Abstract

The use of photovoltaic technology is crucial to meet Europe´s ambitious climate and energy objectives set for 2030. To facilitate this shift, technological innovation is a key prerequisite, and the provision of public funding for related research and development is an important trigger. For this study, a vast set of data has been collected to explore how the EU and its Member States, plus Norway and Turkey, have so far invested in photovoltaic research and development. Based on historic values and actual trends, the authors additionally outline the possible future evolution of the investigated public funding. The study aims to shed light on the development of funding from the early 1970s until 2017 (most recent data available) and provide a forecast for 2030 (based on a business-as-usual scenario). According to results, at the national level, public funding had a considerable and steady rise after the OPEC´s oil embargo in 1973, reaching a first peak in the mid-1980s. The authors predict that, according to the most recent trends, by 2030, these will surpass 200 million € annually. In comparison, EU funding has steadily increased since its inception in the late 1980s up until 2007, but its evolvement is distinctively different, evidencing high fluctuations. The cumulative stock is also examined. National sources outweigh EU programs by a factor of almost five, and the stock should surpass 7 billion € by 2030. Based on the analysis and related insights, recommendations are elaborated on how the development of funding could inform policy strategies and actions to support research and development for photovoltaic technology.

You have full access to this open access chapter, Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Why is facilitating investment into research and development of the photovoltaics (PV) sector important for the EU? Renewable energy sources have an important role to play at the global level—not only in Europe. This refers first to the positive effect they have on lowering CO2 (and other greenhouse gas) emissions, which in turn then has a direct effect on fighting global warming, and second to the contribution they make to a more diversified energy mix, as well as energy security and independence (El-Agraa 2017). The EU has set ambitious climate and energy targets to be achieved by 2030 (EC 2018a), and electricity generation through PV can help in meeting those targets by contributing attributes like: scalability of solar parks; vast availability of raw materials; easy installation; simplicity of operation; and the low maintenance costs of PV plants (Twidell et al. 2006).

Europe has been at the top in terms of technology innovation for PV for decades (EC 2017a), providing important support for creating the necessary conditions that make PV nowadays a feasible electricity production alternative (Popp 2006; Gallaher et al. 2012). The combination of cost reduction, increased international competitiveness and continuous technological innovation (IRENA 2017) has enabled the accelerated growth of PV capacity in the EU since 2007 (Fig. 1). This growth coincided with a growing market and an increase in electricity consumption in the EU of about 24% from 1990 to 2016 (EC 2018b), resulting in a year-over-year increase of approximately 0.84%. The trend is in part driven by the growing appetite of the European population to increase its level of comfort by using electrical devices, which at the same time can be highly energy intensive (Pezzutto et al. 2016) and to partly offset energy efficiency improvements (EC 2012a).

Installed PV capacity (GW) in the EU, yearly (blue) and accumulated (yellow) (IRENA 2019)

To enable the transition to a higher use of PV, public investments in research and development (R&D) is a priority. The resulting innovation also contributes to the affordability and access to critical technologies (Mission Innovation 2015) and helps to bridge the gap between theoretical studies and commercial deployments and attracts private investments by de-risking technology (EC 2019a). Exemplary publications that emphasize the importance of R&D toward the development of renewable energy sources (RES) and thus meeting named targets until 2030 are among others: the Energy Roadmap 2050 (EC 2012b); the European Strategic Energy Technology Plan (SET-Plan 2017); and the European Energy Security Strategy (EC 2014). Except for the Mission Innovation initiative, which specifically stipulates that members will double their clean energy R&D investment by 2021, other publications do not provide any specific quantitative targets on PV R&D in order to meet the 2030 climate and energy targets. To potentially inform the development of such targets, as an initial step, this study focuses on tracking all public investments made in the EU, plus Norway and Turkey (Iceland and Switzerland have not been taken into consideration because they are not members of the SET-Plan PV Temporary Working Group (Hünnekes et al. 2017), aiming to address these research questions:

-

1.

What level of PV R&D funding has been provided so far by countries covered by the study, and how much is expected in the next decade?

