Abstract

The aim of this chapter is to make the scenario calculations fully transparent and comprehensible to the scientific community. It provides the scenario narratives for the reference case (5.0 °C) as well as for the 2.0 °C and 1.5 °C on a global and regional basis. Cost projections for all fossil fuels and renewable energy technologies until 2050 are provided. Explanations are given for all relevant base year data for the modelling and the main input parameters such as GDP, population, renewable energy potentials and technology parameters.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Scenario studies cannot predict the future, but they can describe what is needed for a successful pathway in terms of technology implementation and investments. Scenarios also help us to explore the possible effects of transition processes, such as supply costs and emissions. The energy demand and supply scenarios in this study are based on information about current energy structures and today’s knowledge of energy resources and the costs involved in deploying them. As far as possible, we also take into account potential constraints and preferences in each world region. However, this remains difficult due to large sub-regional variations. Our energy modelling primarily aims to achieve a transparent and consistent scenario, an ambitious but still plausible storyline from several possible techno-economic pathways. Knowledge integration is the core of this approach because we must consider different technical, economic, environmental, and societal factors. The scenario modelling follows a hybrid bottom-up/top-down approach, with no cost optimising objective functions. The analysis considers the key technologies required for a successful energy transition, and focuses on the roles and potential of renewable energies. Wind and solar energies have the highest economic potential and dominate the pathways on the supply side. However, variable renewable power from wind and photovoltaics (PV) remains limited by the need for sufficient secured capacity in energy systems. Therefore, we also consider concentrated solar power (CSP) with high-temperature heat storage as a solar option that promises large-scale dispatchable and secured power generation.

5.1 Scenario Definition

Scenario modelling was performed for three main scenarios that can be related to different overall carbon budgets between 2015 and 2050 and derived mean global temperature increases. The (around) 5.0 °C Scenario was calculated based on the Current Policies scenario published by the International Energy Agency (IEA) in World Energy Outlook 2017 (IEA 2017), and the emission budget for this scenario simply uses and extrapolates from the corresponding narratives. The 2.0 °C and 1.5 °C Scenarios were calculated in a normative way to achieve defined emission budgets.

5.1.1 The 5.0 °C Scenario (Reference Scenario)

The reference case only takes into account existing international energy and environmental policies. Its assumptions include, for example, continuing progress in electricity and gas market reforms, the liberalization of cross-border energy trade, and recent policies designed to combat environmental pollution. The scenario does not include additional policies to reduce greenhouse gas (GHG) emissions. Because the IEA’s projections only extend to 2040, we have extrapolated their key macroeconomic and energy indicators forward to 2050. This provides a baseline for comparison with the 2.0 °C and 1.5 °C Scenarios.

5.1.2 The 2.0 °C Scenario

The first alternative scenario aims to achieve an ambitious emissions reduction to zero by 2050 and a global energy-related CO2 emissions budget between 2015 and 2050 of around 590 Gt. The scenario is close to the assumptions and results of the Advanced E[R] scenario published in 2015 by Greenpeace (Teske et al. 2015). However, the scenario includes an updated base year, more coherent regional developments of energy intensities, and reconsidered trajectories and shares of renewable energy resource (RES) deployment. The 2.0 °C Scenario represents a far more likely pathway than the 1.5 °C Scenario, because the 2.0 °C case takes into account unavoidable delays due to political, economic, and societal processes and stakeholders.

5.1.3 The 1.5 °C Scenario

The second alternative scenario aims to achieve a global energy-related CO2 emission budget of around 450 Gt, accumulated between 2015 and 2050. The 1.5 °C Scenario requires immediate action to realize all available options. It is a technical pathway, not a political prognosis. It refers to technically possible measures and options without taking into account societal risks or barriers. Efficiency and renewable potentials must be deployed even more quickly than in the 2.0 °C Scenario. Furthermore, avoiding inefficient technologies and behaviours are essential strategies for developing regions in this time period.

5.2 Scenario World Regions and Clusters

The regional implementation of the long-term energy scenarios is defined according to the breakdown of the ten world regions of the IEA WEO 2016 (IEA 2016a, b). This approach has been chosen because the IEA also provides the most comprehensive global energy statistics and, in contrast to the regional breakdown of the IEA WEO 2017, it is also consistent with the Energy [R]evolution study series. Table 5.1 provides a country breakdown of the ten world regions considered in the scenarios.

Regional conditions play an important role in the layout of the scenario pathways. Therefore, scenario building tries to take into account important factors, such as current demand and supply structures, RES potentials, urbanization rates, and as far as possible, societal and behavioural factors. The following sections provide some regional information. Statistical data for the energy systems in the regions can be found in Sect. 5.3.

5.2.1 OECD North America

The energy system in OECD North America (USA, Canada, and Mexico) is dominated by developments in the USA, where more than 80% of the region’s demand occurs. In the highly developed countries of the USA and Canada, reducing the demand for energy by increasing efficiency will play a crucial role in decarbonisation. However, the high energy intensity (i.e., the high demand per capita or per gross domestic product [GDP]) requires even more ambitious measures than in other regions to reduce the energy demand as quickly as possible. In Mexico, in contrast, increasing living standards and the increasing population will increase the difficulties associated with reducing the energy demand, despite ambitious increases in efficiency. Wind and solar power generation will be the backbone of the power supply in OECD North America. They will be supplemented by hydro power (mainly in Canada) and also concentrated solar power (CSP). The high potential for CSP in Mexico and the southern parts of the USA will allow the large-scale use of CSP plants for grid balancing and grid stabilization. This will reduce the need for power storage, demand-side management, and other balancing strategies. In the large metropolitan areas in North America, electromobility and hydrogen cars will enter the market earlier and at a faster rate than in many other world regions. Large biomass potentials (residues) mean that biofuels could play important roles as climate-neutral fuels to bridge the gap until new powertrain technologies dominate the vehicle market. In the heating sector, particularly for process heat, solid biomass and biogas will be required as alternative fuels until the (direct or indirect) electrification of the heat sector is accomplished.

5.2.2 Latin America

Latin America’s energy system is dominated by Brazil, which accounts for around half the region’s energy demand. In the reference (5.0 °C) scenario, this region has a particularly high demand for electrification and a strong increase in CO2 emissions per capita. Latin America has the highest urbanization rate of all non-OECD regions. This provides opportunities for efficiency measures and the large-scale electrification of the heat and transport sectors based on renewable resources. Latin America has a high overall potential for the use of renewable energies (Herreras Martínez et al. 2015) and the largest biomass potential of all regions. It already meets more than 60% of its power demand from renewable sources, and higher shares are the focus of research (Nascimento et al. 2017; Barbosa et al. 2017; Gils et al. 2017). However, in many studies, heat and transport demands are not integrated into the assessments, even though the region has a large potential for renewable heat and decarbonised transport. Given the abundance of biomass, there is potential for generating more than 12 EJ from residues (Seidenberger et al. 2008). Biomass will also play a significant role in the industry sector. Because the region has a long experience of biofuels, they will play a major role in the 2.0 °C and 1.5 °C Scenarios, especially in Brazil, where bioethanol for transport is already competitive (Lora and Andrade 2009; La Rovere et al. 2011; Nass et al. 2007). However, the high urbanization rate in Latin America means there is also an opportunity to develop electromobility early. In the power sector, the use of biomass from residues will help to balance the increasing share of variable renewable energy from the excellent solar and wind resources. Grid extensions will contribute to inter-regional stability (Nascimento et al. 2017).

