Abstract

Most governments around the world have put in place policies to support the deployment of wind and solar technologies, as they are going to play a key role in the decarbonisation of energy systems and to achieve United Nations’ Sustainable Development Goals. At low levels of deployment, these technologies typically do not raise significant issues, but to reach high shares of power generation, integration measures will be needed. These include enabling the maximum use of flexibility from existing and new plants, changing the way transmission and distribution grids are operated and expanded, increasing the deployment and availability of storage and demand-side mechanisms. Adequate policies are needed to enable the deployment of these measures while minimising the overall power systems costs, ultimately ensuring their affordability.

The author wishes to thank Manuel Baritaud, Marco Cometto, Karolina Daszkiewicz, David Wilkinson and Matthew Wittenstein for their comments, views and support. The views and opinions expressed are solely the views of the author and do not represent a statement of the views of any other person or entity.

Lecturer at Institut d’études politiques de Paris (SciencesPo), energy consultant in Baroni Energy Consulting and former Head of Power Sector Analysis in the World Energy Outlook team of the International Energy Agency.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

- Integration

- Power systems

- Solar PV

- Wind

- Flexibility

- Energy storage

- Transmission and distribution grids

- Electricity

- Economics

- LCOE

1 Introduction

The energy world is undergoing a profound transformation, driven by a combination of technological, economic and environmental factors, with changing costs and ways for producing energy, and new and more efficient means to consume it. This transformation is often referred to as the “clean energy transition”. The power sector is the largest CO2 emitting energy sector and is therefore central to any decarbonisation strategy. It also plays a pivotal role in reducing the carbon footprint of final uses by increasing their electrification.

The last two decades have seen a spectacular growth of wind (initially onshore and, more recently, also offshore) and solar (mostly photovoltaics) technologies, pushed by policies put in place by governments around the world to support their deployment. The continued deployment led to a strong decrease of investment costs of these technologies, which triggered more ambitious goals and more countries to support them. This created a virtuous snow-ball effect between policy support, increased targets, development and cost reductions.

In the last 20 years, global electricity generation of wind and solar PV combined increased more than 110-fold in absolute terms, increasing from a mere 0.1% of global electricity generation in 1998 to 7% in 2018 (IEA Statistics 2020), and reaching much higher levels in some countries. This level of deployment is set to increase in all countries and in all scenarios developed by all major institutions—with an ever-growing role in decarbonisation scenarios coherent with the goals agreed during UNFCCC’s Conference of Parties 21 (COP 21) held in Paris.

Despite the encouraging recent trends, the continued expansion of these technologies cannot be taken for granted, and it is the duty of all actors involved—policymakers, industry, financial institutions, academia—to anticipate the challenges ahead and to provide early solutions. The aim of this chapter is not to provide optimal deployment levels of wind and solar technologies in the power mix, but rather to provide a guide of the characteristics of these technologies and of the major challenges faced by the power sector in reaching such high level of deployment.

2 Characteristics of Non-dispatchable Renewable Energy Sources

Non-dispatchable generation refers to the electricity generation from technologies that cannot (or have limited ability to) adjust their power output to match electricity demand, as their source is weather-dependent. Downward adjustments are still possible by curtailing generation, as well as upward ramping is possible if pre-curtailment had previously been envisaged. But no generation is possible if the resource is unavailable.

The availability of renewable energy sources varies widely across the globe and the technologies exploiting them have different history and levels of maturity. Hydropower was the first renewable source to be used, with its early steps dating back to the late nineteenth century. By 2018, there were almost 1300 GW of hydropower installed capacity globally (IRENA 2019a), generating over 60% of total renewable power production.

As electricity systems developed, it increasingly became clear that flexibility (i.e. being readily dispatchable) was a fundamental characteristic for matching electricity demand and supply. With hydropower exhibiting this characteristic in addition to being a relatively cheap source, reservoirs and pumped storage plants were developed and deployed worldwide. Other important dispatchable renewable technologies include geothermal and bioenergy.

Over the last two decades, two newer renewable technologies with different characteristics than conventional technologies, and in particular with a limited flexibility, have made sizable inroads into the electricity mix: wind and solar photovoltaics (PV ). These are the focus of this chapter. There are several other non-dispatchable renewables-based technologies (such as marine energy), which also may play a role in the future power mix but for now are still in relatively early stages of development.

2.1 Technologies and Their Characteristics

Several renewables-based technologies can be classified as non-dispatchable. These include wind onshore, wind offshore, solar PV, concentrating solar power (CSP) without storage, hydropower run-of-riverFootnote 1 (RoR), and marine (tide and wave) energy (Table 16.1). The main common characteristic is that their electricity generation changes with the variations of the related natural source (wind, sun, rainfall patterns, moon attraction) and cannot be increased or decreased at will to match the variations in electricity demand. The costs, level of maturity and global diffusion varies significantly for each of these technologies.

Wind, solar PV and hydropower RoR have reached the highest level of maturity and deployment among non-dispatchable renewables, while solar concentrating solar panel (CSP) and marine energy can still be considered at their infancy stage, with low deployment rates and high electricity generation costs. Furthermore, the future deployment of solar CSP is expected to be associated with thermal storage, therefore bringing this technology out of the non-dispatchable renewable group.

Hydropower potential is still very large globally, with the strongest deployment in future years likely to come from developing countries and regions such as China, Latin America, India, Southeast Asia and Africa. In advanced economies, the hydropower remaining potential, as well as environmental and social issues, limit greatly the possible further exploitation of medium and large hydro sites (i.e. sites that support capacities greater than 10 MWFootnote 2), but further deployment of small, mini or micro run-of-river systems may be expected. Solar and wind potentials are vast (see related chapters), but nonetheless with strong variations from region to region. A differentiation between technical and realisable potential needs to be introduced to fully understand the feasibility of tapping into these vast potentials.

An important element to take into consideration is the quality of each resource. The solar irradiance,Footnote 3 the speed and variation of wind or the seasonality of water inflows are often translated in power station terms through capacity factors. This measures the ratio (expressed in percentage terms) between the electricity generated by the power station and the maximum theoretical outputFootnote 4 that could be produced over a given period (typically one year).

Capacity factors of non-dispatchable renewables can differ significantly across regions and technologies. Typically, the capacity factors of offshore wind farms can reach the highest levels, in the range of 35% to 65%, with some of the highest levels being reached in the North and Baltic seas in Europe (IEA 2019a) (Fig. 16.1). Onshore wind and hydropower RoR can also reach very high levels in the best sites (up to around 60% and 80% respectively), for example in Brazil, while the other non-dispatchable technologies usually are limited to a 10–25% range. Solar PV often oscillates in the lower side of the non-dispatchable technologies range, mainly due to the inability to generate during night. Due to the nature of solar irradiance, solar capacity factors are highest towards the equator and lowest towards the poles.