-

2.

What is the difference between the national and European level of funding?

-

3.

What level of cumulative funding stock can be expected by 2030?

2 Materials and Methods

At the beginning of this study, a thorough analysis of the sources of public funding for PV R&D provided by Member States (MS), plus Norway and Turkey and by the EU, has been carried out, to answer the research questions just listed. With regard to questions 1 and 2 on funding at the national level, the International Energy Agency’s (IEA) database was used as the main source (IEA 2019a). A comprehensive database including nominal values of PV R&D funding was then assembled, including inputs that date back to 1974. To adjust these values to 2018 prices, EU inflation values from the International Monetary Fund (IMF 2018) have been applied to ensure consistency throughout the analysis. To gain further input to question 2, a considerable number of EU funding programs were screened. However, when analyzing those more in depth, immediately a highly unequal distribution of share became evident. The European Framework Programs for Research and Innovation have historically represented the largest individual sources of funding. The most recent one—Horizon 2020—provides for approximately 85% of PV R&D funding. Accordingly, the Community Research and Development Information Service (CORDIS) database was used as the main source of information for EU funding (EC 2019). Using all the historical data collected with regard to questions 1 and 2, adjusted to 2018 prices, a future scenario (Business as usual (BAU), please see Sect. 2.2) for each case (national and EU funding) was produced, to answer question 3. These scenarios estimate both the annual and accumulated funding stock until 2030.

It needs to be noted that, according to metadata specifications provided by the IEA (2020), the possible overlap between national and EU R&D funding is reduced to a minimum. Data are submitted by national institutions, such as ministries and agencies, which in dedicated country notes outline related considerations and measures to avoid double counting. However, overlaps cannot be completely excluded.

The following sections provide further insights into methodological considerations with regard to data sources, scenarios development and cumulative funding stock calculations.

2.1 Photovoltaic Research and Development Funding at National and European Union Levels

The IEA R&D data service provides data on funding from EU MS, plus Turkey and Norway, provided in real values from 1974 onwards (IEA 2019b). The EU Research and Innovation funding programs—FP1 to H2020, spanning from 1984 to 2020—are the main arm of funding for R&D, in the respect that they provide the largest share of resources (Bointner 2016a). Analysis of historic R&D funding can be found in multiple publications and reports such as the World Economic Council’s (WEC) Annex I (Valdalbero 2010) and from the EU/EC (EC 2009; EC 2015a; European Parliament 2015; EC 2017b).

The database constructed is vast, enabling the quantification of public PV R&D funding of the parties under scrutiny, and it appears to be the single source comprising a time series since the 1970s. Individual project information is available for FP6, FP7 and H2020.

2.2 Scenarios for Public Research and Development Investment Until 2030

The BAU scenario presumes that the ongoing trend of R&D funding based on historical values will continue its performance in the coming years. This entails that no major changes that could have an important impact on the estimations, especially those related to energy policy, will occur in the near future. The reason for creating a BAU scenario is to anticipate future R&D developments taking into consideration the current situation in Europe. The BAU scenario results are likely to be suitable also because the probability that all participants under examination radically change their energy R&D policies is very low, and, even if one contributor does indeed make important changes, the impact this may have on the overall picture is of minor consequence.

2.3 Cumulative Funding Stock for Photovoltaics

To neutralize the fluctuating nature of R&D funding, the cumulative funding stock is introduced, ensuring more stability and predictability and also enabling the possibility to calculate a highly reliable linear-regression equation based on historic data. It contains the year-to-year sum of R&D funding from 1974 to 2017. As in the other cases, a forecast represented in an accumulated form until 2030 is presented.

2.4 Literature Appraisal and Methodology Review

By using the IEA R&D database, some limitations arise, starting with the fact that not all EU MS participate in the IEA (Croatia, Bulgaria, Lithuania, Cyprus, Latvia, Romania, Malta, and Slovenia do not), and those that actually are a part do not always provide annual data (EC 2015b). There were no adjustments made to the original database for missing entries in the form of ‘gap filling’ or similar methodologies. Nevertheless, according to Wiesenthal et al. (2012), out of the entirety of R&D funding, IEA member countries account for almost 100%, so the missing MS contribution is safely considered as negligible. As for the EC, since funding is done through programs, the earliest data available is from 1987.

