Abstract

There is a variety of problems in the valuation of firms. That is why the evaluator has to make some simplifications in order to come up with a result. That also goes for the theory of valuation. We will take the first step in assuming that the firm has no debt. In simplifying with this assumption, we shall see that a number of economic problems can be discussed. In the next step we will turn to indebted firms.

You have full access to this open access chapter, Download chapter PDF

There is a variety of problems in the valuation of firms. That is why the evaluator has to make some simplifications in order to come up with a result. That also goes for the theory of valuation. We will take the first step in assuming that the firm has no debt. In simplifying with this assumption, we shall see that a number of economic problems can be discussed. In the next step we will turn to indebted firms.

3.1 Unlevered Firms

Whoever has to value levered firms, also has to be able to value unlevered firms. Both are mutually conditional.

By itself, this claim does not shed any light. It should be understood that if a levered firm is spoken of without naming any further details, then that remains unclear. Are we dealing with a heavily or only moderately levered firm? Will the firm’s debt increase, or are the responsible managers planning to reduce the firm’s credit volume? In contrast to a levered firm in which this must all be explained in detail, the circumstances of an unlevered firm are clear and simple. When we speak of an unlevered firm, we mean a firm, which will not have debts today, nor anytime in the future. Of course it is difficult to believe that there are actually such firms in our world. But this—no doubt fully correct assessment—does not matter here. All we want to state is that what we mean by an unlevered firm is completely straightforward, while by a levered firm it is not so clear without further information.

Cost of Capital and Leverage

A firm’s cost of capital essentially depends upon two influences: firstly, the firm’s business risk, and secondly, its indebtedness. It is fundamentally valid that the greater the risk is and the greater the firm’s debt-equity ratio is, that much higher the expected returns are. And if we make the connection between this law and the considerations of the preceding paragraph, then the cost of capital of an equity-financed firm is straightforward, while the cost of capital of an indebted firm is dependent upon the level of debt. Of course this is all only valid so long as we keep all other influences upon the cost of capital—particularly the business risk and the tax rate—constant.

The indebted firm’s cost of capital is needed in order to be able to correctly value it. To put it more exactly: the cost of capital is needed of a firm, which has two things in common with the firm to be valued. These regard, namely, its business risk and its debt. If you want to determine this cost of capital by using empirical data from the capital market, you typically get into the following situation. You go to the trouble of finding a firm that belongs to the same, or at least very similar risk class (comparison firm) and estimate the expected value of the returns, which the financiers receive. In doing so you almost always have to observe that the comparison firm is financed differently than the firm to be valued. But if the debt now has an influence on the amount of the cost of capital, the comparison firm’s cost of capital cannot simply be applied to the firm to be valued. As we already made clear, indebted firms are not necessarily comparable even when they belong to the same risk class. And it is exactly here that the equity-financed firm comes into play as reference firm.

The indebted firm, this will become clear in a moment, is under any circumstances more valuable than an equity-financed company with identical cash flows. Hence, raising debt will serve as a leverage that can increase the firm’s value. In this case one also speaks of a leverage effect caused by debt. That is why we will use the expressions indebted and levered as well as equity-financed and unlevered as synonyms.

Unlevering and Relevering

In order to determine the cost of capital of the firm to be valued, the comparison firm’s cost of capital is to be adjusted because of the reasons described here. Academics, who are involved with the theoretical side of valuation of firms, have to develop functional equations, which allow for the cost of capital of the—levered—comparison firm to be converted into the unlevered firm’s cost of capital. If they are successful, then the equations can be used to infer the reference firm’s cost of capital from the comparison firm’s cost of capital (unlevering), but also to infer the cost of capital of the firm to be valued from the reference firm’s cost of capital (relevering).

And thus the circle is complete: whoever wants to value a levered firm, must also be able to value an unlevered firm. The academics are then naturally required to live up to the expectations placed on them and must actually be in the position to develop the necessary adjustment equations. Should they fail at this, then the discounting of levered firms’ cash flows with the appropriate cost of capital must simply be forgotten.

Notation

In the first chapter of this book, we spoke of free cash flows and firm values without troubling ourselves with how the firms are financed. Now we are concentrating on firms, which are completely equity-financed. Therefore, the relevant symbols get an appropriate index. We use a superior u for unlevered firms. We will, for instance, designate the free cash flows after corporate income taxes of such firms with \(\widetilde {\mathit {FCF}}^u_t\), and the firm values with \(\widetilde {V}^u_t\). Notice that since only cash flows after taxes can be paid to the owners of the firm, \(\widetilde {\mathit {FCF}}^u_t\) will denote free cash flows after corporate income tax. Unlevered firms have only one single group of financiers. For the returns that the owners are expecting we will use the symbol \(\widetilde {k}^{E,u}_t\).

3.1.1 Valuation Equation

We assume in the following that it is possible to successfully come up with the required adjustment equations and will actively attempt to do so ourselves as best we can. Under this condition, the cost of capital of the totally equity-financed firm can be considered to be known. We assume that the evaluator knows the unlevered firm’s conditional expected free cash flows \( \operatorname *{\mathrm {E}}\left [\widetilde {\mathit {FCF}}^u_s|\mathcal {F}_t\right ]\) for time s = t + 1, …, T.

Definition 3.1 (Cost of Capital of the Unlevered Firm)

Cost of capital \(\,\widetilde {k}^{E,u}_t\) of an unlevered firm are conditional expected returns

The reader should notice that we use the cash flows after corporate income tax in our definition of cost of capital. Therefore, \(k^{E,u}_t\) are variables after corporate income tax, too. The question, how we can defer from these any cost of capital before tax is not our concern, since we do not investigate how the value of a company changes with a changing of the tax rate. Although possibly time dependent, our tax rates are fixed once and for all today. Nevertheless, if anyone tries to determine the cost of capital before tax he cannot operate on grounds of our theory since it does not tell anything about how the value of a firm changes with the tax rates.

The valuation of the unlevered firm is absolutely unproblematic under these conditions.

Theorem 3.1 (Market Value of the Unlevered Firm)

If the cost of capital of the unlevered firm \(k^{E,u}_t\) are deterministic, then the value of the firm, which is only financed with owners’ equity, amounts at time t to

We do not have to further involve ourselves here with the proof of the assertion. We already handled it in a generalized form in Sect. 2.3.3 and do not need to bore our readers here by repeating ourselves.Footnote 1

3.1.2 Weak Auto-Regressive Cash Flows

In Theorem 3.1 we determined a valuation equation for unlevered firms that the evaluator can only use if she knows the cost of equity of the unlevered firm. This condition can only very rarely be counted upon in practice. If the required conditions to use the theorem are not met, then the valuation is anything but a trivial problem.

Cash Flows of the Unlevered Firm

You can only get further in such a situation if the adjustment equation already mentioned above is available. The derivation of such an equation is, however, only possible if the appropriate suppositions are met. In the following sections of this book we will develop adjustment equations for demanding cases. Our results are indeed based on a special condition regarding the structure of the unlevered firm’s free cash flows after taxes. From now on we will assume that the cash flows form a so-called weak auto-regressive process.Footnote 2 The reader may rest assured that without recourse to this assumption, development of correct adjustment formulas is doomed to fail.

Assumption 3.1 (Weak Auto-Regressive Cash Flows)

There are real numbers gt > −1 such that

is valid for the unlevered firm’s cash flows after taxes.

We must assume that gt is greater than − 100% in order to prevent cash flows from having oscillating signs which would be rather unrealistic. It is not necessary to assume that gt is positive, so shrinking cash flows are not excluded with Assumption 3.1.

Uncorrelated (Additive) Increments

In order to understand this assumption, we firstly look at the increments of the cash flow process. In formal notation we thus have

gt is a deterministic amount that is already known in t = 0. What does our assumption on weak auto-regressive cash flows imply for the increments εt+1? It will imply that these increments have expectation zero and are uncorrelated to each other (sometimes called “white noise” although this in fact refers to independent increments).

