Abstract

Life insurance players have started realizing that their business depends on customer service and customer satisfaction. This research, using confirmatory factor analyses, proposes a six dimensional service-quality instrument consisting of ‘assurance’, ‘personalized financial planning’, ‘competence’, ‘corporate image’, ‘tangibles’ and ‘technology’ in life insurance. A causal model, using structural equation modeling, is suggested to investigate the effects of the proposed service quality instrument on customer satisfaction (‘satisfaction with agents’, ‘satisfaction with functional services’, ‘satisfaction with company’ and finally with ‘overall satisfaction’). The proposed framework attempts to provide a blueprint for appropriate course of action (by life insurance service providers) to create a base of satisfied customers through quality services.

Similar content being viewed by others

INTRODUCTION

The life insurance industry like many other financial services industries is facing a rapidly changing market, new technologies, economic uncertainties, fierce competition and more demanding customers and the changing climate has presented an unprecedented set of challenges. Just like companies of other business domains, life insurance also considers their customers as the most important asset. However, the most critical issue is whether this customer orientation is reflected in their strategies.

Life insurance providers increasingly recognize that today's customers who insist on improvements in quality of services have many alternatives and, therefore, may more readily change providers if not satisfied. This is evident from the not so uncommon practice of ‘policy lapses’ readily embraced by dissatisfied policyholders. The decrease in customer loyalty has made management of service quality and customer satisfaction critically important factors for insurance players. The life insurance providers need to reconfigure their strategy and business to sustain or improve their competitive advantage, and for this they first need to consider how to create a satisfied customer base that will not be eroded even in the face of fierce competition.

For answering this fundamental question, these companies must realize the necessity of studying and understanding various antecedents of customer satisfaction. A number of studies in different fields confirmed that service quality is the antecedent towards customer satisfaction.1, 2, 3, 4 Therefore, the insurance players need to realize that business depends on client service and the satisfaction of the customer and therefore it is imperative for them to improve customer service quality.

THEORETICAL OBSERVATIONS

Service quality

Service quality takes a prominent position in the marketing management literature. Service quality is usually defined as the customer’s impression of the relative inferiority/superiority of a service provider and its services,5 and is often considered similar to the customer’s overall attitude towards the company.6, 7, 8 Researchers have tried to conceptualize and measure service quality and explain its relation to the overall performance of companies and organizations.

A common denominator of research on service quality is the conclusion that, because services are intangible, heterogeneous, and their ‘production’ and ‘consumption’ are usually inseparable, the process used by customers to evaluate service quality is exceptionally composite and cannot be easily identified. The idea that services are evaluated both by the outcome and by the production and delivery process is commonly accepted.

On service quality modeling, Grönroos’9 model divides the customer's perceptions of any particular service into two dimensions, namely technical and functional quality. Parasuraman et al 10 proposed the gap model of service quality that operationalized service quality as the gap between expectations and performance perceptions of the customer. Further, Murfin et al 11 developed the service quality model for medical services. Soteriou and Stavrinides12 developed the service quality model for bank branch in order to optimally utilize its resources. Zhu et al 13 and Seth et al 14 proposed the service quality model highlighting the information technology-based service options to investigate the relationship between IT-based services and customer’s perceptions of service quality. On the basis of their conceptual/empirical studies, researchers derived and proposed different service quality dimensions for various service applications as illustrated in Table 1.

However, the most widely used service quality measurement tools include SERVQUAL6 and SERVPERF.1The SERVQUAL scale measures service quality based on difference between expectations and performance perceptions of customers using 22 items and five dimensional structures. In the SERVPERF scale, service quality is operationalized through performance only scores based on the same 22 items and five dimensional structure of SERVQUAL.

SERVQUAL is appreciated by researchers13, 20 for its robust and well defined structure. However, some authors1, 21 found the SERVPERF scale to outperform the SERVQUAL scale in terms of both reliability and validity. But SERVQUAL has more and diverse applicability.

Customer satisfaction

Satisfaction, as discussed by Oliver,22 involves ‘an evaluative, affective, or emotional response’. In his book, Oliver22 provided a definition that he thought was consistent with theoretical and empirical evidence available to him at the time. He defined satisfaction/dissatisfaction as ‘the consumer’s fulfilment response, the degree to which the level of fulfilment is pleasant or unpleasant’. Therefore, satisfaction is the customer’s overall judgment of the service provider.23 Crompton and MacKay24 stated, ‘Satisfaction is a psychological outcome emerging from an experience, whereas service quality is concerned with the attributes of the service itself’.

Relationship between service quality and customer satisfaction

Quality and customer satisfaction have long been recognized as playing a crucial role for success and survival in today's competitive market. Considerable research has been conducted on these two concepts.

