Abstract

Housing supply restrictions, including historic preservation policies, minimum lot sizes and height limitations, are typically approached with static Pigouvian tools, but these policies also have dynamic implications. Restricted supply will typically make quantities, which determine construction employment, less volatile, and prices, which determine financial stability, more volatile. A prominent exception occurs when supply-unconstrained areas build so much during a boom that construction halts during the bust, and in that case, elastic supply can be associated with both price volatility and a limited ability to use credit instruments to boost employment during a bust. As institutions with counter-cyclical missions grapple with housing policies, they must recognize that housing regulation interacts with monetary policy, and that reforming housing policy may have implications for the business cycle.

I am grateful for financial support to the Taubman Center for State and Local Government. I received helpful comments from seminar participants at the Netherlands Bank.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

1 Introduction

A large literature now documents that housing supply restrictions can increase housing prices, decrease construction and even distort national productivity (Katz and Rosen 1987; Glaeser et al. 2005; Hsieh and Moretti 2017). Almost all of the policy analysis of these restrictions, which are even more prevalent in Europe than in the U.S., focuses on static microeconomic issues, such as the negative externalities from new construction (Glaeser et al. 2005; Glaeser and Ward 2009). Yet there are also dynamic implications of restricting housing supply, and these dynamic implications matter both for counter-recessionary policy and for reforming land-use policies.

Real estate is a major asset class, and real estate busts are often associated with the onset of larger banking crises, such as the Asian financial crisis of 1997 and the global financial crisis that began in 2007. Looking forward, the great Chinese housing boom may also end up having consequences for the global economy. The elasticity of housing supply helps determine whether a real estate boom ends in a financial crisis or an employment crisis, or both.

When real estate booms are modest, then the intuition of supply and demand holds. Elastic areas, like the American south, will see larger fluctuations in the amount of building, and hence the amount of construction employment. Inelastic areas, including much of urban Europe, will see larger fluctuations in prices, and smaller construction fluctuations, which is more likely to generate major shifts in the balance sheets of financial organizations that are long in real estate. When real estate booms are so large that construction disappears in the ensuing bust, then more elastic supply may be associated with larger busts in both price and employment, which is what was observed in Phoenix and Las Vegas after 2007.

In highly elastic areas, credit market interventions will generally shift the level of construction rather than price, and hence this will boost employment but do less to help underwater buyers and their creditors. In inelastic areas or elastic areas with excessive overbuilding, credit market interventions will impact price, rather than employment, directly. In boom periods, such price increases would normally increase consumption (Case et al. 2005), but during busts underwater borrowers are often unable to borrow against their housing value and so the consumption effects will be muted (Ganong and Noel 2017). If, during a boom, the level of excess supply reaches the point that construction is likely to disappear entirely during the bust, then the central bank must expect that its counter-recessionary tools will be quite limited.

One message of this paper is that financial market interventions, like monetary easing, that impact the willingness-to-pay for housing, are mediated by the physical limitations on housing markets. Credit-related interventions that are meant to make housing more affordable, such as raising loan-to-income limits, will have little impact on housing consumption unless building restrictions are also eased. The second message is that housing-market reform must consider the implications for cycles. If European countries were to adopt a more permissive construction policy, then they would presumably be exchanging an environment with more price volatility for an environment with more employment volatility. That shift might require less bank oversight and better unemployment insurance in the construction industry. If it is less dangerous for the larger economy to relax building restrictions during a boom, then given the slow pace of reform it may be necessary to start planning those reforms years in advance, even during a bust.

2 Hot Property Markets and the Microeconomics of Construction Constraints

If you had asked the residents of Amsterdam or New York City in 1978 what their city’s largest problems 40 years in the future would be, few would have said the high cost of housing. Many might have mentioned crime or urban unemployment or the loss of manufacturing jobs. Indeed, those who bought homes and apartments in those years were seen as gigantic risk-takers, buying themselves a seat on an urban Lusitania.

Four decades later, Amsterdam and New York are rich and safe. Both found post-industrial future in information-intensive industries, such as finance, which recall the erstwhile prominence of the Dutch West Indies Company in both places. The loss of the industrial base can even seem like an asset, since pollution fled along with the factories. Indeed, almost none of the front-page problems from the 1970s remained on a primary concern. Moreover, both Amsterdam and New York manage to succeed as centers of consumption, as well as production, as shown by the ability of both cities to attract tourists and reverse commuters.

