Abstract

Property wealth represents the most important wealth component in nearly all OECD countries. Homeownership is linked to wealth accumulation in several ways: Wealthier households are more likely to buy a house or apartment, home owners tend to save more and rising house values typically yield higher returns than money in a bank account. Moreover, owners can borrow on a mortgage to finance, e.g., the formation of an enterprise or other economic activities. At the aggregate level, these relations can explain why countries with low rates of homeownership tend to have a high wealth inequality.

This paper looks at wealth and homeownership in Germany and Switzerland. These countries show the lowest proportion of owner-occupiers in Europe and a high wealth inequality. We analyse to what extent this high inequality can be explained by homeownership status. In the first part of this contribution, we review explanations for the low share of owner-occupiers in the two countries. In the second part, we analyse wealth and homeownership empirically using data of the SHP and the German Socio-Economic Panel (SOEP) from 2012. We make use of decomposition methods to analyse how renter and owner households differ in wealth levels and wealth inequality.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Introduction

Although wealth is a central dimension of social inequalities, scientific attention to wealth inequality is relatively recent (e.g., OECD 2015). Several studies have pointed out that wealth inequality is particularly high in countries with low homeownership rates (Kaas et al. 2015; Mathä et al. 2014).

In this contribution, we focus on homeownership and wealth in Switzerland and Germany, which show the lowest proportion of owner-occupiers in Europe with about 40% and 50% of households, respectively. Other European countries have ownership rates of more than 90%, for example, in Romania, Lithuania or Hungary (Eurostat 2015). Nevertheless, real estate represents the most important wealth component, even in Switzerland and Germany (Grabka 2014; Swiss Federal Statistical Office 2014).

Homeownership is not only related to wealth inequality but also to average net worth. There are different explanations for the relationship between homeownership and wealth. First of all, only relatively wealthy households might be able to purchase their own home. Because real estate is typically the most valuable asset category, low ownership rates translate into low values for net wealth at the individual and the country level (Kaas et al. 2015). Secondly, house ownership has shown to have a positive effect on saving behaviour (e.g., Di et al. 2007) and thus contributes to higher wealth levels and lower wealth inequality. The forced repayments of mortgages are an important driver for regular savings. Thirdly, lower wealth inequality may result from rising values of real estate. Usually, investment in property yields higher returns than the money in bank accounts. Fourth, property wealth enables an owner to borrow on a mortgage to finance, e.g., a formation of an enterprise or other economic activities, which will pay off later. Having said that, fifth, one can also argue that wealth levels and wealth inequality depend on the extent of the social security system, particularly for old age and health. The necessity for private wealth accumulation tends to be smaller in countries with a comprehensive social security system, as is the case in Germany and Switzerland. Compulsory levies impair wealth accumulation and the investment in housing and leave a large part of the population with a small net worth.

Some of these mechanisms present a causal effect of homeownership on wealth accumulation. Owning a home provides financial security and produces (additional) wealth. This implies that wealth inequality could be lowered by encouraging homeownership. However, there have been doubts on the financial and social benefits of owning for low-income households (Shlay 2006). The housing burst in several countries (e.g., US, Spain or Ireland), and the numerous foreclosures in particular, have raised awareness about the risks of homeownership. Homeownership is particularly risky for low-income households that finance their property with a high level of debt. In a financial crisis, market values decline, while the debt remains unchanged, thus leading to indebtedness. For example, in the US, the median net worth dropped by 44% between 2007 and 2010, and the share of owner-occupiers shrank by nine percentage points (Wolff 2016). In sum, it is controversial whether facilitating access to property to households with little wealth is a means to fight social inequalities.

Homeownership in Switzerland and Germany

Switzerland’s ownership rate is low from a comparative perspective but has increased in the last decades from 31% in 1990 to 37% of all households in 2010. This increase is somewhat surprising considering that owning has become more expensive relative to both renting and to the average income (OECD.Stat 2016). Since 2000, prices for private real estate have risen by 159%. The high prices due to the scarcity of land and high construction quality standards present the most frequently mentioned reason for the low ownership rate. Other explanations are a well-functioning rental market with protection for renters (restrictions on rent increases and eviction), a restrictive mortgage system and high down-payment requirements.Footnote 1 There is a wide variation in ownership rates within Switzerland, with low ownership in urban areas and ownership rates over 50% in rural areas.

