Abstract

The forest-based bioeconomy relies on using forests as a source of raw material for producing materials and energy, as well as for a variety of other ecosystem services. The uses of forests and wood are many and, to some extent, competing. Can a limited resource simultaneously and sustainably provide raw materials for products, feedstock for energy production, and other ecosystem services? Over one-third of the land area in the EU is covered by forests, but there are large differences between the member states regarding both forest area and growing stock of wood. The harvesting of roundwood has been steadily increasing. In addition to roundwood, other tree parts, as well as residues from forest industries and post-consumer wood, are being used for both materials and energy production. There are non-negligible uncertainties regarding the future availability of forest biomass in the context of climate change, as well as difficulties to concern all the relevant constraints on biomass supply in relation to availability assessments and the difficult-to-predict effects of policies. Despite the above, it can be concluded that there is still potential to increase the utilisation of forest biomass in most of the EU regions, but this might affect the provisioning of other important ecosystem services.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

5.1 European Forests and the Utilisation of Biomass

Aside from other services, the EU’s forests represent a vast raw-material resource. Forests account for 38% of the EU28 land area (Forest Europe 2020a). In 2019, this amounted to 162 mill. ha in total, of which 138 mill. ha was available for wood supply. Forests are, however, unevenly distributed, and the share of forest area is generally higher in Northern Europe (up to 74% in Finland) than in Central or Southern Europe, where it is between 30 and 40% in many countries (e.g. France, Germany, Italy, Poland and Spain), or even less. Of the total EU28 forest area, 60% occurs in only five member states––Sweden, Finland, Spain, France and Germany.

The growing stock of the EU28 forests available for wood supply amounts to nearly 23 billion m3 (Forest Europe 2020a). The five biggest growing-stock countries account for 60% of this total, these being Germany (3.5 billion m3), France (2.9 billion m3), Sweden (2.7 billion m3), Poland (2.4 billion m3) and Finland (2.2 billion m3). The high volumes in Central Europe can be explained by a high stocking density (m3 ha−1) in the forests in relation to the somewhat lower density in Northern Europe. The above figures considered stemwood only, but branches and stumps are also potential sources of woody biomass. Such woody components can increase the aboveground biomass by 50% (Camia et al. 2018).

The woody biomass used to produce materials and energy comes from various sources. In 2015, the share of woody biomass in the EU28 that was harvested directly from domestic forests was nearly 57%, and the rest originated from imports, byproduct and coproduct supply, wood pellet supply, post-consumer wood and unaccounted sources (Cazzaniga et al. 2019b). Forest biomass comprises roundwood and primary residues, i.e., logging residues (consisting of crown biomass and stemwood loss), small-diameter trees and stumps.

There has been a clearly increasing trend in roundwood harvesting volumes in the EU28 in this millennium, apart the financial crisis that caused a slump in 2008–2009 (see Fig. 1.4 in Chap. 1 – Box: Forest Bioeconomy in the EU). Roundwood production increased from 486 mill. m3 (overbark) in 2000 to 578 mill. m3 in 2019––an increase of almost one-fifth (Food and Agriculture Organization [FAO] 2020). The five countries with the largest forest resources for wood production also harvest most of the roundwood (Fig. 5.1). In Fig. 5.1, the impact of the economic slump due to the financial crisis in 2009 is clearly visible.

Several severe storms have occurred in recent years in Europe (Forzieri et al. 2020; Senf and Seidl 2020) and their effects can be seen in terms of harvested volumes. For example, storm Gudrun in January 2005 damaged 75 mill. m3 of roundwood in Sweden, causing a supply peak of more than 30 mill. m3 (Gardiner et al. 2010). Likewise, the peak caused by storm Kyrill in January 2007, which damaged 37 mill. m3, is also discernible in Fig. 5.1. However, contrary to the two above-mentioned storms, the effect of storm Klaus in February 2009 in France, which damaged 43 mill. m3, is barely visible. Similarly, storms and other disturbances in different countries have also had significant effects. For example, the storm Vaia in Italy resulted in about 8 mill. m3 of damaged wood–– approximately the same amount as harvested in an entire year in Italy. Also, the recent dry summers in Central Europe, followed by severe bark-beetle outbreaks, have produced large amounts of damaged wood. Disturbances can have a strong impact on the local forest sector, first by creating a pulse of available timber from salvage harvesting, but later resulting in a shortage of local timber supply.

In addition to roundwood, primary residues are also being utilised, but mainly in energy production. Unfortunately, there are no EU-level statistics on the consumption of primary residues, and even national statistics may be weak. Germany, Sweden and Finland are probably the top three countries in the EU. According to Brosowski et al. (2016), the annual consumption of logging residues for energy use in Germany in 2012 was 4.0–10.5 Tg. Assuming a basic density of 400 kg m−3 for conifers and 500 kg m −3 for broadleaves, the consumption would have been roughly 9–23 mill. m3. In Sweden, the consumption of forest fuels between 2013 and 2018 was 15.2–20.2 TWh (Energimyndigheten 2020). This equates to approximately 8–10 mill. m3, assuming 1 solid m3 equals 2 MWh. In Finland, the consumption for the same period was 7–8 mill. m3 (Natural Resources Institute 2020).

The other sources of woody biomass can be divided into secondary and tertiary forestry residues and trade. Trees grown outside of forests and short-rotation coppice grown on forest or agricultural land are minor sources that are not discussed here. The secondary forestry residues (aka industrial residues) are the side products of wood processing or come from the production of wood products, and include sawdust and cutter chips, bark, slabs, lumpwood residues and black liquor (Lindner et al. 2017).

The wood resource balance introduced by Cazzaniga et al. (2019b) does not employ the same classification as above, but divides the secondary residues into sawmill residues, other industrial residues, wood pellets and black liquor. In 2015, over 87 mill. m3 of sawmill residues, 11 mill. m3 of other industrial residues, 38 mill. m3 of wood pellets and 67 mill. m3 of black liquor were used in the EU28 (Cazzaniga et al. 2019b). The cascading flows of these side-streams are illustrated in Fig. 5.2.

