Abstract

This contribution examines the relationship between trust and economic growth. Taking panel data and using a fixed-effects estimation for a 41-country sample over the time period from1980 to 2004 and with a total of 129 observations, tis points out that economic growth is negatively related to an increase in trust. This negative finding is in contrast to most empirical findings using a cross-sectional design. The common knowledge which has governed the nature of discussions in the social sciences and economics for the last 10 years, namely that trust is generally positively related to economic performance, must be seriously questioned. From a policy point of view, an increase in trust is crucial for countries with low levels of trust, but can likely be neglected by countries with sufficient levels of trust and may even hamper economic performance in countries with high levels of trust. The relationship is tested in the context of EU countries, OECD countries, and developing countries. Interpersonal trust and systemic trust are differentiated.

Originally published in: Felix Roth. Does too much trust hamper economic growth? Kyklos, Vol. 62, No. 1, 2009, pp. 103–128.

Felix Roth wishes to thank Stephan Klasen, Fran Tonkiss, seminar participants of the research seminar for Ph.D. candidates at the chair of Stephan Klasen, the participants in the summer school of the postgraduate program The Future of the European Social Model, the participants in the 2006 Ratio Colloquium for Young Social Scientists: Trust, Reciprocity and Social Capital, the participants in the workshop and summer school program Social Capital, Corporate Social Responsibility, and Sustainable Economic Development, the participants in the Post Graduate Summer School Civil Society, Social Capital and Democracy, and the participants in the Symposium on Social Capital in European Regions for valuable comments and suggestions.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

Recent years have seen interest in the theoretical and empirical relationship between social capital and economic growth. Social capital is said to be “the glue that holds societies together” and it is emphasized that “without it no economic growth or human well-being is possible” (Serageldin 1999, p. iii). Empirical research shows that there is a positive relationship between interpersonal trust and economic growth (Knack & Keefer, 1997; La Porta et al., 1999; Whiteley, 2000; Zak & Knack, 2001; Beugelsdijk et al., 2004). In contrast to existing works, which examine the relationship between social capital and economic growth using a cross-section research design, this contribution uses a panel research design.

2 Theoretical Links Between Social Capital, Trust, and Economic Growth

2.1 Social Capital and Trust

Many economists focus on the concept of trust when talking about social capital (Knack & Keefer, 1997; Solow, 1999; Whiteley, 2000; Berggren & Jordahl, 2006; c.f. Bjørnskov, 2003; Sabatini, 2008). Tonkiss (2000) comments that “trust regularly features—together with norms and networks—within definitions of social capital” (p. 78). But how is trust related to social capital? Although there are various definitions of social capital (Bourdieu, 1983; Coleman, 1988, 1990; Putnam, 1993; Fukuyama, 1996, p. 26; Temple 2001 in OECD, 2001, p. 39; Ostrom, 1999, p. 176; Newton, 1997, p. 576; for a wide range of definitions see Woolcock, 1998, p. 189), trust is considered to be the most important dimension of social capital (Coleman, 1990; Fukuyama, 1996; Newton, 1997, p. 576; Ostrom, 1998; Uslaner, 1999, p. 122; Tonkiss, 2000; Zak & Knack, 2001).

Therefore, this contribution focuses primarily on the dimension of trust in the concept of social capital in the following empirical application.

Although there is a variety of definitions of trust (Fukuyama, 1996, p. 26; Misztal, 1996, p. 16; Delhey & Newton, 2005, p. 311; Dasgupta 1997, p. 5 in Ostrom, 1998, p. 12; Luhmann, 2000, pp. 1, 27), recent literature distinguishes between three different forms: 1) thick trust, 2) interpersonal or generalized trust, and 3) systemic or institutional trust (Putnam, 2000, p. 137; Newton, 1997, p. 578, ff.; Luhmann, 2000).

Newton (1997) and Williams (1988) classify trust that is generated by family networks as thick trust. In contrast, interpersonal or generalized trust is defined as trust that is generated by looser, secondary relations in modern societies, based on everyday interaction between people who do not otherwise know each other. Most scientists focus on interpersonal trust when examining the relationship between economic growth and trust, as it should facilitate cooperation and lower transaction costs in economic systems. Economic systems tend to be characterized by a substantial degree of differentiation, and exchange activity frequently depends upon trust in strangers. Interpersonal trust can be regarded as a good indicator of the levels of solidarity in society, as well as a good indicator of the overall level of social cohesion in society. This survey item, which is used in several international surveys, is likewise used in this contribution when discussing trust.

The third category of trust, systemic or institutional trust, refers to the confidence people have in certain institutions. When discussing systemic trust here, the focus is on trust in the parliament, the police, the armed forces, and major companies.

2.2 Relationship Between Social Capital, Trust, and Economic Growth

Arrow (1972) argues that the presence of virtues such as trust plays a significant role in the operation of economic systems (p. 345). He builds his assumption upon the paradigm of exchange and elaborates that the process of exchange requires or is greatly facilitated by virtues such as trust (p. 345). For Fukuyama (1996), a nation’s well-being and its ability to compete depend upon the level of trust inherent in a society (p. 7). This argument is built upon his belief that economic activity itself is part of the social life and constitutes itself according to the norms, rules, and moral obligations of a society (p. 7). Robert Putnam (1993) comes to the conclusion that high stocks of social capital in an economic region “bolster the performance of the polity and the economy, rather than the reverse” (p. 176). He puts forward four arguments why social capital has a positive effect on the economy: 1) it facilitates coordination and cooperation for mutual benefit, 2) it solves dilemmas of collective action, 3) it reduces the incentives for opportunism, and 4) it reduces egoism (1995, p. 76). In line with this argument, Sen (1999) argues that “the development and use of trust in one another’s words and promises can be a very important ingredient of market success” (p. 262) and that “no society would be viable without some norms and rules of conduct” (Sen, 1977, p. 332).

According to Whiteley (2000), interpersonal trust has three direct channels through which it might stimulate economic growth (p. 451).

