Abstract

In the first part of this chapter, we introduce the reader to the concept of corporate social responsibility. We outline different underlying motivations of CSR for a firm. Furthermore, we elaborate on different channels through which CSR is linked to the maximization of firm value. Specifically, we examine the impact of CSR on firm valuation through future cash flows and the required expected rates of returns. In the second part, we introduce the EU taxonomy as a possible solution towards the problem of evaluating firms’ CSR performance. The EU taxonomy is aimed to channel investments towards sustainable opportunities by ensuring transparency about firms’ environmental performance. We also explain its practical relevance, limitations, and future developments. Overall, we emphasize the role of unified efforts in green transformation.

You have full access to this open access chapter, Download chapter PDF

Keywords

1 Introduction

The term “shareholder value maximization” became prominent in the 1980s (Rappaport 1986). The paradigm that all firm activities should be focused on generating value for the firm’s investors—in other words increase firm value—has however been dominant in businesses and financial markets much longer. It can be traced back to the capitalist motive of capital accumulation (Marques 2020). Over the last decades, many have made out the capitalist motive of firm wealth maximization as the gravedigger of the natural environment and thus the basis of our wealth and life on earth. In the popular discourse, capitalism is widely blamed as the root cause for natural destruction (The Guardian n.d.; Forbes n.d.; Global Social Challenges n.d.). Especially young people blame capitalism for climate change. A poll among Britons aged 16 to 34 finds that 75 percent agree with the statement that “Climate change is caused by big corporations that pollute the atmosphere […]. Therefore, capitalism is the problem not the solution.” (Institute of Economic Affairs n.d.). Sociologists have coined the term “treadmill of production” to describe how the capitalist desire for growth and capital accumulation destroys the natural environment without succeeding in improving individuals’ well-being (Schnaiberg 1984; Schnaiberg and Gould 1994). Overall, there is an overwhelmingly negative sentiment that the capitalist motive of firm value wealth maximization is to blame for environmental destruction.

This gradually declining opinion towards firms has led to the evolvement of “corporate social responsibility” (CSR), which can be described as the practice of introducing environmental and social factors to corporate decision making. The development of this concept thus was not proactive, but a reaction towards society questioning the legitimacy of large corporations (Brown 2008; Lee and Carroll 2011). Over the last decades, CSR has made its way to the top of research agendas and is widely considered an absolute necessity of doing business by many practitioners (Lindgreen et al. 2009). This trend has led to a seeming erosion of the paradigm of firm value maximization. Section 2 of this chapter takes a closer look at common definitions of CSR.

Much hope for a successful transformation towards a sustainable economy rests on firms acknowledging this concept. One example of societies counting on such engagement by firms is given by the transformation towards a sustainable energy production. Based on the EU Member State National Energy and Climate Plans (NECPs), the EU Commission estimates that achieving the current EU 2030 climate and energy goals alone requires annual investments in energy production and consumption to increase by a total of €350 billion during the current decade. This effort also requires large amounts of investments by firms. Moreover, climate change is not the only environmental sustainability issue where firms’ commitment is required. Water pollution, biodiversity loss, and plastic pollution are only few of the other issues which require action at substantial cost.

This raises the question as to which forces could induce firms and their managers as the main decision-makers in day-to-day business to spend the enormous amounts required or, more generally, consider environmental and social sustainability in their decision making. A first solution would be simply by establishing legal rules to which firms and their managers have to obey. However, there are limits for fulfilling goals by simple force, as decision-makers may try to evade legal requirements. A second possibility is that firm managers’ preferences inherently drive them to achieve sustainable goals. Though this might be the case, there may also be managers that are mainly interested in personal (positive) monetary consequences. One way for managers to increase personal welfare may be to raise firm value, which often serves as the basis for managerial compensation. We thus detail how CSR relates to firm value by impacting its two determinants: (expected) firm cash flows and the minimum expected average rate of return which investors require to provide funds to the firm. In such a situation where CSR also implies higher firm value, there would be no real conflict of interest between sustainability goals and firm value maximization apparently easing the way to a green transformation of the economy. Section 3.1 points out negative consequences of CSR on firm value, which are due to managers selfishly spending firm resources, and Sect. 3.2 explains the positive effects of CSR, which are a consequence of stakeholders behaving more favorably towards the firm.

One especially relevant stakeholder group in this context are investors. Non-monetary gratifications also affect how investors value financial assets and thus firms. It has long been observed that firms are valued at a lower price if their business model contradicts social norms. The increased emphasis on sustainability among investors consequently leads to sustainability being a determinant of financial instruments’ prices. Section 4 details the channels behind investor preferences for social and environmental engagement demanding lower returns from firms, i.e., firms having a lower cost of capital. These rely on so-called CSR-conscious investors, i.e., investors forfeiting profits in exchange for the so-called moral dividend sustainable firms provide, polluting firms being avoided by this investor type, and lower riskiness of sustainable firms due to, for example, a reduced threat of lawsuits or consumer boycotts.

Even though all of these channels discussed in Sect. 4 provide convincing incentives for managers to engage in CSR, an issue that has yet not been addressed is that of whether these incentives bring anything new to the table. Given that CSR already affects firm value due to its impact on cash flows, which is a result of other stakeholders’, e.g., customers’, reactions, we address the question of the added benefit of investors considering CSR in Sect. 5. We explain that, firstly, firms can alter their business model to focus on, e.g., non-CSR-conscious customers and thus largely avoid the consequences of consumer boycotts by CSR-conscious customers. Due to diversification consideration, firms cannot focus on only a minor group of investors without cost. Secondly, stock market investors are typically better informed about the operations of the firm than other stakeholders are. Thirdly, investors are widely considered to be the most relevant stakeholders by managers. And finally, managers are more likely to adjust their behavior when pressured by multiple rather than by only one single stakeholder group.

However, for investors to be able to consider firms’ CSR effectively, they need access to information on this issue. Section 6 points out that there is a lack of reliable information on CSR. Section 7 goes on to introduce the reader to the EU taxonomy on sustainable activities, which intends to remedy this problem. In this section, we also explain the lawmaker’s concept behind the EU taxonomy, its application in practice and point to future developments as well as limitations of the EU taxonomy. Given the effect that CSR-conscious investing can have on businesses and the economy as a whole, the EU taxonomy will constitute a cornerstone of the green transformation of the EU economy.

Overall, this chapter outlines why and how CSR and CSR-conscious investing can contribute to a green transformation of modern societies by reconciling the goals of firm value maximization and environmental sustainability. Central to this harmonization is that sustainability is increasingly perceived as a value of outstanding relevance. This shift in perception puts pressure on firm managers to meet stakeholders’ expectations regarding firms’ sustainability. Failing to satisfy such demands increasingly has monetary consequences for firms and for managers. The increasing awareness towards environmental issues thus not only has led to the emergence of CSR, but it also provides managers with incentives to include sustainability issues in their decision-making processes. This chapter points out that the overwhelmingly negative perception of capitalism and the motive of firm value maximization as the “gravedigger of the natural environment” is misleading. In fact, firm value maximization (mostly) has to satisfy the social norms prevalent within societies. For long, stakeholders, such as customers, have not placed enough emphasis on sustainability to ensure that it is considered in corporate boardrooms.

We acknowledge however in the concluding Sect. 8 that these concepts have limitations and that other actions are needed to achieve a transformation towards an ecologically sustainable society. Despite this chapter focusing on the role of firms and investors, other societal actors are also of major relevance for these efforts, as they will also bear a substantial burden of the transformative process.

2 What is Corporate Social Responsibility?

According to ISO 26000, social responsibility is the “responsibility of an organization for the impacts of its decisions and activities on society and the environment, through transparent and ethical behavior that: contributes to sustainable development, including the health, and the welfare of society, takes into account the expectations of stakeholders, is in compliance with applicable law and consistent with international norms of behavior, and is integrated throughout the organization and practiced in its relationships.” Beyond that, numerous definitions of corporate social responsibility (CSR) have emerged from the scientific literature. However, the common theme among all definitions is a reference to ethics, sustainability, and stakeholders. Moreover, it seems widely acknowledged that CSR only refers to actions that go beyond firms’ legal requirements (Carroll 1991; Barnea and Rubin 2010).