5.2.3 OECD Europe

The OECD Europe region includes countries with quite different energy supply systems, different potentials for renewable energy sources, and different power and heat demand patterns. High solar potentials and low heat demand for buildings are characteristic of the south. The northern and western parts of Europe have high wind potentials, especially offshore wind. In northern and central Europe, there are high potentials for hydropower and a high energy demand for space heating (such as in Eastern Europe). Biomass potentials exist predominantly in the north and east, but are only limited in the southern regions. The industrial demands for electricity and process heat are quite different in highly industrialized countries, such as the Scandinavian countries, Germany, and France compared with some eastern and southern countries. Most European countries, particularly European Union (EU) member countries, already have policies and market mechanisms for the implementation of renewable energy. The European Network of Transmission System Operators (ENTSO-E) can be used as a well-established basis for the further development of an interconnected European grid, which would be able to implement the large-scale and long-range transmission of renewable power to demand centres. This may also lead to important interconnections to the Middle East/North Africa (MENA) region and Eastern Europe/Eurasia. The possible large-scale importation of solar thermal electricity from MENA countries via high-voltage direct-current lines has been described in many studies and still represents a promising option in the long term, despite the currently difficult political conditions.

5.2.4 Eastern Europe/Eurasia

The Eastern Europe/Eurasia region includes some eastern EU member countries that are not part of the OECD, some other countries of the former Yugoslav Republic, and several countries of the former Soviet Union. However, the region is dominated by the economy and energy system of Russia. The main energy carrier today is natural gas, followed by oil. The region has large energy resources in biomass and wind power, but also geothermal energy and PV. Eastern Europe/Eurasia is the only world region that may face a significant population decline with expected demographic developments, particularly in Russia. Today, the region has by far the highest final and primary energy demand per $GDP. This indicates the existence of energy-intensive industries, but also large efficiency potentials in all sectors. The high heat demand, large rural areas, enormous oil and natural gas potentials, and the uneven distribution of economic wealth are some of the major challenges in this region. So far, only low expansion rates for renewable energies have been achieved in the region.

5.2.5 The Middle East

The Middle East consists of a series of oil-dependent countries, all of which have tremendous solar potential. The transport demand in the Middle East is very high, as is the electrification rate in urban areas, where currently almost 70% of the fast-growing population lives. Therefore, the electrification of transport systems is a major target in our scenarios. For many Middle East countries, water scarcity is a problem, and there are opportunities to combine large CSP plants with water desalination, to reduce the pressure on water supply systems. Biomass is very scarce, so its use must be limited to high-temperature process heat, especially in industry, where other renewable sources cannot be used. This will lead to a high demand for hydrogen or synthetic fuels. Naturally, this also limits the potential for combined heat and power generation (CHP), which is primarily seen as a transition technology to provide the most efficient use of the remaining fossil fuels and low-value biomass wastes. However, because the Middle East has extraordinary solar and wind potentials (Nematollahi et al. 2016; Hess 2018), the solar market is taking off. Projects with a capacity of 11 GW are planned for 2018 (MESIA 2018). With the extraordinarily high number of full-load hours, there is also the potential to use high-temperature solar heat. These resources also provide excellent conditions for hydrogen production, which are extensively exploited in the 2.0 °C and the 1.5 °C Scenarios. Therefore, the Middle East is a model solar and hydrogen region.

5.2.6 Africa

Africa is a very heterogeneous region, both economically and geographically. One of the few things African nations have in common is their very fast population growth. Africa includes the arid regions of North Africa, the undeveloped sub-Saharan region, and the emerging market of South Africa. North Africa features a high electrification rate and a strong dependence on oil. The water and biomass potentials for energy are very low, because water and biomass are prioritized for nutrition (or at least nutrition competes strongly with energy use). The region has outstanding solar irradiation, an excellent renewable energy source. Sub-Saharan Africa is characterized by low urbanization and a lack of access to electricity for two-thirds of its people (IEA 2014). Its energy supply is characterized by a high share of low-efficiency forms of generation, such as traditional biomass use. There is a general lack of energy services. Modernizing traditional biomass use could lead to significant reductions in energy demand, while maintaining or improving energy services (van der Zwaan et al. 2018). A broad variety of renewable energy sources, including biomass, hydro, geothermal, solar, and wind, have great potential. However, it will be a major challenge to find the investment required to tap these power sources under the present economic conditions (van der Zwaan et al. 2018). The picture is somewhat different in South Africa, which has a coal-based energy system and a comparatively stable and well-connected electricity grid, with access to electricity for more than 85% of its population (IEA 2014). The dependence on traditional biomass is extensive in the household and commerce sectors. Over 700 million people rely on fuel wood or charcoal for cooking on inefficient cooking stoves or open fires, with an efficiency of 10–20%. Modern biomass technologies provide multiple advantages. The introduction of more-efficient technologies, even those as simple as improved cooking stoves (with an average efficiency of 25%) or biogas stoves (with an average efficiency of 65%) (IEA 2014), will reduce the biomass input and thus the primary energy demand. This will also alleviate the heavy pressure on the ecosystem from the unsustainable exploitation of natural forests. The introduction of modern technologies will improve the supply of useful energy, lower indoor pollution, and improve living standards. Therefore, we assume in our scenarios that the overall biomass efficiency will improve from 35% in 2015 to 65% in 2050, while biomass’s share will decrease and be partially replaced by electric power and solar heat.

5.2.7 Non-OECD Asia

The Non-OECD Asia region includes all the developing countries of Asia, except China and India. This group covers a large spectrum in terms of size, economy, stability, and developmental status. The region is spread over a large area from the Arabian Sea to the Pacific. Electricity access varies widely in these countries, according to WEO 2014. In Southeast Asia, the average access is 77%, with only 30% access in Myanmar and Cambodia, and nearly 100% access in Singapore, Thailand, and Vietnam. In Indonesia, there is 76% access (92% in urban areas), in Bangladesh 60% (90%), and in Pakistan 69% (88%). In Southeast Asia, 46% of the population still relies on traditional biomass, with the highest use in Myanmar (93%) and Cambodia (89%). In Indonesia, 42% of the population used biomass for cooking in 2012; in Bangladesh the figure was 89%; and in Pakistan, it was 62%. The lowest values are in Singapore (0%), Malaysia (0%), and Thailand (24%). The scenarios thus cover the whole band-width of renewable resources and technological development, even though the outlooks for individual countries deviate widely from the average.

5.2.8 India

India has a fast-growing population of over 1.2 billion people and is the world’s seventh largest country by area. However, the population density is already 2.7 times higher than that in China. Due to its climate, India has a rather limited CSP potential but a large potential for PV power generation. Its wind power potential is expected to be limited by land-use constraints, but the technical potential estimated from available meteorological data is large. According to the WEO 2014 database, electricity access is on average 75%, with 94% in urban areas and 67% in rural areas. In India, about 815 million people still relied on the traditional use of biomass for cooking in 2012. Due to population and GDP growth, increasing living standards, and increasing mobility, it is expected that the energy demand in India will increase significantly, although large potentials for efficiency savings exist. Electrification is a core strategy for decarbonisation in India, which, combined with the rising demand for energy services, will lead to strong growth in the per capita and overall electricity demand. It is also expected that the need for mobility in India will increase rapidly and more strongly than in other regions of the world.

5.2.9 China

China has great potential renewable energy resources, especially for the generation of solar thermal power in the west, onshore wind in the north, and offshore wind in the east and southeast. Photovoltaic power generation could play an important role throughout all parts of China. The expansion of hydropower generation is currently also seen as a major strategy, but the potential for small hydro systems is rather low. China will face further large increases in energy demand in all sectors of the energy system. Chinese economic prosperity has mainly been underpinned by coal, which provides over two-thirds of China’s primary energy supply today (IEA WEO 2014). The increase in electricity use due to higher electrification rates will be a major factor in the successful expansion of renewable energy in the industry, building, and transport sectors. In China, nearly all households are connected to the electricity grid. However, according to WEO 2014, about 450 million Chinese still relied on the traditional use of biomass for cooking in 2012. China has pledged to reduce CO2 emissions before 2030, and already has some ambitious political targets for renewable energy deployment.