Firstly, trust has a direct effect on economic performance by reducing transaction costs. Transaction costs evolve during the economic process of exchange and specialization and are defined as the costs associated with banking, insurance, finance, wholesale, and retail trade, or in terms of dealing with lawyers and accountants, etc. (North, 1990, p. 28). For North, the transaction costs are a part of the costs of production. Taking this new production function into consideration, high-trust societies should produce a higher output than low-trust societies as the cost for transactions like monitoring, enforcing, and protecting contracts is smaller. People who trust each other do not spend as much time or money protecting their property rights. They might be able to solve their problems without lawyers or lawsuits.

Secondly, trust has a direct influence on growth because it enables actors to solve collective action problems (Whiteley, 2000, p. 451). These arguments are in line with Hardin (1982) and Ostrom (1990). In high-trust societies, it should theoretically be easier to cope with free rider problems that evolve, for example, with smog problems, CO2 emissions, and clean neighborhoods (Hardin, 1982, p. 9), as well as, for example, the problem of overfishing (Ostrom, 1990, p. 3). Generally, in high-trust societies, people will not so readily take advantage of the public infrastructure.

The third direct effect is that principal-agent problems might be much less significant in high-trust societies (North, 1990, pp. 32, 33). According to Knack and Keefer (1997), two arguments can be mentioned in this context: 1) if entrepreneurs devote more time to monitoring possible malfeasance by partners, employees, and suppliers, they will have less time to devote to innovation in new products or processes: and 2) employment contracts in which managers rely on employees to accomplish tasks can be difficult to monitor. Fukuyama (1996) argues that high-trust communities are not as dependent on extensive contracts and legal regulations (p. 26) and that cooperation in high-trust societies will not have to be enforced by coercive means (p. 27). He concludes that “if people who have to work together in an enterprise trust one another, … doing business costs less” (p. 27).

It has been argued thus far that trust, and therefore the facilitation of collective action, leads to economic development and growth. But is this necessarily or always the case?

One starting point for a possible negative relationship between trust and economic growth can be found in the literature on collective action by Mancur Olson (1982). This literature admittedly deals with the dimension of networks rather than the dimension of trust, but the discussion proves quite relevant for these purposes. Olson analyses the relationship between collective action and economic performance in quite a contrary way. For example, collective action can undermine the state’s power to implement necessary reforms or agendas to maintain high economic growth rates. Olson argues that stable societies are in danger of accumulating “collusions” and “organizations of collective action” over time (p. 41). If a society accumulates too many organizations that function as special interest groups, economic growth is harmed by reduced efficiency, by income being aggregated in the societies in which they operate, and by political life being made more divisive (p. 47). To give one example, if a state desires to implement labor market reform in which, for example, employee rights are reduced, a sector with cheap labor is implemented, working hours are extended, and social spending on unemployment benefits and support is decreased to reduce the costs of the labor factor, a highly trusting and solidaristic society would more likely oppose the state’s efforts at reform and will, via the mobilization of collective action, stop the reform agenda, and therefore limit the potential of higher economic growth rates. This argument is built upon Putnam’s empirical findings that a vibrant civil society is crucial for high levels of trust (Putnam, 1993, 1995). In fact, it could be actors within civil society such as church groups, professional groups, and Social Movements Organizations (SMOs) that oppose the state’s will to implement reforms. Similarly, the number of workers being members of labor unions might be a critical factor for the existence of high levels of trust (Putnam, 1993, 1995, 2000). For Putnam himself, civic associations and stocks of interpersonal trust are clearly interlinked. As such, the negative relationship between trust and economic growth could be driven by associational activity. Groups with strong bonding ties may produce, on an aggregated scale, a high interpersonal trust stock, while reducing economic outcomes, as described above. Although being aware of various negative outputs that can evolve from a strong civil society, Putnam never really clarified the extent to which civic engagement and high stocks of trust may hamper economic performance.

3 Previous Findings

Using a cross-sectional analysis with 29 market economies as units of observations, Knack and Keefer (1997) discover that trust, in particular, as well as norms, matter for economic growth, but that associations do not. Their social capital variable is measured taking 21 observations from the first wave of the World Value Survey (1981–1984) and eight observations from the second wave of the WVS (1990–1993). Thus, the authors utilize trust values from 1990 to 1993 to explain the economic growth rate from 1980 to 1992. The authors were aware of the endogeneity problem and argue that reverse causation is not problematic due to the fact that the correlation between countries from the first and second wave of the WVS is very high (0.91).

In 2001, Zak and Knack reinvestigated the empirical results from Knack and Keefer were published in 1997. They used a cross-sectional analysis and observations from 41 market economies. They used all three waves from the WVSs of 1981–1984, 1990–1993, and 1995–1997, the Eurobarometer and a government-sponsored survey for the case of New Zealand. Their dependent variables were investment share as a percentage of GDP, averaged over the period from 1970 to 1992, and average annual growth in per capita income over the same period. Depicting the relationship between trust and economic growth, the authors came to the conclusion that a positive relationship exists between trust and growth. They determined that growth rises by nearly 1% point on average for each 15% point increase in trust (p. 309).

Beugelsdijk et al. (2004) analyzed the statistical robustness of the results of Knack and Keefer and Zak and Knack along four dimensions of robustness. They concentrated on the statistical significance and explored the influence of changing sets of conditioning variables on the estimated effect of trust. Moreover, they analyzed the sensitivity of the results for using different proxies or specifications for basic variables like human capital. Finally, they investigated the effects on the significance and effect size when the 29-country sample by Knack and Keefer was extended by 12 in the Zak and Knack paper. They conclude that the empirical literature on trust and economic growth seems to be plagued more by data limitations than by econometric problems such as omitted variable biases. The authors come to the conclusion that “their extensive robustness analysis further adds to the empirical evidence that trust matters for explaining variation in economic performance” (p. 132) (Table 7.1).

Berggren et al. (2007) conducted an extensive robustness analysis of the relationship between trust and growth by investigating a latter time period and a larger sample size. The authors worked with 63 countries using data on trust from the fourth version of the WVS and from the Latinobarometro, as well as new data on growth, to separate time and sample effects. They investigated whether previous results on the trust-growth relationship for the period of 1970–1992, studied by Zak and Knack and Beugelsdijk et al., also hold for the 1990s. They learned that when outliers are removed (here they mention China, specifically) the trust-growth relationship is only statistically significant (with significance at the 95% level) in 10% of their 1140 regressions and that it is half as large compared to the results that had been previously reported. The authors emphasize however that their results do “not necessarily mean that trust is unimportant for growth, but its importance seems to be more limited and uncertain than previously claimed” (p. 1).

