Abstract

In order to successfully achieve sustainable corporate development, enterprises have to define and implement a pragmatic strategy. In that pursuit, the discussion of motivation and reasoning behind incorporating sustainability strategies serves as a prelude to the thematic examination of challenges and courses of action in corporate strategy development and implementation. Especially in the context of sustainability, additional legislative and stakeholder requirement considerations make managing these tasks effectively, however, much more challenging. The firm’s overall objectives thus become multidimensional and have to be broken down to the individual departments and business fields. Consequently, considerable effort has to be devoted to the planning, measurement and evaluation, steering and control as well as optimisation and communication processes of the holistically defined corporate value creation. Furthermore, a solution for enterprise sustainability management and its evaluation is necessary for ultimately balancing economic, ecological and social performance factors, to ensure optimized decision-making.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

1 Organisational Framework for Sustainable Development

With respect to the increasing competitiveness, cost and price pressure as well as the limited availability of natural resources, efficiency—as the maxim of manufacturing—stands as an imperative. Nowadays, a new sense of responsibility towards future generations is emerging, as insights on the long-term effects of over-exploitation and environmental pollution are increasing. In the context of the evolution of this responsibility towards internal and external stakeholders, enterprises are confronted with the imminent challenge of adapting strategic orientation and operative value creation accordingly.

The linkage between the economic, ecological and social perspectives of the interaction of enterprises with their environment however, poses unique challenges in terms of potential internal conflicts of objectives. At the same time, it is questionable to what extent the attainment can be related to the three perspectives of sustainability. Thus long-term strategic orientation has to be recognised as a premise for sustainable development, so that potential short-term performance discrepancies are not misinterpreted as deficits, or implied as representing poor decision-making. This is assuming that sustainability is more than an ideological construct for the conscious influence and control of human and entrepreneurial behaviour. Instead, it has to be conditional to certain criteria and traceable or ascertainable. Numerous approaches for operationalising sustainable management are therefore focused on indicators, but remain, however, limited in their extent or integrity in order to avoid complexity.

The three-dimensional differentiated approach requires the simultaneous safeguarding of the economic, ecological and social capacity of the respective system and its environment for both the current and future generations (Dyllick and Hockerts 2002). Building on the definition of the German Bundestag, safeguarding economic performance is herein based on ensuring an adequate competitive situation as a driver of innovation and as a price-building mechanism, without however at the same time limiting the welfare of the individual involved. The preservation, and in some cases, the restoration of the capacity of natural systems, is thus the main objective of the environmental perspective. In that pursuit however, societal order is only sustainable if solidarity and social justice stand as the prerequisites to individual freedom and development in the process of determining the change of conditions and structures (Enquete-Kommission 1998).

Eco-effectivity strategies pursue absolute objectives in terms of reducing environmental pollution, as achieved through the use of renewable energy sources, recirculation of products, by-products and materials into product lifecycles or natural systems, as well as the limitation of environmental pollutants. Eco-effectivity thus refers to the degree of objective attainment, where the target is directly tied to the reduction of environmental or social burdens (Schaltegger 2000).

The fundamental strategy of efficiency is based on the objective of increasing resource productivity through the minimisation of resources deployed in relation to the maximised output with respect to the entire lifecycle. This is commonly achieved through product and process optimisation or innovation as well as procedures and product characteristics profiles that influence the operating condition and lifespan of the product (Enquete-Kommission 1998; OECD 2010). The eco-efficiency strategy hence refers to resource efficiency in relation to production processes. The substitution of conventional materials—therein enabling the use of less material or the construction of lightweight structures, recyclable materials or those that have lower pollution potential—serves to support the pursuit of eco-efficiency. Socio-efficiency can be expressed in an analogy, wherein value added is expressed in relation to social burden (Schaltegger 2007).

The analysis of a growing world population and simultaneous depletion of natural resources inevitably calls for confrontation with human consumer behaviour (Huber 2011). Sufficiency in an economic context here describes an alignment of consumer behaviour towards a sufficient consumption that accounts for resource depletion with existing technologies. Applied to the organisational level, this entails a limitation of production to a level below the possible growth boundary, so as to avoid overconsumption of natural resources (Huber 2000). The potential for growth of enterprises is not directly limited by the sufficiency strategy. The environmental and social impact is however minimised when implicit consideration of the long-term utilisation of products is taken into account. This represents an attempt at finding an optimal balance between economic value creation and the reduction of environmental pollution and social burden (Bergmann 2010).

Beyond process and product optimisation, the consistency strategy requires a structural change in the utilisation of resources and energy as well as restructured usage of natural drains. This explicitly calls for innovation capability with respect to new technologies, material as well as processes and products (Huber 2011).

This basic model can be extended by four fundamental principles, including responsibility, cooperation, and circular as well as functional orientation. These are possible operational principles held by economic actors, yet are in some cases redundant reiterations of the specifications of strategies and principles on a conceptual level (Dyckhoff and Souren 2008).

From a system theoretical point of view, cause-effect relationships are possible within and between the three dimensions of sustainability. These (inter-) dependencies may be positive or negative, respectively weakening or strengthening effects on the baseline objective of preserving ecological, economic and social capital. The dependencies may be characterised by place, time and reflexivity (Gleich and Gößling-Reisemann 2008). Hence, the effects of actions implemented may appear within the given system currently under consideration or surface in different systems. Simultaneous and delayed effects are often more difficult to detect however, as simultaneous effects may be interpreted as independent, while latent effects may go completely undetected.

2 Incorporating Sustainability Strategies

In order to meet the requirements set forth by the triple bottom line (Dyllick and Hockerts 2002) and the sustainability strategies, enterprises have to adapt their own corporate strategies. In this section, the reasoning behind implementing sustainability as part of the corporate strategy is examined, and the main motivational aspects are highlighted.