The legislation that is relevant for ownership varies strongly between cantons and municipalities, but there is no general political promotion of homeownership (Thalmann 1999). Despite different taxes for homeowners (wealth tax, income tax on imputed rents, transfer taxes, property taxes), owners have a small tax advantage over renters (Bourassa and Hoesli 2008).Footnote 2 However, also taxes vary strongly among cantons and municipalities.

In Germany, the share of owner-occupiers was 46% in 2010 (Statistisches Bundesamt 2013). However, there are significant differences between East and West Germany. While the respective share is almost 50% in the West, only about a third of all East-German households are owner-occupiers (Grabka 2014). Since reunification, the share of owner-occupied households increased by eight percentage points in both parts of the country.

In East Germany, the low share of owner-occupied households can be explained by the socialistic economic system in the GDR, which did not promote the possession of property. In West Germany, the respective share is still rather low because of the vast demolition during the World War II. In addition, about 14 million displaced persons fled between 1945–1950 from formerly German regions in the East to the GDR and FRG. Thus, there was a significant shortage of living space after World War II (Kesternich et al. 2014). The government in West Germany reacted with housing programmes, particularly through social housing.Footnote 3 Private housing construction was promoted by the tax deductibility of construction costs or mortgage interest. From 1996 to 2006, this has been replaced by a direct monetary value. Since then, there has been no nation-wide programme that promotes homeownership in Germany. Another reason for the low share of owner-occupied housing in Germany is its long tradition of a well-developed rental market with a comprehensive rent control, thus leading to rather low rental prices. When comparing the costs for renting compared to an acquisition of owner-occupied housing, Voigtländer (2014) finds that for nearly three-fourths of German counties, renting was superior to buying in 2009.Footnote 4 Since 2009, there has been a strong increase in property prices, particularly in city regions. Sales prices for condominiums have increased by 55% between 2009 and 2016 (Kholodilin and Michelsen 2017).

Until 1982, the acquisition of owner-occupied property was burdened by a real estate transfer tax of 7%. Between 1982 and 2006, a reduced nationwide tax of 3.5% was established. Since then, every federal state can set its own tax rates that vary between 3.5% in Bavaria and 6.5% in Brandenburg. A property tax must be paid by owner-occupiers, but the taxable value is—like in Switzerland—clearly below market values. There are no other owner-specific taxes.Footnote 5

In sum, house ownership in Germany and Switzerland shares many similarities: low share of homeownership, high (and rising) house prices, a well-developed renter market, a restrictive mortgage system and high down-payment requirements. The main differences are the high population growth combined with the limited land in Switzerland, while population is shrinking in rural areas in Germany but growing in cities.

Data

For Switzerland, we use data of the Swiss Household Panel (SHP) from 2012 that include two questions on wealth. A first question asks homeowners to estimate the value of their property after deducting mortgages. In a second question, respondents are asked to estimate the amount of the remaining wealth. Wealth information is available for 4467 households; values for 812 have been imputed. Because of these general questions, wealth estimates are approximate. It is therefore important to compare data of the SHP with other available data sources, even if true values are unknown.

For two reasons, the average levels of net worth are likely to be underestimated in the SHP. First, general questions yield typically lower values than when information is collected for different wealth components separately. Second, surveys in general do not adequately cover the very top of the wealth distribution. Because wealth is extremely concentrated, outliers have an enormous impact on the average measures. According to tax records, 1% of Swiss residents hold 40% of the total wealth (Foellmi and Martínez 2017). Because this study focusses on comparisons between groups rather than wealth concentration, we are however not interested in the top wealth holders.

