Abstract

Energy supply goes through significant change as production and productivity evolve. When an energy revolution occurs it can drive social development and move society forward

DRC Team Lead of Special Report 1:

Wang Xiaoming from the Research Department of Industrial Economy, DRC of the State Council of China.

Shell Team Lead of Special Report 1:

Nie Shangyou and Professor Wang Yunshi from University of California, Davis, USA.

Contributors:

Guo Jiaofeng from DRC of the State Council of China; Liu Bing and Zhang Wenqiang from Shanghai AILNG Energy Technology Co., Ltd.; Shi Shude from the Research Department of Management and Consulting, State Grid Energy Research Institute Co., Ltd.; Yang Guang from the Energy Research Institute, National Development and Reform Commission; Li Jifeng from the State Information Center, Government of China; Zeng Ming, Wang Yuqing and Long Zhuhan from the North China Electric Power University, Beijing; and Feng Yujia from Tsinghua University, Beijing.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

1 Definition Implications of the Energy Revolution

1.1 Elements of the Energy Revolution

1.1.1 Defining the Energy Revolution

Energy supply goes through significant change as production and productivity evolve. When an energy revolution occurs it can drive social development and move society forward.

Scientists and research institutes define energy revolution differently. Here are four examples:

-

“The purpose of a revolution in energy production is to accelerate the transition away from fossil fuels to clean and low-carbon energy, and to accelerate the growth of nuclear energy, renewables and natural gas in the primary energy consumption mix in China.”Footnote 1

-

“The heart of the energy revolution is to improve efficiency and societal benefits. Restrictions limiting environmental impacts should be the red lines for energy development and investment to enable a clean and low-carbon energy economy to thrive.”Footnote 2

-

“The energy revolution makes fundamental changes to the energy mix and energy industry. The excessively high cost of developing and using the predominant types of primary energy, and the mismatch between the benefits they provide and the negative impacts they make, drive innovation and the substitution of new energy carriers for old ones.”Footnote 3

-

“Energy revolution is the evolution of the energy system by society. Unlike social and political revolutions, energy revolution is evolutionary. When the existing energy system can no longer adapt to social and economic change, a new energy system is required to replace it. This triggers transformation in supply and demand, including significant change in energy resources, technologies, management and public perception. The current energy revolution is adopting a scientific approach to energy use and replacing the conventional energy system with one that is efficient, clean, low-carbon and smart to help drive society forward.”Footnote 4

At the 6th meeting of the Central Leading Group for Financial and Economic Affairs in June 2014, President Xi launched his Four Types of Energy Revolution and One Cooperation as the new energy strategy for China’s energy security and development. This strategy requires a revolution in energy demand to curb unreasonable consumption; a revolution in energy supply to develop a diversified supply system of multiple sources; a revolution in energy technology to stimulate innovation and modernisation; a revolution in the energy system to fast-track development; and strengthening international cooperation to guarantee energy security. President Xi made clear that whichever definition is adopted, energy revolution is a combination of energy supply diversification, energy demand changes, energy technology advances, energy system innovations and far-reaching changes in the global energy landscape.

1.1.2 Definition and Elements of the Energy Supply Revolution

China’s energy revolution is a significant attempt to accelerate the energy transition, guarantee national energy security, meet the nation’s demand for energy, improve energy efficiency and combat global climate change. Some researchers have proposedFootnote 5 that this involves optimising the energy mix, reducing the use of coal and coal’s share in primary energy consumption, and developing a modern energy supply system that is efficient, clean, low-carbon and diversified. To understand the elements of the energy revolution, the following three factors need to be taken into consideration:

(1) The energy supply revolution will be a revolution in the true sense of the word

Revolution implies the transition from something old to something new, triggered by fundamental change. There are many factors that may cause an energy revolution, such as technological advances, changes in resource availability, environmental constraints or geopolitical disruptions. In the energy revolution, the old refers to the high-carbon and high-pollution energy supply structure dominated by coal and oil, while the new refers to a low-carbon, clean, diversified, stable and smart energy system. With regard to the objectives of energy revolutions, there are sharp differences between countries. China, for example, has an abundance of coal and a shortage of oil and gas. Despite recent technical advances, the economic feasibility of renewable energy still falls far behind fossil fuels. Therefore, in addition to focusing on renewables in its energy revolution, China also needs to attach great importance to the clean and efficient use of coal.

Energy revolution also implies fundamental change in energy supply. This does not happen overnight, but systematically and gradually in politics, technology, the economy and the environment. It is, therefore, important to weigh the pros and cons of each factor to understand its role in the energy revolution.

(2) The energy supply revolution will lead to major changes in the supply chain

Revolution can optimise the effectiveness and flexibility of supply and increase the share of high-quality energy in the mix to better meet demand and change the way energy is used. Optimisation helps remove obstacles to technological advances and encourages system innovations, driving the energy revolution forward. A revolution in supply is a cornerstone of the broader energy revolution. But it needs to be supported by similar revolutions in consumption, technology, demand and the energy system itself.

(3) The aim of the energy supply revolution is to combat climate change, meet demand and guarantee energy security

The most important role of the energy revolution is to meet the demand for energy and improve people’s quality of life, while combating global climate change. In the transition from high-carbon to low-carbon energy, the energy revolution focuses on the supply of cleaner conventional energy and the development of renewable energy. This will enable energy supply to match demand more effectively and adapt to change more flexibly.

The energy revolution aims for energy security. Close to 70% of China’s energy comes from coal, which makes China the country suffering the most from coal-smoke pollution and the world’s largest greenhouse gas emitter. As a result, China shoulders increasing pressure from the international community to reduce its emissions. As the scramble for oil and gas intensifies, the difficulty of accessing resources in international markets is mounting. China’s oil imports are surging, around 80% of which come from the Middle East and North Africa. Such a high dependency on one region, in combination with a lack of strategic oil reserve capacity, weakens China’s ability to respond to emergencies. A weak emergency response system increases the risk of long-term dependency on international oil resources. The energy revolution must therefore focus on China’s specific conditions and aim to ensure energy security.

1.1.3 Implications of the Energy Revolution for China

At the 6th meeting of the Central Leading Group for Financial and Economic Affairs in 2014, President Xi defined the specific requirements of the energy revolution: to develop a diversified energy supply system; create a diversified domestic supply system to ensure energy security; vigorously promote clean and efficient coal use; focus on more non-coal energy supply sources to develop an energy supply system based on coal, oil and gas, nuclear power and renewable energy; strengthen the power transmission and distribution systems; and build energy storage facilities.

These requirements reflect China’s actual conditions. China has many challenges to address, including excess capacity in fossil energy (mainly coal), insufficient supplies of renewable energy, intense environmental constraints, and severe defects in the energy supply system. Alleviation of excess capacity in the coal sector, optimisation of the energy supply system, and robust development of clean energy are, therefore, high on the energy revolution agenda.

1.2 Characteristics of the Energy Revolution

1.2.1 Key Characteristics

(1) Changes in primary energy

(1) Fossil fuels

Fossil fuels include coal, oil and gas. Coal mining and coal utilisation technologies are relatively mature, but due to high levels of pollution coal’s share of the energy mix will decrease dramatically as the energy revolution moves forward. In the future, clean coal mining technologies will be widely deployed to enable scientific and efficient exploitation, and investments in safety will also increase. This will enable the cost-effective and safe exploitation of coal resources.

China has limited proven resources of conventional oil and gas. There is great potential for unconventional oil and gas in China. However, due to the limitations of technology and other factors, the utilisation rate of unconventional oil and gas remains low. The energy revolution, therefore, needs to shift to more unconventional oil and gas, deep-sea and deep-shale oil and gas resources. It needs to accelerate the exploration and production of shale gas and coalbed methane through technology intensification and innovation, and it needs to promote a low-cost, clean and green energy strategy.