Average simulated capacity factors for offshore wind worldwide. (Source: IEA 2019a)

Over the last two decades, solar PV and onshore wind technologies have seen impressive capacity growth—each adding over 500 GW globally. Economies of scale led to a sharp decrease in costs for both technologies. The decrease of onshore wind costs was due to two main factors: the improvements in manufacturing and installation costs on one side and the increase of average capacity factors on the other. These two factors brought the weighted-average global levelised cost of electricity (LCOE)Footnote 5 to drop by 35% in less than 10 years (IRENA 2019b). Similar factors to onshore wind formed the basis of the cost decrease for offshore wind, but this was also coupled with improved operating and maintenance costs. The increase in size of wind turbines played a key role in increasing capacity factors, with larger generators, and longer blades (resulting in larger swept areas and increased power output) leading to lower costs per kilowatt.

Generation cost decreases have been the sharpest and most successful than any other technology for solar PV systems, driven by PV module cost reductions, together with falling costs for the entire balance of system costs (BoS), that were in turn led by inverter cost reductions. The observed prices for solar PV systems and the actual costs of its components can differ significantly depending on eventual subsidies provided by some governments to manufacturers. All these elements have led solar PV module prices to follow a 20–22% experience curve (i.e. the price reduction for each doubling of capacity) (Fig. 16.2), with a decrease of over 90% in less than a decade.

Decreasing investment prices for solar photovoltaics modules. (Source: Paula Mints 2019)

2.2 Key Properties

The electricity generation of non-dispatchable renewables (sometimes called intermittent or variable renewables in other publications) cannot be adjusted with respect to the variations of electricity demand unless curtailment takes place (if the generation is in excess) or if prior curtailment has been foreseen (to be able to ramp up). In any case, no generation is possible when the resource is not available (e.g. during night for solar PV or when wind does not blow).

The hourly (or sub-hourly) electricity-generation profile of the non-dispatchable renewables technologies and the way that they match (or not) the hourly electricity demand is critical with larger shares of deployment. An illustrative profile of onshore wind and solar PV is shown in Fig. 16.3. The variability of generation from different projects may be smoothed if the geographical area is sufficiently large, provided that enough grid transmission capacity is available in the considered area. Conversely, the situation may be compounded if the generation profiles of the different projects are similar, with peaks and valleys appearing during the same hours. However, the combination of different non-dispatchable technologies may offset and somewhat complement each other to reduce the overall variability of the total, for example in places where onshore wind generation is stronger in winter, but quite low in calm summer days with generation from solar PV that is generally stronger in summer months and can be much lower in winter ones.

Illustrative generation profile of onshore wind and solar PV for a given month. (Source: Synthetic data, not based on specific systems)

The challenge of integrating these sources in power systems has been summarised in the International Energy Agency’s World Energy Outlook 2016 (IEA 2016a) through three key properties:

-

1.

Scarcity. This situation happens when the generation from non-dispatchable renewable resources is insufficient to meet electricity demand at its highest levels, requiring other types of installed capacity or solutions to meet demand. This issue is strictly linked to the system adequacy issue discussed in the next section.

-

2.

Variability. The rapid change of electricity generation from non-dispatchable sources requires the ramping up or down (or the start and stop) of generation from dispatchable sources in the given time. The time required by these generators to react, in particular for ramping up generation, is dependent on the type of technology and on whether the plant needs to start or was already generating. Forecasting methodologies to accurately estimate the future wind and solar PV generation can therefore play a very important role.

-

3.

Abundance. At high levels of penetrations of wind and solar PV in power systems, periods of excess generation can occur, in particular in periods of low demand. This issue is linked to curtailment, with important implication on system stability and electricity pricing (see Sect. 3.4).

3 The Changing Structure of Power Systems

The introduction of growing shares of non-dispatchable generation sources is set to change the way power system are structured and operated. Following the properties discussed in the previous section, several changes to power systems must be considered: the type and amount of the capacity installed, the way that electricity demand is going to be satisfied, the impact on the electricity dispatching mechanism and its consequences on power prices.

3.1 Impact on System Adequacy

Power systems can be schematically characterised by three elements: The generation facilities, the demand centres and the grids that allow to transport the energy from the first to the second. Electricity demand fluctuates every moment (for the sake of simplicity, we will approximate it to “every hour”) and its profile over time changes depending on the use (e.g. industrial use, lighting or cooking have very different hourly patterns). Typically, demand at night is lower than during the day, summer demand is higher where air conditioning systems dominate, while winter demand is higher where electric space heating in cold temperature regions is strong.

Throughout the history of deployment of power systems, reliability and security of supply have been a central concern. The ability of meeting demand at its highest levels (peak demand) has been a fundamental characteristic of power system and markets. The system adequacy of a power system measures if enough generation and transmission capacity is present in the system in order to meet demand at all times (ENTSO-E 2015).

To be able to meet peak demand, enough capacity needs to be present in the system, once all unavailable capacity has been excluded and a security margin has been accounted for. A loss of load expectation (LOLE)Footnote 6 indicator can be calculated to measure the adequacy of the system. This margin is often called reserve margin or capacity margin. The unavailable capacity takes into account unexpected outages, services reserve, maintenance and non-usable capacity. The last component is particularly linked to the deployment of wind and solar PV technologies and is linked to their capacity credit, which indicates the portion of wind and solar PV capacity that can be reliably expected to generate electricity during times of peak demand in the network to which it is connected.

Indicative availability of capacity at peak demand for selected technologies as a share of installed capacity is shown in Fig. 16.4, where an average rate of unexpected outages has been considered for dispatchable fossil fuel and nuclear plants, and an indicative capacity credit for wind and solar PV technologies. It should be noted that generally the capacity credit of non-dispatchable technologies depends on several factors, and primarily on the resource, the generation profile and the match or mismatch with the demand profile.Footnote 7

Indicative availability of capacity at peak demand by selected technology. (Source: author’s elaboration)

The contribution (capacity credit) of non-dispatchable technologies to system adequacy tends to become progressively lower as their share of total generation increases, while the capacity credit can increase when different areas with different profiles are better interconnected. An important implication of the low capacity credit of wind and solar PV technologies is that with increasing installed capacity of these technologies, the total installed capacity in a system increases significantly, as other types of capacity are needed for the system adequacy. For example, if in a system with 100 GW of dispatchable plants we add an equal amount of onshore wind and of solar PV (100 GW each, with a capacity credit of 10%), the total capacity in the system will be roughly around 280 GW, after retiring 20 GW of the existing dispatchable plants.

The consequences of this increase of capacity in the system on electricity generation and electricity pricing are explored in the following sections.

3.2 Impact on the Mix, Type and Operations of Plants in the System

The fluctuations of electricity demand require different power plants types to operate in varied ways. Load duration curvesFootnote 8 (LDC) have long been used to represent in a simple way electricity demand and the type of power plants needed in a system by their utilisation rate or capacity factor. A classical way to classify them is by decreasing utilisation rate into baseload (with a typical capacity factor of 75–90%), mid-load (with a typical capacity factor of 40–60%) and peak-load plants (with a typical capacity factor of 0–15%). Linked to load duration curves, screening curves represent fixed and variable costs of thermal power plants over all the 8760 hours of generation in a given year, allowing to identify the cost-optimal thermal generation mix given a set of investment, operating and maintenance (O&M) and fuel cost data. The utilisation of these curves, while allowing to simplify the representation of hourly electricity demand, loses the temporal continuity of each hour, limiting its use to evaluate flexibility needs, such as ramping of power plants or charging and discharging of storage devices.

