or another outcome from the High-Level Segment that China is likely to host back-to-back with COP-15. Engaging in this issue with other major economies is important. While China may seek to demonstrate global leadership, the impact will be greater if other major importers are included. As the host of COP-15 and one of the world’s largest players in soft commodity markets, China has the power to make this happen.

9.4.1.2 Establish an Inter-ministerial National Committee on Value Chain Security and Sustainability

In order to take this policy commitment forward, China could announce its intent to form a long-term Inter-Ministerial Committee focusing on value chain security and sustainability (Tentative name: National Committee on Value Chain Security and Sustainability). This Committee would address both soft and hard commodities. It could begin by following up on the recommendations of this Special Policy Study on soft commodities and gradually expand to cover other commodity value chains.

An Inter-Ministerial Committee is desirable because commodity value chains cross the jurisdictional and expertise boundaries of ministries. Trade, finance, agriculture, forestry, customs, and environment are all involved to some degree with commodity trade and thus should be represented. The severe disruptions to global value chains brought on by the COVID-19 pandemic further highlight the need for a comprehensive and unified response. Turning political commitment on green value chains into action therefore requires a “whole of government” approach. An Inter-Ministerial Committee could provide this, facilitating cross-sectoral cooperation and releasing policy guidance on the design and implementation of value chain security and sustainability initiatives in China.

The National Committee on Value Chain Security and Sustainability could be led by the Ministry of Ecology and Environment and jointly coordinated with the Ministry of Foreign Affairs, the Ministry of Commerce, China International Development Cooperation Agency, the General Administration of Customs, the Ministry of Agriculture and Rural Affairs, the State Forestry and Grassland Administration, and China Banking and Insurance Regulatory Commission. Depending on the progress of the work, other relevant government agencies could participate.

The main responsibilities of the Committee would include: (i) studying and approving proposed value chain security options and initiatives; (ii) reviewing and formulating proposed policy measures related to value chain security; (iii) coordinating and establishing a cooperation mechanism on value chain security and sustainable development; (iv) assessing and resolving problems in value chain security and sustainable development; and (v) periodically reviewing progress in improving value chain security and linking it to sustainable development objectives.

The Committee would be supported by the work of a new Global Green Value Chain Institute, as discussed below.

9.4.1.3 Establish a Global Green Value Chain Institute

In order to provide the best technical and policy advice to the Inter-Ministerial Committee, China could announce at CBD COP-15 that it will establish a Global Green Value Chain Institute. The institute would engage experts and stakeholders (e.g., governments, companies, financial institutions, research institutions, and civil society organizations) to develop more detailed commodity-specific plans on what China and other major economies can do to “green” their global value chains, how to do it (including pilot applications), and who needs to do what. The institute would initially emphasize soft commodities since they are most relevant to biodiversity and to the CBD. But the institute would address hard commodities as well.

Because the issues of greening value chains involve both environmental and trade issues, it will be crucial to the success of the proposed institute that it be jointly anchored in the Ministry of Environment and Ecology and the Ministry of Commerce. The institute could be either a new organization or a part of the recently established BRI Green Development Institute. Either way, the institute would be responsible to the Inter-Ministerial Committee, befitting its comprehensive cross-sectoral mandate. The institute would be a first of its kind and enable China to develop a centre of excellence on how to achieve legal, secure, and sustainable global value chains, an issue of increasing importance and interest to governments worldwide.

This institute would inform and support policy development and implementation by: (i) conducting scientific research to develop implementation plans of green value chains by type of commodity and sector; (ii) analyzing relevant policy pathways and institutions to determine which parts of government and industry need to be involved in order to achieve particular policy outcomes; (iii) developing guidance to ensure legality standards and requirements for import and export of raw materials and products are met; (iv) supporting sustainable production in producer countries through trade, finance, and development assistance; (v) building a collaborative network of stakeholders and information sharing and communication platform to encourage participation from relevant stakeholders, including industry, enterprises, and civil society, including those working on social and gender-related issues; and (vi) coordinating with international platforms such as the BRI and APEC to create synergies and exchange good practices on green value chains.