Whereas there exists a widespread agreement that understanding what contributes to customer satisfaction could be the key to achieving competitive advantage, an overview of the literature shows that as a theoretical construct, customer satisfaction is problematic to define and operationalize, especially in relation to perceived service quality. Some authors have suggested both that perceived service quality and customer satisfaction are distinct constructs,22, 25 and that there is a causal relationship between the two.1, 4, 26 In some cases, however, the constructs have been used interchangeably.22, 25, 27, 28, 29 It would seem that at the most general level, perceived service quality and customer satisfaction are evaluation or appraisal variables related to customer judgments about a product.22, 27 By defining perceived quality as the customer’s long-term, cognitive evaluations of a company’s service delivery, and customer satisfaction as a short-term emotional reaction to a specific service performance, Lovelock and Wright30 bring the time dimension into discussion. They argue that satisfaction is by default experience-dependent as customers evaluate their levels of satisfaction or dissatisfaction after each service encounter. In turn, this information is used to update customer perceptions of quality. However, quality attitudes are not necessarily experience-dependent (for example they can be based on word of mouth or advertising). In other words, it is satisfaction that determines quality and not vice versa. Oliver’s22 research on the direction of the causal relationship between perceived quality and satisfaction adds to the discussion by indicating that the direction depends on the level at which the measurement is conducted: at the single-transaction level there is a strong quality–affects–satisfaction relationship; and at the multiple-transaction level there is a strong satisfaction–affects–quality relationship, as overall satisfaction judgments influence consumers’ views about perceived quality. Parasuraman et al 28 address these issues directly by developing two different models: a single-transaction (encounter) model and a multiple-transaction (global) model, in which they differentiate between past and present transactions. However, in both models it is perceived quality that influences customer satisfaction. Thus, their work supports the dominant view in the literature: that with regard to quality satisfaction is the super-ordinate construct.1, 4, 25, 26, 31, 32, 33

Indian life insurance sector

The US$41-billion Indian life insurance industry is considered to be the fifth largest life insurance market in the world. It is growing at a rapid pace of 32–34 per cent annually, according to the Life Insurance Council (www.lifeinscouncil.org).34 The total number of life insurers registered with the Insurance Regulatory Development Authority (IRDA) has gone up to 23. Since the opening up of the insurance sector in India, the industry has received Foreign Direct Investment (FDI) to the tune of $525.6 million.

Life Insurance Corporation's (LIC) new premium collection touched $ 9.58 billion in the April–December 2009 period while the combined business of the 22 private insurers grew to US$5.07 billion from the previous year, as per data collated by IRDA (www.irdaindia.org).35 The LIC posted a 50 per cent growth in new premium collection in the first 9 months of the 2010 fiscal, increasing its market share to 65 per cent from 56 per cent a year ago. In 2010 fiscal year, it crossed the $54.1 billion mark in total premium income by the end of March 2010, showing a growth of 29 per cent (www.ibef.org).36

The potential for expansion of the market is huge as India is far behind world averages in terms of insurance penetration, and insurance density. Therefore, there is a tremendous opportunity in a vast untapped market. Add to this the rising per capita income and a growing middle class, and the picture is all the more promising. Insurance companies in the developed world, where insurance has much higher penetration, realize the huge potential of insurance industry in India. The government is likely to reintroduce the Insurance Bill that proposes to increase the FDI cap in private sector insurance companies from 26 per cent to 49 per cent. This would increase the entry of many more business houses in the industry.

But, as an increasing number of business houses enter the life insurance industry, even survival is going to be difficult for many companies. In the face of such stiff competition, organizations need to make sure that they put their efforts in the right places.

Previous research indicated that a comparison of mean scores on the importance of service attributes provides a very effective method of measuring the ability of services to meet the needs of the customers.37 Perceived service quality has a significant effect on the attitude towards obtaining insurance.38 Moreover, the degree of success in the implementation of enterprise mobilization in the life insurance industry is positively correlated to the management performance of external aspects like providing increased customer satisfaction.39 It has been observed that insurance agents should constantly monitor the level of satisfaction among his/her customers to keep themselves close to the customers for fulfilling their needs.40 Customer satisfaction and the salesperson's relation orientation significantly influences the future business opportunities and as the salespersons are able to enhance their relationships with the clients, clients are more satisfied and are more willing to trust, and thus secures the long-term demand for the services.41 The company and agent's service quality as well as recommendations of friends are factors that significantly affect decisions of purchasing life insurance policies.42

To enhance customer satisfaction, life insurance providers ideally should measure and improve the approaches to delivery of service. In addition, it is mandatory that they commence a search for the important quality dimensions in the life insurance sector. The service quality dimensions could be a basis for differentiation for the players, which could be developed into a Sustainable Competitive Advantage in the long run. These non-price instruments are usually ascribed more potency than price changes, because they are hard to match. Any reaction from the competitors to match any of these may require a change in the entire service strategy.43

OBJECTIVES OF THE STUDY

The purpose of this article is to explore and consequently confirm the underlying dimensions of consumer perceptions of service quality vis-à-vis life insurance sector. It also attempts to represent and estimate the multiple and interrelated causal relationships among these perceptual service quality dimensions with the overall satisfaction with life insurance services. It has been attempted to understand and measure the complex and interdependent relationships between service-quality dimensions, satisfaction dimensions and overall satisfaction with life insurance services.

RESEARCH METHODOLOGY

Conclusive Cross-sectional Descriptive Research Design has been used to study the service quality structure and its key dimensions in life insurance sector. The survey instrument was a SERVQUAL type questionnaire relevant to the insurance industry. The questionnaire was divided into two sections. In the first part, respondents were asked to evaluate parameters on service quality relevant to insurance industry (on a 5 point scale anchored at ‘strongly agree’ and ‘strongly disagree’). This part consists of 26 statements for performance scores, regarding various aspects of service quality. In the second part information related to different socioeconomic and demographic criteria like income, age, profession, educational qualification and so on was collected.

These service quality aspects were identified by a detailed exploratory identification process. This included five focus group discussions (with 40 life insurance policyholders); eight in-depth interviews (three with branch managers and five with agents of various life insurance companies). Content analysis of focus group discussions and depth interviews was performed. In content analysis, the responses (oral as well as written) were categorized and classified. Then they are coded for tabulation purpose. Thereafter the frequency counts (of different categories) were compared. The method deployed was qualitative content analysis (inductive category development and deductive category application).44 These responses were augmented from current literature in order to draw a wider and more in-depth inventory of service quality items in life insurance context. Finally, 26 attributes of service quality in life insurance sector were identified after the process.

