Abstract

In this study, we investigate how total factor productivity (TFP), alongside income, price, and population, shapes energy consumption in the long-run in Saudi Arabia, the world’s number one oil exporter. To do so, we first estimate a production function and construct the associated TFP series, and then assess TFP’s impact on energy consumption. To take into consideration the stochastic properties of the variables, we employ unit root and cointegration methods. We also correct estimations and test results for potential small sample bias. Our main finding is that TFP has a statistically significant impact on energy consumption in the long-run. The main contribution of our research is that to the best of our knowledge this is the first study that estimates energy consumption effects of TFP for Saudi Arabia. We believe that our research would be useful for Saudi Arabian policymakers in understanding how TFP, a representation of technological progress, institutional development, innovations, openness, and R&D development, influences energy consumption over time. Saudi Vision 2030, the strategic road map of Saudi Arabian development, implies rational behavior and lowering the pace of energy consumption in the country. Thus, TFP improvement is a sustainable way to attain these goals.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The study of productivity is a very important topic in the applied literature, as the analysis of productivity is crucial to an understanding of the economy and how it changes. The pursuit of productivity growth and productivity stimulation is also one of the central goals that emerging countries are pursuing in the face of globalization. In the past, changes in gross domestic product per capita were used as a simple measure of output growth and productivity growth. The more recent sophistication of the empirical analysis of productivity has highlighted the importance of the developments in production technology and the efficiency whose dynamics can be represented by total factor productivity (TFP). Among the many lines of analysis, there is the analysis of the role of energy in the economic growth of many developing countries, pioneered by the study of Kraft and Kraft [1], who unveiled the causal relation between energy consumption and economic growth. In addition, the new environmental awareness has highlighted that economic development may create a conflict with environmental sustainability, addressing the issue of enhancing productivity to mitigate the impact of energy consumption on economic growth through deterioration of the quality of the environment. Most of the recent literature has continued to investigate the impact of energy consumption on TFP ([2,3,4] inter alia). At the same time, one can think that TFP as a representative of technological progress and efficiency measures may also have certain implications in lowering energy consumption. Theoretically, it can be derived from the production function framework and empirically; some studies (e.g., see [4,5,6]) have found the causality running from TFP to energy consumption. However, to the best of our knowledge, there has not been a comprehensive investigation of the impact of TFP on energy consumption.

In this study, we conduct an econometric analysis of how TFP alongside income, price, and population shapes energy consumption in Saudi Arabia, the world’s number one oil exporter. We believe that there is a value in conducting this analysis for developed, developing, and less-developed countries. For Saudi Arabia, it would be additionally useful because of the following two reasons. First, there is a policy willing to stimulate rational consumption of energy as highlighted in the Fiscal Balance Program of Saudi Vision 2030 [7]. Second, a number of studies show that domestic energy consumption in Saudi Arabia is considerably high compared to other similar countries, which can lead to some consequences [8,9,10,11,12]. Both of these would imply lowering the pace of domestic energy consumption, for which TFP can be considered as one of the sustainable factors. We first estimate the production function, construct the TFP series, and then explore its impact on energy consumption over the period 1989–2015.

The key finding of this study is that TFP has a statistically significant negative effect on energy consumption in the long-run, which is theoretically expected and empirically explainable. We also find that income and population have a positive impact on energy consumption while energy price is negatively associated with energy consumption. To the best of our knowledge, this is the first study that estimates the long-run energy consumption effects of TFP in the case of Saudi Arabia and, thus, intends to fill this gap in the literature. This is the main contribution of this research. Another contribution is that the study employs different unit root and cointegration methods in testing and estimating the long-run elasticities to get robust results. Also, it applies a small sample bias correction to the obtained estimations and test results. We believe that our research would be useful for Saudi Arabian policymakers to understand how TFP as a representation of factors such as technological progress, institutional development, innovations, openness, and R&D development can shape energy consumption over time in Saudi Arabia. This understanding can be helpful particularly in implementating policy measures aimed at achieving some targets in Saudi Vision 2030 related to energy efficiency and lowering the pace of energy consumption in the country. Policymakers may also wish to consider how and which factors can be improved to lower energy consumption.

The remainder of the study is organized as follows. Section 2 reviews the related literature. Section 3 presents the theoretical framework, while Sect. 4 discusses the econometric methodology. The data used in the study is documented in Sect. 5. Section 6 conducts an empirical analysis for the production function and TFP calculation, while Sect. 7 analyzes energy consumption. Section 8 discusses the results of the empirical analyses. Section 9 concludes the paper.

2 Literature Review

There is a vast literature devoted to the (potential) causal relationship between energy consumption and economic growth. Ozturk [13], Smyth and Narayan [14], and Hasanov et al. [15] reviewed many of these papers. Unlike the energy consumption-economic growth nexus, few papers investigate the relationship between energy consumption and TFP. In addition, the existing studies mainly focused on causality; only a few investigated the impact of energy consumption on TFP. Again, the first (and main) strand of the existing literature examines the causality between aggregate/disaggregated energy consumption and TFP. Since the main focus of our study is not investigating causality but rather estimating TFP elasticity of energy consumption, we will shortly mention some of the causality-related studies. Tugcu and Tiwari [16] investigate the direction of the causal relationship between different types of energy consumption and TFP growth in the BRICS countries from 1992 to 2012 using the panel bootstrap Granger causality test. The Granger causality and dynamic panel estimation technique is also used in Al-Iriani [17], Costantini and Martini [18], Ladu and Meleddu [6] to examine the long-run relationship between TFP and energy consumption. Jorgenson [19], Kelly et al. [20], and Boyd and Pang [5] investigated the causality impacts between TFP and energy consumption for the US, while Adenikinju [21] did the same for Nigeria, and Sahu and Narayanan [22] for did the same for India. Moreover, Worrell et al. [23] reviewed more than 70 studies examining the effects of energy efficiency on TFP in the case of US industry.