To begin, the institute could focus on the three soft commodity-focused policy measures outlined in Sect. 9.4.2 (below), including strengthening measures to reduce the import of soft commodities from illegal sources; strengthening commodity due diligence and traceability systems; and investing in domestic capacity to rationalize food value chains and improve sustainable diets. In addition, the institute could work to build soft commodity considerations into broader ongoing Chinese policy arenas, including trade agreements, South–South cooperation, green finance, and green BRI, etc. (see Sect. 9.4.3 below).

These six proposed initial areas of work for the institute emerged as high priorities for action in the course of preparing this Special Policy Study, based on their potential effectiveness in catalyzing sustainable soft commodity production and their potential feasibility for uptake (or relevance) in the Chinese context.

9.4.2 Adopt Mandatory and Voluntary Measures to Green Soft Commodity Value Chains

China should adopt a mix of regulatory and market-based approaches to drive progress towards green soft commodity value chains. This should include measures to achieve three critical outcomes:

-

A.

Strengthen measures to reduce the import of soft commodities from illegal sources.

-

B.

Strengthen due diligence and traceability systems.

-

C.

Invest in domestic capacity to rationalize food value chains and improve sustainable diets.

In pursuing these policies (especially A and B), China should seek to harmonize its “greening” standards with those of other leading countries.

9.4.2.1 Strengthen Measures to Reduce the Import of Soft Commodities from Illegal Sources

What is it?

China could strengthen its import management of the legality of soft commodities, building on the latest revision of the Forest Law and comparable legality standards in other major markets. Strengthening measures to reduce the import of soft commodities from illegal sources would strongly support the efforts of governments in producing countries aiming to discourage illegal production and the trade of soft commodities. Illustrative examples of illegality include palm oil grown on land where forests were cleared without a permit in Indonesia and soybeans grown on a farm that has cleared more forest than is allowed by the Brazilian Forest Code.

Mechanisms for implementing such measures would need to be developed in close cooperation with relevant producer countries and might need to be tailored to the specifics of individual commodity value chains. This would normally require the producer country to develop legality standards and verification systems for the production of soft commodities that could be recognized under the Chinese measures.

Chinese policy would encourage—and eventually require—companies importing soft commodities to China to exercise due diligence to ensure the commodity was produced legally in the source country. A range of incentives could be employed to motivate non-responsive companies to act, ranging from mere warnings at the outset up to civil and criminal penalties when a binding regulatory framework will eventually be developed. This would send a strong signal to foreign exporters that they need to ensure that the soft commodities they ship to China have been produced in accordance with the laws of the country where the commodities originated.

Given the size and complexity of China’s soft commodity imports, measures to ensure the legality of imports would need to be designed and implemented following a clearly articulated and phased approach (e.g., by commodity, by country) to allow Chinese importers and foreign exporters to review and adjust their sourcing practices in a manner that prevents supply disruptions, and to harmonize Chinese policy with those of producer country governments.

Who needs to act?

Chinese agencies would need to cooperate with counterpart agencies in each relevant producer country to clarify what qualifies as the legal production of specific soft commodities and coordinate with any relevant producer country standards and systems that are in place to verify legality. Within China, multiple ministries would need to collaborate to set due diligence requirements to be applied by companies to verify the legality of imported soft commodities and to define penalties and consequences for importers that fail to exercise due diligence. These ministries would likely include the Ministry of Ecology and Environment, the Ministry of Commerce, the Ministry of Agriculture and Rural Affairs, the National Forestry and Grassland Administration, the State Administration for Market Regulation, the General Administration of Customs, and the Ministry of Foreign Affairs. Working with technical experts, these ministries could also provide tools and training to private sector actors on how to meet the new legality obligations. Given the need for overall policy coordination, the role of the proposed Inter-Ministerial Committee would be critical, supported by the technical work of the proposed institute.

How does this build on existing Chinese efforts?

China is already taking steps toward legal import standards for soft commodities. For example, China has developed a draft national timber legality verification framework and piloted voluntary legality verification standards among a few timber companies in recent years. In December 2019, the Standing Committee of the National People’s Congress adopted a revised Forest Law that includes legality requirements for timber product value chains. Article 65 of the revised Forest Law stipulates that “timber trading and processing companies shall establish ledgers to record input and output of raw materials and products. It is forbidden for any organization and individual to purchase, process and transport timber from illegal sources such as knowingly unlawful or wanton.” Building on these first steps, China could consider expanding legality due diligence and verification requirements to the import of major soft commodities beyond timber, namely soybeans, palm oil, and beef.