While the term strategy stems from a military context (Clausewitz 1935; Giles 1910), the conceptual integration into the context of corporate management in terms of strategic planning and later strategic management, was undertaken over half a century by scholars from varying fields (Will 2012). Originating from conceptions of efficiency as the main driver of productivity (Taylor 1911) and the relation of experience to cost-efficiency (Henderson 1973), competitiveness then took over the corporate strategy discussion, later expounded upon with differentiated business strategies (Porter 1985). The basis for developing a strategy can be dominated by external circumstances such as the market or environment. Moreover, the enterprise typically positions itself through the lens of its internal resource-based perspective—creating value and competitiveness through the deployment of core competencies (Prahalad and Hamel 1990). In that process, a basic definition of strategy as the long-term oriented behaviour of the corporation in pursuit of achieving defined objectives (Welge 2001) needs to be expanded, to account for meeting the corporation’s (and its internal and external stakeholders) objectives together with safeguarding the same possibility for future generations. In so doing, economic, ecological and social capital have to be expanded, yet sustained for the future (Dyllick and Hockerts 2002).

Based on the historic development of the term and discipline, limitations set forth by sustainability strategies seem contradictory and require closer examination. Initially, the motivational aspects attached to integrating sustainability requirements into the corporate reality are analysed. As for the scientific development of this aspect, a main structuring characteristic lies in the origin of the motivation. Where early contributions were focused on external factors, internal motivation and connecting drivers have gained in significance. Figure 1 gives an overview of the main motivational factors and drivers for corporate sustainability (Bansal and Roth 2000; van Marrewijk and Werre 2003; van Marrewijk 2003; Schaltegger and Burritt 2005; Epstein and Buhovac 2014; Windolph et al. 2014; Lozano 2015; Engert et al. 2016).

Motivational factors and drivers for corporate sustainability

Upon consideration of the motivations behind implementing sustainability into the corporate strategy, a new or adapted strategy has to be defined. In a procedural approach to strategy development, the main imperatives and courses of action are discussed in the following section. Here we propose considering the options to (1) adjust the corporate strategy to include objectives regarding economic, ecological and social performance; (2) to define a specific sustainability strategy as part of the corporate strategy and (3) to redefine the corporate strategy based on the premise of creating a holistic sustainability strategy (Figge et al. 2002). After the successful implementation of sustainability aspects in the strategizing phase, proactive management is needed in order to achieve the sustainability objectives.

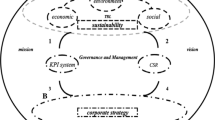

3 Management of Corporate Sustainability Performance

The management of organisations is described here in a stepwise approach (Fig. 2), addressing the building blocks of the business model, the corporate strategy, the business processes and the resources deployed. In order to improve the performance—in this particular context the sustainability performance—purposeful actions need to be planned, implemented and monitored. Overall, the dynamics of the business operation, decisions taken and the outcome, all need to be recognised in order to establish a comprehensive view of the cause-effect relations within and across the organisation’s borders. Communication with relevant stakeholders takes on a key role in that process, as transparency requirements increase. Internal and external communication must become an established activity of organisations that aim to make information available about their performance beyond the standard financial data reporting.

Stepwise approach for the management of corporate sustainability (Galeitzke et al. 2016)

3.1 Definition of the Business Model and Business Success as the Baseline for Strategy Development

The path of sustainable corporate development needs to be outlined for any business with specific deliberation on its internal and external environment. To achieve sustained success, the organisation must pinpoint its concrete objectives and values. These should be, furthermore, clearly understood, accepted and supported by the employees of the organisation (ISO 2009). It is therefore necessary to explicate the business model and the enterprise’s potential innovation as an integral or complementary part of strategy development.

To do adequate justice to the topic of sustainability as a whole, the following perspectives have to be considered within the process of business model definition/innovation:

1. Economic Perspective—While the traditional economic challenges are to increase the company’s value and to increase the profitability of products and services, the challenge with regards to economic sustainability lies in making environmental and social management as economical as possible.

2. Environmental Perspective—All actions of an enterprise affect its ecosystem. Thus, companies are encouraged to reduce the absolute level of their negative environmental impact resulting from production processes, products, services, investments etc. to a considerable extent, where the largest possible decrease is desirable. The largest possible decrease is however desirable.

3. Social Perspective—In order to achieve sustainable value creation within the social dimension, the social issues of focus have to provide a real competitive advantage. Such advantages could be obtained by increasing revenues, or reducing risks or operational costs. In this pursuit, the tension between social and economic pressure is relieved as both society and businesses enjoy tangible benefits at the same time.

Combining fragments or modules of a company is a fundamental aspect in several business model definitions (Osterwalder and Pigneur 2011; Johnson et al. 2008; Wirtz 2010; Mitchell and Coles 2003), serving the purpose of creating products and services and thereby creating, providing and maintaining value (Wirtz 2010; Johnson et al. 2008; Osterwalder and Pigneur 2011). In this context, value creation is used for strengthening the customer relationship and competitive advantage (Wirtz 2010). These components of business model innovation can be summarised as illustrated in Fig. 3.

Constituents of business model innovation definitions (Schallmo 2013)

Nowadays innovation is a major key for sustainability due to the fact that the future society demands innovative products, processes and services, without losing out on efficiency (Clausen 2011). Product or incremental process innovations are neither a guarantee for success nor sufficient for coping with the emerging information, knowledge and time-competition (Stern and Jaberg 2010). Against this background, the innovation of business models has arisen as a new discipline, providing organisations with supplementary guidelines for differentiation models in the market place in pursuit of securing long-term competitive advantage. Relating the business model concept to sustainability (Lüdeke-Freund 2010) defines a sustainable business model as “a business model that creates competitive advantage through superior customer value and contributes to a sustainable development of the company and society.”

A business model basically defines the way in which a company operates. Sustainable Business model innovation can be an important leverage for change in a company to be considered sustainable and for coping with the emerging challenges in this context. This furthermore entails an expansion of the business model scope beyond green (FORA 2010), product-service-systems (Tukker 2004) or social issues (Yunus et al. 2010; Bocken et al. 2014). Brocken et al. developed a set of sustainable business model archetypes clustered by technological, social and organisational perspective for innovations as shown in Fig. 4 (Bocken et al. 2014).

Sustainable business model archetypes (Bocken et al. 2014)

These archetypes can be interpreted as an approach for business model innovation towards sustainability. They can initially assist in the process of embedding sustainability into existing business models or for the purpose of radical re-engineering of the business models and for delivering a sound starting point from which to broaden economic, environmental and social aspects in tackling the complementary process of strategy development.

3.2 Strategy Development

Today, enterprises are forced to align their own objectives with the needs of all their stakeholders. Particularly at a time characterised by shorter product life cycles, decreasing prices, new technologies, global markets and increasing sustainability demands, enterprises require an efficient process for their strategy development activities.