5.2.10 OECD Pacific

OECD Pacific consists of Japan, New Zealand, the peninsula of South Korea, and the continent of Australia. The region is dominated by the high energy demand in Japan, which has rather limited renewable energy resources. The lack of physical grid connections prevents power transmission between these countries. Therefore, it is a huge effort to supply the large Japanese nation with renewable energy and to stabilize the variable wind power without tapping the large solar potential in other countries, such as Australia. Here, hydrogen and synfuels will not only be used for the long-term storage of renewable power, but also as an option for balancing the renewable energy supply across borders. The early market introduction of fuel-cell cars in Japan may support such a strategy. Following the accident at Fukushima and the implementation of feed-in tariffs for renewable electricity, the expansion rates for renewable energies, in particular PV, have risen sharply.

5.3 Key Assumptions for Scenarios

5.3.1 Population Growth

Population growth is an important driver of energy demand, directly and through its impact on economic growth and development. The assumptions made in this study up to 2050 are based on United Nations Development Programme (UNDP) projections for population growth (UNDP 2017 (medium variant)). Table 5.2 shows that according to the UNDP, the world’s population is expected to grow by 0.8% per year on average over the period 2015–2050. The global population will increase from 7.4 billion people in 2015 to nearly 9.8 billion by 2050. The rate of population growth will slow over this period, from 1.1% per year during 2015–2020 to 0.6% per year during 2040–2050. From a regional perspective, Africa’s population growth will continue to be the most rapid (on average 2.2%/year), followed by the Middle East (1.3%/year). In contrast, in China and OECD Pacific, a population decline of about 0.1%/year. is expected. The populations in OECD Europe and OECD North America are expected to increase slowly through to 2050. The proportion of the population living in today’s non-OECD countries will increase from its current 81% to 85% in 2050. China’s contribution to the world population will drop from 19% today to 15% in 2050. Africa will remain the region with the highest population growth, leading to a share of 26% of world population in 2050. Satisfying the energy needs of a growing population in the developing regions of the world in an environmentally friendly manner is the fundamental challenge in achieving a sustainable global energy supply.

5.3.2 GDP Development

Economic growth is a key driver of energy demand. Since 1971, each 1% increase in the global GDP has been accompanied by a 0.6% increase in primary energy consumption. Therefore, the decoupling of energy demand and GDP growth is a prerequisite for the rapid decarbonisation of the global energy industry. In this study, the economic growth in the model regions is measured in GDP, expressed in terms of purchasing power parity (PPP) exchange rates. Purchasing power parities compare the costs in different currencies of fixed baskets of traded and non-traded goods and services. GDP PPP is a widely used measure of living standards and is independent of currency exchange rates, which might not reflect a currency’s true value (purchasing power) within a country. Therefore, GDP PPP is an important basis of comparison when analysing the main drivers of energy demand or when comparing the energy intensities of countries.

Although PPP assessments are still relatively imprecise compared with statistics based on national incomes, trade, and national price indices, it is argued that they provide a better basis for global scenario development. Therefore, all the data on economic development in the IEA World Energy Outlook 2016 (WEO 2016a, b) refer to purchasing-power-adjusted GDP in international US$ (2015). However, because WEO 2016 only covers the time period up to 2040, projections for 2040–2050 in the 5.0 °C, 2.0 °C, and 1.5 °C Scenarios are based on German Aerospace Center (DLR) estimates, which are mainly used to extrapolate the GDP trends in the world regions used in our modelling.

GDP growth in all regions is expected to slow gradually over the coming decades (Table 5.3

). It is assumed that world GDP will grow on average by 3.2% per year over the period 2015–2050. China, India, and Africa are expected to grow faster than other regions, followed by the Middle East, Africa, other non-OECD Asia, and Latin America. The growth of the Chinese economy will slow as it becomes more mature, but it will nonetheless become the economically strongest region in the world in PPP terms by 2020. The GDP in OECD Europe and OECD Pacific is assumed to grow by 1.3–1.5% per year over the projection period, while economic growth in OECD North America is expected to be slightly higher (2.1%). The OECD’s share of global PPP-adjusted GDP will decrease from 45% in 2015 to 28% in 2050.

5.3.3 Technology Cost Projections

The parameterization of the models requires many assumptions about the development of the particular characteristics of technologies, such as specific investment and fuel costs. Therefore, because long-term projections are highly uncertain, we must define plausible and transparent assumptions based on background information and up-to-date statistical and technical information.

The speed of an energy system transition also depends on overcoming economic barriers. These largely relate to the relationships between the costs of renewable technologies and their fossil and nuclear counterparts. For our scenarios, the projection of these costs is vital in making valid comparisons of energy systems. However, there have been significant limitations to these projections in the past in relation to investment and fuel costs.

In addition, efficiency measures also generate costs which are usually difficult to determine depending on technical, structural and economic boundary conditions. In the context of this study, we have therefore assumed uniform average costs of 3 ct per avoided kWh of electricity consumption in our cost accounting.

During the last decade, fossil fuel prices have seen huge fluctuations. Figure 5.1 shows oil prices since 1997. After extremely high oil prices in 2012, we are currently in a low-price phase. Gas prices saw similar development (IEA 2017). Therefore, fossil fuel price projections have also seen considerable variations (IEA 2013, 2017) and have had a considerable influence on scenario results ever since.

Historic development and projections of oil prices (bottom lines) and historical world oil production and projections (top lines) by the IEA according to Wachtmeister et al. (2018)

Although in the past, oil-exporting countries provided the best oil price projections, institutional price projections have become increasingly accurate, with the International Energy Agency (IEA) leading the way in 2018 (Roland Berger 2018). An evaluation of the oil price projections of the IEA since 2000 by Wachtmeister et al. (2018) showed that price projections have varied significantly over time. Whereas the IEA’s oil production projections seem comparatively accurate, oil price projections showed errors of 40–60%, even when made for only 10 years ahead. Between 2007 and 2017, the IEA price projections for 2030 varied from $70 to $140 per barrel, providing significant uncertainty regarding future costs in the scenarios. Despite this limitation, the IEA provides a comprehensive set of price projections. Therefore, we based our scenario assumptions on these projections, as described below.

However, because most renewable energy technologies provide energy without fuel costs, the projections of investment costs become more important than fuel cost projections, and this limits the impact of errors in the fuel price projections. It is only for biomass that the cost of feedstock remains a crucial economic factor for renewables. Today, these costs range from negative costs for waste wood (based on credit for the waste disposal costs avoided), through inexpensive residual materials, to comparatively expensive energy crops. Because bioenergy holds significant market shares in all sectors in many regions, a detailed assessment of future price projections is provided below.

Investment cost projections also pose challenges for scenario development. Available short-term projections of investment costs depend largely on the data available for existing and planned projects. Learning curves are most commonly used to assess the future development of investment costs as a function of their future installations and markets (McDonald and Schrattenholzer 2001; Rubin et al. 2015). Therefore, the reliability of cost projections largely depends on the uncertainty of future markets and the availability of historical data.

Fossil technologies provide a large cost data set featuring well-established markets and large annual installations. They are also mature technologies, where many cost reduction potentials have already been exploited.