The second strand of the literature is devoted to investigating the impact of energy consumption (aggregate or disaggregated) on TFP. Hisnanick and Kymn [2] studied the impact of petroleum and non-petroleum energy consumption on TFP growth in the US manufacturing sector using data from 1958 to 1985. Using the relationship as described by Eq. (7), and disaggregating energy consumption to petroleum and non-petroleum types, Hisnanick and Kymn [2] investigated the productivity slowdown, analyzing the simple growth rates of manufacturing output and relevant factor inputs. The study concluded that the decline in productivity is mainly influenced by disaggregated energy components, namely petroleum and non-petroleum energy consumption. Likewise, Moghaddasi and Pour [3] studied the impact of energy consumption on agricultural TFP in the case of Iran, using data from 1974 to 2012. The study first estimated the respective elasticities of input factors using the Cobb–Douglas production function and then calculated TFP using the Solow residuals approach. After calculating TFP, the study estimated TFP growth as a function of agricultural energy consumption and concluded that a 1% increase in the sector’s energy consumption leads to a 0.56% decrease in TFP growth. Tugcu [4] studied the impact of three types of energy consumption, namely alternative, fossil, and renewable energy consumption on TFP for the Turkish economy, employing the autoregressive distributed lag (ARDL) bound testing approach to data ranging from 1970 to 2011. The study concludes that renewable energy consumption has a positive impact on TFP, while other two types of energy consumption have a negative impact on TFP. The study calculated TFP using the Cobb–Douglas production function with two factors. In addition, the estimated long-run and short-run elasticities of alternative, fossil, and renewable energy consumption were −0.29, −2.1, and 0.8; −0.24, −1.7, and 0.7, respectively. Furthermore, the study concludes that there are bidirectional causalities between TFP and these types of energy consumption. Ladu and Meleddu [6] examined the causality relationship between energy consumption and TFP for the regions of Italy, applying the dynamic panel estimation technique to the data from 1996 to 2008, and found that there is a bidirectional relationship between the variables. Furthermore, the study concluded that in the short-run, TFP has a negative impact on energy consumption, while its impact is positive in the long-run. The study employed the Cobb–Douglas production function with two inputs in order to calculate TFP.

An interesting stream of this literature focuses on energy productivity. Haider and Ganaie [24] investigated the impact of energy productivity (GDP per unit of energy use), trade openness, and CO2 emissions on TFP employing a vector error correction model (VECM) to Indian data from 1971 to 2013. The study used TFP data from Penn World Table version 8.1 and concluded that energy productivity has a negative impact on TFP. In addition, Haider and Ganaie [24] found that there is one-directional causality from energy productivity to TFP. The long-run energy productivity elasticity of TFP is found to be −0.8. One of the conclusions from the reviewed studies above is that there is causality running from TFP to energy consumption ([4,5,6] inter alia). In addition, from a theoretical point of view, TFP as a representation of factors like improvements in applied equipment and machinery, technological progress, and increases in research and development (R&D) would be expected to reduce energy consumption through efficiency gains—something that could be tested empirically. However, as can be seen from the reviewed literature, there is no study that explicitly estimates the impact of TFP on energy consumption, either in aggregate or in disaggregated form. This is the gap in the existing literature that our study addresses.

3 Theoretical Framework

3.1 TFP Calculation

As detailed in Diewert [25, 26], TFP can be calculated using either direct or indirect methods. Direct methods involve the calculation of an aggregated index as representative of all inputs used in production. Here TFP is approximated as a ratio of output quantity to the aggregated input index. There are two widely used direct TFP calculation methods: the model proposed by Kendrick [27] and the one proposed by Divisia [28] (see Diewert [25] inter alia for detailed information). The indirect methods involve estimating an appropriate production function, from which TFP is calculated. As in direct methods case, there are two often used approaches: Solow residual method and Solow model [29,30,31]. Since we used the Solow residual method, only this method is described here. In this approach, first the logarithm expression of the Cobb–Douglas-type production function in the case of two inputs is estimated econometrically [32, 33]Footnote 1:

where Q, L, and K are output, labor, and capital, respectively. \(\alpha_{1}\) and \(\alpha_{2}\) are the elasticities of output with respect to labor and capital, respectively. \(\ln\) represents the natural logarithm, and t denotes time. If we take derivatives of both sides of (1) with respect to time, and consider that

and

here ∆ is difference operator and ‘\({\prime }\)’ stands for derivative, then we get:

Considering (4) in the expression for derivative, we obtain the below equation:

Here the TFP growth can be found solving (5) for \(\frac{{\Delta A}}{A}\):

With new notations, (6) can be written in the below form:

where \(\dot{\text{tfp}}_{t} = \frac{{{\Delta }A_{t} }}{{A_{t} }}\) is TFP growth, \(\dot{Q}_{t} \,{\text{is}}\,{\text{output}}\,{\text{growth}}\,{\text{and}}\,\dot{L}_{t}\) and \(\dot{K}_{t}\) are growth values of inputs, respectively. From (7), it can be interpreted that growth in TFP is a part of production growth which cannot be explained by the inputs’ growth. \(\dot{\text{tfp}}_{t}\) is called the ‘Solow residual.’

3.2 Energy Consumption Modeling

The conventional energy demand equation can be written as a function of income, Y, and price, P, as follows (see [34, 35] inter alia):

As discussed in Beenstock and Dalziel [36] and recently in Hasanov [37], among other studies, demographic factors, such as population, POP, or population age group, can be considered as drivers of energy consumption [38,39,40,41,42]. Thus, (8) can be augmented to (9):

Finally, (9) can be extended with TFP following the functional specification similar to the one in Nordhaus [34]. Actually, it is not difficult to see how TFP can be included in the energy demand equation in the production function framework (theoretical derivations of this extension are provided in Mikayilov and Hasanov [43]).