The World Bank, for example, defines corporate social responsibility as the “commitment of businesses to behave ethically and to contribute to sustainable economic development by working with all relevant stakeholders to improve their lives in ways that are good for business, the sustainable development agenda, and society at large.” Carroll’s (1991) view on CSR encompasses the widest array of aspects, where he defines CSR as a business behavior that is economical, environment-friendly, legal, and socially supportive. According to Salzmann (2013), economic and legal aspects of CSR in Carroll’s (1991) definition are associated with extrinsic preferences while ethical and philanthropic aspects are related to intrinsic aspects.

Benabou and Tirole (2010) distinguish between three categories of CSR based on the motivation underlying the CSR activities. The first category is “strategic CSR” which is aimed at securing a competitive advantage, advertising, or promoting a favorable image. This category is motivated by the axiom “doing well by doing good.” Moreover, the rationale behind this category is that the profits earned by the firm will primarily benefit the shareholders as well as other stakeholders. This view indicates that CSR represents a win–win outcome for shareholders and stakeholders, as doing good for other stakeholders can indirectly increase firm value (Benabou and Tirole 2010; Deng et al. 2013).

The second category is “not-for-profit CSR,” which is also labeled “delegated philanthropy” (Benabou and Tirole 2010) or “altruistic CSR” (Liang and Renneboog 2020). This category emerges from societal or stakeholder demand and expectations towards the firm. It is characterized by shareholders being willing to forgo profits in favor of the overall social well-being (Liang and Renneboog 2020; Bagnoli and Watts 2003).

The third category of CSR considers the agency situation between shareholders and managers. This type of CSR emerges when firms’ managers want to invest in philanthropic activities regardless of other stakeholders’ benefits. The underlying managerial motivation can range from reputational gains to personal pet projects. Such initiatives are not aligned with firm value wealth maximization and are thus referred to as doing good with other people’s money (Benabou and Tirole 2010).

While CSR belonging to the first category is by definition in the interest of shareholders, CSR from the second category is not. CSR belonging to the third category only is in the interest of managers. In the next sections, we will elaborate in detail how CSR can be detrimental or advantageous for shareholders. From the perspective of corporate finance, the dominant concern of shareholders is that of increasing firm value. Firm value depends on the firm’s (i) future cash flows and its (ii) cost of capital. Higher (expected) future cash flows correspond to higher firm value, as the firm will use its future cash flows to repay investors for their initial investment outlay. The higher the payments that investors obtain for the initial investment outlay, the more highly they will value the firm. A firm’s cost of capital is the minimum expected rate of return that investors require in order to provide funds to the firm. Investors evaluate the payoffs they receive from the firm against its cost of capital. A higher cost of capital thus means that investors will value the firm at a lower price. Assuming a simple situation, where a firm delivers a perpetual and constant expected cash flow, firm value is given by

The next sections elaborate in detail on how CSR can affect future cash flows and the cost of capital. Section 3.1 explains how CSR affects future cash flows. We first point out the negative consequences of CSR on firms’ cash flows, which are due to managers selfishly spending firm resources. The positive effects of CSR—elaborated in Sect. 3.2—are due to stakeholders behaving more favorably to the firm. We will explain that this behavior affects cash flows in the case of product and factor market participants of the firm, namely employees, customers, and suppliers, as well as when considering governments and the public at large. Only when investors react more favorably to the firm, CSR has an effect on the firm’s cost of capital.

3 The Effects of CSR on Future Cash Flows

3.1 Negative Effects of CSR on Firm Value Due to Managerial Opportunism

In line with the third category of CSR according to Benabou and Tirole (2010), CSR viewed as a “private provision of public goods” may negatively affect a firm’s performance if it represents private benefits for the managers in terms of reputation, job security or other tangible and intangible benefits. Empirical evidence indeed shows that managers over-engage in CSR for private benefits (Krüger 2015; McWilliams et al. 2006; Cheng et al. 2013), to seek personal gains like job security by avoiding close monitoring (Carroll 1991), to enhance their reputation as good citizens (Barnea and Rubin 2010; Surroca and Tribó 2008), to hide earnings management (Prior et al. 2008; Chih et al. 2008; Muttakin et al. 2015) and to mask the adverse impacts of their decisions (McCarthy et al. 2017). Eventually, the violation of managers’ agency role by investing in CSR will lead to inefficiency of investments and hence deterioration of shareholders’ wealth (Masulis and Reza 2015).

3.2 Positive Effects of CSR on Firm Value Due to Stakeholder Reactions

The positive effects of CSR on cash flows refer to the first category of CSR according to Benabou and Tirole (2010) and manifest in terms of developing intangible assets like human capital and the reputation which ultimately results in enhanced competitiveness of the firm (Jiao 2010). The literature also predominantly confirms this perspective that CSR promotes the financial performance of firms. For instance, a meta-analysis by Margolis et al. (2007) documents that approximately half of the existing empirical studies confirm a positive effect of CSR on financial performance. Friede et al. (2015) even find that more than 90% of the empirical studies confirm this relationship. Similarly, other studies associate CSR with better financial performance and ultimately with higher firm value (Jo and Harjoto 2012; Al-Tuwaijri et al. 2004; Burnett and Hansen 2008; Erhemjamts et al. 2013; Rodgers et al. 2013). These studies measure financial performance in terms of accounting-based proxies (e.g., return on equity or return on assets) as well as market-based proxies (e.g., market-to-book ratio or long-term stock returns).

Various other researchers have also investigated the impact of different components of CSR on firm value. For instance, Guenster et al. (2011) conclude that firms’ environmental performance is positively related to their value while other researchers provide evidence for a positive effect of social performance on firm value (Jiao 2010; Orlitzky et al. 2003). These mechanisms also have implications for firms’ CSR performance itself, as firm value considerations motivate managers to behave socially and environmentally responsible (Heinkel et al. 2001; Ghoul et al. 2011).

The next two sections detail how CSR can increase firm cash flows by changing how either employees, suppliers, and customers or governments and the public at large behave towards the firm.

3.2.1 Employees, Suppliers, and Customers

CSR improves the perception of customers, suppliers, and employees about the firm (Campbell et al. 1999). Thus, CSR leads firstly to increased sales volumes due to customers being willing to pay higher prices for sustainable products (Lins et al. 2017) and lower risks of consumer boycotts (Waddock and Graves 1997). Secondly, CSR reduces the risks of strikes since employees behave more loyally towards the firm. It also leads to higher employee motivation and satisfaction (Edmans 2012), thus increasing productivity. Thirdly, suppliers offer more favorable conditions to firms with a better CSR performance (Dai et al. 2021).

By enhancing the image that these participants of the firm’s product and factor markets have about the firm, CSR contributes to increasing the firm’s cash flow and thus positively affects firm value. Moreover, high-CSR firms are also more innovative when it comes to developing new business models, products, and services thus securing the basis for future cash flows (Nidumolu et al. 2015; Famiyeh 2017). For example, Porter and Linde (1995) argue that “green” firms are not only more proactive in adopting strategies which involve finding innovative solutions to harmful waste and pollution challenges, but also with regard to other matters.

3.2.2 Governments and Public at Large

Governments are interested in firms’ CSR, as such business practices meet governmental policy objectives. This works by not only achieving environmental goals but also human development goals. Similarly, since CSR involves the interaction of a broad variety of stakeholders, it is used to regulate the roles and relations among all stakeholders including civil society, businesses, and governments (Steurer 2010).

The general public being the direct recipient of CSR activities can pressurize firms in terms of private politics, through protests and lawsuits. In some cases, activists even go as far as buying enough shares of a firm to initiate a proxy vote (Eesley and Lenox 2006). Along these lines, previous studies conclude that CSR can lower penalties for existing regulatory violations while it also decreases the likelihood of new legal cases (Hong and Liskovich 2015; Barnett et al. 2018). This underlying risk associated with environmental violations can seriously affect firm’s cash flow and ultimately its value. British Petroleum’s (BP) Deepwater Horizon oil spill of 2010 is a good example of how firms’ cash flows can be adversely affected due to the ever-active role of governments and the general public. The incident has costed BP an amount of 63.4 billion dollars, to cover the clean-up costs and legal fees till September 2018.

Beyond reducing potential clean-up costs or legal fees, certain aspects of CSR are likely to become more relevant as they reduce a firm’s Pigouvian tax burden. Governments are currently seriously considering to intensify the use of Pigouvian taxes which are based on environmental taxation to internalize the negative environmental externalities. Even though Pigouvian taxation is often criticized for its political infeasibility, Germany has recently implemented carbon price reforms. The pressure for such meaningful legislation is partly attributed to the young public, represented by Fridays for Future and partly due to the EU Effort Sharing Regulation (Edenhofer et al. 2021).