The term strategy was first recorded in the late 1950s in the economic doctrine of the Harvard Business School. As instruments of corporate management first evolved from the concept of strategy, the terms strategic planning, and consequently strategic management have been established. In English-speaking countries (Chandler 1962; Ansoff 1965; Schendel and Hofer 1979; Porter 1980), prominent pioneers provided crucial foundations. From this 50-year history of the strategy concept in the context of corporate governance, the following features of a strategy can be derived: the consideration of actions of other actors, proactivity and long-term orientation (Staehle and Conrad 1994).

Strategy in its initial context is generally used to establish conditions that will guarantee long-term economic success and thus the continuity of the company. For this purpose, a strategic success ensues, which ultimately leads to advantages over competitors (Rüegg-Stürm 2005; Grant 2005).

The development of a comprehensive strategy which not only concentrates on competitive benefits and thus on the economic value, presents itself however to be a much more complicated undertaking. With regards to the aspect of sustainability, the environmental and social dimensions have to be taken into account, and, moreover, the cause-impact relations likewise have to be adequately assessed.

Several companies appear to be active in the field of sustainability management. They may publish, for example, extensive sustainability reports. Yet their efforts nevertheless often remain unclear from a strategic perspective. Rather, the impression that sustainability issues are being tracked often tends to be the case, more than they are actually proceeding on the basis of a clear strategy (Baumgartner and Ebner 2010).

The development of a comprehensive enterprise strategy which meets all given requirements from internal and external stakeholders and specifically contains sustainability perspectives, is a process which requires a structured approach in the interest of keeping the complexity and uncertainty at a minimum level. The process of strategy development can be divided into four major phases as presented in Fig. 5 (Will 2012).

Strategy development

In the first step, information is preliminarily collected which describes the current situation of the company for establishing a general consensus on the initial situation (e.g. information about business environment, general corporate objectives or the corporate profile incl. development of earnings).

In the second step, the products and markets are categorised so as to quantify their respective contribution toward the overall business result. For visualisation, the findings can be represented e.g. in a product-market-chart. Based on this analysis, the current market situation of the company is evaluated. The aim of this step is to obtain a first rough estimation of the yield model to derive interesting advancements from the existing business model in the next step.

The major decisions regarding the incorporation of sustainability into the strategic decision-making process are derived in the step of assessing the strategic options for corporate sustainability. The starting point for the determining of suitable strategic options is captured in step 1, featuring the general corporate objectives and the current trends in the business environment. In addition, the current situation of the company examined in step 2 leads to the necessity of a fundamental decision on how exactly the company would like to deal with the challenge of sustainability without losing any growth potential. Baumgartner and Ebner (2010) recommend a set of profiles for sustainability strategy (Table 1) as a first means of orientation in the strategic decision-making process.

Each of these positions the company wants to occupy has to be evaluated by taking into account risks, chances and possible development scenarios regarding market penetration, product differentiation, market expansion or diversification. For the analysis of the relationship between sustainability and competitive strategy, (Baumgartner and Ebner 2010) propose two criteria: costs caused by the strategy, and the recipient of the resulting benefits.

Finally, a selection of a strategic option based on the assessment from the previous step has to take place in order to arrive at the detailed strategic objective as a conclusion.

Since an enterprise consists of several different units and elements which are interconnected on several levels (active vs. passive or strong vs. weak relationship), it is necessary to consider all influences and possible side-effects within the process of strategy implementation. In this context, many companies use enterprise processes as a common backbone for the different management disciplines with the objective of fast and consistent realisation of strategic issues at all levels of the enterprise (Jochem and Balzert 2010).

The use of process management approaches for transferring complex strategies down to the operational business will be examined in the following section.

3.3 Process Definition and Modelling

Process definition and modelling is of great importance in the pursuit of achievement of the company’s strategic and operational objectives. The aim is to improve the efficiency on the one hand, and the effectiveness of the company on the other hand, so that its total value can be increased. Processes and process management are connected to two essential signifiers for ensuring effectiveness and efficiency in the company. First, the corporate strategy determines the processes which are required and which strategic objectives are to be implemented alongside them. It forms the basis for process identification and target orientation. This involves changes in corporate strategy, entailing changes in the processes itself. Secondly, the customer or stakeholder orientation determines what expectations and requirements have to be met through the processes. Therefore, the process definition extends from the requirements of the customer to the delivery of the process results to the client. It is important that the terms of the processes of corporate strategy and customer reference in the context of process management are coordinated (Jochem and Balzert 2010). Figure 6 illustrates the connection of corporate strategy and its operationalisation via an integrated management.

Connection of corporate strategy and process management

The comprehensive development and implementation of a corporate sustainability strategy which meets the requirements of the economic, environmental and social perspective, require a sound information basis from which to proceed. The various management disciplines involved have to be addressed in such a way that the attendant complexity is reduced to a minimum. A promising approach for visualizing and therein explaining the interrelation of varied enterprise objects lies in enterprise modelling.

In Vernadat’s view (1996), an enterprise model is the basis for the understanding of a company, whereby the relevant structural and dynamic components and their interactions are described.

Enterprise modelling describes relevant processes and structures of a company or organisation and their mutual relationships. The applications are designed extend to the illustration of the enterprise architecture, the root cause analysis of operational problems, strategy development, process optimisation or the management of business collaborations, among other topics (Sandkuhl et al. 2013).

Thus, the process management commences with the alignment of the processes and the sustainability strategy, which means defining the value-adding processes and objectives to be achieved. In the following phase of process design, the defined processes will be designed in detail, modelled and optionally documented. In the course of the implementation of the processes in the organisation of the company, the evaluation of the processes is carried out in terms of target-achievement, and where applicable, harmonisation or standardisation can be required. Finally, the actual controlling of processes follows, related to the entire corporate controlling process, resulting in impacts on the strategic development.

Both the challenges and the opportunities which integrated mapping of process management and sustainability offers, lie mainly in the mastery of increasingly complex planning processes. Based on enterprise models that unite the perspectives of different strategic planning disciplines and also support them with integrated model-based planning and evaluation instruments, the objective of corporate sustainability is pursued holistically (Dyllick and Hockerts 2002).

