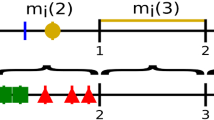

Abstract

We observe the effects of the three different events that cause spread changes in the order book, namely trades, deletions and placement of limit orders. By looking at the frequencies of the relative amounts of price changing events, we discover that deletions of orders open the bid-ask spread of a stock more often than trades do. We see that once the amount of spread changes due to deletions exceeds the amount of the ones due to trades, other observables in the order book change as well. We then look at how these spread changing events affect the prices of stocks, by means of the price response. We not only see that the self-response of stocks is positive for both spread changing trades and deletions and negative for order placements, but also cross-response to other stocks and therefore the market as a whole. In addition, the self-response function of spread-changing trades is similar to that of all trades. This leads to the conclusion that spread changing deletions and order placements have a similar effect on the order book and stock prices over time as trades.

Graphical abstract

Similar content being viewed by others

References

R. Cont, Quant. Finance 1, 223 (2001)

T. Chordia, R. Roll, A. Subrahmanyam, J. Financ. Econ. 65, 111 (2000)

W. Breymann, J. Am. Stat. Assoc. 101, 850 (2006)

J.-P. Bouchaud, J. Doyne Farmer, F. Lillo, How markets slowly digest changes in supply and demand, arXiv:0809.0822v1 (2008)

A. Chakraborti, I. Muni Toke, M. Patriarca, F. Abergel, Econophysics: Empirical facts and agentbased models, arxiv:0909.1974 (2009)

B. Tóth, Y. Lempérière, C. Deremble, J. de Lataillade, J. Kockelkoren, J.-P. Bouchaud, Phys. Rev. X 1, 021006 (2011)

Z. Eisler, J.-P. Bouchaud, J. Kockelkoren, The price impact of order book events: market orders, limit orders and cancellations, arXiv:0904.0900 (2009)

T.A. Schmitt, R. Schäfer, M.C. Münnix, T. Guhr, Europhys. Lett. 100, 38005 (2012)

T.A. Schmitt, D. Chetalova, R. Schäfer, T. Guhr, Europhys. Lett. 103, 58003 (2013)

J.A. Hausman, A.W. Lo, A.C. MacKinlay, An Ordered Probit Analysis of Transaction Stock Prices, Working Paper 3888, National Bureau of Economic Research, 1991

A. Kempf, O. Korn, J. Financ. Markets 2, 29 (1999)

R.F. Engle, A. Dufour, J. Finance 55, 2467 (2000)

V. Plerou, P. Gopikrishnan, X. Gabaix, H.E. Stanley, Phys. Rev. E 66, 027104 (2002)

B. Rosenow, Int. J. Mod. Phys. C 13, 419 (2002)

J.-P. Bouchaud, J. Kockelkoren, M. Potters, Quant. Finance 6, 115 (2004)

S. Mike, J. Doyne Farmer, An empirical behavioral model of liquidity and volatility, arXiv:0709.0159 (2007)

J.-P. Bouchaud, Y. Gefen, M. Potters, M. Wyart, Quant. Finance 4, 176 (2004)

S. Wang, T. Guhr, Market Microstruct. Liquid. 3, 1850008 (2017)

S. Wang, R. Schäfer, T. Guhr, Eur. Phys. J. B 89, 105 (2016)

S. Wang, R. Schäfer, T. Guhr, Eur. Phys. J. B 89, 207 (2016)

M. Benzaquen, I. Mastromatteo, Z. Eisler, J.-P. Bouchaud, J. Stat. Mech. 2, 023406 (2017)

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Grimm, S., Guhr, T. How spread changes affect the order book: comparing the price responses of order deletions and placements to trades. Eur. Phys. J. B 92, 133 (2019). https://doi.org/10.1140/epjb/e2019-90744-3

Received:

Revised:

Published:

DOI: https://doi.org/10.1140/epjb/e2019-90744-3