3 Results

The outcomes are divided into four sections: (Sect. 3.1) funding provided at national level; (Sect. 3.2) funding provided by the EU; (Sect. 3.3) the sum of both sources; and finally (Sect. 3.4) a snapshot of the cumulative funding stock.

As for going beyond the scope of this paper, the results are presented at an aggregated level and not at national/regional levels and have not been indicated as a percentage of GDP. A more in-depth discussion is expected to occur in any follow-up publications.

3.1 National Level: European Union Member States Plus Norway and Turkey

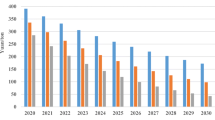

Figure 2 shows the annual investments made in PV R&D at the national level (EU MS plus Norway and Turkey) from 1974 to 2030. From 2018 to 2030, the expected BAU scenario is based on historic data. In the aftermath of the Yom Kippur war (1973), the Organization of Petroleum Exporting Countries (OPEC) proclaimed an oil embargo that abruptly disrupted the global price of oil, which subsequently skyrocketed. Consequently, European countries found themselves very much exposed reliance on foreign supplies, and new and alternative ways of securing the much needed energy resources had to be procured. This marked the beginning of PV R&D funding in 1974. Not long after that, in 1979, another oil crisis took place with the advent of the Iranian revolution, mirrored by a subsequent spike in funding (as seen in Fig. 2) reaching more than 200 million € in 1984. The initial years of PV R&D funding are characterized by their high volatility, very much like oil prices. So, it is not surprising that the following period up until the early 2000s has shown greater stability, similar to the performance of oil prices. A second distinct period becomes apparent from 2005 onwards. It is characterized by a strong and sustained increment in funding, also linked to a lesser correlation and decoupling from oil prices and increasingly influenced by stricter policies to comply with climate and energy targets (Bointner 2016b).

Photovoltaics research and development investment of the European Union Member States plus Norway and Turkey. Period: 1974–2017 and projected funding until 2030 (million. €, BAU scenario, 2018 exchange rates and prices). The orange vertical line indicates the year from which the forecasted values are displayed—the same applies to following charts

3.2 European Union

Figure 3 shows the annual investments made in PV R&D at the EU level from 1987 until 2030. From 2018 to 2030, the expected BAU scenario is based on historical data. At first glance, it is discernible that the scale of investments is much lower than at the national level. The accumulated values are almost five times lower, averaging in the same timeframe around 25 million € at the EU level and 125 million € at the national level. Another clearly distinctive characteristic is the constant fluctuation of investments across the years (Baccini and Urpelainen 2012). The funding scheme of the EU is based on the implementation of FPs, which have short durations and whose objectives are rethought and reshaped at the beginning of each cycle, meaning there is a natural progression within each program’s duration from less to more. This situation explains why, in the years 2003 and 2014 (each time at the beginning of a new FP), funding drops to almost 0 € and then quickly recovers. Funding is expected to remain constant at 2017 levels until 2030—around 35 million € a year, though it can be assumed that a funding drop will occur linked to the duration of the next program, Horizon Europe (2021–2027).

Photovoltaics research and development investment of the European Union. Period: 1987 to 2017 and projected funding until 2030 (million €, BAU scenario, 2018 exchange rates and prices)

3.3 National and European Union Levels

When both values for Figs. 2 and 3 are summed up, a set of data emerges as displayed in Fig. 4.

Photovoltaics research and development investment of the European Union Member States plus Norway and Turkey and the European Union. Period: 1987–2017 and projected funding until 2030 (million. €, BAU scenario, 2018 exchange rates and prices)

As previously mentioned, since the national funding is almost five times larger, when adding the funding amounts coming from EU programs, there is not much divergence from what Fig. 2 displays. Moreover, less fluctuations occur from one year to the next, progressing in a smoother way. The year with the highest peak of funding is 2009 (nearly 230 million €), though a new record is expected for 2030, reaching a maximum of 260 million €.