It is not immediately recognizable that this assumption really implies uncorrelated noise terms. In order to prove that, we have to carry out a little calculation. In doing so, we will again make use of the rules for conditional expectations. We first of all show that the noise terms’ expectation disappears,Footnote 3

Now we come to the proof that the noise terms are uncorrelated. We look at two points in time s < t and have to show that the covariance Cov[εs, εt] disappears. We already know that the noise terms’ expectations are zero. And so from the covariance it immediately follows:

From the rules as well as from the definition of noise term it follows:

Now we concentrate on the conditional expectation, which comes up in the last equation and get the following from the rules as well as the fact that cash flows are weak auto-regressive:

The covariance disappears, which is exactly what we wanted to show.

Independent (Additive) Increments

Until now, we have proven that the vanishing expectation of the noise terms εt+1 as well as their uncorrelation results from the Assumption 3.1. You may get the impression that the reverse is true as well. This is not the case. For reasons of order, we have to ascertain that it is the condition

which is logically sufficient to weak auto-regressive cash flows.

To understand this condition, we refer to the fact that numerous financial models work on the assumption that a firm’s free cash flows would follow a random walk. What does that mean? It means that the cash flows possess increments, which are independent from each other and distributed identically. The noise terms εt+1 have an expectation of zero, are distributed identically and are mutually independent.

This is a big assumption, far bigger than the one we made. The independence of the noise terms implies, for instance, that the increments of the cash flow in t is not connected to the cash flows from years 1 to t − 1. If we have been looking at continuously growing cash flows in the last few years, that by no means suggests that this growth will remain in year t. You cannot draw any conclusions in the least from the development of the years 1 to t − 1 for the year t! Uncorrelation in contrast does not pose such a strong challenge.

While uncorrelation excludes only a linear relation, independence negates every single causal relation: In our notation independence is equivalent to

for any function f(x).Footnote 4 Compare this to the equation above, where f needs only to be linear. If the equation does not hold for any linear function, then there may well be any other nonlinear functional relation f. Independent random variables have always correlation zero, but uncorrelated random variables are—apart from normally distributed random variables—not independent from each other. This again makes clear that in the assumption on weak auto-regressive cash flows we are dealing with a weaker formulation. We are not insinuating any random walk with regard to the cash flows within the framework of our theory, but are instead working on the basis of the less demanding uncorrelated growth.

Multiplicative Versus Additive Increments

Understanding auto-regressive cash flows is not an easy task. In the previous section, we looked at additive increments of cash flows in order to find an appropriate way of interpretation. But the additive context is by no means compelling. We could have used a multiplicative link as well. In the following, we will briefly discuss this and show that the result does not change at all. So, whether we go the additive or a multiplicative path is pure taste. A multiplicative relation is defined by

First, we will check which properties of the error terms εt guarantee that the cash flows turn out to be weak auto-regressive once again. By inserting Assumption 3.1 in the definition we get

This means that

is sufficient and necessary for weak auto-regression. Differences between additive and multiplicative increments only play a role when the distributions of the error terms come into play. However, these differences are not important in the following. The result can also be seen by taking the logarithm on both sides of Eq. (3.2),

In a multiplicative model the logarithms of the cash flows follow an additive model with \(\log \left (1+\varepsilon _{t+1}\right )\) representing the error terms.Footnote 5 Based on these considerations we will restrict ourselves on additive error terms from now on.

Justification of Weak Auto-Regressive Cash Flows

Every economic theory is based on assumptions. The numerous jokes usually told about us economists are based on the fact that we occasionally apply unrealistic, odd conditions. Economists who would like to be taken seriously must put up with the question as to whether their assumptions are justifiable. May we actually insinuate in good conscience that the Assumption 3.1 is met in terms of a firm’s free cash flows? Isn’t this assumption perhaps totally “far-fetched”?

From our experience, practically engaged evaluators normally do not deal at all with the question as to which distribution laws uncertain future cash flows follow. On the contrary they limit themselves to estimating the expectations of these future cash flows. It can now be shown that there are always state spaces with upwards and downwards movements like that analogous to Fig. 2.2 for whatever sequence of expectations you like. Assumption 3.1 is thus met in this model.Footnote 6 But that does not mean anything else than that an evaluator working with estimated expectations of cash flows can operate upon the basis that—so to speak behind the scenes—there is always a state space that corresponds to the Assumption 3.1. All in all, that is why we hold the assumption on weak auto-regressive cash flows to be practically acceptable.

The question can be raised at this point as to why exactly the unlevered firm’s cash flows should be weak auto-regressive. It is obvious that our Assumption 3.1 is arbitrary and it does not make any sense to hide that. Couldn’t we have just as well replaced our assumption with the condition that the free cash flows of a levered firm are weak auto-regressive? Could this levered firm be chosen in just any way, or would it have to be a firm with a particular financing policy? We must give a clear answer to the questions raised here: Varying results would be gotten in any case for the valuation equations, which we will be developing in the following. What is more, we think the following ascertainment is important: If it were to be supposed that a levered firm has weak auto-regressive cash flows, then it would not necessarily follow that the free cash flows of a firm with a different financing policy have this same characteristic as well.Footnote 7

Conclusions from Weak Auto-Regressive Cash Flows: Dividend-Price Ratio

If cash flows are weak auto-regressive, then it can be proven that the unlevered firm’s value is a multiple of the free cash flow. To put it differently, the unlevered firm must always show a deterministic dividend-price ratio. This result is well-known in the case of a perpetual rent from the Williams/Gordon-Shapiro formula.

Theorem 3.2 (Williams/Gordon-Shapiro Formula)

If the cost of capital is deterministic and cash flows are weak auto-regressive, then for the value of the unlevered firm

holds for deterministic and positive \(d^u_t>0\) which will be called dividend-price ratio.

We have banned the proof for this theorem to the appendix.

The last proposition shows that the expected capital gains of the unlevered firm rate is deterministic

and is zero in particular if the dividend-price ratio is constant and the growth rate is zero.

Conclusions from Weak Auto-Regressive Cash Flows: Discount Rates

We had already made it clear in the introduction that for the case under certainty, the returns and not the yields present the appropriate means of determining the value of cash flows. Now we take up the question as to the relation which exists between returns and discount rates. Let us take a look in order to get a certain idea of the free cash flows of any year you like. Without further assumptions on the capital market, we cannot act as if a claim to this single cash flow will be traded. Otherwise, the owner of a share would have claims to dividends, so to speak, but not to the share price of the security. Nevertheless, the question that we want to ask ourselves is: what price should an investor pay at time t < s for an isolated free cash flow \(\widetilde {\mathit {FCF}}^u_s\)?

Although we have not precisely developed the basic elements of the arbitrage theory, we may make use of the fundamental theorem in terms of an analogous argument. If we can actually value levered as well as unlevered firms with this principle, then this should also be possible for the claim to an isolated cash flow. This cash flow is valued by constituting the expectation in terms of the risk-neutral probability and then discounting it with the riskless rate,Footnote 8

The above expression gives the value of the free cash flows \(\widetilde {\mathit {FCF}}^u_s\) at time t. It is immediately noticeable that this valuation formula, albeit extremely elegant, is totally useless: we know next to nothing about the probability measure Q. We will now turn our attention to a second outcome, which can be gotten from the fact that cash flows are weak auto-regressive. If cash flows are weak auto-regressive, then there is another way to value them which is of interest to us. In order to let that become clear, we must precisely define the term discount rate, which has until now been only vaguely introduced. For that we will make use of a few preliminary considerations.

Under the discount rate κt we understand that number, which allows the price of the cash flow \(\widetilde {\mathit {FCF}}^u_{t+1}\) at time t to be determined. According to our statements up to present, the discount rate κt shall serve as an instrument to value the single cash flow \(\widetilde {\mathit {FCF}}^u_{t+1}\), or using the subjective probabilities we must have

Yet, this consideration alone is not sufficient for our purposes. We do not simply want to make use of the discount rates to value cash flows, which are each one single period away from the time of valuation. If we are, for instance, dealing with the valuation of the cash flow \(\widetilde {\mathit {FCF}}^u_{t+2}\) at time t, then we want to manage this task with two discount rates, namely with κt as well as with κt+1 in just such a way that

is valid. But now it is not so unmistakably clear whether κt is serving the valuation of the cash flow \(\widetilde {\mathit {FCF}}^u_{t+1}\) or the cash flow \(\widetilde {\mathit {FCF}}^u_{t+2}\). And we can also no longer assume that the discount rate κt from Eq. (3.3) agrees with κt from Eq. (3.4).Footnote 9 We will thus suggest a definition for the discount rates that takes the cash flows to be valued into consideration and which requires a somewhat more complicated notation.