4 How Does CSR Reduce the Cost of Capital?

Classical finance views an investment’s riskiness as the only determinant of the minimum expected rate of return that investors demand from that investment besides the riskless interest rate for lending (Markowitz 1952). The logic behind this view is simple: Generally, risk-averse investors demand higher expected returns as a compensation for risk. However, behavioral finance has demonstrated that investors do not solely consider monetary aspects in their financial decision making but that also other features of an investment affect the cost of capital. Importantly, investors also take into account to what extent investment projects comply with their moral norms. Examples of this are so-called sin stocks. Firms that make profits from, for example, weapons manufacturing, tobacco, or sex-related services, are deemed immoral by many investors and thus investors are only willing to invest in these firms, if they offer on average a higher return as a compensation (Hong and Kacperczyk 2009; Bolton and Kacperczyk 2020). Since sustainability has become an important aspect of moral norms, this mechanism thus reduces the cost of equity capital (Ghoul et al. 2011) and debt capital (Goss and Roberts 2011; Attig et al. 2013) of firm firms which behave socially responsible.

Moreover, Dhaliwal et al. (2011) finds that when firms start CSR-related disclosures, they enjoy a reduction in the cost of equity in the subsequent years. This effect works by reducing the information asymmetry regarding CSR and hence attracting CSR-dedicated institutional investors. Several other studies also conclude that strict disclosure standards regarding CSR are useful in reducing informational asymmetry and ultimately the cost of capital for the firm (Hail and Leuz 2006; Chen et al. 2009). In this section, we explain at least four distinct channels through which CSR reduces firms’ cost of capital in more detail. Common to them is the argument that investors consider CSR as a moral obligation and that this belief determines investors’ behavior towards the firm.

-

(i)

Moral Dividend: Moral Behavior of Firms Compensates for Lower Returns

Financial markets have a “discriminatory taste” for CSR, which is not explained by the traditional risk and return relationship (Derwall 2007). Bollen (2007) finds that cash inflow volatility of funds with a focus on firms, which behave socially responsible, is lower than that of their “conventional” counterparts. Although these funds yield relatively lower returns, the investors’ inclination to such funds may be attributed to investors’ non-financial utility. As already mentioned, this component is often labeled as a “moral (or social) dividend.” Liang and Renneboog (2020) define moral dividend as “the return given up in exchange for an increase in utility driven by the knowledge that one invests ethically.”

-

(ii)

Enlarging the Investor Base: Investors Screen Out Amoral Firms

CSR also results in a lower cost of capital, since more investors are willing to supply a sustainable firm with funds. Heinkel et al. (2001) show that negative or exclusionary screening by investors leads to fewer investors—or a smaller investor base—for firms with low levels of CSR. If there is an undersupply of funds to the firm, the cost of capital to acquire sufficient funds will naturally increase. In simple words, more investments in high CSR-performing firms increase the supply of capital for these firms and hence decrease the corresponding cost of capital while divesting out of low CSR-performing firms decreases the supply of capital and hence increases the cost of capital for these firms. However, this effect depends on the relative size of socially responsible investment opportunities as compared to alternative opportunities available in the capital market (Haigh and Hazelton 2004; Statman 2000).

-

3.

Stabilizing the Investor Base: CSR-Conscious Investors Are More Loyal in Times of Crisis

Bollen (2007) and Renneboog et al. (2011) find that CSR-conscious investors do not withdraw their funds even in the case of low returns. Hence, high-CSR firms are more secure that their investors will not leave the firm during times of crisis.

However, CSR-conscious investors are repaid for their loyalty in times of crisis. For instance, during the 2008–2009 financial crisis, companies with a high CSR performance achieved four to seven percentage points higher shareholder returns than companies with low CSR performance, as measured by the intensity of CSR. This works via higher cash flows in the form of higher sales growth and gross profit margins and a decreased cost of capital, as these high CSR firms can more easily raise capital in financial crises (Friede et al. 2015).

-

(iv)

Risk Reduction

CSR can influence the cost of capital via reducing firm risk (Chava 2014). Firm risk is associated with the idea that low-CSR firms are considered riskier by investors. Waddock and Graves (1997) point out that firms with low CSR are relatively more exposed to lawsuits. As a compensation for this higher risk, investors demand higher rates of return from low-CSR firms (Ghoul et al. 2011; Chava 2014). Similarly, Attig et al. (2013) show that higher CSR engagement leads to better credit ratings and ultimately lower financing cost.

5 What is the Additional Value of Investors Considering CSR?

As highlighted by our previous sections, the reactions of numerous stakeholders to a firm’s CSR activities are relevant for firm value. This leads to the question as to whether investor reactions, specifically demanding a lower cost of capital, provide any incentives for managers to engage in CSR that go beyond the incentives provided by the reactions of those stakeholders that affect the firm’s cash flow. These additional incentives could be questioned against the backdrop of managers already considering CSR due to its impact on firm cash flows and thus firm value. In this section, we address this issue and explain as to why CSR-conscious investing offers a meaningful incentive for managers to engage in CSR. In doing so, we highlight the role of CSR-conscious investing for promoting the transformation of economies towards more sustainability.

5.1 No Extreme Clientele Effect

The effects of investors screening out firms and of customers screening out firms are distinct due to diversification considerations. In the case of investors and customers alike, not all actors will equally consider CSR as important. Regarding customers, firms can specifically target non-CSR-conscious customers and thus escape the consequence of being screened out by groups of customers to some extent. The behavior of the non-CSR-conscious customers towards the firm does not change by the firm being screened out by other customers. The same does not hold for investors. In their case, screening out low-CSR firms by some investors also changes the behavior of non-CSR-conscious investors towards the firm.

Specifically, when CSR-conscious investors divest from low-CSR firms, the remaining non-CSR-conscious investors forego their potential of diversification when they decide to hold on to low-CSR firms and thus demand a higher cost of capital. This mechanism is outlined in a theoretical model by Heinkel et al. (2001), who assume two types of investors: “green” investors who value CSR and “neutral” investors who are not concerned about any ethical inclination towards CSR. All investors have the opportunity to invest in two kinds of firms. “CSR-oriented” firms fulfill the requirements of a green investor while the other firms do not consider CSR and therefore are not considered by green investors unless a firm is reformed and starts considering CSR. After green investors have excluded such firms, the risk-sharing pattern changes for the existing few neutral investors who hold (all) the stocks of non-CSR firms. As a consequence, these neutral investors expect a higher rate of return to compensate them for their lack of diversification. The higher expected rates of return due to this lack of risk-sharing lead to a decline in share prices of non-CSR firms as compared to their green counterparts.

5.2 Better Informed Actors

5.2.1 More “Adequate” Reaction

The stakeholders of firms differ regarding the extent of information they have with respect to firm sustainability. For example, customers of an average consumer goods firm do not have the resources or capabilities to assess the sustainability of the firm. They have to rely on the little information they obtain from the press and are easily deceived by advertisements. A sizable part of the shares of most firms is held by large institutional investors (Duggal and Millar 1999; Elyasiani and Jia 2010) who assess firms thoroughly (Daniel et al. 1997; Baker et al. 2010). These investors thus have much better information on the firm’s sustainability and can punish firms for behaviors that would not be noticed by customers. In this regard, institutional investors have an upper hand when it comes to influencing a firm’s policy and screening out polluting firms.

5.2.2 Quicker Reaction

Investors are the most salient stakeholders based on situations when they exhibit high levels of power, legitimacy, and urgency. Out of Mitchell’s et al. (1997) three-factor framework for stakeholder’s salience: power, legitimacy, and urgency, urgency is found to be the best predictor of shareholders’ salience (Agle et al. 1999). Urgency in this context refers to investors’ potential to create time-sensitive pressure on firms, for example in the form of deadlines or reflects an investor’s determination or assertiveness and “willingness to apply resources”(Gifford 2010). Investors are therefore expected to inspire a relatively quicker reaction towards new information as compared to other stakeholders.

Du et al. (2017) as well as Cordeiro and Tewari (2015) demonstrate that stock prices take no longer than a few days to adjust to CSR-related news. The authors argue that investors react to CSR, because they expect it to influence the firm’s cash flows in the ways pointed out above (due to employees’, customers’, suppliers’, regulators’, public reactions).