La Porta et al. (1999), using an OLS regression on 39 countries and a cross-section design with a dependent variable, per capita GDP growth rate from 1970 to 1993, found a significant positive relationship between trust and economic growth. They concluded that “in sum trust enhances economic performances across countries” (p. 317) and that “despite economist’s skepticism … theories of trust hold up remarkably well when tested on a cross-section of countries” (p. 320).

Whiteley (2000) examined the relationship between trust and economic growth in the framework of a modified neoclassical model of economic growth. Using cross-section designs in a 34-country sample, and using the timeframe of 1970–1992, he came to the conclusion that an index of three trust indicators from the World Value Survey (1990–1993) has a positive effect on economic growth, with an impact as great as the variable human capital and conditional convergence. His findings support the idea that “values play a key role in explaining cross-national variations in economic performance and that they cannot be ignored in any properly specified model of economic growth” (p. 460).

In contrast to these findings, Heliwell (1996), taking an OECD country sample (17 OECD countries), found a negative relationship between trust and productivity growth from 1960 to 1992 (associations and social capital, an equally weighted combination between trust and associations, are also negatively related to productivity growth). His results seem to be the only cross-country indication of a negative effect between trust and economic performance.

These empirical studies involve a critical and important step in focusing on the concept of trust when reflecting upon economic growth. Their cross-section design strongly supports the hypothesis that trust is relevant to economic growth. Nevertheless, they all neglect to examine how changes in trust affect economic growth. For policy decision-making, however, it might be more relevant to analyze the effect of changes in trust on economic performance. Furthermore, using a fixed-effects model provides two advantages. Firstly, unobserved heterogeneity can be controlled for. Secondly, the problem that the interpretation of the trust items differs across countries can be addressed.

4 Data and Measurement

4.1 Operationalization

The World Value Survey presents only limited data on trust. The trust variable is constructed, as it is usually agreed upon by scholars from various disciplines (Inglehart, 1990, 1999; Knack & Keefer, 1997; Paxton, 1999, 2002; Uslaner, 1999; Alesina & La Ferrara, 2000; Putnam, 2000; Whiteley, 2000; Zak & Knack, 2001; Van Oorschot & Arts, 2005; Delhey & Newton, 2005; Berggren & Jordahl, 2006), by aggregating the answer, “Most people can be trusted.”Footnote 1 (after deleting the “Don’t know.” answers) to the item, “Generally speaking, would you say that most people can be trusted or that you need to be very careful in dealing with people?” (WVS 1999–2002).Footnote 2 It is thereby possible to compare the stock of trust in different nations, from developed to developing, including transition states. The stock of trust varies from 2.6% in Brazil 1995–1997 (Inglehart 2000) to 66.5% in Denmark 1999–2002 (European Values Study Group and World Values Survey Association, 2004). There are various critiques of this operationalization.Footnote 3

4.2 Model Specification

To be able to compare these results with previous empirical work conducted on the relationship between trust and economic growth, a version of the economic growth model used by Knack and Keefer (1997), Zak and Knack (2001), Beugelsdijk et al. (2004), and Berggren et al. (2007) was used. Furthermore, a version of this type of growth model was used by Forbes (2000) when analyzing the relationship between inequality and economic growth in a panel setting from 1965 to 1995.

In the baseline model, economic growth is estimated as a function of the natural logarithm of initial income, the price level of investment, human capital, and interpersonal and systemic trust. An estimate of an unbalanced panel was made. The baseline growth model for the fixed-effects estimation is modelled as follows:

where i represents each country and t represents each time period (with t = 1–5); Growthi,t is the average annual growth for country i at period t; Trusti,t-1, Incomei,t-1, Human Capitali,t-1, PPPIi,t-1, and are respectively trust, income, human capital, and price level of investment for country i during period t–1; αi represents a group-specific constant term and wi,t is the error term.

4.3 Measurement of Data

Data on income and growth are based on per capita income between 1980 and 2004, adjusted for purchasing power parity (PPP, expressed in constant 2000 US Dollars), are drawn from the World Development Indicator Database, 2006. Since yearly growth rates incorporate short-run disturbances, growth is averaged over 5-year periods. The dependent variable here is an average growth rate per capita for the periods 1980–1984, 1985–1989, 1990–1994, 1995–1999, and 2000–2004.

-

The data on the price level of investment, population growth as a proxy for the factor, Labor, the investment share of GDP at constant prices, and openness at constant prices, are drawn from the Penn World Table 6.1 (Heston et al., 2002). The variables were constructed by using lagged variables (1979, 1984, 1989, 1994, and 1999) to reduce the problem of endogeneity.

-

The data on interpersonal trust and systemic trust are drawn from four waves of the WVS 1981–1984, 1990–1993, 1995–1997 (Inglehart et al., 2000), and 1999–2002 (European Values Study Group and World Values Survey Association, 2004) and the Eurobarometer 25 (Rabier et al., 1988) providing data for 1986.

-

The data on human capital are based on Barro and Lee (2000) and refer to the total years of schooling of the total population aged 25 and over. Data were taken for 1980, 1985, 1990, 1995, and 2000.

5 Descriptive Statistics

The country sample consists of 41 countries. Table 7.2 lists all interpersonal trust values for the included country observations in my dataset. Twenty-seven out of 30 OECDFootnote 4 countries and 14 out of 15 EU15Footnote 5 countries are included. The observations were made over the time period from 1980 to 2004 providing five time periods with a total of 129 cases for the analysis.

In contrast to the consensus that interpersonal trust is a constant variable, formed by the cultural background of a nation (Knack & Keefer, 1997; Zak & Knack, 2001; Knowles, 2005; Delhey & Newton, 2005, p. 314; c.f. Inglehart, 1997, p. 224; Inglehart, 1999, p. 95; Noelle, 2005, p. 5), a closer look at Table 7.2 highlights the existing variance in trust, with a strong decline in trust between the years 1990 and 1995.Footnote 6

Only Germany, Japan, and India have increased their levels of trust. On the other end of the scale, the two liberal economies, the UK and the US, face a severe decline. The US loses 14.4% of interpersonal trust and the UK, 12.2%. Poland and Finland face the most severe losses; Poland loses 16.6%, Finland loses 15.1%, South Africa loses 10.1%, China loses 7.8%, and Sweden loses 6.4%. Argentina and Mexico lose around 5%. Only Chile and Norway behave in a more stable manner.