Evidently, (10) differs from the conventional energy demand equation as it has TFP as an individual independent variable in the modeling framework. For the econometric estimation purposes of our study here, (10) can be re-written as the following explicit functional form:

where \({\text{ec}}\), \({\text{tfp}}\), \({\text{gdp}}\), \({\text{ep}}\), and \({\text{pop}}\) stand for energy consumption, TFP, gross domestic product, energy price, and population, respectively; e is the error term; \(b_{0} , \ldots , b_{4}\) are the coefficients to be estimated econometrically. It is expected that \(b_{1} < 0\) and \(b_{3} < 0\), while \(b_{2} > 0\) and \(b_{4} > 0\). All variables are in the natural logarithmic form.

4 Econometric Methodology

We begin the investigation by testing the employed variables for unit root. To examine the unit root properties of variables, the augmented Dickey–Fuller (ADF, [44]) and Phillips–Perron (PP, [45]) unit root tests are applied. We also conduct unit root tests with structural breaks, namely the ADF with structural breaks (ADFBP hereafter), which is advanced by Perron [46], Perron and Vogelsang [47, 48], and Vogelsang and Perron [49]. Once the integration order of the variables is identified, the existence of a long-run relationship among the variables should be tested. We employed a bound test for cointegration proposed by Pesaran and Shin [50], and Pesaran et al. [51] as a principal tool in our cointegration analysis. In addition, as a robustness check of the existence of long-run comovement, the Johansen and Juselius [52] and Johansen [53] cointegration test is also used. We select the Johansen test over other cointegration tests given that this is only the test that can deal with more than one cointegrating relationship if more than one explanatory variable is involved in the analysis. Unlike the Johansen method, other cointegration tests assume only one cointegrating relationship between the variables regardless of the number of explanatory variables in the analysis. Obviously, this can lead to improper analysis and inferencing. Also note that we apply the small sample bias correction developed by Reinsel and Ahn [54] and Reimers [55] to the Johansen test results to get more robust conclusions. After determining the cointegration relationship among the variables, the long-run relationship/coefficients need to be estimated. In empirical estimations, the autoregressive distributed lag (ARDL) [50, 51] is used as the main estimation method, since it outperforms other cointegration techniques in the small sample case. As with the cointegration exercise, in empirical estimations of the long-run relationship, we also employed the VECM [52, 53] approach. As the employed unit root tests and cointegration techniques are commonly used methods, they are not described here. Instead, interested readers can refer to Dickey and Fuller [44], Phillips and Perron [45], Enders [56], Stock and Watson [57], and Dolado et al. [58], for the unit root tests, and Pesaran and Shin [50], Pesaran et al. [51], Johansen and Juselius [52], and Johansen [53], for the cointegration tests and techniques.

5 Data

The study uses annual data for Saudi Arabia from 1989 to 2015. The description of the variables is as follows:

-

GDP is real gross domestic product at 2010 prices, measured in million riyals, and used as a proxy for income variable. This data is taken from the General Authority for Statistics of the Kingdom of Saudi Arabia [59].

-

CS is the real total economy capital stock, in million riyals, 2010 prices, calculated based on the perpetual inventory method using the investment data taken from GASTAT [59]. Initial capital output ratio and depreciation rate were set to 1.5 and 5%, respectively, following the related studies for the Saudi Arabian economy ([60, 61] inter alia). This variable is used to measure the capital input.

-

ET is total employment in thousand persons and is taken from GASTAT [59]. This variable is used as a measure for labor input.

-

EC is demand for energy in the total economy, in million tons of oil equivalent (MTOE). It is calculated as the sum of sectorial energy consumption based on IEA data [62]. This is our dependent variable in energy demand specification.

-

POP is the total domestic population, in thousand persons, taken from the United Nations [63] database. POP is used in energy consumption specification as one of the main drivers of energy consumption.

-

EP is the real domestic crude oil price, in riyals per ton of oil equivalent. Nominal price values are collected from different royal decrees and publically available documents of the related government institutions. Then it is deflated by the GDP deflator, 2010 = 100, to get real values. We use the domestic price of crude as a measure for energy prices, since the domestic prices of other energy types in Saudi Arabia are mainly determined by the domestic price of crude.

-

TFP is calculated based on the production function estimation results using the growth accounting framework. Details of the calculation are provided in Sect. 6.3.

The graphs of the variables, in logarithmic forms, are given in Fig. 1, while descriptive statistics are presented in Table 1.

Graphical illustration of the variables

6 Empirical Analysis

This section documents the results of the unit root tests, cointegration tests, and long- and short-run estimations.

6.1 The Unit Root Test Results

Table 2 reports the results of the ADF and PP unit root tests.

It is straightforward that the null hypothesis of unit root cannot be rejected for the log levels of the variables according to both the ADF and PP test results as the upper part of the table presents. Regarding the first differences of the log levels, i.e., growth rates of the variables, again the ADF and PP test results decidedly indicate stationarity for all the variables except for cs. Also pop does not seem to be the first difference stationary according to the PP test statistic. The graphical illustration of cs shows something like a gradual break in its development trend since 2004. Therefore, we apply the ADF test with structural breaks, i.e., ADFBP to cs and Δcs. For cs, we set an intercept and a trend in the test equation and allow a break in trend. Then we specify three lags as a maximum and use the Schwarz selection criteria to determine the optimal lag. Finally, we select innovative break type as the break happens gradually and specify 2004 as the first year of the new regime. The estimated sample ADFBP statistic is −3.49, while the critical values are −4.56, −3.96, and −3.67 at the 1%, 5%, and 10% significance levels. These suggest that cs has a unit root with the structural break. In other words, the variable is non-stationary. If there is a break in the trend of a variable, then there should be a shift in the first difference of it (e.g., see [64, 65]). This implies that Δcs has a shift in its level starting in 2004. In testing ∆cs, we include an intercept and a trend in the test equation and allow a break in the intercept. The rest of the setup is the same as for cs. Now, the estimated sample ADFBP statistic is −4.35, while the critical values are −4.37, −3.76, and −3.46 at the 1%, 5%, and 10% significance levels. This implies that Δcs is stationary at the 5% significance level. Thus, our conclusion for cs is that it is non-stationary at the level but stationary when the first difference is considered both in the presence of the structural break. As for pop variable, the ADF suggests that the variable is I(1) process, i.e., non-stationary in levels but stationary in first differences. Moreover, conventional wisdom and the findings of the earlier studies also indicate that the variable is I(1). Hence, we consider population as an I(1) process. Thus, our conclusion for the unit root test exercise is that all the variables are non-stationary in their levels but are stationary when they are first-differenced, i.e., all the variables follow I(1) processes.