5.3 Salience of Investor Interests

Gifford (2010) deploys Mitchell et al. (1997) framework of power, legitimacy, and urgency in order to establish the salience of shareholders in contrast to other stakeholders. Mitchell et al. (1997) state that shareholders’ “power” is embedded in their ability to use their governance-related privileges, “legitimacy” is provided by the legal institutions and society in general, and “urgency” lies in the shareholders’ capacity to establish deadlines for their demands. In this vein, managers generally consider the interests of investors relatively stronger than those of other stakeholders of the firm. This could be due to the fact that managers are legally obliged to act in the best interest of investors in most legal systems and only recently laws that allow managers to also consider the interest of other stakeholders have gained more and more ground (Alexander et al. 1997).

5.4 Multiplicative Effects

Rowley (1997) points out that managers respond to the interaction of multiple stakeholders rather than to each stakeholder individually. In this vein, Neville and Menguc (2006) propose that only considering a stakeholder’s independent effect on the firm’s CSR is too narrowly framed, as a simple dyadic relationship ignores the relatively complex interaction effect of other stakeholders in the stakeholders’ network. The authors therefore introduce the concept of stakeholders’ multiplicity, according to which stakeholders sometimes compete, coordinate, or complement each other to exert influence over the firm. For instance, protest groups tend to persuade consumers in order to abstain them from buying a certain product or employees may lobby with governments or engage in “whistle-blowing” to influence the legislative process.

Thus, not only the separate effects of CSR-conscious investors’ influence must be considered, when looking at their relevance, but the multiplicative effect of their behavior which considers other stakeholders as well. However, there are no empirical studies which quantify these interactions or multiplicity of effects of investors with other stakeholders on firms’ decisions regarding CSR. There only exists anecdotal evidence which shows that interaction effects of shareholders and other stakeholders like environmental activists can lead to significant decisions against a firm: For instance, activists in the Netherlands set various protests to pressurize large pension funds to divest from environmentally adverse companies including oil, coal, and gas companies. ABP being one of the largest pension funds was sued by a climate action group to divest from fossil fuel companies in order to comply with the terms of the Paris climate agreement. Owing to such pressures, ABP announced that it would divest €15 bn worth of investments by the first quarter of 2023.

6 The Problem of Evaluating Firms’ CSR Performance

This far, we have highlighted the important and unique ways in which CSR-conscious investing contributes to transforming economies towards more sustainability. However, CSR-conscious investors are faced with one major challenge. They have limited means to assess the CSR performance of firms.

This problem has not been resolved by the increasing number of independent rating agencies over the past years (Boffo and Patalano 2020). The EU Commission has found in a recent consultation that the rating market is not functioning well today (European Commission n.d.-a). The major shortcoming of ratings is related to a lack of transparency on the methodology applied by the provider (European Commission n.d.-a). Additionally, the ratings from different agencies can strongly diverge related to the framework, methodology, metrics, key indicators, qualitative judgment, and weighting of subcategories (Boffo and Patalano 2020). The unaudited and different rating outcomes across providers also raise the question of reliability and biases leading to better ratings for specific firms within the methodology (Boffo and Patalano 2020). Liang and Renneboog (2020) point out a correlation of only 0.3 among different raters, which casts serious doubts on the validity of CSR ratings as compared to a correlation of 0.99 for credit ratings among top raters. Beyond varying methodologies, differences in ratings can also be attributed to deviating definitions of CSR (Chatterji et al. 2016).

Sustainability reporting has gained significant importance over the past years. It has been regulatorily anchored in the EU’s Non-Financial Reporting Directive (NFRD) since 2018, thus far, only obliging large companies with more than 500 employees to disclose social and environmental corporate data (Hahnkamper-Vandenbulcke 2021). Yet, with the growing sustainability reporting also of firms outside the scope of the NFRD, many analyses have been performed, identifying several shortcomings in implementing the reporting under the NFRD. Primarily, since no standardized reporting framework is predetermined, a flexibility for firms to choose from several reporting frameworks such as the commonly known Global Reporting Initiative (GRI), the United Nations Global Compact, or the United Nations Sustainable Development Goals (SDGs) remains (Hahnkamper-Vandenbulcke 2021). As a result of the various reporting frameworks, sustainability reports are lacking a comparable basis (Hahnkamper-Vandenbulcke 2021). Additionally, past analyses have repeatedly demonstrated that the disclosed data companies report often exhibit insufficient quality (Alliance for Corporate Transparency 2020). Thereby, reported information is frequently limited to general policies, not including any measurable, science-based targets and key performance indicators (e.g., greenhouse gas emissions) related to these policies (Alliance for Corporate Transparency 2020).

This lack of a harmonized and transparent methodology to evaluate the CSR activities of firms’ not only leads to an informational deficit on the investors’ side when it comes to firms’ sustainability. Moreover, it allows firms to either misstate an exaggerated CSR focus or to conceal potentially harmful information. This practice is often referred to as “greenwashing,” a term which designates “sugar-coating” of environmental and social engagement.

Overall, transparent and reliable CSR data from firms are needed to redirect capital flows towards sustainable investments and incorporate sustainability risks into the decision-making process of banks and investors. For this reason, a pan-European sustainable finance strategy was introduced, with one of the primary objectives being the development of a robust and science-based classification system—the EU taxonomy. The EU taxonomy aims to provide a common language for investors, companies, and policymakers on economic activities that can be considered environmentally sustainable (European Commission n.d.-b). Thus, general climate and environmental objectives are translated into science-based, activity-specific criteria measuring the environmental performance of, e.g., firms or financial products. The next section provides the reader with an overview of the EU taxonomy for sustainable activities.

7 The EU Taxonomy for Sustainable Activities

Until 2018 the EU market lacked sustainability-focused regulatory standards providing transparency for sustainable business practices and financial products (Pettingale et al. 2022). Under the Action Plan on financing sustainable growth presented in March 2018, the EU made the first attempt to introduce an EU-wide classification system (the so-called EU taxonomy) for sustainable economic activities with the purpose of reorienting capital flows towards sustainable investments (Canfora et al. 2021). The result was the formation of the Taxonomy Regulation which entered into force in July 2020 (Canfora et al. 2022).

Yet, the Taxonomy Regulation defines only the framework for developing and applying the EU taxonomy. The actual EU taxonomy, including an “operational list” of science-based technical screening criteria for defining environmentally sustainable economic activities, is implemented through so-called Delegated Acts supplementing the Taxonomy Regulation (Canfora et al. 2022). In this way, the EU for the first time intends to provide a common understanding for companies, investors, and policymakers of what is understood as a sustainable investment based on the evaluation of scientific based screening criteria for economic activities (European Commission n.d.-b).

Moreover, the EU taxonomy plays a crucial role in aiming to achieve the goals under the European Green Deal, as the EU has firmly anchored the further implementation and development of the EU taxonomy Delegated Acts at the core of financing the transition (Canfora et al. 2021).

7.1 Key Aspects of the EU Taxonomy Framework

The Taxonomy Regulation (Art. 9) addresses the following six environmental objectives, which are further elaborated in the individual delegated acts:

-

(1)

climate change mitigation,

-

(2)

climate change adaptation,

-

(3)

the sustainable use and protection of water and marine resources,

-

(4)

the transition to a circular economy,

-

(5)

pollution prevention and control, and

-

(6)

the protection and restoration of biodiversity and ecosystems (Gräf and Weidner 2020).

A first Delegated Act (also referred to as “Climate Delegated Act”) on sustainable activities for climate change mitigation and adaptation objectives (1)–(2) was already formally adopted in 2021 and has been applicable since January 2022. A second Delegated Act expected for 2022 will encompass the four remaining environmental objectives (3)–(6) and some additional criteria for the climate-related environmental objectives (1)–(2) (European Commission n.d.-a).