A pilot study was conducted with a small sample size of 60, to clarify the overall structure of questionnaire. The respondents provided comments on clarity of some items and confirmed face validity of items in the questionnaire. The respondents for the pilot survey (different category of life insurance policyholders) were chosen by shopping mall intercept sampling method.

Quota and shopping mall intercept sampling schemes have been employed (respondents were intercepted/selected at fixed locations in various offices of insurance companies, marketplaces, shopping malls, institutions, offices and localities of various cities according to defined quotas). One thousand questionnaires were filled from different respondents (policyholders). However, 868 questionnaires were found complete in all respects. The response rate was 86.8 per cent. An attempt has been made to keep the sample fairly representative across the demographic variables by constructing quotas according to different socioeconomic and demographic criteria like income, age, profession, educational qualification and so on (Table 2).

The areas of our sampling are various cities like Lucknow, Delhi-NCR, Mumbai, Bangalore and Hyderabad. The time frame of the study was July 2009–December 2009. Primary-stage sampling units were the respondents who purchased at least one life insurance product (whole life insurance policy and/or an endowment policy) in the past 3 years. The questionnaires were administered personally to ensure the authenticity of information provided by the respondents.

Validity analysis

Content validity

For the present study, the content validity of the instrument was ensured as the service quality dimensions and items were identified from the literature and exploratory investigations, and were thoroughly reviewed by professionals and academicians.

Reliability analysis

We examined the reliability of the data by running reliability test. For various sets (total number of sets being six) of associated factors used in the questionnaire, values of coefficient alpha (Cronbach's α) have been obtained. Among the reliability tests that were run, the minimum value of coefficient alpha (for performance scores) obtained was 0.743 (substantially higher than 0.6, which is the thumb value for the lower limit of acceptability for satisfactory internal consistency reliability), which shows that data have satisfactory reliability and the inconsistency as caused by random error has been at a manageable level (Table 3).

DATA ANALYSIS

Exploratory factor analysis (EFA)

In order to explore the underlying dimensions of consumer perceptions of service quality vis-à-vis life insurance sector (as expressed by performance scores on 26 statements), EFA was performed. The factor analysis results are shown in Tables 4 and 5. First, appropriateness of factor analysis for the data has been checked by Bartlett's test of sphericity and Kaiser-Meyer-Olkin (KMO) measure of sample adequacy. Bartlett's test is used to examine the hypothesis that the population correlation matrix is an identity matrix, that is the variables are uncorrelated in the population. KMO measure indicates the proportion of variance in the variables, which is common variance, that is, which might be caused by underlying factors. The results from Table 4 shows that value of KMO statistic is very high (0.955) and Bartlett's test of sphericity is significant (sig=0.000), which reveals that data are appropriate for factor analysis. The total variance accounted for by all of the six components explains nearly 78.3 per cent of the variability in the original 26 variables (Table 5). So, we can reduce the original dataset by using these six components (Eigen values greater than 1 as shown in Table 5) with only 21.7 per cent loss of information.

The Rotated Component Matrix reveals six factors (which represent the six broad perceptual dimensions of service quality termed as assurance, competence, personalized financial planning, corporate image, tangibles and technology) derived from 26 variables (which represent the consumer perceptions of life insurance policyholders vis-à-vis service quality). To confirm the six-dimensional structure of customer perceived service quality in life insurance sector (as obtained by EFA); we have used confirmatory factor analysis (CFA).

Confirmatory factor analysis

Factor analysis is primarily an exploratory technique because of researcher's limited control over which variables are indicators of which latent construct. Structural Equation Modeling (SEM), however, can play a confirmatory role because the researcher has complete control over the specification of indicators for each construct. So, CFA provides enhanced control for assessing unidimensionality and has more construct validity than EFA.45 CFA is used here, particularly for validation of scales for the measurement of constructs derived from EFA. ‘LISREL 8.8 for Windows’ software was used for this purpose.

Validity analysis

The estimates of measurement model and the construct loadings, as provided by the statistical software package LISREL 8.8, are presented in Table 6. As there is no offending estimate in the construct loadings, various goodness-of-fit criteria have been assessed.

Overall model fit

The first assessment of goodness of fit for the model is done for the overall model (Table 7). It provides the degree to which the specified indicators (variables) represent the hypothesized constructs (dimensions). The three useful types overall model fit measures are: absolute, incremental and parsimonious fit measures.

Absolute fit measures

Value of Goodness-of-Fit Index (GFI) is 0.937, which is higher than the recommended value of 0.90 and Adjusted Goodness-of-Fit Index (AGFI) is 0.879, which is though lower than the recommended level (0.90) but close to it. Value of Root Mean Square Residual (RMSR=0.082) is quite low. Therefore, all the measures provide acceptable support for acceptability of overall model.

Incremental fit measures

These measures assess the incremental fit of the model compared to a null model. Null model is hypothesized as a single factor model with no measurement error. Here, both Tucker-Lewis Index (TLI) and Normed Fit Index (NFI) are higher than the recommended level of 0.90.

Parsimonious fit measures

This is the final measure, which assess the parsimony of the proposed model. It evaluates the fit of the model versus the number of estimated coefficients needed to achieve that level of fit. AGFI (0.879) is close to the recommended level of 0.90 and Normed Chi-square (1.82) is within the recommended range of 1.0 to 2.0. These results provide support to model parsimony.

Therefore, we can say that all the measures of overall model goodness of fit provide the acceptability to the proposed model.