Why is it important?

Ensuring the legality of imported soft commodities is a fundamental feature of green soft commodity value chains for three principal reasons. First, it demonstrates respect for the laws of producer countries and thereby contributes to strong and stable trade and political relationships. Second, it levels the economic playing field for Chinese importers who are obeying the law but who are undercut by cheap, illegal imported products. Third, it provides a clear demonstration of China’s support for international norms and agreements on global environmental sustainability and cooperation.

Where is this emerging as the new global norm?

If China were to establish and implement due diligence requirements with respect to the legality of soft commodity imports, it would be joining a growing list of countries ushering in a new era of legal trade. For example, the EU, the United States, Japan, Australia, and South Korea have implemented legality regulations on timber in recent years, and more countries are in the process of developing similar measures. The EU, for instance, requires importers to conduct due diligence to assess and mitigate the risk of illegal timber products entering the EU market. In 2017, South Korea amended its Act on the Sustainable Use of Timbers to regulate the legality of imported and domestically produced timber and timber products. In 2019, the European Commission issued a major communication on Stepping up EU Action to Protect and Restore the World’s Forests. This policy commits the EU to “promot[ing] trade agreements that include provisions on the conservation and sustainable management of forests and further encourage trade of agricultural and forest-based products not causing deforestation or forest degradation” [56]. As of mid-2020, the U.S. Congress was considering analogous legislative measures.

9.4.2.2 Strengthen Due Diligence and Traceability Systems

What is it?

The Chinese government could encourage companies (both state-owned and non-state-owned enterprises) to strengthen due diligence and traceability systems to achieve greener soft commodity value chains. “Due diligence” is a risk management process implemented by a company to identify, prevent, mitigate, and account for how it addresses environmental and social risks and impacts in its operations, supply chains, and investments. Traceability is the ability to follow a product or its components through the stages of the supply chain (e.g., point of production, processing, manufacturing, and distribution).

A diverse array of tools and approaches (e.g., risk assessment, certification, remote sensing, supplier warranties and reporting, computerized product tracking, blockchain technology) are already available to support due diligence and traceability. The Accountability Framework Initiative guidance on supply chain assessment and traceability [57] can help with the selection of approaches calibrated to the risk associated with a given commodity sourced from a particular region. Very importantly, a properly designed due diligence and traceability system can reduce costs and facilitate the adequate supply of green soft commodities. COFCO International’s pioneering approach (Box 9.8) provides an example of a potentially promising stepwise risk-based approach. Due diligence and traceability systems can be developed and applied voluntarily or be built into government regulatory controls.

The Chinese government could encourage companies to green their soft commodity value chains through regulations that set standards of due diligence and traceability (including within the proposal discussed in the section above to regulate against the import of illegally-produced commodities). Such regulations could help create a level playing field such that companies that comply with the regulations are not put at a competitive disadvantage against companies trading in cheaper, illegal products.

Box 9.8. A Risk-Based Approach to Due Diligence and Traceability That Reduces Costs

COFCO International and others are exploring the following approach (and variations thereof) when conducting due diligence and traceability of “green” soybean value chains originating in high deforestation-risk areas in Brazil:

-

Take it step-by-step. Don’t try to pursue all aspects of sustainability at once. Rather, start by focusing on a few of the most important and timely issues. Currently, securing “deforestation-free” (and avoiding “deforestation-linked”) soft commodities is one of those issues. Over time, pursue additional sustainability issues at a well-managed pace.

-

Use a “cut-off” date for “deforestation free.” Agree not to source a commodity that is linked to deforestation after a “cut-off” date. Agricultural products grown/raised on a tract of land are not considered “green” or “sustainable” if a forest was cleared on that tract of land to make way for the commodity after the cut-off date. These dates can be set via a multi-stakeholder process and can cover a biome or smaller region. For example, the cut-off date for soy in the Amazon biome is 2008.

-

Request supplier boundaries. Ask suppliers to provide the boundaries of their farms/ranches, or of the jurisdictions (e.g., municipality, district) from which they source.