For renewable technologies, the picture is more mixed. For example, hydro power is, like fossil fuels, well established and provides reliable data on investment costs. Other technologies, such as PV and wind, are currently experiencing tremendous developments in installation and cost reduction. Solar PV and wind are the focus of cost monitoring, and considerable data are already available on existing projects. However, their future markets are not easily predicted, as can be seen from the evolution of IEA market projections over recent years in the World Energy Outlook series (compare for example IEA 2007, 2014, 2017). For PV and wind, small differences in cost assumptions will lead to large deviations in the overall costs, and cost assumptions must be made with special care. Furthermore, many technologies feature only comparably small markets, such as geothermal, modern bioenergy applications, and CSP, for which costs are still high and for which future markets are insecure. The cost reduction potential is correspondingly high for these technologies. This is also true for technologies that might become important in a transformed energy system but are not yet widely available. Hydrogen production, ocean power, and synthetic fuels might deliver important technology options in the long term after 2040, but their cost reduction potential cannot be assessed with any certainty today.

Thus, cost assumptions are a crucial factor in evaluating scenarios. Because costs are an external input into the model and are not internally calculated, we assume the same progressive cost developments for all scenarios. In the next sections, we present a detailed overview of our assumptions for power and renewable heat technologies, including the investment and fuel costs, and the potential CO2 costs in the scenarios.

5.3.3.1 Power and CHP Technologies

The focus of cost calculations in our scenario modelling is the power sector. We compared the specific investment costs estimated in previous studies (Teske et al. 2012, 2015), which were based on a variety of studies, including the European Commission-funded NEEDS project (NEEDS 2009), projections from the European Renewable Energy Council (Zervos et al. 2010), investment cost projections by the IEA (2014), and current cost assumptions by IRENA and IEA (IEA 2016b). We found that investment costs generally converged, except for PV. Therefore, for consistency reasons, the investment costs and operation and maintenance costs for the power sector are based primarily on the investment costs within WEO 2016 (IEA 2016b) up to 2040, including their regional disaggregation. We extended the projections until 2050 based on the trends in the preceding decade.

For renewable power production, we used investment costs from the 450 ppm scenario from IEA 2016b. For technologies not distinguished in the IEA report (such as geothermal CHP), we used cost assumptions based on our own research, from the Energy [R]evolution Scenario 2015 (Teske et al. 2015). As the cost assumptions for PV systems by the IEA do not reflect recent cost degressions, we based our assumptions on a more recent analysis by Steurer et al. (2018), which projects lower investment costs for PV in 2050 than does the IEA. The costs for onshore and offshore wind in Europe were adapted from the same source, in order to reflect more recent data. The cost assumptions for hydrogen production come from our own analysis in the PlanDelyKaD project (Michalski et al. 2017). Table 5.4 summarizes the cost trends for power technologies derived from the assumptions discussed above for OECD Europe. It is important to note that the cost reductions are, in reality, not a function of time, but of cumulative capacity (production of units), so dynamic market development is required to achieve a significant reduction in specific investment costs. Therefore, we might underestimate the costs of renewables in the reference (5.0 °C) scenario compared with the 2.0 °C and 1.5 °C Scenarios. However, our approach is conservative when we compare the reference scenario with the 2.0 °C or 1.5 °C Scenarios. The cost assumptions for the other nine regions are in the same range, but differ slightly for different renewable energy technologies. Fossil fuel power plants have a limited potential for cost reductions because they are at an advanced stage of technology and market development. Gas and oil plants are relatively cheap, at around $670/kW and $822/kW, respectively. CHP applications and coal plants are more expensive, ranging between $2000/kW and $2500/kW. The IEA sees some cost reduction potential for expensive nuclear plants, tending towards $4500/kW by 2050, whereas gas might even increase in cost.

In contrast, several renewable technologies have seen considerable cost reductions over the last decade. This is expected to continue if renewables are deployed extensively. Fuel cells are expected to outpace other CHP technologies, with a cost reduction potential of more than 75% (from currently high costs). Hydro power and biomass remain stable in terms of costs. Tremendous cost reductions are still expected for solar energy and offshore wind, even though they have experienced significant reductions already. Although CSP might deliver dispatchable power at half its current cost in 2050, variable PV costs could drop to 35% of today’s costs. Offshore wind could see cost reductions of over 30%, whereas the cost reduction potential for onshore wind seems to have been exploited already to a large extent (Table 5.4).

In the 2.0 °C and 1.5 °C Scenarios, hydrogen is introduced as a substitute for natural gas, with a significant share after 2030. Hydrogen is assumed to be produced by electrolysis. With electrolysers just emerging on larger scale on the markets, they have considerable cost reduction potential. Based on the Plan-DelyKaD studies (Michalski et al. 2017), we assume that costs could decrease to $570/kW in the long term.

5.3.3.2 Heating Technologies

Assessing the costs in the heating sector is even more ambitious than in the power sector. Costs for new installations differ significantly between regions and are interlinked with construction costs and industry processes, which are not addressed in this study. Moreover, no data are available to allow the comprehensive calculation of the costs for existing heating appliances in all regions. Therefore, we concentrate on the additional costs resulting from new renewable applications in the heating sector.

Our cost assumptions are based on a previous survey of renewable heating technologies in Europe, which focused on solar collectors, geothermal, heat pumps, and biomass applications. Biomass and simple heating systems in the residential sector are already mature. However, more-sophisticated technologies, which can provide higher shares of heat demand from renewable sources, are still under development and rather expensive. Market barriers will slow the further implementation and cost reduction of renewable heating systems, especially for heating networks. Nevertheless, significant learning rates can be expected if renewable heating is increasingly implemented, as projected the 2.0 °C and 1.5 °C Scenarios.

Table 5.5 presents the investment cost assumptions for heating technologies for OECD Europe, disaggregated by sector. Geothermal heating displays the same high costs in all sectors. In Europe, deep geothermal applications are being developed for heating purposes at investment costs ranging from €500/kWth (shallow) to €3000/kWth (deep), with the costs strongly dependent on the drilling depth. The cost reduction potential is assumed to be around 30% by 2050.

Heat pumps typically provide hot water or space heat for heating systems with relatively low supply temperatures, or they supplement other heating technologies. Therefore, they are currently mainly used for small-scale residential applications. Costs currently cover a large band-width and are expected to decrease by only 20% to $1450/kW by 2050.

For biomass and solar collectors, we assume significant differences between the sectors. There is a broad portfolio of modern technologies for heat production from biomass, ranging from small-scale single-room stoves to heating or CHP plants on an MW scale. Investment costs show similar variations: simple log-wood stoves can be obtained from $100/kW, but more sophisticated automated heating systems that cover the whole heat demand of a building are significantly more expensive. Log-wood or pellet boilers range from $500 to 1300/kW. Large biomass heating systems are assumed to reach their cheapest costs in 2050 at around $480/kW for industry. For all sectors, we assume a cost reduction of 20% by 2050. In contrast, solar collectors for households are comparatively simple and will become cheap at $680/kW by 2050. The costs of simple solar collectors for swimming pools might have been optimized already, whereas their integration in large systems is neither technologically nor economically mature. For larger applications, especially in heat grid systems, the collectors are large and more sophisticated. Because there is not yet a mass market for such grid-connected solar systems, we assume there will be a cost reduction potential until 2050.

5.3.4 Fuel Cost Projections

5.3.4.1 Fossil Fuels

Although fossil fuel price projections have seen considerable variations, as described above, we based our fuel price assumptions up to 2040 on the WEO 2017 (IEA 2017). Beyond 2040, we extrapolated from the price developments between 2035 and 2040. Even though these price projections are highly speculative, they provide a set of prices consistent to our investment assumptions. Fuel prices for nuclear energy are based on the values in the Energy [R]evolution report 2015 (Teske et al. 2015), corrected by the cumulative inflation rate for the Eurozone of 1.82% between 2012 and 2015 (Table 5.6).