But economic revitalization and declining crime rates meant an increase in demand for real estate. This revitalized demand was met in both places by quiescent supply. In both cities, height restriction and historic preservation limit the ability of private new construction to satiate demand. In the decades after World War II, the Netherlands built a great deal of social housing and New York City built massive public housing structures. While the Dutch social housing system is far more successful than its public housing counterpart within the U.S., both cities reduced their new supplies of public housing in recent decades. As rising demand hit fixed supply, prices rose dramatically.

The scarcity of urban space is one cause of the social unrest that is linked to urban inequality and gentrification. The demand of the rich for urban space would not be so harmful to the poor if living space was elastically supplied. When houses are in short supply and real estate becomes a zero-sum game, then a boost in demand from the rich raises prices for the poor.

Progressive leaders now see the costs of the limited housing supply, but instead of deregulating, they promote new regulations, such as inclusionary zoning, meant to supply a modest number of “affordable units.” These units are then allocated to lucky lottery winners. Under Mayor Bloomberg, developers could choose to include affordable units and would be rewarded with the ability to build up. Under Mayor DeBlasio, inclusionary zoning has become mandatory. Conventional microeconomics suggests that mandatory inclusionary zoning represents a tax on the construction of market-rate units to subsidize non-market rate units.

Microeconomic analysis tries to measure the negative externalities from construction, and then finds that those externalities, at least in New York and Massachusetts, are far smaller than the implicit tax of building that is created by zoning (Glaeser et al. 2005; Glaeser and Ward 2009). De Groot et al. (2015) present the closest similar analysis for the Netherlands. The case for restricting new construction is certainly stronger in central Amsterdam, which is truly part of the cultural patrimony of the world, than it is in most of New York.

The public debate about high housing prices, macroeconomic evidence suggesting that restrictions can distort the entire economy (Hsieh and Moretti 2017) and concern about real estate as a vast asset class have increasingly lead macroeconomists to take an interest into hot property markets. That interest is most welcome, especially since macroeconomically oriented entities, like central banks, typically enjoy a privileged place in policy debates. Yet as macroeconomists turn their minds to housing supply, they should also consider the implications that housing supply restrictions have for the business cycle.

3 Housing Bubbles, Credit Conditions and Extrapolative Beliefs

Housing markets are typically volatile, moved both by changing economic fundamentals and by shifts in beliefs that seem closer to animal spirits. In the U.S., there is strong momentum in housing-price changes over 1-year frequencies, and strong mean reversion over 5 year frequencies. Both facts are compatible with a model in which semi-rational buyers extrapolate underlying trends from recent growth in housing prices (Glaeser and Nathanson 2017).

The most popular rational explanations for wide swings in housing prices is that they are being driven by credit conditions, either borrowing rates or approval rates. Glaeser et al. (2012) present theory and data suggesting that swings in interest rates were far too small to explain much of the price boom and bust between 2000 and 2010 within the U.S., at least if we assume buyer rationality. If buyers are not rational, then interest rates could play a role in generating price swings perhaps by generating small price movements that then lead to extrapolative bubbles.

In this section, we take the existence and macroeconomic importance of housing bubbles as given, and ask what impact housing-supply restrictions will have on the housing cycle and on macroeconomic responses to that cycle. I present a simple model of housing volatility that is based on Glaeser et al. (2008). I first (and primarily) treat the case where housing volatility is generated by an irrationally overoptimistic belief in high future housing prices. I then speculate briefly on the impacts of housing supply when bubbly beliefs become more endogenous.

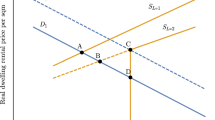

The flow utility from owning a house is a function of an exogenous demand shift (At) and the overall number of households (Nt) and so equals At − γNt. The temporal indifference condition is that Pt = At − γNt + βδE(Pt+1), so that the price equals the flow utility plus the discounted expected value of the price tomorrow, where β is the discount factor and 1 − δ represents the depreciation of the housing stock. The cost of supplying housing is a function of the flow of new housing construction, denoted It, and this must equal the expected price next period so that Ct + c1It = E(Pt+1). Finally, the flow of motion for the housing stock is that Nt+1 = δNt + It, where δ represents the share of housing that remains after each period.