As an indication for data quality, one can compare the wealth levels in the SHP with national accounts. Net worth per capita in the SHP amounts to 200,548 CHF, while the respective figure from the national accounts shows an average net worth of 263,466 CHF per person (Swiss National Bank, net worth corrected for pension funds). Wealth in the SHP therefore amounts to 76% of the national accounts.Footnote 6 Another test of the SHP data is a comparison with CH-SILC 2015, which included a relatively detailed wealth module. The average net worth per person in SILC 2015 was 254,139 CHF, which was slightly higher than in the SHP 2012.Footnote 7 But considering the general wealth increases between 2012 and 2015, the values seem relatively close. Overall, the SHP seems well suited to study differences between owners and renter households.

For Germany, we make use of the Socio-Economic Panel (SOEP). The SOEP started in 1984 and expanded to East Germany in 1990. As the SHP, the survey is representative for the population and is conducted every year. We also use the survey year 2012 with more than 10,000 households, where information about ten different asset and debt components had been collected.

In the following we analyse data at the household level. Wealth is measured as per capita net worth, which is the sum of all assets less the value of debts. Wealth is however censored at 0 in Switzerland (no negative values).Footnote 8 The wealth measure does not include occupational pension plans and promised entitlements to public retirement payments or household effects.

Results

House Ownership, Wealth and Age

We start with descriptive characteristics of the average wealth and wealth inequality.Footnote 9 First of all, Table 12.1 shows that Swiss residents are much wealthier than German residents. Secondly, owner households are much wealthier than renter households (five times in Switzerland, seven times in Germany). Even if owner households are a minority (46% in Germany, 37% in Switzerland) they own as much as 86% of the total wealth in Germany and 75% in Switzerland. Thirdly, Table 12.1 shows the decomposition of wealth inequality for the Squared Coefficient of Variation (SCV). Only 3.6% of the inequality in Switzerland and 6.7% in Germany are due to differences between groups. Thus, wealth inequality occurs mainly within owners and renters. Forth, the SCV and the Gini index by group reveal that inequality within renter households is considerably higher than inequality within owner households. Not the wealth gap between owners and renters but the lower inequality within owner households is the main reason that low homeownership rates are associated with high wealth inequality. An increasing share of homeowners implies a lower wealth inequality.

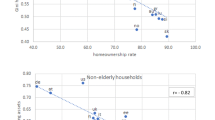

We next look at the relationship between age and wealth. Homeownership has shown to be most beneficial for wealth accumulation when houses are bought at a young age. Households have a longer period to accumulate wealth and to repay mortgage debt, respectively. Figure 12.1 predicts the nonlinear relationship between wealth and age of the household head (main income earner in Switzerland, reference person in Germany) using linear regression. The figure shows that house owners are wealthier than renter households but that the gap widens substantially over the life cycle. While the difference between the average wealth of owners and renters is rather small for household heads up to 40 years, it increases quickly thereafter.

Age wealth profiles by ownership status 2012. Note: Predicted wealth refers to national currencies. Information for owners in Switzerland below 30 years of age is not presented due to a small number of observations. Source: SHP, SOEPv32, private households only

There are different possible explanations for this pattern (see also Alik-Lagrange and Schmidt 2015). A first is that young renters also include future property buyers. They might either be saving to buy their own property or even possess the necessary assets but are waiting for a good opportunity to buy a home. At older ages, there are fewer households that prefer owning over renting and can afford buying at the same time. While this effect arises mainly through self-selection into homeownership, more savings of owner-occupiers are a second explanation for the increasing wealth gap between owner and renter households. Thirdly, owner-occupiers, who have been owners for a longer time, may have profited more strongly from rising property’s values than younger owners. Fourthly, the probability for significant inheritances is higher at higher ages. Wealth differences between renters and owners in precursor generations can insofar carry forward. Finally, the differences between ages might also be driven by cohort effects. But considering the similarity from Germany and Switzerland, it is unlikely that major historical events like the World War II and the German reunification are main explanations for the rising wealth gap between owners and renters with age in Germany.

