Abstract

The purpose of the article is to determine the place and role of budgeting in the system of methods of managerial accounting of contractual relationship of cluster. The research was conducted within the concept of institutional economy, concept of enterprise management, concept of financial management, and concept of clustering of economy. This determined the choice and use of the methodology of the research, based on the method of institutional, financial, problem, systemic, and structural & functional analysis, synthesis, induction, deduction, formalization, and modeling of economic systems. The authors determined the specifics of management of contractual relationship of cluster, analyzed the system of methods of managerial accounting of contractual relationship of cluster, and determined problems and perspectives and developed recommendations for development of budgeting as a ley method of managerial accounting of contractual relationship of cluster. As a result, the authors came to the conclusion that budgeting occupies the central place and performs the key role in the system of methods of managerial accounting of contractual relationship of cluster.

1 Introduction

At present, under the influence of the processes of globalization of the world economy, transnationalism of entrepreneurial activities, and post-industrialization of socio-economic systems, the number and frequency of economic operations grow quickly. The strategy of achievement of the “scale effect” and maximization of sales volumes becomes more popular in the global markets. All of this leads to formation of transaction economy.

Transaction economy is an economic system in which economic deal or transaction occupies a central place in the system of economic relations. Under these conditions, importance and actuality of minimization of transaction costs and management of transaction or contractual relationship of entrepreneurial structures grow.

In addition to that, many modern socio-economic systems develop by the cluster type. This supposes formation of sectorial economic clusters in various spheres of national economy. Cluster features more complex transaction relationships than between separate enterprises as the structure of cluster is complex and many-sided.

Taking into account that the main idea of creation of economic cluster consists in maximization of effectiveness of economic activities of its members, development of methodology for optimization of its contractual relationship is a perspective direction for scientific research.

This work offers a hypothesis that budgeting occupies a central place and plays a key role in the system of methods of managerial accounting of contractual relationship of cluster. The purpose of the article is determination of the place and role of budgeting in the system of methods of managerial accounting of contractual relationship of cluster.

2 Literature Overview

Managerial accounting is the process of collection and analysis of information and making managerial decisions regarding various aspects of activities of enterprises (Jacková 2016). Managerial accounting is the basis of modern business (Otley 2016), as it provides planned and systemic nature of its development (Libby et al. 2015) and is a guarantee of effective management (Chenhall and Moers 2015).

Contractual relationship of enterprises appear as a result of conclusion of business deals (Johnson and Sohi 2016). They are registered officially and are performed on the basis of contract and current legislation (Subramanian et al. 2016). Contractual relationships are necessary for stable functioning of enterprises in market (Vasconcelos 2014), as they provide predictability of its relations with business partners (Ding et al. 2013).

Budgeting is the process of collection and processing of information for compilation of budget and management of enterprises’ finances (Schlegel et al. 2016). Foundations of budgeting, as a method of managerial accounting, are set in works of such modern authors as Popesko and Šocová (2015), Ji and Lejeune (2015), Dudin et al. (2015), etc.

Economic cluster is an economic system consisting of many enterprises united on the basis of a certain attribute (Popkova et al. 2013a). The sense and specifics of functioning and development of cluster are viewed in the works by Popkova et al. (2013b, 2015a, b), etc.

Literature review on the topic of the research showed that despite the high level of elaboration of its particular aspects, the problem of determination of the place and role of budgeting in the system of methods of managerial accounting of contractual relationship of cluster remains unsolved in contemporary science, which causes necessity for conduct of further research.

3 Research Methods

The research is performed within the concept of institutional economics, concept of management of enterprise, concept of financial management, and concept of clustering of economy. This pre-determined choice and use of the methodology of the research, which is based on the method of institutional, financial, problem, systemic, and structural & functional analysis, synthesis, induction, deduction, formalization, and modeling of economic systems.

In order to substantiate the necessity for managerial accounting of contractual relationship of cluster, the authors of this work use the concept of transaction economy, within which they determine the role of contract as a reflection of transaction in modern economic system and analyze the process of formalization and institutionalization of contractual relationship of cluster.