If the exogenous parameters are fixed so that Ct = C and At = A, then the steady state values for population and price (N and P) equal \( \overset{\sim}{N}=\frac{A-C\left(1-\beta \delta \right)}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) and \( \overset{\sim}{P}=\frac{c_1\left(1-\delta \right)A+\gamma C}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \). With fully rational actors, then given any starting value Nt(as long as \( \frac{\left(1-\theta \right)}{\left(\delta -\theta \right)}\overset{\sim}{N}>{N}_t \) which implies that Pt+1 is greater than C), \( {N}_{t+j}=\overset{\sim}{N}+{\theta}^j\left({N}_t-\overset{\sim}{N}\right) \), \( {I}_{t+j}=\left(1-\delta \right)\overset{\sim}{N}+{\theta}^{j-1}\left(\theta -\delta \right)\left({N}_t-\overset{\sim}{N}\right) \) and \( {P}_{t+j}=\frac{c_1\left(1-\delta \right)A+\gamma C}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma}+{c}_1{\theta}^{j-1}\left(\theta -\delta \right)\left({N}_t-\overset{\sim}{N}\right) \), where \( \theta =\frac{\left(\left(1+\beta {\delta}^2\right){c}_1+\gamma \right)-\sqrt{{\left(\left(1+\beta {\delta}^2\right){c}_1+\gamma \right)}^2-4\beta {\delta}^2{c}_1^2}}{2\beta \delta {c}_1}<\delta \).

If \( \frac{\left(1-\theta \right)}{\left(\delta -\theta \right)}\overset{\sim}{N}<{N}_t \), then we have reached the vertical part of the supply curve, and It+j = 0, until \( \frac{\left(1-\theta \right)}{\left(\delta -\theta \right)}\overset{\sim}{N}>{N}_{t+j} \). If t + k denotes the time period in which building begins again, then \( \frac{N_{t+k}}{1-\delta}>\frac{\left(1-\theta \right)}{\left(\delta -\theta \right)}\overset{\sim}{N}>{N}_{t+k} \). At time t + k, \( {P}_{t+k}=C+{c}_1\left(1-\delta \right)\overset{\sim}{N}+{c}_1{\theta}^{j-1}\left(\theta -\delta \right)\left({\left(1-\delta \right)}^k{N}_t-\overset{\sim}{N}\right) \). Iterating, the prices during earlier periods satisfy \( {P}_{t+j}=\frac{1-{\left(\beta \delta \right)}^{k-j}}{1-\beta \delta}A-\frac{1-{\left(\beta \delta \left(1-\delta \right)\right)}^{k-j}}{1-\beta \delta \left(1-\delta \right)}\gamma {\left(1-\delta \right)}^j{N}_t+{\left(\beta \delta \right)}^{k-j}{P}_{t+k} \).

We can interpret bubbles in this model as errors about future values of A (or C). For example, assume that in time t, the city is in steady state, and builder (and buyers) believe that next period the new value of A will equal φ + A, with φ > 0. This belief implies that the new steady-state population will be \( \frac{A+\varphi -C\left(1-\beta \delta \right)}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \). Consequently, while the bubble lasts, \( {I}_t=\frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)+\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) and \( {P}_t=C+{c}_1\frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)+\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \), which means that price has increased by \( \frac{c_1\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) (relative to the steady state) due to the belief bubble and quantity has increased by \( \frac{\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \).

If the bubble lasts exactly one period (I am being consciously vague about the length of a period), then buyers and builders recognize that there has been an error and that there has been too much building. If \( \frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)}{\left(\delta -\theta \right)\left(1-\theta \right)}>\varphi \) so that \( \frac{\left(1-\theta \right)}{\left(\delta -\theta \right)}\overset{\sim}{N}>{N}_t \), then there is building even after the bubble. In that case, the post-bubble level of housing construction will equal \( {I}_t=\frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)-\left(\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \), which represents a fall of \( \frac{\left(\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) relative to pre-bubble levels, and \( \frac{\left(1+\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) relative to the level during the bubble \( C+{c}_1\left(1-\delta \right)\overset{\sim}{N}+{c}_1{\theta}^{j-1}\left(\theta -\delta \right)\left({N}_t-\overset{\sim}{N}\right) \).