3.4 Cumulative Funding Stock

Results regarding the cumulative funding stock until 2013 are provided in Figs. 5, 6 and 7.

Cumulative funding stock for photovoltaics originated from research and development investment of the European Union Member States plus Norway and Turkey (million €, BAU scenario, 2018 exchange rates and prices)

Cumulative funding stock for photovoltaics originated from research and development investment of the European Union (Mln. €, BAU scenario, 2018 exchange rates and prices)

Accumulated funding for photovoltaics originated from research and development investment of the European Union Member States plus Norway and Turkey and at the European Union level (million €, BAU scenario, 2018 exchange rates and prices)

Figure 5 shows data of PV R&D funding in 1987 to amount to 1 billion. €, taking into consideration historic funding at the national level starting more than a decade before. Since then, the cumulative funding stock has grown steadily at almost the same pace until 2004. Afterward, the figure shows an accelerated growth, and an all-time maximum of 4.9 billion € is achieved in 2017, paving the way to the expected mark of 5.9 billion € by 2030.

Figure 6 shows the cumulative funding stock induced by R&D expenditures at EU level until 2030.

The chart follows a different pattern than Fig. 5. Due to the highly fluctuating nature of the EU R&D funding, two distinct flatter areas can be identified at the beginning of the 1990s and during the mid-2000s, which match the periods of funding lack seen in Fig. 3. In 2017, the funding stock reached 800 million €, and by 2030, it is expected to surpass 1.1 billion €.

Finally, Fig. 7 displays the sum of monetary indications given in previous Figs. 5 and 6.

The situation is similar to the one in Fig. 4, where the resulting trend is highly influenced by the higher relevance of national investments. Also, in this case, the higher fluctuations are softened, and the trend is shaped more linearly, but still an inflection point can be noticed in 2004, just as in Fig. 5. The year 2017 totals 5.7 billion €, while the expected amount of accumulated funding is 7.3 billion € by 2030.

4 Discussion

The provided results over three to four decades indicate how PV R&D funding has been highly sensitive to world events with an impact on the energy markets, resulting in the exploration of alternative means of production. Originally forced by the energy crises in the 1970s, the EU quickly sought alternative sources to achieve energy security and found a momentarily effective solution in nuclear power (Bointner 2016b). However, as the market cooled down in subsequent years and the cold war came to an end, a lower necessity to explore substitutes to traditional energy sources emerged, as the world economy thrived thanks to cheap and abundant fossil fuels from new markets. Thus, the political will to advance on the subject dwindled down. During this period, a stagnation in PV R&D occurred, so when a policy shift started in the EU in the 1990s, the funding had to be considerably increased. Largely due to the signing of international agreements (Rio ’92, Kyoto ’97, Cancun ’10, Paris ’15), a growing number of natural disasters linked to a changing climate (Fang et al. 2019) and later on fueled by Fukushima’s 2011 nuclear disaster in Japan (Goebel et al. 2015), the notion of energy security became more renewable energy inclusive, encompassing also climate change and security concerns. Furthermore, a growing population with an appetite for energy intensive devices that provide higher living comfort (Pezzutto et al. 2019) create pressure on demand that is only partly offset with increasing efficiency levels for buildings and appliances. RES and as such PV technology partially provide a solution to these problems, particularly, as the EU agreed to comply with stricter climate and energy targets for 2030 and 2050 and their likely upward revision due to a dire necessity to keep global warming at lower values (EC 2019c).

Since the late 2000s, PV has experienced a dramatic price drop to date (Wang and Barnett 2019), but it has been largely due to economies of scale. Installed capacity grows by giant leaps each year (IRENA 2019), so PV R&D has become fundamental to enable developments that make possible fully unleashing the potential of the technology. To accomplish an efficient allocation of resources and prevent the duplication of research, the EU should take a comprehensive approach to fostering knowledge transfer and joint initiatives, as well as developing policies that make financing provided for the sector more transparent.