Definition 3.2 (Discount Rates of the Unlevered Firm)

Real numbers \(\kappa ^{t\to s}_t, \kappa ^{t\to s}_{t+1} \ldots \) are called discount rates of the cash flow \(\widetilde {\mathit {FCF}}^u_s\) of the unlevered firm at time t, if they satisfy

We stress that this is only one of many conceivable definitions. We could, for instance, also define the discount rates as yields instead of the version we have chosen. If we do not do so, it is due solely to practical considerations.

We can, on the basis of definition (3.2), clarify the question as to whether the cost of capital kE, u prove to be appropriate candidates for discount rates of the unlevered cash flows. In answering this question we fall back upon the assumption that the cash flows of the unlevered firm are weak auto-regressive. Cost of capital does not then just only prove itself as appropriate discount rates. It has, much further, the pleasant characteristic that it is independent of the particular cash flow to be valued \(\widetilde {\mathit {FCF}}^u_s\). This characteristic will later prove itself to be very helpful.

Theorem 3.3 (Equivalence of the Valuation Concepts)

If the cost of capital is deterministic and the cash flows of the unlevered firm are weak auto-regressive, then the following is valid for all times: s > t

This is the same as to say that cost of capital are indeed discount rates regardless of s > t ≥ τ

That this theorem follows from the met assumptions can hardly be so easily recognized. Since the proof would demand a fair amount of space and perhaps not even be of interest to every reader, we have banned it to an appendix.Footnote 10

Critical readers could suspect that this theorem has to do with a simple application of the definition of the cost of capital. This would most definitely be a wrong conclusion and in order to make it more understandable, we would like to go into it in more detail. Just equating Eq. (2.8) with Theorem 3.1 leads us in terms of unlevered firms to the result

The preceding equation is of little surprise, as it only claims the equivalence of two different ways of calculation: either the risk-neutral probability and the riskless interest rate is used, or the evaluator applies the subjective probability and the (correspondingly) defined cost of capital. Since the cost of capital is now so defined that both expressions give identical values, there is no reason to worry about coming up with equal firm values.

Of surprise, however, is the declaration that not only do the sums agree in the last equation, but the summands as well. This is everything but obvious, as the simple example

shows. The reader should keep both statements (i.e., the identity of the sums as well as the identity of the summands) clearly separate. Our statement is everything but self-evident and is thoroughly in need of a proof.

A First Look at Default

Until now we had purposely not included the case in which the firm to be valued can go bankrupt. But as the company grows, the probability of going into default is increasing.

If the court in charge allows for the commencement of bankruptcy proceedings, the consequences for creditors, suppliers, employees, owners, and managers are determined in detail by the bankruptcy law. As a rule a liquidator is placed in charge of the business affairs and examines how each party’s payment claims can best be settled. The liquidator makes suitable suggestions within a given time frame and tries to get the agreement of the creditors and the court.

There are principally three possibilities. You can try to rehabilitate the firm, that is, to re-establish the profitability through suitable restructuring measures. In order to do this, the creditors must be willing to renounce some of their claims. If that is not feasible, then the insolvent firm can be transferred over to a bail-out firm and the creditors are paid off by the sales proceeds. If such a solution is also not practical, then there is no other option than to close down and liquidate the firm. What then remains is the smaller the faster the breakup of the firm takes place.

In the following we only assume that in determining future cash flows as well as in laying down future financing and investment policies, all conceivable developments were taken into consideration. If all conceivable developments are being spoken of, then that also includes situations in which the firm goes into default or has gone into default.

Unlevered firms can go bankrupt if claims of tax authorities, employees, and the like are not satisfied. Formal insolvency proceedings are regulated differently from one jurisdiction to the other. However, most countries apply similar default triggers. Usually, illiquidity and over-indebtedness are typical default triggers. A company gets illiquid if its net cash flows (i.e., cash flows to equity or CFE) are negative. A company is over-indebted if the value of equity is negative (whereas market as well as book values are being used in this definition).Footnote 11 Similarly, e.g., the UK Insolvency Act initiates bankruptcy proceedings if a firm either does not have enough assets to cover its debts (i.e., the value of assets is less than the amount of the liabilities), or it is unable to pay its debts as they fall due.

Let us first concentrate on the case of an unlevered firm. It is tempting to suggest that an unlevered company is illiquid if the owners’ net cash flows turn out to be negative or \(\widetilde {\mathit {FCF}}^u_t(\omega )<0\). But it is clearly apparent that this definition has its pitfalls when used in a DCF context. Why do we have to emphasize this? If net cash flows are positive, the company pays money to the owners. But if not, it is just the other way round: the owners pay money to the company if net cash flows appear to be negative. Now, if a sufficient amount of money is paid to the company, the firm is no longer illiquid. The owners simply rectify the unpleasant situation. Hence, if and only if the owners do not completely comply with their reserve liabilities, one can actually speak of a lack of liquidity of the company.

We hold the following: whenever the owners cannot or do not meet their funding obligations, the company effectively faces illiquidity.Footnote 12 However, the mere existence of negative net cash flows does not automatically imply such a run of events. We should therefore speak of the danger of illiquidity that arises if net cash flows turn out to be negative or \(\widetilde {\mathit {FCF}}^u_t(\omega )<0\).

Let us now turn to over-indebtedness as the second default trigger. How could this term be interpreted when we look at an unlevered firm? We will characterize such a situation by \(\widetilde {V}^u_t(\omega )<0\). If this condition is fulfilled, from the owner’s point of view continuing the business would be out of the question. It would undoubtedly be appropriate to speak of “not continuable unlevered firms.” However, for systematic reasons we use the terms “in danger of illiquidity” and “in danger of negative equity,” provided the mentioned inequality is met.

The following proposition will show that now over-indebtedness and danger of illiquidity are in the case of unlevered firms merely equivalent. Both default triggers in fact turn out to coincide and it was too much of an effort to distinguish both cases. But it will turn out that in the case of a levered firm things will become much more complicated.

Theorem 3.4 (Default of the Unlevered Firm)

Consider an unlevered firm with weak auto-regressive cash flows. If the company is in danger of illiquidity at date t in some state, it will also be in danger of negative equity at the same date for the same state.

This immediately follows from Proposition 3.2.

Notice that the market value of equity for corporations cannot be negative, since they have limited liability. The market value of non-corporations, say partnerships, can be negative though. This is the reason why we speak only of danger of insolvency instead of insolvency itself. Our theorem mainly discloses how a consistent valuation model even of an unlevered firm has to be built in order to avoid such logical contradictions.

We now have the basic elements of our theory on discounted cash flow. In the following sections it must be shown what can be done with these basic elements.