Woody biomass flows in the EU28 in 2015 (in mill. m 3 solid wood equivalent overbark). (Source: Cazzaniga et al. 2019a)

Tertiary forestry residues (i.e. post-consumer wood) include wooden material that is available at the end of its use as a wooden product. In 2015, the consumption of tertiary residues in the EU28 was estimated at 37 mill. m3 (Cazzaniga et al. 2019b).

Furthermore, wood is traded between the EU and other countries. Between 2010 and 2018, the EU was a net importer of roundwood, bringing in 11–18 mill. m3 (overbark) more than it exported (FAO 2020). In 2019, however, the direction of the stream reversed, with the EU exporting 2 mill. m3 more than it imported. To a large extent, this amonnt can be attributed to the Central European bark-beetle infestation, which has forced the Czech Republic, in particular, to greatly increase their timber exports.

One single country stands out among the exporters to the EU-Russia alone has exported 7–10 mill. m3 of industrial ronndwood and wood chips between 2010 and 2017 (FAO 2020). Russia’s forest area is five times larger than the EU’s, and its exports to conntries like Finland and Sweden are substantial. However, basing the feedstock sourcing of bio-based businesses solely on Russian wood imports would be challenging for several political and infrastructural reasons (Leskinen et al. 2020; Box: Huge Russian forest resources -a reality or an illusion?).

5.2 Availability of Forest Biomass

The growing stock and increment rates of Europe’s forests have been increasing almost continuously over the last several decades (Gold et al. 2006; Forest Europe 2020a). In fact, Albania is the only country in the whole of Europe that has reported a decrease in growing stock between 1990 and 2015. In recent years, the increase has been especially rapid in Central-East Europe (including Ukraine, Belarus and Georgia outside of the EU).

The major reasons for the increasing growing stock include: the fellings and natural losses that together have been less than the gross increment; the increasing increment rates and changes in forest management that have caused forests to become denser (e.g. Vilén et al. 2016); nitrogen deposition (e.g. de Vries et al. 2009; Etzold et al. 2020); as well as the combined effect of nitrogen deposition, increased atmospheric CO2 concentrations and climate change (Pretzsch et al. 2014; Flechard et al. 2020).

The relation of annual fellings to the net annual increment (NAI) is a key sustainability indicator of wood production. Generally, if the fellings fall below the NAI, the growing stock is increasing. Correspondingly, if the fellings are more than the NAI, the growing stock is decreasing. On average, 75% of the NAI was utilised by the EU28 in 2015 (Forest Europe 2020a). However, the utilisation rates varied considerably, from 99% in Belgium to 44% in Romania (and probably even lower in countries lacking data).

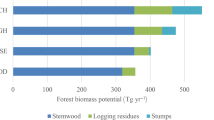

The NAI is only a rough estimate of the maximum potential availability of wood from forests, as it does not consider the stocking level of the forests, imbalances in forest age structures, the potential availability of biomass from primary residues, or ecological and socioeconomic factors. Furthermore, numerous technical, environmental, economic and social constraints, which limit the availability of forests to harvesting, need to be considered. Such factors can include soil productivity, soil and water protection, biodiversity protection, technical recovery rates, the soil bearing capacity, forest-owner behaviour, the profitability of wood production (harvesting), and regional land-use plans (Verkerk et al. 2011, 2019; Barreiro et al. 2017; di Fulvio et al. 2016; Kärkkäinen et al. 2020). When taking age-structure and stocking level into account, and correcting for the constraints, the woody biomass potential from EU forests has been estimated to range between 663 and 795 mill. m3 a−1, of which some 80–90% is stemwood, the rest being mainly logging residues (Verkerk et al. 2011, 2019; di Fulvio et al. 2016; Jonsson et al. 2018). These biomass potentials are fairly stable over time.

The highest potentials per unit of land area can be found in parts of Northern Europe (southern Finland and Sweden, Estonia and Latvia), Central Europe (Austria, the Czech Republic and southern Germany), southwest France and Portugal (Fig. 5.3).

Estimated spatial distribution of forest biomass availability in 2020 (t⋅ha−1a−1) (left) and unused potential per unit of land (t⋅ha−1a−1) (right). (Source: Verkerk et al. 2019)

Comparing the potential in the EU with the average roundwood production in 2010–2019, which was 539 mill. m3 (FAO 2020), reveals that over 80% of the stemwood potential is already in use. In fact, the share of utilised potential could be even higher. The number for roundwood production has been found to underestimate fellings due to, for example, unregistered fuelwood fellings in private forests (Jochem et al. 2015). In some of the areas, wood use is already at a high level, indicating little potential for increased use (Verkerk et al. 2019). Such areas include southern Sweden and southwestern France. However, in some regions, the potential could allow a considerable increase in utilisation.

The utilisation rate of primary forestry residues is substantially lower than for stemwood. Yet in places where the utilisation rate is high, the competition from residues can increase supply costs. For example, in southern Finland, the consumption of residues is expected to top the harvesting potential (Anttila et al. 2018).

Dees et al. (2017) estimated the potentials for secondary forestry residues in the EU28 to be 190 and 194 mill. m3 for 2020 and 2030, respectively. The total potential was further broken down into residues from the sawmill industry, pulp and paper industry, and other wood-processing industries, with shares of 43, 37 and 20% in 2012, respectively. Naturally, these potentials depend directly on the production of the industries.

5.3 Outlook for Forest Biomass Availability

Increasing harvesting to the limit of the potentially available volumes implies an increasing need for labour and machinery. While these have so far not been considered as constraints in the availability assessments, mobilising more wood is likely to increase the need for skilled labour. To some extent, this lack could be alleviated by mechanisation and technological development. Technological development could also increase the potentials, if formerly technically unavailable or too-costly resources became available. For example, developing models to estimate the right time to harvest a site on sensitive soil could remove a technical constraint (Salmivaara et al. 2020).

Mobilising such potentially available volumes would mean a more intensive use of the EU’s forest resources compared to the current situation. At the same time, the EU is trying to maintain and strengthen its forest carbon sinks. The EU’s Land Use, Land-Use Change and Forestry Regulation (EU 2018) requires that the carbon sinks of a member state be compared to a reference level, assuming a continuation of historical (2000–2009) forest management practices. Should the future forest carbon sink be lower than the reference level, a member state would generate carbon debits. It will be important to assess how increasing wood use will affect the carbon balances of forests, wood products and through substitution effects.