5 Conclusions

The results illustrate how, within the past three to four decades, PV R&D funding from the MS, Turkey and Norway is almost five times higher than that provided at the EU level. Considering the size of the EU budget and its approach to technological neutrality, this is not surprising, although it highlights the importance of improving the effectiveness by combining EU and Member State efforts. More importantly, in contrast to national funding, EU expenditures are characterized by high and repeated fluctuations. This makes it difficult to forecast annual values—especially when the ending of the funding program occurs. It also puts into question whether the investments can be considered sufficiently steady. Overall, national and EU R&D funding for PV are expected to reach an all-time maximum value of about 260 million € in 2030.

In light of growing PV R&D funding (national and at EU level) over the past 30–40 years, the expected importance of this type of RES in contributing to climate and energy objectives set for 2030 becomes evident. Sufficient public expenditures for PV will be fundamental to preserve and increase the impact of such a crucial technology. In this sense, a constant and less fluctuating funding provision for PV R&D would be of advantage, lowering the possibility of knowledge loss, as well as achieving innovation more efficiently and effectively.

Finally, it has to be highlighted that R&D is key to the generation of innovation, which in turn nourishes economic and social growth. Hence, in light of potential upcoming economic crisis, an adequate funding provision for such a relevant RES sector can be considered of high importance to the EU and its MS.

References

Baccini L, Urpelainen J (2012) Legislative fractionalization and partisan shifts to the left increase the volatility of public energy R & D expenditures. Energy Policy 46:49–57

Bointner R, Pezzutto S, Sparber W (2016) Scenarios of public energy research and development expenditures: financing energy innovation in Europe. WIREs Energy Environ 5:470–488

Bointner R, Pezzutto S, Grilli G, Sparber W (2016) Financing innovations for the renewable energy transition in Europe. Energies 9(12):990

Di Valdalbero D (2010) The power of science: economic research and European decision-making: the case of energy and environment policies

EC (2012b) Energy roadmap 2050

EC (2009) Evaluation of the sixth framework programmes for research and technological development 2002–2006

EC (2012a) Energy efficiency directive. Accessed 30 July 2019, from https://ec.europa.eu/energy/en/topics/energy-efficiency/energy-efficiency-directive

EC (2014) European energy security strategy

EC (2015a) Ex-post-evaluation of the 7th EU Framework Programme (2007–2013)

EC (2015b) Capacity mapping: R&D investment in SET-Plan technologies

EC (2017a) Overview of EU funds for research and innovation. Accessed 5 Aug 2019 from https://ec.europa.eu/eurostat/statistics-explained/index.php/Europe_2020_indicators_-_R%26D_and_innovation.

EC (2017b) SET-Plan TWP implementation plan final draft

EC (2018a) 2030 climate & energy framework. Accessed 30 July 2019, from https://ec.europa.eu/clima/policies/strategies/2030_en

EC (2018b) Energy, transport and environment indicators

EC (2019a) Fourth report on the State of the Energy Union

EC (2019b) EU open data portal. Accessed 17 June 2019, from https://data.europa.eu/euodp/en/data/dataset?vocab_concepts_eurovoc=eurovoc.europa.eu

EC (2019c) Revision for phase 4 (2021–2030). Accessed 7 August 2019 from https://ec.europa.eu/clima/policies/ets/revision_en

El-Agraa A (2017) The European Union: economics and policies

Fang J, Lau CKM, Lu Z, Wu W, Zhu L (2019) Natural disasters, climate change, and their impact on inclusive wealth in G20 countries. Environ Sci Pollut Res Int 26(2):1455–1463

Gallaher M, Link A, O’Connor A (2012) Public investments in energy technology. Edward Elgar Publishing, Northampton

Goebel J, Krekel G, Tiefenbach T, Ziebarth N (2015) How natural disasters can affect environmental concerns, risk aversion, and even politics: evidence from Fukushima and three European countries. J Popul Econ: Int Res Econ Popul Househ Human Resour 28(4):1137–1180

