Abstract

Japan’s debt-to-gross domestic product (GDP) ratio is the highest among Organisation for Economic Co-operation and Development (OECD) countries. This chapter will answer the question of whether Japanese government debt is sustainable. While the Domar condition and Bohn’s condition are often used in the literature to check whether a government’s debt situation is in a dangerous zone, this chapter will show that the Domar condition is obtained only from the government budget constraint (namely the supply of government bonds) and does not take into account the demand for government bonds. A simple comparison of the interest rate and the growth rate of an economy using the Domar condition is not adequate to check the stability of a government’s budget deficit. Both the interest rate and the growth rate of the economy are determined endogenously in the model. This chapter shows that Bohn’s condition satisfies the stability of the government budget in the long run by imposing constraints on the primary balance. However, Bohn’s condition does not achieve economic stability—even if the condition is satisfied, the recovery of the economy may not be achieved. This chapter will propose a new condition that satisfies both the stability of the government budget and the recovery of the economy. The chapter will shed light on these issues both theoretically and empirically. The empirical findings declare that in order to achieve fiscal sustainability based on the optimal fiscal policy rule provided in this chapter, both sides of the Japanese government budget (expenditure and revenue) need to be adjusted simultaneously. Moreover, the results show that the decrease in government expenditure must be more than the increase in tax revenue.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Notes

- 1.

In Feb 2016, the BOJ took further steps, and started a negative interest rate policy, by increasing massive money supply through purchasing long-term Japanese government bonds (JGB), Previously the BOJ only purchased short-term government bonds. This policy has flattened the yield curve of JGBs. Banks started to reduce purchasing government bonds, because the yield of short-term government bonds' became negative, and even for long-term government bonds up to 15 years the interest rates became negative. for more information see: Yoshino, Taghizadeh-Hesary, Miyamoto (2017) and Yoshino, Taghizadeh-Hesary, Tawk (2017)

- 2.

“Abenomics” refers to the economic policies advocated by Shinzo Abe, who became Prime Minister of Japan for a second time when his Liberal Democratic Party won an overwhelming majority in the general election in December 2012. Abenomics is distinguished by a set of policies comprising “three arrows”: (1) aggressive monetary policy, (2) fiscal consolidation, and (3) a growth strategy. For more information, see Yoshino and Taghizadeh-Hesary (2014b).

- 3.

We assume that the consumption function is a Keynesian consumption function, non-Ricardian type.

- 4.

\( \frac{\partial {B}_t}{\partial {G}_t}=\frac{B_{t-1}}{b_1-{B}_{t-1}}+1,\kern0.5em \frac{\partial {Y}_t}{\partial {G}_t}=\frac{\left({d}_1+{i}_1\right)+{d}_1{i}_1}{\Delta},\kern0.5em \frac{\partial \Delta {B}_t}{\partial {G}_t}=\frac{B_{t-1}}{b_1-{B}_{t-1}}+1 \)

- 5.

\( \frac{\partial {B}_t}{\partial {T}_t}=-\left(\frac{B_{t-1}}{b_1-{B}_{t-1}}+1\right),\kern0.5em \frac{\partial {Y}_t}{\partial {T}_t}=-\frac{\left({d}_1+{i}_1\right){c}_1+{d}_1{i}_1}{\Delta},\kern0.5em \frac{\partial \Delta {B}_t}{\partial {T}_t}=-\left(\frac{B_{t-1}}{b_1-{B}_{t-1}}+1\right) \)

- 6.