The deployment of non-dispatchable energy technologies requires the introduction of an intermediate step in order to keep using these two useful approaches (the load duration curve and the screening curve). Residual load duration curves (RLDC) are obtained by subtracting the hourly generation of non-dispatchable technologies from the hourly electricity demand, and then applying the same re-ordering from highest to lowest level as for the LDCs. An example is shown in Fig. 16.5 for different levels of solar PV capacity penetration into a fictitious power system.

Example of residual load duration curve. (a) Hourly electricity demand, electricity generation from solar PV (60 GW) and residual load demand in January. (b) Load duration curve, and residual load duration curve with deployment of 30, 60 and 100 GW of solar PV. (Source: author’s elaboration)

Residual load duration curves are often very close to load duration curve at peak levels, while they become steeper along the curve, the more wind and solar technologies are added into the system. This change of the steepness of the RLDC has the effect to increase the need for peak- and mid-load plants, and to reduce the need for baseload ones.Footnote 9 Negative values of the RLDC indicate excess generation that, in absence of integration measures, would be curtailed.

The low capacity credit of wind and solar PV plants (as seen in Sect. 3.1) brings a second important implication for the dispatchable power plants. As capacity in the system is higher and generation from wind and solar PV gets dispatched first in the merit order due to their near-zero variable cost, the utilisation factor of dispatchable plants is decreased.

A third effect—that, as mentioned, cannot be captured by the RLDC—is linked to the variability of the generation of wind and solar technologies and how it relates to electricity demand from hour to hour. As can be seen in the example of California ((Source: CAISO Fig. 16.6), where peak demand occurs in the evening, a growing share of solar PV in the mix keeps reducing the residual electricity demand around midday. This leads to a strong call on dispatchable generators in the late hours of the afternoon (from around 17:00 to around 20:00), requiring ramping of dispatchable plants two-to-three times higher than in the case without solar PV. Consequently, there is a growing call for greater flexibility of dispatchable generators. The increase of ramping services (up and down) of dispatchable generators can increase the costs linked to standby and lead to faster wear and tear of the plants, eventually decreasing their efficiency and lifetime, unless adequate retrofit for such operations is foreseen.

Residual hourly demand in a typical spring day in California. (Source: CAISO 2019)

3.3 The Rise of Distributed Generation

Wind and solar PV projects can have very different sizes, ranging from few kilowatts to several hundreds of megawatts (currently up to 1200 MW for offshore wind and solar PV projects and several thousands of megawatts for onshore wind farms). For this reason, they can be broadly separated into utilities-scale and buildings-scale, with the latter often divided between commercial and residential scales. While the utility-scale projects tend to have similar size to conventional plants (that can range from 50–400 MW for gas plants up to 500–1600 MW for coal or nuclear plants and to more than 10,000 MW for the largest hydropower plants) in terms of location and connection to the grids, the building-scale ones are much more numerous, more distributed over geographical areas and generally connected to lower-voltage grids.

Power systems saw a major change over the last few decades as markets moved from monopolies to liberalised markets, increasing the number of generators and generally of actors on the market. While the new wind and solar PV utility-scale projects fit more into this path, the deployment of commercial and residential scale plants are increasing substantially the number of power producers from few dozens to thousands or millions.

These producers are often connected to mid- or low-voltage levels grids (distribution grids), generally closer to demand centres, and are often consumers of electricity themselves. This new category of “prosumers” (producers and consumers of electricity) is actually not new. Autoproducers of electricity have existed for decades in many countries (UN Statistics 2020), but this role was predominantly linked to enterprises which produced their own electricity for their own business/activity needs (e.g. heavy industry) and sold the excess.

The main change introduced by prosumers is their number, scale and diffusion. This is already having an important impact on transmission and distribution grids, and is expected to change the way that transmission system operators (TSO) and distribution system operators (DSO) function and interact, including the possibility for DSOs to provide flexibility services to the system through the aggregation of small active actors (TSO–DSO 2019).

3.4 The Merit Order Effect

The introduction of high quantities of power generation from non-dispatchable sources can have a significant effect on the hourly merit order dispatch.Footnote 10 As wind and solar PV have usually near-zero marginal cost, they are positioned at the beginning of the merit order and they usually push more expensive generating technologies out of the merit order stack. This effect changes hour by hour and can be very pronounced, limited or null depending if their generation is high, moderate or near zero. For example, in the case of solar PV, this can correspond to pronounced periods of generation around midday during summer days, limited during winter days, or no impact at night.

The overall merit order effect on annual electricity prices depends on several factors, including the level of deployment, the type, mix and geo-localisation of wind and solar PV technologies, their generation profile, the match or mismatch with the hourly electricity demand, the eventual bottlenecks in transmission and distribution grids, and the mix and marginal cost of the dispatchable plants.

An additional important element that can affect the merit order is represented by the level of capacity adequacy (e.g. if the system is in a situation of overcapacity or conversely lack of capacity) and the speed with which wind and solar PV capacity are being added to the system. In the case of lack of capacity in the system, the additional non-dispatchable capacity is likely to help the adequacy, but have limited effect in term of impact on the average wholesale electricity prices.Footnote 11 In the case of overcapacity coupled with very high deployment rate of non-dispatchable technologies, the reduction of average wholesale prices is likely to be more pronounced.

Increasing levels of non-dispatchable generation have the effect of making the residual load duration steeper and steeper—as illustrated in Fig. 16.5b—with increasingly lower prices corresponding to the low end of the curve. When the levels of wind and solar PV generation are such that too much generation is present in the system, and that the dispatchable plants cannot reduce further due to physical constraints, curtailment of non-dispatchable generation occurs (Fig. 16.7). In these situations of electricity oversupply, the electricity prices are typically at zero or near-zero.Footnote 12

Example of curtailment of non-dispatchable sources. (Source: author’s elaboration)

The addition of any type of plant to a power system usually reduces the average electricity price—even if by a small amount—as it replaces some more expensive plant in the merit order (except for cases of replacement of capacity) that would otherwise be utilised. This can have a significant impact on the revenues perceived by individual electricity generators. In the case of non-dispatchable renewables, the price reduction often occurs during the hours of highest generation (e.g. solar PV), therefore exacerbating the reduction of revenues that can be perceived from the market. Ensuring that market mechanisms can provide the right type of price signals and that these are sufficient for the necessary investments to be forthcoming is a key issue of any market design, as it will be discussed later in this chapter (see Sect. 5.2).

4 Main Integration Options

Low levels of wind and solar PV in the power mix can usually be integrated in power systems without major challenges and without adopting integration measures on a large scale, unless specific bottlenecks appear, often due to sub-regional concentrations. The higher the share of non-dispatchable sources, the more there will be a need to use a combination of integration measures, and to increase them in scale. The mix of these measures depends on the characteristics of each power system, and a coordinated approach is needed to reduce the costs involved (e.g. the choice between adding new storage or new transmission lines).