An important and critical success factor remains however unconsidered within enterprise models. The implementation of a sustainable development strategy requires not only an excellent knowledge of the internal processes and structures, but also, for example, of relationships with customers and partners, i.e. intangible assets. The role of such assets in terms of sustainability is briefly introduced in the next section, along with an approach for the integration of these values into the development of corporate sustainability.

3.4 Resource Definition and Impact Analysis

In order to provide products or services, an organisation will combine different types of resources like human skills and knowledge, natural materials and social structures, by using machinery, infrastructures and financial assets. A sustainable organisation will maintain and, wherever possible, enhance these capital assets, rather than exhaust them (“capital stewardship”) (Knight 2006; ARE and DEZA 2004). In turn, the design of the business processes constitutes the interrelation of the business operation, its resources and performance as well as the impact on the economic, social and environmental dimensions (Fig. 7). If, for instance, economic sustainability is interpreted as an expansion of the private welfare maximisation, enterprises have to ensure the long-term functionality and effective performance of their operation. Consequently, the design of the business processes needs to be directed towards the effective, efficient and beneficial use as well as towards the development of the capital assets involved. In this context, the capital-based approach refers to the relevance of different types of resources and makes a basic distinction between tangible and intangible resources. These are then employed in business processes to improve the organisational performance.

Reference model for corporate sustainability

Tangible resources, meaning those resources that are material or substantial, are composed of financial, manufactured and natural capital (IIRC 2013).

Financial capital is the sum of available financial resources that are utilised to fund the organisation’s operation. Thus, the product and service provisions are financially sustained through capital obtained via revenues, investments, debt, equity or grants.

Manufactured capital meanwhile comprises all physical objects that are employed by the organisation in order to produce and deliver its products and services. This physical part of the production system includes infrastructure and buildings, operating equipment as well as measuring, storage and transport utilities (Westkämper and Decker 2006). These objects can be obtained from third parties or in-house production.

On the basis of the classical understanding of “land” as a major factor of production, natural capital comprises all natural resources, processes and systems available (Harris and Roach 2013; IIRC 2013).

The classification of intellectual capital as an intangible resource follows the principle of the harmonisation of intellectual capital factors into standard repositories. Human, structural and relational capital are herein subdivided into standard success factors (Mertins and Will 2008) which map the most common types of intellectual capital. In order to comply with the system attached to modelling processes, the repository of intellectual capital factors needs to be adapted on a case-by-case basis. At the same time, considerations for directing this approach towards sustainable corporate development are taken in the following adaptation delineation.

The competence model forms the basis for the human capital factors. It was developed through empirical studies and quantifies specifics of enterprises analysed. Here a more generic approach is taken, which in turn is detailed through the consideration of role- and activity-based competencies. Human capital is thus defined as the sum of professional, social, personal and methodological competence. The peculiarity of these competences is dependent on the specific role occupied or on the activity itself, and in a wider sense, likewise on the strategic consideration of paradigms such as sustainable development.

The structural capital requires a distinct consideration of those capital factors that are activity-based (cooperation and knowledge transfer, product and process innovation), and the objectified factors (management instruments, explicit knowledge and corporate culture). While all factors are indeed structural factors of intangible resources, the implications on the activities of the model as condition transformation of objects such as “knowledge,” need to be observed and incorporated into the process model creation.

In relational capital, a new configuration considers relations on micro-, meso- and macro-level in order to integrate social aspects in a distinguished manner. At the micro level, the external relationships of the enterprise with individual actors are considered, while cooperation partners, supplier-, customer- and investor-relationships constitute the meso-level as individual “dyadic” relationships (Provan et al. 2007). Relationships to public bodies (legislative, funding) and society moreover are considered within the macro-level of relational capital. This allows for a focused definition of all relevant stakeholders and the enterprise’s relationships to those stakeholders.

At this point, an assessment of the cause-effect relationships can be implemented following a cross-factor impact assessment of all resource factors (Alwert et al. 2005). Identifying closed-loop interrelations is an attempt to address the system’s theoretical discussion of the introduction, where weakening or strengthening dependencies are identified and expressed in relation to a specific analysis object (Galeitzke et al. 2015).

The definition of resources (tangible and intangible) builds the basis for analysing the interrelations within the different resource categories and helps to identify fields of action for improving on the sustainability performance of their deployment. The following section introduces an approach for action planning and monitoring by using extended enterprise models.

3.5 Action Planning and Monitoring Through Allocation in Process Models

The most brilliant sustainability strategies can turn into disasters if they are not entirely or only insufficiently implemented. A key factor for a successful implementation of the sustainability strategy lies in the planning of operational actions and the availability of evaluations for monitoring and tracking qualitative and quantitative aspects. The measurement, control and communication of information on sustainability require the interaction between various actors, evaluation methods and operational data (Maas et al. 2016).

Figure 8 presents a framework concept for the description, analysis and monitoring of sustainability, specifically their interrelation with enterprise models.

Model-based framework the management of corporate sustainability performance

Applying this framework, one can ensure that a systematic embedding of the individual sustainability strategies, objectives, their monitoring and its implementation takes place in the planning phase.

The enterprise model characterises the core area of the framework presented. It represents an enterprise within all its aspects of strategic objectives, products, organisation, processes, tangible and intangible resources and their interrelation to each other. Once the variables that contribute to the characterisation of sustainability are modelled, a detailed action plan for the achievement of the strategic objectives is required. In order to coordinate this multi-dimensional sustainability system, mechanisms for prioritising them, clustering mechanisms for mapping them to the different dimensions of sustainability, as well as mechanisms for describing the relation aspects between them, are all necessary. To make best use of the scarce resources of an enterprise, an initial selection is necessary. To that end, a two-dimensional prioritisation-matrix can be used. The matrix differentiates between the dimensions “need for action (urgency)” and “feasibility”—each of them assuming the characteristic values low, medium and high. The matrix (Fig. 9) can help identify which measures are urgent and how easy or difficult they are to implement (Kohl et al. 2014).

Prioritisation-matrix (Orth et al. 2011)

It reveals the urgency level of the actions, along with their feasibility. The optimisation of the energy use might, for example, be highly urgent, but need not be easily feasible due to contractual ties. Furthermore, the enhancement of the material efficiency could be highly urgent, but not very feasible, due to the complex processes along the value chain that can only be altered with the application of enormous effort.