Figure 7.1 shows the relationship between the changes in trust for the period [1995–1990] and the changes in growth in the period [9599–9094] for all countries (“Before and After” Comparison). The change in the trust level in the US of −14.4% is associated with a change in the annual growth for that period of 1.2%. In the US, a decline in trust went hand in hand with a rise in annual growth. In the UK, the same picture is replicated. The change in the trust level of −12.2% is associated with a change in the annual growth rate of 2.08%. The Scandinavian countries Finland and Sweden support the findings on the US and the UK. The decline in trust of −15.1 and −6.4% corresponds to an increase in the growth rate of 5.8% and 2.9%. The transition countries Poland and Bulgaria behave in the same manner. In Poland the decline in the trust level of 16.6% is related to the increase of 5.2% in annual growth. This relationship changes when observing Argentina and India. In Argentina, a decline in the level of trust of −5.8% corresponds to a decline in the annual growth rate of −4.3%. In India, an increase in the level of trust of 3.4% is followed by an increase in the annual growth rate of 1.7%. In the cases of Argentina and India, there seems to be a positive relationship between trust and economic growth. Taking all countries into consideration, a weak negative relationship exists between delta Trust and delta Growth with an R-Square value of 0.173. Considering only OECD countries, the R-Square rises to 0.461.

Scatter plot between Δ trust [1995–1990] and Δ growth [9599–9094]

6 Econometric Analysis

6.1 Cross-Sectional Analysis

First of all, using a cross-section design, an OLS model is estimated with robust estimators of standard errors for the dataset. For the dependent variable, the average growth rate of GDP per capita for the 15-year period from 1990 to 2004 is used. The country sample consists of 32 countries due to data limitations from the interpersonal trust value in the 1990s. All variables used here are stock variables. Interpersonal trust values are all taken from the second wave of the WVS which was conducted from 1990 to 1993. The variable Human Capital is applied for the 1990s and the price level of investment is taken from 1989.

Regression 1 in Table 7.3 indicates that all variables have the expected signs except the human capital variable. A negative significant coefficient for the income variable (conditional convergence) is produced; likewise, a negative significant coefficient for the price level of investment is produced and the positive significant relationship between interpersonal trust and economic growth is replicated. This result, the positive relationship between Interpersonal Trust and Economic Growth, is in accordance with most empirical findings using a cross-section design (see here particularly Knack & Keefer, 1997; Zak & Knack, 2001).

6.2 Pooled Panel Analysis

Secondly, an estimate for the model using a pooled panel analysis is made. A pooled panel analysis is similar to the method of a standard ordinary least-square estimation, but in order to obtain more reliable estimates of the parameters, a pooled panel estimation widens the database by pooling the time series of the country sample. Hence, the pooled panel consists of 129 observations with 41 individual cases. Using a pooled panel regression and examining all 129 observations, Regression 2 in Table 7.3 replicates the result from the cross-section design and the results of most empirical research. A significant positive coefficient for the trust variable is obtained. However, the proxy for the human capital variable “average years of schooling” shows no significant relationship to economic growth. Furthermore, conditional convergence shows no significant relationship to economic growth. Overall the model does a poor job of describing the variance in the short-term growth rates utilized. Only 22% of the variance of economic growth can be explained by the model. As transition countries follow an economic growth pattern that is quite different from the rest of the countries in the sample, Regression 3 uses a country sample excluding the six transition countries. This country sample still has 115 observations. All variables have the expected signs and are significant. This yields conditional convergence, a positive relationship between human capital and economic growth, a positive relationship between interpersonal trust and economic growth, and a negative coefficient for price levels of investment. Some 35% of the variance in international growth can be explained. Regression 4, taking a country sample without transition countries, modulates trust as a curvilinear relationship to economic growth by including the squared term of interpersonal trust into the regression. Astonishingly, the curvilinear relationship is highly significant. All variables in the regression have the expected signs and are highly significant (99% level of significance). The linear and squared terms of interpersonal trust are each statistically significant: 0.16 (4.42) and −0.0015 (−3.24). These estimates imply that starting from a low-trust country (where the interpersonal trust value is for instance 2.8, as in Brazil), increases in interpersonal trust tend to stimulate economic growth. However, the positive influence attenuates as the level of trust rises and reaches zero when the indicator takes on a mid-range of 53.3. Therefore, an increase in the level of trust appears to enhance economic growth in countries that have initial low levels of trust but to retard economic growth for countries that have already achieved a substantial level of trust. The model is able to explain 39% of variance in international growth rates (4% more than the linear modulation).

Regression 5 examines an OECD-23 countries sample.Footnote 7 A significant curvilinear relationship exists between trust and economic growth. All other variables have the expected signs and behave significantly. Conditional convergence, a positive relationship between human capital and growth and a negative relationship between price level of investments and economic growth, exists. Figure 7.2 shows the partial regression plot between trust and economic growth for the OECD-23 sample. The positive influence attenuates as the level of trust rises and reaches zero when the indicator takes on a mid-range of 42.5.