Measurement model fit

After analyzing and accepting the goodness of fit for the overall model, all the six constructs (dimensions) are evaluated at two levels:

-

examining the variable loadings for statistical significance;

-

assessing the dimension's reliability, variance extracted, unidimensionality and convergent validity.

Results from Table 6 indicate that all the variables are significant (sig <0.05); as the t-values associated with each of variable loadings exceed the critical value for 5 per cent level of significance. Thus, it can be said that all the variables are significantly related to their specified dimensions. This substantiates the proposed relationship among variables and their dimensions.

In the second step, the estimates of the reliability, the variance-extracted measures and the various fit indices for each dimension (to assess the representativeness of each dimension) have been analyzed (Table 8). Results of Construct Reliability show that reliability coefficients of all dimensions exceed the recommended level of 0.700. Further, it has been found out that there is substantial extraction of variance (more than 50 per cent) for all the dimensions. Therefore, major portion of variances of variables have been accounted for by these considered dimensions, as obtained by CFA.

The Comparative Fit Index (CFI) values obtained for all the six dimensions of service quality are more than 0.90 (recommended level) as shown in Table 8. This indicates a strong evidence of unidimensionality, showing the strong representativeness of constructs. This also establishes the Construct Validity of the model. Construct Validity is the assessment of the degree to which an operationalization correctly measures its targeted variables.46

Bentler-Bonett coefficient47 is used to measure Convergent Validity of the model, which is the measure of the degree to which multiple methods of measuring a variable provide the same results.46 Results from the Table 8 show that all six dimensions have Bentler-Bonett Goodness of Coefficient more than 0.90, which is above the required level. This indicates substantial Convergent Validity. Finally, GFI for all of the six dimensions having values more than 0.9 (recommended level) shows best fit of the considered model.48

The overall model goodness-of-fit results and the measurement model fit results provide substantial support for confirmation to the proposed six-dimension model of consumer perceptions of service quality vis-à-vis life insurance sector.

Factors extraction results

As obtained in the Table 6, the CFA provided the construct loading for various factors (dimensions).

Factor 1 incorporates the variables – ‘Trained and well-informed agents’, ‘Approaching from customer's point of view’, ‘Trusting agents when explaining policies’, ‘Clarity in explaining policy's terms and conditions’ and ‘Understanding intimately specific needs’. These variables reflect that policyholders are assured that they are being dealt with representatives who are well versed with the nitty-gritty's of the service and intend to act as someone who would help them to identify their specific needs, and also provide solution accordingly. As all these variables assure the policyholder of knowledge of agents and their ability to inspire trust and confidence, this factor has been labeled as assurance.

Factor 2 consists of variables – ‘Provision of flexible payment schedule’, ‘Availability of flexible product solution’, ‘Provisions for convertibility of products’, ‘Supplementary services’. Life insurance involves long-term association, hence policyholder moves through different life cycle stages in this long period and his needs and preferences change accordingly. Here, all these variables are depicting handling of these changing preferences by providing flexible solutions and convertibility options and giving personalized services. Therefore, this factor can be labeled as personalized financial planning.

Factor 3 has variables – ‘Staff dependable in handling customer's problems’, ‘Efficient staff’, ‘Easy access to information’, ‘Prompt and efficient grievance handling mechanism’ and ‘Prompt and hassle free claims settlement’. These components talk about the ability of the service provider to perform service dependably and efficiently and also about their willingness to provide hassle-free and prompt services. Therefore, this factor can be labeled as competence.

Factor 4 incorporates variables – ‘Adequate no. of branches’, ‘Accessible location of the branch’, ‘Good ambience of the branch’, and ‘Possessing good certification and credentials’. As all these components are related to providing physical facilities and communication materials, therefore this factor has been labeled as tangibles.

Factor 5 has variables – ‘Innovativeness in introducing new products’, ‘Courteous agents’, ‘Value for money’, ‘Simple and less time consuming procedure for purchasing a policy’, and ‘Financially stable company’. All these components are related to creating an overall image of the organization in the eyes of the customers. Therefore, this factor can be labeled as corporate image.

Factor 6 incorporates variables – ‘Easy online transaction’, ‘Prompt complaint handling, online’ and ‘Proactive information through e-mail or SMS’. As all these components are related to use of modern aids in providing service, therefore this factor has been labeled as technology.

Structural equation model for customer satisfaction with service quality

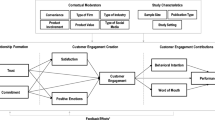

SEM is a multivariate technique combining aspects of multiple regression and factor analysis to estimate a series of interrelated dependence relationships simultaneously. Here, SEM has been used to represent the multiple and interrelated dependence relationships among six dimensions of consumer perceived service quality (exogenous variables); three satisfaction components: ‘satisfaction with the life insurance agents’, ‘satisfaction with functional services provided by the life insurance sector’ and ‘satisfaction with the insurance company’ (endogenous variables); and finally with the ‘overall satisfaction with the life insurance services’ (endogenous variable). In the model, ‘overall satisfaction’ has been considered as a function of ‘satisfaction with contact person’ (agent), ‘core service’ (functional services) and ‘institution’ (company); as proposed by Gronroos49 and Lehtinen.50 The services literature49, 50 distinguishes between the quality produced as the customer interacts with the contact resources of the organization, what the customer actually gets as a result of interaction (core elements) and the image of the company.

SEM is useful for estimating the interdependent multiple relationships and representing the latent concepts (satisfaction) in these relationships. The prime objective is to understand and measure this complex relationship between service-quality dimensions, satisfaction dimensions and overall satisfaction with life insurance services.