Finally, even if ecological constraints are generally considered in biomass availability studies, higher harvesting levels could still affect carbon storage, biodiversity and other forest functions other than wood production. In order to protect biodiversity, the EU Biodiversity Strategy proposes to increase the area of protected forest (European Commission 2020). The strategy also aims to increase the quantity, quality and resilience of EU forests. It proposes to achieve this by planting 3 billion additional trees in the EU by 2030 and by establishing protected areas for at least 30% of the land in Europe, with stricter protection of European forests. The effect of this strategy on forest biomass availability remains to be seen.

5.4 Research Implications

There is a substantial body of literature relating to the harvesting potential of forest biomass in Europe. Despite the improved understanding this provides, important challenges remain relating to the availability of data, ownership structures and behaviour, and climate change (Barreiro et al. 2017; Nabuurs et al. 2019), all of which require further research.

Existing studies on biomass availability typically rely on national forest inventory data, with these data forming a solid basis for availability estimations (Vidal et al. 2016). In recent years, countries have shifted towards statistical inventories, which has improved the reliability and accuracy of the inventory results. However, forest inventories mostly rely on national definitions, which reduce their comparability, although progress is being made in overcoming this (Alberdi et al. 2016, 2020; Gschwantner et al. 2019). A key challenge relates to the availability of such inventory data, as they are not always readily available (Nabuurs et al. 2019). Improved availability would support ‘top-down’ assessments of biomass availability, which, together with ‘bottom-up’ assessments, provide important insights into biomass availability (Barreiro et al. 2017) and European forest resources more generally. An improved availability of data would also facilitate the increased use of remote-sensing-based data to provide up-to-date and large-scale information on Europe’s forest resources (e.g. Moreno et al. 2017), and thus also biomass availability assessments.

It is evident that climate change will affect forests and forest biomass availability. Some European regions may benefit from the increased growth, while others will face reduced productivity or suffer from extreme events and natural disturbances (Lindner et al. 2014; Reyer et al. 2017; see also Chap. 3) and, thereby, the availability of wood. The frequency and intensity of forest disturbances are also likely to increase in the future (Seidl et al. 2014, 2017). Forest disturbances can cause strong peaks in biomass availability and will increase logistics costs, with the capacity of nearby industries potentially not being able to digest sudden supply peaks. For the industry, a constant supply of uniform quality is desirable, whilst for forest owners, forest damage means lowered timber quality and prices. Future climate change impacts (including disturbances) need to be included in long-term forest planning (Senf and Seidl 2020), as well as in studies assessing biomass availability.

To anticipate the impacts of climate change, strategies are being explored to improve the resilience of forests in the context of climate change. A key strategy is to increase species diversity––especially by increasing the share of broadleaved species––in temperate and boreal forest stands to improve forest resilience (Jactel et al. 2017; Astrup et al. 2018). Increasing species diversity will eventually affect the type of biomass assortments that will be available to the industry from forests. Further research is needed on how changes in biomass availability and quality may affect forest industries.

Forest owners typically have multiple objectives when managing their forests, and their attitude to mobilising more wood is unclear. While harvest probability generally increases with higher productivity of the region and species, there are important differences in harvesting decisions relating to local conditions, such as site accessibility, the state of the forest resource (age), specific subsidies, and the importance of other forest services (Schelhaas et al. 2018). Forest owner behaviour, and heterogeneity therein, should be considered in future studies on biomass availability (Blennow et al. 2014; Rinaldi et al. 2015; Stjepan et al. 2015; Sotirov et al. 2019).

5.5 Key Messages

-

Existing studies indicate that a higher harvest level from EU forests could be sustained, but this will be associated with lower carbon storage in forest ecosystems, as well as impacts on other functions that forests have, including biodiversity.

-

There are large differences between the European regions regarding harvesting potential and actual utilisation rate.

-

The impacts of climate change on productivity are expected to vary across Europe. Climate change is expected to increase the frequency and intensity of forest disturbances, which can cause strong peaks in biomass availability and disrupt timber markets.

Box 5.1 Some Trends in the Global and the EU Forests

Antti Asikainen

Natural Resources Institute Finland, Joensuu, Finland

Forests cover 4,06 billion hectares (31%) of the world’s total land area (FAO 2020b). Since 1990 the world has lost 178 million ha of forest, but the rate of net forest loss has been decreasing in recent decades. In Europe, Oceania and Asia, the forest area has been increasing whereas in Africa and South America it has been decreasing (FAO 2020b). Global drivers effecting the entire land-use sector are behind the changes of forest area. Increasing global population and changes in the diet have created growing demand for food production and land for farming and crazing. Commercial agriculture is the most important driver of deforestation followed by local agriculture, urban expansion, infrastructure and mining (Hosonuma et al. 2012). Forest degradation, however, is driven by timber harvesting opening the forest areas for low intensity farming and grazing and subsequent human induced fires (Hosonuma et al. 2012).

In the EU, area of forest land has steadily increased since 1990’s (Eurostat 2020). Hosonuma et al. classify developing countries in four forest transition (FT) phases. Pre transition countries have high forest cover and low deforestation rate, deforestation is at its highest in early and late transition phases, whereas in post transition phase forest cover starts to increase due to reforestation. Although this classification was designed for developing countries, it fits well to industrialized countries, too. EU countries in the last 50–100 years can be classified to post transition phase, where large reforestation programmes resulted to increasing forest cover.

The conversion of forest into other uses, mainly to farmland, pastures and cities, roads and other human infrastructures has been the major factor behind the negative climate impacts in land use sector. Thus, a central element for climate smart forestry is that forests stays as forests. Landowners and governments seek economic returns for their assets including land. When forest-based livelihoods offer less income, other land uses e.g. agriculture, mining and urban expansion take land. There are also reverse processes going on. For instance, in Finland in 1969 to 2002s due to overproduction of agricultural goods low value farm slots have been reforested. In total 240,000 hectares were replanted with the governmental support. More recently (2007–2013), the EU’s rural development policy induced an increase of 1 to 2% of the forest area in some Member States/Regions such as ES – Asturias, ES - Castilla y León, ES – Galicia, HU, LT, UK – England, UK - Northern Ireland, and of 3% in UK – Scotland totaling c.a. 290,000 ha and even more is expected to be afforested by 2020 (Anon. 2017). Uruguay is an illustrative example of large-scale, market driven reforestation for the needs of rapidly growing pulp industry. Its forest area has increased 1990–2016 from 8000 km2 to almost 19,000 km2 (Anon. 2020).