The price in the first period of the bust will equal \( \frac{c_1\left(1-\delta \right)A+\gamma C-{c}_1\left(\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \), which is a decline of \( \frac{c_1\left(\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \), relative to prices before the bubble, and of \( \frac{c_1\left(1+\delta -\theta \right)\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) relative to the bubble’s peak. Booms will have smaller effects on construction and larger effects on prices in places with inelastic housing supply. This result is an unsurprising application of the basic logic of introductory economics, but it fails if the boom is sufficiently large.

If (1 − δ)(A − C(1 − βδ)) < (δ − θ)(1 − θ)φ, then the boom generates so much an oversupply of housing that there will be no construction during the immediate recovery. In that case, construction will fall by \( \frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)+\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) relative to the bubble and \( \frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma} \) relative to the pre-bubble period. More elastic areas will have the largest drops in construction, and presumably employment as well. These areas had the most employment to lose, and the elastic regions overbuilt by the larger amount.

The price during the bust will equal \( \frac{1-{\left(\beta \delta \right)}^k}{1-\beta \delta}A-\frac{1-{\left(\beta \delta \left(1-\delta \right)\right)}^k}{1-\beta \delta \left(1-\delta \right)}\gamma \frac{\left(1-\delta \right)\left(A-C\left(1-\beta \delta \right)\right)+\left(1-\theta \right)\varphi}{c_1\left(1-\beta \delta \right)\left(1-\delta \right)+\gamma}+{\left(\beta \delta \right)}^k{P}_{t+k} \). When there is no construction during the bust, more elastic supply will lead to a larger price drop because there was so much overbuilding. This result may capture the experience of places like Las Vegas and Phoenix, where supply was enormous during the boom, and the crash was also enormous. The puzzle about these cities is that buyers during the boom seemed oblivious to the fact that these areas were elastically supplied with housing.

This discussion treated the size of the erroneous belief as given, but it also seems quite plausible that overoptimism is easier to sustain in markets where supply is constrained. Homes along the Keizersgracht are in fixed supply. The view is lovely and urbane and we can easily believe that a greater fool will show up shortly who is willing to by the home at an even higher price. It is almost impossible for economists to know whether a rare and intrinsically attractive product in fixed supply is overpriced or underpriced. Conversely, economics has a clear prediction about the equilibrium price of products that are generated flexibly with a simple constant-returns-to-scale production technology, which is true of housing in many markets, such as Houston. If bubbles are more likely to occur in supply-constrained settings, then the extra volatility of price bubbles generates another reason why macroeconomists should be interested in housing supply.

3.1 Housing Supply Elasticity and Counter-Recessionary Policy

After the bust, the monetary authority may try to boost the demand for housing, with low interest rates and other credit market interventions. Any sort of full analysis of interest rates is beyond the scope of this paper. I treat an interest rate intervention as an increase in the value of the discount factor, β. As long as the bubble was modest, a reduction in the interest rate will increase the value of housing and boost the amount of construction. Moreover, the impact of lower interest rates on prices will be higher in places where housing supply is more inelastic. The impact of lower interest rates on construction employment will be higher in places where housing supply is more elastic.

If the ultimate goal of monetary policy is to increase labor demand, then low interest rates should do this directly through the construction sector in places that have inelastic supply for housing. In places where the supply of housing is inelastic, then the impact of lower interest rates on the economy must either come from outside the housing sector, or through wealth effects. While Case et al. (2005) find significant effects of housing wealth on consumption, Ganong and Noel (2017) find that these effects are muted during the Great Recession, possibly because people cannot borrow against their houses during the downturn.

This logic suggests that in unconstrained areas, like Texas, macroeconomic policy should worry primarily about layoffs associated with a downturn in the housing market. Robust unemployment insurance may be a natural means of protecting against the job loss. In constrained areas, housing fluctuations will appear mostly in changing housing prices. Larger price changes may require more financial regulation that anticipates housing price volatility. Specifically, it may be sensible for regulators to consider any historic tendency towards mean reversion of housing prices when imposing balance-sheet requirements on lenders.