The adoption of the optimal mix of solutions depends also on the level of deployment of non-dispatchable technologies and on the type of requirements in terms of time response (from seconds to months) and location (Fig. 16.8). Four main integration options can be identified and will be discussed in this section:

-

Flexibility of power plants

-

Energy Storage

-

Demand-side response

-

Transmission and distribution grids and interconnections

Range of options for integration. (Source: IEA 2018)

Wind and solar technologies can also contribute themselves to their own integration, through careful choice of siting, using technological advancements (e.g. new wind turbines that reduce fluctuations of wind, inverter size lower than peak capacity of the PV module, changing the orientation of PV modules to allow to produce more during “shoulder hours”), or allowing for pre-curtailment to be able to ramp up production during a forecasted need. The pre-curtailment, though, must show a clear economic case, as it requires to limit production during a period to be able to increase it at a later stage.

The highest share of combined generation of wind and solar PV in the world on average in 2018 was reached in Denmark, where about 50% of total annual generation came from non-dispatchable sources, primarily wind (IEA Statistics 2020). This high level was reached thanks to several factors, with high levels of interconnection with the neighbouring countries playing a primary role.

While solar PV is still limited as a share of total generation, with only California passing the double-digit share (at around 14%) and Italy ranking second in the world at around 8%, several countries have surpassed the 15% threshold of wind share in their power mix, with some even exceeding the 30% threshold. This is the case for several States in the centre of the United States (EIA 2020) (with a high quality of wind resources), while several countries in Europe produced more than 20% of their mix from wind and solar PV combined (e.g. Ireland, Germany, Spain, the United Kingdom), and a similar level is being approached in other areas in Asia, such as in the Inner Mongolia province in China.

4.1 Increasing Flexibility of Power Plants

Flexibility in power systems is not new, nor is it linked to the deployment of non-dispatchable sources. Electricity supply has been matching the variations of electricity demand for decades, and the flexibility of power plants was central to achieve this goal. The novelty introduced by non-dispatchable renewable sources is primarily represented by the scale of the hour-to-hour variations of wind and solar electricity production that are present in few systems today and are expected to appear and increase in scale in many power systems in the coming future (Fig. 16.9).

Range of simulated hour-to-hour variations in output for new projects by technology, 2018. (Source: IEA 2019a)

Today, the flexibility of power systems is mostly provided by power plants, with a smaller role for interconnectors. At global level, battery and interruptible industrial customers still play a marginal role (IEA 2018). Hydropower plants with reservoir storage often provide the greatest flexibility at least cost—but this resource is limited in many countries—while gas-fired plants are typically the most flexible albeit pricier alternative. In some countries, such as France, nuclear power can contribute significantly to the flexibility of the system. The flexibility requirements depend on the mix of power plants present in a system and can vary significantly over the year. For example, in the United States, with combined high penetration of wind and solar PV, high levels of flexibility can be expected to be needed during spring (NREL 2013).

Greater flexibility can come from existing plants, but many of these plants (e.g. older plants designed originally for baseload operation) might require retrofit or refurbishment to increase ramping capabilities, minimum level of sustainable output and accelerated timing for shut down and start up. An example can be provided by the case of China, where high levels of curtailment of wind generation have been registered, in particular in the north-western provinces. One of the main causesFootnote 13 of the curtailment has been identified in the lack of flexibility of fossil-fuelled plants, and of combined heat and power (CHP) plants in particular. Providing these plants with higher flexibility has allowed to decrease the curtailment levels (CEM 2018).

4.2 Energy Storage

Electricity cannot be easily stored in large quantities, contrary to the case of fossil fuels (see chapter on Energy Storage), and it needs to be stored through some other form of energy means. Gravitational, mechanical, chemical and thermal are the most common forms. An important difference to consider between these forms of storage is whether they can shift the use of electricity over time (like in the case of hydro storage or batteries) or they convert it to another energy form (like in the case of thermal storage).

The main technology that allows electricity storage today is pumped storage hydropower (PSH) that stores electricity in the form of gravitational potential energy. In 2018, 155 GW of hydropower pumped storage capacity was installed globally (IEA 2019b), representing over 90% of power storage capacity worldwide. Compressed-air, flywheel and other storage technologies, while promising, are still quite limited. Hydrogen production and storage hold very interesting potential, but cost and development of infrastructure could delay ambitions and deployment (IEA 2019c).

Storage in form of heat is being considered in several countries. Denmark and Sweden, for example, have robust district heating networks and an extensive use of CHP plants. Excess generation from non-dispatchable sources can be used in electric boilers (DTU 2019), therefore allowing for heat storage and reducing the need for fossil fuels. Further projects are being explored to store high temperature heat for use in industrial applications. In China, the use of heat storage and pumped hydro storage is being considered to reduce the curtailment of wind electricity generation (Zhang et al. 2016).

Battery storage—the majority of which are lithium-ion—has been soaring over the last few years, to reach about 8 GW in 2018. About 60% of the total installed capacity has been added in the last two years, showing how a combination of policies (targets and subsidy schemes) and costs reductions can support technology deployment. Over 60% of the 3 GW added in 2018 were for batteries behind the meter, and the rest for utility-scale (IEA 2019d). These two market segments hold very large potential for further development.

In the case of the residential segment, one of the main drivers for battery deployment is expected to come from the increase of self-consumption, in particular as the selling price to the grid of the electricity produced by distributed wind and solar PV will become more reflective of market price and not determined by support policies. In the case of utility-scale, batteries can provide different system and ancillary services, with duration ranging from seconds to hours. Frequency regulation has been an important factor for deployment.

Electrical storage (such as batteries) can play a very important role in the integration of non-dispatchable renewable technologies, in particular if excess generation (and curtailment) is present in the system (Fig. 16.10). In this case, the charging of the battery happens at near-zero cost, and most of the discharging can take place in the following hours when the generation from dispatchable plants is highest and correspondingly the electricity price received or potentially saved (if it reduces own needs when exposed to high price signals) by the storage operator.

Reduction of curtailment of non-dispatchable renewables and of dispatchable plants’ generation through storage. (Source: author’s elaboration)

The electricity price differential between charging and discharging is a fundamental parameter for the economic viability of battery storage, as the investment cost and the number of cycles that the battery is called upon in a year (which generally renders storage uneconomical for seasonal storage). As can be seen in the figure, storage capacity reduces the call on other dispatchable plants, and consequently is likely to reduce the overall electricity price in those hours. This operation can be repeated for growing amounts of battery capacity, until the selling electricity price that is achieved reduces the profits to a level that makes economically unprofitable adding further capacity into the system.

4.3 Demand-Side Response

Electricity demand must be matched in every moment by corresponding electricity generation. Historically, electricity generation has been adjusted to match the fluctuations of electricity demand, as the majority of the generators present in the system were dispatchable units, and demand was relatively inflexible. The more non-dispatchable generators will be added into the system, the more this paradigm will change. Electricity demand can—and is set to—contribute to the flexibility of the system, adjusting to the availability of low cost non-dispatchable generation.

While storage shifts electricity production of non-dispatchable technologies to periods when it is needed, demand-side measures can help the integration of wind and solar PV by shifting demand to the moments in which the generation of these technologies is highest (Fig. 16.11). Demand-side measures are aimed at lowering electricity consumption in moments when generation from dispatchable source (and consequently the electricity price) is higher, and shifting demand to moments of high non-dispatchable generation. An example is provided by delaying the use of appliances in the residential sector.