Path diagram has been constructed by LISREL 8.8 to depict the series of causal relationship (Figure 1). This diagram represents predictive relationships between constructs and associative relationships among constructs. The path diagram forms the basis of path analysis for the SEM. It is the procedure for empirical estimation of the strength of each relationship (path) depicted in the path diagram. After developing the model and portraying it in path diagram, the model has been specified in a more formal terms (in the structural equations, and in the measurement model).

SEM for customer satisfaction with service quality in life insurance industry.Note: Values in the figure are Construct Loading Coefficients for each endogenous construct with its exogenous constructs, indicating degree of causal relationship between them.

Model estimation

The desired structural equation model was estimated with LISREL 8.8 and expressed in Table 9. The corresponding measurement model specifies the correspondence of indicators to constructs at two stages. At the first stage of structural equation model, associative relationship of the six exogenous constructs (quality dimensions) with the three endogenous constructs (satisfaction dimensions) has been considered. At the second stage, it has been attempted to define endogenous construct (overall satisfaction) as the function of the three satisfaction dimensions.

Evaluating goodness-of-fit criteria

First, the inconsistency in the estimated path coefficients has been checked, in terms of offending estimates (coefficients exceeding the acceptable limits, that is standardized coefficients exceeding 1). Results from Table 9 clearly indicate the absence of any offending estimate.

Overall model fit

The overall fit of the structural equation model has been examined, at the first stage, to ensure that model is an adequate representation of the entire causal relationship (from six service quality dimensions to three satisfaction dimensions to the final overall satisfaction).

Absolute fit measures

The value of the likelihood Chi-square is 119.422 and is statistically significant (Table 10). Values of GFI and AGFI are both more than the required level of 90 per cent, both RMSR (RMSR=0.082) and Root Mean Square Error of Approximation (RMESA=0.071) are at moderate acceptable level of 80 per cent. These results clearly indicate that the considered model is substantially acceptable.

Incremental fit measures

At this stage, the considered model is evaluated in comparison to a null model. The value of Chi-square is 427.54, therefore there is substantial improvement in terms of reduction in the Chi-square value, because of the estimated coefficients in the proposed mode (Table 10). Results (Table 10) show that both TLI and NFI have values more than the required level of 0.90.

Parsimonious fit measures

Lastly parsimonious measures are considered. Results (Table 10) show that CFI (0.914) is above the threshold limit but both Parsimonious Normed Fit Index (PNFI=0.872) and Parsimonious Goodness-of-Fit Index (PGFI=0.822) are near to the desired threshold limit. So, the considered model can be considered as marginally acceptable.

Measurement and structural model fit

After ensuring the goodness of fit for overall model, measurement and structural model fit are examined. It has been found that all the construct loadings for the model are significant at 5 per cent level of significance (Table 9). The value of R-square for the entire model is obtained as 0.726, which is substantially high and significant (Table 10).

The overall model goodness-of-fit results and the measurement model fit results provide substantial support for the acceptance of the considered structural equation model for service quality and customer satisfaction in the life insurance industry.

Structural equation model for customer satisfaction

After examining the goodness of fit, reliability and validity measures, path coefficients of different causal relationships of the proposed customer satisfaction model have been considered. The results from the structural equation model (Table 9 and Figure 1) show that ‘satisfaction with life insurance agents’ can be significantly explained by ‘assurance’. ‘Personalized financial planning’ has significant impact upon ‘satisfaction with life insurance agents’ and ‘satisfaction with functional services provided’, but there is substantial difference in the strength of the relationship. ‘Personalized financial planning’ has a major impact upon ‘satisfaction with functional services’. ‘Competence’ significantly affects both ‘satisfaction with functional services’ and ‘satisfaction with the life insurance company’ with almost equal magnitude. ‘Corporate image’ has significant impact upon both ‘satisfaction with the company’ and ‘satisfaction with functional services’. While comparing the strength of relationships, we can say that ‘corporate image’ has higher impact upon ‘satisfaction with the company’ as compared to that on ‘satisfaction with functional services’. Further, as compared to ‘corporate image’, ‘competence’ has significantly higher impact upon ‘satisfaction with functional services’. ‘Tangibles’ significantly affects ‘satisfaction with the company’. Similarly, ‘technology’ has influence upon ‘satisfaction with functional services’. But both of these relationships are moderate in nature.

Therefore, results from the path analysis suggest that ‘assurance’ and ‘personalized financial planning’ are significant predictors of ‘satisfaction with the insurance agent’, who is the main channel of communication and business between customer and the insurance company. Here, ‘assurance’ is the major predictor of this satisfaction. Further, ‘personalized financial planning’, ‘technology’, ‘competence’ and ‘corporate image’ are significant predictors of ‘satisfaction with the functional services provided by the insurance company', which is the main driver of relationship between the customer and the company. Here, ‘competence’ and ‘personalized financial planning’ are the major predictors. Lastly, ‘competence’, ‘corporate image’ and ‘tangibles’ are the significant predictors of ‘satisfaction with the insurance company’, with ‘competence’ being the major predictor, followed by ‘corporate image’.

At the second stage, customers’ ‘overall satisfaction’ with the service quality in life insurance industry can be explained in terms of three satisfaction components (endogenous variables): ‘satisfaction with the life insurance agents’, ‘satisfaction with functional services provided by the life insurance sector’ and ‘satisfaction with the insurance company’. Here, the all three relationships are significant. ‘Overall satisfaction’ is best explained in terms of ‘satisfaction with functional services’ (0.883), closely followed by ‘satisfaction with agents’ (0.728). On the other hand, ‘satisfaction with the insurance company’ has much lower influence upon ‘overall satisfaction’ (0.402). So, it can be said that these three satisfaction components are significant determinants of overall customer satisfaction.