Forest area as a proportion of total land area is a global indicator of the UN Sustainable Development Goals (SDGs). It is also included in the set of the EU SDG indicators used to monitor progress towards the SDGs in the EU context. It is important to recognize the effects of global trade into forest area. The EU has paid attention into its impacts on global land use induced by e.g. importing of soybean, wheat and other cereals and agricultural products (COM 2019).

Box 5.2 Huge Russian Forest Resources – A Reality or an Illusion?

Antti Mutanen and Sari Karvinen

Natural Resources Institute Finland, Joensuu, Finland

Based on a quick glance at the forest statistics, the forest resources of the Russian Federation (Russia) can be considered simply huge. According to the Food and Agriculture Organization’s (FAO) most recent Global Forest Resource Assessment, Russia’s forested area of 815 million ha is the largest of all the countries in the world, whilst the growing stock of 81.1 billion m3 is the second largest after Brazil (FAO 2020c). Forests available for wood supply (FAWS, as defined by the FAO) account for over 80% of the total forest area and growing stock.

The easily created image of immense taiga providing virtually endless forest resources is, however, somewhat deceiving. A more detailed investigation of the statistics has revealed that the growth rate of Russian forests is low. The estimated net annual increment is about 1.0 billion m3 in the total forest area and 850 million m3 in the FAWS area, which translates into an average net increment rate of merely 1.3 m3ha−1a−1 (Forest Europe 2020b; Roslesinforg 2021). For comparison, the average net increment rate (FAWS) is about 4.9 m3ha−1a−1 in Finland and 4.8 m3ha−1a−1 in Sweden (Forest Europe 2020b). The low growth rate of Russian forests is attributable to harsh climatic conditions (more than half of the forests are situated on permafrost soils), unfavourable age structures (about half of the coniferous forests are classed as mature and over-mature), as well as the prevailing forest management practices (extensive forestry based on large-scale clear-fellings and natural regeneration combined with a low level of tending seedling stands and intermediate fellings).

In addition to the growth rate, the utilisation rate of forests is also low in Russia. In the peak year of 2018, wood harvesting reached 240 million m3, and the ratio of fellings to growth (FAWS) was 28% (Forest Europe.

2020b; FAOSTAT 2021). For comparison, the corresponding ratio was 71% in Finland and 79% in Sweden. The low ratio of fellings to growth is obviously far from being a desirable state of affairs in Russia. The administratively set annual allowable cut (AAC, raschetnaya lesoseka) for the whole country is currently 730 million m3, or about 85% of the net annual increment (FAWS). The determination of the AAC is based on the characteristics of the forest, such as age and tree species composition. The AAC represents the level of wood harvesting that is sustainable, in terms of timber production and preserving the biodiversity and protective functions of the forests, which, according to the Russian forest-use classification system, belong to the exploitable and protective classes (Order of the Federal…). Moreover, the AAC can be considered the target level of wood harvesting in the state-owned forests, used, for example, as the basis for lease payments in leased forest areas (Forest Code…).

The current level of the AAC has been criticised by Russian experts as being an unrealistic overestimate of the wood production potential (Shvarts 2018; Strategiya razvitiya lesnogo…). The foremost reason for this is the inadequate infrastructure, especially the lack of a comprehensive forest road network and missing railway connections, which means that vast expanses of Russia’s forests are currently simply unreachable. In addition, the AAC does not take into account the natural conditions, such as slopes, forest quality or use restrictions, adequately. It has been estimated that, without a considerable investment in infrastructure, the realistic AAC for the whole of Russia is currently about 340 million m3 (Strategiya razvitiya lesnogo…).

In Fig. Box 5.1, the area covered by forests is contrasted with the forest area considered accessible for transport. The accessible forests are concentrated on the European part of Russia, where the infrastructure is relatively well developed and where the majority of the production capacity of the Russian forest industry is located. However, the most easily accessible forests, within a reasonable transportation distance to forest industry complexes, were felled decades ago, which, combined with poor forest management practices, has led to a deterioration in forest quality; that is, coniferous forests have been replaced by deciduous ones. Moreover, in some regions, a marked share of the coniferous forests is accessible only during winter due to the low bearing capacity of the forest soils, which, under warming climate conditions, makes wood procurement vulnerable (Goltsev and Lopatin 2013). Thus, in many regions in the European part of Russia, the forest industry is suffering from an inadequate supply of coniferous timber assortments, especially sawlogs, and simultaneously, there is practically no demand for deciduous pulpwood (State Council…2013). This situation has led to the overexploitation of the remaining coniferous forests, while natural losses have grown rapidly in the deciduous forests.

Forests and potentially productive forests accessible for transport. The area of forested land (680 million ha) is based on Landsat data and includes areas with forest cover (canopy cover) greater than 20% and potential regeneration areas, such as logging sites and burnt areas. The FAO’s definition of a forest sets the canopy cover threshold at 10%, hence the difference in forest area estimates (680 vs. 815 million ha). Potentially productive forests accessible for transport are forest areas (excluding nature-protection areas and intact forest landscapes) in which the long-term potential average increment is more than 1 m3ha−1 (based on the Moderate Resolution Imaging Spectroradiometer (MODIS) Net Primary Production product) and the forest transportation distance to an existing road network is less than 1 km (Lopatin 2017)

Various stakeholders in the Russian forest sector, including wood processors, logging companies, the Federal Forestry Agency (Rosleskhoz), regional forest management bodies, and environmental non-governmental organisations, consider intensive sustainable forest management (ISFM) to be a viable means for tackling the problems relating to the low productivity and deteriorating quality of the forests (Gosudarstvennaya programma Rossiyskoy…; Shmatkov 2013a, b; Intensivnoye lesnoye khozyaystvo…2015). The forest management practices under the ISFM are basically the same as those used in the Nordic countries––mainly artificial regeneration, active tending of seedling stands, first thinnings and other intermediate fellings, followed by the final felling. By applying ISFM, more wood could be produced per hectare and per year than currently, which would help to secure the wood supply for the forest industry, while simultaneously easing the pressure on opening intact forest areas to logging.