Reduction of curtailment of non-dispatchable renewables and of dispatchable plants’ generation through demand-side management. (Source: author’s elaboration)

Deferring (or anticipating) consumption by few hours can increase electricity demand during the hours when the production of non-dispatchable renewables would have been otherwise lost or difficult to use. The economic incentive of this action is given by the electricity price differential between the avoided consumption and the actual consumption. The higher this differential is, the higher the potential that can be achieved with different measures in different sectors.

Demand response is not new to power systems, but until recently, it was limited only to large industrial or commercial customers (mainly for load shedding) and, in some cases, enabled by night and day tariffs. Digitalisation, the deployment of smart appliances and internet of things, the surge of distributed prosumers, the diffusion of smart meters, the increase of electric vehicles and smart charging, all contribute to increase the accessibility of a much greater number of actors to participate and to increase the flexibility of electricity demand.

Regulation, time-of-use and real-time tariffsFootnote 14 can play a key role in the effective realisation of the demand-side potential. The potential of demand-side response is huge, and has been estimated at 4000 TWh worldwide for the year 2017 (IEA 2018). Most measures shift the consumption for a duration that spans typically from 1 hour up to 8 hours, with upfront and operating costs that are quite limited for a range of options.

The sectors with the highest potential are the commercial and residential ones, but industry and transport (especially with the multiplication of electric vehicles) can have a significant impact too. The potential varies significantly by country or region, with significant differences over the different periods of the year, making the realisable potential much more limited than the theoretical one. Policies and regulation will be key to unlock this potential.

4.4 Transmission and Distribution Grids and Interconnections

Power grids have been the backbone of power systems for decades, allowing to connect supply and demand centres, to link and share resources, and to sustain security and reliability of power systems. Transmission and distribution grids are playing—and are set to continue to play—a central role also in terms of connecting and facilitating the integration of wind and solar PV technologies.

Expanding transmission capacity can allow to exploit more remote resources. Grid-expansion planners need to carefully evaluate the cost of such infrastructure against the value and quality of the resource and whether the grid expansion is needed for the overall power system needs. For example, in China, a significant expansion of HVDC lines is planned to connect the north-west provinces to the load centres in the south-east provinces, which will allow to exploit the wind and solar resources in those provinces and export towards high-demand centres. Expanding transmission capacity can also allow to connect and develop additional resources, as in the case of offshore wind through submarine extensions, connecting new farms, creating new power hubs, and eventually allowing to create meshed networks to increase security and reaching better integration throughout different regions.

Interconnections across different areas can have a double value for the integration of non-dispatchable renewables. On one side, they contribute to smooth the fluctuations of generation of different wind and solar PV plants (Fig. 16.12), and on the other they allow to even out different regional electricity demand profiles. Increased interconnection across different areas also allows to better integrate electricity markets and decrease price differences across regions. The Clean Energy for All Europeans Package adopted by the European Union in 2019 (EC 2019) has among its targets to “allow at least 70% of trade capacity to cross borders freely, making it easier to trade renewable energy across EU borders and hence support efforts to reach the EU’s binding goal of 32 % renewables by 2030”. Grid codes can play a crucial role to reach this goal (IRENA 2016).

Impact of increasing interconnection on hourly capacity factors of wind power in selected regions, 2014. (Source: IEA 2016a)

The diffusion of distributed generators is likely to change the relative role of transmission system operators and distribution system operators, as discussed earlier in this chapter, and will call for increased interaction and coordination. The level of deployment of the different integration means is going to affect each other. Economics and policy support are at the basis of the different choices of the mix of integration measures, but also the type and scale of the solutions will be an influencing factor. The impact of the deployment of battery storage and demand response on electricity grids can be very different depending on if they increase auto-consumption at the sites where they are deployed. In this case, the call on the grids is likely to decrease. If, instead, their deployment allows for higher consumption in neighbouring areas, the call on distribution grids is likely to increase. If the deployment of storage or demand-side measures takes place at utility scale or in places geographically distant, the call on both transmission and distribution grids is likely to increase.

5 Economic Implications

5.1 Economic Value of System Flexibility

Flexibility is set to play a central role in future power systems. Nonetheless, it has been a key feature also of past systems. All flexibility options were already present in power systems: interconnections to share adequacy reserves (and therefore lower costs), interruptible loads, storage (mainly in the forms of pumped storage hydropower plants) and—mainly—flexibility from existing power plants.

The value of flexibility was often expressed by the higher value and remuneration of plants operating during peaking hours. These plants were typically low-investment, high-fuel cost plants, running for only few dozen or hundreds of hours per year. The other flexibility measures were often aimed at reducing peak demand and move load towards increased utilisation of cheaper baseload plants (e.g. in the case of night and day tariffs).

In these systems, there was a very good correspondence between base, mid and peak demand with base, mid and peak prices, as ensured by the use of merit-order dispatching—once constraints and bottlenecks in a balancing area had been taken into account. The increase of non-dispatchable renewable capacity in power systems is set to change this correspondence, moving the hours with the highest electricity prices away from peak demand periods, but rather to correspond with the peak hours of residual electricity demand (see Sect. 3.2). Similarly, the lowest prices are likely to happen at times of high production from non-dispatchable sources, which in some systems may no longer correspond to the periods of lowest demand. For example, in systems with high shares of solar PV, peak residual demand tends to occur in early morning or late afternoon, while the lowest residual demand occurs in summer midday times. Significant variations of electricity prices can then arise with increasing hour-to-hour variation of wind and solar PV electricity production.

The value of increased system flexibility reflects the value of exploiting the highest possible volumes (its entirety might not be always economically viable) of available non-dispatchable generation. In other words, the introduction of growing shares of wind and solar PV generation in the system tend to make the residual curve steeper, while the introduction of growing amounts of integration measures (such as demand- side measures or battery storage) tend to turn the residual curve flatter again, avoiding (or reducing the amount of hours) for it to go negative, and for the related prices to reach near-zero levels (Fig. 16.13). Moreover, the value of flexibility is also important on the intraday, balancing and system services markets (e.g. frequency regulation).

Indicative impact of integration measures on residual load duration curve and prices. (Source: author’s elaboration)

The mix of generating technologies and of integration measures depends on a variety of factors. It is mostly affected by economics and by policy, decisions and can change significantly across countries or power balancing areas. The level of decarbonisation that is aimed for and the targeted speed of transformation of the system, the eventual introduction of carbon pricing, the availability of renewable resources (e.g. how much hydropower can still be added in the system, or the type, quality and distance of wind and solar resources from demand centres), the ban or introduction of technologies (e.g. nuclear or CCUS) and the power market rules, all play a fundamental role in determining the mix.

The value of an additional plant in a given system depends on its impact on the other technologies and measures and on the overall system costs. The introduction of growing shares of wind and solar PV has an impact on their own competitiveness and ability to recoup their investment costs. The next two sections discuss the decreasing value of the electricity generated by non-dispatchable sources, and the limitations of the use of LCOEs for the evaluation of competitiveness and possible ways to overcome these limitations.