6.2 The Results from the Cointegration Tests and Long-Run Estimations

The conclusion about the integration orders of the variables makes it reasonable for us to test whether our variables are cointegrated. As mentioned in Sect. 4, the ARDL is our main cointegration test and long-run estimation method as we have a small sample size. At the same time, in order to make more proper inferences about the long-run relationship among the variables, we also use the Johansen cointegration tests for robustness.

6.2.1 The Results from ARDL Method

In the ARDL estimation of Eq. (1), we set the maximum lag order to be three and use the Schwarz information criterion to select the optimal lag length following the seminal studies by Pesaran and Shin [50] and Pesaran et al. [51].Footnote 2 The results are reported in Table 3.

Table 3 shows that the selected specification, ARDL (1, 0, 3), successfully passes the serial correlation, ARCH, heteroscedasticity, normality, and mis-specification tests. Besides, the sample value of F-statistic from the Wald test strongly suggests a cointegrating relationship among the variables even after a small sample adjustment. The estimated long-run coefficients of labor and capital have theoretically expected signs and magnitudes, and they are statistically significant.

6.2.2 The Results from Johansen Method

First, we construct a VAR specification for Eq. (1). Intercept and time trend are included in the VAR as exogenous variables. Then, we specify three lags as a maximum order as we did in the ARDL analysis. The Schwarz information criterion, which is more relevant in small samples, suggests two lags as optimum. Additionally, the lag exclusion test shows that two lags should not be reduced to one. Hence, we specify two lags as the optimum which provides non-correlated residuals as tabulated in Panel A of Table 4. The table also reports other diagnostics and also cointegration test results.

Evidently, the residuals of the VAR successfully pass normality and heteroscedasticity tests, and it is stable as no root lies outside the unit circle. The cointegration test option that we employ includes an intercept but not a trend. We select this option as none of the other options provides economically meaningful and statistically significant results.Footnote 3 The adjusted Trace and Max-eigenvalue statistics show that there is only one cointegrating relationship among the variables at the 5% and 10% significance levels, respectively. Since we find a cointegration among the variables, it would be meaningful to estimate this long-run relationship for gdp, although the small sample span here would not allow us to rely on these estimates. Nonetheless, we reported them in Panel F just for comparison purposes. The main message of Sect. 6.2.1 is that the ARDL findings, that there is one cointegrating relationship among the variables, are supported by the Johansen method. Additionally, the estimated long-run elasticities from the methods are quite close to each other.

6.3 Constructing TFP Series

In this section, we first calculate the TFP growth following the growth accounting approach, i.e., using Eq. (7). We use labor and capital elasticities of output estimated using ARDL method reported in Table 3.Footnote 4 Then, we construct the TFP level as we will investigate whether it has an impact on energy consumption in the long-run. The second graph in the second row of Fig. 1 above illustrates the level values of the constructed TFP series. Finally, we compare our constructed TFP growth series with the one retrieved from the Penn World Table [66] for a robustness check. In order to make the TFPs comparable, we re-scaled the PWT TFP from 1 to 100 scale and then take the difference. Figure 2 illustrates both TFPs’ growth patterns.

Calculated TFP and PWT-based TFP, 1989–2015

The time profiles of both series are quite similar. We will not discuss the profiles here, but it is worth mentioning that such a similar pattern would indicate that our estimations and calculations seem quite reasonable.

Our main conclusions from Sect. 6 can be summarized as follows:

-

Our variables can be considered I(1) processes. In other words, they are non-stationary at their log levels and stationary at their growth rates.

-

There is a long-run relationship between output, labor, and capital. This estimated relationship is consistent with production function theory, given both the capital and labor elasticities are positive and the latter is greater than the former.

-

The calculated TFP and given TFP from PWT follow a very similar pattern over the period considered.

7 An Empirical Analysis of Energy Consumption

This section first tests the existence of cointegration between energy consumption and the considered factors in Eq. (11), and then estimates the long-run relationship between them.Footnote 5 Our main cointegration test and long-run estimation tool is the ARDL, and the Johansen method is used for a robustness check as we did in Sect. 6.

7.1 The Results from ARDL Method

The number of explanatory variables in Eq. (11) is twice that of Eq. (1). Besides, we have a small number of observations. Therefore, we set the maximum lag number to one to avoid over-parameterization and save some degree of freedom in the estimations.Footnote 6 If this lag order of one is not sufficient to remove the serial correlation from the residuals of the ARDL estimation, then we will increase the lag order to two or three until we will have serially uncorrelated residuals in our estimations. Fortunately, the estimated ARDL specification, with a maximum lag order of one, does not have any issue with the residuals’ serial correlation. Moreover, it successfully passes all the other post-estimation tests as Table 5 documents.

The sample values of the F-statistic from the Wald tests strongly suggest a cointegrating relationship between energy consumption and the explanatory variables after small sample adjustments. The estimated long-run coefficients of the explanatory variables have the theoretically expected signs and are statistically significant.

7.2 The Results from the Johansen Method

We construct VAR specifications for Eq. (11). Regarding exogenous variables, we included only an intercept since including a time trend leads to instability in the VAR.Footnote 7 Then, we set one lag maximum, as we did in the ARDL analysis, because of the number of variables and small sample size. The Schwarz information criterion, which is more relevant in small samples, as well as the lag exclusion test and lag selection criteria all indicate that one lag is optimal. One lag provides non-correlated residuals as documented in Panel A of Table 6.