Partial regression plot for 23 OECD countries—trust and economic growth (1980–2004)

6.3 Panel Analysis

In order to explore how changes in trust levels affect economic growth, the model is estimated using a panel analysis. The standard methods of panel estimation are fixed-effects or random-effects. The fixed-effects estimates are calculated from differences within each country; the random-effects estimation, in contrast, incorporates information across individual countries as well as across periods. The major drawback with the random-effects analysis is that it is consistent only if the country-specific effects are not correlated with the other explanatory variables. A Hausmann specification test can evaluate whether this independence assumption is satisfied (Hausman, 1978; Forbes, 2000, p. 874). The Hausmann test applied here indicates that the fixed-effects model should be used.Footnote 8

Regressions 1 through 4 in Table 7.4 consider the case of linear regression with panel data. As there has been no research conducted on panel data of which the author is aware, it seems most appropriate to begin the estimation of the panel data using the linear regression method. As there is the possibility of cross-sectional heteroskedasticity, a robust estimation technique is used. The coefficients are the same with and without the robust estimation technique; however, the robust estimator produces larger standard errors. The fixed-effects estimations use 41 countries with a total of 129 observations. It is an unbalanced panel. Regression 1 in Table 7.4 contradicts the results of all previous empirical works (Knack & Keefer, 1997; La Porta et al., 1999; Whiteley, 2000; Zak & Knack, 2001, Beugelsdijk et al., 2004; cf. Heliwell, 1996), as well as these results from the cross-section design and the pooled panel analysis, a negative (−0.08) and significant (−2.52) coefficient for the interpersonal trust variable is obtained, indicating that changes in trust and economic growth are negatively related to each other. All other variables in the model have the expected signs. Significant conditional convergence, a positive relationship between human capital and economic growth, and a significant negative coefficient for the variable price level of investment all appear. Some 28% of the within-variance can be explained. Regression 2 presents the random-effects model. As expected when employing a random-effects model, the positive result from the cross-sectional and the pooled panel analysis is replicated. It indicates a positive (0.04) and significant result (significance at the 90% level). Regression 3 shows the results for the growth model when the six transition countries are omitted from the country sample. Interestingly, the relationship between interpersonal trust and economic growth can also be modeled curvilinearly in the 115-country sample when trying to explain the within-variation with a fixed-effects model. In country observations with lower levels of trust, an increase in trust seems to have a positive effect on economic growth, whereas in country observations with high levels of trust, a decrease in trust seems to have a positive effect on economic growth. Regression 4 estimates the 115-country sample with a random-effects model. The results from Regression 4 in Table 7.3 are replicated.

6.3.1 Sensitivity Analysis

Since the negative relationship between interpersonal trust and economic growth in Regression 1 in Table 7.4 challenges econometric work using a cross-sectional design, the robustness of the results must be tested. To test the sensitivity of the results, Table 7.5 shows several specification tests including the exclusion of influential observations, the alteration of case specifications, the inclusion of additional regressors, the restructuring of the data, resampling techniques, and clustering for human capital. The first row of Table 7.5 (labelled “None”) reports the results, standard errors, and regression coefficient, taken from Regression 1 in Table 7.4. Successive rows reflect the effects of interpersonal trust on economic growth when the indicated change is made.

The second row of Table 7.5 reports the results after omitting the case of Poland from the country sample. As can be inferred from Fig. 7.1, the case of Poland exhibits the strongest negative relationship between changes in trust and changes in economic growth (specifically, a decrease in interpersonal trust of 16.6% is associated with an increase in economic growth of 5.2%). As suspected, Poland plays an important part in explaining the relationship between trust and economic growth. Although the relationship between trust and economic growth remains significant (significance at the 90% level) the coefficient decreases from −0.08 to −0.06.

In the third row, the case of Greece is omitted. As can be inferred from Table 7.2, Greece’s level of trust decreases by 26.7%, whereas its economic growth rate increases by 2.91%. After deleting Greece from the country sample, the relationship between changes in trust and changes in economic growth loses statistical significance.

Rows 4 through 12 examine the different country samples. When analyzing an OECD country sample, changes in trust and changes in economic growth are negatively related (which is strongly influenced by the data on Poland). In the OECD 23-country sample, the relationship can be either linearly modulated or curvilinear. In the linear modulation, a significant negative result appears; however, the curvilinear relationship explains 16% more of the variance in international growth rates. As with the sample of the OECD-23 countries, the EU-15 countries sample can be modulated in both relationships, either linear or curvilinear. In the linear modulation, a significant negative coefficient (strongly influenced by the data on Finland and the United Kingdom) appears; the curvilinear model, however, is able to explain 52% of the within-variation (18% more than the linear model). Apart from Poland and Greece, the negative relationship between trust and economic growth seems to be driven by the highly developed countries from the sample of liberal countriesFootnote 9 (significance at the 99% level) and the Scandinavian countries sample. As already seen in Fig. 7.1, in the United Kingdom and the United States, a strong decrease in trust is associated with an increase in economic growth. Row 11 examines the sample of developing countries sample.Footnote 10 An increase in interpersonal trust is associated with an increase in economic growth (as the author is currently investigating the changes within particular cases, it is not problematic at this time to include China in the sample). After excluding the case of China, the relationship is still significant (90% level) and positive (0.16)). Countries from Latin America (Row 12) face a positive relationship between changes in trust and economic growth. The theoretical claim that, considering developing countries, trust level changes should have a positive effect on economic growth is hereby verified.

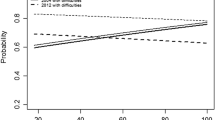

Figure 7.3 illustrates the findings between trust and economic growth from Regression 3 in Table 7.4. In a country with a low level of trust, an increase in trust is associated with an increase in economic growth if the increase in trust takes place on the left side of the distribution (the maximum value of the graph is 30). Once a threshold of 30% of trust is exceeded, the increase in trust will hamper economic growth.

Predicted relationship between trust and economic growth—fixed-effects estimation

Row 13 includes the variable Openness. The trust coefficient stays statistically significant. The model now explains 46% of the within-variation of economic growth (18% more than the original result from Regression 1 in Table 7.4). Openness seems to be a very important variable when trying to explain the within-variation of economic growth. Rows 14 and 15 include the two Solow parameters, Investment Share of GDP and Population Growth. The trust coefficient remains statistically significant.

Rows 16 through 19 include four indicators of systemic trust variables: 1) confidence in the parliament, 2) confidence in the forces, 3) confidence in the police, and 4) confidence in major companies. None of the four systemic trust variables is statistically significantly related to economic growth. However, confidence in companies is related to interpersonal trust as this variable loses statistical significance when the item is included in the regression. Furthermore, when examining an OECD or EU-15-country sample, the variables Confidence in the Parliament and Confidence in major companies are both negatively related to economic growth. Particularly in the Liberal Market Economies (LMEs), a decline in Confidence in the Parliament is associated with an increase in economic growth (significance at the 99% level).