Russian experts have estimated that the ISFM could raise the harvesting volumes to 3–4 m3ha−1 in the Northern Taiga Zone and to 5–6 m3ha−1 in the Central and Southern Taiga Zones (Saint-Petersburg Forestry…2015). For comparison, the harvesting intensity was 4.0 m3ha−1 (FAWS) in Finland in 2019 (Finnish Forest Statistics 2020). Figure Box 5.2. demonstrates the hypothetical harvesting volumes for different harvesting intensities and for different forest areas under the ISFM. If the ISFM was applied in all the forests classed as exploitable, according to the Russian forest-use classification system, and assuming that 4 m3ha−1 could be harvested, the total harvested volume would be 2.4 billion m3 across the whole of Russia; that is, almost tenfold the current harvesting volumes or more than threefold the AAC. If the ISFM was applied to the forest area considered accessible with the existing infrastructure, the harvesting level would be 430 million m3, or roughly 60% of the AAC and 1.9 times higher than the current harvesting volumes. On the European part of Russia, applying the ISFM to the accessible forests would hypothetically lead to a harvesting volume of twice the current fellings and equal to the AAC. Thus, changing the forestry doctrine from extensive to intensive could greatly increase forest productivity in Russia, as well as the sustainable harvesting volumes. In several pilot areas, such as the Republics of Komi and Karelia, Arkhangelsk, Vologda, Irkutsk, Kirov and the Leningrad region, forestry norms already allow ISFM practices. However, there are no statistics on how large a scale the leaseholders have adopted, or are planning to adopt, the ISFM methods.

Realised wood harvesting, the 2019 AAC, harvesting potentials under the ISFM in exploitable forests and accessible forests in the whole of Russia and in the European part of Russia. Accessible forests are the same as in Fig. 5.1. (Sources: Saint-Petersburg Forestry…2015; Lopatin 2017; Finnish Forest Statistics 2020; Rosleskhoz 2020; Roslesinforg 2021; Yedinaya mezhvedomstvennaya 2021)

Many factors need to be considered when interpreting the harvesting potentials presented in Fig. 5.2. Although a forest area may be classed as accessible, there may not be any demand for the wood due to the tree species being wrong or the transportation distance to a processing plant being too long. In other words, besides the physical accessibility, economic accessibility is also needed. Moreover, a shift to the forest management practices of the ISFM requires investments in forest regeneration, the tending of seedling stands and a forest road network, a skilled workforce, and time. Taking the example of the road network, a ‘conditionally adequate’ road density for forestry is, on average, 5 m ha−1, according to a Russian assessment (State Council…2013). The current forest road density is about 3 m ha−1, thus the construction of 1 million km of new roads would be required to reach an adequate density in Russia’s exploitable forests. The costs would be EUR 13 billion, using the Finnish pricing level (Finnish Forest Statistics 2020). In practice, the costs would be more substantial, as road construction costs are higher in Russia (Petrunin 2013; Havimo et al. 2017). To achieve the forest road density in Finland (10 m ha−1; Uotila and Viitala 2000), more than 4 million km of new roads and EUR 57 billion would be required. For comparison, in 2019, forestry financing totalled EUR 1.1 billion, of which EUR 0.3 billion was invested by the forest leaseholders (Accounts Chamber…2020).

How to create incentives for forest leaseholders to invest in management activities with payback times that will, at best, be decades in the future, when there are also no guarantees that the lease period will be continued? Where to find enough workers to execute labour-intensive operations, such as tending seedling stands and thinnings, which are not that common in Russia? At present, using Finland as an example, the number of forestry workers in relation to the exploitable forest area is four times higher than in Russia, and even though there would be a willingness and the assets available to invest in forest management as well as the necessary workforce, materialisation of the full harvesting potential provided by the ISFM would take decades.

Russian forests are vast by area and volume, and for decades, the realised harvesting volumes have been far less than the AAC, the growth or the myriad different kinds of harvesting potential estimates. It would be tempting to interpret that there is a substantial – even astronomical – potential to increase the material use of forests in Russia. However, it is unrealistic to assume that the harvesting levels could be raised considerably in the short or medium terms. This fact has also been acknowledged in the Russian forest sector development strategy, whose most positive scenario for the harvesting level of 2030 is 286 million m3. In the long term, it would be quite possible to reinforce both the growth and harvesting volumes greatly. However, in order to realise this development path, several challenges have to be overcome. Infrastructure has to be developed, forest management rethought, the use of wood diversified, the operating environment stabilised, etc. Naturally, money is needed, but also politically sensitive issues, such as the private ownership of forests and the role of foreign investors, have to be discussed at a profound level.

The vast forest resources have always tempted non-Russian wood processors to source feedstock from Russia. However, the task has never been an easy one. During the last few decades, Russia has aimed at restricting roundwood exports, and the means to do this have included protective export duties, quotas and different regulations that complicate export procedures (Karvinen et al. 2019). In fact, after a years-long period of relatively stable trade conditions, roundwood sourcing from Russia to Europe will again become significantly more difficult in the very near future. A plan to ban exports of softwood and valuable hardwood from Russia was announced at the end of 2020 (Presidential instructions…2020). As a consequence, tariff quotas for softwood (spruce and pine) are to be removed from 2022 onwards (Government Decree…396). Under the valid regulation on customs duties, this will lead to prohibitive duties – for softwood, a minimum of €55 m −3 (Government Decree…754). A new development that has been raised is the possibility of restricting the export of softwood chips. It has been suggested that softwood chips be added to the products crucial for the internal Russian market on which temporary export restrictions or an export ban can be imposed (Draft of Government Decree…). The message is quite clear – harvested roundwood should be processed in Russia to create value added.