If the bubble is big enough so that there is no ex post construction, then marginal changes in the interest rate will certainly not induce any change in construction levels or in construction employment. The price effects of changes in the interest rate can be significant. Yet again, those price effects may not translate into consumption and employment if people are unable to borrow against their housing wealth. Consequently, housing and real estate cycles have the potential to end up in recessions where standard monetary policy tools have little ability to impact the economy through the housing sector.

The relative impotence of monetary policy during a bust suggests the stronger need for macro-prudential policies during a boom. This analysis suggests that big housing booms are not just larger versions of small housing booms, but they lead to a categorically more difficult situation ex post. Consequently, it may be sensible to lean aggressively against big building booms, even if smaller building booms can be safely ignored.

4 The Complementarities Between Housing and Macroeconomic Policy

I now turn to the topic of housing market reform, particularly in the Netherlands. I first discuss some microeconomic considerations, and the turn to housing reform and the business cycle. I end this section by discussing the timing of land reform over the course of the business cycle.

The basic microeconomic case for building reform in the Netherlands, and much of Europe and coastal America, is that prices are far higher than construction costs. This fact does not imply that there should be more building everywhere. The distinctive beauty and character of Amsterdam could easily be destroyed by massive rebuilding in the city center. Yet, I suspect that there are places in the Netherlands where the difference between the willingness to pay and the marginal cost of construction are higher than any plausible negative externality from new building.

Even though the Netherlands is small geographically, the space needs of the Netherlands are likely to be limited, at least by U.S. standards. If the country needed to build one million more housing units, that might require about 100 million square meters of built space. The number of square kilometers required to deliver this space is 100 divided by the maximum Floor Area Ration (FAR), the average height at which building is possible.

At an average FAR of 10 (which is extremely high), one million homes require only 10 km2, which is a circle with a radius of 1.8 km. At an average FAR of 5, one million homes require only a circle of land with a radius of 2.5 km. Large housing-supply growth is compatible with very modest loss of land, and little disturbance of historic city centers, as long as heights can be high enough.

Naturally enough, there would have to be sufficient demand for these higher-rise dwellings to justify their construction, which generates a link between the land use deregulation and transit access. For new construction to generate the most value, it needs to be in areas that are within easy commuting distance of the economic centers of the Netherlands, which include Amsterdam, Rotterdam and Brabant.

These then are the key ingredients in the microeconomic considerations around housing space. How much land to decontrol? How much density to allow in that land? How close will the land be to central cities? How much transportation access will there be? It is not the place of this essay to resolve these issues, but rather to stress that as macroeconomists enter into these debates, they must also consider other questions.

A more elastic supply of space in the long run, which means easier new building and easier rebuilding, seems likely to lead to more housing consumption and lower prices. More consumption means more construction employment and more volatile construction employment. Construction employment also means more immigration and more volatile immigration.

Macroeconomists should recognize that added employment volatility may be a downside of allowing more building, but that downside should be offset by decreasing housing-price volatility. As loan defaults are far rarer in the Netherlands than in the U.S. because of full recourse mortgages, this reduction in price volatility may be less important than it would be in the U.S. context. If Dutch consumers also spent their housing wealth, then increased price stability would lead to less consumption volatility.

Yet even if there was more elastic supply on the urban edge, some areas of the Netherlands would still be quite constrained. Owners within those areas could still experience large changes in housing wealth, even if prices on the urban edge were more fixed. Consequently, it is possible that increasingly elastic housing supply could boost employment volatility while still maintaining large amounts of price volatility among the most valuable Dutch homes.

I suspect it is unlikely that the Netherlands could ever experience a massive housing overbuild of the form seen in Las Vegas, Phoenix and possibly Spain in 2006. Still, if deregulation were massively successful, macroeconomically oriented entities would still need to display some prudential care against the possibility of such events.

A final issue is the relation between the business cycle and the timing of land reform. Typically, interest in land-market reforms heats up when prices are rising during a boom. This process occurred in Massaschusetts between 2003 and 2006. A similar interest in land-use control reform is going on now in coastal California. Yet interest in such reform then disappears during a bust for understandable reasons.