Due to conduct of institutional analysis, this work analyzes the sense of cluster as an economic institute and determines foundations of its contractual relationship. Based on the concept of management of enterprise, the work studies the methods of managerial accounting which accessible for cluster. With the help of conceptual provisions of financial management, the articles views budgeting as a financial tool in the system of methods of managerial accounting of cluster contractual relationship.

Within the concept of clustering of economy, the authors of this paper founds the sense of cluster as an economic category, determine specifics of its contractual relationship as a unique structural phenomenon, and view the system of internal relations in enterprises within cluster and the system of interrelations between cluster and environment. Also, the authors use the foundations of synergetic approach during study of cluster and methods of managerial accounting of its contractual relationship as an economic system.

4 Results

4.1 Specifics of Management of Cluster Contractual Relationship

Peculiarities of the structure of cluster, as a socio-economic system, determine specifics of its contractual relationships which are formed within two levels: internal and external. Internal level includes conclusion of contracts and transactions between cluster members.

A typical example of such contractual relationship is transactions between R&D institutes and industrial enterprise regarding buy and sell of new technologies. As a rule, it is relationship contracts which are built on the basis of not only formal mechanisms but on the basis of the system of informal relations and insider’s information of cluster members; they may even have an implicit form.

The external level includes contractual relationship between cluster and its contractors. For example, it could be relationship between industrial enterprises of cluster and their suppliers. Such contracts are usually neo-classical, they are more formalized, and are concluded in explicit form.

A common feature of intra-cluster and contractual relationship in the internal level and cluster relationship in the external cluster is the fact that they are built on the basis of the principle of economic effectiveness. According to this principle, the contract parties conclude it for the purpose of receipt of own profit and maximization of advantages from cooperation. This principle is also coordinated with the market’s mechanism which works inside the cluster and outside it.

4.2 The System of Methods of Managerial Accounting of Cluster Contractual Relationship

This work distinguished the following components in the system of methods of managerial accounting of cluster contractual relationship:

-

planning and selection—the process of setting the tasks of initiating contractual relationship, consideration of possible variants of contracts conclusion and potential business partners of cluster, and determination of criteria of their comparison and selection of the most optimal ones;

-

grouping and systematization—the process of structuring of potential business partners of cluster, determination of their common and different attributes, and formation of comprehensive idea on the situation in the market, where the contract is to be concluded;

-

cost estimation and calculation—the process of analysis of transaction costs related to conclusion of the planned contract with different potential business partners;

-

analysis and evaluation—the process of determination of potential profits from conclusion of various contracts with various potential business partners;

-

rating and establishing limits—the process of determination of maximum allowable level of transaction costs for cluster and minimum profit necessary for acknowledging the contract to be expedient;

-

budgeting—the process of determination of expediency of conclusion of the contract with this business partner through comparison of costs and profits and development of control variables for further evaluation of its effectiveness;

-

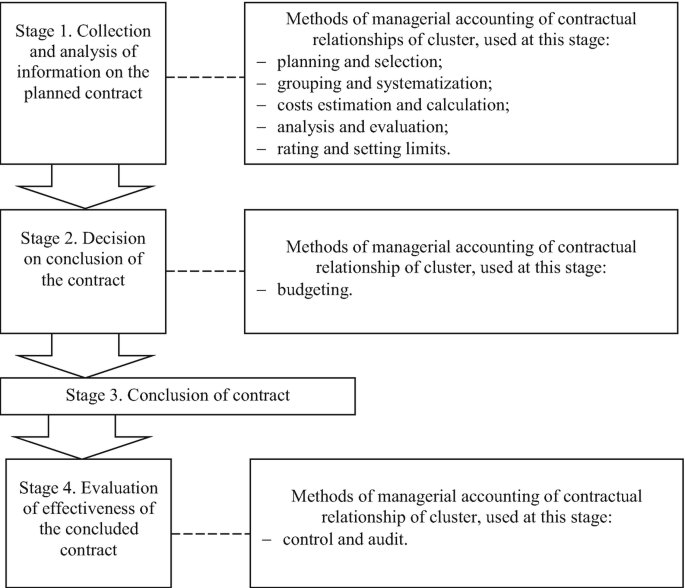

control and audit—the process of monitoring of results of conclusion of contract, the process of its performance, and evaluation of its effectiveness with the system of previously developed criteria (Fig. 1).