References

Alberdi I, Michalak R, Fischer C, Gasparini P, Brändli U-B, Tomter SM et al (2016) Towards harmonized assessment of European forest availability for wood supply in Europe. For Policy Econ 70:20–29

Alberdi I, Bender S, Riedel T, Avitable V, Boriaud O, Bosela M et al (2020) Assessing forest availability for wood supply in Europe. For Policy Econ 111:102032. https://doi.org/10.1016/j.forpol.2019.102032

Anttila P, Nivala V, Salminen O, Hurskainen M, Kärki J, Lindroos TJ, Asikainen A (2018) Regional balance of forest chip supply and demand in Finland in 2030. Silva Fenn 52(2):10.14214/sf.9902

Astrup R, Bernier PY, Genet H, Lutz DA, Bright RM (2018) A sensible climate solution for the boreal forest. Nat Clim Chang 8:11–12

Barreiro S, Schelhaas M-J, McRoberts RE, Kändler G (eds) (2017) Forest inventory-based projection systems for wood and biomass availability. Springer, Cham

Blennow K, Persson E, Lindner M, Faias SP, Hanewinkel M (2014) Forest owner motivations and attitudes towards supplying biomass for energy in Europe. Biomass Bioenergy 67:223–230

Brosowski A, Thrän D, Mantau U, Mahro B, Erdmann G, Adler P et al (2016) A review of biomass potential and current utilisation – status quo for 93 biogenic wastes and residues in Germany. Biomass Bioenergy 95:257–272

Camia A, Robert N, Jonsson R, Pilli R, García-Condado S, López-Lozano R, … Giuntoli J (2018) Biomass production, supply, uses and flows in the European Union: First results from an integrated assessment, EUR 28993 EN. Publications Office of the European Union, Luxembourg. 10.2760/539520

Cazzaniga NE, Jonsson R, Palermo D, Camia A (2019a) Sankey diagrams of woody biomass flows in the EU-28. EC Joint Research Centre, Publications Office of the European Union, Luxembourg. https://doi.org/10.2760/227292

Cazzaniga NE, Jonsson R, Pilli R, Camia A (2019b) Wood resource balances of EU-28 and member states. EC Joint Research Centre, Publications Office of the European Union, Luxembourg https://doi.org/10.2760/020267

de Vries W, Solberg S, Dobbertin M, Sterba H, Laubhann D, van Oijen M et al (2009) The impact of nitrogen deposition on carbon sequestration by European forests and heathlands. For Ecol Manag 258:1814–1823

Dees M, Elbersen B, Fitzgerald J, Vis M, Anttila P, Forsell N, … Höhl M (2017) Atlas with regional cost supply biomass potentials for EU 28, Western Balkan countries, Moldavia, Turkey and Ukraine. https://www.s2biom.eu/images/Publications/D1.8_S2Biom_Atlas_of_regional_cost_supply_biomass_potential_Final.pdf. Accessed 21 May 2021

Di Fulvio F, Forsell N, Lindroos O, Korosuo A, Gusti M (2016) Spatially explicit assessment of roundwood and logging residues availability and costs for the EU28. Scand J Forest Res 31:691–707

Energimyndigheten (2020) Production of unprocessed forest fuels by fuel type and feedstock origin. https://pxexternal.energimyndigheten.se/pxweb/en/?rxid=2c91707b-7c5e-405bb132-3aac75a4a172. Accessed 10 June 2020

Etzold S, Ferretti M, Reinds GJ, Solberg S, Gessler A, Waldner P et al (2020) Nitrogen deposition is the most important environmental driver of growth of pure, even-aged and managed European forests. For Ecol Manag. https://doi.org/10.1016/j.foreco.2019.117762

EU (2018) Regulation (EU) 2018/841 of the European Parliament and of the Council of 30 May 2018 on the inclusion of greenhouse gas emissions and removals from land use, land-use change and forestry in the 2030 climate and energy framework, and amending Regulation (EU) No 525/2013 and Decision No 529/2013/EU. https://eur-lex.europa.eu/eli/reg/2018/841. Accessed 21 May 2021

European Commission (2020) EU biodiversity strategy for 2030. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0380

FAO (2020) FAOSTAT. Forestry production and trade. http://www.fao.org/faostat/en/#data/FO. Accessed 8 June 2020

FAO, ITTO and United Nations (2020) Forest product conversion factors. Rome. https://doi.org/10.4060/ca7952en

Flechard CR, Ibrom A, Skiba UM, de Vries W, van Oijen M, Cameron DR et al (2020) Carbon–nitrogen interactions in European forests and semi-natural vegetation – part 1: fluxes and budgets of carbon, nitrogen and greenhouse gases from ecosystem monitoring and modelling. Biogeosciences 17:1583–1620

Forest Europe (2020a) State of Europe’s Forests 2020. https://foresteurope.org/state-europes-forests-2020. Accessed 21 Dec 2020

Forzieri G, Pecchi M, Girardello M, Mauri A, Klaus M, Nikolov C et al (2020) A spatially explicit database of wind disturbances in European forests over the period 2000–2018. Earth Syst Sci Data 12:257–276

Gardiner B, Blennow K, Carnus J-M, Fleischer P, Ingemarson F, Landmann G, … Usbeck T (2010) Destructive storms in European forests: Past and forthcoming impacts. Final report to the European Commission. DG Environment. http://ec.europa.eu/environment/forests/pdf/STORMS%20Final_Report.pdf. Accessed 24 May 2021

Gold S, Korotkov A, Sasse V (2006) The development of European forest resources, 1950 to 2000. For Policy Econ 8:183–192

Gschwantner T, Alberdi I, Balázs A, Bauwens S, Bender S, Borota D et al (2019) Harmonisation of stem volume estimates in European National Forest Inventories. Ann For Sci. https://doi.org/10.1007/s13595-019-0800-8

Jactel H, Bauhus J, Boberg J, Bonal D, Castagneyrol B, Gardiner B et al (2017) Tree diversity drives Forest stand resistance to natural disturbances. Curr For Rep 3:223–243

Jochem D, Weimar H, Bösch M, Mantau U, Dieter M (2015) Estimation of wood removals and fellings in Germany: a calculation approach based on the amount of used roundwood. Eur J For Res 134:869–888