(2) Non-fossil energy

Non-fossil energy includes renewables and nuclear power. The strategy of the energy revolution for renewables is as follows:

-

(1)

hydropower—construct a fleet of hydropower plants, as planned, that comply with stringent environmental protection standards, as the ecologic protection redline should never be crossed;

-

(2)

wind power—develop a wind power control and management system that fulfils the requirements of large-scale grid connection, improve equipment quality, establish a sector-specific mechanism to remove inefficiency, and construct support facilities like energy storage;

-

(3)

solar power—build solar power plants in the north-west desert region of China and grid-connected rooftop solar power in east and central China to ensure the development of complementary solar energy technologies;

-

(4)

bioenergy—increase R&D investment in non-grain biofuels to replace petroleum fuel with liquid biofuels at scale in several industries; and

-

(5)

heating—deploy proven solar, biomass and geothermal energy technologies in heating applications. The pace of solar and wind energy development should match the speed of the energy transition to prevent excessive capacity build-up.

In nuclear, China should increase investment in nuclear power stations in the eastern coastal region, create Chinese nuclear power technology brands and become a global centre for nuclear power plant development and manufacturing.

(2) Changes in secondary energy

(1) Transition from primary to secondary energy

The energy revolution increases the share of electricity (from fossil fuels and renewables) in the energy mix. As electricity’s share increases, and the proportion of non-fossil energy use rises, the power supply system becomes cleaner and more efficient. Power consumption in the service industry and households will increase, while that in manufacturing gradually decreases.

(2) Combination of centralised and distributed energy systems

China has adopted a centralised approach to energy supply and demand, which will remain dominant in China’s energy system for some time. Distributed energy systems provide less power per generating unit and much lower generating efficiency than centralised energy systems. However, their flexibility and environment-friendliness make them an important means of addressing pollution and energy shortage. As such, they are indispensable to the energy revolution and integral to China’s future energy system. An optimal combination of centralised and distributed energy systems would guarantee a stable and efficient supply of energy and optimise China’s energy mix.

1.2.2 Drivers

(1) Less pressure on global energy supply

Growth in global energy demand is slowing down. Influenced by the shale gas revolution in the USA, some Latin American countries are developing their domestic oil and gas resources and have made clear progress to reduce their dependency on imports from other states. This eases the pressure on global supply and demand and encourages countries to diversify their energy supply. As the share of renewable energy grows globally, diversified energy supply will become an irreversible trend.

(2) Opportunities in the energy revolution

At the opening ceremony of the 2018 Summer Davos Forum, Li Keqiang, Premier of China’s State Council, said the Chinese economy is at a crucial stage of transition, from old to new growth drivers. It is faced with structural contradictions and downward pressure in several regions and industries. However, opportunities coexist with challenges. In the energy industry, China continues to implement its Internet + strategy and roll out the Energy Internet which, by integrating the energy industry with digitalisation, boosts innovation and new energy forms and revitalises energy supply. Natural gas, a clean energy carrier, is another of China’s energy priorities. China’s proven gas reserves are increasing rapidly, and exploration of natural gas hydrates has achieved major breakthroughs. As technology and innovation advance, natural gas has great potential to partly replace coal and oil.

(3) Environmental constraints are driving the energy revolution

As Wang Jinnan, Vice Director and Chief Engineer of the Chinese Academy for Environmental Planning points out, China tops the world in terms of emissions of almost all air pollutants, including carbon dioxide. Despite measures to control and prevent pollution, thick haze often hangs over large parts of China. Along with almost 200 other signatories, China ratified the United Nations Framework Convention on Climate Change (UNFCCC) at the 2015 Paris Climate Conference, which took effect in December 2016. Air pollution is inextricably linked to energy supply. In the face of unprecedented pressure, the need to protect the environment forces the energy revolution to accelerate the transition to clean, low-carbon energy.

1.3 Evaluating the Energy Revolution

As energy production transits from coal to low carbon, the latter’s share of the energy mix becomes a key criterion for judging the success of the energy revolution. However, a revolution cannot be achieved overnight. Rather, it is an evolving process that takes place under certain conditions. It is influenced by specific factors and has significant impacts on energy supply in certain geographies. And it can create profound change over time. To decide whether the changes China is experiencing can be considered an energy supply revolution, we look at four countries that have undergone energy revolutions: the UK, France, Japan and Germany.

1.3.1 Energy Revolutions in Four Countries

The UK’s energy revolution started with the discovery of North Sea oil in the 1960s. In 1973, coal made up 84% of the country’s energy production and oil accounted for 44% of total energy consumption. As the production capacity of UK North Sea hydrocarbons expanded, the share of oil and gas in energy production and consumption rose rapidly, while that of coal decreased. By 1983, the UK was one of the world’s top 10 oil producing countries and an important oil and gas exporter across the globe. At a time when overall energy demand was stable, the share of gas in the energy mix increased rapidly in the UK, becoming a major alternative to coal.

Japan’s energy revolution can be clearly divided into three stages based on energy mix share. Stage 1 is changes in the supply of primary energy to the power industry, reflected by a higher share for oil and a smaller share for coal. In 1973, the first oil crisis spurred a transition from oil to gas and nuclear power, which started stage 2 of Japan’s energy revolution. Use of gas in the energy mix grew from 1.6 to 19.2%, and that of nuclear power from 0.6 to 11.8%. Thanks to reduced costs and improvements in equipment efficiency, the use of coal rose from 16.9% to 22.6%. Following the Fukushima nuclear accident in 2011, Japan initiated stage 3 of its energy revolution by phasing out nuclear power.

In France, oil and coal made up a high share of the energy mix before the energy transition. As a result of the first oil shock, Prime Minister Pierre Messmer announced a large nuclear power development programme (the Messmer Plan) in 1974, which included 13 1,000-megawatt nuclear power plants. This not only completely changed France’s electricity sector, it made France a major force in nuclear power and related technologies. Currently, nuclear makes up 75% of total power output in France, which is a substantial contribution to France’s energy self-sufficiency.

Germany passed the Renewable Energy Sources Act in 2000, pioneering the transition from fossil fuels to renewable energy. Coal and nuclear power were the major sources of energy in Germany at that time. According to Stephan Kohler, former head of the German Energy Agency and director of the Center of Sino-German Renewable Energy Partnership, the goal of Germany’s energy transition is mainly to phase out nuclear power and fossil fuels by 2050. After the Fukushima disaster in 2011, the German government decided to shut down nuclear reactors permanently and make wind and solar power the basis of Germany’s future low-carbon energy system. As Stephan Kohler pointed out in 2000, 5% of Germany’s then energy consumption came from renewables, especially hydropower. By the end of 2016, this had risen to 33%, with solar power especially registering explosive growth.

1.3.2 Timelines of the Energy Revolutions

Starting with the discovery of North Sea oil in 1968, the UK’s natural gas revolution can be divided into two stages. In stage 1 from 1968 to 1990, the supply of natural gas grew dramatically. It was used mainly by households and industry, with a very small amount used for power generation. In 1991, a large gas field with sufficient reserves for 15 years was discovered along the North Sea coast, marking the outset of stage 2 of the UK’s energy revolution. The UK government increased the use of natural gas in power generation, which far exceeded that used by industry.

Japan’s energy revolution began in 1960. It is now going through its third energy transition. The first transition, from 1960–73, substituted oil for coal. As a result of the first oil crisis, Japan underwent a second transition, from oil to gas and nuclear power, from 1973–2011, which is the focus of this report. The third transition took place after the Fukushima disaster in 2011, when Japan started to phase out nuclear power.

The first oil crisis also triggered France’s transition to nuclear power from 1974. In June 2017, Nicolas Hulot, French energy and environment minister, announced that the government planned to shut down several nuclear reactors. The move was intended to decrease the share of nuclear power in total power output from 75% to 50%, but the timeline remained unclear.