-

Leverage satellite imagery. Access historical satellite imagery of the supply location during the year of the cut-off date. At the same time, access recent satellite imagery of the supply location. Compare the imagery. If forests were not there in the cut-off date year, then the commodity grown/raised on that location is deforestation free. If forests were there, then the commodity is not deforestation free. Continue to use recent imagery to monitor the adherence of suppliers to the deforestation-free objective. Today, much of the satellite imagery needed to do this analysis is freely available.

-

Engage suppliers. Besides informing suppliers of this due diligence and traceability system, work with them to ensure they implement practices that avoid deforestation. One important component is to offer technical and/or financial assistance to boost crop and/or livestock yields on their existing farmland and grazing land. This engagement can be facilitated by involving other supply chain actors, financial institutions, and non-governmental organizations.

This approach is low cost. The necessary data are freely available. The analysis can be done from one’s office, and it does not require someone going to a farm/ranch to do an on-site audit or verification. Combining this with a “mass balance” approach further keeps costs low when transporting the commodity to its destination. With a “mass balance” approach, the deforestation-free commodity can be mixed with non-deforestation-free commodities during processing and transport, but the volumes are tracked via ledger or blockchain (as opposed to keeping the tons of deforestation-free commodity physically segregated from the tons of non-deforestation-free commodity).

Who needs to act?

Due diligence and traceability measures require action by companies at all points within a commodity value chain. Pre-competitive, sector-wide collaboration to set standards and harmonize approaches can reduce inefficiencies that would otherwise result if each company developed its own unique approach.

For China to introduce regulations on due diligence and traceability for soft commodities, the Ministry of Ecology and Environment would need to coordinate with the Ministry of Commerce, the State Administration for Market Regulation, the General Administration of Customs, the Ministry of Agriculture and Rural Affairs, the National Forestry and Grassland Administration, and the Ministry of Industry and Information. The Government of China could use or build upon a suite of rapidly improving approaches, technologies, and systems that already exist (Box 9.9). It will be particularly important to engage with business enterprises when further developing and implementing due diligence and traceability systems in order to ensure the approaches used fit business processes and are cost-effective.

How does this build on existing Chinese efforts?

Box 9.9. Examples of Approaches and Tools to Support Due Diligence

A diverse array of existing tools and approaches can support companies to exercise due diligence and comply with related regulations. These include:

-

Free online forest monitoring systems that enable companies and regulatory agencies to access publicly available satellite and related data and assess which regions have ongoing deforestation. Companies can overlay this geospatial data with their suppliers’ sourcing areas to monitor deforestation and other risks that directly impact their own value chains.

-

Voluntary certification systems, based on a sustainability standard governed by a multistakeholder body, that offer third-party verification that commodities were produced in compliance with the standard and that the chain of custody is adequately controlled.

-

Mandatory producer-country certification systems that monitor and enforce compliance with regulatory standards for sustainable production and trade of soft commodities.

-

“Jurisdictional approaches” wherein an entire geographic or political region (e.g., a state, province, district, municipality) takes action to ensure soft commodities are produced legally and that targets for reduced deforestation or conversion of other ecosystems are met. Some jurisdictions have “produce and protect compacts” whereby farmers agree to avoid expansion into forests in exchange for assistance to improve yields on existing farmland.

-

“Risk screening” approaches where retailers, manufacturers, and traders distinguish regions or companies deemed “lower risk” (e.g., a high degree of confidence in legality and no deforestation or human rights breaches) from those deemed “higher risk.” Importers can prioritize the use of stricter control measures on higher-risk sources. These include legality verification, certification, greater traceability, and supplier engagement with continued purchasing contingent on suppliers making progress towards full compliance with sustainability standards. Here again, monitoring of land-use change impacts can come from free, publicly available satellite and related data.

China already has elements of due diligence and traceability in its regulations on products such as timber, food, and drugs. China also is at the forefront of digital technologies such as big data and blockchain, which can facilitate the traceability of commodity value chains and can build upon this technological leadership. The Chinese Academy of Forestry has developed a draft national timber legality verification system that would institute measures for verification of legal compliance, from forest management all the way through the value chain (“chain of custody”). This system has been piloted with a few large timber companies in recent years. China could build on this experience, expanding to small- and medium-sized enterprises, imported timber, and other soft commodities. In addition, the Ministry of Commerce has established a National Important Products Traceability System to track the production and distribution of key products such as food, drugs, rare earth minerals, and dangerous products. As a start, the ministry could add soft commodities to this system. Moreover, the proposed BRI Big Data Platform could save and provide data that feeds into traceability efforts.