Jonsson R, Blujdea V, Fiorese G, Pilli R, Rinaldi F, Baranzelli C, Camia A (2018) Outlook of the European forest- based sector: Forest growth, harvest demand, wood-product markets, and forest carbon dynamics implications. iForest 11:315–328

Kärkkäinen L, Haakana H, Hirvelä H, Lempinen R, Packalen T (2020) Assessing the impacts of land-use zoning decisions on the supply of Forest ecosystem services. Forests. https://doi.org/10.3390/f11090931

Leskinen P, Lindner M, Verkerk PJ, Nabuurs GJ, Van Brusselen J, Kulikova E, Hassegawa M, Lerink B (eds) (2020) Russian forests and climate change. What science can tell us 11. European Forest Institute. https://doi.org/10.36333/wsctu11

Lindner M, Dees M, Anttila P, Verkerk P, Fitzgerald J, Datta P, Glavonjic B, Prinz R, Zudin S (2017) Assessing Lignocellulosic Biomass Potentials From Forests and Industry. In: Panotsou C (Ed.), Modeling and Optimization of Biomass Supply Chains: Top-Down and Bottom-up Assessment for Agricultural (pp. 127–167). Forest and Waste Feedstock. Academic Press

Moreno A, Neumann M, Hasenauer H (2017) Forest structures across Europe. Geosci Data J 4:17–28

Nabuurs GJ, Verweij P, van Eupen M, Pérez-Soba M, Pülzi H, Hendriks K (2019) Next-generation information to support a sustainable course for European forests. Nat Sustain 2:815–818

Natural Resources Institute Finland (2020) Solid wood fuel consumption in heating and power plants by region. Statistical database. http://statdb.luke.fi/PXWeb/pxweb/en/LUKE/LUKE04%20Metsa04%20Talous10%20Puun%20energiakaytto/01a_Laitos_ekaytto_maak.px/?rxid=9a0b5502-10d0-4f84-8ac5-aef44ea17fda Accessed 10 June 2020

Pretzsch H, Biber P, Schütze G, Uhl E, Rötzer T (2014) Forest stand growth dynamics in Central Europe have accelerated since 1870. Nat Commun. https://doi.org/10.1038/ncomms5967

Reyer C, Bathgate S, Blennow K, Borges JG, Bugmann H, Delzon S et al (2017) Are forest disturbances amplifying or canceling out climate change-induced productivity changes in European forests? Environ Res Lett. https://doi.org/10.1088/1748-9326/aa5ef1

Rinaldi F, Jonsson R, Sallnäs O, Trubins R (2015) Behavioral modelling in a decision support system. Forests 6:311–327

Salmivaara A, Launiainen S, Perttunen J, Nevalainen P, Pohjankukka J, Ala-Ilomáki J et al (2020) Towards dynamic forest trafficability prediction using open spatial data, hydrological modelling and sensor technology. Forestry 93:662–674

Schelhaas MJ, Fridman J, Hengeveld GM, Henttonen HM, Lehtonen A, Kies U et al (2018) Actual European forest management by region, tree species and owner based on 714,000 re-measured trees in national forest inventories. PLoS One. https://doi.org/10.1371/journal.pone.0207151

Seidl R, Schelhaas MJ, Rammer W, Verkerk PJ (2014) Increasing forest disturbances in Europe and their impact on carbon storage. Nat Clim Chang 4:806–810

Seidl R, Thom D, Kautz M, Martin-Benito D, Peltoniemi M, Vacchiano G et al (2017) Forest disturbances under climate change. Nat Clim Chang 7:395–402

Senf C, Seidl R (2020) Mapping the forest disturbance regimes of Europe. Nat Sustain. https://doi.org/10.1038/s41893-020-00609-y

Sotirov M, Sallnäs O, Eriksson LO (2019) Forest owner behavioral models, policy changes, and forest management. An agent-based framework for studying the provision of forest ecosystem goods and services at the landscape level. For Policy Econ 103:79–89

Stjepan P, Mersudin A, Dženan B, Petrovic N, Stojanovska M, Marceta D, Malovrh SP (2015) Private forest owners’ willingness to supply woody biomass in selected south-eastern European countries. Biomass Bioenergy 81:144–153

Verkerk PJ, Anttila P, Eggers J, Lindner M, Asikainen A (2011) The realisable potential supply of woody biomass from forests in the European Union. For Ecol Manag 261:2007–2015

Verkerk PJ, Fitzgerald JB, Datta P, Dees M, Hengeveld GM, Lindner M, Zudin S (2019) Spatial distribution of the potential forest biomass availability in Europe. For Ecosyst. https://doi.org/10.1186/s40663-019-0163-5

Vidal C, Alberdi IA, Hernández Mateo L, Redmond JJ (2016) National Forest Inventories: assessment of wood availability and use. Springer, Cham

Vilén T, Cienciala E, Schelhaas MJ, Verkerk H, Lindner M, Peltola H (2016) Increasing carbon sinks in European forests: effects of afforestation and changes in mean growing stock volume. Forestry 89:82–90

Reference from Box 5.1

Anon (2017) Evaluation study of the forestry measures under rural development technical report. September 2017 https://doi.org/10.2762/06029. 176 p

Anon (2020) World data atlas. https://knoema.com/atlas/Uruguay/topics/Land-Use/Area/Forest-area

FAO (2020b) Global forest resource assessment 2020. Key findings. 14 .COM 2019. Stepping up EU Action to Protect and Restore the World’s Forests. COM 2019 352 final. 21 p

Hosonuma N, Herold M, De Sy V, De Fries RS, Brockman M, Verchot L, Angelsen A, Romijn E (2012) An assessment of deforestation and forest degradation drivers in developing countries. Environ Res Lett 7(2012):12. https://doi.org/10.1088/1748-9326/7/4/044009

Reference from Box 5.2

Accounts Chamber of the Russian Federation (2020). Otchet o rezul’tatakh sovmestnogo ekpertno- analiticheskogo meropriyatiya “Analiz effektivnosti ispol’zovaniya lesnykh resursov Rossiyskoy Federatsii v 2016–2018 godakh” [Report on the results of a common expert-analytical measure “The analysis of efficiency of using forest resources in the Russian Federation in 2016–2018”]

FAO (2020c) Global Forest Resources Assessment 2020: Main report. Rome. https://doi.org/10.4060/ca9825en