In 2000, Germany embarked on a transition to renewable energy. In September 2010, the minister responsible for the Federal Ministry for Economic Affairs and Energy announced Germany’s medium- and long-term energy policies and identified the energy transition targets for 2050.

1.3.3 Pathway Options for Energy Revolution

The UK discovered North Sea oil when its domestic energy resources were scarce. The first oil crisis accelerated drilling and exploitation in the North Sea and escalated the use of natural gas. The UK’s energy revolution was therefore driven by resource shock.

During the first oil crisis, oil prices soared and the cost of oil-fired power generation in France and Japan spiralled. High oil consumption and a lack of domestic resources forced the two countries to carry out an energy revolution. France has few oil, coal and gas resources, but relatively abundant uranium ore. France decided to transition to nuclear power, while Japan chose to replace oil with gas and nuclear power.

Germany spearheaded the transition from high-carbon to low-carbon energy to reduce air pollution from fossil fuels and to strengthen energy security. The transition to renewable energy is now a common trend in energy revolutions.

1.4 Pathways to Energy Revolution

1.4.1 Economic Development, Energy Security and Environmental Protection

According to the above analysis of energy revolutions in four countries, the UK, France and Japan sought an energy transition before and after the first oil crisis due to a lack of domestic energy resources. They needed to limit the potential impacts of an energy supply shortage on their economies and energy security. Germany’s energy supply revolution occurred relatively late. In addition to economic development and energy security, Germany also took environmental pollution from fossil fuels into consideration, and eventually decided to point its energy revolution towards renewable energy.

All four energy revolutions targeted economic development, energy security and environmental protection. These same three factors apply to China’s energy revolution as well.

First, economic development is a permanent goal. China has many challenges that need to be urgently addressed, such as overpopulation, large income inequality and regional imbalances in economic development. The energy revolution can satisfy people’s energy demands and create high-tech and low-energy-consumption industries, bringing new employment opportunities. More jobs will reduce income inequality and regional development imbalances, helping to deliver the government’s goal of economic prosperity.

Second, the energy revolution can reduce China’s dependency on other countries for energy and lower potential supply risks, thus improving energy security.

Finally, the severe haze and air pollution challenges facing China are closely related to its underdeveloped energy system. In addition, pressure from the international community on greenhouse gas emissions makes environmental protection another goal of China’s energy revolution.

In recent years, as China’s economic development entered the new normal of lower growth rates, the energy industry also entered a new phase. China’s energy system is shifting from growth in quantity to a phase consistent with the new era of socialism with Chinese characteristics and China’s new normal economy. As new businesses start up, and energy technology innovation and deployment accelerate, the three factors of economic development, energy security and environmental protection become increasingly interdependent.

1.4.2 Scenarios for China’s Energy Revolution

The scenarios for China’s energy revolution are based on the following four factors.

First, in alignment with the government’s Chinese Dream strategy, China’s socioeconomic development scenario forecasts socioeconomic development and energy service demand for 2020, 2030 and 2050.

Second, in accordance with the Energy Supply and Consumption Revolution Strategy (2016–30) to forecast end-use energy demand and to analyse the possible and recommended pathway.

Third, we have conducted research on the impact on the energy supply system in three scenarios (High, Medium and Low) in which electricity and gas replace scattered coal and the Recommended and Limit scenarios in which electric vehicles replace internal combustion engines.

Fourth, we forecast China’s future primary energy supply in the Recommended scenario for its energy revolution pathway.

1.4.3 Outlook for China’s Energy Revolution and Scenario Analysis

China’s future population, floor space growth and trends in major industrial products are analysed to forecast China’s socioeconomic development and energy service demand in 2050. Energy consumption in agriculture, industry and buildings, transport, the service industry and households, is predicted in order to estimate future total end-use energy demand. The scenarios for replacing scattered coal and internal combustion engines are analysed to estimate electricity and natural gas consumption and total energy demand for vehicles in 2050.

A review of China’s socioeconomic development and energy service demand reveals that China’s population will peak by 2030. As the population ages, China’s future workforce will decline in absolute terms. China’s floor space is forecast to peak at about 92 billion cubic metres by 2040. The rapid expansion of the real-estate industry will come to an end, and its ability to stimulate economic growth will weaken. China’s automobile industry maintains strong momentum, but growth is expected to slow after 2030 due to gradual market saturation. Iron and steel output will fall in line with declining annual average floor space, and the steel recycling rate will gradually improve. The nonferrous metal industry will see continuous growth in energy consumption to 2030, and new building materials will gradually replace old ones. By 2030, China will achieve the government’s goal of “common prosperity” and avoid the middle-income trap of developing countries. In 2030, China’s GDP will exceed that of the USA, making it the world’s largest economy. In 2050, China’s economic growth will shift from production-driven to consumption-driven. As industrial restructuring accelerates, China’s GDP will reach and exceed the level of moderately developed countries.

In agriculture, machinery will be powered by electricity, especially by renewables and biofuels, instead of by fuel oil. Use of scattered coal will start to disappear. Energy use in industry and buildings is expected to peak in 2025–30, and then steadily decline. In iron and steel, as the mainstream technologies gradually shift to a more balanced use of long-term and short-term objectives, the use of coal will fall sharply and that of natural gas, electricity and heat increase significantly. In the transport sector, petrol, diesel and kerosene remain dominant, but the rate of replacing them with electricity, natural gas and biofuels will increase significantly. Energy consumption in transport will continue to grow to 2030, then slowly decline. Energy demand in the service industry will increase continuously throughout the period to 2050 and use of coal will decrease rapidly as the service industry modernises and replaces scattered coal with electricity and gas. Household electricity demand will remain steady.

In summary, China’s end-use energy demand will stay at peak level between 2030–50. Specifically, energy demand in agriculture, industry, building construction and transport will peak in 2020, 2025–30 and 2030–40 respectively. In the service and household sectors, peak energy demand will not be reached until 2050.

Three rate of change scenarios (Fast, Medium and Slow) are also analysed for substituting electricity and gas for scattered coal (SEGFSC). For the pathway for the electric vehicle sector, a recommended scenario and an extreme scenario (featuring accelerated development) are analysed, leading to energy demand forecasts for petrol, diesel and electricity.

In the Recommended scenario, the share of electricity in end-use energy demand rises steadily. In the SEGFSC and electric vehicle scenarios total energy consumption will decline, although not significantly, as electricity and gas are more efficient than coal and oil. This will increase demand for electricity and gas, but to a manageable extent. However, a rapid increase in the number of electric vehicles will boost demand for electricity. The power system will therefore require sufficient backup capacity or better demand-side management to meet this uncertainty.

In the Recommended scenario, electricity demand is divided into four segments—peak load and ancillary services, intermediate load, base load and distributed load. Clean power’s share of energy supply will gradually increase, wind and solar will rise rapidly, and nuclear power steadily. Gas-fired power generation’s share will remain around 10% in 2050, while hydropower’s will gradually decrease despite its growing generating capacity.

In the Recommended scenario, China’s total primary energy demand will continue to grow. Coal and oil will peak then decline. The share of non-coal in energy supply is expected to increase to 73% by 2050, whereas oil will rise then gradually fall as the scale of replacing the internal combustion engine with electric vehicles rapidly expands. Meanwhile, clean energy will gradually play a critical role in meeting energy demand. In addition, the rising rate of electrification will increase the share of power generation in energy supply.

1.5 Impacts of the Energy Revolution

The Recommended scenario analyses the impacts of the energy revolution on the following four aspects: energy supply, industry and capacity conversion, investment, and employment.

(1) The energy revolution changes the energy supply system by transforming production and innovating new energy supply technologies to safeguard national energy security. The shift in production from centralised generation to an optimal combination of centralised and distributed energy improves efficiency and encourages the development and use of clean energy. Technology advances are reflected in the development and deployment of the Energy Internet (Internet +). Internet + is a combination of complementary energy sources in an optimised mix of centralised grids and distributed energy networks that is low carbon and intelligent. With support from Energy Internet technologies, demand response becomes a crucial forcing mechanism to accelerate supply-side change and improve energy management. In the Recommended scenario, China’s energy imports will continue to rise in the short term, but as renewable energy and nuclear power advance, China’s dependency on energy imports will fall.