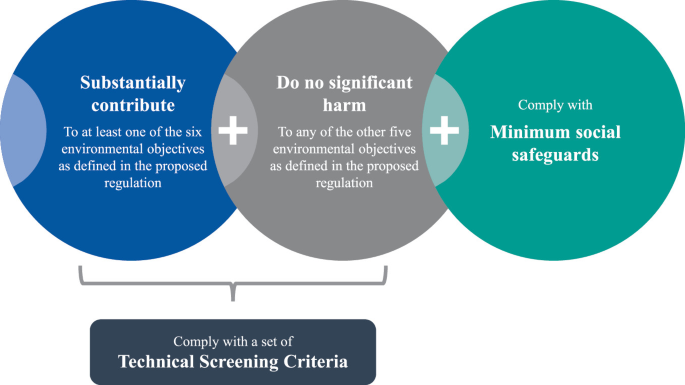

Moreover, the Taxonomy Regulation in Art. 3 defines four basic requirements that must be fulfilled for economic activities listed in a delegated act to qualify as sustainable and thus be considered taxonomy-aligned. Thereby an economic activity must:

-

(a)

substantially contribute (SC) to at least one of the six environmental objectives,

-

(b)

do no significant harm (DNSH) to any of the other five environmental objectives,

-

(c)

comply with a set of minimum social safeguards (e.g., with regard to social and human rights) listed in the Taxonomy Regulation, and

-

(d)

fulfill a set of activity-specific technical screening criteria (TSC), defining SC and DNSH for the respective activity (see Fig. 1) (Gräf and Weidner 2020)

Fig. 1

Requirements for taxonomy-aligned activities (Gräf and Weidner 2020)

Yet, for an economic activity to be considered “taxonomy-aligned,” the activity has to be considered “taxonomy-eligible” in the first place, meaning that the economic activity related to a specific code of the statistical classification of economic activities in the EU—Nomenclature of Economic Activities (NACE)—simply needs to be on the list of activities included in the first delegated act (UNEP Fi and EBF 2022). Activities that are not listed and, therefore, are not taxonomy-eligible cannot achieve the status of being taxonomy-aligned (UNEP Fi and EBF 2022). Conversely, this does not necessarily mean that the activities are considered polluting. Currently, the EU taxonomy focuses on activities considered to be “having the biggest impact” by making a substantial contribution to the specific objective.

Furthermore, given the complexity of each environmental objective, different criteria can be required for an economic activity to achieve a substantial contribution. In these terms, for the climate-related objectives, three types of economic activities differing slightly in for the way of achieving substantial contribution were categorized:

-

(1)

activities that in and of themselves contribute substantially to one of the six environmental objectives,

-

(2)

transitional activities where there are no technologically and economically feasible low-carbon alternatives, but that support the transition to a climate-neutral economy, and

-

(3)

enabling activities that qualify by making a substantial contribution to one or more of the objectives and where that activity (a) does not lead to a lock-in in assets undermining long-term environmental objectives, considering the economic lifetime of those assets and (b) has a substantial positive environmental impact on the basis of lifecycle considerations (UNEP Fi and EBF 2022).

7.2 The EU Taxonomy in Practice

The Taxonomy Regulation mandates three user obligations. On the one hand, the Taxonomy Regulation makes it mandatory throughout the Sustainable Finance Disclosure Regulation (SFDR) for financial market participants whose financial products promote, among other characteristics, environmental or social characteristics or have sustainable investment as their objective, to disclose the share of investments in taxonomy-aligned activities (Canfora et al. 2022). For all other financial products, financial market participants must include a clear disclaimer that the financial product does not consider the EU criteria for environmentally sustainable economic activities (Canfora et al. 2022).

On the other hand, the Taxonomy Regulation also obliges large companies that are already required to provide a non-financial statement under the Non-Financial Reporting Directive (NFRD) to disclose the share of their revenue from taxonomy-aligned activities as well as the share of their investments (CapEx), or where relevant operational expenses (OpEx) (Canfora et al. 2022).

Under Article 8 of the Taxonomy Regulation and the Non-Financial Reporting Directive (NFRD), currently, only around 11,700 large listed companies, banks, and insurance companies with more than 500 employees are obliged to report EU taxonomy-related information (Baumüller and Grbenic 2021). Therefore, the European Commission has adopted a proposal for a Corporate Sustainability Reporting Directive (CSRD) which could extend the scope of the NFRD to include all “large” companies, reducing the threshold from 500 to 250 employees (European Commission n.d.-c). This change would broaden the scope of entities that need to integrate a non-financial disclosure into their management report from 11,700 to about 49,000 (European Commission n.d.-d). Nevertheless, according to the EU definition of small and medium enterprises (SMEs), most (i.e., all non-publicly listed) SMEs would still fall out of the scope. Therefore, SMEs (that are not exceptionally subjected to the NFRD) may only voluntarily disclose their EU taxonomy compliance (UNEP Fi and EBF 2022).

The mandatory corporate taxonomy disclosure aims to stimulate investment in sustainable activities, offer transparency and protection against “greenwashing” to all stakeholders, and provide the financial sector with the data they need to redirect capital to genuinely environmentally sustainable activities (Pettingale et al. 2022).

Lastly, the EU and the Member States are also required to apply the EU taxonomy when setting out measures, i.e., EU or national standards or labels for financial products (e.g., the EU Ecolabel criteria for retail financial products) or corporate bonds (e.g., the EU Green Bond Standard) presented as sustainable) (Canfora et al. 2022).

7.3 EU Taxonomy Applicability and Timeline

The timeline for disclosure obligations differs for non-financial and financial undertakings required to report on the EU taxonomy (see Fig. 2).

The disclosure requirements for corporate reporting on taxonomy-eligibility apply from January 1, 2022, for the climate objectives and are extended to the other four environmental objectives and the reporting on taxonomy-eligibility as well as taxonomy-alignment from January 1, 2023 (Pettingale et al. 2022). The reporting covers the fiscal year ending 2022 or respectively 2023 (Pettingale et al. 2022). For the subsequent years, the reporting scope for different corporate sizes is continuously extended according to the CSRD. As of January 1, 2024, also, all financial undertakings will need to report taxonomy-eligibility and alignment (before that, only taxonomy-eligibility) of their underlying investment; however, only if corporates have reported this information themselves beforehand (Humphreys 2021).

Further changes to the disclosure obligations on the EU taxonomy will be introduced through the CSRD that will amend the current NFRD, expanding the reporting scope and information scale. Table 1 indicates the changed reporting characteristics anticipated by amending the NFRD through the CSRD.

Thereby, the CSRD is expected to be adopted by the end of 2022, with first reporting obligations anticipated from January 1, 2025, for all large companies as well as all listed small and medium enterprises (SMEs) (UNEP Fi and EBF 2022). Furthermore, as of January 1, 2026, reporting obligations for all listed SMEs are foreseen under the CSRD (UNEP Fi and EBF 2022). Yet, the final application dates for all stakeholders reporting under the CSRD are still to be officially released.

7.4 Limitations of the EU Taxonomy

Although the EU taxonomy is considered a dynamic tool with criteria regularly updated and more activities going to be covered under its scope in the future, currently, only 13 sectors are included in the climate delegated act, with significant industries, i.e., agriculture, being excluded (Pettingale et al. 2022).

Considering the existing narrow framework of the EU taxonomy, including a list of 88 technical screening criteria for the climate change mitigation and 95 for the climate change adaptation objective, the other four environmental objectives (at the moment being under preparation), as well as the social dimension (with currently only a first framework for a social taxonomy being under development) of sustainability, still remain unaddressed (Pettingale et al. 2022; European Commission n.d.-c).

A reason for the limited spectrum of activities within the EU taxonomy lies in its first development phases, including only criteria on activities that have a high impact (high-emitting activities) or high improvement potential (zero-emitting activities); however, not addressing “moderate-emitting activities” with minor impact on the environment (Decoene and Blum 2021). Yet, such activities might be crucial in the transition to climate neutrality and less demanding for defining technical screening criteria (Decoene and Blum 2021).

As a result of the limited number of sectors, activities, and environmental objectives currently being addressed within the EU taxonomy, undertakings may not be able to declare any activities from their portfolio as taxonomy-eligible (Pettingale et al. 2022). Noting that a second Delegated Act addressing the remaining four objectives is currently under development and expected for next year, however, taking a harmonized approach as to the first Delegated Act, including only a limited number of activities and sectors prioritized by high impact and improvement potential (Platform on Sustainable Finance n.d.-a). Furthermore, the EU taxonomy framework provides a limited incentive for undertakings not considered taxonomy-eligible to transition to more sustainable business practices or investments (Pettingale et al. 2022).

Additionally, even though the EU Taxonomy builds on robust and transparent methodologies as well as processes involving external expert groups (e.g., Technical Expert Group, Platform on Sustainable Finance, and Member State Expert Group) with the primary aim of creating a science-based classification for environmentally sustainable activities, the influence of politics is an important parameter of the process itself.