Fig. 1

Process and system of methods of managerial accounting of cluster contractual relationship

As is seen from Fig. 1, the process of managerial accounting of contractual relationship of cluster goes through four main stages. The first stage includes collection and analysis of information on the planned contract. Most of methods of managerial accounting of contractual relationship of cluster are used here: planning and selection, grouping and systematization, cost estimates and calculation, analysis and evaluation, and rating and setting limits.

The second stage includes making decision on conclusion of a contract with the help of the budgeting method. The third stage includes conclusion of a contract between cluster and its business partner. The fourth stage includes evaluation of effectiveness of the concluded contract with the help of methods of managerial accounting of contractual relationship of cluster as control and audit.

According to the authors of this article, the most important, complex, and responsible stage is making a decision on conclusion of contract. As this stage supposes the use of only the budgeting method, it occupies the central position and plays a key role in the system of methods of managerial accounting of contractual relationship of cluster.

4.3 Perspectives and Recommendations for Development of Budgeting as a Key Method of Managerial Accounting of Contractual Relationship of Cluster

The most popular problems of the use of the method of budgeting in the process of managerial accounting in contractual relationship of cluster are the following. Firstly, large complexity of budgeting. The process of budgeting supposes processing of large volume of information, which requires a lot of time and efforts, as a slightest mistake can distort the final result.

Secondly, lack of data for compilation of precise calculations and forecasts. It is very difficult to study the full situation in the market and develop a comprehensive idea of all possible variants of cluster contractual relationship cluster. Incompleteness or distortion of initial information leads to strengthening of approach and reduction of probability of the compiled forecasts, which may be a reason for making wrong managerial decisions.

Thirdly, a large number of cluster members, the interests of which should be taken into account and regulated. Most of interested parties seek various goals and interests, which significantly complicates the process of management of cluster contractual relationship, as compared to particular enterprise. Consideration of interest of some members of cluster and ignoring the others may lead to its destruction.

Perspectives of solving these issues are related to perfection of the process of budgeting and the use of systemic approach to conduct of managerial accounting of cluster contractual relationship. For development of budgeting, as a key method of managerial accounting of cluster contractual relationship, this work offers the following recommendations:

-

automatization of the process of budgeting—using the newest software will allow simplifying and accelerating the process of budgeting and reducing the role of subjective components in the process of performance of calculations and decision making;

-

creation and development of informational system for budgeting—availability of renewed data base on possible variants of development of cluster contractual relationship will allow simplifying the process of decision making;

-

optimization of cluster contractual relationship—for regulation of interests of various members of cluster, it is necessary to find their balance. If it’s impossible to conclude a contract that fully corresponds to interests of all members of the cluster and that satisfies only some of them, it is expedient to conclude the next contract that corresponds to the interests of other members, in order to preserve the cluster.

5 Conclusions

Thus, as a result of the research, the offered hypothesis was proved and it was confirmed that budgeting occupies a central place and plays a key role in the system of methods of managerial accounting of cluster contractual relationship, as it is used within the most responsible stage of this process and cannot be substituted.

It should be concluded that peculiarities of functioning of economic cluster cause conclusion of contractual relationship at the internal level. For that, it is expedient to unite into a cluster horizontally and vertically integrated enterprises.

Contractual relationship at the internal level are characterized by lower level of uncertainty and risk. Transaction costs for their conclusion are lower than at external level, due to absence of necessity for their full formalization and detalization and the possibility for performance of these relationships based on mutual trust.