As soon as the prioritisation is complete, a suitable set of indicators has to be derived. Due to that fact, numerous methods, guidelines and norms have been developed (Kohl et al. 2013; Neugebauer et al. 2015; ISO 2013; VDI 2016), which offer evaluation mechanisms, and finally, indicators for expressing the degree of target achievement. A further consideration is then omitted at this point. Once the suitable indicators are aligned with the planned actions and thus with the strategic objectives, the monitoring via the usage of operational data has to be realised. Business intelligence and reporting tools that are only capable of visualising performance indicators are no longer sufficient for capturing the complex requirements of a comprehensive sustainability approach (Schneider and Meins 2012). Moreover, a solution for network sustainability management and its evaluation is required for balancing economic, ecological and social dimensions (Wilding et al. 2012). In the context of sustainable development, economic, environmental and social aspects have to be presented in a context-sensitive manner. To provide task or role-oriented information, the framework supports a so-called “view concept.” The views contain the relevant information for typical application and modelling purposes. They offer a focused cut without changing the models themselves. An evaluation component offers role-specific model evaluation views, summarizing relevant indicators and enterprise information in a central system, and allows their evaluation according to model elements.

The framework also allows a derivation of integrated reporting which complies with national and international standards. All elements described in the section above and integrated into the integrated model-based framework, are represented also in reporting guidelines for the communication of sustainability. The following section briefly introduces the major approaches.

3.6 Integrated Reporting

Companies are exposed to a growing number of required reports for internal as well as external reporting purposes (e.g. Intellectual-Capital-Statements, environmental reports, corporate social responsibility reports or sustainability reports). Given this situation of information overload, a comprehensive integration of various reports seems to be worthwhile. An integrated reporting format would not only reduce the internal preparation efforts, but also contribute to the standards, as for example formulated in the EU directive “Accounts Modernization Directive” on non-financial enterprise reporting (Clausen et al. 2006). While large enterprises communicate non-financial data and information to their stakeholders, small enterprises so far lack the means to report on their effort and achievements in implementing sustainable strategies. This section highlights our research contribution on integrated reporting.

In 2011, Eccles and Saltzman (2011) defined integrated reporting as “a single document that present and explain a company’s financial and nonfinancial—environmental, social, and governance (ESG)—performance.” This definition highlights the content and origin of integrated reports. In addition to traditional financial information, contents regarding the sustainability of the companyFootnote 1 are of note. Hence, in the following, the phenomena surrounding “sustainability reporting” will be discussed in detail before the connection to integrated reporting will then be drawn.

Sustainability reports document the environmental, social and economic engagements that enterprises are making in dealing with internal and external resources. They satisfy the increased need for information on the part of stakeholders. For sustainability reporting, criteria and an array of guidelines are already available. Worldwide attention has been paid to the Global Reporting Initiative (GRI). Since 2013, the meanwhile fourth version of the so-called “G4 Guidelines”—is available (Global Reporting Initiative 2013). Since the so-called “CSR directive” of the European Union was released, all reports published after the 6th of December 2016 have to be prepared “in accordance” with the G4-Guidelines (Guideline 2014/95/EU). When developing the guidelines, the GRI had several objectives in mind. One was to offer a bridge-builder for sustainability reporting on the path toward integrated reporting. The G4-Guidelines are therefore also applicable and implementable in integrated reporting (Soyka 2013).

The International Integrated Reporting Council (IIRC)—established in August 2010—consists of representatives from corporate, investment, accounting, securities, regulatory, academic and standard-setting sectors as well as from civil society (IIRC 2011). In September 2011, the IIRC released its first discussion paper, offering an initial proposal for the development of an “International Integrated Reporting Framework.” More than 200 responses were received from a wide range of stakeholder groups. The (IIRC 2012) published the results in 2012. The current IIRC proposal considers arguments for integrated reporting, and describes guiding principles and content while offering preliminary suggestions for the development of an international “integrated reporting framework” (IIRC 2013).

Central to Integrated Reporting is the organisation’s business model, i.e. “the process by which an organisation seeks to create and sustain value” in the short-, medium- and long-term perspective. This model is embedded into a system of inputs, business activities (the core of the business model) and outputs, as well as outcomes. In this context, value creation is not done by or within the organisation alone. It is influenced by external factors, e.g. the economic conditions and societal issues which represent risks and opportunities in the external environment. Furthermore, relationships to employees, partners, networks, suppliers and customers have an impact on the organisation’s value creation process. All organisations depend on different resources and relationships for their success. In that process, the IIRC framework uses the concept of “multiple capitals” for explaining how an organisation creates and sustains value. According to the framework, an integrated report should display an organisation’s stewardship not only with regards to financial capital, but also with other forms of “capital” (e.g. manufactured, human, intellectual, natural and social), along with their interdependencies.

According to the IIRC, integrated reporting explains linkages between an organisation’s strategy, governance and financial performance and the social, environmental and economic context within which it operates. Based on this, the IIRC formulates suggestions for integrated reporting—consisting of seven guiding principles and nine key content elements. The guiding principles underpin the preparation of an integrated report, based on the interconnected key content elements.

The Guiding Principles are: | The Content elements are: |

|---|---|

A. Strategic focus and future orientation B. Connectivity of information C. Stakeholder relationships D. Materiality E. Conciseness F. Reliability and completeness G. Consistency and comparability | A. Organisational overview and external environment B. Governance C. Business model D. Risks and opportunities E. Strategy and resource allocation F. Performance G. Outlook H. Basis of preparation and presentation I. General reporting guidance |

The approach of the IIRC gives comprehensive understanding of tangible and intangible resources and suggests interdependencies between corporate action and results. Since the IIRC approach aims for a harmonisation of reporting, a special focus is set on the enterprise’s external communication.

Originally, the approach was developed for large companies that are publicly traded. However, an approach for small- and medium-sized enterprises (SME) must be “downsized” or “downsizable” for the special purposes of SME (Bornemann et al. 2011). Because the IIRC approach principle is based on this, flexibility for an adaption is thus built-in.