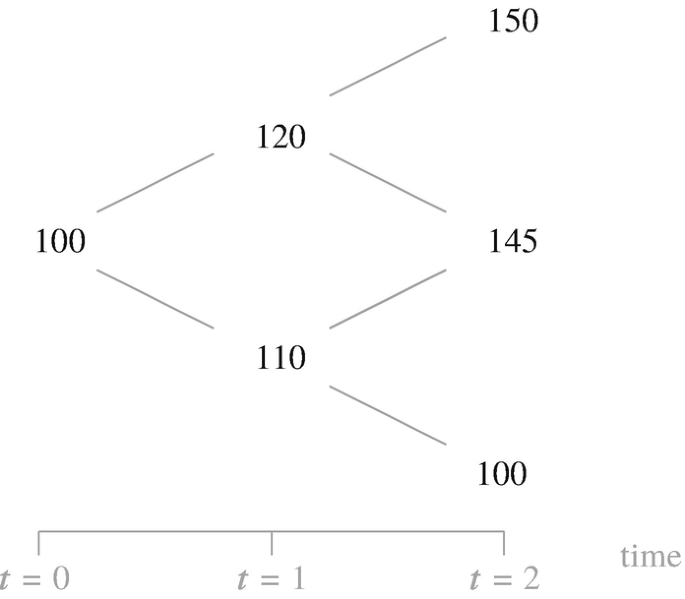

3.1.3 Example (Continued)

The Finite Case

Beforehand we want to take up our example from Sect. 2.2.3 and establish the value of the unlevered firm. As we have seen the cash flows follow a weak auto-regressive development. In addition, we assume that the cost of capital of the unlevered firm is constant in time and amounts to 20%. According to Theorem 3.1, it is obvious what market value the unlevered firm has at time t = 0,

Although the use of this calculation is perhaps not recognizable yet here, we want to determine the market value of the unlevered firm for time t = 1 as well. This is not clear, because we cannot yet know today, if the outcome at time t = 1 will result in the condition up or down. Depending upon the condition, we are discounting different cash flows. In the condition of up, we getFootnote 13

while for the condition of down

is what we get. With that we get altogether

Using the same technique the value of the unlevered firm at t = 2 is given by

An additional result, which, however, is not required for the valuation of the unlevered firm but which will be used subsequently, is that the risk-neutral probability Q can be worked out. To this end we suppose a riskless interest rate of rf = 10% and consider a particular time, for example, t = 3. Due to Theorem 3.3, we have

Assume that state ω occurred at time t = 2. The last equation translates to

The conditional Q-probabilities add to one

The conditional P-probabilities of an up- or a down-movement each come to 0.5. From that we get, for example, at ω = dd

Using this idea at any time t and any available state ω we can finally determine all conditional probabilities. We have summarized our results in Fig. 3.1.

Conditional probabilities Q in the finite example

The Infinite Case

Let the unlevered cost of capital be kE, u = 20%. Then the value of the unlevered firm is using rule 4 (remember g = 0)

As in the finite example we can evaluate the conditional up- and down-probabilities. To this end we assume that rf = 10%. Due to Theorem 3.3, we have at any time t

This is equivalent to

or

The cash flow \(\widetilde {\mathit {FCF}}^u_t(\omega )\) cancels. Furthermore the growth rate of the cash flows is zero (g = 0) and we arrive at

The conditional Q-probabilities add to one

From that we get for the infinite example

regardless of t and ω.

This is an interesting result. The factors u and d cannot be chosen arbitrarily if the cost of capital are to be constant. Furthermore we can see that

must hold in order to ensure positive Q-probabilities. Any increase of the cost of capital enforces a decrease of the corresponding d.

3.1.4 Problems

-

1.

The next two problems shall clarify the differences between additive and multiplicative increments. The error terms ε may be iid with values of 0.5 or − 0.5, respectively, with 50% probability. In this case there is no growth, i.e., g = 0.

-

(a)

Consider additive increments. Assume that the cash flows follow the process

$$\displaystyle \begin{aligned} \widetilde{\mathit{FCF}}^u_t=1+\varepsilon_1+\varepsilon_2+\ldots+\varepsilon_t \,. \end{aligned}$$Show that under these conditions the cash flows form a binomial tree.

-

(b)

Now, look at multiplicative increments. Consider cash flows that follow the process

$$\displaystyle \begin{aligned} \widetilde{\mathit{FCF}}^u_t=(1+\varepsilon_1)(1+\varepsilon_2)\cdots(1+\varepsilon_t) \,. \end{aligned}$$Show that the logarithmized cash flows are binomially distributed.

-

(a)

-

2.

Let error terms ε be iid.

-

(a)

Consider additive increments that are normally distributed with expectation 0 and variance 1. The cash flows may follow the process

$$\displaystyle \begin{aligned} \widetilde{\mathit{FCF}}^u_t=1+\varepsilon_1+\varepsilon_2+\ldots+\varepsilon_t \,. \end{aligned}$$Show that \(\widetilde {\mathit {FCF}}^u_t\) must be normally distributed with expectation 1 and variance t.

-

(b)

Switch to multiplicative increments that are lognormally distributed with expectation 0 and variance 1. The cash flows follow the process

$$\displaystyle \begin{aligned} \widetilde{\mathit{FCF}}^u_t=(1+\varepsilon_1)(1+\varepsilon_2)\cdots(1+\varepsilon_t)\,. \end{aligned}$$Are the cash flows now lognormally distributed with expectation 1 and variance t?

-

(a)

-

3.

Assume that cash flows follow a process as in (3.1). Show that

$$\displaystyle \begin{aligned} 0= \operatorname*{\mathrm{E}}\left[\varepsilon_{t+1}|\mathcal{F}_t\right] \end{aligned}$$is sufficient for the cash flows to be weak auto-regressive. Show furthermore that the noise terms are uncorrelated, i.e., for s > t

$$\displaystyle \begin{aligned} \text{Cov}\left[\varepsilon_s,\varepsilon_t\right]=0\;. \end{aligned}$$ -

4.

Consider the binomial tree from Fig. 3.2 (additive increments). Up- and down-movements have the same probability, notice that we not necessarily require \(\widetilde {\mathit {FCF}}^u_2(ud)=\widetilde {\mathit {FCF}}^u_2(du)\).

-

(a)

Determine all possible distributions of the noise terms ε at time t = 2 such that

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\varepsilon_2|\mathcal{F}_1\right]= \operatorname*{\mathrm{E}}\left[\varepsilon_2\right]=0 \end{aligned}$$Fig. 3.2

Independent and uncorrelated increments in Problem 4

holds (uncorrelated additive increments).

-

(b)

Determine all possible distributions of the noise terms ε at time t = 2 such that furthermore

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[f(\varepsilon_2)|\mathcal{F}_1\right]= \operatorname*{\mathrm{E}}\left[f(\varepsilon_2)\right] \end{aligned}$$holds for any function f(x) (independent additive increments).

-

(a)

-

5.

Consider the binomial tree from Fig. 3.3. Up- and down-movements have the same probability, again we do not require \(\widetilde {\mathit {FCF}}^u_2(ud)=\widetilde {\mathit {FCF}}^u_2(du)\). In this example the noise terms are multiplicative instead of additive.

Fig. 3.3

Independent and uncorrelated increments in Problem 4

-

(a)

Determine all possible distributions of the noise terms ε at time t = 2 such that

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\varepsilon_2|\mathcal{F}_1\right]= \operatorname*{\mathrm{E}}\left[\varepsilon_2\right]=0 \end{aligned}$$holds (uncorrelated multiplicative increments).

-

(b)

Determine all possible distributions of the noise terms ε at time t = 2 such that furthermore

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[f(\varepsilon_2)|\mathcal{F}_1\right]= \operatorname*{\mathrm{E}}\left[f(\varepsilon_2)\right] \end{aligned}$$holds for any function f(x) (independent multiplicative increments).

-

(a)

-

6.

Let the dividend ratio at time t be defined as

$$\displaystyle \begin{aligned} \text{div}_t:= \frac{\operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]}{\widetilde{V}^u_t}\,. \end{aligned}$$Show that it is deterministic for weak auto-regressive cash flows and determine it given the growth rate gt and the dividend-price ratio \(d^u_t\). Do the same for the capital gains ratio

$$\displaystyle \begin{aligned} \text{gain}_t:= \frac{\operatorname*{\mathrm{E}}\left[\widetilde{V}^u_{t+1}-\widetilde{V}^u_t|\mathcal{F}_t\right]}{\widetilde{V}^u_t}\;. \end{aligned}$$ -

7.

Assume that the cost of capital kE, u are deterministic and constant. The firm is infinitely living (T →∞). Assume that the cash flows of the unlevered firm are weak auto-regressive as in Assumption 3.1 for deterministic and constant g with − 1 < g < kE, u.

-

(a)

Find a simple formula for the value of the firm \(\widetilde {V}^u_t\) analog to Theorem 3.1. Evaluate the capital gains and the dividend ratio for that case.

-

(b)

What happens to the firm value if g ≥ kE, u?

-

(c)

Show that the free cash flows are furthermore weak auto-regressive under Q as well, i.e.,

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\!_Q\left[\widetilde{\mathit{FCF}}^u_{t+1}\right]=\left(1+g^Q_t\right)\widetilde{\mathit{FCF}}^u_t\;. \end{aligned}$$and determine \(g^Q_t\).