Nevertheless, and considering that renting is a viable option in Switzerland and Germany, it is surprising that renters hardly accumulate wealth over the life cycle. Thus, other forms of self-selection might be relevant to explain the wealth difference. For example, if hedonists, who prefer current consumption over savings, are more prevalent among renters, this selection could explain the lower wealth levels of renters.

Another remarkable finding of Fig. 12.1 is the shape of the curve for owners at older ages. While the German households start dissaving at around age 65, the average wealth of owner-occupiers and to a smaller extent of renter households continues to rise to about 80 years of age in Switzerland. One possible explanation for this diverging pattern is the lack of care insurance in Switzerland compared to Germany, which encourages wealth accumulation even after retirement to finance care costs.Footnote 10 In contrast, intergenerational wealth transmissions might play an important role for the observed dissaving effect in Germany (Westermeier et al. 2016).

Explaining the Ownership Wealth Gap

To better explain the differences between renters and owners, we use decomposition methods, which are widely used for other group differences, most frequently for the gender–wage gap. The most widely used method is the Oaxaca-Blinder decomposition. Juhn et al. (1993) expanded this approach beyond the mean to different quantiles of the distribution and suggested decomposition into three components: characteristics, coefficients and residuals. More recently, counterfactual distributions are used to explain the differences between groups (see Fortin et al. 2010 for a review on decomposition methods). Here, we adopt the method proposed by Chernozhukov et al. (2013), which uses conditional quantile regression. Estimates have been obtained with the Stata command cdeco (for quantiles) and jmpierce (for the mean). The conditional wealth distribution of renters is used as the benchmark. This nonparametric decomposition method is advantageous because it not only focusses on the mean but also does not require assumptions about the underlying distribution.

To mitigate the influence of outliers in the wealth distribution, we apply the inverse hyperbolic sine transformation (Johnson 1949) of net worth for the conditional distribution. Explanatory variables encompass age, household type, gender, permanent income and its square term, educational levels, urban municipality, migration background, wealthy parents, bad health, the presence of siblings and received inheritances and bequest.

Results in Table 12.2 show that differences in these observable characteristics (column 2) explain only a small part of the wealth differences between renters and owners. At the mean, different socioeconomic characteristics explain 16% of the wealth differences in Switzerland and 32% in Germany, respectively. Looking at quantiles, we can see that composition effects become more important if one moves up in the wealth distribution. In Switzerland, the different characteristics of owners and renters explain 16% of the wealth gap at the 25th percentile and 29% at the 90th percentile. In Germany, the composition effect increases from 9% at the 10th percentile to 67% at the 90th percentile. The higher permanent income of owners compared with renters is the most important driver for the composition effect. However, the effects of observed characteristics (price effects in column 3) are much more important for wealth differences. For example, being an owner and having the exact same characteristics as a renter will lead to a higher net worth in both countries. Rising values of properties and more regular savings of house owners compared to renters are possible explanations for this finding. The impact of unobserved price and quantities is more relevant at the lower and the upper end of the wealth distribution. This indicates that other factors not considered in the regression analyses may play a role.

Summary

This chapter addressed the wealth inequality and wealth differences between owner and renter households in Switzerland and Germany. We have found that owner-occupiers hold on average five or seven times more per capita net worth than renters. Only a small part of wealth inequality can be explained with the wealth gap between owners and renters. In addition, wealth inequality is much lower in the group of owners. The high wealth inequality among renters is an important explanation for wealth inequality in Germany and Switzerland.