Additionally, the estimated VAR is well-behaved in terms of residual diagnostics and stability tests. We employ the cointegration option of intercept but not trend in the test equation. We select this option since none of the other options provide economically meaningful and statistically significant results.Footnote 8 Panel E in the table reports that the adjusted Trace and Max-eigenvalue statistics reject the null hypothesis of no cointegration in favor of the alternative hypothesis of at most one cointegrating relationship among the variables in Eq. (11) at the 1% significance level. We can estimate the numerical values of the long-run relationships for ec as we find that there is a cointegrating relationship among the variables in Eq. (11). However, the sample size that we have does not allow us to rely on these estimates. Nonetheless, we report them in Panel F of the tables just to compare them to the long-run relationships estimated by the ARDL method in Table 5. The finding of the Johansen method supports that of the ARDL, i.e., there is one cointegrating relationship between the variables. Additionally, the estimated long-run elasticities of all the variables from ARDL and the VEC specifications are quite close to each other in magnitude.

8 Discussion

8.1 Unit Root and Cointegration

We concluded that our variables are I(1) processes, i.e., the log level of the variables is non-stationary, but their growth rates are stationary. Non-stationarity implies that impacts to the log level of the variables can result in permanent changes. Such impacts can be internal, as a result of policy, or external, such as fluctuations in oil and other commodity prices or movements in international labor or financial markets. Hence, the (log) levels of the variables should not be used for predicting future trends because of their non-stationarity. Unlike non-stationarity, stationarity implies that any impacts to the variables can create only temporary changes. Therefore, mean, variance, and covariance values of the stationary variables do not change over time as they ‘dance’ around their mean value.Footnote 9 Since we found that the levels of our variables are non-stationary, there is the possibility that the relationship among such variables is meaningless or spurious, unless a theoretically articulated/predicted relationship can be established. Two different tests were used to determine the cointegration properties of our variables. The test results presented in Table 3 and Table 4 indicated that the level relationship between output, labor, and capital is not spurious and it is in line with the theory of production function for the Saudi Arabian economy. The theory of production function simply articulates that labor and capital are the main drivers of economic growth (see, [32, 33]). Likewise, the test results reported in Tables 5 and 6 showed that the level of energy consumption moves together with the levels of income, price, population, and TFP in the long-run. In other words, the variables established a long-run relationship, which can be explained theoretically. Indeed, the theory of consumption predicts that income and price are its main determinants.

8.2 Production Function, TFP Calculation, and Growth Accounting

Again, we found a long-run relationship between output, labor, and capital in the Saudi Arabian economy, which is consistent with the theory of production. The results of the long-run estimations using ARDL reported in Table 3 and those obtained from the Johansen method reported in Table 4 are quite close to each other, which would be an indication of robustness. According to the results, a 1% increase in employment is associated with a 0.6% increase in GDP in the long-run ceteris paribus. Likewise, the Saudi Arabian economy grows by 0.2% if the capital stock increases by 1% in the long-run if other factors are constant. Both findings are, again, in line with the theory of production and therefore, we think that they do not need any detailed explanation. However, some findings are worth mentioning. It appears that labor has a greater role than capital in the production of goods and services in the Saudi Arabian economy during the period 1989–2015. This finding is in line with the theory of production and economic growth (see, [32, 33, 29,30,31]). We are only aware of one study, Aljebrin [67], that estimates the elasticities of output with respect to labor and capital coefficients of production inputs, being 0.57 and 0.67, respectively. The labor elasticity is very close to ours, while that of the capital stock is higher than what we find. Additionally, Aljebrin [67] finds an increasing return to scale for the Saudi Arabian economy, which would be difficult to justify as its is a developing economy.

The estimations suggest that there are decreasing returns to scale, as the sum of the elasticities is slightly smaller than unity, in the economy during the period considered. A constant return to scale (i.e., the sum of the elasticities equal to one) was rejected statistically. So, there is not a strict one-to-one relationship between production and its inputs. In other words, if both labor and capital increased by 1%, then GDP will increase by 0.84%. We do not conduct a detailed investigation for this as it is beyond the scope of our main focus, which is the relationship between energy consumption and TFP. But it could be an interesting area for future research.

We calculated TFP using growth accounting, and Fig. 1 and 2 illustrate the level and growth rates of TFP, respectively. Overall, the TFP level has an upward trend if we consider the entire period 1989–2015. However, if we ignore the first three years, in which the TFP level has a huge jump, and only consider the remaining period, we observe that its overall trend declines until 2002, then moves upward up to 2008, then declines again, and finally trends up from 2010. This pattern can be associated, among other things, with the dynamics of the international oil price, a factor that plays a significant role in the Saudi Arabian economy. The IMF [68] and Mitra et al. [69], among others, also find a similar association for the TFP in Saudi Arabia. In addition, there is another association between the TFP level and the budget spending since the economy, in particular its fiscal stance, relies on oil exports and thereby oil revenues, which are significantly shaped by the international price of oil. Figure 3 illustrates the TFP level, the price of Arabian Light, and the budget spending on a normalized scale to make them comparable.

TFP level, the price of Arabian Light, and budget spending

Evidently, from the graph, the TFP level follows the dynamics of the oil price and budget spending. This might show that TFP improvements in the Saudi Arabian economy are mainly driven by government support among other determinants such as openness and institutional development.

Finally, we very briefly did a growth accounting to determine how the factors of production contribute to Saudi Arabia's economic growth over time. Table 7 presents the results for sub-periods.