Row 20 includes social expenditure in the regression (OECD, 2004). If the welfare state creates high levels of interpersonal trust and negatively affects economic growth (see Atkinson, 1999 for a detailed discussion of the relationship between the welfare state and economic growth), an increase in welfare state activity would go hand in hand with an increase in levels of interpersonal trust and a decrease in economic growth. However, the trust coefficient is not altered by the inclusion of social expenditure. The hypothesis, that social expenditure could explain the negative relationship between trust and economic growth, must be rejected. (However, due to data restrictions, the hypothesis was only tested in 27 OECD countries with a total of 84 observations).

Row 21 includes the Gini-Coefficient.Footnote 11 On the one hand, taking the empirical results from Forbes (2000) for granted, an increase in social inequality is related to an increase in economic growth. On the other hand, an increase in social inequality seems to be strongly related to a decrease in interpersonal trust. Knack and Keefer (1997), Zak and Knack (2001), Knack and Zak (2002), in particular, as well as Delhey and Newton (2005) and Rothstein and Uslaner (2005), have given first empirical proof that trust is stronger in nations with more equal income among their citizens. However, the trust coefficient is again not altered. The hypothesis that social inequality could explain the negative relationship between trust and economic growth has to be rejected. (Here, also due to data restrictions, the hypothesis was only tested in 20 OECD countries with a total of 62 observations.)

Row 22 examines an unbalanced panel for the time period, 1990–2004. This procedure allows the exclusion of data derived from the Eurobarometer 25. After excluding the first two periods (1980–89), trust is still negatively and significantly related to economic growth. Row 23 considers a balanced panel with 15 countries and 45 country observations examining economic growth from 1990 to 2004 using data from the second, third, and fourth waves of the WVS. Trust is negatively related to economic growth. When using a balanced panel from 1980 to 2004 (Row 24) taking five countries with 15 observations into consideration, trust loses statistical significance (primarily due to the small number of observations).

Row 25 shows the result when clustering for the Human Capital variable. (Clustering for the other variables does not change the results.) This procedure produces an estimator “that is robust to cross-sectional hereroskedasticity and within-panel serial correlation which is asymptotically equivalent to that proposed by Arellano (1987)” (Stata Corporation, 2005, p. 293).

Rows 26 and 27 introduce resampling techniques. Either when using Bootstrap Estimation or Jackknife Estimation, the coefficient remains statistically significant (however only at the 90% level).

7 Conclusion

This contribution examined the relationship between trust and economic growth. Two findings are especially important.

First, taking panel data and using a fixed-effects estimation for a 41-country sample over the time period from 1980 to 2004 and with a total of 129 observations, this contribution points out that economic growth is negatively related to an increase in trust. This negative finding is in contrast to most empirical findings using a cross-sectional design. The negative relationship seems to be mainly driven by developed countries from the OECD (here specifically Poland, Greece, and the United States), and the EU-15 (here particularly the United Kingdom and Finland), and very strongly by LMEs and Scandinavian countries. However, when considering a country sample which excludes the six transition countries, a curvilinear relationship appears. In countries with low initial levels of trust, an increase in trust leads to an increase in economic growth (samples for developing countries and Latin American countries). In countries with high initial levels of trust, an increase in interpersonal trust leads to a decrease in economic growth (especially in the samples of LMEs and Scandinavian countries). The curvilinear relationship can be replicated in a sample of OECD-23 countries, as well as in an EU-15-country sample, meaning that in those countries in the OECD and EU-15 which have low initial stocks of trust, as for instance Portugal, an increase in trust is associated with an increase in economic growth.

Second, when analyzing the relationship between interpersonal trust and economic growth in a cross-section of countries using either a cross-section, pooled panel, or random-effects design, the positive results from previous empirical research were replicated. However, when examining a country sample which excluded the six transition countries, a curvilinear relationship between interpersonal trust and economic growth was detected. In countries with low initial levels of trust, an increase in trust is associated with an increase in economic growth. But once a threshold of trust is surpassed, an increase in trust harms economic growth.

Taking these results into consideration, theoretical implications and empirical findings between trust and economic growth must be reevaluated. More theoretical and empirical research is necessary to clarify the relationship. From a policy point of view, it is important to differentiate between countries with high and low initial levels of trust. An increase in trust is crucial for countries with low levels of trust, but can likely be neglected by countries with sufficient levels of trust and may even hamper economic performance in countries with high levels of trust. The common knowledge which has governed the nature of discussions in social science and economics for the last 10 years, that trust is positively related to economic performance, must be seriously questioned. The relationship depends on the level of trust already existing in a country, thus determining whether it is important to invest in trust-building policies or not.

Still one has to bear in mind that the marked difference across time and across countries, and particularly the difference between a cross-section analysis using long-term growth, could have to do with the fact that a 5-year average of growth could be more sensitive to business cycle influences than, for example, a 10- or 15-year average. Although 5-year growth averages are commonly used for analyzing short- or medium-term growth dynamics, it is not yet fully clear if business cycle considerations can be neglected without caution.

Furthermore, despite the fact that these results appear to be statistically robust and in line with theoretical assumptions, it is possible that the findings are partly due to the omission of some variable not considered, or that measurement error affected the results, or that the model is misspecified in other ways. Further investigations are necessary to corroborate the findings to be able to answer relevant policy questions.

Notes

- 1.

In the Eurobarometer 25, the answer is “Most people could be trusted.”

- 2.

The ending of the question is slightly different in the first three waves of the WVS and the Eurobarometer 25: “[One] can’t be too careful in dealing with people.” (WVS 1981–84; WVS 1990–93; WVS 1995–97) and “[One] could not be too careful in dealing with people.” Eurobarometer 25 (Rabier et al., 1988).

- 3.

This approach is criticized by referring to the non-comparability of the different cultural backgrounds of the countries that participate in the WVS. Researchers question whether data from China can be compared to data from Germany, when the etymological meaning of the term trust differs in the languages. Although correct, this criticism must be disregarded when comparing different cultures, in so far as intercultural comparison would otherwise be made impossible. One must therefore be pragmatic in using the data are available. Furthermore, recent research provides evidence that individuals from the different countries did interpret the question from the WVS in similar ways (Paxton, 2002, p. 261) and that the trust data are valid and of high quality as they correlate highly to a natural experiment done by the Readers Digest (Knack & Keefer, 1997, p. 1257). Glaeser et al. (2000) doubts that the item measures trusting behavior, and believes that it measures the overall level of trustworthiness in a society. Jagodzinski and Manabe (2005) state that the item does not measure trust but misanthropy, instead, and it was taken as an index of misanthropy by Rosenberg. Sobel (2002, p. 151), Portes (2000, pp. 4 ff.), and Durlauf and Fafchamps (2005) criticise the method of aggregation. For them social trust should more accurately be measured on a micro- and meso-level.