Expert groups, such as the previous Technical Expert Group on Sustainable Finance (TEG) and the Platform on Sustainable Finance (PSF) now anchored in the EU Taxonomy Regulation (Art. 20), play a vital role in the development of the EU taxonomy, bringing together the best expertise on sustainability from industry, the public sector, civil society, academia and the financial sector (European Commission n.d.-e). Their main purpose is to advise the EU Commission on the further expansion of the EU taxonomy, providing recommendations on technical screening criteria based on robust methodologies and scientific evidence (European Commission n.d.-b).

Yet, against the scientific recommendations of the Platform on Sustainable Finance (PSF), a Complementary Climate Delegated Act (CDA) was adopted in July 2022, including specific nuclear and gas activities under stringent conditions within the EU taxonomy (European Commission 2022). Instead, the EU PSF, in its response to the CDA, has advised that activities related to the energy generation from fossil fuels and nuclear facilities are not in line with the Taxonomy Regulation and should rather be considered in an intermediate or amber taxonomy that is under development (Platform on Sustainable Finance 2022). Future EU taxonomy developments and policies especially targeting future generations, have the potential to strengthen the science-policy interface, improving transparency, and making the evidence and rationale for all decisions accessible to all (Allen et al. 2021). Nonetheless, the EU Taxonomy displays one of the most advanced and ambitious approaches to developing a classification system for environmentally sustainable activities.

While the EU taxonomy in its current framework features limitations, the development of the taxonomy will maintain by including further activities over time, as well as updating the technical screening criteria for the activities already included to ensure it always reflects the latest scientific and technological developments. As of now, the EU taxonomy, for the first time, represents a unified classification system labeling activities as sustainable and providing a common language for all stakeholders.

7.5 Future Developments—The Environmental Taxonomy as the Starting Point for a Social Taxonomy

In order to achieve the SDGs and meet the financing gap in developing countries, vast investments of about $2.5 to $3 trillion a year are needed in these countries for social sustainability. The current EU taxonomy framework focuses mainly on the environmental dimension, only considering social and governance aspects by requiring undertakings to meet the minimum safeguards (Platform on Sustainable Finance n.d.-b).

Thus, while the present EU taxonomy has limited inclusion of social sustainability aspects and an environmental focus, the EU has made its first attempts to develop a social taxonomy (Pettingale et al. 2022). In this context, the European Commission has provided a mandate to a subgroup of the Platform on Sustainable Finance to deliver recommendations on extending the EU taxonomy, including social objectives (Platform on Sustainable Finance n.d.-b).

Following the current EU taxonomy for environmentally sustainable economic activities, the social taxonomy would likewise define socially sustainable activities by adopting the key aspects from the environmental EU taxonomy framework. Thus, the Platform on Sustainable Finance for a future social taxonomy proposes to develop social objectives, adopting the substantial contribution and “do not significantly harm” (DNSH) principle (Platform on Sustainable Finance n.d.-b).

While the EU Commission, with the experts from the Platform on Sustainable Finance, continues to develop the environmental and social EU Taxonomy, antagonizing the current limitations of the EU taxonomy, undertakings should form future reporting and business strategies with the EU taxonomy and the future coming framework in mind.

8 Conclusion

This chapter mainly tried to link CSR-related activities with the classic firm value maximization objective. We conclude that changing preferences among firm stakeholders towards more sustainability orientation reconcile at least to some degree the concepts of firm value maximization and sustainability. The central mechanism behind this harmonization is that stakeholders behave increasingly favorable towards firms that exhibit a higher CSR performance. This favorable treatment increases firm cash flows and reduces the expected returns required by investors and thus leads to an overall increase in firm value, which provides managers with an incentive for CSR engagement. The paradigm of shareholder wealth maximization or firm value maximization thus has the potential to contribute to an effective transformation of economies towards more sustainability. For this mechanism to work successfully, it is however crucial that corporate transparency on the issue of CSR is further improved. The EU taxonomy marks a pivotal step towards achieving more transparency in this domain.

Despite the valid limitations that the EU taxonomy features in its form today, it also marks the starting point for an increasingly regulated disclosure of firms’ sustainability data based on a scientific methodology at a time when stakeholders have pleaded for more consistent and transparent sustainability reporting. Furthermore, from 2025 onwards, a considerably broader reporting based on the EU Taxonomy and unified European sustainability reporting standards (ESRS) will be established, indicating that firms cannot continue to rely on disclosing only general policies and data to receive a positive rating or to be labeled as a sustainable investment. Instead, firms will need to base their sustainability strategies on aligning with the EU taxonomy.

Even though firms not falling under the EU taxonomy today might be tempted to wait for further developments or an extended social taxonomy before aligning their business strategy with the EU taxonomy, the principles on which the methodology is designed are clear and, ultimately, it can be expected that the sustainability performance of all companies within the EU will be assessed based on these principles. Moreover, the access to sustainable capital flows will be increasingly interlinked to driving a sustainable transformation based on EU taxonomy-alignment and the adequate disclosure of the relevant data.

The future will show to what extent the transparency introduced by the EU taxonomy disclosures and the availability of corporate sustainability data will prompt a meaningful change in firms’ sustainability strategies and whether this will lead to a transition towards a (more) sustainable economy.

There are however limits to what CSR-conscious investing and thus the increased transparency on sustainability can achieve. Generally, CSR-conscious investing is more suited for promoting incremental transformation processes rather than disruptive changes in the economy. This is due to the fact that many firm assets are long-lived. An example of this are power plants. Obtaining financing for a new coal power plant might have become too costly for this energy form to be economically feasible. However, many coal power plants that are currently still in operation have been funded when carbon emissions were not a relevant concern for investors. Funding considerations do not provide a direct incentive for divesting from these long-lived assets. In addition, particularly high-risk sustainable innovations will not be financed without hesitation even by “green” investors which means that public subsidies and thus risk-taking by the whole society may be necessary. Thus, promoting transparency on firm’s CSR performance is unlikely to achieve the transformation pursued by the EU on its own. Other regulatory actions are presumably needed.

References

Agle BR, Mitchell RK, Sonnenfeld J (1999) Who matters to CEOs? An investigation of stakeholder attributes and salience, corporate performance, and CEO values. Acad Manag J 42:507–525

Alexander JC, Spivey MF, Wayne Marr M (1997) Nonshareholder constituency statutes and shareholder wealth: a note. J Bank Financ 21:417–432. https://doi.org/10.1016/S0378-4266(96)00047-7

Allen B, Hiller N, Traverso M, Ostojic S (2021) Strengthening the science-policy interface for sustainable investments

Alliance for Corporate Transparency (2020) Improving climate and sustainability corporate disclosure policies to enable sustainable finance—an analysis of the climate-related disclosures of 300 companies from Central, Eastern and Southern Europe pursuant to the EU non-financial reporting directive

Al-Tuwaijri SA, Christensen TE, Hughes K (2004) The relations among environmental disclosure, environmental performance, and economic performance: a simultaneous equations approach. Accounting, Organ Soc 29:447–471. https://doi.org/10.1016/S0361-3682(03)00032-1

Attig N, El Ghoul S, Guedhami O, Suh J (2013) Corporate social responsibility and credit ratings. J Bus Ethics 117:679–694. https://doi.org/10.1007/s10551-013-1714-2

Bagnoli M, Watts SG (2003) Selling to socially responsible consumers: competition and the private provision of public goods. J Econ Manag Strateg 12:419–445. https://doi.org/10.1162/105864003322309536

Baker M, Litov L, Wachter JA, Wurgler J (2010) Can mutual fund managers pick stocks? Evidence from their trades prior to earnings announcements. J Financ Quant Anal 45:1111–1131. https://doi.org/10.1017/S0022109010000426

Barnea A, Rubin A (2010) Corporate social responsibility as a conflict between shareholders. J Bus Ethics 97:71–86. https://doi.org/10.1007/s10551-010-0496-z

Barnett ML, Hartmann J, Salomon RM (2018) Have you been served? Extending the relationship between corporate social responsibility and lawsuits. Acad Manag Discov 4:109–126. https://doi.org/10.5465/amd.2015.0030

Baumüller J, Grbenic SO (2021) Moving from non-financial to sustainability reporting: analyzing the EU Commission’s proposal for a Corporate Sustainability Reporting Directive (CSRD). Facta Univ Ser Econ Organ:369. https://doi.org/10.22190/fueo210817026b