5.1.1 Changing Value of Wind and Solar PV Electricity Production

The increase of overall installed capacity in power systems following the increase of wind and solar PV capacity and the related effects on the merit order can have—as discussed above—a significant impact on the wholesale electricity prices. The hourly power prices are set to change only marginally in hours of low generation from non-dispatchable renewable sources. Conversely, they decrease substantially during the hours of very high generation from non-dispatchable sources.

At high levels of penetration of non-dispatchable renewables sources in the overall power mix, during the hours of highest generation, the hourly wholesale prices can reach zero or near-zero levels. The hours in which wind and solar PV generate the most will therefore register the lowest levels of prices. The value of the generation from an additional plant in those hours will therefore be minimal, bringing the overall value to decrease at growing levels of penetration in the mix (Hirth 2013).

This effect—often referred to as the “auto-cannibalisation” effect—has important implications on the evaluation of competitiveness (see below the section on LCOEs), on the system value of each technology, on the evaluation of eventual subsidies and on the mechanisms to put in place for these plants to recover their investments. If wind and solar PV plants recover their investments through out-of-power market mechanisms (such as subsidy mechanisms or long-term power purchase agreements), the evaluation of the market value is important to assess the extent of subsidies and the possibility and timing for an eventual phase-out. If these plants are going to participate more and more in electricity markets, this evaluation is key to assess their possible future deployment. If the deployment of capacity is centrally planned, this evaluation can provide very important information to evaluate the optimal low-carbon capacity mix.

5.1.2 Competitiveness, LCOE and System Costs

Wind and solar PV technologies have been deployed fast thanks to support policies and to falling costs. As their cost decreases, they are approaching competitiveness with other sources and the need to have a proper evaluation method is more and more concrete. Nonetheless, the evaluation of competitiveness of different power generating sources can be very complex, as several parameters need to be taken into account. A first step in this process is to assess the cost of production of different generation technologies. These include the fixed costs (investment and operating and maintenance), the cost of capital, the variable costs (fuel, operating and maintenance, eventual CO2 pricing), efficiency, construction time, lifetime (or cost recovery period), the amount of electricity generated, and (in some cases) the decommissioning costs.

An indicator that is often used and that combines all these elements together is the Levelised Cost of Electricity (LCOE) (see footnote 53). This indicator has the advantage to be practical and easy to calculate, at least in its simplified version. It does present, though, several limitations, among which: it is most often based on a fixed amount of operating hours over the entire lifetime (at least in the simplified formula); it doesn’t include externalities (if not priced, such as CO2 emissions); it doesn’t show the value of specific technologies to the power system; it doesn’t include information about grid costs or integration costs; it considers the costs but not the value of the electricity produced.

Overall, the LCOE is a flawed indicator to evaluate competitiveness (Joskow 2011), in particular when comparing plants used for different uses (e.g. peak vs. baseload plants) and even more to compare dispatchable and non-dispatchable technologies. As the generating technologies cannot be considered in isolation one from another, the overall system costs should be considered (NEA 2012), including balancing costs, adequacy costs, grid costs, the cost of integration measures.

To properly allow the evaluation of competitiveness across technologies, several studies and institutions have developed indicators to complement or surpass the LCOE limitations. Among these: the Levelized Avoided Cost of Electricity developed by the United States’ Energy Information Administration (EIA 2019), System Costs developed by the OECD’s Nuclear Energy Agency (NEA 2019), System LCOE (Ueckerdt et al. 2013) and the Value Adjusted LCOE (VALCOE) developed by the International Energy Agency (IEA 2018).

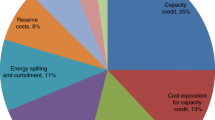

The indicator (VALCOE) developed by the International Energy Agency, for example, includes three main components of adjustment—energy, capacity and flexibility—respectively to account for the value of electricity produced, the contribution to system adequacy and to the flexibility of the system (Fig. 16.14). Many indicators—including the IEA’s—while recognising the need to include grid costs (in particular the effect on distribution grids) and electricity security considerations, still do not include them, often due to the difficulties linked to their evaluation.

Levelised cost of electricity (LCOE ) vs. value adjusted LCOE (VALCOE). (Source: IEA 2018)

5.2 Impact on Power Markets and Attractiveness to Invest in New Plants

The introduction of large shares of non-dispatchable renewables in power systems has, as discussed above, an impact on the amount and type of capacity installed, and the way that power plants operate. Overall, this leads to a significant increase of the installed capacity in a determined power balancing area, a decrease of the utilisation factors of dispatchable plants and a decrease of wholesale power prices (at least in the short term).

Power markets have been designed to provide appropriate price signals for the efficient dispatching in the short term, and to incentivise adequate investment in the long term. While the merit order dispatch continues to be the most efficient way in the short term to select the power plants that will run each hour, the changes introduced by wind and solar PV in power systems raise the question whether the market signals will be sufficient in the long term to stimulate enough investments in new power plants to ensure capacity adequacy and to achieve low-carbon power systems. This impact can be very different if a plant seeks to recover the majority of its revenues through power market mechanisms or through support mechanisms (IEA 2016b).

Power plants that traditionally look for revenues through power markets have seen their profits decrease through a combined effect of lower amounts of running hours and decreased power prices. The issue of revenues being insufficient to stimulate new investment is not new, in particular for peak-load plants, and has been present well before the large increase of wind and solar PV. This has been and is leading to changes in some countries from the originally designed “energy-only” markets to include growing remuneration for capacity, flexibility and ancillary services mechanisms. While the role of these components may be limited now, it can be expected to grow following the increasing shares of non-dispatchable renewables.

Nonetheless, many power plants nowadays do not receive the bulk of their revenues from the power market. Several types of support measures are in place across many countries. Feed-in-tariffs (FiTs), Contracts for Difference (CfD), premiums, tax exemptions or credits and long-term power purchase agreements (PPAs) (with or without auctions to award them) are some of the most common forms (Hafner et al. 2020). Mostly designed for supporting the take-off of renewable sources, these mechanisms are now frequently adopted for nuclear power plants, carbon capture, utilisation and storage (CCUS) demonstration plants, and in some cases also for fossil fuel-fired capacity.

The support measures for renewable sources have been evolving throughout the last 15 years, and it is very likely that they will continue to become more sophisticated and adapted to the needs and requirements of each power system. However, if the majority of investment in new power plants is set to take place through non-power market mechanisms, the validity and existence of power markets for long-term signals could be put into question (Joskow 2018).

While the decreasing costs of wind and solar PV technologies has brought them closer to competitiveness, the “auto-cannibalisation effect” (i.e. the reduction of possible revenues on the power markets for wind and solar PV) discussed above puts in question the ability of these plants to sustain the current (or even an accelerated) pace of deployment without a continuation of some form of support measures.

A key and common characteristic among most low-carbon technologies is given by the importance of the weighted average cost of capital (WACC) in their overall generating cost. Wind and solar PV, like most of these technologies, are capital-intensive, with little or no fuel cost. The different types of risks associated to the project are reflected in the WACC, making it a crucial element for the viability of new investments. Private investors usually can successfully handle market risks (such as those linked to commodities fluctuation), but can be wary of uncertainties surrounding political and regulatory risks. Conversely, adequate policy measures can moderate financing risks and costs of low-carbon projects, therefore playing a central role in their competitiveness and in reducing overall system costs.