Voters are far less interested in reducing housing prices during a recession. Cyclical concerns also suggest that hammering a down market further may be counter-productive. Surely, it would be far easier and economically healthier for housing market deregulation to coincide with the upswing in a market. Yet achieving this happy coincidence will not be easy, given the long delays in generating anything as contentious as land deregulation.

If deregulation is going to coincide with an upswing, then almost surely there needs to be enabling legislation passed during a downswing that will make progress relatively quick once prices start to move again. A similar argument also suggests that any desired reductions in public support for housing market entities like Fannie Mae and Freddie Mac should be set in motion during a downturn, but then implemented during an upturn.

5 Conclusion

Housing is typically analyzed through a static, or at least non-cyclical perspective. Yet housing markets frequently display enormous booms and busts that move larger financial markets along with them. The increasingly inelastic supply of housing in cities like Amsterdam seems likely to make housing-price fluctuations more severe, which increases the need for sound macro-prudential polices that protect against price drops. Conversely, there is less need to worry about large drops in construction employment.

Generally, we need worry less about price fluctuations in areas where housing supply is elastic, such as Texas, except when bubbles become so extreme that construction completely disappears during a bust. In those cases, elastic supply can be associated with extreme shifts in both price and quantity. Ex-post attempts to boost housing prices in these areas may have little impact on either employment or consumption if borrowers are largely underwater. In China, today, there are many third- and fourth-tier cities where construction has been enormous and there is at least the possibility of large price drops.

Going forward, macroeconomic policy should take the microeconomics of housing markets more seriously. Housing policy should consider more seriously the macroeconomic implications of any changes that would impact the elasticity of housing supply. The need to bring together the financial and the real sides of the housing markets is one of the clearest implications of the housing bust of 2007 and the Great Recession that followed it.

References

Case, K. E., Quigley, J. M., & Shiller, R. J. (2005, May). Comparing wealth effects: The stock market versus the housing market. The B.E. Journal of Macroeconomics (De Gruyter), 5(1), 1–34.

De Groot, H. L. F., Marlet, G., Teulings, C., & Vermeulen, W. (2015). Cities and the urban land premium. Cheltenham: Edward Elgar Publishing.

Ganong, P., & Noel, P. (2017). The effect of debt on default and consumption: Evidence from housing policy in the great recession (Unpublished Working Paper).

Glaeser, E. L., & Nathanson, C. G. (2017). An extrapolative model of house price dynamics. Journal of Financial Economics, 126(1), 147–170.

Glaeser, E. L., & Ward, B. A. (2009). The causes and consequences of land use regulation: Evidence from greater Boston. Journal of Urban Economics, 65(3), 265–278.

Glaeser, E. L., Gyourko, J., & Saks, R. (2005). Why is Manhattan so expensive? Regulation and the rise in housing prices. The Journal of Law and Economics, 48(2), 331–369.

Glaeser, E. L., Gyourko, J., & Saiz, A. (2008). Housing supply and housing bubbles. Journal of Urban Economics, 64, 198–217.

Glaeser, E. L., Gottlieb, J. D., & Gyourko, J. (2012). Can cheap credit explain the housing boom? In Housing and the financial crisis (pp. 301–359). Chicago: University of Chicago Press.

Hsieh, C.-T., & Moretti, E. (2017). Housing constraints and spatial misallocation (NBER Working Paper # 21154).

Katz, L., & Rosen, K. T. (1987). The interjurisdictional effects of growth controls on housing prices. The Journal of Law and Economics, 30(1), 149–160.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2019 The Author(s)

About this chapter

Cite this chapter

Glaeser, E.L. (2019). The Macroeconomic Implications of Housing Supply Restrictions. In: Nijskens, R., Lohuis, M., Hilbers, P., Heeringa, W. (eds) Hot Property. Springer, Cham. https://doi.org/10.1007/978-3-030-11674-3_8

Download citation

DOI: https://doi.org/10.1007/978-3-030-11674-3_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-11673-6

Online ISBN: 978-3-030-11674-3

eBook Packages: Economics and FinanceEconomics and Finance (R0)