- 4.

Luxembourg, New Zealand, and the Czech Republic had to be excluded due to data restrictions.

- 5.

Only Luxembourg had to be excluded.

- 6.

Although trust values intercorrelate strongly (comparing every combination of two waves gives values from 0.75 to 0.93), there are still very important changes over time. If the wealthiest nation in the world, the United States, and the United Kingdom lose nearly one-third of their original trust level, trust cannot be treated as a constant variable. These changes in trust must be highlighted and examined. Taking the case of Germany for instance clarifies that over the timespan from1950 to 2005, there is steady increase of the level of interpersonal trust (Noelle, 2005). To emphasize the US case once more: Inglehart (1999, p. 95) and Uslaner (1999, p. 132) show that there is a decline in interpersonal trust from 58%in 1960 to 36%in 1994. Paldam (2007), who has worked independently on the analysis of the variance in interpersonal trust, discovers that there exists a great variance in the interpersonal trust data over time.

- 7.

The OECD country sample, which includes the three transition countries Slovak Republic, Poland, and Hungary as well as Iceland, has to be differentiated to an OECD23 country sample as the three transition countries are hard to interpret. Iceland is often excluded in cross-country investigations due to the size of its economy.

- 8.

The test statistic is χ2(4) = 1129.17. This rejects the null hypothesis at any standard of significance.

- 9.

Following Hall and Soskice (2001) Liberal Market Economies include the following five countries: the United States, the United Kingdom, Canada, Australia, and Ireland.

- 10.

The developing country sample includes the 11 countries South Africa, Bangladesh, Pakistan, Philippines, China, India, Argentina, Venezuela, Brazil, Peru, and Chile.

- 11.

Data on income inequality are based on the UN-database, WIDER. Only data originally drawn from the Luxembourg Income Study (LIS) are taken.

References

Alesina, A., & La Ferrara, E. (2000). The determinants of trust, NBER working paper 7621.

Arrow, K. (1972). Gifts and Exchanges. Philosophy and Public Affairs, 1, 343–362.

Atkinson, A. B. (1999). The Economic Consequences of Rolling back the Welfare State. MIT Press.

Barro, R., & Lee, J.W. (2000). International data on educational attainment: Updates and implications. (CID Working Paper, 42, April 2000) – HUMAN CAPITAL UPDATED FILES.

Berggren, N., & Jordahl, H. (2006). Free to trust: Economic freedom and social capital. Kyklos, 59, 141–169.

Berggren, N., Elinder, M., & Jordahl, H. (2007). Trust and growth: A shaky relationship. Empirical Economics. Forthcoming.

Beugelsdijk, S., de Groot, H., & van Schaik, A. (2004). Trust and Economic Growth: a Robustness Analysis. Oxford Economic Papers, 56, 118–134.

Bjørnskov, C. (2003). The happy few: Cross country evidence on social capital and life satisfaction. Kyklos, 56, 3–16.

Bourdieu, P. (1983). Ökonomisches, Kulturelles und Soziales Kapital. In R. Kreckel (Ed.), Soziale Ungleichheiten (Vol. 2, pp. 35–74). Soziale Welt.

Coleman, J. (1988). Social capital in the creation of human capital. American Journal of Sociology, 94, 95–120.

Coleman, J. (1990). Foundations of social theory. Belknap Press of Harvard University Press.

Delhey, J., & Newton, K. (2005). Predicting cross-national levels of social trust: Global pattern or nordic exceptionalism? European Sociological Review, 21, 311–327.

Durlauf, S. N., & Fafchamps, M. (2005). Social Capital. In P. Aghion & S. Durlauf (Eds.), Handbook of Economic Growth: Volume 1B (pp. 1639–1699). Elsevier.

European Values Study Group and World Values Survey Association. (2004). European and world values surveys integrated data file, 1999–2002, release I [Computer File]. 2ndICPSR version. ICPSR Study Number 3975. Cologne, Germany: Zentralarchiv für Empirische Sozialforschung (ZA)/Tilburg, Netherlands: Tilburg University/ Amsterdam, Netherlands: Netherlands Institute for Scientific Information Services (NIWI)/ Madrid, Spain: Analysis Sociologicus Economicos y Politicos (ASEP) and JD Systems (JDS)/ Ann Arbor, MI: Inter-university Consortium for Political and Social Research [producers], 2004. Cologne, Germany: Zenralarchiv für Empirische Sozialforschung (ZA)/Madrid, Spain Analisis Sociologicos Economicos y Politicos (ASEP) and (JDS)/Ann Arbor, MI: Inter-university Consortium for Political and Social Research [distributors].

Forbes, K. J. (2000). A reassessment of the relationship between inequality and growth. American Economic Review, 87, 869–887.

Fukuyama, F. (1996). Trust—The social virtues and the creation of prosperity. Free Press Paperbacks.

Glaeser, E., Laibson, D. I., Scheinkman, J. A., & Soutter, C. L. (2000). Measuring Trust. The Quarterly Journal of Economics, CXV, 811–846.

Hall, P., & Soskice, D. (2001). Varieties of capitalism. Oxford University Press.

Hardin, R. (1982). Collective action. Johns Hopkins University Press.

Hausman, J. A. (1978). Specification tests in econometrics. Econometrics., 46, 1251–1271.

Heliwell, J. (1996). Economic growth and social capital in Asia, NBER working paper 5470.

Heston, A., Summers, R., & Aten, B. (2002). Penn world table version 6.1. Center for International Comparisons at the University of Pennsylvania (CICUP).

Inglehart, R. (1990). Culture shift. Princeton University Press.

Inglehart, R. (1997). Modernization and postmodernization – Cultural, economic and political change in 43 societies. Princeton University Press.