Goksin K, McNerney J, Trancik J (2016) Evaluating the causes of cost reduction in photovoltaic modules. Energy Policy 123(2018):700–710

Goksin K, McNerney J, Trancik J (2017) Evaluating the causes of cost reduction in photovoltaic modules. Energy Policy 123:700–710

Hünnekes C, Sinke W, Belloni F (2017) Implementation plan of the PV temporary working group

IEA (2019a) Statistics data browser. Accessed 17 June 2019 from https://www.iea.org/statistics/?country=WORLD&year=2016&category=Energy%20supply&indicator=TPESbySource&mode=chart&dataTable=BALANCE

IEA (2019b) R&D online data service. Accessed 1 Aug 2019 from https://www.iea.org/statistics/RDDonlinedataservice/

IEA (2020) Energy technology RD&D budgets database documentation. Accessed 12 May 2020 from https://iea.blob.core.windows.net/assets/93e91574-f4d8-47a9-b70d-8e150623734f/RDD_Documentation.pdf

IMF (2018) IMF database. Accessed 17 June 2019 from https://www.imf.org/external/%0bpubs/ft/weo/2013/02/weodata/weorept.aspx?sy=1987&ey=2017&scsm=1&ssd=1&sort=country&ds=.&br=1&pr1.x=53&pr1.y=11&c=998&s=PCPIPCH&grp=1&a=1

Mission Innovation (2015) Joint statement. Accessed 30 July 2019 from https://mission-innovation.net/about-mi/overview/joint-launch-statement/

IRENA (2017) Renewable power generation costs in 2017

IRENA (2019) Trends in renewable energy. Accessed 7 Aug 2019 from https://public.tableau.com/views/IRENARETimeSeries/Charts?:embed=y&:showVizHome=no&publish=yes&:toolbar=no

European Parliament (2015) Overview of EU Funds for research and innovation

Pezzutto S, Fazeli R, De Felice M, Sparber W (2016) Future development of the air-conditioning market in Europe: an outlook until 2020. WIREs Energy Environ 5:649–669

Pezzutto S, Croce S, Zambotti S, Kranzl L, Novelli A, Zambelli P (2019) Assessment of the space heating and domestic hot water market in Europe—open data and results. Energies 12(9):1760

Popp D (2006) Innovation in climate policy models: implementing lessons from the economics of R&D. Energy Econ 28:596–609

SET-Plan (2017) At the heart of energy research and innovation

Twidell J, Weir T, Weir A (2006) Renewable energy resources. Routledge

Wang X, Barnett A (2019) The evolving value of photovoltaic module efficiency. Appl Sci 9(1227):2019

Wiesenthal T, Leduca G, Haegeman K, Schwarz HG (2012) Bottom-up estimation of industrial and public R&D investment by technology in support of policy-making: the case of selected low-carbon energy technologies. Res Policy 41(1):116–131

Acknowledgements

The research leading to these results has received funding from the Horizon 2020 program, under Grant Agreement number 842547; Project name: Actual execution of the Implementation Plan for Photovoltaics and monitoring the Implementation Plan’s delivery; Acronym: PV Impact. Moreover, we are thankful to our colleague Amy Segata (Eurac Research) for the elaboration of this study’s figures.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2021 The Author(s)

About this paper

Cite this paper

Pezzutto, S., De Negri, J.F., Gantioler, S., Moser, D., Sparber, W. (2021). Public Research and Development Funding for Photovoltaics in Europe—Past, Present, and Future. In: Bisello, A., Vettorato, D., Ludlow, D., Baranzelli, C. (eds) Smart and Sustainable Planning for Cities and Regions. SSPCR 2019. Green Energy and Technology. Springer, Cham. https://doi.org/10.1007/978-3-030-57764-3_8

Download citation

DOI: https://doi.org/10.1007/978-3-030-57764-3_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-57763-6

Online ISBN: 978-3-030-57764-3

eBook Packages: EnergyEnergy (R0)