Some findings from this growth accounting are worth mentioning. It seems that the labor contribution was the main driver of economic growth in Saudi Arabia in all periods except for 1989–1994. Also, labor has a growing contribution over time. The capital contribution increases over time, indicating a growing role for capital in economic development. The TFP contribution to economic growth can be characterized as ‘on’ and ‘off.’ We think this is simply because TFP developed with ups and downs as discussed above. Our conclusion from this accounting exercise is that the role of the non-oil sector in economic growth outweighs that of the oil sector. This is because the oil sector is not labor intensive (as is well known). In contrast, the non-oil sector is labor and capital intensive. In fact, Fig. 4 illustrates the growing share of the non-oil sector in the overall economy.

Sector contributions to GDP, %

We compare our findings with those of earlier studies on the Saudi Arabian economy. Our findings are similar in terms of magnitude of calculated TFP for Saudi Arabia to the results of Alkhareif et al. [70], Algarani [71], Mousa [61]. Moreover, Dubey et al. [72] also mentioned that Saudi Arabia experienced slightly positive TFP growth in the non-oil sector.

8.3 Energy Consumption and TFP

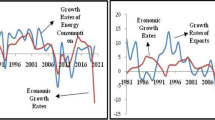

Finally, we estimated the impact of the TFP level on energy consumption in the long-run alongside income, price, and population. For robustness, we used two different approaches, namely the ARDL and Johansen methods. The estimation results from these two methods are documented in Tables 5 and 6, respectively, and are very close to each other. According to the results, a 1% increase in TFP level leads to a 0.9% decrease in energy consumption in the long-run, keeping other factors unchanged. Theoretically, the negative energy consumption effects of TFP can be derived from the production function framework. One explanation for this negative association is that theoretically, TFP is representative of technological progress, institutional development, R&D development, awareness, and the use of efficient technology, which would all lead to efficiency gains and thereby result in less energy consumption. Figure 5 portrays the Saudi Arabian data on energy intensity and TFP on a normalized scale.

Energy intensity and TFP

Evidently from the figure, any increases in TFP coincide with lowering energy intensity and vice versa over the period. One can easily see an empirical negative association between energy consumption and TFP here for the Saudi Arabian economy. Another observation from the figure is that energy intensity has two significant downward level shifts in its path: one since 2003 and another since 2011. The last development not only caused a level downshift but also formed a flatter slope of the energy intensity trend. These developments in energy intensity might be related to the above-mentioned elements of TFP improvements.

Estimation results also show that a 1% increase in income and population cause a 0.2% and 1.5% rise in energy consumption in the long-run, respectively. Besides, the results indicate that energy consumption can be reduced by 0.1% if the energy price is raised by 1%. Since our main interest in this study is TFP, we do not discuss the impacts of income, price, and population in detail. However, the findings are in line with the theoretical expectations and the findings of prior empirical studies of the Saudi Arabian economy, although there are not enough studies using total energy consumption. For example, 0.27 was estimated for the GDP elasticity of total energy consumption both in per capita term by Gazder [11].Footnote 10

9 Conclusions and Policy Insights

As stated in the introduction, the analysis of TFP is very important, and existing studies either estimate the impact of energy consumption on TFP or test for Granger causality between the two. However, to the best of our knowledge, none of the earlier studies examined the impact of TFP on energy consumption, although it is theoretically straightforward and empirically useful to do so. This motivated us to estimate the long-run energy consumption effects of TFP in the Saudi Arabian economy. In the cointegration analysis framework, we first estimated a production function and constructed the associated TFP series. Then we assessed how TFP, alongside income, price, and population, shapes energy consumption in Saudi Arabia, the world’s number one oil exporter. The key finding of this study was that TFP has a statistically significant negative effect on energy consumption in the long-run. We additionally found that income and population have positive impacts on energy consumption, while the energy price has a negative impact.

We believe that our research would be useful in helping Saudi Arabian policymakers to understand how TFP can lower energy consumption in the long-run. Usually, TFP is thought to reflect factors like technological progress, institutional development, innovations, openness and R&D development. In this regard, policymakers could consider how and which of those mentioned factors might be improved, while also considering the stylized facts of the economy, in order to lower the pace of energy consumption. Saudi Vision 2030—the strategic roadmap of Saudi Arabia’s development—implies greater energy efficiency and a lower pace of energy consumption in the country. Thus, TFP improvement would be a sustainable way to obtain these goals.

Change history

28 November 2019

In the original version of the book, the Chapter “How Total Factor Productivity Drives Long-Run Energy Consumption in Saudi Arabia” was not published under the open access category. The category has been changed. The erratum chapter and book have been updated.

Notes

- 1.

At the beginning of the study, we also included energy as a factor of production in (1). However, with the short sample represented by the available data, we could not find any significant impact of energy on production in the empirical analysis. Hence, we excluded it from the empirical analysis.

- 2.

We include two pulse dummy variables to capture the 1999 and 2002 crises in the ARDLBT estimations. Also note that our estimation and testing period here and hereafter is 1992–2015 as our data starts in 1989 and three lags are considered as a maximum.

- 3.

The test results on the other cases can be obtained from the authors under request. Also note that we include the pulse dummy variables in the VAR as we did in the ARDL estimations, but we exclude them when we perform the cointegration test.

- 4.

We prefer the labor and capital elasticities estimated using ARDL to those from the VEC in constructing the TFP because it is well known that the former provides more reliable estimates in the small samples. VEC estimation-based TFP construction can be obtained from the authors in the case of interest. Note that the VEC-based TFP is very similar to the ARDL-based TFP since the estimated numerical values from the methods are quite close to each other.

- 5.

Note that we do not analyze the short-run effects of the TFP and other factors on energy consumption, but this could be considered in future research.

- 6.

We include a pulse dummy in the ARDL estimation as a deterministic regressor to capture an increase in the energy consumption in 2008 which is caused by the boom in the Saudi Arabian economy in the same year as it is not fully captured by GDP. The dummy variable appears statistically significant. However, we do not include it in the long-run estimation.

- 7.

We include a pulse dummy in the estimations as a deterministic exogenous regressor for the same reason as we did in the ARDL estimation (see footnote 5). However, we do not include it in the cointegration test although the inclusion of it does not change the results at all. Details can be obtained from the authors under request.