-

(a)

-

8.

A straightforward extension of weak auto-regressive cash flows would be that for every t

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]=\widetilde{\mathit{FCF}}^u_t+X_t, \end{aligned}$$where Xt is a random variable satisfying

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[X_t|\mathcal{F}_{t-1}\right]=\operatorname*{\mathrm{E}}\,\!\!_Q\left[X_t|\mathcal{F}_{t-1}\right]=0 \end{aligned}$$and furthermore Xt is uncorrelated to \(\widetilde {\mathit {FCF}}^u_t\). Hence, this random variable is white noise and has no price at t − 1. Several problems will be devoted to this special case.

-

(a)

Assume that the firm will live forever (T →∞). Verify that the value of the company having constant cost of capital satisfies

$$\displaystyle \begin{aligned} \widetilde{V}^u_t=\frac{\widetilde{\mathit{FCF}}^u_t}{k^{E,u}}+\frac{X_t}{k^{E,u}}\;, \end{aligned}$$and show that the variance of the firm value \(\widetilde {V}^u_t\) is strictly greater than the variance of the corresponding cash flow \(\widetilde {\mathit {FCF}}^u_t\) if kE, u < 100%.

-

(b)

Verify that

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\widetilde{V}^u_{t+1}|\mathcal{F}_t\right]=\widetilde{V}^u_t \end{aligned}$$and hence the expected capital gains rate is zero.

-

(c)

In this particular case the cost of capital may be used as discount rates (Theorem 3.3). Verify this by showing that

$$\displaystyle \begin{aligned} \frac{\operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]}{1+k^{E,u}}=\frac{\operatorname*{\mathrm{E}}_Q\left[\widetilde{\mathit{FCF}}^u_{t+1}| \mathcal{F}_t\right]}{1+r_f} \end{aligned}$$and

$$\displaystyle \begin{aligned} \frac{\operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+2}|\mathcal{F}_t\right]}{(1+k^{E,u})^2}=\frac{\operatorname*{\mathrm{E}}_Q\left[\widetilde{\mathit{FCF}}^u_{t+2}| \mathcal{F}_t\right]}{\left(1+r_f\right)^2}\;. \end{aligned}$$

-

(a)

-

9.

Another straightforward extension of weak auto-regressive cash flows would be to assume

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]=\widetilde{\mathit{FCF}}^u_t+C \end{aligned}$$for constant C ≠ 0 (see, for example, Feltham and Ohlson (1995) or Barberis et al. (1998), although they consider a different approach). Several problems will be devoted to this special case.

-

(a)

Prove that the infinitely living unlevered firm having constant cost of capital satisfies

$$\displaystyle \begin{aligned} \widetilde{V}^u_t=\frac{\widetilde{\mathit{FCF}}^u_t}{k^{E,u}}+\frac{1+k^{E,u}}{(k^{E,u})^2}\,C\;. \end{aligned}$$Hint: You might want to use

$$\displaystyle \begin{aligned} \sum_{s=1}^\infty \frac{s}{(1+x)^s}=\frac{1+x}{x^2}\qquad \text{if}\; x> 0\;. \end{aligned}$$ -

(b)

Show that the expected capital gains rate of the unlevered firm is not zero.

-

(c)

Show that

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\,\!\!_Q\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]= \frac{1+r_f}{1+k^{E,u}}\,\widetilde{\mathit{FCF}}^u_{t}+ \frac{r_f}{k^{E,u}}\,C \end{aligned}$$for the expectation of the cash flow under Q. Does Theorem 3.3 still hold?

-

(a)

-

10.

The Definition 3.2 of a discount rate is cumbersome since it always refers to the time the cash flow is paid and the time the cash flow is valued as well. The aim of this problem is to show that even in simple cases if \(\kappa ^{r\to s}_t\) shall be independent from r and s, this can lead to a contradiction.

Consider cash flows that are independent from each other and identically distributed. In this case the conditional expectation

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right], \quad \operatorname*{\mathrm{E}}\,\!\!_Q\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right],\ldots \end{aligned}$$will always be a real number.Footnote 14 Furthermore, the discount rate \(\kappa ^{r\to s}_t\) shall depend neither on r nor on s

$$\displaystyle \begin{aligned} \kappa^{r\to s}_t=\kappa_t. \end{aligned}$$-

(a)

Show that the discount rates are equal to rf = κt.

-

(b)

Show that they cannot be equal if the expectations do not coincide, i.e.,

$$\displaystyle \begin{aligned} \operatorname*{\mathrm{E}}\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]\neq \operatorname*{\mathrm{E}}\,\!_Q\left[\widetilde{\mathit{FCF}}^u_{t+1}|\mathcal{F}_t\right]. \end{aligned}$$

-

(a)

3.2 Basics About Levered Firms

We now bring to a close the debate of unlevered firms and turn towards the truer-to-reality case of the levered firm. To do so we first of all need a clear separation between equity and debt.Footnote 15 In addition, we will work out in which the taxation of levered firms is different from the unlevered firm. These differences in taxation influence the value of the firm. And the degree of influence on value is dependent upon the type of financing policy the managers of the firm to be valued are operating under. In connection to the fundamental representation of this relation, we will analyze how numerous conceivable forms of financing policy effect value of firms and derive each appropriate valuation equation.

3.2.1 Equity and Debt

To come quickly to a needed result, we suppose that the firm to be valued is a corporation, where financiers can be divided into two groups. The financiers come up with capital, which the managers use to employ on risky investments. In return, the financiers get securities which we term debt or equity, as the case may be. Although we presume our choice of words is already sufficiently clear, we do, however, want to get down an important characteristic of the securities. We assume that equity and debt are traded on capital markets, that is, they can be bought and sold at any time. The securities thus have market prices, and we designate the market value of the equity at time t with \(\widetilde {E}_t\), and the market value of the debt with \(\widetilde {D}_t\). The tilde over the symbol makes it clear that a random variable is being dealt with. If we want to express that there are no random variables, we write Dt. Interest paid at time t + 1 is \(\widetilde {\,I\,}_{t+1}\).

The firm’s generated net profit in total is uncertain and is distributed among the financiers so that debt financiers (creditors, debt holders) are taken care of first, while the equity financiers (owners, shareholders) have to make do with what possibly remains. Further financiers are not to be considered. The distribution rule is completely straightforward.

Notation

In the equations that we have used until now, we were always dealing with free cash flows and values of firms. In the previous chapter, when unlevered firms were dealt with we added the index u to the symbols which we needed. Now we will use the index l, since levered firms are being dealt with. We thus write \(\widetilde {\mathit {FCF}}^l_t\). For the equity cost of capital of the levered firms we will use the symbol \(\widetilde {k}^{E,l}_t\).

We will have to introduce a whole range of other symbols. It will always be recognized when these symbols are used in the context of an unlevered firm by index u. If, on the other hand, a levered firm is being dealt with, we will make that clear with the index l.

The Firm’S Market Value, Debt-Equity Ratio, and Leverage Ratio

The goal of our theory is the establishment of the market value of a firm. For the market value of the levered firm at time t, we use the symbol \(\widetilde {V}^l_t\). The market value of the firm is equal to the sum of the equity’s market value and the debt’s market value,

Debt equity ratios and leverage ratios will play a big role in our further considerations. The debt ratio measures the proportion of debt to the market value of the firm,

while the leverage ratio (debt-equity ratio) is defined in the form

Even though we will use the debt ratios in later sections, we can also apply the leverage ratio. Since both quantities can easily be converted into each other this is not a limitation,

is valid. With these symbols we stress that all quantities are measured in market values.

Book Values

In a few sections of this chapter the book value of equity and debt will be dealt with. These are those values, with which the owners’ or creditors’ claims are to be found in the balance books of the firm to be valued. As symbols for debt and equity for book values, we use \(\widetilde { \underline {D}}_t\) and \(\widetilde { \underline {E}}_t\), respectively. The sums of equity and debt at time t are written in the form

We will notate

for the debt ratio measured in book values, and

for the correspondingly measured leverage ratio. Again, debt ratio and leverage ratio can easily be converted into each other.