5.3.4.2 Biomass Prices

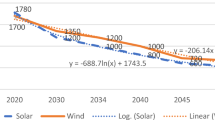

Biomass prices depend on the quality of the biomass (residues or energy crops) and the regional supply and demand. The variability is large. Lamers et al. (2015) found a price range of €4–4.8/GJ for forest residues in Europe in 2020, whereas agricultural products might cost €8.5–12/GJ. Lamers et al. modelled a range for wood pellets from €6/GJ in Malaysia to 8.8€/GJ in Brazil. IRENA modelled a cost supply curve on a global level for 2030 (see Fig. 5.2), ranging from $3/GJ for a potential of 35 EJ/year. up to $8–10/GJ for a potential up to 90–100 EJ/year (IRENA 2014) (and up to $17/GJ for an potential extending to 147 EJ).

Global supply curve for primary biomass in 2030 (IRENA 2014)

IRENA projected regional supply costs for liquid and other biomass sources in 2030 based on a global biomass use of around 108 EJ, using current primary biomass prices as a proxy (see Table 5.7). Liquid biofuels demand higher prices because of their production and transformation processes; ‘other biomass’ includes primary biomass, such as fuel wood, energy crops, and residues.

The prices cited above hold true for modern biomass applications. Traditional biomass use is still often based on firewood or other biomass, which is acquired without a price (and with the labour cost not considered). No price data are yet available for a considerable range of residues. Therefore, the average primary biomass costs across the complete energy system in many regions are lower than the available market prices for biomass commodities. Consequently, today’s market prices represent the upper limit of today’s biomass costs.

Therefore, for our scenarios, we assumed a lower average biomass price in all regions, starting from the lower end of the cost supply curve at around $7.50/GJ for OECD regions, with predominantly modern applications. For Africa, Latin America, and Asia, including Russia, which have abundant biomass residue potential, current prices were assumed to be $3/GJ. For the remaining regions (the Middle East, and Eastern Europe), we assumed $5/GJ.

The prices for primary biomass will increase proportionately to the IRENA reference price for ‘other biomass’ by 2030, following the increasing uptake of modern biomass technologies and increasing trade, representing a further biomass potential uptake along the supply curve. For the period until 2050, we consider that biomass prices will be stable. The prices calculated by IRENA are valid for a demand of 108 EJ/year. The biomass demand considered in this study never exceeds a total of 100 EJ/year. However, the international trade in biomass may heavily influence biomass prices in the future, representing a significant source of uncertainty in our assumptions.

5.3.5 CO2 Costs

The WEO 2017 (IEA 2017) considers the future price of CO2 in the power and industry sectors. There is considerable variation between the current policy scenario, the new policy scenario, and the 450 ppm scenario, not only in value, but also in regional range. Various studies have indicated a close relationship between decarbonisation and the implicit or explicit CO2 price (regardless of the most efficient implementation measure). On the one hand, the carbon price is a precondition for a decarbonisation of the energy sector (Lucena et al. 2016), but on the other hand, decarbonisation may limit the costs of CO2 emissions if an efficient pricing measure is in place (Jacobson et al. 2017). Because the scenarios in this study rely heavily on effective reductions in CO2 emissions, we used the CO2 prices of the 450 ppm scenario in the 2.0 °C and 1.5 °C Scenarios. In the reference case, we deviated from the WEO 2017, which applies rather low CO2 emission costs. Instead, we applied CO2 costs equivalent to the cost of the resulting climate damage. Based on existing studies of fossil-energy-induced damage (Anthoff and Tol 2013; Stern et al. 2006), we assumed that $78/t of CO2 is a plausible cost estimate in the wide range of estimates of the social costs of CO2 emissions (Table 5.8).

5.4 Energy Scenario Narratives and Assumptions for World Regions

The scenario-building process involves many assumptions and explicit, but also implicit, narratives about how future economies and societies, and ultimately energy systems, may develop under the overall objective of ‘deep and rapid decarbonisation’ by 2050. These narratives depend on three main strategic pillars:

-

Efficiency improvement and demand reduction: stringent implementation of technical and structural efficiency improvements in energy demand and supply. These will lead to a continuous reduction in both final and primary energy consumption. In the 1.5 °C Scenario, these measures must be supplemented with responsible energy consumption behaviour by the consumer.

-

Deployment of renewable energies: massive implementation of new technologies for the generation of power and heat in all sectors. These will include variable renewable energies from solar and wind, which have experienced considerable cost reductions in recent years, but also more expensive technologies, such as large-scale geothermal and ocean energy, small hydro power, and CSP.

-

Sector coupling: stringent direct electrification of heating and transport technologies in order to integrate renewable energy in the most efficient way. Because this strategy has its limitations, it will be complemented by the massive use of hydrogen (generated by electrolysis) or other synthetic energy carriers.

Some alternative or probably complementary future technical options are explicitly excluded from the scenarios. In particular, those options with large uncertainties with respect to technical, economic, societal, and environmental risks, such as large hydro and nuclear power plants, unsustainable biomass use, carbon capture and storage (CCS), and geoengineering, are not considered on the supply side as mitigation measures or—in the case of hydro—not expanded in the future. The sustainable use of biomass will partly substitute for fossil fuels in all energy sectors. However, this use will be limited to an annual global energy potential of less than 100 EJ per year for sustainability reasons, according to the calculations of Seidenberger et al. (2008), Thrän et al. (2011), and Schueler et al. (2013).

The transformations described in the two alternative scenarios are constrained, to a certain degree, by current short- to medium-term investment planning, as described in the reference case, because most technical and structural options to change the demand or supply side require years of planning and construction. This means that both alternative scenarios start deviating significantly from the reference case only after 2025. However, some short-term developments shown in the IEA WEO Current Policies scenario have been corrected and are not adopted in the alternative scenarios because there is newer statistical information (that renders the reference development implausible). This is the case for the IEA estimates of demand development in some regions and sectors, and it is partly true for investments in fossil-fuel-based heat and power generation.

5.4.1 Efficiency and Energy Intensities

It is obvious that a major increase in energy efficiency is the backbone of each ambitious transition scenario, because energy efficiency significantly reduces the need for energy conversion and infrastructure investment. The development of the future global energy demand is determined by three key factors:

-

Population growth, which affects the number of people consuming energy or using energy services. Associated with this, increasing access to energy services in developing countries and emerging economies is an additional influencing factor, bearing in mind that this could mean power grid access or the implementation of isolated, usually small-scale, local power systems.

-

Economic development, which is commonly measured as GDP. In general, GDP growth triggers an increase in energy demand, directly via additional industrial activities and indirectly via an increase in private consumption arising from the higher incomes associated with a prospering economy.

-

Energy intensity, which is a measure of how much final energy is required in the industrial sector to produce a unit of GDP. Efficiency measures help to reduce energy intensity and can result in a decoupling of economic growth and final energy consumption. In the ‘Residential and other’ sector, energy intensity refers to the per capita demand for final energy (for electrical appliances and heat generation). Efficiency improvement is also a result of reduced conversion losses, in particular those achieved by replacing thermal power generation with renewable technologies, which leads to a further reduction in the primary energy intensity.

The reference scenario and both target scenarios are based on the same projections of population and economic growth. Therefore, the scenarios represent the specific, although widely accepted, development of future societies. However, the future development of energy intensities differs between the reference and alternative scenarios, taking into account the different efficiency pathways and therefore the successful implementation of measures to intensify required investments in efficient technologies or to change consumer behaviour.

The assumptions made about the potential to further increase the economic and technical efficiency in all sectors are based on various external studies. However, the lower benchmarks for the assumptions on efficiency potentials are derived from the Current Policies scenario of the IEA WEO 2017 (IEA 2017). The upper benchmarks for efficiency potentials per world region are taken from Graus et al. (2011), Kermeli et al. (2014), and recently published low-energy-demand scenarios developed by Grubler et al. (2018).