Benabou R, Tirole J (2010) Individual and corporate social responsibility. Economica 77:1–19. https://doi.org/10.1111/j.1468-0335.2009.00843.x

Boffo, R., Patalano R (2020) ESG investing: practices, progress and challenges. OECD Paris

Bollen NPB (2007) Mutual fund attributes and investor behavior. J Financ Quant Anal 42:683–708

Bolton P, Kacperczyk MT (2020) carbon premium around the World. SSRN Electron J.https://doi.org/10.2139/ssrn.3550233

Brown RE (2008) Sea change: Santa Barbara and the eruption of corporate social responsibility. Public Relat Rev.https://doi.org/10.1016/j.pubrev.2007.08.003

Burnett RD, Hansen DR (2008) Ecoefficiency: defining a role for environmental cost management. Accounting, Organ Soc 33:551–581. https://doi.org/10.1016/j.aos.2007.06.002

Campbell L, Gulas CS, Gruca TS (1999) Corporate giving behavior and decision-maker social consciousness. J Bus Ethics 19:375–383. https://doi.org/10.1023/A:1006080417909

Canfora P, Arranz Padilla M, Polidori O, Pickard Garcia N, Ostojic S, Dri M (2021) Substantial contribution to climate change mitigation: a framework to define technical screening criteria for the EU taxonomy

Canfora P, Arranz Padilla M, Polidori O, Garcia PN, Ostojic S, Dri M (2022) Development of the EU sustainable finance taxonomy—a framework for defining substantial contribution for environmental objectives, 3–6

Carroll AB (1991) The pyramid of corporate social responsibility: toward the moral management of organizational stakeholders. Bus Horiz 34:39–48. https://doi.org/10.1177/0312896211432941

Chatterji AK, Durand R, Levine DI, Touboul S (2016) Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strateg Manag J.https://doi.org/10.1002/smj.2407

Chava S (2014) Environmental externalities and cost of capital. Manage Sci 60:2223–2247. https://doi.org/10.1287/mnsc.2013.1863

Chen KCW, Chen Z, Wei KCJ (2009) Legal protection of investors, corporate governance, and the cost of equity capital. J Corp Financ 15:273–289. https://doi.org/10.1016/j.jcorpfin.2009.01.001

Cheng I, Hong H, Shue K (2013) Do managers do good with other people’s money? NBER Working Paper Series. Natl Bur Econ Res. http://www.nber.org/papers/w19432

Chih HL, Shen CH, Kang FC (2008) Corporate social responsibility, investor protection, and earnings management: Some international evidence. J Bus Ethics 79:179–198. https://doi.org/10.1007/s10551-007-9383-7

Cordeiro JJ, Tewari M (2015) Firm characteristics, industry context, and investor reactions to environmental CSR: a stakeholder theory approach. J Bus Ethics 130:833–849. https://doi.org/10.1007/s10551-014-2115-x

Dai R, Liang H, Ng L (2021) Socially responsible corporate customers. J Financ Econ 2021. https://doi.org/10.1016/j.jfineco.2020.01.003

Daniel K, Grinblatt M, Titman S, Wermers R (1997) Measuring mutual fund performance with characteristic-based benchmarks. J Finance 52:1035–1058. https://doi.org/10.1111/j.1540-6261.1997.tb02724.x

Decoene U, Blum O (2021) 3 ways to expand EU taxonomy and accelerate green transition. World Economic Forum

Deng X, Kang J-K, Low BS (2013) Corporate social responsibility and stakeholder value maximization: evidence from mergers. J Financ Econ 110:87–109. https://doi.org/10.1016/j.jfineco.2013.04.014

Derwall J (2007) The economic virtues of SRI and CSR. Erasmus Research Institute of Management (ERIM)

Dhaliwal DS, Khurana IK, Pereira R (2011) Firm disclosure policy and the choice between private and public debt*. Contemp Account Res 28:293–330. https://doi.org/10.1111/j.1911-3846.2010.01039.x

Du S, Yu K, Bhattacharya CB, Sen S (2017) The business case for sustainability reporting: evidence from stock market reactions. J Public Policy Mark 36:313–330. https://doi.org/10.1509/jppm.16.112

Duggal R, Millar JA (1999) Institutional ownership and firm performance: the case of bidder returns. J Corp Financ 5:103–117. https://doi.org/10.1016/S0929-1199(98)00018-2

Edenhofer O, Franks M, Kalkuhl M (2021) Pigou in the 21st century: a tribute on the occasion of the 100th anniversary of the publication of the economics of welfare. Int Tax Public Financ. https://doi.org/10.1007/s10797-020-09653-y

Edmans A (2012) The link between job satisfaction and firm value, with implications for corporate social responsibility. Acad Manag Perspect 26:1–19. https://doi.org/10.5465/amp.2012.0046

Eesley C, Lenox MJ (2006) Firm responses to secondary stakeholder action. Strateg Manag J 27:765–781. https://doi.org/10.1002/smj.536

El Ghoul S, Guedhami O, Kwok CCY, Mishra DR (2011) Does corporate social responsibility affect the cost of capital? J Bank Financ 35:2388–2406. https://doi.org/10.1016/j.jbankfin.2011.02.007

Elyasiani E, Jia J (2010) Distribution of institutional ownership and corporate firm performance. J Bank Financ 34:606–620. https://doi.org/10.1016/j.jbankfin.2009.08.018

Erhemjamts O, Li Q, Venkateswaran A (2013) Corporate social responsibility and its impact on firms’ investment policy, organizational structure, and performance. J Bus Ethics 118:395–412. https://doi.org/10.1007/s10551-012-1594-x

European Commission (2022) EU taxonomy: complementary climate delegated act to accelerate decarbonisation 2022

European Commission (n.d.-a) Summary report targeted consultation on the functioning of the ESG ratings market in the EU and on the consideration of ESG factors in credit ratings

European Commission (n.d.-b). EU taxonomy for sustainable activities

European Commission (n.d.-c) Commission Delegated Regulation (EU) 2021/2139 supplementing Regulation (EU) 2020/852 of the European Parliament and of the Council by establishing the technical screening criteria for determining the conditions under which an economic activity qualifies

European Commission (n.d.-d) Proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as regards corporate sustainability reporting

European Commission (n.d.-e) Platform on sustainable finance. https://finance.ec.europa.eu/sustainable-finance/overview-sustainable-finance/platform-sustainable-finance_en

Famiyeh S (2017) Corporate social responsibility and firm’s performance: empirical evidence. Soc Responsib J 13:390–406. https://doi.org/10.1108/SRJ-04-2016-0049

Forbes (n.d.) System change not climate change: capitalism and environmental destruction. https://www.forbes.com/sites/rainerzitelmann/2020/07/13/system-change-not-climate-change-capitalism-and-environmental-destruction/?sh=75809bac6d72. Accessed 9 Jan 2023

Friede G, Busch T, Bassen A (2015) ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J Sustain Financ Invest 5:210–233. https://doi.org/10.1080/20430795.2015.1118917

Gifford EJM (2010) Effective shareholder engagement: the factors that contribute to shareholder salience. J Bus Ethics 92:79–97. https://doi.org/10.1007/s10551-010-0635-6

Global Social Challenges (n.d.) Is the fundamental cause of climate change capitalist economic growth? https://sites.manchester.ac.uk/global-social-challenges/2021/05/05/is-the-fundamental-cause-of-climate-change-capitalist-economic-growth/. Accessed 9 Jan 2023

Goss A, Roberts GS (2011) The impact of corporate social responsibility on the cost of bank loans. J Bank Financ. https://doi.org/10.1016/j.jbankfin.2010.12.002

Gräf F, Weidner J (2020) Sustainable Finance-Taxonomie—Ein Klassifizierungssystem soll erstmals ein einheitliches Verständnis der Nachhaltigkeit von wirtschaftlichen Tätigkeiten in der EU schaffen

Guenster N, Bauer R, Derwall J, Koedijk K (2011) The economic value of corporate eco-efficiency. Eur Financ Manag 17:679–704. https://doi.org/10.1111/j.1468-036X.2009.00532.x

Hahnkamper-Vandenbulcke N (2021) Briefing implementation appraisal non-financial reporting directive.