The relationship between the endogenous variables representing the three satisfaction components has also been examined. There is a strong and significant relationship between ‘satisfaction with agents’ and ‘satisfaction with functional services’ (0.808). Similarly, ‘satisfaction with financial services’ and ‘satisfaction with the insurance company’ are correlated with marginally lower value (0.711). Relationship between satisfaction with life insurance agents and satisfaction with life insurance companies is significant but has substantially lower magnitude (0.534).

DISCUSSION AND MANAGERIAL IMPLICATIONS

This article strives to derive a reliable and valid measurement instrument for the Indian life insurance industry. For this, an exploratory qualitative study was undertaken to better understand the key dimensions of service quality. The insights obtained from the exploratory qualitative study revealed the emergence of new factors: for example ‘technology’, in affecting the overall service quality. These findings were confirmed through extensive analysis procedures using exploratory and confirmative factor analysis. Finally, for assessing customer perceived service quality, a six dimensional instrument comprising of ‘assurance’, ‘personalized financial planning’, ‘competence’, ‘corporate image’, ‘tangibles’ and ‘technology’ was revealed.

Further, the study investigates the causal relationship between these service quality dimensions and overall customer satisfaction. The current study analyzes overall ‘customer satisfaction’ through ‘satisfaction with agents’, ‘satisfaction with functional services’ and ‘satisfaction with company’. According to the results of path analysis, all three influence ‘overall customer satisfaction’ in the life insurance setting.

It is found that the major predictor of ‘overall customer satisfaction’ was ‘satisfaction with functional services’, followed by ‘satisfaction with agents’ and ‘satisfaction with company’. This clearly reflects the priorities of the policyholders. ‘Satisfaction with functional services’ is the primary determinant of the relationship with the insurance services. Customers want that these service should be provided to them efficiently (prompt and hassle-free) as they perceive life insurance as a guard against the uncertainties of the future. Further, they demand flexible solutions and convertibility options related to investment options and consequently they desire that the services should be personalized involving efficient handling of these changing preferences. Customer will not settle for anything mediocre in the context of functional services because it is the major contributor to their perception of quality and thereby satisfaction vis-à-vis insurance services. At the second place in the hierarchy, there is ‘satisfaction with the agent’. This is because customers perceive the role of agents as their means of contact with the service bought and also view the necessity for an ongoing interaction with the agents. An insurance policy is almost always sold by an agent who, in 80 per cent of the cases, is the customer’s only contact.51 Life insurance is a professional service that is characterized by high involvement of the customers with their agents, primarily owing to the importance of tailoring specific needs, the variability of the products available, the complexity involved in the policies and processes.52 This necessitates the involvement of customers in every aspect of the transaction. So, customers seek long-term relationships with their insurance agents and their service providers for delivery of tailored and efficient functional services, in order to reduce risks and uncertainties.53

On the other hand, ‘satisfaction with the insurance company’ has much lower influence upon overall satisfaction (0.402). This might be attributed to the fact that in life insurance, there is not much contact between the insurance companies and the policyholders. It is the agent, who takes the center stage of this relationship, in majority of cases. Moreover, there is not much difference between companies and their policies because of the strict guidelines by the regulators.

Analyzing the first level of the proposed relationship, ‘satisfaction with functional services’ has been strongly affected by ‘competence’, closely followed by ‘personalized financial planning’. This is expected as ‘competence’ implies that the agent will be prepared to deliver on the terms of the life insurance policy when it is redeemed. It also means that the customer can count on the efficiency of the grievance handling mechanism to resolve any problems that may arise at any point of time in future. As for the ‘personalized financial planning’, it is actually the customization in the life insurance and obviously a significant contributor in keeping customers satisfied in the long run. To a much lesser extent; ‘corporate image’ and ‘technology’ also impact the satisfaction with functional services.

‘Assurance’ of the service quality is the most important predictor of ‘satisfaction with agents’. This is understandable, because superior customer services and the inspiration by the insurance agent provides confidence to mitigate the perceived risk in purchasing the life insurance product Giving due importance to customers and his/her needs, exhibiting sincerity, trust and integrity are essential in quality insurance services. To a much lesser extent, ‘satisfaction with agents’ has also been related to ‘personalized financial planning’ dimension of service quality. This is because life insurance creates a long-term relationship. Over a period of lifetime, the policyholders’ needs keep changing. Therefore to keep him satisfied it is essential that the agent monitors and tailors the offerings to cater to the changing needs.

‘Competence’ followed by ‘corporate image’ are the major predictors of ‘satisfaction with company’. As for ‘corporate image’, a possible explanation could be that the components investigated in this dimension, that is financial stability and innovation in financial products, are widely recognized as the key success factors in this industry.54

This study has some important managerial implications. It reiterates that life insurance service providers and managers should also be aware that customer satisfaction is primarily based on service quality. They should consider the relative value (contribution) to customer satisfaction of each dimensions of the service quality and consequently allocate different levels of resources according to this hierarchy. They should have a clear concept of what constitute customer satisfaction before they can attempt to measure it and its relationship with service quality dimensions. Thus quality improvements by management should not just focus on improving customer satisfaction but also target on improving the customers’ perception of service quality. In other words, the service providers should try to continuously improve both service quality and customer satisfaction.

CONCLUSIONS

The study adds to small but growing volume of literature examining service quality and customer satisfaction in developing economies. It confirms the need to tailor research techniques of determining service quality attributes, developed in the West to the context of Indian life insurance.