5.4.1.1 Industrial Electricity Demand

‘Industrial electricity demand’ refers to many appliances of different sizes and purposes. Large potentials for saving electricity have been identified in various studies in most branches of industry. This particularly applies to electric drives for compressed air, pumps, and fans. The scenario model approach distinguishes between electric appliances and power-to-heat devices for space and process heating. The consumption of electricity per GDP varies widely between regions, depending on their industrial structures and efficiency standards. The trajectories for industrial electricity demands are constrained by the abovementioned lower and upper benchmarks and aim for similar electricity uses per $GDP in the industrial sectors in all regions by 2050. The resulting trajectories for OECD and non-OECD countries are shown in Table 5.9. The average global electricity demand for electric appliances in ‘industry’ (without power-to-heat) will decrease from 55 kWh/$1000 GDP in 2015 to 36 kWh/$1000 in 2050 in the reference case, but to 24 kWh/$1000 in the 2.0 °C Scenario and 23 kWh/$1000 in the 1.5 °C Scenario. However, the increased electrification of industrial heat in both alternative scenarios almost cancels out the greater efficiency increases in those two scenarios when compared with the reference case. The average power-to-heat share in industry will increase in this period from 6% to 34% in 2050 in the 2.0 °C Scenario and to 37% in the 1.5 °C Scenario. In the 1.5 °C Scenario, the annual electricity demand for industrial electrical appliances will be around 5% lower than in the 2.0 °C Scenario between 2020 and 2025, and up to 10% lower between 2025 and 2035. However, between 2035 and 2050, the electricity demand for electric appliances in the industry sector converges under the two scenarios.

5.4.1.2 Demand for Fuel to Produce Heat in the Industry Sector

Industrial heat is required for different purposes and at different temperatures. Currently, industrial (process) heat is mainly produced by burning fossil fuels. Biomass plays a minor role, except in heat use from the combustion of residues and biogenic waste. Some low- and medium-temperature heat is produced by co-generation plants with combined heat and power provisions. Power-to-heat makes up only a small percentage of the industrial energy demand for heat. Regional differences in the nature of industry, especially in terms of the presence of energy-intensive heavy or manufacturing industries, strongly influence the amounts of low-, medium-, and high-temperature heat that must be produced today and in the future (because we assume that the regional industry structure will remain the same). Various technological improvements, process substitutions, and innovations are technically possible and have been implemented to some extent already. An important example is highly efficient waste heat recovery. Shorter investment cycles and incentives to replace old technologies will help to reduce energy consumption as quickly as possible. It is obvious that incentives are essential to trigger rapid innovation and the implementation of new technologies. Any political strategy for introducing such a pathway requires strong support from various industry stakeholders and regional or even global governance to overcome the economic and technical obstacles and conflicting interests. Therefore, both alternative scenarios assume that the conditions exist to allow rapid technological change. Table 5.10 provides the resulting final energy demands for heating per $GDP for OECD and non-OECD countries. The average global values will decrease from 680 MJ/$1000 GDP in 2015 to 366 MJ/$1000 in 2050 in the reference case, and to 185 MJ/$1000 in the 2.0 °C Scenario and 172 MJ/$1000 in the 1.5 °C Scenario. Compared with the 2.0 °C Scenario, the 1.5 °C Scenario assumes a significantly more rapid reduction in the industrial heat demand. Between 2020 and 2025, the annual energy demand for heat will be up to 8% lower under the 1.5 °C Scenario than under the 2.0 °C Scenario, and up to 17% lower between 2025 and 2035. After 2035, the difference will decrease again, and by 2050, it will be around 7%.

5.4.1.3 Electricity Demand in the ‘Residential and Other’ Sector

The electricity demand in the ‘Residential and other’ sector includes electricity use in households, for commercial purposes, and in the service and trade sectors, fishery, and agriculture. Besides lighting, information, and communication, a large amount of electricity is used for cooking, cooling, and hot water. It has been estimated that in 2015, electricity use for heating had a global average share of 5% of the final energy use for heating. It is assumed that this share will increase significantly to 30% in 2050 in the 2.0 °C Scenario and to 37% in the 1.5 °C Scenario. These increases are attributed to sector coupling, the provision of storage for variable renewable energy in the heat sector, and the provision of high-temperature heat without fuel combustion. The average global electricity use for appliances in the ‘Residential and other’ sector will decrease in the reference case from 78 kWh/$1000 GDP in 2015 to 60 kWh/$1000 in 2050, whereas it will decrease to 38 kWh/$1000 in the 2.0 °C Scenario and to 37 kWh/$1000 in the 1.5 °C Scenario, a reduction of more than 50% relative to today’s energy consumption. The average global electricity use for appliances in the ‘Residential and other’ sector, which is related to per capita consumption, will increase in the reference scenario from 1350 kWh/capita in 2015 to 2370 kWh/capita in 2050, whereas it will increase to only 1490 kWh/capita in the 2.0 °C Scenario and to 1460 kWh/capita in the 1.5 °C Scenario. Table 5.11 shows the changes in electricity use for appliances in OECD and non-OECD countries (without electricity for heating). Significant reduction potentials are assumed for all world regions. Similar to the development in the industry sector, between 2020 and 2025, the annual power demand for electrical appliances in the ‘Residential and other’ sector will be around 5% lower in the 1.5 °C Scenario than in the 2.0 °C Scenario, and more than 10% lower between 2025 and 2035. After 2035, the two scenarios will converge again, so that in 2050, the global demand will be only 2% higher in the 2.0 °C Scenario than in the 1.5 °C Scenario.

5.4.1.4 Fuel Demand for Heat in the ‘Residential and Other’ Sector

The fuel demand for heat in households has quite different characteristics depending on the consumption structures in each world region and their climatic conditions. In regions with harsh winters, the heat demand is dominated by the building sector (space heat and hot water in private and commercial buildings), but in regions with a comparatively warm climate, the demand for space heat is generally low and heat is predominantly used for cooking and as low-temperature heat for hot water. In the commercial sector, the energy mix for heat is more diverse. The medium- to high-temperature process heat demand arises in this sector. Reducing the final energy use for heating will involve reducing the demand (e.g., by improving the thermal insulation of building envelopes) and replacing inefficient procedures and technologies, such as the traditional use of biomass, which is still widely used for cooking and heating in some regions. In contrast to traditional biomass, the efficiency of electrical appliances can improve significantly, and they produce zero direct emissions and no air pollution. Table 5.12 shows the assumed average final energy demand for heating in OECD and non-OECD countries. The average global consumption will decrease from 560 MJ/$1000 GDP in 2015 to 280 MJ/$1000 in 2050 in the reference scenario, but to 173 MJ/$1000 in the 2.0 °C Scenario and to 160 MJ/$1000 in the 1.5 °C Scenario. The average global per capita energy demand for fuels in ‘Residential and other sectors’ will decrease from around 12,600 MJ/capita per year in 2015 to 11,700 MJ/capita in the reference case. This will mainly be due to a shift in the global population shares towards the developing regions. Compared with the reference scenario, the energy intensity will decrease to 7300 MJ/capita in the 2.0 °C Scenario and to 6700 MJ/capita in the 1.5 °C Scenario. The 1.5 °C Scenario assumes a significantly stronger reduction in demand than the 2.0 °C Scenario. In the 1.5 °C Scenario, additional efficiency measures will reduce the final energy demand until 2025 by around 5%, and by up to 13% between 2025 and 2035 (compared with the 2.0 °C Scenario). Thereafter, the differences will become smaller, finally reaching around 8% by 2050.