Facilitated by the decrease of storage and demand-side technology costs and by the increasing digitalisation of appliances and information systems, the power sector is also seeing the emergence of new actors. A growing role could be played by aggregators such as virtual power plants (VPPs) that pull together decentralised producers and consumers, storage owners, flexible load, and are enabled by smart meters and smart grids.

5.3 Impact on Electricity Prices and Affordability

The way electricity prices are formed depends on several factors and on the market rules of each power system. End-user electricity prices typically include (IEA 2012):

-

Wholesale electricity generation costs: capital costs of power plants, fuel and eventual CO2 costs, operating and maintenance costs;

-

Adequacy and balancing costs;

-

Transmission and distribution costs: capital costs of network infrastructure and operation and maintenance costs;

-

Metering, billing and other commercial costs; and,

-

Taxes and subsidies such as Value-added taxes, subsidies (such as renewable source specific ones) and other taxes and subsidies.

Wind and solar PV technologies have been deployed thanks to subsidies, which are often paid by consumers through an additional component on the end-user tariffs (such as the Erneuerbare Energien Gesetz (EEG) component in Germany). Conversely, as previously discussed, the introduction of growing amounts of wind and solar capacities in power systems has the effect of reducing wholesale prices to at least partially compensate the increase of end-user prices due to subsidies (Cludius et al. 2013).

The anticipated continuing reduction of investment costs of wind and solar PV technologies is expected to contribute to moderate or reduce the overall system costs. Whether this decrease will be compensated by the cost of adequacy and balancing cost, and of integration measures (e.g. investments in transmission and distribution grids, dispatchable low carbon sources, storage or demand-side technologies), is the object of several studies.

The overall power system costs will also depend on additional solutions and interactions with other sectors such as with the transport sector (smart charging of electric vehicles), the heat sector (possibly using excess of non-dispatchable renewables in water-heater boilers), or with other energy vectors (such as hydrogen).

The evaluation of the relative economics and the integration with policies in other sectors is set to play a fundamental role. In particular, the coordination of renewable policies with energy efficiency ones can be very important to reduce (or mitigate the increase) of electricity (and energy, at large) bills for end-use consumers. The affordability of the transformation towards a low-carbon power sector for end users will critically hinge on the ability of minimising the costs involved, without forgetting the need for dedicated policies aimed at removing inequalities and supporting the poorest part of population.

6 Conclusions

Non-dispatchable renewable energy sources are set to play a key role in the decarbonisation of electricity generation and are set to increase in the power mix in all countries. Their particular properties—scarcity, variability and abundance depending on the time of production (within a day, month or season)—are changing the way power systems have been operated till now. Low shares of these technologies in the power mix do not pose significant challenges, while the impact increases with growing shares.

The change in system adequacy calculations, the much higher amounts of capacity present in the systems, lower capacity factors of dispatchable plants, the need for greater system flexibility, the changes in the merit order and the electricity pricing mechanisms, and a greater number of actors on the producing side are the main challenges identified in this chapter.

Several solutions already exist: improving the flexibility of existing power systems and making this a requirement for future capacity additions, expanding the role and interconnection of electricity grids (with an evolving interaction between TSOs and DSOs), enhancing and enabling the development of storage capacity and demand-side management technologies.

The ability to tap into all these options will hinge critically on adequate policies being put in place for these technologies to be deployed and to participate in power markets. The minimisation of the overall system costs may require to coordinate the deployment of some of the integration measures—e.g. the choice between adding new storage or new transmission or distribution lines—as the value of each choice depends on its relative economics with all other choices.

The economic impact is uncertain, and efforts need to be made in particular from policymakers making this transformation affordable to consumers, and ensuring that businesses are not at a disadvantage with their competitors. The mix of low-carbon technologies to achieve the decarbonisation of the power sector is set to depend on relative economics, but policies will play a key role to make sure that the different integration options are deployed to their full potential.

Notes

- 1.

Run-of-river hydropower indicates a power station with no or very small reservoir capacity. Its electricity generation is therefore dependent on the variability of the water stream. As water cannot be stored (except in some cases for small quantities), excess supply of water is lost.

- 2.

Small hydropower can be defined as having a capacity smaller than 10 MW, medium hydropower from 10 to 100 MW and large hydropower plants for capacities larger than 100 MW.

- 3.

The solar irradiance is often expressed through indicators such as direct normal irradiance (DNI), diffuse horizontal irradiance (DHI) or global horizontal irradiance (GHI).

- 4.

Obtained multiplying the installed (maximum) capacity by the number of hours in the period considered (8760 hours in the case of one year).

- 5.

The levelized cost of electricity (LCOE ) is an indicator of the average cost per unit of electricity generated by a power plant. Under the standard formulation, LCOE is the minimum average price at which electricity must be sold for a project to “break-even”, providing for the recovery of all related costs over the economic lifetime of the project (IEA 2016a).

- 6.

Loss of load expectation (LOLE) is the number of hours in a given period (generally one year) in which the available generation plus import cannot cover the load in an area (ENTSO-E 2015).

- 7.

In systems where the production of non-dispatchable renewables coincides well with peak demand, the capacity credit at low penetration rates can be higher than in the figure.

- 8.

Load duration curves are obtained by reorganizing the hourly electricity demand from the highest value to the lowest throughout all the 8760 hours in a year (i.e. 365 days by 24 hours).

- 9.

The optimal mix of low-carbon technologies depends on several factors and is not the object of this chapter.

- 10.

The merit order dispatch is a commonly used method to rank electricity generators according to their increasing marginal cost (or variable cost), reporting the amount of electricity generated by each plant on the x-axis and the corresponding variable cost on the y-axis. It is usually built for each hour (or sub-hour period, depending on the market) to determine which plants will generate for a given level of demand. The highest marginal cost of the plants that are brought online determines the price in each hour. As demand changes every hour along with the availability of the different plants, so will the hourly electricity price. The annual electricity price is given by the average of the 8760 hourly prices, weighted by the hourly generation.

- 11.

Depending on how the shortage is priced, the hourly and the average wholesale prices could potentially be reduced too.

- 12.

The phenomenon of negative electricity prices observed in some markets is voluntarily excluded from this chapter, as this can be only a transitory phenomenon and not a long-term one. Should this prove not to be the case, “near zero” prices should be substituted with “near-zero or negative prices”.

- 13.

Another important cause was the lack of transmission capacity.

- 14.

“Energy storage in the electricity system means the deferring of an amount of the energy that was generated to the moment of use, either as final energy or converted into another energy carrier” (EC 2017).

- 15.

In time-of-use tariffs, retail prices typically change in pre-determined sets of hours, regardless of system conditions, while in real-time tariffs retail prices change dynamically according to system conditions. Smart meters are needed for the latter.