(2) The energy revolution drives change in the energy system and guides development of the energy industry. As coal will continue to dominate China’s short-term energy mix, low-carbon energy and clean coal should be the focus in the near future. The oil and gas sector will concentrate on innovating greener technologies and accelerating the exploitation of unconventional resources. China will make vigorous efforts to drive the development of clean energy. It will invest more in technology innovation to lower costs and improve energy efficiency. Power conversion will be cost-efficient, clean and green. It will replace fossil fuels with clean energy and increase the amount of electricity in end-use consumption.

(3) The energy revolution drives the energy industry to invest in clean energy and the cleaner use of fossil fuels. To deliver the energy strategy of a diversified supply system, the participation of various types of investor is needed.

(4) The energy revolution will make the structural imbalances in the labour market more severe. There will be more job opportunities for highly skilled people, but rising unemployment for those in the conventional energy sector. This applies to those regions and provinces that rely on conventional energy, less so on those developing new energy sectors. It may force some provinces to carry out an energy transition and reduce their dependence on conventional energy. So doing would spur their economy, ease unemployment and make for healthier and more stable development.

2 Precedents and Prospects of International Energy Revolutions

2.1 Energy Companies in Transition—Responses to Future Trends

2.1.1 Introduction

Strategies and organisational structures within the oil and gas industry are the result of historical market conditions that are likely to change over the coming decade. Oil and gas markets have traditionally been characterised by rising demand and prices. This has led companies to focus on megaprojects that require intense coordination. As a result, pyramid organisational structures with multiple levels of oversight have become the industry norm. However, the oil and gas industry faces large structural shifts that can affect its organisational and strategic structures in the future.

Specifically, two trends are likely to trigger change. First, structurally lower oil and gas prices are becoming increasingly likely. This is due to a combination of technology and policy that increases supply and reduces demand. Supply is increasing as horizontal drilling and hydraulic fracturing techniques are diffused and climate policies—together with energy efficiency improvements—curb demand. Second, technology disruptions in energy markets are becoming more likely. Digitalisation and innovations in decarbonisation will increasingly change how energy is produced and consumed, which will ultimately lead to changes in existing markets.

Oil and gas companies have already begun to adjust their strategies and organisational structures. The industry is currently characterised by two strategic themes. First, oil and gas companies, including Equinor, Total and Shell, have begun to invest in renewable energy technologies, such as solar and wind, to diversify their portfolios. Second, companies are shifting their hydrocarbon investments away from conventional mega-ventures towards smaller more flexible projects, such as shale wells, which can be scaled up or down in response to market changes. These strategic changes have been accompanied by organisational adjustments. New, smaller investments are more reliant on trial and error, agile local teams and rapid coordination. Recognising this, oil and gas companies like BP and ExxonMobil, are adopting flatter organisational structures that allow for greater local autonomy.

However, oil and gas companies are at the start of a long journey. It is, therefore, useful to study responses in comparable sectors that have faced similar structural shifts for longer. The postal and power sectors are good examples as they, like oil and gas, are heavily regulated, capital-intensive industries dominated by large state-owned enterprises. Furthermore, they have faced structural shifts similar to those expected in oil and gas. The postal industry has faced falling letter volumes in the past decade and companies in the sector have already adapted their organisational structures and strategies. Likewise, the electric utility sector can be seen as a frontrunner for oil and gas; it has long been challenged by large technology disruptions in the form of increasingly price competitive renewables. These parallels make postal and power companies’ useful cases for exploring future strategic and organisational changes in the oil and gas industry.

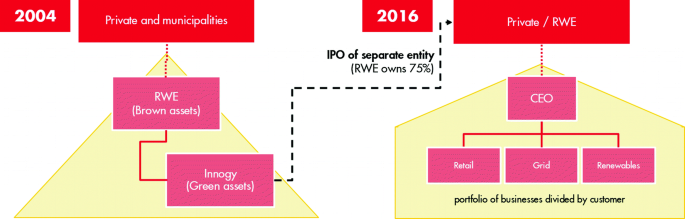

The postal and power cases show that company-specific motives and context can lead to different but rational strategic responses to the same structural shift. Some companies, such as United States Postal Service (USPS) and RWE (circa 2004), changed very little in response to structural shifts, while others, such as Deutsche Post and DONG Energy (now Ørsted), transformed or diversified their companies completely. Little strategic change was observed in situations where owners valued security of the existing service and nearer term profits. In the case of USPS and RWE in the early 2000s, their strategy was to harvest the short-term value of legacy assets. In companies, such as the UK’s Royal Mail—where stakeholders valued longer-term profitability but were constrained by regulation, conflicting interests or limited capital—business strategy focused on streamlining and redirecting resources to new capabilities. In cases where owners sought to expand the business, had relevant capabilities and sufficient capital, the strategic shift was more aggressive than for those acting later or facing resistance. As an example, both Deutsche Post and DONG Energy moved early and used rents from legacy activities to finance their strategic transformation to international logistics and offshore wind respectively. In contrast, late movers such as RWE and Innogy SE suffered from capital constraints, which slowed their strategic transition.

Organisational change needs to align with the adopted strategies and business models. In all our cases, companies started out with relatively hierarchical, top-down organisational structures. Where the strategic focus remained on the traditional business model, as with USPS and RWE, organisational change was limited to making the prevailing structure more effective. Where new business growth was the main priority, all companies first ensured some separation between new and old—this gave the new business sufficient autonomy to grow. Where new businesses had similar underlying characteristics to the traditional business, as with Royal Mail and DONG Energy, organisational change focused on reorienting the existing structure and flattening the hierarchy, but not on a radical shift to a horizontal structure. In contrast, radically new product or service models involved far-reaching organisational change. As Deutsche Post transformed from a German mail delivery firm to an international logistics company it also changed its organisational model. Notably, it shifted focus from production to consumers and organised itself around a series of relatively autonomous divisions supported by cross-cutting service divisions. Innogy’s split from RWE in 2016 resulted in a more radical turn towards business unit autonomy focused on customers, allowing a more agile shift in investment across units based on results.

Motive and context will likely determine how Chinese oil and gas companies respond to lower prices and new technology disruptions. Drawing on the postal and power cases, four archetypes of potential strategy response arise:

-

Supply security focused harvesters: These companies ensure supply security or near-term employment, and harvest value from legacy assets during the transition period. However, as was the case with USPS, they face the risk of shrinking considerably as the market changes around them.

-

Constrained niche growers: These companies have aspirations for growth, but regulation or capital constraints prevent them from moving beyond conventional oil and gas business areas. They focus on streamlining their core functions and growing within niche markets such as chemicals.

-

Dividing conquerors: Acknowledging the potential for misaligned internal incentives, these companies split into two with one focused on harvesting value from legacy hydrocarbon assets to deliver near-term supply security, dividends or employment, and the other focused on delivering long-term growth by developing new technologies or wider energy sector diversification.

-

Transformative diversifiers: In contrast to the above, these companies move quickly to a new energy service model, catalysing change and gradually selling off their least profitable legacy assets to finance the transition. They have the potential to deliver long-term growth but are riskier; supply security, employment and profitability outcomes are uncertain.

The different archetypes for oil and gas company strategy will be accompanied by several organisational considerations. Supply security focused harvesters will likely maintain a top-down approach with central control of big decisions. In contrast, constrained growers will have to enable agile decentralised units to efficiently capture niche markets. Their central functions will be focused on portfolio optimisation, as well as asset management and organisational efficiency. Companies that face significant internal cannibalisation between old and new business units will likely become dividing conquerors. Like Royal Mail and DONG Energy, these companies will strategically and operationally split, but could be managed as a conglomerate that carries over existing organisational strengths. Finally, transformative diversifiers will likely adopt more horizontal organisations structured around energy services rather than production. Like Deutsche Post, their organisations will likely be flatter with a series of relatively autonomous units supported by service divisions that leverage synergies across the group.