Our research further shows that service quality dimensions influence customer satisfaction with agents, functional services and with company, which, in turn, has an impact on overall satisfaction. In practical terms, this means that improving service quality increases satisfaction with agents, functional services and with company, all three of which ultimately enhance the overall customer satisfaction vis-à-vis life insurance services.

From managerial standpoint, this means that the better the perceived service quality, the higher the satisfaction with agents, functional services and company and therefore with overall satisfaction. For that reason the service quality variables used in our research and the three customer satisfaction measures should be constantly controlled in their performance and improved. Competitive strategies based upon vital aspects of the service quality as obtained in the research would prevent stretching of resources, and assist in creating satisfaction so desired by consumers.

Although this study focuses on life insurance industry in India, however, the results and recommendations of this article can be used for service quality improvements and consequently improving customer satisfaction of life insurance industries of other countries as well. This can be performed by incorporating necessary changes in service quality aspects in accordance with socio-economic environment of that nation.

Future research

The current study has been a cross-sectional study, but to determine the causal paths of the studied variables a longitudinal study would have been more appropriate, so to have a better understanding of how perceptions about service quality relate to satisfaction and loyalty. Further investigation in future might examine the service needs and requirements, as well as drivers of satisfaction for specific customer types; this is obviously an important way of segmenting markets.

It is clear that in our case the suggested constructs provided sufficient support for the satisfaction and service quality analysis. Other variables like price perception, switching cost and so on influence customer satisfaction, and including such variable(s) in the study would have made the research models more robust and interesting.

References

Cronin, J.J. and Taylor, S.A. (1992) Measuring service quality: A re-examination and extension. Journal of Marketing 56 (7): 55–68.

Deruyter, K., Bloemer, J. and Peeters, P. (1997) Merging service quality and service satisfaction: An empirical test of an integrative model. Journal of Economic Psychology 18 (4): 387–406.

Jayawardhena, C. and Foley, P. (2000) Changes in the banking sector-the case of Internet banking in the UK. Internet Research 10 (1): 19–31.

Spreng, R.A. and Mackoy, R.D. (1996) An empirical examination of a model of perceived service quality and satisfaction. Journal of Retailing 72 (2): 201–214.

Bitner, M.J. and Hubert, A.R. (1994) Encounter satisfaction versus overall satisfaction versus quality. In: R.T. Rust and R.L. Oliver (eds.) Service Quality – New Directions in Theory and Practice. Thousand Oaks, CA: Sage Publications, pp. 72–94.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1988) SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing 64 (1): 12–40.

Zeithaml, V.A. (1988) Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. Journal of Marketing 52 (3): 2–22.

Bitner, M.J. (1990) Evaluating service encounters: The effects of physical surroundings and employee responses. Journal of Marketing 54: 69–82.

Grönroos, C. (1982) A service quality model and its marketing implications. European Journal of Marketing 18 (4): 36–44.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1985) A conceptual model of service quality and its implications for further research. Journal of Marketing 48 (Fall): 41–50.

Murfin, D.E., Sclegelmilch, B.B. and Diamantopoulos, A. (1995) Perceived service quality and medical outcome: An interdisciplinary review and suggestions for future research. Journal of Marketing Management 11 (1–3): 97–117.

Soteriou, A.C. and Stavrinides, Y. (2000) An internal customer service quality data envelope analysis model for bank branches. International Journal of Bank Marketing 18 (5): 246–252.

Zhu, F.X., Wymer, W.J. and Chen, I. (2002) IT-based services and service quality in consumer banking. International Journal of Service Industry Management 13 (1): 69–90.

Seth, A., Momaya, K. and Gupta, H.M. (2008) Managing the customer perceived service quality for cellular mobile telephony: An empirical investigation. Vikalpa 33 (1): 19–34.

Lehtinen, U. and Lehtinen, J.R. (1991) Two approaches to service quality dimensions. The Service Industries Journal 11 (3): 287–305.

Rosen, L.D. and Karwan, K.R. (1994) Prioritizing the dimensions of service quality. International Journal of Service Industry Management 5 (4): 39–52.

Johnson, R.L., Tsiros, M. and Lancioni, R.A. (1995) Measuring service quality: A systems approach. Journal of Services Marketing 9 (5): 6–19.

Siu, N.Y.M. and Cheung, J.T. (2001) A measure of retail service quality. Marketing Intelligence and Planning 19 (2): 88–96.

Mehta, S.C. and Lobo, A. (2002) MSS, MSA and Zone of Tolerance as measures of service quality: A study of the life insurance industry. Second International Services Marketing Conference, University of Queensland.

Carman, J.M. (1990) Consumer perceptions of service quality: An assessment of the SERVQUAL dimensions. Journal of Retailing 66 (1): 33–55.

Jain, S.K. and Gupta, G. (2004) Measuring service quality: SERVQUAL vs. SERVPERF scales. Vikalpa 29 (2): 25–37.

Oliver, R.L. (1997) Satisfaction: A Behavioral Perspective on the Consumer. New York: McGraw-Hill.

McDougall, G.H.G. and Levesque, T. (2000) Customer satisfaction with services: Putting perceived value into the equation. Journal of Services Marketing 14 (5): 392–410.

Crompton, J.L. and MacKay, K.J. (1989) Users’ perceptions of the relative importance of service quality dimensions in selected public recreation programs. Leisure Sciences 11: 367–375.

Taylor, S.A. and Baker, T.L. (1994) An assessment of the relationship between service quality and customer satisfaction in the formation of consumer's purchase intentions. Journal of Retailing 2: 163–178.