- 8.

The test results on the other cases can be obtained from the authors on request.

- 9.

Socioeconomic variables follow weak stationarity but not strong stationarity, as their mean, variance, and covariance are not strictly constant over time. Strong stationarity is the case in the natural sciences. A detailed discussion of this can be found in econometrics textbooks (e.g., [56]).

- 10.

References

Kraft J, Kraft A (1978) On the relationship between energy and GNP. J Energy Dev 3:401–403

Hisnanick JJ, Kymn KO (1992) The impact of disaggregated energy on productivity: a study of the US manufacturing sector, 1958–1985. Energy Econ 14:274–8

Moghaddasi R, Pour AA (2016) Energy consumption and total factor productivity growth in Iranian agriculture. Energy Rep 2:218–220

Tugcu CT (2013) Disaggregate energy consumption and total factor productivity: a cointegration and causality analysis for the Turkish economy. Int J Energy Econ Policy 3(3):307–314

Boyd GA, Pang JX (2000) Estimating the linkage between energy efficiency and productivity. Energy Policy 28(5):289–296

Ladu MG, Meleddu M (2014) Is there any relationship between energy and TFP (total factor productivity)? A panel cointegration approach for Italian regions. Energy 75:560–567

FBP (2018) Fiscal balance program. Saudi Vision 2030. http://vision2030.gov.sa/en

Alshehry A, Belloumi M (2015) Energy consumption, carbon dioxide emissions and economic growth: the case of Saudi Arabia. Renew Sustain Energy Rev 41:237–247

Bayomi N, Fernandez J (2017) Trends of energy demand in the Middle East: a sectoral level analysis. Int J Energy Res 42(2):731–753

Gately D, Al-Yousef N, Al-Sheikh H (2012) The rapid growth of domestic oil consumption in Saudi Arabia and the opportunity cost of oil exports foregone. Energy Policy 47:57–68

Gazder U (2017) Energy consumption trends in energy scarce and rich countries: comparative study for Pakistan and Saudi Arabia. In: World renewable energy congress-17. https://doi.org/10.1051/e3sconf/20172307002

Mehrara M, Oskoui K (2007) The sources of macroeconomic fluctuations in oil exporting countries: a comparative study. Econ Model 24(3):365–379

Ozturk I (2010) A literature survey on energy-growth nexus. Energy Policy 38(1):340–349

Smyth R, Narayan PK (2015) Applied econometrics and implications for energy economics research. Energy Econ 50:351–358

Hasanov F, Bulut C, Suleymanov E (2017) Review of energy-growth nexus: a panel analysis for ten Eurasian oil exporting countries. Renew Sustain Energy Rev 73:369–386

Tugcu CT, Tiwari AK (2016) Does renewable and/or non-renewable energy consumption matter for total factor productivity (TFP) growth? Evidence from the BRICS. Renew Sustain Energy Rev 65:610–616

Al-Iriani MA (2006) Energy-GDP relationship revisited: an example from GCC countries using panel causality. Energy Policy 34:3342–3350

Costantini V, Martini C (2010) The causality between energy consumption and economic growth: a multi-sectoral analysis using non-stationary cointegrated panel data. Energy Econ 32:591–603

Jorgenson DW (1984) The role of energy in productivity growth. Am Econ Rev 74(2):26–30

Kelly HC, Blair PD, Gibbons JH (1989) Energy use and productivity: current trends and policy implications. Annu Rev Energy 14:321–352

Adenikinju AF (1998) Productivity growth and energy consumption in the Nigerian manufacturing sector: a panel data analysis. Energy Policy 6:199–205

Sahu SK, Narayanan K (2011) Total factor productivity and energy intensity in Indian manufacturing: a cross-sectional study. Int J Energy Econ Policy 1(2):47

Worrell E, Laitner JA, Ruth, M, Finman H (2003) Productivity benefits of industrial energy efficiency measures. Energy 28(11):1081–1098

Haider S, Ganaie AA (2017). Does energy efficiency enhance total factor productivity in case of India. OPEC Energy Rev 41(2):153–163

Diewert WE (1988) The early history of price index research. NBER working paper series, no. 2713. https://doi.org/10.3386/w2713

Diewert WE (1992) The measurement of productivity. Bull Econ Res 44(3):163–198

Kendrick JW (1958) Measurement of real product. In: A critique of the United States income and product accounts. Conference on research in income and wealth. Princeton University Press, Princeton, pp 405–426

Divisia F (1926) L’ indice monetaire et la theorie de la monnaie. Societe anonyme du Recueil Sirey, Paris

Solow R (1956) A contribution to the theory of economic growth. Quart J Econ 70:65–94

Solow RM (1957) Technical change and the aggregate production function. Rev Econ Stat 39:312–320

Swan TW (1956) Economic growth and capital accumulation. Econ Rec 32:334–361

Cobb CW, Douglas PH (1928) A theory of production (PDF). Am Econ Rev 18:139–165

Douglas PH (1976) The Cobb-Douglas production function once again: its history, its testing, and some new empirical values. J Polit Econ 84:903–916

Nordhaus WD (1975) The demand for energy: an international perspective, Cowles foundation discussion paper no 405. http://cowles.yale.edu/sites/default/files/files/pub/d04/d0405.pdf. Accessed 20 Sept 2018

Beenstock M, Willcocks P (1981) Energy consumption and economic activity in industrialized countries: the dynamic aggregate time series relationship. Energy Econ 3(4):225–232

Beenstock M, Dalziel A (1986) The demand for energy in the UK. Energy Econ 8(2):90–98

Hasanov FJ (2018) Re-consideration of theoretical framework for industrial energy consumption. Empirical results from an energy sector augmented macroeconometric model for Saudi Arabia. In: Forthcoming in the proceedings of the 2nd international conference on energy, finance and the macroeconomy, Montpellier, France, 24–26 Oct 2018