Motive and context are not set in stone but controlled by stakeholders, and the Chinese government can therefore shape strategic and organisational outcomes in its oil and gas industry. As the owner of national oil companies, the Chinese government can shift the motive driving strategic and organisational change. Supply security requirements could be lifted by reducing fixed reserve targets; incentives to maintain unproductive workers could be minimised by reducing local political oversight; and near-term profitability motives could be eased by adopting longer-term key performance indicators for managers. Furthermore, as a regulator and key stakeholder, the Chinese government influences the context in which oil and gas companies will respond to structurally lower prices and technology disruptions. For example, capacity development could be supported through public-private R&D schemes, regulatory constraints could be reduced by lifting natural monopolies, and capital limitations could be minimised by providing policy clarity (this would allow rents from legacy assets to be channelled sooner towards financing new investments). An important lesson from both the postal and power sectors is that the government is key in setting the conditions that determine strategic and organisational change. Policymakers who recognise this will be able to directly or indirectly shape the future of the Chinese oil and gas industry.

2.1.2 Future Trends in the Oil and Gas Industry

The oil and gas sector faces new trends that could induce change in business strategy and companies’ organisational structure. Trends have always arisen to create new challenges and opportunities in the oil and gas sector, as the discovery of new resources, technologies and political shocks have changed the fundamental characteristics of the market. For example, the emergence of powerful state-owned oil companies in the 1960s and 1970s forced many international oil companies to transform their business models to focus on megaprojects in hard-to-reach places. The future appears to hold even more substantial changes due to advances in technology and decarbonisation, which have already begun to affect energy markets and will become more prevalent over time. Oil and gas companies are already considering changing their strategies and organisational models in response to these trends and will need to continue to do so in the future.

This report focuses on the two main trends facing the oil and gas sector: (1) structurally lower oil and gas prices, and (2) an increasing set of disruptive technologies. The trend of structurally lower prices reduces margins and makes high-cost supply uncompetitive. It is already occurring, as new shale resources continue to increase supply, and is likely to strengthen as decarbonisation policies reduce fossil fuel use. Several technology disruptions are also impacting the sector, including those driven by digitalisation and increasing low-carbon R&D flows. These can rapidly shift value within the energy sector, which will require oil and gas companies to be more versatile if they are to capitalise on opportunities in areas of new value and avoid risks in areas of declining value. This report examines the broad impact of these shifts in business strategies, and the implications for future organisational change within oil and gas companies (Fig. 1).

Structural shifts will alter the business strategies and organisational structure of oil and gas companies

Companies will need to understand the implications of these trends and how to respond best to them in order to thrive. It is possible to draw parallels between the trends facing the oil and gas industry today and the trends that other sectors have already experienced and responded to. This report aims to use the learnings from cross-sectoral responses to better understand the possible set of strategic and organisational responses of oil and gas companies to structurally lower prices and increased technology disruption, as well as the factors that will affect those responses.

(1) Current strategies

Current strategies and organisational structures within the oil and gas industry have been shaped by historical market conditions. The main strategy employed in recent years has been the development and management of megaprojects with large volumes of recoverable resources: in 2005, 60% of oil production was from giant fields of more than 0.5 billion barrels of recoverable resources. This focus on quantity has been driven by the historical trends of growing demand and generally increasing, if fluctuating, prices, as seen in Fig. 2. Given these trends, replacement ratios have been of key importance for oil and gas companies, which have focused on accumulating reserves and been less concerned about the cost of extracting those reserves.

Note Giant fields are defined as having more than 0.5 billion barrels of recoverable resources. Source International Energy Agency, BP, Robelius (2007)

Megaprojects, and the pyramid organisational structure that facilitates them, have been motivated by historical trends.

Effectively deploying large, complex projects requires extensive coordination that has encouraged pyramid organisational structures with multiple layers of oversight. These megaprojects are technologically demanding and usually involve complex multiparty relationships, as well as high commercial and environmental risk. Given these features, a pyramid structure that allows for strong oversight is required to ensure all aspects of the project are under control and that coordination between them is achieved.

(2) Structurally lower prices

Rising supply from unconventional sources and plateauing demand make it likely that prices will remain lower for longer. Recent advances in drilling technology, such as hydraulic fracturing and horizontal drilling, have made new oil and gas resources available. This has shifted the global supply curve outwards, putting downward pressure on prices, and is likely to continue as these technologies are deployed globally.

The economic logic for this is described in Fig. 3, where a shift out of the supply curve and a contraction of the demand curve can lead to significantly reduced producer surplus, illustrated by the difference in size between the original red area of producer surplus and the new blue area. This is accentuated by the steepness of the global oil and gas supply curve at the higher levels of quantity—this means that a small fall in demand can cause the price and surplus to fall rapidly.

Source Vivid Economics

The trends of the oil and gas industry will likely result in significantly tighter margins for producers.

There have already been sharp falls in oil and gas prices in recent years, demonstrating the potential for structurally lower prices. The trend is already in place. Oil prices have been consistently around $50 per barrel since 2015, as US oil shale resources have contributed to a supply glut that has driven down prices to pre-2005 levels. The overall impact of this on oil and gas companies can be seen in their share price during and after the final quarter of 2014 in Fig. 4. The average share price of five major oil and gas companies fell by more than 30% from 2014 to the trough in 2016 and has yet to recover.

Source BP, Google Finance

The fall of oil prices in late 2014 coincided with sharp drops in the share price of major oil companies.

New, relatively low-cost supply sources are becoming increasingly available as technology improves, driving production above predicted levels. New technologies have reversed persistent declines in production and have exceeded historical expectations, as illustrated in Fig. 5. The U.S. Energy Information Administration (EIA) forecasts for oil production in both the 2002 and 2012 Annual Energy Outlook did not fully anticipate the impact that new fracking methods would have on increasing tight oil supply, as conventional oil production has continued to diminish. The result has been a near doubling of oil production from its trough in 2008 to its peak in 2015.

Note Total US oil production includes conventional and tight oil. Source EIA (2017)

New tight oil sources have pushed total US oil production to heights that exceeded forecasts.

The low-carbon transition will reduce demand for fossil fuels in favour of low-carbon alternatives over time. Decarbonisation has been an increasingly important priority in energy in recent years and now has widespread support, as demonstrated by the signing of the Paris Agreement in 2015. As a result, policies are in place globally to phase out fossil fuels and promote low-carbon energy sources. Figure 6 shows potential pathways for primary oil and gas demand in two EIA scenarios: a reference scenario that reflects the world’s announced decarbonisation policies and a 2-degree scenario (2DS), which assumes additional policies to limit global warming to 2°C. In the reference scenario, demand for oil and gas rises, but if additional policies are put in place to limit global warming to 2°C as intended, then demand for both oil and gas is expected to fall sharply in the future. This reduction in oil and gas demand due to decarbonisation will likely reduce prices, and so contribute to structurally lower prices.

Source IEA Energy Technology Perspectives 2017

Primary demand for oil and gas falls sharply under the IEA’s 2-degree scenario (2DS), presenting a challenge to the oil and gas sector.

In a future of structurally lower prices, the decision of whether to divest or diversify into new areas will gain greater importance. Oil and gas companies face the risk of lower margins in their main areas of operation. As a result, there may be value in pursuing strategies such as divesting or diversifying to attempt to maintain profits in the future. The potential strategy options and the factors that induce different types of responses are discussed in Sect. 2.1.3.