Why is it important?

Due diligence and traceability are fundamental to green value chains. This is because they enable importers, financiers, the government, and consumers to distinguish those tons or shipments of soft commodities that meet “green” criteria from those that do not. When used in combination, due diligence and traceability can verify a commodity’s source location, the chain of custody, and compliance with legality, sustainability, and/or safety standards. They often also make good business sense, enabling companies to better manage logistics and ensure financial discipline throughout the value chain, as well as providing a competitive advantage to companies that can demonstrate they are procuring commodities from known and sustainable sources.

Where is this emerging as a new global norm?

An increasing number of multinational companies are using due diligence and traceability systems to achieve greener soft commodity value chains. For instance, companies such as Cargill, Golden Agri Resources, Louis Dreyfuss, Mondelez, and Walmart use “Global Forest Watch Pro” to monitor their soft commodity supply chains—starting at the farm—to distinguish green from non-green supplies. Food giants like Mars, Unilever, and Wilmar use the Palm Risk Tool to identify sources of palm oil that are at “high risk” of being unsustainably grown. COFCO International now tracks its soybean supply chains from several Brazilian sources. In response to China’s Food Safety Law of 2015, Chinese beef processor Kerchin has deployed blockchain and other traceability technologies to track the production and shipping of frozen beef—thereby avoiding the risk of contaminated meat entering its supply chain.

Governments are introducing traceability systems, too. For example, Indonesia uses bar codes to track timber from harvest to port and subsequently grants export permits through an online system. New Zealand and Uruguay have developed national traceability systems for cattle to ensure meat quality, sanitary standards, the transparency of origin, and chain of custody.

9.4.2.3 Invest in Domestic Capacity to Rationalize Food Value Chains and Improve Sustainable Diets

What is it?

China could invest in the technology and manufacturing capacity to produce nutritious, plant-based foods that meet growing domestic (and international) demand for protein. By becoming a plant-based protein manufacturing “powerhouse,” China could increase food self-sufficiency, improve citizen health (e.g., lower saturated fat and cholesterol levels in domestic diets), increase food safety (e.g., less risk of contamination), and reduce the risk of zoonotic diseases. The resulting value chain would be less reliant on imports (which is better for stability and for trade balances) and “greener” (e.g., no deforestation and low greenhouse gas emissions). In addition, this investment would create an entirely new 21st-century industry where China could attain global market leadership.

Who needs to act?

Action would be needed by both the public and private sectors. For example, the Ministry of Agricultural and Rural Affairs could coordinate with the State Administration for Market Regulation (as well as the Ministry of Industry and Information) to ensure an adequate domestic supply of raw material and to set any needed national standards for plant-based foods. Public and private investment into food science research and innovation are needed to accelerate plant-based protein product development.

How does this build on existing Chinese efforts?

China’s large investment in agricultural technology and land infrastructure makes it well-positioned to meet the demand for plant-based meat ingredients. As one of the world’s largest producers of pulses and exporters of plant-based raw materials, China has already developed processing infrastructure that can support this new industry. In 2016, for instance, China had the capacity to process over three quarters of global soy protein isolate and half of textured soy protein. Soybean is currently the most utilized raw material to manufacture plant-based meat products in China. Other candidate raw materials grown in China include konjac, soybean, and fungi.

Chinese investors are already devoting financial resources to startups to advance technological development and begin to scale these products. For example, Bits × Bites—China’s first venture capital firm devoted to food tech—has invested in several plant-based startups around the world. Some Chinese plant-based companies, such as Whole Perfect Food and Godly, are starting to become well recognized.

Investing in this growing set of opportunities also fits with China’s broader efforts to ensure food security. Amid the COVID-19 pandemic, China has prioritized food security and a stable supply of agricultural products in its efforts to maintain supply chain security and competitiveness. In 2020, China will develop a new national medium-to-long-term food security plan and carry out a response plan to ensure food security under COVID-19 [58]. The NDRC has highlighted diversifying the import of major agricultural products and securing a stable and safe supply of key products, including grain, edible oil, meat, eggs, fruits, and vegetables in its annual draft report to the People’s Congress in May 2020 [58].

Why is it important?