Gotlieb, J.B., Grewal, D. and Brown, S.W. (1994) Consumer satisfaction and perceived quality: Complementary or divergent constructs? Journal of Applied Psychology 76 (6): 875–885.

Iacobuci, D., Grayson, K.A. and Ostrom, A. (1994) The calculus of service quality and customer satisfaction: Theoretical and empirical differentiation and integration. In: A. Swartz, D.E. Bowen and S.W. Brown (eds.) Advances in Services Marketing and Management: Research and Practice. Greenwich, CT: JAI.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1994) Reassessment of expectations as a comparison standard in measuring service quality: Implications for further research. Journal of Marketing 58 (1): 111–124.

Mittal, V., Ross, W.T. and Baldasare, P.M. (1998) The asymmetric impact of negative and positive attribute-level performance on overall satisfaction and repurchase intentions. Journal of Marketing 1: 33–47.

Lovelock, C. and Wright, L. (1999) Principles of Service Marketing and Management. Englewood Cliffs, NJ: Prentice Hall.

Anderson, E. and Sullivan, M. (1993) The antecedents and consequences of customer satisfaction for firms. Marketing Science 12 (1): 125–143.

Anderson, E.W., Fornell, C. and Lehmannn, D.R. (1994) Customer satisfaction, market share, and profitability: Findings from Sweden. Journal of Marketing 58 (July): 53–66.

Cronin, J.J. and Taylor, S.A. (1994) SERVPERF versus SERVQUAL: Reconciling performance-based and perceptions-minus-expectations measurement of service quality. Journal of Marketing 58 (1): 125–131.

Life Insurance Council. (2010) (online) http://www.lifeinscouncil.org, accessed 14 February 2010.

Insurance Regulatory and Development Authority. (2010) (online), http://www.irdaindia.org, accessed 20 February 2010.

India Brand Equity Foundation. (2010) (online), http://www.ibef.org, accessed 27 February 2010.

Ennew, C.T., Reed, G. and Vand Binks, M.R. (1993) Importance/performance analysis and the measurement of service quality. European Journal of Marketing 27 (2): 59–70.

Arora, R. and Stoner, C. (1996) The effect of perceived service quality and name familiarity on the service selection decision. Journal of Services Marketing 10 (1): 22–34.

Luarn, P., Lin, T.M.Y. and Lo, P.K.Y. (2003) An exploratory study of advancing mobilization in the life insurance industry: The case of Taiwan's Nan Shan Life Insurance Corporation. Internet research. Electronic Networking Applications and Policy 13 (4): 297–310.

Joseph, M., Stone, G. and Anderson, K. (2003) Insurance customers’ assessment of service quality: A critical evaluation. Journal of Small Business and Enterprise Development 10 (1): 81–92.

Tam, J.L.M. and Wong, Y.H. (2001) Interactive selling: A dynamic framework for services. Journal of Services Marketing 15 (5): 379–396.

Chow-Chua, C. and Lim, G. (2000) A demand audit of the insurance market in Singapore. Managerial Auditing Journal 15 (7): 372–382.

Gayathri, H., Vinaya, M.C. and Lakshmisha, K. (2006) A pilot study on the service quality of insurance companies. Journal of Services Research 5 (2): 123–138.

Marying, P. (2000) Qualitative content analysis. Forum: Qualitative Social Research 1 (2), Art.20-June 2000, http://www.qualitative-research.net/index.php/fqs/article/view/1089.

Ahire, S.L., Golhar, D.Y. and Waller, M.A. (1996) Development and validation of TQM implementation constructs. Decision Sciences 27 (1): 23–56.

O. Leary-Kelly, S.W. and Vokurka, R.J. (1998) The empirical assessment of construct validity. Journal of Operations Management 16 (4): 387–405.

Bentler, P.M. and Bonett, D.G. (1980) Significance tests and goodness of fit in the analysis of covariance structures. Psychological Bulletin 88: 588–606.

Joreskög, K.G. and Sorböm, D. (1990) LISREL 8 user's Reference Guide. Lincolnwood, IL: Scientific Software International.

Grönroos, C. (1986) Developing Service Quality: Some Managerial Implications. Swedish School of Economics: Helsinki, Finland, pp. 4–7. Unpublished working paper.

Lehtinen, J. (1985) Quality Oriented Services Marketing. Helsinki, Finland: Service Management Institute, pp. 50–57.

Crosby, L.A., Evans, K.R. and Cowles, D. (1990) Relationship quality in services selling: An interpersonal influence perspective. Journal of Marketing 54 (July): 68–81.

Tsoukatos, E. and Rand, G.K. (2006) Path analysis of perceived service quality, satisfaction and loyalty in Greek insurance. Managing Service Quality 16 (5): 501–519.

Crosby, L.A. and Stephens, N. (1987) Effect of relationship marketing on satisfaction, retention, and prices in the life insurance industry. Journal of Marketing Research 24 (4): 404–411.

Scott, R. (2000) Shaping the future of the life agency force. Coverage 26 (1): 22–26.

Author information

Authors and Affiliations

Corresponding author

Additional information

2has an experience of over 5 years in teaching marketing subjects. Her interest areas are Services Marketing, Customer Relationship Management, Marketing Research and Consumer Behavior. She is currently pursuing doctoral program in the arena of services marketing. She has eight publications in various international and national journals like International Business Research, Convergence Asia, Synergy, and so on to her credit.

Rights and permissions

About this article

Cite this article

Siddiqui, M., Sharma, T. Analyzing customer satisfaction with service quality in life insurance services. J Target Meas Anal Mark 18, 221–238 (2010). https://doi.org/10.1057/jt.2010.17

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jt.2010.17