FAOSTAT (2021) Forest product statistics. Forestry production and trade. http://www.fao.org/faostat/en/#data/FO. Accessed 17 May 2021

Finnish Forest Statistics (2020) Natural Resources Institute Finland

Forest code of the Russian Federation 04.12.2006 N 200-FZ

Forest Europe (2020b) State of Europe’s Forests 2020. Ministerial Conference on the Protection of Forests in Europe

Goltsev V, Lopatin E (2013) The impact of climate change on the technical accessibility of forests in the Tikhvin District of the Leningrad region of Russia. Int J For Eng 24(2):148–160. https://doi.org/10.1080/19132220.2013.792150

Gosudarstvennaya programma Rossiyskoy Federatsii “Razvitiye lesnogo khozyaystva” na 2013–2020 gody [State programme of the Russian Federation “Development of forestry” 2013–2020] Government Decree of the Russian Federation 18.03.2021 No. 396

Government Decree of the Russian Federation 30.8.2013 No. 754 (including changes upto 18.3.2021)

Havimo M, Mönkönen P, Lopatin E, Dahlin B (2017) Optimising forest road planning to maximise the mobilisation of wood biomass resources in Northwest Russia. Biofuels 8(4):501–514. https://doi.org/10.1080/17597269.2017.1302664

Presidential instructions following the meeting on the development and decriminalization of the forest sector. 6.11.2020. http://www.kremlin.ru/acts/assignments/orders/64379. Accessed 17 May 2021

Draft of Government Decree “Changing the list of products especially important for the internal market of the Russian Federation…”. https://regulation.gov.ru/p/112935. Accessed 17 May 2021

Intensivnoye lesnoye khozyaystvo: Obyazannost ili osoznannaya neobkhodimost? [Intensive forestry: Responsibility or the recognition of necessity?] 2015. Ustoychivoye lesopol’zovaniye 1(41):34–41. https://wwf.ru/upload/iblock/b01/07-_5_.pdf. Accessed 17 May 2021

Karvinen S, Mutanen A, Petrov V (2019) Effects of the export restrictions on birch log market in Northwest Russia. Balt For 25(1):105–112. https://doi.org/10.46490/vol25iss1pp105

Lopatin E (2017) Ranzhirovaniye uchastkov lesov Rossii po vozmozhnosti vnedreniya metodov intensivnogo ustoichivogo lesnogo khozyaystva [Ranking of Russian forest areas possible for intensive sustainable forest management]. Ustoichivoye lesopol’zovaniye No. 4(52):2–7. https://wwf.ru/upload/iblock/b3f/01.pdf. Accessed 17 May 2021

Order of the Federal Forestry Agency 27.5.2011 N 191

Petrunin N (2013) Lesnoye bezdorozh’e (Roadless forest). “Derewo.ru” 5:30–33

Roslesinforg (2021) Lesa Rossii [Russian forests]. https://roslesinforg.ru/atlas. Accessed 17 May 2021

Rosleskhoz (2020) Svedeniya o zemlyakh lesnogo fonda [Information on the forest fund land]. http://rosleshoz.gov.ru/opendata/7705598840-ForestFund. Accessed 15 April 2020

Saint-Petersburg Forestry Research Institute (2015) Kontseptsiya intensivnogo ispol’zovaniya i vosproizvodstva lesov [The concept of intensive use and regeneration of forests]. Saint Petersburg Forestry Research Institute. FBU “SPBNIILH”, St. Petersburg

Shmatkov N (ed) (2013a) Intensivnoye ustoichivoye lesnoye khozyaystvo: Bar’ery i perspektivy razvitiya [Intensive sustainable forestry: Barriers and development perspectives]. WWF Russia, Moscow

Shmatkov N (ed) (2013b). Strategiya razrabotki sistemy lesokhozyaystvennykh i prirodookhrannykh normativov dlya Sredne-tayezhnogo lesnogo rayona s tselyu vnedreniya modeli ustoichivogo intensivnogo lesnogo khozyaystva [Strategy for compiling the forestry and nature protection norms for the central taiga forest zone with the aim of implementing sustainable and intensive forestry]. Materials of the round table 18 March 2013, St. Petersburg. WWF, Moscow

Shvarts E, Shmatkov H, Kobyakov K, Rodionov A, Yaroshenko A (2018) Nekotorye prichiny krizisa lesnogo sektora i puti vykhoda iz nego [Some reasons for the crisis in the forest sector and ways out]. Ustoichivoye lesopol’zovaniye No. 3(55):4–16. https://wwf.ru/upload/iblock/e0b/02.pdf. Accessed 15 Apr 2020

State Council of the Russian Federation (2013). Doklad o povyshenii effektivnosti lesnogo kompleksa [Report on increasing efficiency of the forest sector]. State Council of the Russian Federation

Strategiya razvitiya lesnogo kompleksa Rossiyskoy Rossiyskoy Federatsii na period do 2030 goda [Forest sector development strategy of the Russian Federation until 2030]. Confirmed by Government Decree 11.2.2021 No. 312

Uotila E, Viitala E-J (2000) Tietiheys metsätalouden maalla. Metsätieteen aikakauskirja 1/2000: 19–33 (in Finnish). https://metsatieteenaikakauskirja.fi/pdf/article6910.pdf. Accessed 15 April 2020

Transliteration: BGN/PCGN romanisation of Russian

Yedinaya mezhvedomstvennaya informatsionno-statisticheskaya Sistema (2021) [The Unified Interdepartmental Statistical Information System]. https://fedstat.ru. Accessed 17 May 2021

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2022 The Author(s)

About this chapter

Cite this chapter

Anttila, P., Verkerk, H. (2022). Forest Biomass Availability. In: Hetemäki, L., Kangas, J., Peltola, H. (eds) Forest Bioeconomy and Climate Change . Managing Forest Ecosystems, vol 42. Springer, Cham. https://doi.org/10.1007/978-3-030-99206-4_5

Download citation

DOI: https://doi.org/10.1007/978-3-030-99206-4_5

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-99205-7

Online ISBN: 978-3-030-99206-4

eBook Packages: Biomedical and Life SciencesBiomedical and Life Sciences (R0)