5.4.1.5 Resulting Energy Intensities by Region

Figure 5.3 shows the final energy intensities related to $GDP for each of the ten world regions between 2015 and 2050 and for both alternative scenarios. The final energy use per GDP will decrease significantly in all regions, but the decreases will be larger (and faster) in OECD countries. This will result in smaller regional differences in the final energy demand compared with the current situation. Compared with the very ambitious assumptions of Grubler et al. (2018) for the specific final energy demands in northern and southern world regions, the assumptions made in this study are conservative. In Grubler et al. (2018), the annual global final energy use, including non-energy consumption, will decrease from 363 EJ in 2015 to 245 EJ by 2050, whereas in our study, the annual global value will decrease to 310 EJ in the 2.0 °C Scenario and to 284 EJ in the 1.5 °C Scenario compared with 586 EJ in the reference case (see Chap. 8). Because the 1.5 °C target requires a significant reduction in emissions before 2030, the 1.5 °C Scenario necessarily reduces the energy demand more rapidly than the 2.0 °C Scenario, but only a slightly lower annual consumption is assumed in 2050.

Development of the specific final energy use (per $GDP) in all stationary sectors (i.e., without transport) per world region under the 2.0 °C Scenario (left) and 1.5 °C Scenario (right)

5.4.2 RES Deployment for Electricity Generation

The power demand will increase significantly in all scenarios. In the 2.0 °C and 1.5 °C Scenarios, this will result from the continuous electrification of the heating and transport sectors, and the increasing production of synthetic fuels for indirect electrification and sector coupling. The available energy sources for renewable power generation and their costs vary from region to region. Therefore, the scenarios follow regionally different strategies and storylines, taking the different regional conditions into account on the supply side. The core strategy is the replacement of conventional thermal power and heat generators with solar, wind, geothermal, and other renewable options for the highly efficient generation of electricity for final energy consumption and the generation of synthetic fuels.

Our estimates of the potential for renewable power generation are based on the results of the REMix EnDat tool developed (Scholz 2012; Stetter 2014; Pietzcker et al. 2014). The technical potentials for solar and wind power in each world region were estimated while taking into account the different exclusion criteria and constraints documented by Stetter (2014). The analysis was used to estimate the ‘economic’ potential for each world region, which is the upper limit of the technological expansion under the different scenarios. ‘Economic’ potentials were derived by assuming the minimum annual full-load hours for each technology. In the case of PV, the assumed global economic potential was estimated to be in the order of 5.4 million TWh per year. The potential of CSP was even larger, at around 5.6 million TWh per year. The annual wind power potentials were estimated to be in the order of 500,000 TWh for onshore wind and around 100,000 TWh for offshore wind.

The harvesting of global solar radiation by PVs has enormous economic potential worldwide. In the last few years, economies of scale have led to a significant cost degression for PV modules, and large PV production capacities have been created. The PV technology also plays a major role in our scenarios because of its decentralized characteristics, which make it easy to build cost-efficient renewable power supplies in rural and isolated areas. However, its restriction to sunny hours causes high daily and seasonal variability. This results in rather low annual full-load hours. Therefore, large quantities of storage capacity must also be installed for short-term storage to support the major expansion of PV. The storage options considered are pumped hydro storage (e.g., by the enhancement of existing hydro sites) and a massive expansion of battery storage. This leads to uncertainties in the total infrastructure costs for the integration of high shares of PV into the power system and the mineral resources required for this. For this reason, the share of PV globally remains in the range of about 30% of total power generation, with the highest shares in the Middle East (40%), followed by OECD North America and Other Asia (35% each). The lowest shares, in the range of 20–25%, are in Eurasia, OECD Europe, Latin America, and China.

Wind power on land will achieve an average global generation share of 25% in 2050 in both alternative scenarios (compared with 8% in the reference case). The highest generation shares for onshore wind are assumed in India and Eastern Europe/Eurasia, at about 30% each. The lowest shares will be in China, the Middle East, and Non-OECD Asia, at 18–23%. For offshore wind, the global generation share will rise to 8% by 2050 under both alternative scenarios, compared with only 1% in the reference scenario. The highest offshore wind shares of 10–15% will be achieved under the 2.0 °C Scenario in the OECD regions and Eastern Europe/Eurasia. The lowest shares are predicted in the Middle East (2%), India (6%), and China (6.5%), where the potential is rather limited. The offshore shares under the 1.5 °C Scenario will tend to be slightly lower because of the stronger focus on PV and onshore wind as the best options for a very rapid expansion of RES.

Compared with PV and wind power, CSP plants promise highly flexible power and heat generation, with high capacity factors due to high-temperature heat storage. The use of heat for desalination can also contribute to secure water supplies in the sunbelt of the world. We assume that its multi-purpose uses and dispatchable generation capability can lead to a significant role for CSP in the medium- to long-term future, although levelized costs of CSP are today still much higher than they are for PV or wind, and investment costs for batteries for short-term electricity storage might also decrease in the future. Therefore, it is assumed that CSP will achieve an average global electricity generation share of 15% by 2050 in the 2.0 °C Scenario and 13% in the 1.5 °C Scenario, compared with 0.5% in the reference case. A high share, close to 30%, will be achieved, especially in the Middle East. This will include electricity generation for export to OECD Europe of up to 120 TWh per year by 2050. High CSP potentials are also assumed for Africa (16%), which will also export up to 280 TWh/year in 2050 from North Africa to OECD Europe—and for China (18–20%) and Non-OECD Asia (15–17%).

Hydro power generation will increase only moderately under the alternative scenarios compared with the reference case. This source has already been tapped and large hydro plants usually have significant ecological and societal consequences. Therefore, the average global power generation share will decrease in the alternative scenarios from today’s 16% to around 8%, whereas the reference scenario assumes a generation share of 14% in 2050. Nevertheless, a 30% increase in the global hydro power generation is assumed between 2015 and 2050. The highest power generation shares in 2050 are assumed to be in Latin America (24%), followed by OECD Europe (11%) and China (10%). The generation of hydro power plays only a minor role in the long term in the Middle East (1%), Africa, and India (each 4%).

Even smaller contributions are assumed for geothermal energy, ocean energy, and biomass. All three options have comparably high power-generation costs, but offer complementary characteristics and availabilities that may stabilize future electricity supply systems. The global average share of geothermal power generation is assumed to be about 5% in 2050, ocean energy use will contribute another 2%, and biomass, including co-generation, will achieve a maximum of 6–7% around 2030 and 5% in 2050. The highest share for geothermal power generation is assumed to occur in Eastern Europe/Eurasia (11%), for ocean energy in OECD Pacific (4%), and for biomass use in Latin America, Eastern Europe/Eurasia, and OECD Europe (8–9%). It is predicted that hydrogen will take an increasing share of the remaining thermal power generation, as a substitute for natural gas in gas turbines and combined cycle gas turbine plants and with increasing contributions from hydrogen fuel cells to co-generation. Figure 5.4 shows the basic storyline in global power generation under the 2.0 °C Scenario.

Development of the average global RES shares in total power generation in the 2.0 °C Scenario

5.4.3 RES Deployment for Heat Generation

Heat generation covers a broad range of processes, including district heat (either from co-generation or public heating plants), direct heating in buildings, and process heat in industry, commerce, and other sectors. Different technologies are considered for each sector, and strong RES expansion is assumed. The increasing heat extraction from co-generation will trigger increasing district heat use, which will stabilizes in the long term or decrease by 2050 with the declining heat demand attributable to ambitious efficiency measures. However, CHP will only contribute significantly in regions with a tradition of district heating and/or a high heat demand in the building sector. No strong expansion of heat grids is assumed in regions without existing heat grids and a low demand for space heat.