3.2.2 Earnings and Taxes

In the foundational chapter of this book, we gave a preliminary introduction of gross cash flows and free cash flows. The terms developed there were perfectly adequate to come up with valuation equations for firms where the financing policy was not set in detail (Chap. 2) or which were totally financed with equity (Sect. 3.1). Now we are supposed to be dealing with levered firms, which forces us to bring more structure to the terms.

Tax Equation

In order to understand the relevant relationships, we again present the ascertaining of free cash flows from Fig. 2.1, but now with a more detailed notation that will be used in this chapter, see Fig. 3.4. Interest on debt is of course only accrued by levered firms. If we add it to the earnings before taxes (EBT), then we get the earnings before interest and taxes (EBIT). If we add accruals, we arrive at the gross cash flow before taxes, also called EBITDA. If we finally deduct the investment expenses and deduct taxes as well, then we get the free cash flow. This cash flow is fully distributed to the owners of the company.

From earnings before taxes (EBT) to free cash flow (FCF)

As was announced earlier, we are limiting ourselves in this chapter to a business tax and leave out the income tax on the shareholder’s level of the company. The tax base of the profit taxes is the earnings before taxes (EBT)

The tax equations should be valid independent of the sign of the tax base. If the tax base is positive, the firm has to pay taxes; if it is, on the other hand, negative, then the firm gets a return in the amount of the tax due. We will not give more realistic models of loss set-off or loss carryback rules than that.

In order to describe the difference between the levered and the unlevered firm we will assume that their investment policies coincide.

Assumption 3.2 (Identical Gross Cash Flows)

The gross cash flows before taxes as well as the accruals and investment expenses of the unlevered firm do not differ from those of the levered firm.

Hence, the EBIT must be just as large for the firm financed by equity as it is for the firm financed by debt. In Fig. 3.4 the third and the fourth lines are thus identical for the levered and unlevered firms, while taxes and free cash flows will show different values. The taxes of the levered firm are thus smaller by the product of the tax rate and interest on debt than the taxes of the firm financed solely by equity

Financing by debt is thus favored in this model.

By Assumption 3.2 the free cash flows before taxes of the levered and unlevered firms are identical, only the tax payments are different,

The firm financed by equity has lower free cash flows than the firm financed by debt, because interest may be deducted from the tax base. The following concerns the question as to the value of these tax advantages. A—if not the—central problem of the DCF theory is the establishment of the value of the tax advantages governed by credit conditions.

3.2.3 Financing Policies

No Default

We are supposing at first that credit is not threatened by default and thus follow a widely held tradition within DCF literature,

This notion flagrantly contradicts the experience of banks with their borrowers. In reality financiers’ claims are obviously under notable threat of default. In a later subsection we will show how default can be handled in our theory.

Components of Tax Advantages

Now we make a first attempt at turning to the valuation of tax advantages of the firm financed by debt. The tax advantages are, as we just determined, attributed to the fact that interest on debt may be deducted in the firm’s tax base. This comes to—in terms of the levered firm—a tax savings (also called tax shield) in the amount of

Whoever is involved professionally with valuation of firms as certified public accountant, investment banker or as business consultant, knows only too well that in practical terms both the tax rate and the interest rate are uncertain. Looking at the assumptions, we have, however, made sure that only the amounts of debt \(\widetilde {D}_{t-1}\) can be uncertain. The interest rate of debt rf as well as the tax rate τ are certain according to the requirements.

Value of Tax Advantages

To value tax advantages appropriately, we need further information about the uncertainty to which they are exposed. It is true, we know—in accordance with the assumption—how high the tax rate and the interest rate will be. But we cannot, however, know without further assumptions regarding the financing policy at time t = 0, how high the debt of the firm to be valued will be at time t > 0.

We have no other options than to come to further assumptions regarding information about the firm’s future debt policy. This is the only way in which we can come up with what amounts of debt \(\widetilde {D}_{t-1}\) will be established in times t > 0, with what risk these amounts bear and how the resulting tax advantages are to be accordingly valued. Without any information of the levered firm the tax advantages cannot be properly valued.

The practically engaged evaluator may perplexedly note here that the valuation of the firm is bound to the assumptions pertinent to it. In so doing the firm value takes on an air of doing what one pleases of it, or—to put it more drastically—an element of manipulation. To that we must answer, every valuation is based on expectation about the future. Whoever does not forecast the turnover numbers, whoever does not know what the cost of materials will be, cannot value a firm. All of these and further assumptions come off as somewhat arbitrary. That also applies for the financing policy of the evaluator.

Different Financing Policies

Now let us turn to different possible financing policies. We find that within this area of DCF literature, two concepts are regularly brought into play. Autonomous financing supposes that the amounts of debt are already fixed at the time of valuation. Financing based on value supposes, in contrast, that the debt ratios are fixed in the present.

We too will examine both financing policies. When debt ratios measured in market values are being dealt with, we will, however, to be more precise refer to it in the following as financing policy based on market values. Moreover, we will bring four further financing policies into the discussion. We will term these policy based on cash flows, policy based on dividends, policy based on book values and on cash flow-debt ratio. These six policies can be characterized in brief by the following:

-

1.

With autonomous financing methods, the future amount of debt is deterministic.

-

2.

With the financing based on market values, the evaluator sets the future debt ratios based on market values.

-

3.

With the financing based on book values, the future debt ratios are not fixed to market values, but rather to book values.

-

4.

With the financing based on cash flows the amount of debt is based on the firm’s cash flows.

-

5.

With the financing based on dividends the firm’s amount of debt is managed so that a previously determined dividend can be distributed.

-

6.

With the financing based on dynamical leverage ratio the evaluator sets the future cash flow-debt ratios.

We cannot and do not want to answer the question here as to which of these financing policies is particularly close to reality. Instead, we see our task as to compile all possibly conceivable financing policies, and to show how to go about valuing when these policies are met. The direction the specific firm goes in depends upon the credit agreements with the financiers as well as the goals and ideas of the managers.

Further, we will not discuss the question, which of the mentioned financing policies maximize the value of the levered company. Later on it will become apparent that with an extended leverage the value of the company increases. Hence, the owners of the company should select a leverage as high as possible if they act rationally. However, here the leverage policy will be considered as a term which is given exogenously. The owners will pursue a prespecified financing policy without racking one’s brains if this policy will be the best option.

Assumption 3.3 (Given Debt Policy)

The debt policy of the firm (although probably uncertain) is already prescribed.

To determine the values of firms under the different financing policies, we require an important equation. The statements of the fundamental theorem of asset pricing are valid for the levered as well as the unlevered firm,Footnote 16 particularly the valuation statements coming out of Theorem 2.2. We thus know that the value of the unlevered firm can be established with equation

The validity of the fundamental theorem does not depend upon how the firm is financed. The value of the levered firm is thus given through the relation

Using (3.9) we can immediately read from both valuation equations that the market value of the levered firm is different from the market value of the unlevered firm only in terms of the value of the tax advantages

With (3.10) and rule 2 (linearity) this yields

We will be able to use this equation for all financing policies. Fernández (2005) gives the same result in the following Presentation:Footnote 17

3.2.4 Debt and Transversality (Again)

In the following we will focus on levered companies that accept loans which run forever. Anyone familiar with basic financial mathematics knows that the present value of a riskless loan equals the sum of discounted cash flows if the credit is temporary. So if credit is granted today in the amount of \(\widetilde {D}_0\) and the borrower in later times pays both interest of \(r_f\widetilde {D}_t\) and (possibly negative) redemptions of \(\widetilde {D}_{t}-\widetilde {D}_{t+1}\), then

must hold if \(\widetilde {D}_T=0\) is assumed.

What will happen for T →∞? One can easily imagine that the loan is not repaid in full. But what does that mean for the above equation? Under what conditions can we state

and under what conditions is this not permissible? Transversality, again, will give the answer. For this reason, we reassume this condition. However, we will concentrate on uncertainty from the beginning. It can immediately be seen that this is an assumption with regard to the infinite finance policy.