Haigh M, Hazelton J (2004) Financial markets: a tool for social responsibility? J Bus Ethics 52:59–71. https://doi.org/10.1016/S1041-7060(07)13003-0

Hail L, Leuz C (2006) International differences in the cost of equity capital: do legal institutions and securities regulation matter? J Account Res 44:485–531. https://doi.org/10.1111/j.1475-679X.2006.00209.x

Heinkel R, Kraus A, Zechner J (2001) The effect of green investment on corporate behavior. J Financ Quant Anal 36:431. https://doi.org/10.2307/2676219

Hong H, Kacperczyk M (2009) The price of sin: the effects of social norms on markets. J Financ Econ 93:15–36. https://doi.org/10.1016/j.jfineco.2008.09.001

Hong H, Liskovich I (2015) Crime, punishment and the Halo effect of corporate social responsibility. Natl Bur Econ Res. http://www.nber.org/papers/w21215

Humphreys N (2021) What the EU ESG taxonomy requires you to report and when. Bloom Prof Serv

Institute of Economic Affairs (n.d.) Left turn ahead: Surveying attitudes of young people towards capitalism and socialism. https://iea.org.uk/publications/left-turn-aheadsurveying-attitudes-of-young-people-towards-capitalism-and-socialism/. Accessed 9 Jan 2023

Jiao Y (2010) (2010) Stakeholder welfare and firm value. J Bank Financ 34:2549–2561. https://doi.org/10.1016/j.jbankfin.2010.04.013

Jo H, Harjoto MA (2012) The causal effect of corporate governance on corporate social responsibility. J Bus Ethics 106:53–72. https://doi.org/10.1007/s10551-011-1052-1

Karatzoglou B, Giannetti BF (2021) A resilient and sustainable world: contributions of cleaner production. Circular Economy

Krüger P (2015) Corporate goodness and shareholder wealth. J Financ Econ 115:304–329. https://doi.org/10.1016/j.jfineco.2014.09.008

Lee SY, Carroll CE (2011) The emergence, variation, and evolution of corporate social responsibility in the public sphere, 1980–2004: the exposure of firms to public debate. J Bus Ethics. https://doi.org/10.1007/s10551-011-0893-y

Liang H, Renneboog L (2020) Corporate social responsibility and sustainable finance: a review of the literature. SSRN Electron J. https://doi.org/10.2139/ssrn.3698631

Lindgreen A, Swaen V, Johnston WJ (2009) Corporate social responsibility: an empirical investigation of U.S. organizations. J Bus Ethics. https://doi.org/10.1007/s10551-008-9738-8

Lins KV, Servaes H, Tamayo A (2017) Social capital, trust, and firm performance: the value of corporate social responsibility during the financial crisis. J Finance 72:1785–1824. https://doi.org/10.1111/jofi.12505

Margolis JD, Elfenbein HA, Walsh JP (2007) Does it pay to be good? A meta-analysis and redirection of research on the relationship between corporate social and financial performance. Ann Arbor 1001:48109–51234

Markowitz H (1952) Portfolio selection. J Finance 7:77–91

Marques L (2020) The illusion of a sustainable capitalism. In: Capitalism and environmental collapse. Springer International Publishing, Cham, pp 333–360. https://doi.org/10.1007/978-3-030-47527-7

Masulis RW, Reza SW (2015) Agency problems of corporate philanthropy. Rev Financ Stud 28:592–636. https://doi.org/10.1093/rfs/hhu082

McCarthy S, Oliver B, Song S (2017) Corporate social responsibility and CEO confidence. J Bank Financ 75:280–291. https://doi.org/10.1016/j.jbankfin.2016.11.024

McWilliams A, Siegel DS, Wright PM (2006) Corporate social responsibility: strategic implications. J Manag Stud 43:1–18. https://doi.org/10.1111/j.1467-6486.2006.00580.x

Mitchell RK, Agle BR, Wood DJ (1997) Toward a theory of stakeholder identification and salience: defining the principle of who and what really counts. Acad Manag Rev 22:853–886. https://doi.org/10.5465/AMR.1997.9711022105

Muttakin MB, Khan A, Azim MI (2015) Corporate social responsibility disclosures and earnings quality: are they a reflection of managers’ opportunistic behavior? Manag Audit J 30:277–298. https://doi.org/10.1108/MAJ-02-2014-0997

Neville BA, Menguc B (2006) Stakeholder multiplicity: toward an understanding of the interactions between stakeholders. J Bus Ethics 66:377–391. https://doi.org/10.1007/s10551-006-0015-4

Nidumolu R, Prahalad CK, Rangaswami MR (2015) Why sustainability is now the key driver of innovation. IEEE Eng Manag Rev 43:85–91. https://doi.org/10.1109/EMR.2015.7123233

Orlitzky M, Schmidt FL, Rynes SL (2003) Corporate social and financial performance: a meta-analysis. Organ Stud 24:403–441. https://doi.org/10.1177/0170840603024003910

Pettingale H, Kuenzer J, Reilly P, De Maupeou S (2022) EU taxonomy and the future of reporting

Platform on Sustainable Finance (2022) Response to the complementary delegated act 2022

Platform on Sustainable Finance (n.d.-a) Technical working group: taxonomy pack for feedback

Platform on Sustainable Finance (n.d.-b) Draft report by subgroup 4: Social Taxonomy

Porter ME, Van der Linde C (1995) Green and competitive: ending the stalemate. Harv Bus Rev:120–134

Prior D, Surroca J, Tribó JA (2008) Are socially responsible managers really ethical? Exploring the relationship between earnings management and corporate social responsibility. Corp Gov an Int Rev 16:160–177. https://doi.org/10.1111/j.1467-8683.2008.00678.x

Rappaport A (1986) Creating shareholder value: the new standard for business performance, vol 164

Renneboog L, Ter Horst J, Zhang C (2011) Is ethical money financially smart? Nonfinancial attributes and money flows of socially responsible investment funds. J Financ Intermediation 20:562–588. https://doi.org/10.1016/j.jfi.2010.12.003

Rodgers W, Choy HL, Guiral A (2013) Do investors value a firm’s commitment to social activities? J Bus Ethics 114:607–623. https://doi.org/10.1007/s10551-013-1707-1

Rowley TJ (1997) Moving beyond dyadic ties: a network theory of stakeholder influences. Acad Manag Rev 22:887–910. https://doi.org/10.5465/amr.1997.9711022107

Salzmann AJ (2013) The integration of sustainability into the theory and practice of finance: an overview of the state of the art and outline of future developments. J Bus Econ 83:555–576. https://doi.org/10.1007/s11573-013-0667-3

Schnaiberg A (1984) The environment: from surplus to scarcity, vol 20. Oxford University Press, New York. https://doi.org/10.1177/144078338402000225

Schnaiberg A, Gould KA (1994) Environment and society: the enduring conflict. St. Martin’s, New York

Statman M (2000) Socially responsible mutual funds (corrected). Financ Anal J 56:30–39. https://doi.org/10.2469/faj.v56.n3.2358

Steurer R (2010) The role of governments in corporate social responsibility: characterising public policies on CSR in Europe. Policy Sci 43:49–72. https://doi.org/10.1007/s11077-009-9084-4

Surroca J, Tribó JA (2008) Managerial entrenchment and corporate social performance. J Bus Financ Account 35:748–789. https://doi.org/10.1111/j.1468-5957.2008.02090.x

The Guardian (n.d.) Capitalism is killing the planet—it’s time to stop buying into our own destruction. Climate crisis. The Guardian. https://www.theguardian.com/environment/2021/oct/30/capitalism-is-killing-the-planet-its-time-to-stop-buying-into-our-own-destruction. Accessed 9 Jan 2023

UNEP FI, EBF (2022) Practical approaches to applying the EU taxonomy to bank lending

Waddock SA, Graves SB (1997) The corporate social performance-financial performance link. Strateg Manag J 18:303–319. https://doi.org/10.1002/(SICI)1097-0266(199704)18:4%3c303::AID-SMJ869%3e3.0.CO;2-G

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2024 The Author(s)

About this chapter

Cite this chapter

Breuer, W., Knetsch, A., Ostojic, S., Traverso, M., Uddin, S. (2024). Corporate Social Responsibility—Conscious Investing and Green Transformation. In: Letmathe, P., et al. Transformation Towards Sustainability. Springer, Cham. https://doi.org/10.1007/978-3-031-54700-3_7

Download citation

DOI: https://doi.org/10.1007/978-3-031-54700-3_7

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-54699-0

Online ISBN: 978-3-031-54700-3