References

California Independent System Operator (CAISO) (2019) Accessed in April 2020. https://www.caiso.com/Documents/FlexibleResourcesHelpRenewables_FastFacts.pdf

CEM (2018) Thermal Power Plant Flexibility, a Publication Under the Clean Energy Ministerial Campaign. https://www.cleanenergyministerial.org/sites/default/files/2018-06/APPF%20Campaign_2018%20Thermal%20Power%20Plant%20Flexibility%20Report_cleanenergyministerial.org__0.pdf

Cludius, J., Hermann, H., and Matthes, F. (2013, May) The Merit Order Effect of Wind and Photovoltaic Electricity Generation in Germany 2008–2012. CEEM Working Paper 3-2013 (PDF). Sydney, Australia: Centre for Energy and Environmental Markets (CEEM), The University of New South Wales (UNSW). http://ceem.unsw.edu.au/sites/default/files/documents/CEEM%20(2013)%2-%20MeritOrderEffect_GER_20082012_FINAL.pdf

DTU (2019) Whitebook Energy Storage Technologies in a Danish and International Perspective, DTU Energy, Department of Energy Conversion and Storage, Roskilde, Denmark.

European Commission (EC) (2017, February) European Commission Staff Working Document, Energy Storage—The Role of Electricity, European Commission, SWD (2017) 61 final. https://ec.europa.eu/energy/sites/ener/files/documents/swd2017_61_document_travail_service_part1_v6.pdf

ENTSO-E (2015) ENTSO-E Scenario Outlook and Adequacy Forecast 2015, Brussels. https://eepublicdownloads.blob.core.windows.net/public-cdn-container/clean-documents/sdc-documents/SOAF/150630_SOAF_2015_publication_wcover.pdf

European Commission (EC) (2019) Clean Energy for All Europeans Package, Brussels. https://ec.europa.eu/energy/en/topics/energy-strategy-and-energy-union/clean-energy-all-europeans

Hafner, Manfred et al. (2020) The Geopolitics of the Global Energy Transition, Policy and Regulation of Energy Transition Chapter, Springer Nature, Volume 73. https://link.springer.com/content/pdf/10.1007%2F978-3-030-39066-2.pdf

Hirth, Lion (2013) The Market Value of Variable Renewables. Energy Policy, 38: 218–236. https://www.neon-energie.de/Hirth-2013-Market-Value-Renewables-Solar-Wind-Power-Variability-Price.pdf

IEA Statistics (2020) International Energy Agency, Paris, Web Page Accessed in July 2020. https://www.iea.org/data-and-statistics/data-tables

International Energy Agency (IEA) (2012) World Energy Outlook 2012, Paris. https://www.iea.org/reports/world-energy-outlook-2012

International Energy Agency (IEA) (2016a) World Energy Outlook 2016, Paris. https://www.iea.org/reports/world-energy-outlook-2016

International Energy Agency (IEA) (2016b) Re-Powering Markets, Paris. https://www.iea.org/reports/re-powering-markets

International Energy Agency (IEA) (2018) World Energy Outlook 2018, Paris. https://www.iea.org/reports/world-energy-outlook-2018

International Energy Agency (IEA) (2019a) Offshore Wind Outlook 2019, Paris. https://www.iea.org/reports/offshore-wind-outlook-2019

International Energy Agency (IEA) (2019b) Renewables 2019 Market Report, Paris. https://www.iea.org/reports/renewables-2019

International Energy Agency (IEA) (2019c) The Future of Hydrogen, Paris. https://www.iea.org/reports/the-future-of-hydrogen

International Energy Agency (IEA) (2019d) Annual Storage Deployment, 2013–2018, Paris, Accessed in December 2019. https://www.iea.org/data-and-statistics/charts/annual-storage-deployment-2013-2018

International Renewables Energy Agency (IRENA) (2016) Scaling Up Variable Renewable Power: The Role of Grid Codes, 2016, Abu Dhabi. https://www.irena.org/publications/2016/May/Scaling-up-Variable-Renewable-Power-The-Role-of-Grid-Codes

International Renewables Energy Agency (IRENA) (2019a) Renewables Capacity Statistics 2019, Abu Dhabi. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Mar/IRENA_RE_Capacity_Statistics_2019.pdf

International Renewables Energy Agency (IRENA) (2019b) Renewable Power Generation Costs in 2018, Abu Dhabi. https://www.irena.org/publications/2019/May/Renewable-power-generation-costs-in-2018

Joskow, Paul L. (2011) Comparing the Costs of Intermittent and Dispatchable Electricity Generating Technologies. American Economic Review, 101(3): 238–241. https://www.aeaweb.org/articles?id=10.1257/aer.101.3.238

Joskow, P. (2018) Challenges for Wholesale Electricity Markets with Intermittent Renewable Generation at Scale: The U.S. Experience, MIT CEEPR Working Paper, Dec 2018. https://economics.mit.edu/files/16650

Nuclear Energy Agency (NEA/OECD) (2012) Nuclear Energy and Renewables. System Effects in Low-carbon Electricity Systems, Paris. https://www.oecd-nea.org/ndd/pubs/2012/7056-system-effects.pdf

Nuclear Energy Agency (NEA/OECD) (2019) The Costs of Decarbonisation: System Costs with High Shares of Nuclear and Renewables, Paris. https://www.oecd-nea.org/ndd/pubs/2019/7299-system-costs.pdf

National Renewable Energy Laboratory (NREL) (2013) The Western Wind and Solar Integration Study Phase 2, Golden, Colorado. https://www.nrel.gov/docs/fy13osti/55588.pdf

Paula Mints (2019, April) Photovoltaic Manufacturer Capacity, Shipments, Price & Revenues 2018/2019, SPV Market Research. Report SPV-Supply6.

TSO–DSO (2019) TSO–DSO Report, An Integrated Approach to Active System Management, Brussels. https://www.edsoforsmartgrids.eu/wp-content/uploads/2019/04/TSO-DSO_ASM_2019_190304.pdf

Ueckerdt, F., Hirth L., Luderer G., and Edenhofer, O. (2013, December 15) System LCOE: What Are the Costs of Variable Renewables? Energy, 63: 61–75. https://www.neon-energie.de/Ueckerdt-Hirth-Luderer-Edenhofer-2013-System-LCOE-Costs-Renewables.pdf

UN Statistics (2020) United Nations Statistics Division, Accessed in April 2020. https://unstats.un.org/unsd/energy/Eprofiles/2015/03.pdf

United States Energy Information Administration (EIA) (2019) Levelized Cost and Levelized Avoided Cost of New Generation Resources in the Annual Energy Outlook 2019, Accessed in April 2020. https://www.eia.gov/outlooks/aeo/pdf/electricity_generation.pdf

United States Energy Information Administration (EIA) (2020) Accessed in April 2020. https://www.eia.gov/electricity/data.php

Zhang, N, et al. (2016) Reducing Curtailment of Wind Electricity in China by Employing Electric Boilers for Heat and Pumped Hydro for Energy Storage. Applied Energy. https://www.sciencedirect.com/science/article/pii/S0306261915013896

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2022 The Author(s)

About this chapter

Cite this chapter

Baroni, M. (2022). The Integration of Non-dispatchable Renewables. In: Hafner, M., Luciani, G. (eds) The Palgrave Handbook of International Energy Economics. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-030-86884-0_16

Download citation

DOI: https://doi.org/10.1007/978-3-030-86884-0_16

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-030-86883-3

Online ISBN: 978-3-030-86884-0

eBook Packages: Economics and FinanceEconomics and Finance (R0)