In-line with the guiding principles and content of the IIRC, the authors have developed a reduced approach with a special focus on SME. This approach uses the five following principles and six content suggestions:

The Guiding Principles are: | The Content elements are: |

|---|---|

A. Materiality B. Integrity C. Connectivity D. Consistency and comparability E. Communicative quality | A. Organisational overview B. External environment C. Business model D. Risks and opportunities E. Performance G. Actions and Outlook |

To enhance the range in the distribution of the report, the approach also suggests using digital media. In addition, the formulated principles likewise profit from the use of digital media. When regarding, for instance, the consistency and comparability principle, the timelines of the KPIs prove to be much more doable in the digital approach than in the case of a classical print-version of a report.

4 Conclusion

The proposed integrated model-based framework for the management of corporate sustainability performance and the presented stepwise approach for implementing the discussed elements can be summarised as illustrated in Fig. 10. It can assist researchers as well as practitioners in gaining a clearer focus on the development and implementation of sustainability business models, sustainability strategies, performance management and reporting, regardless of whether transparency or decision support is taken as an a priori perspective. It also enables managers to improve their understanding of how the different management disciplines interact on sustainability topics and how to tackle increasing complexity in a context-sensitive and role-based concept.

Framework for management of corporate sustainability performance

Further steps in the area of sustainability performance management are nevertheless needed to extend the scope towards complete supply chains in order to manage, evaluate and control the performance of complex value-creation networks. Here, detailed concepts for an intuitive handling of data occurrence means that services for its selection, combination and aggregation, all have to be examined. In addition, several evaluation methods like the LCA already exist on the market, but connection mechanisms have to be developed to allow for reliable steering, controlling and monitoring. On top of the data-driven development needs, the knowledge transfer to the industrial community also has to be strengthened in order to improve and support the corporate sustainability orientation process as a whole.

Notes

- 1.

The terms “sustainability”, “environmental, social and governance” (ESG), “non-financial” or “corporate social responsibility” (CSR) reporting are frequently used interchangeably. They describe reports with different degrees of focus on environmental, social or corporate governance issues (Ioannou and Serafeim 2011).

References

Alwert, Kay, Peter Heisig, and Kai Mertins. 2005. Wissensbilanzen — Intellektuelles Kapital erfolgreich nutzen und entwickeln. Berlin: Springer.

Ansoff, H.I. 1965. Corporate strategy: An analytic approach to business policy for growth and expansion. New York: McGraw-Hill.

ARE, and DEZA. 2004. Nachhaltige Entwicklung in der Schweiz: Methodische Grundlagen. http://www.are.admin.ch/themen/nachhaltig/00260/index.html?lang=de. Accessed 20 June 2016.

Bansal, Pratima, and Kendall Roth. 2000. Why companies go green: a model of ecological responsiveness. Academy of Management Journal 43(4): 717–736. doi:10.2307/1556363.

Baumgartner, Rupert J., and Daniela Ebner. 2010. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustainable Development 18(2): 76–89. doi:10.1002/sd.447.

Bergmann, Lars. 2010. Nachhaltigkeit in Ganzheitlichen Produktionssystemen. Schriftenreihe des Instituts für Werkzeugmaschinen und Fertigungstechnik der TU Braunschweig. Essen: Vulkan-Verl. Techn. Univ., Diss.—Braunschweig, 2009.

Bocken, N.M.P., S.W. Short, P. Rana, and S. Evans. 2014. A literature and practice review to develop sustainable business model archetypes. Journal of Cleaner Production 65: 42–56. doi:10.1016/j.jclepro.2013.11.039.

Bornemann, Manfred, Kay Alwert, and Ronald Orth. 2011. Comments on the discussion paper Towards Integrated Reporting—Communicating Value in the 21st Century.

Chandler, Alfred D. 1962. Strategy and structure: Chapters in the history of the industrial enterprise. Cambridge: MIT Press.

Clausen, Jens. 2011. Mit Innovationen auf den Weg zur Nachhaltigkeit. http://www.globalcompact.de/sites/default/files/jahr/publikation/1a_clausen_jens_-_mit_innovationen_zur_nachhaltigkeit_-_borderstep_institut.pdf. Accessed 21 June 2016.

Clausen, Jens, Thomas Loew, and Walter Kahlenborn. 2006. Lagebericht zur Lageberichterstattung. http://www.umweltbundesamt.de/sites/default/files/medien/publikation/long/3236.pdf. Accessed 20 June 2016.

Clausewitz, Carl v. 1935. Vom Kriege. Leipzig: Quelle & Meyer.

Dyckhoff, Harald, and Rainer Souren. 2008. Nachhaltige Unternehmensführung: Grundzüge industriellen Umweltmanagements; mit 13 Tabellen. Berlin: Springer.

Dyllick, Thomas, and Kai Hockerts. 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11(2): 130–141. doi:10.1002/bse.323.

Eccles, Robert G., and Daniela Saltzman. 2011. Achieving sustainability through integrated reporting. Stanford Social Innovation Review (Summer 59).

Engert, Sabrina, Romana Rauter, and Rupert J. Baumgartner. 2016. Exploring the integration of corporate sustainability into strategic management: A literature review. Journal of Cleaner Production 112: 2833–2850. doi:10.1016/j.jclepro.2015.08.031.

Enquete-Kommission. 1998. Innovationen zur Nachhaltigkeit.

Epstein, Marc J., and Adriana R. Buhovac. 2014. Making sustainability work: Best practices in managing and measuring corporate social, environmental, and economic impacts. San Francisco: Berrett-Koehler Publishers.

Figge, Frank, Tobias Hahn, Stefan Schaltegger, and Marcus Wagner. 2002. The sustainability balanced scorecard—linking sustainability management to business strategy. Business Strategy and the Environment 11(5): 269–284. doi:10.1002/bse.339.

FORA. 2010. Green business models in the Nordic Region: A key to promote sustainable growth. http://www.danishwaterforum.dk/activities/Water_and_green_growth/greenpaper_fora_211010_green_business%20models.pdf. Accessed 20 June 2016.

Galeitzke, Mila, Nicole Oertwig, Ronald Orth, and Holger Kohl. 2016. Process-oriented design methodology for the (inter-) organizational intellectual capital management. Procedia CIRP 40: 674–679. doi:10.1016/j.procir.2016.01.153.

Galeitzke, Mila, Erik Steinhöfel, Ronald Orth, and Holger Kohl. 2015. Strategic intellectual capital management as a driver of organisational innovation. International Journal of Knowledge and Learning 10(2): 164–181. doi:10.1504/IJKL.2015.071622.