Assumption 3.4 (Debt Policy Satisfies Transversality)

The debt policy of the firm satisfies the transversality condition,

To fully understand this assumption, let us look at two (extreme in our eyes) examples of infinite financing policies. In the first case transversality will be violated, in the second one it will be fulfilled. Our readers must decide, whether the examples are intuitively clear.

First, assume that the payment obligations due to interest liabilities will be completely credit-financed. This boils down to the relation

and it is immediately clear that the transversality condition cannot be fulfilled: The creditor increases his loan from year to year and never gets a refund. Equation (3.13) can therefore never be satisfied for a positive \(\widetilde {D}_0\). In finite time the credit might grow enormously, but would eventually be repaid.

The next example shows that Eq. (3.13) can be sustained with a financing policy that is only slightly different from the previous one. To this end, let us assume that an investor finances only half of the interest obligations by a credit. Again, the loan is increasing year by year. And it is also true that in finite time there is never a refunding. However, the new policy is now described by

Anyone who believes that Eq. (3.13) is not fulfilled under this policy is wrong. This follows directly from

The difference between the two financing policies is quickly detected. For Eq. (3.13) to be satisfied, the lender must receive any payments from the debtor at any time. The compounding effect then ensures complete refunding of the loan. However, if the redemption payments go back to zero (as in the first example), the transversality condition is inevitably violated.

The issue raised here is only important for credit agreements with an infinite duration. Therefore, we will treat T →∞ only exceptionally, and will regularly restrict ourselves to contracts with finite duration.

3.2.5 Default

Authors who are involved in credit risks take care to thoroughly discuss default probabilities. Surprisingly, it is the same facts of the case that are regularly disregarded in the DCF literature. There is no doubt that it is necessary to pursue the question as to how a firm can be valued with the risk that it will not be able to meet all its credit obligations.

It will turn out that in the case of a levered firm default is becoming much more manifold.

There are legal stipulations that regulate under what conditions default for a levered company is given. We have already stressed that in most countries of the world there are several factors that can lead to bankruptcy. Lack of liquidity is such a factor everywhere. But there are also countries in which the managers are required to start bankruptcy proceedings when the firm’s balance sheets read that the assets no longer cover the debts, or when the finance plans indicate the inability to pay in the near future.

Homogenous Expectations

Up to now we have worked on the basis that debt and equity financiers are equally well informed. This condition is of particular importance with the threat of insolvency and can surely be seen critically. But there is no getting around conceding certain information about the firm to the debt financiers. No one loans out money without having beforehand checked up on the contract partner’s business ideas, risks, and market chances in some detail. Yet asymmetric information as a rule is truer to reality than our condition of homogenous expectations. It, however, applies that whoever wants to deviate from this assumption, has to very precisely define the information which both sides either have or do not have access to.

Identical Cash Flows and Default

Until now we have worked on the basis of some assumptions within the framework of our theory which should also remain valid in the case of default. We would in the following like to briefly discuss how we justify that.

We had thus continually assumed that gross cash flows from levered and unlevered firms are not different from each other. It should be stressed that until now levered firms not in danger of going into default have been dealt with. If we want to maintain the assumption, then it must be broadened to include the gross cash flows of the firm in danger of going into default and that not going into default being the same.

That is quite a far-reaching limitation. A firm can of course get into a situation due to financial difficulties which has consequences for its gross cash flows. Financial strains often cause suppliers as well as clients to reconsider continuing doing business with the firm affected. Some clients leave altogether or cancel long-term contracts; suppliers may deliver only on condition of prepayment. Managers who would remain faithful to the firm under more favorable circumstances look for other jobs, taking with them the important know-how required in such times and aggravating the crisis. All the financial consequences of a high leverage which we have pointed out here, are usually referred to in the literature as indirect costs of default. It can then be said that in our model we abstract the existence of such costs of default. But indirect costs of default are difficult to quantify. If you wanted to substitute with a more realistic premise and at the same time avoid having the new assumption remaining subject to change, then despite all difficulties, you would have to formulate a functional relation between gross cash flows and advanced leverage. A firm’s gross cash flows have two components in a model of several periods: on the one hand their amount, and on the other their duration. Our assumption says that increasing leverage affects neither the amount nor the duration of the gross cash flows.

Let us now open up the question as to how great the amount is that the owners receive at time t. The starting point was the firm’s identical gross cash flows before interest and tax \(\widetilde {\mathit {GCF}}_t\). To arrive at the free cash flows from here, we have to deduct the firm’s (internally financed) investments and taxes. It needs to be further clarified how these amounts differ from each other when dealing with, on the one hand, an unlevered firm and, on the other, a levered firm also in danger of going into default. Again, we only get further with the assumption that the investment and accruals of the firm in danger of going into default agrees with that of the firm not in danger of going into default. We can thus sum up our conditions in the following specification of Assumption 3.2.

Assumption 3.5 (Gross Cash Flows and Default)

The gross cash flows as well as the investment and accruals of the unlevered firm do not differ from those of the firm in danger of going into default.

Bankruptcy Estate

If the company does not file for bankruptcy, then the creditors’ claims can be satisfied in full. Two parties are to be differentiated here, the state and the investor. The order in which the claims of the finance administration and the other creditors are satisfied does not matter as long as we are not dealing with going into default. The owners’ claims will be settled last in any case. In the worst case the shareholders can end up with nothing. Since corporations do not have personal liability, we can disregard the owners having to make payments from their private pockets in very unfavorable situations.

As a rule the requisitioned property does not suffice in the case of bankruptcy to completely settle up with the state and the creditors. Thus it does matter which claims take priority. Is the state to be completely taken care of first? Or, are the other creditors to be paid off while the state has to stay? Answers are provided by the pertinent legal stipulations. We do not want to discuss that any further here, but solve the problem by introducing an appropriate assumption that is (more or less) satisfied in most industrial countries.

Assumption 3.6 (Prioritization of Debt)

The tax office’s claims come before those of other creditors. The cash flows are always sufficient to at least pay off the tax debts in full.

The tax office will therefore be given priority over the creditors when dealing with a firm in danger of going into default so that the tax claims can be satisfied in full. And the default is never so drastic in our concept that the state loses a share of its claims.

Notation

The notation used so far is not sufficient for the deliberations to be put forth in the following. Let us again suppose that the firm took in a credit of \(\widetilde {D}_t\) at time t. In the earlier section the variable \(\widetilde {D}_t\) signified two different things, namely for one, the credit which the firm took in at time t, and, for the other, the amount, which apart from the interest it redeems at time t + 1.Footnote 18 In case of default, the amount, which the company amortizes at the time t + 1, will not coincide with the repayment sum to which it is legally obligated. \(\widetilde {D}_t\) shall be the credit which has been raised at time t and \(\widetilde {D}_{t+1}\) the corresponding amount a year later. Consequently, the difference between \(\widetilde {D}_t\) and \(\widetilde {D}_{t+1}\) accounts for the amount which the company needs to pay back to the creditor (or, if this amount is negative, has to be raised). In the following we will assume that the company pays back the amount \(\widetilde {R}_{t+1}\) which can be at the most as high as \(\widetilde {D}_t - \widetilde {D}_{t+1}\), hence

If the repayment sum is smaller than the amount which the company owns its creditors, the term

describes a remission of debts. We do not need a new symbol for the interest \(\widetilde {\,I\,}_{t+1}\) resulting at time t + 1.

Only looking at the relationship between the firm to be valued and its financiers in the case of default, it does not matter how the existing remainder of funds is distributed among the interest and principle repayment due. In terms of the tax office, however, it is different, since interest lowers the tax base, and the debt repayment, in contrast, does not.