Below are the results of the regressions:

Equation 3.4: Demand for government bonds: Δ(B t ) = 8444390 + 1336455(r t )

Equation 3.7: Investment function: Δ(I t ) = 85153 − 2125[Δ(r t )]

Equation 3.8: Consumption equation: C t = 9445 + 0.53(YD t )

Equation 3.9: Deposit equation: \( \Delta \left({W}_t^D\right)=-10828237+0.22\left({YD}_t\right)-675616\left({r}_t\right) \)

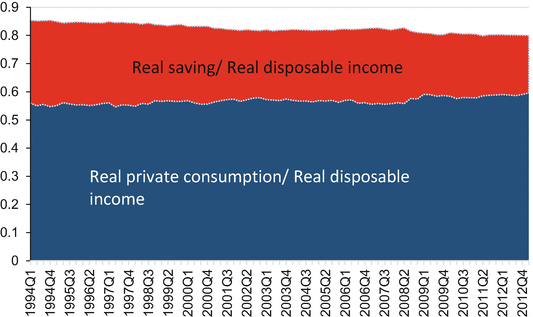

Equation 3.8 shows the marginal propensity to consume to be 0.53, and Fig. 3.8 empirically shows this fact.

Fig. 3.8

Japanese real private consumption and real household savings as a percentage of real disposable income, 1994Q1–2013Q1. (Source: Nikkei NEEDS)

References

Bohn H (1998) The behavior of US public debt and deficits. Q J Econ 113(3):949–963

Bohn H (2005) The sustainability of fiscal policy in the United States, CESifo working paper no 1446. Center for Economic Studies and Ifo Institute, Munich

Domar ED (1944) The burden of the debt and the national income. Am Econ Rev 34(4):798–827

Hoshi T, Ito T (2014) Defying gravity: can Japanese sovereign debt continue to increase without a crisis? Econ Policy J 29(7):5–44

McNelis P, Yoshino N (2012) Macroeconomic volatility under high accumulation of government debt: lessons from Japan. Adv Complex Syst 15 Suppl No (2):1250057-1–1250057–29

Polito V, Wickens M (2007) Measuring the fiscal stance. Discussion paper in Economics, No. 2007/14. The University of York, York

Yoshino N, Mizoguchi T (2010) The role of public works in the political business cycle and the instability of the budget deficits in Japan. Asian Econ Pap 9(1):94–112

Yoshino N, Mizoguchi T (2013a) Optimal fiscal policy rule to achieve fiscal sustainability: comparison between Japan and Europe. Presented at Singapore economic review conference, Singapore, August 2013

Yoshino N, Mizoguchi T (2013b) Change in the flow of funds and the fiscal rules needed for fiscal stabilization. Public Policy Rev 8(6):775–793

Yoshino N, Taghizadeh-Hesary F (2014a) Three arrows of “Abenomics” and the structural reform of Japan: inflation targeting policy of the central bank, fiscal consolidation, and growth strategy, ADBI working paper no 492. Asian Development Bank Institute, Tokyo

Yoshino N, Taghizadeh-Hesary F (2014b) An analysis of challenges faced by Japan’s economy and Abenomics. Jpn Polit Econ 40(3–4):37–62

Yoshino N, Taghizadeh-Hesary F (2016) Causes and remedies of the Japan’s long-lasting recession: lessons for China. Chin World Econ 24:23–47

Yoshino N, Taghizadeh-Hesary F, Miyamoto H (2017) The effectiveness of the negative interest rate policy in Japan. Credit Cap Markets – Kredit und Kapital 50(2):189–212

Yoshino N, Taghizadeh-Hesary F, Tawk N (2017) Decline of oil prices and the negative interest rate policy in Japan. Econ Pol Stud 5(2):233–250

Yoshino N, Vollmer U (2014) The sovereign debt crisis: why Greece, but not Japan? Asia Eur J 12(3):325–341

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Asian Development Bank Institute

About this chapter

Cite this chapter

Yoshino, N., Mizoguchi, T., Taghizadeh-Hesary, F. (2017). Optimal Fiscal Policy Rule for Achieving Fiscal Sustainability: A Japanese Case Study. In: Yoshino, N., Taghizadeh-Hesary, F. (eds) Japan’s Lost Decade. ADB Institute Series on Development Economics. Springer, Singapore. https://doi.org/10.1007/978-981-10-5021-3_3

Download citation

DOI: https://doi.org/10.1007/978-981-10-5021-3_3

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-10-5019-0

Online ISBN: 978-981-10-5021-3

eBook Packages: Economics and FinanceEconomics and Finance (R0)