Abstract

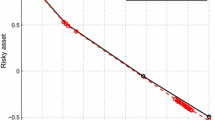

Consideration was given to the optimal control of discrete stochastic systems by the probabilistic quality criterion. The new characteristics of the Bellman equation for this class of problems were examined, and the two-sided estimate of the Bellman function was determined. The problem of optimal control of the security portfolio with one riskless and a given number of risk assets was considered by way of example. The class of strategies featuring asymptotic optimality was established using the two-sided estimate of the Bellman function.

Similar content being viewed by others

References

Malyshev, V.V. and Kibzun, A.I., Analiz i sintez vysokotochnogo upravleniya letatel’nymi apparatami (Analysis and Design of Precision Control of Flight Vehicles), Moscow, Mashinostroenie, 1987.

Zubov, V.I., Lektsii po teorii upravleniya (Lectures on Control Theory), Moscow: Nauka, 1975.

Afanas’ev, V.N., Kolmanovskii, V.B., and Nosov, V.R., Matematicheskaya teoriya konstruirovaniya sistem upravleniya (Mathematical Theory of Control System Design), Moscow: Vysshaya Shkola, 2003.

Krasovskii, N.N., On Optimal Control under Random Perturbations, Prikl. Mat. Mekh., 1960, vol. 24, no. 1, pp. 64–79.

Azanov, V.M. and Kan, Yu.S., Design of Optimal Strategies in the Problems of Discrete System Control by the Probabilistic Criterion, Autom. Remote Control, 2017, vol. 78, no. 6, pp. 1006–1028.

Azanov, V.M. and Kan, Yu.S., One-parameter Problem of Correcting the Trajectory of the Flight Vehicle by the Probability Criterion, Teor. Sist. Upravlen., 2016, no. 2, pp. 1–13.

Kibzun, A.I. and Ignatov, A.N., Reduction of the Two-Step Problem of Stochastic Optimal Control with Bilinear Model to the Problem of Mixed Integer Linear Programming, Autom. Remote Control, 2016, vol. 77, no. 12, pp. 2175–2192.

Kibzun, A.I. and Ignatov, A.N., The Two-Step Problem of Investment Portfolio Selection from Two Risk Assets via the Probability Criterion, Autom. Remote Control, 2015, vol. 76, no. 7, pp. 1201–1220.

Vishnyakov, B.V. and Kibzun, A.I., A Two-Step Capital Variation Model: Optimization by Different Statistical Criteria, Autom. Remote Control, 2005, vol. 66, no. 7, pp. 1137–1152.

Kibzun, A.I. and Kuznetsov, E.A., Optimal Control of the Portfolio, Autom. Remote Control, 2001, vol. 62, no. 9, pp. 1489–1501.

Bunto, T.V. and Kan, Yu.S., Quantile Criterion-based Control of the Securities Portfolio with a Nonzero Ruin Probability, Autom. Remote Control, 2013, vol. 74, no. 5, pp. 811–828.

Grigor’ev, P.V. and Kan, Yu.S., Optimal Control of the Investment Portfolio with Respect to the Quantile Criterion, Autom. Remote Control, 2004, vol. 65, no. 2, pp. 319–336.

Jasour, A.M., Aybat, N.S., and Lagoa, C.M., Semidefinite Programming for Chance Constrained Optimization over Semialgebraic Sets, SIAM J. Optim., 2015, vol. 25, no. 3, pp. 1411–1440.

Jasour, A.M. and Lagoa, C.M., Convex Chance Constrained Model Predictive Control, arXiv Preprint, 2016, arXiv:1603.07413.

Jasour, A.M. and Lagoa, C.M., Convex Relaxations of a Probabilistically Robust Control Design Problem, 52nd IEEE Conf. Decision Control, Firenze, 2013, pp. 1892–1897.

Kan, Yu.S. and Kibzun, A.I., Problems of Stochastic Programming with Probabilistic Criteria, Moscow: Fizmatlit, 2009.

Kibzun, A.I. and Kan, Yu.S., Stochastic Programming Problems with Probability and Quantile Functions, Chichester: Wiley, 1996.

Kan, Yu.S., Control Optimization by the Quantile Criterion, Autom. Remote Control, 2001, vol. 62, no. 5, pp. 746–757.

Author information

Authors and Affiliations

Corresponding author

Additional information

Original Russian Text © V.M. Azanov, Yu.S. Kan, 2018, published in Avtomatika i Telemekhanika, 2018, No. 2, pp. 3–18.

Rights and permissions

About this article

Cite this article

Azanov, V.M., Kan, Y.S. Bilateral Estimation of the Bellman Function in the Problems of Optimal Stochastic Control of Discrete Systems by the Probabilistic Performance Criterion. Autom Remote Control 79, 203–215 (2018). https://doi.org/10.1134/S0005117918020017

Received:

Published:

Issue Date:

DOI: https://doi.org/10.1134/S0005117918020017