Giles, Lionel. 1910. Sun Tzu on the art of war: The oldest military treatise in the world. London: Luzac & Co.

Gleich, Arnim v., and Stefan Gößling-Reisemann. 2008. Industrial Ecology: Erfolgreiche Wege zu nachhaltigen industriellen Systemen. Wiesbaden: Vieweg + Teubner Verlag.

Global Reporting Initiative. 2013. Sustainability Reporting Guidelines: Version 4.0. https://www.globalreporting.org/standards/g4/Pages/default.aspx. Accessed 20 June 2016.

Grant, Robert M. 2005. Contemporary strategy analysis, 5th ed. Malden, Mass. [u.a.]: Blackwell.

Harris, Jonathan M., and Brian Roach. 2013. Environmental and natural resource economics: A contemporary approach, 3rd ed. Armonk: M.E. Sharpe.

Henderson, Bruce C. 1973. The Experience curve-reviewed (Part IV): the growth share martrix of the product Portfolio. Boston: Boston Consulting Group.

Huber, Joseph. 2000. Industrielle Ökologie. Konsistenz, Effizienz und Suffizienz in zyklusanalytischer Betrachtung. In Global change - globaler Wandel: Ursachenkomplexe und Lösungsansätze; causal structures and indicative solutions, ed. Rolf Kreibich and Udo E. Simonis. Wissenschaft in der Verantwortung. Berlin: Arno Spitz.

Huber, Joseph. 2011. Allgemeine Umweltsoziologie. 2., vollst. überarb. Aufl. Wiesbaden: VS Verlag für Sozialwissenschaften.

IIRC. 2011. Towards Integrated Reporting: Communicating Value in the 21st Century. http://integratedreporting.org/wp-content/uploads/2011/09/IR-Discussion-Paper-2011_spreads.pdf. Accessed 20 June 2016.

IIRC. 2012. Towards Integrated Reporting—Communicating Value in the 21st Century: Summary of Responses to the Summar of Responses to the September 2011 Discussion Paper and Next Steps. http://integratedreporting.org/wp-content/uploads/2012/06/Discussion-Paper-Summary1.pdf. Accessed 20 June 2016.

IIRC. 2013. The International <IR> Framework. http://integratedreporting.org/wp-content/uploads/2015/03/13-12-08-THE-INTERNATIONAL-IR-FRAMEWORK-2-1.pdf. Accessed 20 June 2016.

Ioannou, Ioannis, and George Serafeim. 2011. The consequences of the consequences of mandatory corporate sustainability reporting. Harvard Business School Working Paper 11–100.

ISO. 2009. Leiten und Lenken für den nachhaltigen Erfolg einer Organisation - Ein Qualitätsmanagementansatz, no. ISO 9004:2009. Berlin: Beuth.

ISO. 2013. Environmental management—environmental performance evaluation - Guidelines, no. DIN EN ISO 14031. Berlin: Beuth.

Jochem, Roland, and Silke Balzert (eds.). 2010. Prozessmanagement: Strategien, Methoden, Umsetzung, 1st ed. Düsseldorf: Symposion Publishing.

Johnson, Mark W., Clayton M. Christensen, and Henning Kagermann. 2008. Reinventing your business model. Harvard Business Review 86(12): 50–59. doi:10.1225/R0812C.

Knight, Dave. 2006. The SIGMA management model. In Management models for corporate social responsibility, ed. Jan Jonker, and Marco de Witte, 11–18. Berlin: Springer.

Kohl, Holger, Ronald Orth, and Oliver Riebartsch. 2013. Sustainability analysis for indicator-based benchmarking solutions. In 11th Global Conference on Sustainable Manufacturing, GCSM 2013// Innovative solutions: Abstracts, ed. Günther Seliger, 567–573. Berlin: Universitätsverlag der TU Berlin.

Kohl, Holger, Ronald Orth, and Erik Steinhöfel. 2014. Process‐oriented knowledge management in SMEs. In Proceedings of the 15th European Conference on Knowledge Management (ECKM), ed. C. Vivas and P. Sequeira, 563–570. Academic Conferences and Publishing International Limited.

Lozano, Rodrigo. 2015. A holistic perspective on corporate sustainability drivers. Corporate Social Responsibility and Environmental Management 22(1): 32–44. doi:10.1002/csr.1325.

Lüdeke-Freund, Florian. 2010. Towards a conceptual framework of ‘business models for sustainability’. In ERSCP-EMSU Conference, 2010, in Delft.

Maas, Karen, Stefan Schaltegger, and Nathalie Crutzen. 2016. Integrating corporate sustainability assessment, management accounting, control, and reporting. Journal of Cleaner Production. doi:10.1016/j.jclepro.2016.05.008.

Mertins, Kai, and Markus Will. 2008. Strategic relevance of intellectual capital in European SMEs and sectoral differences. InCaS: Intellectual Capital Statement—Made in Europe. In Proceedings of the 8th European Conference on Knowledge Management, Barcelona.

Mitchell, Donald, and Carol Coles. 2003. The ultimate competitive advantage: Secrets of continually developing a more profitable business model, 1st ed. San Francisco: Berrett-Koehler.

Neugebauer, Sabrina, Julia Martinez-Blanco, René Scheumann, and Matthias Finkbeiner. 2015. Enhancing the practical implementation of life cycle sustainability assessment—proposal of a Tiered approach. Journal of Cleaner Production 102: 165–176. doi:10.1016/j.jclepro.2015.04.053.

OECD. 2010. Eco-innovation in industry: Enabling green growth, 1st ed. Paris: OECD.

Orth, Ronald, Stefan Voigt, and Ina Kohl. 2011. Praxisleitfaden Wissensmanagement: Prozessorientiertes Wissensmanagement nach dem ProWis-Ansatz einführen. Stuttgart: Fraunhofer.

Osterwalder, Alexander, and Yves Pigneur. 2011. Business model generation: Ein Handbuch für Visionäre, Spielveränderer und Herausforderer. Frankfurt am Main: Campus.

Porter, M.E. 1985. Competitive advantage: Creating and sustaining superior performance. New York: Free Press.

Porter, Michael E. 1980. Competitive strategy: Techniques for analyzing industries and competitors. New York: Free Press.