(3) Disruptive technologies

Disruptive technologies are shifting the sources of value in energy markets, driven by digitalisation and decarbonisation. Digitalisation is the automatic collection of large quantities of data and the application of computing power to the data to enable better decision-making. Its use in other (non-energy) sectors has driven rapid advances. Collecting big data with remote sensors is already prevalent in the oil and gas industry, and there is enormous potential for digitalisation in other areas of the energy system through smart technology that enables dynamic, autonomous energy systems. Decarbonisation policies have increased R&D spending (01.2.7) and raised market expectations about the long-term value of new innovation across various parts of the energy system. This has resulted in major advances, including those related to power generation (like wind and solar), oil and gas exploitation (floating liquefied natural gas and advanced seismic analysis for oil and gas exploration), and energy demand (electric vehicles and smart homes with demand-side response).

This has created opportunities and risks for the oil and gas sector. The impact of these technologies, whether marginal or revolutionary, will have repercussions on oil and gas companies. For example, sensors on drills are collecting masses of high-quality real-time geological data that allow for more cost-effective extraction. Smart grids can better coordinate decentralised variable generation and minimise curtailment rates—this makes renewables more productive and reduces the need for fossil fuel peaking plants to balance the energy system. And reductions in carbon capture and storage (CCS) costs could make the large-scale use of gas in power and industry low carbon (Fig. 7).

Source OECD

R&D is shifting towards new areas, increasing the potential for disruptive technologies to emerge.

(4) Initial responses

Oil and gas companies have started to adjust their strategies, shifting towards smaller-sized projects and investing in renewables. Structurally lower prices and technology disruption have already begun to appear and affect the oil and gas industry, driving initial responses. Some major companies have begun to integrate renewables into their portfolio to gain presence in a market that is rapidly growing, thanks to widespread policy incentives and improving renewable technologies—both Equinor and Total have made recent renewable energy investments. There has also been a shift away from the historical focus on megaprojects, as shown in Fig. 8. Investment in smaller fields has been consistently higher since 2009 and is expected to continue into the near future as flexible shale projects and lower extraction costs become increasingly prominent in a future of lower prices.

Source Rystad Energy, Bloomberg (2017)

Investment in smaller projects has been greater than investment in megaprojects since 2009.

These changes in strategy have also led to organisational adjustments—this has been prominent as companies have implemented more shale projects. Successful shale projects rely on a very different approach to that of megaprojects. Shale projects are smaller and far less complex but require trial and error and multiple iterations to be successful. This is more suited to a flatter organisational structure with agile, local teams and rapid coordination between business development and exploration divisions. Given this, large companies have tended to separate their shale operations into autonomous subsidiaries to preserve the flatter structure that makes them successful, rather than integrate them. This is just one example, but the expectation is that oil and gas companies will be faced with scenarios of a similar nature and possibly on a larger scale.

2.1.3 Case Studies of Responses in Other Sectors

(1) Introduction

The prevailing structural shifts that are facing oil and gas are not unique—other sectors have already experienced and responded to similar transitions. The postal sector has faced structurally lower demand since the early 2000s due to steadily declining letter volumes. Letters have historically been a major source of value, and their decline has had a severe impact on the financial performance of postal companies. Power generation utilities have faced disruptive technologies in the form of ever-cheaper renewable generation backed by favourable policies, impacting the profitability and longevity of their traditional assets.

Figure 9 shows the perspective we are taking for the case study analysis: structural shifts can lead to changes in business strategy, which then motivate change in organisational structure. The trends of lower prices and increasing technology disruptions have caused fundamental structural shifts in the postal and power utility sectors. Companies have employed a range of business strategies to respond to these trends and subsequently have often had to adjust their organisational structure to facilitate their new strategies. We analyse the response of each company at specific points in time to better understand the factors influencing their adoption of different strategies in response to similar sector-wide trends.

Source Vivid Economics

We study archetypical responses in comparable sectors to understand how oil and gas might change.

These cases provide examples of how the oil and gas industry can respond to trends, and what the outcomes of different responses may be. Studying other sectors that have experienced similar price and technology trends can help to guide the future strategy and organisational decisions of oil and gas companies. It provides an understanding of the potential consequences from different types of responses and the factors that motivate these responses, particularly when there is no clear dominant strategy for adapting to these structural shifts (Fig. 10).

Source Vivid Economics

Structural shifts lead to changes in business strategy, which in turn lead to changes in organisational structure—but the exact changes depend on motive and context.

(2) Motive and context framing

The cases show that company-specific motives and context can lead to a range of different but rational responses to the same structural shift. Companies can rationally have different strategy responses to the same trend if they face different decision factors, namely the motive of the owners and context of the company. For example, even if two companies have the same motives and overarching goals, the different regulatory environments each faces may force them to choose different strategies in response to a trend. The motive of a company is derived from the owners and broadly encompasses the desire to maintain service and employment security, the time preferences of cash flows (the weight placed on profit today versus profit in the future) and whether the risk preferences of the company are suitable to encourage expansion into new areas of value. The context of a company is the operational conditions that affect its ability to implement different strategies—this includes the regulation it faces, internal or external capital constraints, and the potential synergies between current business areas and future ventures.

We have analysed the different responses of three companies in each sector. Understanding the motive and context allows for the outcomes of each company’s response to be understood holistically and deeper parallels to be drawn to the potential future responses of the oil and gas industry.

Two companies demonstrate a relatively minimal response, with a continued focus on improving their current business through the existing organisational model. USPS, protected by a monopoly on letters but banned from entering new non-postal markets, represents the minimal response or “hold firm” approach to industry-wide trends, both in terms of business strategy and organisational structure. RWE is the parallel example in the utilities sector, preserving a focus on its traditional assets rather than on integrating renewables.

Our four other cases all chose to split their old from their new businesses organisationally, although in different ways. Both the UK’s Royal Mail and Innogy were legally split from larger companies to help them reorient their business; Deutsche Post split its businesses organisationally but did not divest; while DONG Energy separated its businesses and then divested old business units.

Two companies pursued business strategies that led to a deep shift towards flatter, less hierarchical organisations. Innogy was separated from RWE in 2016 to focus on new energy markets and has taken measures to increase the autonomy of its business units (based on target customers) and enable more agile investment and divestment in rapidly changing markets. Deutsche Post was privatised in 2000; it then diversified from its former core business, both geographically and in terms of products offered. To support this, it took an organisational shift towards decentralised and autonomous divisions.

Two other companies pursued quite different business strategies, with both seeking to change their organisations, yet without radically changing their organisational structure. Royal Mail was unbundled and privatised in 2013 to increase focus on competitive mail and parcel services; and it took a range of measures to de-layer the organisation, reduce operational costs and reorient its corporate culture and processes towards customer service. DONG Energy is an even more extreme example of business strategy change, completely divesting its oil and gas exploration assets to focus on offshore wind generation. While this was accompanied by various changes in organisational culture and responsibilities, it has not (yet) resulted in the degree of diversification and decentralisation seen in Innogy and Deutsche Post.

Table 1 illustrates the role that motive and context plays and the general response archetypes that each of our cases falls into. In response to structural shifts, companies within the same sector and facing the same shifts have chosen alternative strategies, due in part to their differing motives and context. This has led to a range of outcomes and organisational shifts—oil and gas companies facing their own unique motives and context can learn from these cases to better guide their future responses.

(3) Lessons from the case studies—the postal sector

(1) United States Postal Service (USPS)

The US government’s priority was for USPS to provide service security. This motive, combined with legislation that constrained USPS to its existing core business areas, meant the business strategy and hierarchical structure remained unchanged in response to declining letter volumes.

-

Context: The Postal Accountability and Enhancement Act of 2006 was passed after USPS posted several years of strong earnings. This act prevented diversification into non-postal areas due to potential cross-subsidisation, with monopoly earnings leading to unfair competition and market distortion. However, the timing of this act was unfortunate, as mail volumes began to decline from 2006 onwards.