Electricity for heating is assumed to play a significant role in future energy systems. In contrast to today’s technology, flexible use is assumed, adjusted to variable feed-ins from variable renewable generation. This implies the availability of heat storages, smart operation controls, and flexible electricity tariffs. Electricity can be used with relatively low investment for space heating and is therefore easily combined with other heating technologies. For example, simple electric heaters can easily be integrated into heat storage or heating grids. However, more-efficient electric heat pumps generally require higher investment in both the heat pump itself and in the heat distribution within the building. Electricity can also be used to provide process heat in industry at high-temperature levels. The alternative scenarios globally assume a significant increase in the average electricity share of the final energy for heating in ‘Industry’ from 6% in 2015 to around 34% in the 2.0 °C Scenario and 37% in the 1.5 °C Scenario by 2050. All regions achieve shares of between 23% and 43%. Electricity shares in the ‘Residential and other’ sector are assumed to grow from 5% in 2015 to 30% in the 2.0 °C Scenario and 35% in the 1.5 °C Scenario.

However, the need for process heat at high temperature levels, problems associated with process integration, and specific process requirements call for additional process-specific strategies for replacing fossil fuels in the industry sector. As mentioned above, electrification is a comparatively efficient strategy. Other strategies are the use of biomass and hydrogen or—with some limitations—concentrated solar energy. While hydrogen is used to provide high temperature process heat in this study, it could—at least partially—be replaced by other synthetic energy carriers, such as synthetic methane, which can be generated from hydrogen and a (renewable) carbon source. This power-to-gas option has the advantage that it can be fed in into the gas grid, and act in storage and transport. However, energy losses are around 20% higher (compared with hydrogen). As a consequence, synthetic methane is not taken into account in the scenarios.

Overall, biomass use for heating in the ‘Residential and other’ sector is decreasing as the traditional and currently inefficient use of biomass is replaced by advanced efficient technologies, and biomass is used in a more efficient way in the energy system. Thus, the average global share of biomass as a final energy source for heating will decrease from today’s 34% to 22% by 2050 in the 2.0 °C Scenario and to 17% in the 1.5 °C Scenario, when direct electrification and indirect electrification (via synthetic gases and fuels) play a stronger role. In contrast, biomass use in the ‘Industry’ sector will increase continuously as the combustion of biomass can be used to generate high-temperature heat for many industrial processes for which renewable low-temperature heat sources are unsuitable. The average global share of biomass for the final energy for heating in the ‘Industry’ sector will increase from 9% in 2015 to 19% by 2050 in the 2.0 °C Scenario and to 14% in the 1.5 °C Scenario. The largest shares are assumed for Latin America (47%) and Africa (35%) in the 2.0 °C Scenario, where biomass residues are still rather abundant, with much lower values for the 1.5 °C Scenario (18–21%). In that scenario, biomass as a transition technology will be avoided due to the earlier development of alternative renewable technologies and electrification. The lowest shares are assumed for the Middle East (4%) and China (7%) in both alternative scenarios because of their limited sustainable potentials.

Solar collectors are suitable for hot water preparation and for supporting heating systems using heat storage. In heat grids, large heat storage systems can also be used to balance the seasonal heat demand and solar generation, and the integration of solar heat at low costs in the long term. The contributions of solar collectors to the heat supply are limited by the temperatures that collectors can provide (below 120 °C for traditional collectors and up to 300 °C for concentrated collectors) and the seasonal variations in regions with significant space heat demand. In the alternative scenarios, the global average share of solar thermal final energy for heating will rise to 19% in the ‘Residential and other’ sector. The largest shares are assumed to be in the Middle East (30–25%), where the abundance of solar radiation can be exploited by concentrated solar heat applications. All other regions have shares between 15% and 22%, considering the limited applicability of concentrated systems. The global average solar share in the ‘Industry’ sector will increase to 16% by 2050. The largest shares are achieved in the Middle East (25%) and Africa (20%) and the lowest shares are assumed in Eastern Europe/Eurasia (9%), followed by the OECD regions (10–13%).

Heat pumps allow very efficient heat supply. System-wide CO2 emissions depend on the CO2 emissions in the power mix. Because of their generation of low-temperature heat, heat pumps play a role in space heating in regions with moderate or cold climates, but large industrial heat pumps can also generate low-temperature heat for industrial processes and tap the enormous potential of waste heat. A continuous improvement in the coefficient of performance of heat pumps, which describes the ratio of useful energy in the form of heat to the required compressor energy in the form of electricity, in all existing plants from an average of 3 today to a value of 4 in 2050 is assumed. The application potential of heat pumps (in terms of MWth) is assumed to be limited by the low temperature of the heat provided, the increasing share of the grid-connected heat supply, the assumed increase in extensive building insulation, and the low space heating demand in some world regions. In addition to heat pumps, an increase in deep geothermal energy use is assumed for the ‘Industry’ sector, with an increase of up to 11% in the global average share of final energy by 2050 under both alternative scenarios.

Hydrogen use for direct heating is linked to the increasing substitution of natural gas with hydrogen in all sectors, except transport. This will lead to a hydrogen share of 12–14% in final energy for heating in the ‘Industry’ sector under the two alternative scenarios and 3% in the ‘Residential and other’ sector under the 2.0 °C Scenario and 4% under the 1.5 °C Scenario. The highest hydrogen shares in ‘Industry’ are assumed for OECD North America (22–23%), followed by other OECD regions, Eastern Europe/Eurasia, China, and the Middle East with shares of 13%–18%. The lowest shares, below 5%, are assumed for Latin America and Africa, where biomass from residues provides a flexible alternative. The highest hydrogen shares in the ‘Residential and other’ sector will be in the Middle East (7–10%), followed by OECD Pacific (6–8%) and OECD Europe (up to 9%) (Figs. 5.5 and 5.6).

Development of the average global RES shares of future heat generation options in ‘Industry’ in the 2.0 °C scenario

Development of the average global shares of future heat-generation options in the ‘Residential and other’ sector under the 2.0 °C scenario

5.4.4 Co-generation of Heat and Power and District Heating

Compared with condensing power plants with high efficiency losses due to waste heat, the co-generation of heat and power (combined heat and power, CHP) allows the highly efficient use of fossil and renewable fuels. If this approach is made more flexible with the help of heat storage, and if it is powered by renewable fuels, such as biomass or hydrogen from renewable electricity, CHP promises to generate not only renewable power in a flexible way but also to integrate efficiently large shares of renewable heat into energy systems via large and small district heating systems. Therefore, co-generation is a particularly good option in regions with high low- to medium-temperature heat demands (e.g., industrial consumers and space heating). Our modelling distinguishes between public generation in large CHP plants and CHP autoproduction. The latter comprises industrial CHP generators but also smaller plants in the ‘Residential and other’ sector. Power-to-heat ratios, efficiencies, and assumed costs reflect these different structural options. The IEA Energy Balances provides statistical values with which to calibrate the co-generation for each world region. The scenarios then assume the similar development of these parameters according to a defined advanced state of technology, with overall efficiencies of 85–90%.

Although absolute electricity generation from CHP will increase in all regions, all scenarios assume a decreasing power generation share for CHP in the long term due to the decommissioning of fossil-fuel generators, the limited availability of biomass, and the assumption that heat losses in CHP technologies will be reduced, leading to higher overall efficiency. Tables 5.13 and 5.14 show the resulting developments for power and heat as intensities summed across the ‘Industry’ and ‘Residential and other’ sectors. Whereas the absolute power supply from CHP will increase in all regions, the power-related intensities will decrease. Under the 2.0 °C Scenario, higher CHP power production is assumed to be higher than in the reference case, as a balancing option for variable renewable sources. CHP plants will play a smaller role in the future, particularly in non-OECD countries.

For heat, the situations are more diverse between the scenarios and regions. While the intensity of heat use from CHP will increase in the OECD regions, it will decrease in the non-OECD regions. Even though the intensity converges between OECD and non-OECD regions under all scenarios, the 2.0 °C and 1.5 °C Scenarios will achieve higher levels of intensity. However, the early reduction in demand in the 1.5 °C Scenario will preclude any additional demand for CHP.

5.4.5 Other Assumptions for Stationary Processes