Liddle B (2011) Consumption-driven environmental impact and age structure change in OECD countries: a cointegration-STIRPAT analysis. Demogr Res 30:749–770

Liddle B (2014) Impact of population, age structure, and urbanization on carbon emissions/energy consumption: evidence from macro-level, cross-country analyses. Popul Environ 35:286–304

Liddle B, Lung S (2010) Age structure, urbanization, and climate change in developed countries: revisiting STIRPAT for disaggregated population and consumption-related environmental impacts. Popul Environ 31:317–343

O’Neill BC, Chen BS (2002) Demographic determinants of household energy use in the United States. Popul Dev Rev 28(2002):53–88

York R (2007) Demographic trends and energy consumption in European Union Nations. 1960–2025. Soc Sci Res 36:855–872

Mikayilov JI, Hasanov FJ (2018) Total factor productivity and energy consumption. Theoretical reconsideration. Preprint with Sage Advance

Dickey D, Fuller W (1981) Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 49:1057–1072

Phillips PB, Perron P (1988) Testing for unit roots in time series regression. Biometrika 75:335–346

Perron P (1989) The great crash, the oil price shock and the unit root hypothesis. Econometrica 57:1361–1401

Perron P, Vogelsang TJ (1992) Nonstationarity and level shifts with an application to purchasing power parity. J Bus Econ Stat 10:301–320

Perron P, Vogelsang TJ (1992) Testing for a unit root in a time series with a changing mean: corrections and extensions. J Bus Econ Stat 10:467–470

Vogelsang TJ, Perron P (1998) Additional test for unit root allowing for a break in the trend function at an unknown time. Int Econ Rev 39:1073–1100

Pesaran HM, Shin Y (1999) An autoregressive distributed lag modeling approach to cointegration analysis. In: Strom S (ed) Econometrics and economic theory in the 20th century: The Ragnar Frisch centennial symposium. Cambridge University Press, Cambridge, UK

Pesaran MH, Shin Y, Smith RJ (2001) Bound testing approaches to the analysis of level relationships. J Appl Econ 16:289–326

Johansen S, Juselius K (1990) Maximum likelihood estimation and inference on cointegration with applications to the demand for money. Oxf Bull Econ Stat 52:169–210

Johansen S (1992) Testing weak exogeneity and the order of cointegration in UK money demand data. J Policy Model 14:313–334

Reinsel GC, Ahn SK (1992) Vector autoregressive models with unit roots and reduced rank structure: estimation, likelihood ratio test, and forecasting. J Time Ser Anal 13:353–375

Reimers HE (1992) Comparisons of tests for multivariate cointegration. Stat Pap 33:335–359

Enders W (2015) Applied econometrics time series. In: Wiley series in probability and statistics, 5th edn. University of Alabama, Tuscaloosa

Stock JH, Watson MW (1993) A simple estimator of cointegrating vectors in higher order integrated systems. Econ J Econ Soc 1:783–820

Dolado JJ, Jenkinson T, Sosvilla-Rivero S (1990) Cointegration and unit roots. J Econ Surv 4:249–273

GASTAT (2018) General authority for statistics of kingdom of Saudi Arabia. https://www.stats.gov.sa/en

IMF International Monetary Fund (2012) IMF country report no 12/27, selected issues, Saudi Arabia

Mousa W (2018) Macroeconomic determinants of Saudi total factor productivity. Appl Econ Finan 5(1):37–44

IEA International Energy Agency (2018) https://www.iea.org/

United Nations (2018) Department of Economic and Social Affairs. Population division. World population prospects, the 2015 revision. 2016. Available online: https://esa.un.org/unpd/wpp/Download/Standard/Population/. Accessed on 24 July 2018

Juselius K (2006) The cointegrated VAR model: methodology and applications. Oxford University Press, Oxford, UK

Hendry F, Juselius K (2001) Explaining cointegration analysis: part II. Energy J 22(1):75–120

PWT (2018) Penn world table 9.0. Federal reserve economic data

Aljebrin MA (2013) A production function explanation of Saudi economic growth 1984–2011. Int J Econ Finan 5(5)

IMF International Monetary Fund (2013) IMF country report no 13/230, selected issues, Saudi Arabia

Mitra P, Hosny A, Abajyan G, Fischer M (2015) Estimating potential growth in the Middle East and Central Asia. IMF working paper, WP/15/62

Alkhareif RM, Bernett WA, Nayef AA (2017) Estimating the output gap for Saudi Arabia. Int J Econ Finan 9(3):81–90

Algarani A (2018) The contribution of local and factor productivity in Saudi Arabia. J Econ Sustain Dev 9(6):138–144

Dubey K, Galeotti M, Howarth N, Lanza A (2016) Energy productivity as a new growth model for GCC countries. KAPSARC working paper, KS-1645-DP039A, Oct 2016

MacKinnon J (1996) Numerical distribution functions for unit root and cointegration tests. J Appl Econ 11:601–618

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37:1979–1990

MacKinnon JG, Alfred AH, Leo M (1999) Numerical distribution functions of likelihood ratio tests for cointegration. J Appl Econ 14:563–577

Acknowledgements

The views expressed in this study are those of the authors and do not necessarily represent the views of their affiliated institutions. We would like to thank Axel Pierru for his valuable comments and suggestions and Chay Allen for his edits. We are responsible for all error and omissions.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2019 The Author(s)

About this chapter

Cite this chapter

Hasanov, F.J., Liddle, B., Mikayilov, J.I., Bollino, C.A. (2019). How Total Factor Productivity Drives Long-Run Energy Consumption in Saudi Arabia. In: Shahbaz, M., Balsalobre, D. (eds) Energy and Environmental Strategies in the Era of Globalization. Green Energy and Technology. Springer, Cham. https://doi.org/10.1007/978-3-030-06001-5_8

Download citation

DOI: https://doi.org/10.1007/978-3-030-06001-5_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-06000-8

Online ISBN: 978-3-030-06001-5

eBook Packages: EnergyEnergy (R0)