-

Motive: The motive of preserving service security subsequently led to Congress vetoing cost-cutting measures, such as ending Saturday deliveries and closing the least busy post offices, despite the obvious cost savings. Workers’ benefits have also been given high priority over profitability, as evidenced by the $51.8 billion USPS has had to spend to prefund pensions for its future workforce. The price of postage is also regulated and is lower than all the major European postal companies, placing further pressure on USPS’s margins.

-

Strategy response: Combined, the above factors have resulted in USPS not adopting a clear strategic response to structurally lower letter volumes. USPS has remained in its core business areas, with falling letter volumes and strong competition in parcels continuing to place pressure on margins. Basic cost-cutting measures, such as reducing headcount, have been implemented, but have not been sufficient to offset the declining value in core businesses. However, supply security has been maintained and the price of postage remains low.

-

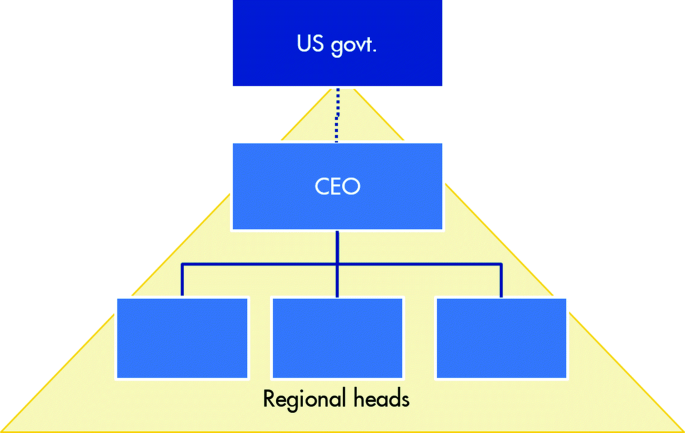

Organisational structure: USPS has remained a government-controlled and regulated monopoly with a top-down hierarchical structure. This multi-layered structure provides strong oversight of operations and drives uniform operational improvement, creating high levels of efficiency (USPS has half the workers per unit of mail compared with Deutsche Post), albeit within a declining market (Fig. 11).

Fig. 11

Source Vivid Economics

USPS remained under government control with a top-down regional structure that helped promote efficiency in a large operation.

(2) Royal Mail

The UK government’s motive in 2011 was returning Royal Mail, which was balance sheet insolvent in 2011, to profitability. This involved the separation and privatisation of the postal service from the postal infrastructure of Royal Mail, which allowed for cost-cutting, delayering and a customer-orientated service culture that returned the postal service to profitability. Growth beyond its core areas has been limited by capital constraints, although Royal Mail has been exploring other markets.

-

Motive: The UK government was focused on returning Royal Mail to profitability after four years of pre-tax losses from 2008–11 that made it a growing liability for the government. Royal Mail has had to contend with declining letter volumes since 2004, the loss of its monopoly in letters in 2006 and, more recently, intense competition in parcels from other European postal operators.

-

Context: Four consecutive years of losses created internal capital constraints that were exacerbated by the stigma of using public funds for investment. As a government-owned company, Royal Mail was bound by strict regulation that made it difficult to renegotiate contracts or alter services. It maintained a universal service obligation that further limited its ability to diversify from its core letters business. It also had a pension plan that accrued large liabilities during the financial crisis of 2008, which contributed to making the firm insolvent.

-

Strategy response: The response was the separation and privatisation of the postal service from the post offices, which remained under public ownership. The government had to take up the pension liabilities of Royal Mail to make its balance sheet solvent and enable privatisation. This enabled Royal Mail to reorient its core business, focusing solely on the service delivered to customers and implementing intense cost-cutting measures that resulted in the closure of a third of mail processing centres and a 10% reduction in headcount after privatisation. These measures were successful in returning the core business areas to profitability, despite minimal revenue growth from 2011 to 2017. However, Royal Mail has not yet been able to significantly diversify, and cost-cutting is unlikely to be a long-term strategy for generating profits. Royal Mail has begun to invest in other geographies and logistic services. These investments have been small due to the constraints of its low capital reserves and dependence on external financing, which prevent large-scale acquisitions of the like Deutsche Post made in the early 2000s.

-

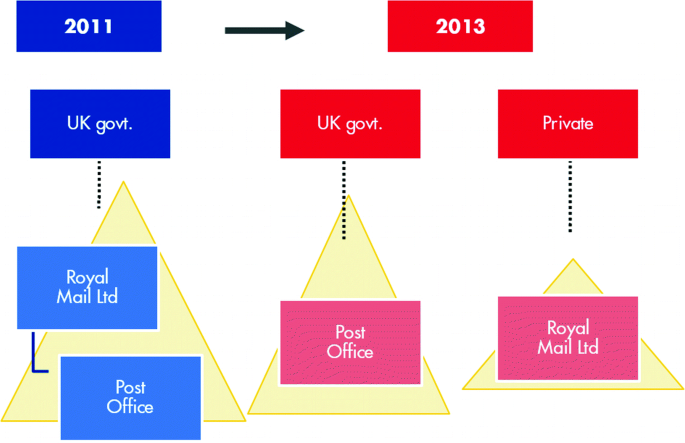

Organisational structure: The separation of the postal service and infrastructure arms allowed for more distinct business models to be implemented. By the Post Office arm remaining in public hands, Royal Mail ensured it could act as network infrastructure for all postal companies, preventing wasted investment and the potential formation of a natural monopoly. The new, service-focused Royal Mail was able to take advantage of its less stringent regulatory environment to implement targeted cost-cutting and investment. To assist in this, Royal Mail brought in a CEO, with significant experience of the public-private transition, to reform the regulatory context and ultimately make the company more profitable (Fig. 12).

Fig. 12

Source Vivid Economics

Royal Mail was separated from the Post Office and privatised to facilitate intense cost-cutting.

(3) Deutsche Post

Deutsche Post began a large programme of acquisitions to diversify its business after it became clear that its domestic market would be threatened by changing legislation. It benefited from favourable timing and had significant cash flows from its traditional business areas, allowing it to finance its acquisitions internally. It also created divisions with a customer focus and increased divisional autonomy, while demonstrating organisational flexibility to maximise synergies across its increasingly broad areas of business.

-

Motive: EU directives led to Germany passing new laws to promote greater competition in its domestic postal market in 1997, making Germany the leader in postal market liberalisation in Europe. At the time, domestic post accounted for more than 75% of Deutsche Post’s revenues. Hence, Deutsche Post was motivated to expand into new value areas, both geographically and within logistic services, to preserve profits as domestic competition inevitably increased.

-

Context: Deutsche Post benefited from favourable timing. Its transition was motivated by legislation, rather than by declining letter volumes. Consequently, it still had the large internal cash flows needed to undertake large acquisitions. Its privatisation in 2001 also afforded it the freedom to undertake radical strategies.

-

Strategic response: Deutsche Post made several large acquisitions that transformed it into a major global logistics company. It made smaller acquisitions in the late 1990s (Danzas and Air Express International) before acquiring DHL and Excel in 2002 and 2005 respectively for more than €8 billion following its privatisation in 2001. DHL had expertise in international express delivery and a developed postal network across the USA and Europe, while Excel made Deutsche Post a major player in supply-side logistics. However, such an extreme strategy comes with inherent risks, as evidenced by Deutsche Post discontinuing its domestic express service in the USA and incurring $3.9 billion in restructuring costs as a result in 2009.