Reduction to the minimum of the share of contractual relationship at the external level of cluster will allow increasing effectiveness of budgeting and managerial accounting on the whole. It is also expedient to use the developed recommendations for development of budgeting as a key method of managerial accounting of contractual relationship of cluster.

Generalized character of the model of contractual relationship of cluster and their managerial accounting, as well as developed recommendations causes certain limitation of results of the performed research. That’s why empirical analysis of the system and methodology of managerial accounting of cluster contractual relationship and of effectiveness of the offered recommendations constitutes the basis for further research in this sphere.

References

Chenhall RH, Moers F (2015) The role of innovation in the evolution of management accounting and its integration into management control. Acc Organ Soc 47:1–13

Ding R, Dekker HC, Groot T (2013) Risk, partner selection and contractual control in interfirm relationships. Manag Acc Res 24(2):140–155

Dudin MN, Kutsuri GN, Fedorova IJ, Dzusova SS, Namitulina AZ (2015) The innovative business model canvas in the system of effective budgeting. Asian Soc Sci 11(7):290–296

Jacková A (2016) Use of management accounting in business management. In: Production management and engineering sciences—scientific publication of the international conference on engineering science and production management, ESPM 2015, pp 113–118

Ji R, Lejeune MA (2015) Risk-budgeting multi-portfolio optimization with portfolio and marginal risk constraints. Ann Oper Res 2(1):154–159

Johnson JS, Sohi RS (2016) Understanding and resolving major contractual breaches in buyer–seller relationships: a grounded theory approach. J Acad Mark Sci 44(2):185–205

Libby R, Rennekamp KM, Seybert N (2015) Regulation and the interdependent roles of managers, auditors, and directors in earnings management and accounting choice. Acc Organ Soc 47:25–42

Otley D (2016) The contingency theory of management accounting and control: 1980-2014. Manag Acc Res 3(1):234–238

Popesko B, Šocová V (2015) Current trends in budgeting and planning: Czech survey initial results. International Advances in Economic Research, pp 1–2

Popkova EG, Morkovina SS, Patsyuk EV, Panyavina EA, Popov EV (2013a) Marketing strategy of overcoming of lag in development of economic systems. World Appl Sci J 26(5):591–595

Popkova EG, Sharkova AV, Merzlova MP, Yakovleva EA, Nebesnaya AY (2013b) Unsustainable models of regional clustering. World Appl Sci J 25(8):1174–1180

Popkova EG, Chechina OS, Abramov SA (2015a) Problem of the human capital quality reducing in conditions of educational unification. Mediterr J Soc Sci 6(36):95–100

Popkova EG, Kuzlaeva IM, Bezrukova TL (2015b) Clustering of internet companies as a new course of development of Russia in modern conditions. Mediterr J Soc Sci 6(4):210–218

Schlegel D, Frank F, Britzelmaier B (2016) Investment decisions and capital budgeting practices in German manufacturing companies. Int J Bus Glob 16(1):66–78

Subramanian N, Rahman S, Abdulrahman MD (2016) Sourcing complexity in the Chinese manufacturing sector: an assessment of intangible factors and contractual relationship strategies. Int J Prod Econ 166:269–284

Vasconcelos L (2014) Contractual signaling, relationship-specific investment and exclusive agreements. Games Econ Behav 87:19–33

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer International Publishing AG

About this chapter

Cite this chapter

Duysenbieva, G.M., Yusufov, N.A., Radzhabov, R.A., Umalatov, K.A. (2017). Place and Role of Budgeting in the System of Methods of Managerial Accounting of Cluster Contractual Relationship. In: Popkova, E.G., Sukhova, V.E., Rogachev, A.F., Tyurina, Y.G., Boris, O.A., Parakhina, V.N. (eds) Integration and Clustering for Sustainable Economic Growth. Contributions to Economics. Springer, Cham. https://doi.org/10.1007/978-3-319-45462-7_5

Download citation

DOI: https://doi.org/10.1007/978-3-319-45462-7_5

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-45461-0

Online ISBN: 978-3-319-45462-7

eBook Packages: Economics and FinanceEconomics and Finance (R0)