If one would like to reduce the high wealth inequality in Switzerland and Germany, promoting homeownership is a possible starting point. Results from a decomposition analysis show that so-called price effects rather than differences in characteristics explain the different wealth levels between owners and renters. There are two main explanations why becoming a homeowner is likely to increase wealth accumulation. Firstly, the rise in the value of property may lead to a higher net worth for owners. Secondly, owners on a mortgage are forced to save on a regular basis and thus accumulate wealth faster than usual tenant households (see also Grabka and Westermeier 2015). Owners might be more homogenous than renters in terms of wealth because rising prices and forced savings due to mortgage repayments affect a large majority of owners in the same way. A central challenge when considering ownership promotion programmes is, on the one side, enabling low-income households to become homeowners and avoiding a “lock-in phenomenon” on the other side, i.e., providing financial aid to affluent persons who would become owners anyway. Furthermore, ownership promotion programmes that alleviate the access to mortgages can bear the risk of creating a bubble, as has been seen in Spain or in the US; thus, well-considered policy reforms must be made.

Notes

- 1.

Requirements are an amortisation over 15 years to 65% of the house value, annual costs of owning a house must not exceed 33% of the gross household income and there is a minimum of 20% deposit for the purchase (second and third pillar assets can be used for this) and a ca. of 4% for close costs.

- 2.

The reasons for the tax advantage are that the taxed value of owner-occupied housing for wealth tax is clearly below market prices, the fact that interests for mortgages and costs for the maintenance of the house can be deducted from taxable income and that capital gains tax rates when a house is sold decrease with tenure in most cantons and taxes are postponed if a new property is bought.

- 3.

To give an example, between 1961 und 1990, 90% of all new dwellings were built with the aid of social housing programmes in Berlin (Holm 2007).

- 4.

Restrictions in the access to mortgages and rather high down-payment requirements and high transaction costs play an additional role preventing or dissuading many young households from buying a property at the beginning of their careers (Chiuri and Jappelli 2003).

- 5.

When selling, owner-occupied property taxes on capital gains were only raised if the time period between acquisition and sale was less than 10 years.

- 6.

National accounts also present the value of real estate. The value for real estate per capita in the SHP is very close to one of the national accounts (101,561 CHF vs. 119,923 CHF). However, because the variable in the SHP refers only to primary residence, the two values cannot be perfectly compared.

- 7.

The SILC data are not well suited for an analysis on homeownership because 34% of respondents have not indicated the current market value but the taxable or purchase value of the house, which are considerably lower. As a consequence, the wealth difference between owners and renters is likely to be underestimated in SILC.

- 8.

In SOEP, the share of households with a negative net worth is 7.5%.

- 9.

Weights provided by the SHP have been calibrated to match the official rate of homeowners.

- 10.

A similar age pattern can be found for the US, where an obligatory nursing care is not implemented either (Grabka et al. 2016).

References

Alik-Lagrange, A., & Schmidt, T. (2015). The pattern of home ownership across cohorts and its impact on the net wealth distribution: Empirical evidence from Germany and the US (Discussion Paper No. 11/2015). Deutsche Bundesbank, Research Centre.

Bourassa, S. C., & Hoesli, M. (2008). Why do the Swiss rent? The Journal of Real Estate Finance and Economics, 40(3), 286–309.

Chernozhukov, V., Fernández-Val, I., & Melly, B. (2013). Inference on counterfactual distributions. Econometrica, 81(6), 2205–2268.

Chiuri, M. C., & Jappelli, T. (2003). Financial market imperfections and home ownership: A comparative study. European Economic Review, 47(5), 857–875.

Di, Z. X., Belsky, E., & Liu, X. (2007). Do homeowners achieve more household wealth in the long run? Journal of Housing Economics, 16(3–4), 274–290.

Eurostat. (2015). Wohnstatistiken. http://ec.europa.eu/eurostat/statistics-explained/index.php/Housing_statistics/de. Accessed 18 Oct 2016.

Foellmi, R., & Martínez, I. Z. (2017). Volatile top income shares in Switzerland? Reassessing the evolution between 1981 and 2010. The Review of Economics and Statistics, 99, 793–809.

Fortin, N., Lemieux, T., & Firpo, S. (2010). Decomposition methods in economics. In O. Ashenfelter & D. Card (Eds.), Handbook of labor economics (Vol. 4A, 1st ed.). Amsterdam: Elsevier.

Grabka, M. M., (2014). Private Vermögen in Ost- und Westdeutschland gleichen sich nur langsam an. DIW Wochenbericht Nr. 40/2014, S. 959–964.