-

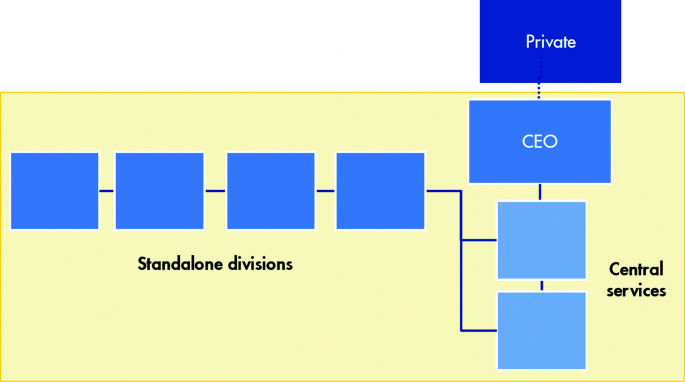

Organisational structure: Deutsche Post has demonstrated flexibility in its organisational structure as it has sought to increase the autonomy and customer responsiveness of its divisions. Similar divisions in new acquisitions were combined to create more efficient networks, and a shift from a three-tier to a two-tier management structure allowed for greater responsiveness to consumer demands. Deutsche Post also formed cross-cutting service divisions to maximise synergies across its new business areas, and a global services unit was introduced in 2006 to provide support across all divisions (Fig. 13 and Table 2).

Fig. 13

Source Vivid Economics

Deutsche Post imposed a flatter organisational structure and central service divisions to maximise synergies.

Table 2 There have been diverging responses among utility companies in response to a similar trend

(4) Lessons from the case studies—the utilities sector

(1) RWE

RWE had a large stock of lignite, coal and nuclear assets in 2004 that were low cost, delivered high returns and provided employment in key shareholder municipalities. Despite new legislation introduced in 2004 promoting renewables, RWE held firm and planned to increase its lignite generation capacity. Hence, RWE kept a centralised organisational structure that could better focus on managing these concentrated, large-scale assets.

-

Motive: In 2004, renewable capacity in Germany was noteworthy, but seemed unlikely to displace the extremely low-cost baseload power provided by lignite and nuclear generation, which had high returns. In addition, German municipalities owned 24% of RWE and relied on the local employment from lignite and coal assets. The employment from lignite generation was also a political tool, leading many politicians to support its use and protect its role in the German energy system, which further disincentivised RWE from diversifying into other technologies.

-

Context: RWE had already invested in improving and expanding its traditional asset base, locking capital into assets with long lifespans. RWE’s previous status as a regional monopoly also fostered a culture of inaction and risk aversion. This was further accentuated by RWE’s history of large cashflows and dividends that investors were not prepared to compromise.

-

Strategic response: RWE did not make any significant additions to its renewable capacity from 2004-10, instead it continued to focus on its legacy assets. In 2004, RWE considered Germany to be “at the beginning of a long-term investment cycle” and the plan was to replace old power stations with more efficient versions, rather than branch off into alternative generation methods. In its 2004 annual report, RWE mentioned the new renewable energy legislation solely in terms of the monetary burden it would place on the company, rather than the opportunities it offered. Consequently, in 2005 RWE announced plans to spend €3.5 billion on two projects to install 3.6 GW of new, optimised lignite generation capacity, which were among the largest projects ever planned in RWE’s history. However, as renewable energy capacity increases at unprecedented rates, RWE has been forced to adopt a harvester mentality, with the aim to derive as much value as possible from its large legacy asset base that will be gradually phased out of Germany’s power system.

-

Organisational structure: RWE maintained the centralised management structure that oversaw its conglomerate of business areas. For its traditional large-scale assets, this allowed for efficient management, but it constrained the autonomy, flexibility and organisational development of its new energy areas and made investment and growth more difficult.

(2) Innogy

Innogy was separated from, but still majority-owned by, RWE in 2016. It contained the green assets of RWE, as well as the network and retail businesses. The motivation for this change was for Innogy to be able to pursue growth opportunities in renewables and other markets without being constrained by the growing liabilities of RWE’s legacy assets or conflicts of interest. By splitting from RWE, Innogy was free to attract fresh investment and implement an organisational structure focused on energy services to better serve its new markets.

-

Motive: Innogy was split from RWE in order to chase growth opportunities. RWE as a whole struggled to come to grips with the changes it was facing and lacked flexibility due to the capital it had invested in its legacy assets.

-

Context: German renewable energy policy had motivated an unprecedented uptake of renewables that has completely altered the state of the energy system—it was clear that the future trend in Germany was one of mass renewable energy generation. In addition, the Fukushima nuclear incident in 2011 resulted in a moratorium on nuclear generation and even greater support for renewable power as a clean alternative.

-

Strategic response: Innogy has marketed itself as a highly innovative company and is pursuing renewable energy opportunities internationally. It is attracting financing as a longer-term investment, which would not have happened if it were still bundled with the legacy assets of RWE, which represent more of a short- to medium-term investment.

-

Organisational structure: Innogy was separated as a partially owned subsidiary of RWE. This removed any association it previously had with the declining legacy asset base of RWE, although 75% of the shares remain in RWE’s hands. Separation afforded Innogy the freedom to pursue its new energy service strategy and reorient the organisation accordingly. Innogy restructured itself in accordance with the different levels of the energy value chain to align with the demands of the end consumer rather than those of production. It also gave units a greater degree of autonomy (flattening the organisational hierarchy), while also pursuing a portfolio approach, whereby investment across those units could be ramped up or down depending on their relative success (Fig. 14).

Fig. 14

Source Vivid Economics

Once Innogy was separated from RWE it adopted a consumer-focused structure, aligning its divisions with areas of the value chain.

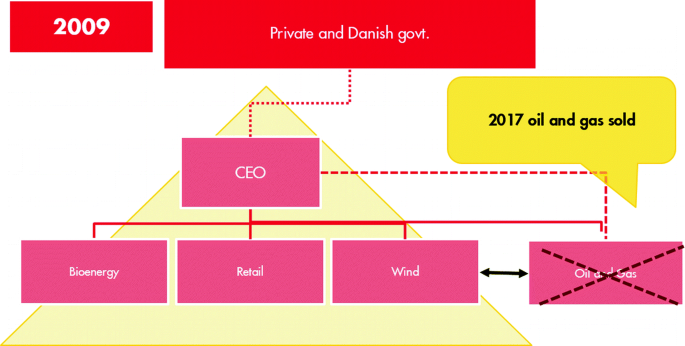

(3) DONG Energy

DONG Energy (now Ørsted) is majority-owned by the Danish government. The company was motivated to pursue offshore wind technology as a reliable source of domestic clean energy to offset declining profits in conventional generation and also develop a new potential growth market.

DONG Energy’s expertise in offshore oil and gas exploration and its experience in pilot offshore wind farms made it ideally placed to aggressively shift its business focus from oil and gas to offshore wind. The company had to change its organisational structure to accommodate this new business area: offshore wind was first added as a division under the CEO to develop, before later becoming the main focus of the company.

-

Motive: Denmark has ample offshore wind reserves and has long promoted wind power with strong domestic subsidies. Declining electricity prices in the Nord Pool power market and fluctuating demand levels reduced thermal generation earnings, making the subsidies and secured earnings from wind generation more appealing.

-

Context: DONG Energy had the necessary skills to drive the development of the offshore wind market. Its offshore oil and gas expertise was easily transferrable and it gained significant experience developing offshore wind farms from its merger with Elsam in 2006, mitigating the risks and barriers to investment.

-

Strategic response: DONG Energy managed to completely transform its main area of focus from oil and gas production to offshore wind generation. Having already completed several medium-sized pilot projects in Denmark in the early 2000s, DONG Energy began seeking out larger opportunities that resulted in an agreement with Siemens in 2009 to buy 1.8 GW of wind turbines. The sheer size of this deal enabled economies of scale to develop in production and deployment and it marked the start of DONG Energy’s commitment to pioneering offshore wind technology. Since 2009 DONG Energy has been involved in the largest offshore wind farms in Denmark (Anholt, 400 MW) and globally (London Array, 640 MW) and has won the bid to deliver the world’s first offshore wind farm of more than 1 GW (Hornsea Project One, 1.2 GW).

-