We proceed on the basis that the tax office allows interest in the amount of \(\widetilde {\,I\,}_{t+1}\) to be deducted from the tax base. On the other hand, the state in many countries insists that during bankruptcy the cancellation of debt be taxed in amount of \(\widetilde {D}_t-\widetilde {D}_{t+1}-\widetilde {R}_{t+1}\). According to (3.8), the following applies for the taxes of the firm which is both levered and in danger of going into default at time t:

Since the unlevered firm’s tax equation does not change and the gross cash flows as well as investments are identical, we now get

The fundamental theorem of asset pricing now also applies to the levered firm in danger of going into default. We can thus establish the relation

Default Triggers

Firstly, we want to examine whether a company that is over-indebted will be illiquid at a future point in time and, vice versa, whether a firm that becomes illiquid will have encountered over-indebtedness. We believe that the relationship between both triggers requires more attention than they are currently given in the literature.Footnote 19 Authors who address valuation problems seem to assume that it does not matter which insolvency trigger is used—a view we challenge although in Proposition 3.4 we have exactly shown that. While default has been intensively investigated in prior research, until now the relationship between these two triggers has not been subject to a detailed analysis. However, for investors and financiers (e.g., in context of insolvency risk forecast) it is important to understand, whether these triggers are substitutes to each other, or whether one trigger is stricter than the other in the sense that one default criterion is met earlier.

We analytically provide evidence that over-indebtedness always implies illiquidity although the converse is not true and that the relationship between both default triggers depends on the given financing policy. To this end, we must define what over-indebtedness and lack of liquidity shall be for levered firms. Whereas illiquidity focuses on cash flows, we will be using the term over-indebtedness if the assets of the firm are smaller in value than its debt. In the following, however, we consider only market values instead of, for example, book values in the case of over-indebtedness. The reason for our approach is obvious: by strictly using market values we are in a position to easily produce clear conceptual relationships and provide necessary and sufficient conditions for bankruptcies. That would be much more difficult, if not impossible, if we used book values or fair values. Hence, falling back on market values is in line with the simplification strategies that prevail in economics.

Definition 3.3 (Default)

For a given financing policy, a levered firm will be in danger of illiquidity at time t in state ω if the cash flows in state ω ∈ Ω do not suffice to fulfill the creditors’ payment claims (interest and net redemption) at time t as contracted,

For a given financing policy \(\overline {D}\), a levered firm will be over-indebted at time t in state s if the market value of debt exceeds the firm’s market value,

Notice that both definitions refer to a future date t and the state ω from today’s point of view. It can easily be seen that our definition covers also the unlevered firm.

Finally, we assess the consequences of bankruptcy. Consider a firm today with a given financing policy that is in danger of illiquidity at time t in state ω but not over-indebted. The management of the said firm will certainly be able to raise credit in order to ensure the continuance of the firm. If this new financing policy does not result in a lack of liquidity, the bankruptcy problem is solved. The situation could be interpreted as follows: the firm uses the new financing policy for refinancing. Illiquidity turns into a mere postponement of payments.

Yet what happens if the first financing policy in question leads to over-indebtedness at date t? Refinancing as in the previous paragraph is not possible since the “substance” of the firm, namely its expected future cash flows, does not suffice to satisfy the creditors’ payment claims. Moreover, we assume that credit is only granted for a single period. Therefore, the creditors anticipate at date t − 1 that the loan will not be repaid in full in t. Consequently, rational creditors will not agree to issue the necessary credit in time t − 1 which again has an impact on the loan granted in t − 2. As a result, we conclude that the creditors are able to detect later over-indebtedness already in t = 0. Within our framework we thus conclude that over-indebted companies are unable to realize their initial financing strategy.

Valuation of Defaulting Firms

The debt holders behave rationally. Therefore, the fundamental theorem of asset pricing is applicable for debt and we have for any time being if \(\widetilde {R}_{s+1}\) is paid off in s + 1

Using rule 5 this gives us

and with rule 4 for all s ≥ t finally

Entering in Eq. (3.15) results in

This equation is not at all different from Eq. (3.11), through which we had precluded bankruptcy risks! That means that including the default risk has no impact whatsoever on the firm’s value. If the financing policy concerns the credit amounts agreed upon, then we do not need to differentiate in the valuation equations between whether the bankruptcy risks are given or not. Just the possibility of default changes absolutely nothing in the valuation equations.

If this outcome is taken seriously, then it seems that even given the risk of bankruptcy, the value of firms can be successfully calculated with the DCF theory. It has of course to be examined if the conditions of the theory are still satisfied even when there are risks of default. And this is exactly where problems could come up: if the danger of going into default exists for the firm, it can happen that the creditors will not want to grant credit to the same extent they would if there was no risk of default. A financing policy which was agreed upon to the neglect of risks of default can no longer be maintained when considering these risks. But if the financing policies differ from each other with and without the inclusion of the risk of default, then the respective values of firms no longer correspond to each other either.

The message of this subsection can be summed up as follows: The problems of valuing firms when the risk of default exists do not lie in the failure of the DCF theory. On the contrary, this theory remains valid. The difficulties of taking the risks of default into consideration lie much more so in that the financing policies which are relevant for the firm must be formulated with more deliberation.

Over-Indebtedness Implies Danger of Illiquidity

Another important implication of Eq. (3.19) concerns the relation of the two bankruptcy triggers.

Disregarding specific assumptions concerning the dynamics of the free cash flows, we can prove that over-indebtedness implies illiquidity. This result is immediately apparent. Just realize that debts represent the present value of cash outflows while assets represent the present value of cash inflows. Having said this, it must be that at some future point of time an outflow is greater than an inflow if debts exceed assets today.

This result is everything but trivial. To this end, consider an unlevered company whose market value contains information about its future cash flows. If we know that this market value is negative, this means that the owners of the company expect (at least in some states, not necessarily in all) that future cash flows are negative as well. That the same idea is true for levered firms is proven in the following theorem.

Theorem 3.5 (Over-Indebtedness Implies Danger of Illiquidity)

If a levered company is over-indebted at time t in some state, then there is a date s ≥ t and a state where the firm is in danger of illiquidity.

Notice that illiquidity does not necessarily imply over-indebtedness.Footnote 20

We prove the theorem by contradiction. To this end, we consider an over-indebted firm that will never be in danger of illiquidity. In this case the inequality

applies for all states ω ∈ Ω and times s ≥ t. Multiplying the preceding inequality by the risk-neutral probabilities and summing up leads to

Dividing by (1 + rf)s−t and adding up over all t results in

Now, (3.18) implies that this sum is nothing more than \(\widetilde {D}_t\) because if debt \(\widetilde {D}_t\) is granted the debtor will get \(\widetilde {\,I\,}_{s}+\widetilde {R}_{s}\) for all s > t (see also Problem 1). Since the term on the left-hand side of the inequality is the firm value \(\widetilde {V}^l_t\), we have a contradiction to over-indebtedness. This was to be shown.

Cost of Debt

If debt were completely riskless, there would be no reason to negotiate an interest rate different from rf with the creditor. Since we will later consider default it might be that in some (possibly very uncertain) states of the world the payments for interest and redemption lie below the riskless rate and therefore the firm demands a higher interest rate in the remaining states. Analogous to the cost of equity this requires a definition of cost of debt. Someone who invests \(\widetilde {D}_t\) today is entitled to payments amounting to \(\widetilde {D}_t+\widetilde {\,I\,}_{t+1}\) less remission of debts. Due to a remission of debts of \(\widetilde {D}_t-\widetilde {D}_{t+1}-\widetilde {R}_{t+1}\), we obtain the following definition.

Definition 3.4 (Cost of Debt)

The cost of debt \(\widetilde {k}^{D}_t\) of a levered firm are conditional expected returns

However, unless there is the probability of default there is no reason whatsoever to assume that the cost of debt is different from the riskless rate

Notice that we do not require the cost of debt to be deterministic today. Although this will be a necessary requirement for different types of cost of capital later,Footnote 21 cost of debt will not be used itself to determine the value of firms and hence need not to be deterministic.

3.2.6 Example (Finite Case Continued)

Let us turn back to our finite example and suppose a tax rate of τ = 50%. Now we will go into the question as to if a particular finance policy can lead to bankruptcy and, if possible, complete our model in a suitable way. To this end let us assume that the provisional (riskless) leverage policy takes the form

We want to evaluate the cash flow \(\widetilde {\mathit {FCF}}^l_t\) of the levered firm with default risk.

In the case of no default the claims of the shareholders at time t amount to

In order to calculate these claims correctly we have to take our assumptions into consideration. First, the unlevered firm’s gross cash flow must not be different from those of the levered firm (Assumption 3.2). Second, the unlevered firm’s tax base must only be different from that of the levered firm by the paid interest and the cancelled debt as in (3.14).