Grabka, M.M., & Westermeier, C. (2015). Real net worth of households in Germany fell between 2003 and 2013. Economic bulletin 34/2015, p. 441–450.

Grabka, M.M., Boenke, T., Wolff, E.N., & Schroeder, C. (2016). A comparative analysis of augmented wealth in Germany and the United States. Paper presented at the IARIW conference 2016, Dresden.

Holm, A. (2007). Der schwindende Rest. Sozialer Wohnungsbau in Berlin. In: MieterEcho 323/August 2007.

Johnson, N. L. (1949). Systems of frequency curves generated by methods of translation. Biometrika, 36, 149–176.

Juhn, C., Murphy, K. M., & Pierce, B. (1993). Wage inequality and the rise in returns to skill. Journal of Political Economy, 101(3), 410–442.

Kaas, L., Kocharkov, G., & Preugschat, E. (2015). Wealth Inequality and homeownership in Europe. University of Konstanz, Working Paper Series 2015–18.

Kesternich, I., Siflinger, B., Smith, J. P., & Winter, J. K. (2014). The effects of world war II on economic and health outcomes across Europe. The Review of Economics and Statistics, 96(1), 103–118.

Kholodilin, K., & Michelsen, C. (2017). Keine Immobilienpreisblase in Deutschland – aber regional begrenzte Übertreibungen in Teilmärkten. DIW Wochenbericht Nr., 25, 503–513.

Mathä, T., Porpiglia, A., & Ziegelmeyer, M. (2014). Household wealth in the European area: The importance of intergenerational transfers, homeownership and house price dynamics. ECB Working Paper 1690, European Central Bank.

OECD. (2015). In it together: Why less inequality benefits all. Paris.

Shlay, A. (2006). Low-income homeownership: American dream or delusion? Urban Studies, 43(3), 511–531.

OECD Stat. (2016). Price to rent ratio. Stats.oecd.org. Accessed on 20 Oct 2016.

Statistisches Bundesamt. (2013). Zensus 2011: 80,2 Millionen Einwohner lebten am 9. Mai 2011 in Deutschland. Pressemitteilung Nr. 188 vom 31.05.2013.

Swiss Federal Statistical Office. (2014). Vermögenslage der privaten Haushalte. Neuenburg: BFS.

Thalmann, P. (1999). Which is the appropriate administrative level to promote home ownership? Swiss Journal of Economics and Statistics (SJES), 135(I), 3–20.

Voigtländer, M. (2014). Mieten oder Kaufen – Eine Analyse für die deutschen Kreise. IW-Trends 2/2014,

Westermeier, C., Tiefensee, A., & Grabka, M. M. (2016). Erbschaften in Europa: Wer viel verdient, bekommt am meisten. DIW Wochenbericht Nr., 17, 375–386.

Wolff, E. N. (2016). Deconstructing household wealth trends in the United States 1983–2013. NBER working paper nr. 22704.

Acknowledgements

This contribution is based on the project “Wealth Distribution in Switzerland and Germany: Evidence from Survey data” financed by the Swiss National Science Foundation (Project FNS – D-A-CH-10001AL_166319).

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

<SimplePara><Emphasis Type="Bold">Open Access</Emphasis> This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.</SimplePara> <SimplePara>The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.</SimplePara>

Copyright information

© 2018 The Author(s)

About this chapter

Cite this chapter

Kuhn, U., Grabka, M. (2018). Homeownership and Wealth in Switzerland and Germany. In: Tillmann, R., Voorpostel, M., Farago, P. (eds) Social Dynamics in Swiss Society. Life Course Research and Social Policies, vol 9. Springer, Cham. https://doi.org/10.1007/978-3-319-89557-4_12

Download citation

DOI: https://doi.org/10.1007/978-3-319-89557-4_12

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-89556-7

Online ISBN: 978-3-319-89557-4

eBook Packages: Social SciencesSocial Sciences (R0)