Inglehart, R. (1999). Trust, well-being and democracy. In M. E. Warren (Ed.), Democracy and trust (pp. 88–120). Cambridge University Press.

Inglehart, R., et al. (2000). World values surveys and European values surveys, 1981–1984, 1990–1993, and 1995–1997 [computer file]. ICPSR version. ICPSR study number 2790. Institute for Social Research [producer], 2000. Ann Arbor, MI: Inter-university Consortium for Political and Social Research [distributor].

Jagodzinski, W., & Manabe, K. (2005). How to measure interpersonal trust? A comparison of two different measures. ZA-Information, 55, 85–96.

Knack, S., & Keefer, P. (1997). Does social capital have a payoff? A cross-country investigation. Quarterly Journal of Economics, 112, 1251–1288.

Knack, S., & Zak, P. J. (2002). Building trust: Public policy, interpersonal trust and economic development. Supreme Court Economic Review, 10, 91–107.

Knowles, S. (2005). The Future of Social Capital in Development Economic Research 2005.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W. (1999). Trust in large organizations. In P. Dasgupta & I. Seregaldin (Eds.), Social capital – A multifaceted perspective (pp. 310–324). The World Bank.

Luhmann, N. (2000). Vertrauen. Lucius and Lucius.

Misztal, B. A. (1996). Trust in modern societies—The search for the bases of social order. Polity Press.

Newton, K. (1997). Social capital and democracy. American Behavioral Scientist, 40, 575–586.

Noelle, E. (2005). Vertrauen ist Besser. Frankfurter Allgemeine Zeitung, 166, 5.

North, D. C. (1990). Institutions, institutional change and economic performance. Cambridge University Press.

OECD. (2001). The well-being of nations – The role of human and social capital. OECD.

OECD. (2004). Social expenditure database (SOCX). www.oecd.org/els/social/expenditure.

Olson, M. (1982). The rise and decline of nations: Economic growth, stagflation and social rigidities. Yale University Press.

Ostrom, E. (1990). Governing the commons: The evolution of institutions for collective action. Cambridge University Press.

Ostrom, E. (1998). A behavioral approach to the rational choice theory of collective action: Presidential Address, American Political Science Association, 1997. The American Political Science Review, 92, 1–22.

Ostrom, E. (1999). Social capital: A fad or a fundamental concept? In P. Dasgupta & I. Serageldin (Eds.), Social capital—A multifaceted perspective (pp. 172–214). The World Bank.

Paldam, M. (2007). Generalized trust—The macro perspective. Article presented at the Workshop and Summer School Social Capital, Corporate Social Responsibility and Sustainable Economic Development at the University of Trento.

Paxton, P. (1999). Is social capital declining in the United States – A multiple indicator assessment? American Journal of Sociology, 105, 88–127.

Paxton, P. (2002). Social capital and democracy: An interdependent relationship. American Sociological Review, 67, 254–277.

Portes, A. (2000). The two meanings of social capital. Sociological Forum, 15, 1–11.

Putnam, R. D. (1993). Making democracy work: Civic traditions in modern Italy. Princeton University Press.

Putnam, R. D. (1995). Bowling alone: America’s declining social capital. Journal of Democracy, 6, 65–78.

Putnam, R. D. (2000). Bowling alone: The collapse and revival of American community. Simon & Schuster.

Rabier, J.-R., Helene, R., & Inglehart, R. (1988). Eurobarometer 25, Holiday Travel and Environmental Problems. April 1986 [Computer File], ICPSR Study Number 8616.

Rothstein, B., & Uslaner, E. M. (2005). All for all: Equality and social trust, LSE health and social care discussion paper number 15. London School of Economics and Political Science.

Sabatini, F. (2008). Social capital and the quality of economic development. Kyklos, 61, 466–499.

Sen, A. K. (1977). Rational fools: A critique of the behavioural of economic theory. Philosophy and Public Affairs, 6, 317–344.

Sen, A. K. (1999). Development as freedom. Anchor books.

Serageldin, I. (1999). Foreword. In: S. Knack (Ed.), Social capital, growth and poverty: A survey of cross-country evidence, social capital initiative working paper 7 (p. iii).

Sobel, J. (2002). Can we trust social capital? Journal of Economic Literature, XL, 139–154.

Solow, R. (1999). Notes on social capital and economic performance. In P. Dasgupta & I. Serageldin (Eds.), Social capital—A multifaceted perspective (pp. 6–10). The World Bank.

Stata Corporation. (2005). Stata longitudinal/panel data reference manual release 9. Stata Press.

Tonkiss, F. (2000). Trust, social capital and economy. In F. Tonkiss & A. Passey (Eds.), Trust and civil society (pp. 72–89). Macmillan.

Uslaner, E. M. (1999). Democracy and social capital. In M. E. Warren (Ed.), Democracy and trust (pp. 121–150). Cambridge University Press.

Van Oorschot, W., & Arts, W. (2005). The social capital of European welfare states: The crowding out hypothesis revisited. Journal of European Social Policy, 15, 5–26.

Whiteley, P. F. (2000). Economic growth and social capital. Political Studies, 48, 443–466.

Williams, B. (1988). Formal structures and social reality. In D. Gambetta (Ed.), Trust: Making and breaking cooperative relations (pp. 443–454). Basil Blackwell.

Woolcock, M. (1998). Social capital and economic development: Toward a theoretical synthesis and policy framework. Theory and Society, 27, 151–208.

Zak, P. J., & Knack, S. (2001). Trust and growth. Economic Journal, 111, 295–321.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License (http://creativecommons.org/licenses/by-nc-nd/4.0/), which permits any noncommercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if you modified the licensed material. You do not have permission under this license to share adapted material derived from this chapter or parts of it.

The images or other third party material in this chapter are included in the chapter’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2022 The Author(s)

About this chapter

Cite this chapter

Roth, F. (2022). Does Too Much Trust Hamper Economic Growth?. In: Intangible Capital and Growth. Contributions to Economics. Springer, Cham. https://doi.org/10.1007/978-3-030-86186-5_7

Download citation

DOI: https://doi.org/10.1007/978-3-030-86186-5_7

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-86185-8

Online ISBN: 978-3-030-86186-5

eBook Packages: Economics and FinanceEconomics and Finance (R0)