Prahalad, Coimbatore K., and G. Hamel. 1990. The core competence of corporation. Harvard Business Review 69(4): 81–92.

Provan, Keith G., Amy Fish, and Joerg Sydow. 2007. Interorganizational networks at the network level: A review of the empirical literature on whole networks. Journal of Management 33(3): 479–516. doi:10.1177/0149206307302554.

Rüegg-Stürm, Johannes. 2005. Das neue St. Galler Management-Modell: Grundkategorien einer integrierten Managementlehre; der HSG-Ansatz. 2., durchges. Aufl., [Nachdruck]. Bern: Haupt.

Sandkuhl, Kurt, Matthias Wißotzki, and Janis Stirna. 2013. Unternehmensmodellierung: Grundlagen, Methode und Praktiken. Berlin: Springer.

Schallmo, Daniel. 2013. Geschäftsmodell-Innovation: Grundlagen, bestehende Ansätze, methodisches Vorgehen und B2B-Geschäftsmodelle. Wiesbaden: Springer Fachmedien.

Schaltegger, Stefan (ed.). 2000a. Wirtschaftswissenschaften. Studium der Umweltwissenschaften. Berlin: Springer.

Schaltegger, Stefan, ed. 2000. 2007. Nachhaltigkeitsmanagement in Unternehmen: Von der Idee zur Praxis: Managementansätze zur Umsetzung von Corporate Social Responsibility und Corporate Sustainability. Berlin: Bundesministerium für Umwelt Naturschutz und Reaktorsicherheit (BMU) Referat Öffentlichkeitsarbeit.

Schaltegger, Stefan, and Roger Burritt. 2005. Corporate sustainability. In The international yearbook of environmental and resource economics 2005/2006: A survey of current issues, ed. Thomas H. Tietenberg and Henk Folmer, 185-. New horizons in environmental economics series. Cheltenham: Edward Elgar.

Schendel, Dan, and Charles W. Hofer. 1979. Strategic management: A new view of business policy and planning. Boston: Little, Brown.

Schneider, Anselm, and Erika Meins. 2012. Two dimensions of corporate sustainability assessment: Towards a comprehensive framework. Business Strategy and the Environment 21(4): 211–222. doi:10.1002/bse.726.

Soyka, Peter A. 2013. The International Integrated Reporting Council (IIRC) integrated reporting framework: Toward better sustainability reporting and (Way) beyond. Environmental Quality Management 23(2): 1–14. doi:10.1002/tqem.21357.

Staehle, Wolfgang H., and Peter Conrad. 1994. Management: Eine verhaltenswissenschaftliche Perspektive. 7. Aufl./ überarb. von Peter Conrad. Vahlens Handbücher der Wirtschafts- und Sozialwissenschaften. München: Vahlen.

Stern, Thomas, and Helmut Jaberg. 2010. Erfolgreiches Innovationsmanagement: Erfolgsfaktoren - Grundmuster - Fallbeispiele. 4, überarbeitete ed. Wiesbaden: Gabler Verlag/GWV Fachverlage GmbH.

Taylor, Frederick W. 1911. The principles of scientific management. New York: Harper & Brothers.

Tukker, Arnold. 2004. Eight types of product–service system: Eight ways to sustainability? Experiences from SusProNet. Business Strategy and the Environment 13(4): 246–260. doi:10.1002/bse.414.

van Marrewijk, Marcel. 2003. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. Journal of Business Ethics 44(2–3): 95–105. doi:10.1023/A:1023331212247.

van Marrewijk, Marcel, and M. Werre. 2003. Multiple levels of corporate sustainability. Journal of Business Ethics 44(2): 107–119. doi:10.1023/A:1023383229086.

VDI. 2016. VDI-Richtlinie: VDI 4070 Blatt 1 Nachhaltiges Wirtschaften in kleinen und mittelständischen Unternehmen - Anleitung zum nachhaltigen Wirtschaften, no. VDI 4070. Berlin: Beuth.

Vernadat, François B. 1996. Enterprise modeling and integration: Principles and applications, 1. ed. London u.a. Chapman & Hall.

Welge, Martin K. 2001. Strategisches Management: Grundlagen - Prozess - Implementierung, 3rd ed. Wiesbaden: Gabler.

Westkämper, Engelbert, and Markus Decker. 2006. Einführung in die Organisation der Produktion. Berlin, Heidelberg: Springer.

Wilding, Richard, Joe Miemczyk, Thomas E. Johnsen, and Monica Macquet. 2012. Sustainable purchasing and supply management: A structured literature review of definitions and measures at the dyad, chain and network levels. Supply Chain Management: An International Journal 17(5): 478–496. doi:10.1108/13598541211258564.

Will, Markus. 2012. Strategische Unternehmensentwicklung auf Basis immaterieller Werte in KMU: Eine Methode zur Integration der ressourcen- und marktbasierten Perspektive im Strategieprozess. ed. Kai Mertins. Berichte aus dem Produktionstechnischen Zentrum Berlin. Stuttgart: Fraunhofer.

Windolph, Sarah E., Dorli Harms, and Stefan Schaltegger. 2014. Motivations for corporate sustainability management: Contrasting survey results and implementation. Corporate Social Responsibility and Environmental Management 21(5): 272–285. doi:10.1002/csr.1337.

Wirtz, Bernd W. 2010. Business model management: Design—Instrumente - Erfolgsfaktoren von Geschäftsmodellen, 1st ed. Wiesbaden: Gabler.

Yunus, Muhammad, Bertrand Moingeon, and Laurence Lehmann-Ortega. 2010. Building social business models: Lessons from the Grameen experience. Long Range Planning 43(2–3): 308–325. doi:10.1016/j.lrp.2009.12.005.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the book’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the book’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2017 The Author(s)

About this chapter

Cite this chapter

Oertwig, N. et al. (2017). Integration of Sustainability into the Corporate Strategy. In: Stark, R., Seliger, G., Bonvoisin, J. (eds) Sustainable Manufacturing. Sustainable Production, Life Cycle Engineering and Management. Springer, Cham. https://doi.org/10.1007/978-3-319-48514-0_12

Download citation

DOI: https://doi.org/10.1007/978-3-319-48514-0_12

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-48513-3

Online ISBN: 978-3-319-48514-0

eBook Packages: EngineeringEngineering (R0)